Market Overview

| Study Period | 2020 - 2031 |

|---|---|

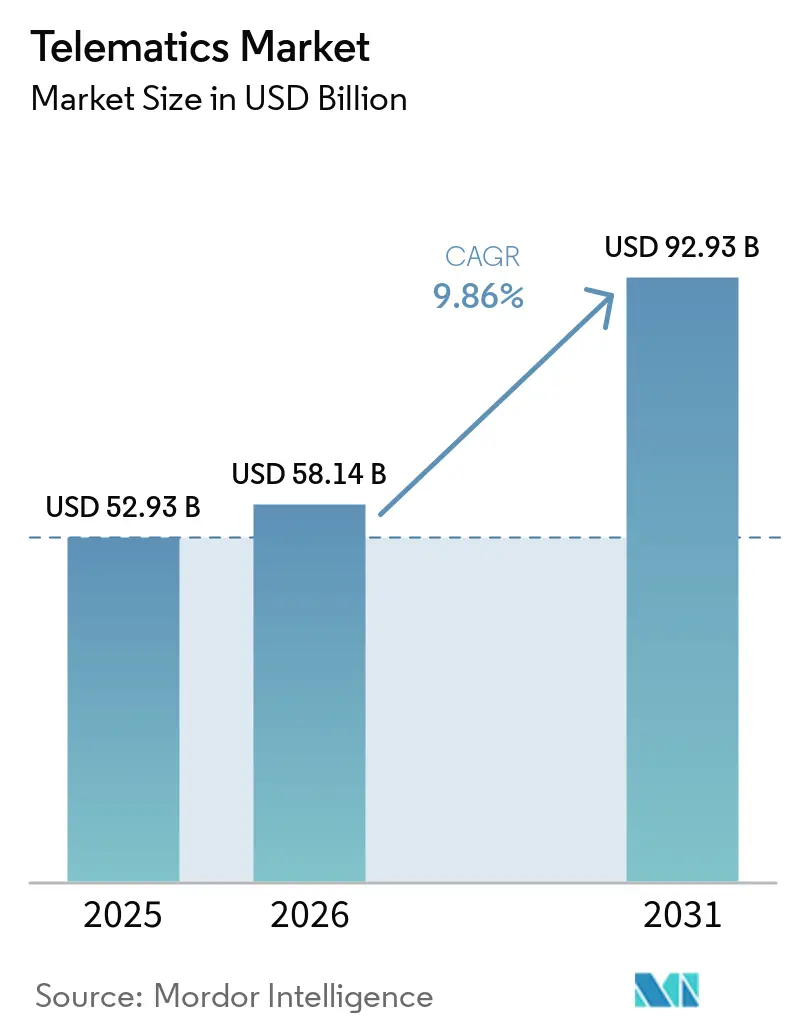

| Market Size (2026) | USD 58.14 Billion |

| Market Size (2031) | USD 92.93 Billion |

| Growth Rate (2026 - 2031) | 9.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Telematics Market Analysis by Mordor Intelligence

The telematics market size was valued at USD 52.93 billion in 2025 and estimated to grow from USD 58.14 billion in 2026 to reach USD 92.93 billion by 2031, at a CAGR of 9.86% during the forecast period (2026-2031). Regulatory mandates, especially eCall in Europe and AIS 140 in India, are compelling automakers and fleets to embed connectivity at the factory level, which accelerates OEM demand.[1]European Commission, “eCall,” road-safety.transport.ec.europa.eu Semiconductor content per vehicle is set to double by 2030, raising hardware costs yet enabling richer data streams that underpin advanced analytics. Usage-based insurance programs, powered by real-time driving data, are expanding quickly across North America and Europe, reinforcing the business case for connected cars. Rapid adoption of 5G and edge computing is transforming telematics from simple tracking to predictive maintenance and vehicle-to-everything communication. Rising cybersecurity compliance costs under UNECE WP.29 and ISO/SAE 21434 are pressuring smaller vendors but giving well-capitalized players a competitive edge.

Key Report Takeaways

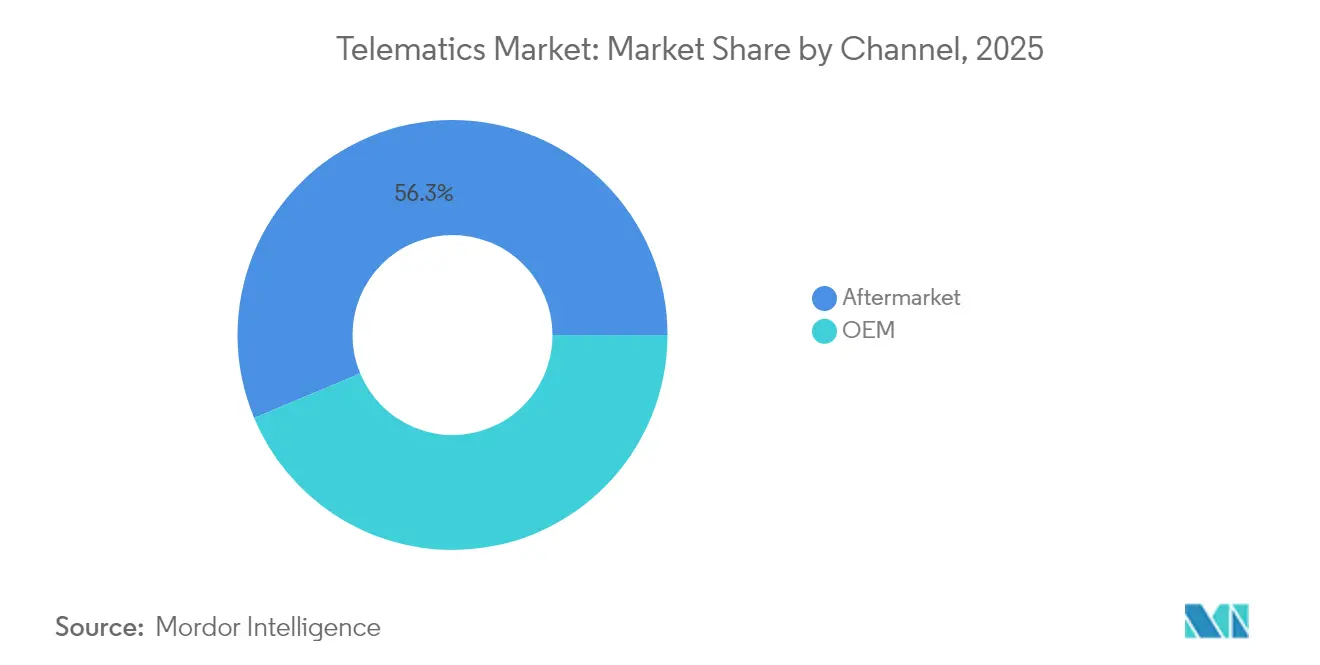

- By channel, the aftermarket segment held 56.30% of the telematics market share in 2025, while OEM solutions are advancing at an 11.62% CAGR through 2031.

- By solution, embedded systems accounted for 47.80% of the telematics market size in 2025 and are growing at a 12.94% CAGR to 2031.

- By offering type, mid-tier services led with 45.70% revenue share in 2025; high-end services are forecast to expand at a 12.63% CAGR.

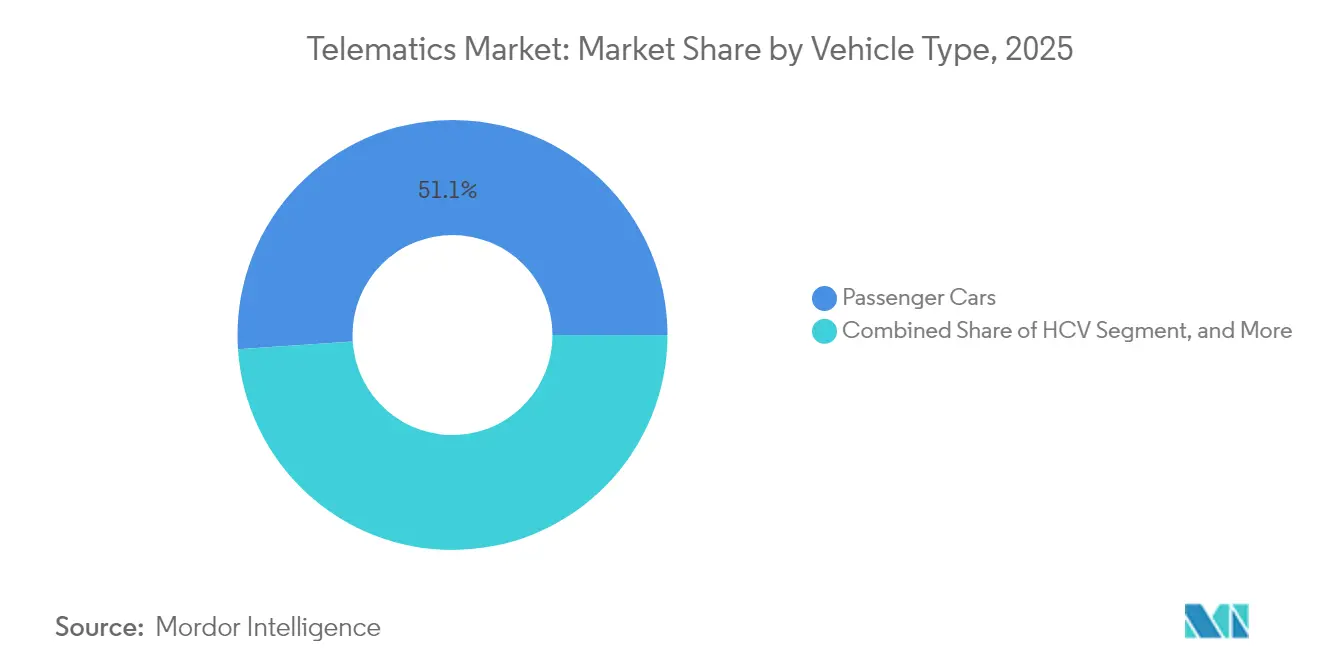

- By vehicle type, passenger cars captured a 51.05% share in 2025, whereas heavy commercial vehicles are projected to rise at a 12.31% CAGR.

- By application, fleet management commanded a 38.25% share of the telematics market in 2025, and car-sharing and subscription services are set to grow at a 13.20% CAGR.

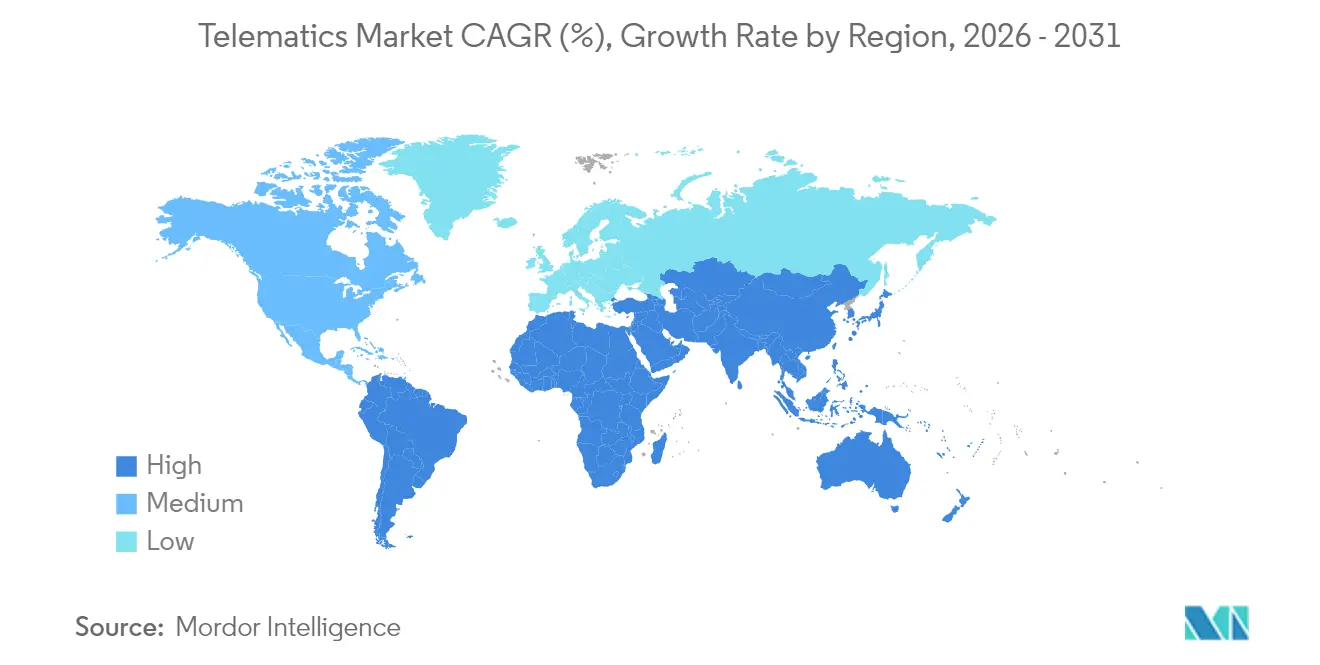

- By geography, Europe held a 31.95% share in 2025, while Asia-Pacific is the fastest-growing region at a 12.26% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Telematics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding OEM-embedded connectivity mandates | +2.10% | Global, with EU and Asia-Pacific leading | Medium term (2-4 years) |

| Usage-based insurance (UBI) adoption surging post-2025 | +1.80% | North America and Europe, expanding to APAC | Short term (≤ 2 years) |

| Government eCall and AIS 140 regulations | +1.50% | Europe (eCall), India (AIS 140), expanding globally | Long term (≥ 4 years) |

| 5G/edge-enabled over-the-air (OTA) analytics | +1.30% | Global, with advanced markets leading | Medium term (2-4 years) |

| Fleet electrification demands real-time battery analytics | +1.20% | Global, concentrated in urban centers | Long term (≥ 4 years) |

| Rise of mobility-as-a-service (MaaS) platforms | +0.90% | Urban centers globally, Europe leading | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding OEM-embedded connectivity mandates

Automakers are integrating telematics directly into vehicle electronics to meet new data-sharing rules such as the EU Data Act, which applies from 2025 and obliges manufacturers to open vehicle data to third-party service providers.[2]Shoosmiths, “The GDPR and EU Data Act,” shoosmiths.com Geotab’s collaboration with Volvo Cars lifts its OEM integrations to more than 157 brands, proving that embedded connectivity is scaling quickly.[3]Geotab, “Volvo Integration,” geotab.com Analysts estimate connected services could yield USD 1,600 revenue per car, incentivizing automakers to treat data as a profit center. Specialized vendors like WirelessCar now offer compliance toolkits that help OEMs operationalize the Data Act, accelerating rollout timelines. As regulations tighten, factory-fitted units are becoming standard, shrinking the addressable aftermarket and reshaping the telematics market.

Usage-based insurance adoption surging post-2025

Insurance carriers are shifting from demographic to behaviour-based pricing, fuelled by real-time driving data. Intuit embedded Zendrive analytics into the Credit Karma app, sending 4 million policy offers to its 6 million members in 2025, which demonstrates mainstream scale.[4]Intuit, “Intuit to Acquire Technology from Zendrive,” investors.intuit.com Kia and LexisNexis rolled out driver-score sharing in 27 EU countries, simplifying customer enrolment while preserving GDPR compliance. Safe drivers can secure premium cuts of up to 30%, boosting consumer demand and improving loss ratios for insurers. Cambridge Mobile Telematics added fuel consumption scoring, proving that insurers now value eco-efficient driving as well as safety. These advances reinforce data-centric underwriting and amplify the telematics market’s growth.

Government eCall and AIS 140 regulations

The EU’s eCall rule made emergency-call systems mandatory in new light vehicles from March 2018, cutting response times by 40% in cities and 50% in rural areas while saving an estimated 2,500 lives annually. The European Commission is now finalizing standards for aftermarket eCall devices to guarantee consistent performance. India’s AIS 140 standard obliges GPS tracking in commercial vehicles and is spurring demand for certified 4G units from suppliers such as Watsoo. Together, these mandates set a universal connectivity baseline that unlocks additional value-added services like insurance telematics and predictive maintenance, widening the telematics market footprint.

5G/edge-enabled over-the-air analytics

Low latency 5G coupled with edge computing lets manufacturers push software updates and run predictive algorithms in real time, moving telematics from passive logging to active problem prevention. Movimento and Aricent’s Closed-Loop OTA Analytics processes 5.4 terabytes of sensor data daily, highlighting the massive data flows that next-gen networks must handle. Global cellular IoT links are forecast to hit 6.4 billion by 2029, and a significant share will come from connected vehicles. Predictive maintenance alerts, V2X messaging and high-precision positioning all rely on 5G, cementing its strategic role in the telematics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cybersecurity compliance cost | -1.40% | Global, with stricter requirements in EU and developed markets | Short term (≤ 2 years) |

| High upfront TCU hardware price volatility | -1.10% | Global, with supply chain concentration in Asia | Medium term (2-4 years) |

| Multi-jurisdictional data-sovereignty hurdles | -0.80% | Global, with complex requirements in EU, US, China | Long term (≥ 4 years) |

| Inertia in legacy commercial fleets | -0.70% | North America and Europe, mature fleet markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating cybersecurity compliance cost

UNECE WP.29 obliges automakers to operate certified Cyber Security Management Systems across the vehicle lifecycle. Compliance demands continuous monitoring, incident reporting and secure update channels, which raises engineering costs and lengthens development cycles. ISO/SAE 21434 adds lifecycle risk-management steps, while the U.S. now blocks connected-vehicle components sourced from certain countries, forcing supply-chain audits. Vendors like HARMAN have built consulting practices to help OEMs navigate certification, showing that compliance is transforming from an engineering task to a line-item expense. Smaller suppliers may struggle to shoulder these costs, slowing new-entrant momentum within the telematics market.

High upfront TCU hardware price volatility

Chip shortages, rising silicon complexity and geopolitical trade frictions are doubling semiconductor content per vehicle from USD 600 to USD 1,200 by 2030. Supply bottlenecks have already delayed fleet upgrades, with vendors like MiX by Powerfleet reporting shipment lags that hinder telematics deployments. Component obsolescence is accelerating as 5G modules replace 4G, leaving inventories at risk of write-offs. These factors inject pricing uncertainty that complicates ROI calculations for fleets, particularly in developing markets where capital budgets are thin, curbing near-term expansion of the telematics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Channel: Aftermarket dominance faces OEM challenge

Aftermarket solutions held 56.30% of the telematics market share in 2025, reflecting their historical role in retrofits and mixed fleets. OEM systems are scaling faster at an 11.62% CAGR to 2031, signalling a pivot toward factory-installed connectivity that delivers cleaner data streams and seamless warranty integration. The telematics market benefits from this dual-channel structure because older vehicles still need retrofit devices, while new cars roll off the line connected.

Regulatory standardization of aftermarket eCall ensures that third-party providers remain relevant, yet OEM data-sharing rules like the EU Data Act favour embedded channels. As automakers commercialize connected-car subscriptions, they capture more downstream value, narrowing the aftermarket’s margin pool. Providers are thus emphasizing analytics and cross-fleet compatibility to preserve their position in the telematics market.

By Solution: Embedded systems lead integration wave

Embedded units accounted for 47.80% of the telematics market size in 2025 and exhibit the highest growth at a 12.94% CAGR. The shift is propelled by predictive maintenance, battery management in EVs, and regulatory data-sharing obligations that all require deep vehicle integration. Smartphone-based offerings remain viable in cost-sensitive fleets, but performance and data fidelity lag behind embedded architectures.

Fleet operators prefer embedded hardware for mission-critical analytics such as smart charging algorithms that cut energy expenses by 55% in electric fleets. As 5G modules become standard, embedded solutions will dominate advanced applications like V2X and high-accuracy positioning, cementing their strategic weight in the telematics market.

By Offering Type: Services drive value creation

Services captured 45.70% of total revenue in 2025, led by mid-tier bundles that balance cost with advanced analytics. High-end services are climbing at a 12.63% CAGR as fleets demand AI-driven insights, eco-scores, and predictive alerts. Hardware is increasingly commoditized, and its margin compression is steering vendors toward recurring software revenues within the telematics market.

Cambridge Mobile Telematics’ eco-score expansion illustrates how differentiated algorithms attract premium pricing. As cyber regulations tighten, compliance-as-a-service models may add another layer of high-end offerings, further elevating the service component of the telematics market size.

By Vehicle Type: Commercial vehicles accelerate adoption

Passenger cars held a 51.05% share in 2025 due to mandatory eCall, yet heavy commercial vehicles will post the fastest 12.31% CAGR as fleet owners leverage telematics to lower total operating cost. Light commercial vehicles stand between consumer comfort and professional duty cycles, supporting stable adoption curves.

Workhorse’s integration of Geotab analytics shows OEMs embedding connectivity to unlock maintenance and routing efficiencies in delivery fleets. Regulatory ELD mandates and rising fuel costs make telematics indispensable in trucking, enriching the commercial slice of the telematics market.

By Application: Fleet management dominates, mobility services emerge

Fleet management led with a 38.25% share in 2025 because it directly cuts operating expenses and keeps fleets compliant. Car-sharing and subscription services are growing at a 13.20% CAGR, driven by urban consumers who value pay-per-use mobility. Insurance telematics, navigation, and predictive maintenance occupy specialized niches but benefit from the same data backbone.

Rental operators aim to boost utilization from 40% in 2023 to 75% by 2028, underscoring how telematics underpins scalable mobility models. As multimodal platforms aggregate bikes, scooters, and cars, integration demands will widen, carving fresh growth tunnels in the telematics market.

Geography Analysis

Europe led the telematics market with a 31.95% share in 2025, underpinned by mandatory eCall, GDPR protections, and an installed base of 27.6 million fleet management units projected by 2028. The EU Data Act, effective in 2025, compels data sharing and is expected to stimulate a new wave of third-party services while maintaining privacy safeguards. Suppliers are branding connectivity suites, such as Continental’s Aumovio, to meet tighter integration and compliance demands.

Asia-Pacific is the fastest-growing region, forecast at a 12.26% CAGR through 2031. India’s AIS 140 mandate and the government’s geospatial investment of INR 100 crore (USD 12 million) will broaden foundational mapping infrastructure. China’s new driver-assistance safety rules also raise the bar for OEM connectivity. Rapid urbanization and large commercial fleets create volume, pulling global vendors into local partnerships and expanding the telematics market size across the region.

North America maintains a mature but still growing base, helped by ELD mandates and sizeable government-fleet deployments such as the US General Services Administration’s 400,000-vehicle contract with Geotab. Fleet management units in the Americas are projected to reach 43 million by 2028. Supply-chain security rules limiting certain foreign components could elevate hardware costs yet may also spur domestic chip investments that stabilize long-term supply for the telematics market.

Competitive Landscape

The telematics market exhibits moderate fragmentation. Powerfleet’s USD 200 million acquisition of Fleet Complete created a 2.6 million-subscriber entity with USD 400 million revenue, illustrating a consolidation trend aimed at scaling software and data analytics. Continental divested Zonar to GPS Trackit to focus on core ADAS and mobility platforms, signalling portfolio realignment among tier-one suppliers.

Technology differentiation is moving toward AI-driven capabilities. Verizon Connect won an IoT award for its real-time video dashcam, and Allstate secured a patent for machine-learning-based driving assistance, both demonstrating competitive emphasis on safety and analytics. Vendors offering WP.29 cybersecurity compliance consulting, such as HARMAN, gain an edge as regulatory complexity deepens.

Strategic alliances are another hallmark. Bridgestone partnered with Geotab to merge tire and telematics data from 4.5 million connected vehicles, aiming to cut emissions and improve safety through joint algorithms. Platform Science plans to acquire Trimble’s transportation telematics unit, reinforcing a software-centric route toward integrated fleet platforms. M&A, AI innovation and compliance expertise thus shape competitive dynamics in the telematics market.

Telematics Industry Leaders

Mix Telematics

AT&T Inc.

Geotab Inc.

Verizon Telematics

Cisco Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Geotab unveiled next-generation GO and GO Plus telematics units featuring on-device AI, Wi-Fi hotspot capability and satellite-ready tracking, with North American availability slated for Q2 2026.

- February 2026: Verizon Connect was named “Top Video Telematics Innovator” in ABI Research’s 2026 commercial ranking for its AI-enabled dash-cam ecosystem.

- February 2026: Geotab launched the GO Anywhere family of rugged asset trackers, the first commercial IoT devices to blend cellular with Starlink Direct-To-Cell satellite coverage.

- January 2026: Verizon Connect published its 2026 Fleet Technology Trends Report, highlighting that 80% of fleets now employ at least one connected solution and that AI video telematics users report a 19% drop in accident costs.

Global Telematics Market Report Scope

Telematics is a system with information technology and telecommunication capabilities that can be used extensively for monitoring remote and movable objects such as automobiles, including vehicles used for various industries' fleet transportation.

The telematics market is segmented by channel (OEM, aftermarket), by solution (smartphone, portable, and embedded), by offering type (hardware, services), and by geography (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided for a value of USD for all the above segments.

By Channel

| Original-Equipment Manufacturer (OEM) |

| Aftermarket |

By Solution

| Embedded |

| Smartphone-based |

| Portable/Plug-in |

By Offering Type

| Hardware |

| Services - Entry-level |

| Services - Mid-tier |

| Services - High-end |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles (LCV) |

| Heavy Commercial Vehicles (HCV) |

By Application

| Fleet Management |

| Insurance Telematics |

| Predictive Maintenance and Diagnostics |

| Navigation and Infotainment |

| Car-sharing and Subscription Services |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Channel | Original-Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Solution | Embedded | |

| Smartphone-based | ||

| Portable/Plug-in | ||

| By Offering Type | Hardware | |

| Services - Entry-level | ||

| Services - Mid-tier | ||

| Services - High-end | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCV) | ||

| Heavy Commercial Vehicles (HCV) | ||

| By Application | Fleet Management | |

| Insurance Telematics | ||

| Predictive Maintenance and Diagnostics | ||

| Navigation and Infotainment | ||

| Car-sharing and Subscription Services | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the telematics market in 2031?

The telematics market is forecast to reach USD 92.93 billion by 2031.

How fast is the telematics market expected to grow?

It is projected to expand at a 9.86% CAGR between 2026 and 2031.

Which region leads current telematics adoption?

Europe holds the largest share at 31.95% in 2025 due to strong regulatory frameworks.

Which application segment is growing the fastest?

Car-sharing and subscription services are advancing at a 13.20% CAGR.

Why are embedded solutions gaining traction?

Factory-integrated units satisfy data-sharing mandates and support advanced analytics, leading to a 12.94% CAGR.

What is a key restraint for market growth?

Rising cybersecurity compliance costs under UNECE WP.29 and ISO/SAE 21434 reduce margins for smaller suppliers.

Page last updated on: