Speech To Speech Translation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

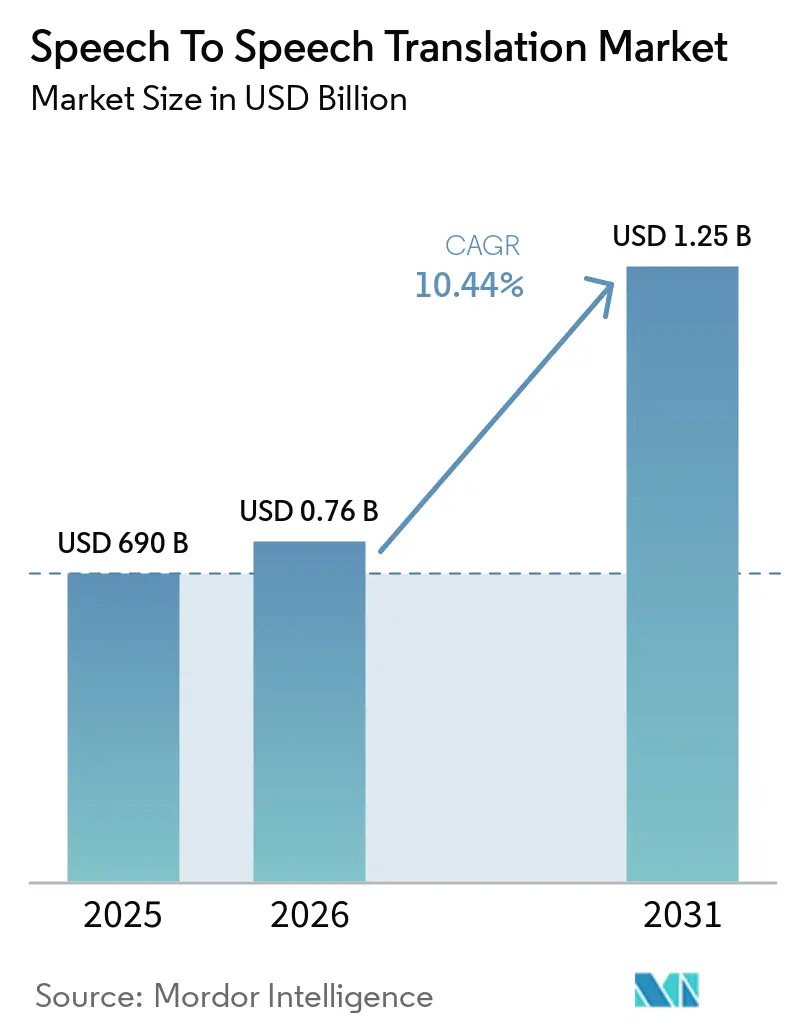

| Market Size (2026) | USD 0.76 Billion |

| Market Size (2031) | USD 1.25 Billion |

| Growth Rate (2026 - 2031) | 10.44% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Speech To Speech Translation Market Analysis by Mordor Intelligence

The Speech to Speech Translation market size is expected to grow from USD 690 million in 2025 to USD 762.04 million in 2026 and is forecast to reach USD 1.25 billion by 2031 at 10.44% CAGR over 2026-2031. This market size expansion reflects deeper neural-network accuracy, increasing 5G availability, and surging enterprise demand for real-time, multilingual voice services. Cloud APIs from hyperscalers now deliver sub-100-millisecond inference, enabling contact-center agents, clinicians, and factory operators to converse naturally across more than 200 language pairs. Hardware specialists continue to refine on-device neural chips that support offline translation; however, software subscriptions dominate due to zero marginal distribution costs. Competitive pressure from bundled big-tech offerings is steering standalone vendors toward low-resource language niches, industrial IoT voice control, and privacy-preserving federated learning. Regulatory incentives—such as language-access mandates in healthcare and e-commerce—add an external tailwind, while dialect accuracy gaps, privacy compliance costs, and on-device chip prices remain key brakes on adoption.

Key Report Takeaways

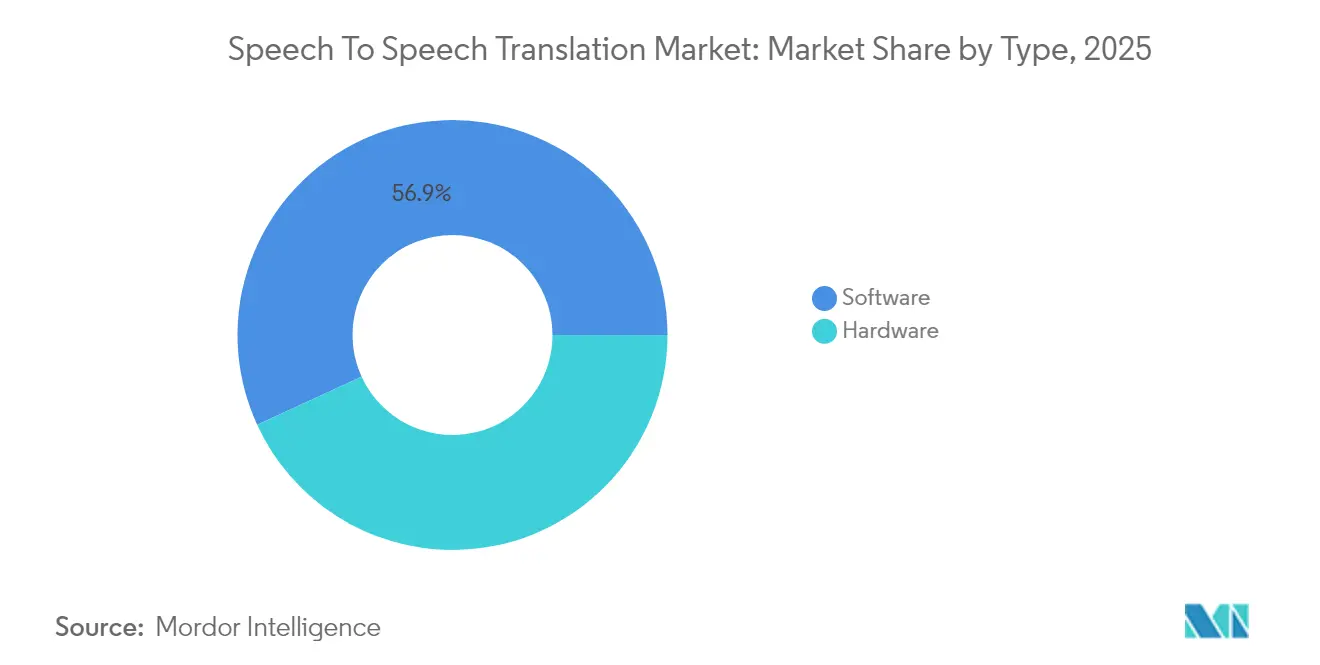

- By type, software held 56.85% share of the Speech to Speech Translation market size in 2025, and it is forecast to grow at a 11.63% CAGR through 2031.

- By deployment mode, cloud commanded 58.20% share of the Speech to Speech Translation market size in 2025, and it is advancing at an 11.74% CAGR. through 2031.

- By application, customer service accounted for 32.55% share of the Speech to Speech Translation market size in 2025; healthcare is the fastest-growing segment at a 13.12% CAGR through 2031.

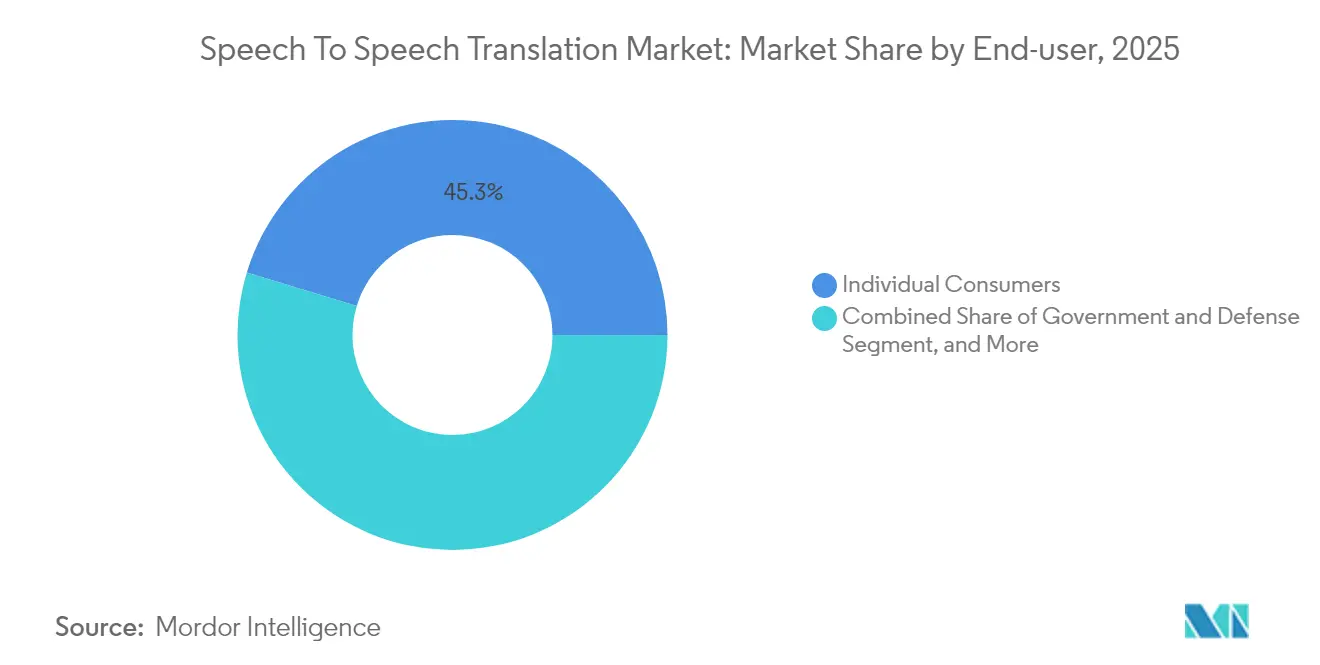

- By end-user, individual consumers captured a 45.30% share of the Speech to Speech Translation market size in 2025, while government and defense is forecast to grow at a 11.93% CAGR through 2031.

- By technology, neural machine translation captured a 57.10% share of the Speech to Speech Translation market size in 2025, while hybrid translation is forecast to grow at a 12.98% CAGR through 2031.

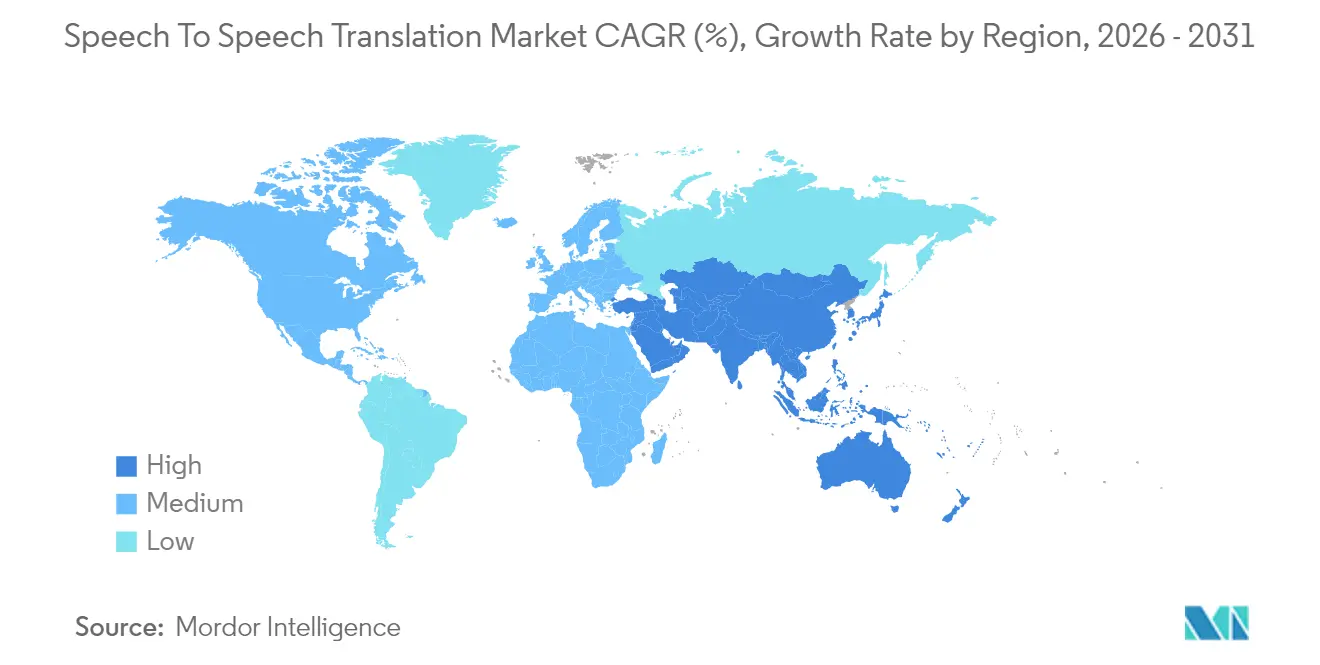

- By geography, North America led with a 36.35% share of the Speech to Speech Translation market size in 2025, while the Asia Pacific is projected to grow at a 12.52% CAGR from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Speech To Speech Translation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Intelligent Voice Assistants | +1.8% | Global, with highest penetration in North America and China | Medium term (2-4 years) |

| Growth of International Tourism and Cross-Border E-Commerce | +2.1% | Asia Pacific, Europe, Middle East | Short term (≤ 2 years) |

| 5G Roll-outs Enabling Low-Latency Cloud Inference | +2.4% | North America, Asia Pacific core markets, spill-over to Middle East | Medium term (2-4 years) |

| Big-Tech Investments in Voice AI Ecosystems | +2.6% | Global, led by North America and China | Long term (≥ 4 years) |

| Industrial IoT Demand for Multilingual Voice Control | +1.2% | Europe, Asia Pacific manufacturing hubs | Long term (≥ 4 years) |

| Tele-health Adoption for Minority Languages | +0.9% | North America, Europe, emerging in Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G Roll-outs Enabling Low-Latency Cloud Inference

Standalone 5G networks now deliver sub-20-millisecond round-trip latency, erasing the chief technical barrier to cloud-based streaming translation. U.S. carriers are expected to activate 5G cores across more than 200 metropolitan areas by mid-2024.[1]Verizon Communications, “5G Standalone Deployment Update,” verizon.com China’s three mobile giants are expected to extend comparable coverage to 95% of prefecture-level cities by early 2025. Smartphones powered by the Qualcomm Snapdragon 8 Gen 3 run local models at 45 TOPS and escalate complex queries to the edge cloud only when accuracy demands it. The hybrid architecture lowers egress fees, keeps sensitive voice on the device, and satisfies stricter healthcare privacy rules in markets such as the United States.

Big-Tech Investments in Voice AI Ecosystems

Microsoft, Google, Amazon, and Meta collectively spent nearly USD 200 billion on AI compute in 2024, funneling substantial capacity into real-time speech translation.[2]Microsoft Corporation, “Fiscal 2024 Annual Report,” microsoft.com Azure AI Speech now supports 120 language pairs in Teams and Dynamics 365, with enterprise API calls up 140% YoY in late-2024. Google’s streaming Cloud Translation API posted 180% usage growth inside Workspace during the same period. Amazon stitched Transcribe and Translate into Connect, trimming average call-handling time by 30% for early adopters. Meta opted for an on-device path: its SeamlessM4T model processes encrypted WhatsApp audio locally, reinforcing privacy claims that appeal to markets wary of cloud storage. Hyperscalers exploit feedback loops across billions of users, monetizing translation as a sticky feature inside broader productivity suites.

Industrial IoT Demand for Multilingual Voice Control

Manufacturers are equipping machinery with voice interfaces that support migrant workforces and reduce the need for touchscreen use in dusty or hazardous environments. Siemens’ Amberg plant logged 92% intent-recognition accuracy across German, Turkish, and Polish in 2024.[3]Siemens AG, “Multilingual Voice Assistant Pilot,” siemens.com Bosch integrated Mandarin–Cantonese translation into assembly lines, cutting worker training time by 25%. Regulatory frameworks, such as IEC 62443-4-2, now prioritize encrypted voice data and local processing, which favors edge hardware in tightly regulated industries.

Growth of International Tourism and Cross-Border E-Commerce

International arrivals rebounded to 1.3 billion in 2024 and are forecast at 1.5 billion by 2026. Cross-border online sales reached USD 1.2 trillion, with multilingual voice bots meeting the language requirements of the Digital Services Act in the EU. Translation earbuds also gained cultural cachet: Timekettle sold 500,000 M3 units in H1-2024, largely to travelers in Europe and North America.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dialect and Code-Switching Accuracy Gaps | -1.4% | Global, acute in multilingual regions of Africa, India, Southeast Asia | Short term (≤ 2 years) |

| Privacy and Data-Security Concerns | -1.8% | Europe (GDPR), North America (CCPA, HIPAA), China (PIPL) | Medium term (2-4 years) |

| High Cost of On-Device Real-Time Translation Hardware | -0.9% | Emerging markets in Latin America, Africa, South Asia | Medium term (2-4 years) |

| Socio-Cultural Resistance to Machine-Mediated Dialogue | -0.6% | East Asia, Middle East, high-context cultures | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Privacy and Data-Security Concerns

Voice spectral features qualify as biometric identifiers under GDPR, CCPA, and China’s PIPL, forcing enterprises to obtain explicit consent and maintain encrypted storage. Healthcare deployments must also comply with HIPAA audit and retention rules, which add to the integration cost and limit cloud vendor selection. Microsoft recorded USD 1.2 billion in additional privacy compliance expenditures in fiscal 2024. Rising deepfake fraud has prompted banks to adopt liveness detection, which introduces latency that can hinder conversational experiences. NIST’s 2025 draft guidance highlights federated learning as a potential remedy, but its adoption is hindered by excessive compute overhead.

Dialect and Code-Switching Accuracy Gaps

Translation accuracy drops sharply when speakers mix languages or use regional dialects. ACL-2024 researchers showed an 18-point accuracy gap for Singlish relative to standard English. Word-error rates doubled for Spanish-English code-switching in a 2024 Computer Speech and Language study. Low-resource languages remain underserved: although Meta’s NLLB-200 lists 200 languages, only a quarter achieve production-grade accuracy, which constrains their adoption in sub-Saharan Africa. Accent variation complicates matters further; Indian English recognition accuracy fell from 85% (Mumbai) to 68% (Assamese accent) in 2024 IIT Delhi tests.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Software Extends Lead Through API Monetization

Software captured 56.85% of 2025 revenue and is on track for 11.63% CAGR to 2031. Usage-based APIs from Microsoft, Google, and Amazon enable contact centers to add real-time multilingual voice capabilities with no hardware capital outlay. Subscription models also ensure users always run the newest transformer checkpoints. Hardware remains important for offline or ruggedized roles. Standalone earbuds catered to mass-market travelers, while server-grade GPU racks supported regulated enterprises. Hybrid devices with neural coprocessors and cloud fallback are the fastest risers, driven by automotive and industrial IoT designs that seek latency under 100 milliseconds. Ongoing ISO work on network-aware model compression should narrow the software-hardware distinction and further boost hybrid adoption.

Hardware suppliers now bundle OTA firmware that syncs with cloud model updates, blurring update cycles with software. Even so, consumer hardware margins are thinning because smartphone OS vendors bundle basic translation at no incremental cost. The Speech to Speech Translation market relies on hardware innovations, such as beam-forming mic arrays, noise suppression, and battery-efficient NPUs, to continue differentiating itself from commodity phones. Vendors that secure defensible industrial or defense niches enjoy price insulation because compliance certificates and rugged housings raise switching costs, a trend likely to persist through 2031.

By Deployment Mode: Cloud Dominates, Edge Narrows the Gap

Cloud held 58.20% of 2025 revenue and is expected to grow at a 11.74% CAGR as enterprises value elastic scaling and SLA-grade uptime. Hyperscalers guarantee sub-second latency for over 100 language pairs, seamlessly integrating translation into existing identity and analytics stacks. On-premise systems maintained a 28.35% share within defense and finance, where air-gapped networks are mandatory. Edge processing’s 13.45% share is small but pivotal: smartphone NPUs now handle up to 10-billion-parameter models. Apple’s iPhone processed 40% of translation requests locally in 2025. By 2031, tighter privacy statutes and improved chip performance will elevate the edge’s role, even as the cloud remains the hub for heavy computation for rare languages.

The hybrid model, combining edge and cloud, best aligns with enterprise privacy policies. A call center can parse routine phrases locally, then escalate domain-specific jargon to the cloud for higher accuracy. This routing slashes data-egress fees and minimizes GDPR exposure, leading many European banks to pilot hybrid gateways in 2025. Hardware vendors embed SIM modules to maintain secure fallback channels, ensuring continuity when corporate VPNs fail. The Speech to Speech Translation market size linked to edge-first architectures is projected to reach USD 168.2 million by 2031, accounting for 13.45% of the segment revenue, provided that chip costs decline as forecast.

By Application: Customer Service Retains Primacy, Healthcare Accelerates

Customer service captured 32.55% of 2025 revenue, reflecting the sector’s relentless push to automate tier-one queries. Amazon Connect users who enabled live translation reported a 25–35% decrease in transfers, resulting in improved Net Promoter Scores. Travel ranked second at 22.10% due to tourist rebound and earbud uptake. Healthcare, although accounting for only 11.35% of 2025 revenue, drives growth with a 13.12% CAGR, buoyed by CMS reimbursement and chronic clinician shortages in minority-language regions. Hospitals using voice translation cut interpreter wait times from hours to minutes, boosting tele-ICU throughput. Media and entertainment followed with an 10.88% growth rate, as YouTube and Spotify piloted auto-voiceovers, expanding creator reach without requiring extra studio time.

EU-funded pilots integrated real-time translation into MOOCs, reducing localization costs and expanding course access. Industrial IoT voice control, still in its nascent stages, promises safety and productivity gains on factory floors. The Speech to Speech Translation market share tied to industrial IoT is forecast to reach 3.85% by 2031 as hands-free interfaces replace touch panels in hazardous zones. Regulation continues to frame adoption: the Americans with Disabilities Act and the incoming European Accessibility Act formalize multilingual access as a right, effectively hard-coding speech translation into public-facing services.

By End-user: Consumers Dominate Volume, Government Leads Growth Potential

Individual consumers accounted for 45.30% of 2025 revenue through the sale of earbuds and mobile apps. Vacation cycles shape quarterly peaks, but embedded phone translation poses a threat to standalone devices. Enterprises held 38.25%, relying on translation to support remote teams and cross-border sales. Government and defense stood at 16.45% yet carries a 11.93% CAGR: U.S. agencies purchased USD 45 million in ruggedized handhelds in fiscal 2024. EU border guards using automated intake translation trimmed processing time by 40%, an operational metric that secures continued funding. Certified vendors with FedRAMP or Common Criteria status will likely dominate forthcoming tenders.

Consumer adoption now extends to smart-speaker ecosystems; Amazon enabled Alexa's multilingual mode for 30 languages in mid-2025, resulting in a 95% usage spike in the first month. That move will pressure headphone makers unless they deepen their niche focus by offering offline models, specialty language packs, or superior audio fidelity. The Speech to Speech Translation market size for government buyers is projected to reach USD 268.5 million by 2031, a five-fold increase from 2024, provided that voice liveness and encryption capabilities keep pace with the requirements of classified networks.

By Technology: Neural Translation Rules, Hybrids Offer Pragmatic Gains

Neural machine translation accounted for 57.10% of 2025 technology revenue, driven by the use of transformer architectures. Statistical and rule-based engines are often used in niche compliance settings or those with limited resources. Hybrid systems, which blend neural, statistical, and rule-based layers, grew at the fastest rate (12.98% CAGR) as vendors seek better trade-offs between accuracy and latency. Microsoft utilizes rule-based glossaries on top of neural outputs to mitigate hallucinations in technical documents; iFLYTEK combines neural streaming for conversational speech with statistical fallbacks for handling rare dialects. IEEE issued 2024 guidelines that endorse ensemble-weighted voting, signaling industry consensus around multi-model pipelines.

Cloud GPUs still favor large-scale neural models, but edge NPUs dictate compact transformers with fewer than 2 billion parameters for offline performance. Quantization and pruning research promises to further compress models without steep accuracy penalties, unlocking sub-1-second latency even on mid-range phones. The speech to speech translation market is now converging on a dual-track R&D agenda: large-scale models for high-resource pairs and ultra-efficient hybrids for field deployment, where bandwidth, power, and privacy create significant constraints.

Geography Analysis

North America retained 36.35% revenue share in 2025, benefiting from hyperscaler cloud APIs and robust 5G roll-outs. U.S. enterprises led orders, driven by ADA compliance and omnichannel customer-experience strategies. Federal 5G grants totaling USD 9 billion accelerated rural coverage, enabling mobile translation services. Canada’s bilingual mandates boost steady demand across health and immigration. Mexico’s maquiladora corridor adopted multilingual voice interfaces to synchronize Spanish-English workflows, aided by Telcel’s 60% 5G population coverage by early 2025. The Speech to Speech Translation market size for North America is forecast to reach USD 512.6 million in 2031, driven by ongoing cloud-service upgrades.

The Asia Pacific will be the fastest-growing region, expanding at a 12.52% CAGR. China dominates the volume through its Baidu, iFLYTEK, and Alibaba ecosystems; the MIIT reported that more than 3.5 million 5G base stations were in operation by mid-2024. Japan leverages translation technology to offset labor shortages in the hospitality industry, with Pocketalk devices surpassing 1.2 million cumulative sales. India’s Bhashini platform harnesses open-source APIs to spur adoption across 22 official languages. South Korea’s Digital New Deal invests USD 1.5 billion into AI infrastructure, while Samsung and LG embed multilingual translation directly into smartphones and appliances. Australia mirrors these trends in tourism and multicultural public services.

Europe accounted for 20.85% of 2025 revenue, shaped by 24 official EU languages and strong privacy oversight. Germany spearheads automotive voice assistants. The U.K. financial sector adopted cloud translation to meet the 'treating customers fairly' guidance. France tends to gravitate toward on-premise deployments to satisfy data localization preferences, and the CNIL enforces strict biometric consent audits. The implementation of the European Accessibility Act in June 2025 will make multilingual access compulsory for telecoms and public websites, promising a new wave of demand. EU Digital Services Act clauses already push e-commerce vendors to support voice bots in member-state languages.

South America and the Middle East and Africa contribute 15.20% combined. Brazil’s cross-border e-commerce platform Mercado Libre added embedded translation in late 2024, facilitating seamless transactions between Portuguese and Spanish speakers. The UAE’s smart-city projects require Arabic-English real-time translation across government kiosks, while Saudi Arabia pursues similar goals tied to Vision 2030. South Africa pilots multilingual visa-processing tools covering Zulu and Xhosa. Nigeria experiments with customer-service translation despite accent challenges; local telcos MTN and Airtel collaborate with startups to strengthen vernacular support.

Competitive Landscape

Microsoft, Google, Amazon, Meta, and Baidu collectively held roughly 48% of the revenue in 2024, underscoring a moderately concentrated field. Hyperscalers leverage proprietary data, subsidized compute, and ecosystem bundling to cement stickiness. Chinese incumbents iFLYTEK and Baidu exploit data localization rules, gaining a near-total share in government and automotive channels. Hardware innovators Waverly Labs, Timekettle, Travis, and Langogo differentiate themselves by latency and offline breadth but confront a margin squeeze as smartphone OEMs embed translation at zero extra cost.

Strategic focus is shifting to low-resource languages and industrial IoT. Cohere and AI21 Labs develop code-switching models targeting underserved bilingual populations. DeepL and Naver’s Papago extend domain-specific glossaries across European and Korean markets, respectively. Vertical integration remains the dominant strategy: Microsoft integrates Azure Speech with Teams, Dynamics, and the Power Platform, achieving 60% higher contract values among multi-service clients. Google ties translation to Meet and Workspace bundles, while Amazon pairs Transcribe-Translate with Connect and S3 analytics. Meta uses on-device processing to position privacy as a compelling differentiator in end-to-end encrypted apps.

Pricing wars loom as hyperscalers push per-minute API charges downward, prompting smaller vendors to chase specialized accuracy rather than volume. Standardized benchmarks from IEEE and open datasets from Bhashini and NLLB level the playing field for new entrants, albeit slowly. Regulatory certifications such as FedRAMP, Common Criteria, and CE mark are becoming key buying criteria for public-sector tenders, favoring mature vendors. Meanwhile, automotive OEMs sign multi-year co-development pacts, such as the one between iFLYTEK and

Venture investment in translation startups dipped in 2024 as capital flowed to foundation-model companies, yet M&A is active. Microsoft’s Nuance unit launched Dragon Medical One with multilingual documentation, instantly tapping its healthcare footprint. Amazon extended Alexa’s remit to household translation, expanding its install base by 95% MoM post-launch. Waverly Labs obtained FCC certification and struck an airline partnership to trial in-flight translation. Collectively, these moves indicate sustained innovation despite the dominance of hyperscalers.

Speech To Speech Translation Industry Leaders

Microsoft Corporation

Google LLC

Amazon.com Inc.

Meta Platforms Inc.

Baidu Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Meta rolled SeamlessM4T into Instagram calls, promising 50 language pairs by year-end.

- March 2025: Baidu debuted Xiaodu smart displays with Mandarin-Cantonese-English translation, recording 500,000 pre-orders.

- February 2025: Google enabled bidirectional streaming translation in Cloud Translation API, boosting Workspace education deployments.

- January 2025: Microsoft released Azure AI Speech real-time translation for 120 language pairs with sub-200-millisecond latency.

Global Speech To Speech Translation Market Report Scope

The Speech to Speech Translation Market Report is Segmented by Type (Hardware (Stand-Alone, Server-Based, Hybrid), Software), Deployment Mode (On-Premise, Cloud-Based, Edge), Application (Travel and Tourism, Healthcare, Customer Service and Contact Centers, Media and Entertainment, Education and E-Learning, Other Application), End-user (Individual Consumers, Enterprises, Government and Defense), Technology (Neural Machine Translation, Statistical Machine Translation, Rule-Based Translation, Hybrid Translation), and Geography (North America, South America, Europe, Asia Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware | Stand-Alone |

| Server-Based | |

| Hybrid | |

| Software |

| On-Premise |

| Cloud-Based |

| Edge |

| Travel and Tourism |

| Healthcare |

| Customer Service and Contact Centers |

| Media and Entertainment |

| Education and E-Learning |

| Other Application |

| Individual Consumers |

| Enterprises |

| Government and Defense |

| Neural Machine Translation |

| Statistical Machine Translation |

| Rule-Based Translation |

| Hybrid Translation |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Type | Hardware | Stand-Alone | |

| Server-Based | |||

| Hybrid | |||

| Software | |||

| By Deployment Mode | On-Premise | ||

| Cloud-Based | |||

| Edge | |||

| By Application | Travel and Tourism | ||

| Healthcare | |||

| Customer Service and Contact Centers | |||

| Media and Entertainment | |||

| Education and E-Learning | |||

| Other Application | |||

| By End-user | Individual Consumers | ||

| Enterprises | |||

| Government and Defense | |||

| By Technology | Neural Machine Translation | ||

| Statistical Machine Translation | |||

| Rule-Based Translation | |||

| Hybrid Translation | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the Speech to Speech Translation market in 2026?

It reached USD 762.04 million in 2026 and is projected to climb to USD 1.25 billion by 2031, expanding at a 10.44% CAGR over 2026-2031.

Which segment grows fastest over 2026-2031?

Healthcare applications lead with a 13.12% CAGR, spurred by tele-health reimbursement and language-access mandates.

Who are the main vendors?

Microsoft, Google, Amazon, Meta, Baidu, and iFLYTEK dominate cloud and domestic deployments, while Waverly Labs and Timekettle focus on hardware form factors.

What role does 5G play?

Standalone 5G lowers network latency below 20 milliseconds, enabling streaming translation and supporting hybrid edge-cloud architectures.

Why is Asia Pacific attractive?

Cross-border e-commerce, large multilingual populations, and rapid 5G roll-outs drive a 12.52% regional CAGR through 2031.

How strict are privacy regulations?

GDPR, CCPA, HIPAA, and China’s PIPL classify voice data as biometric, imposing consent, encryption, and localization requirements that raise integration costs.

Page last updated on: