Telemetric Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

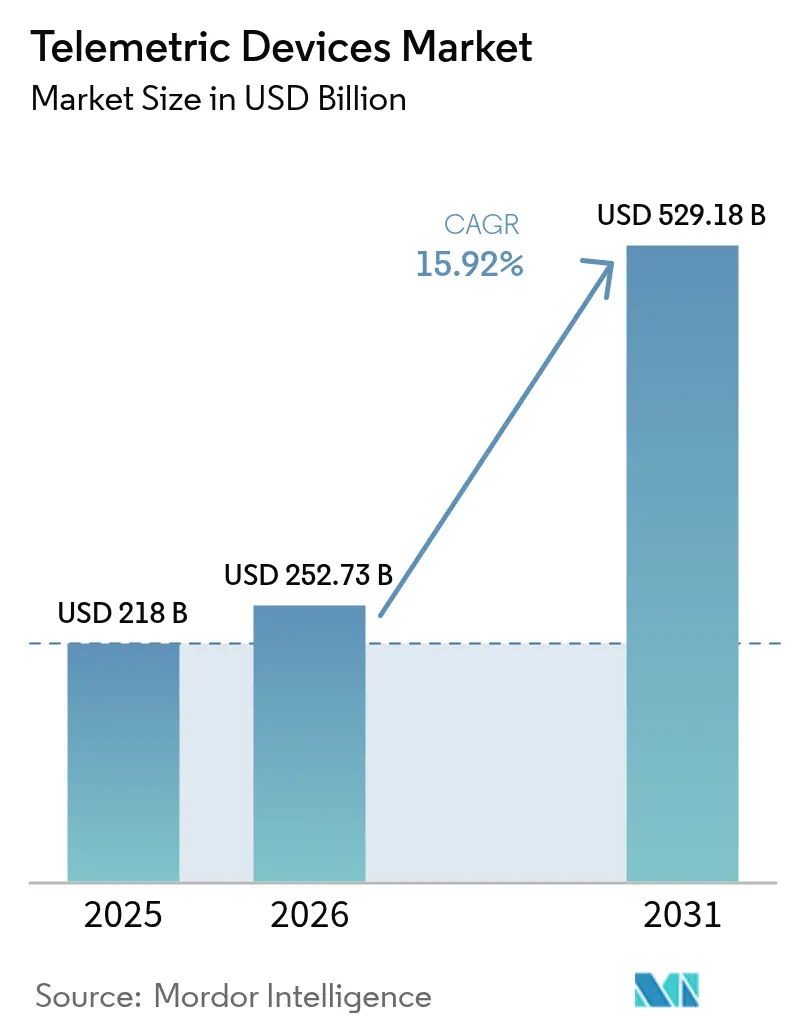

| Market Size (2026) | USD 252.73 Billion |

| Market Size (2031) | USD 529.18 Billion |

| Growth Rate (2026 - 2031) | 15.92% CAGR |

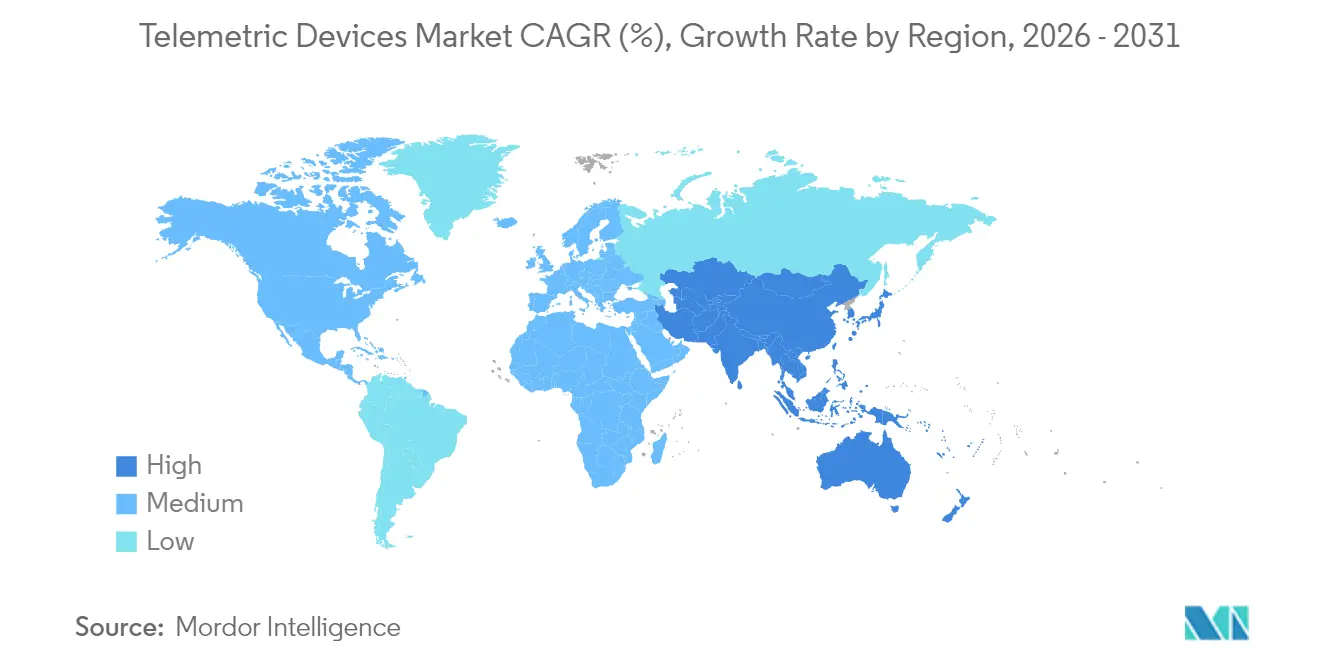

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Telemetric Devices Market Analysis by Mordor Intelligence

Telemetric Devices Market size in 2026 is estimated at USD 252.73 billion, growing from 2025 value of USD 218 billion with 2031 projections showing USD 529.18 billion, growing at 15.92% CAGR over 2026-2031.

Demand is shifting from reactive monitoring toward predictive intelligence across healthcare, industrial, energy, and defense domains. Growth springs from miniaturized biosensors entering clinical trials, satellite-IoT constellations that extend coverage to remote areas, and low-power wide-area (LPWA) modules that lower connectivity costs for small and mid-sized enterprises. Healthcare remains the largest application, industrial predictive-maintenance programs continue to scale, and regulatory mandates for real-time asset tracking sustain the sector’s strong outlook.

Key Report Takeaways

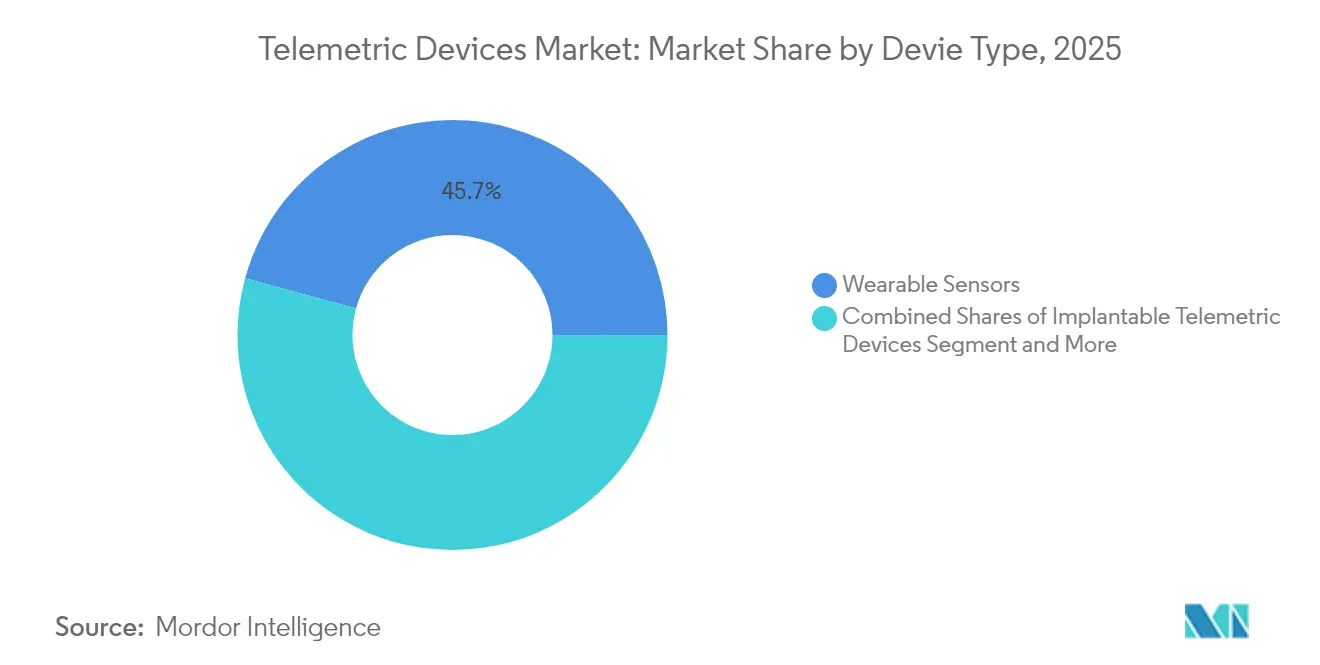

- By device type, wearable sensors led with 45.74% of telemetric devices market share in 2025, while ingestible capsules are projected to grow at an 18.41% CAGR through 2031.

- By component, hardware retained 51.35% of the telemetric devices market size in 2025; software analytics is poised for a 16.02% CAGR to 2031.

- By communication technology, cellular solutions held 47.88% share of the telemetric devices market in 2025, whereas LPWAN protocols show the fastest growth at a 18.86% CAGR.

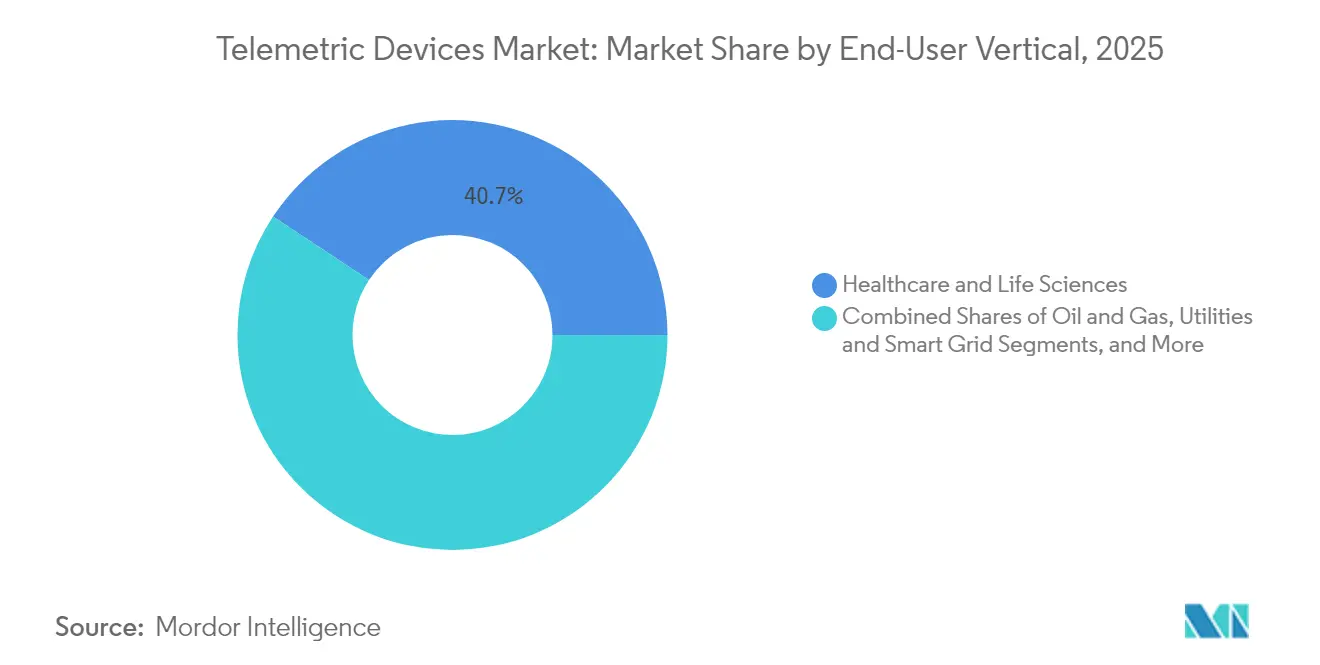

- By end-user vertical, healthcare commanded 40.72% revenue share in 2025 in telemetric devices market, and transportation and logistics is forecast to expand at a 16.74% CAGR through 2031.

- By region, North America captured 37.46% of the telemetric devices market share in 2025; Asia Pacific is advancing at a 17.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Telemetric Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of IoT-enabled healthcare and wearable monitoring | +4.2% | North America and Europe | Medium term (2-4 years) |

| Industrial shift toward predictive maintenance | +3.8% | APAC manufacturing hubs | Long term (≥ 4 years) |

| Regulatory mandates for real-time asset tracking | +2.1% | North America and EU | Short term (≤ 2 years) |

| Falling cost of LPWA modules | +2.9% | Emerging markets worldwide | Medium term (2-4 years) |

| Satellite-IoT constellations for remote telemetry | +1.8% | Remote regions in APAC and Africa | Long term (≥ 4 years) |

| Miniaturized implantable biosensors in trials | +1.4% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosion of IoT-Enabled Healthcare and Wearable Monitoring

Healthcare telemetry is moving beyond bedside monitors to preventive wellness solutions. The University of Hong Kong’s organic electrochemical transistor platform processes patient data locally, cutting transmission costs and latency. Nanotechnology now shrinks continuous-glucose sensors by 95% without performance loss.[1]T. Liu, “Nanotechnology Advances in Glucose Monitoring,” mdpi.com AI-enhanced algorithms embed predictive analytics in wearables to forecast acute events. Clinical trials of wirelessly controlled drug-delivery microchips show adherence gains that rival traditional injections. These advances transform connected devices from passive recorders into active therapeutic tools.

Industrial Shift Toward Predictive Maintenance

Oil and gas wells can generate more than 10 TB of sensor data each day; analytics platforms now identify maintenance windows that avoid costly shutdowns.[2]BDO Insights, “Oil & Gas Digital Transformation,” bdo.com Edge devices installed on offshore rigs process information locally, preventing safety risks tied to network latency. Utilities adopting Industry 4.0 practices report sizeable cuts in unplanned downtime. Japanese plants deploy on-premise monitoring systems to offset labor shortages, reinforcing global appeal for autonomous asset care. Cost-avoidance incentives keep industrial telemetry growth intact through 2030.

Regulatory Mandates for Real-Time Asset Tracking (Oil and Gas, Aviation)

Regulators now treat continuous telemetry as a prerequisite for operating critical infrastructure. The U.S. Bureau of Safety and Environmental Enforcement emphasizes real-time offshore monitoring to prevent spills. Aviation authorities expand tracking rules from flight-data recorders to entire maintenance systems, raising adoption in airlines and MRO providers. Smart-grid standards issued by NIST drive utilities to combine telemetric devices with grid-edge intelligence. FCC allocations for unmanned aircraft unlock dedicated frequencies for telemetry applications, underscoring federal commitment to always-on monitoring.

Falling Cost of LPWA Modules

Commodity pricing for LPWA hardware now puts large-scale telemetry within reach of small businesses. LoRaWAN modules deliver multi-year battery life for sparse deployments, while NB-IoT suits high-density urban use cases. With chip supplies stabilizing in 2025, module vendors scale production at lower cost. Enterprises favor private LoRaWAN networks for data sovereignty and key management. As costs fall further, the telemetric devices market finds fresh demand in agriculture, utilities, and smart-city lighting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront hardware and integration costs | -2.8% | Emerging markets worldwide | Short term (≤ 2 years) |

| Data-privacy and cybersecurity concerns | -2.1% | EU and North America | Medium term (2-4 years) |

| Spectrum congestion in sub-GHz bands | -1.4% | Dense urban areas | Medium term (2-4 years) |

| Proprietary protocol fragmentation | -1.9% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Hardware and Integration Costs

Capital expenses remain a hurdle, particularly for small enterprises. Chip supply volatility, exposed by raw-material shortages in 2024, pushed component prices higher and delayed new projects. Integration with decades-old machinery needs custom middleware, inflating budgets. Automakers such as Ford have adjusted production lines in response to electronics shortages, illustrating ripple effects on telemetry suppliers. Vendors respond with modular, plug-and-play architectures, yet complex industrial environments still rely on bespoke engineering, prolonging ROI timelines.

Data-Privacy and Cybersecurity Concerns

Connected devices create expansive attack surfaces. The FDA’s new Quality System Regulation final rule effective February 2026 imposes stricter security controls on medical telemetry. Industrial control systems now bridge operational and IT networks, inviting cyber threats that could disrupt national infrastructure. EU data-localization laws add encryption and auditing costs. Security-by-design frameworks help, but new compliance layers slow decision making in risk-averse industries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Ingestible Capsules Accelerate Internal Monitoring

Wearable sensors held 45.74% of telemetric devices market share in 2025, underscoring consumer familiarity with wristbands and patches. Ingestible capsules now represent the most dynamic category, advancing at an 18.41% CAGR through 2031 as clinicians embrace non-invasive internal diagnostics. Swallowable capsule robots that anchor to intestinal tissue enable multi-day monitoring without external intervention. Sub-0.1-mm³ temperature sensors add new diagnostic options while leaving no surgical footprint. Remote fixed-site modules remain essential for harsh industrial environments such as upstream oil pipelines. Wearable formats move toward on-device AI, transforming basic readings into personalized early-warning systems. Bio-degradable materials under study could phase out removal surgeries, improving patient acceptance and broadening use cases for the telemetric devices market.

Healthcare innovators prioritize ingestible telemetry because internal data yield richer clinical insight than surface sensors. Capsule endoscopy evolved from still-image capture to live data streaming, supported by LPWA back-haul that extends battery life. Athletes and soldiers test ingestible thermometers for core-temperature surveillance in extreme climates. These developments point to a future where internal sensors complement external wearables, together delivering holistic patient profiles.

By Component: Software Analytics Command Value Creation

In 2025, hardware captured 51.35% of telemetric devices market size, reflecting the cost of sensors, microcontrollers, and antennas. Software analytics, however, post a 16.02% CAGR to 2031, emphasizing the pivot from raw data to actionable insight. Edge-processing libraries compress time-series information locally before cloud upload, cutting bandwidth by up to 90%. Power-management chips with energy-harvesting inputs now double service life in remote meters. As device count grows, orchestration platforms that manage firmware and security updates at scale distinguish leading vendors.

Predictive-maintenance suites integrate physics-based models with machine-learning classifiers, enabling operators to schedule service only when probability of failure rises. Healthcare analytics engines combine multi-sensor streams to generate early diagnostic flags, pushing reimbursement models toward outcome-based care. With interoperability gaining importance, open-API platforms position themselves as the glue connecting diverse hardware in the telemetric devices market.

By End-User Vertical: Transportation and Logistics Gain Momentum

Healthcare retained 40.72% of 2025 revenue owing to chronic-disease management and hospital-at-home initiatives. Transportation and logistics, however, is set to expand at a 16.74% CAGR, driven by fleet telematics, cold-chain monitoring, and autonomous-vehicle development. GPS-enabled trackers paired with predictive algorithms boost fleet productivity and slash fuel use, with 75% of managers confirming efficiency gains. Oil-pipeline operators employ fiber-optic telemetry to sense leaks in real time, complying with tightening environmental regulations. Aerospace programs integrate secure satellite links for missile-defense telemetry, attracting sizeable defense budgets.

Beyond conventional sectors, agriculture adopts soil-moisture sensors to optimize irrigation and reduce water use. Utilities deploy smart meters that transmit voltage and consumption every few minutes, sharpening grid stability. The breadth of industry uptake reinforces the telemetric devices market’s diversified growth trajectory.

By Communication Technology: LPWAN Challenges Cellular Supremacy

Cellular networks owned 47.88% market share in 2025, leveraging 4G/5G infrastructure for high-bandwidth applications such as video telematics. LPWAN solutions, including LoRaWAN and NB-IoT, register the steepest ascent at 18.86% CAGR, valued for ultra-low power and deep-indoor reach. Analysts expect LoRaWAN and NB-IoT to account for 3.5 billion connections by 2030.. Satellite Non-Terrestrial Networks (NTNs) extend coverage to deserts and oceans, with Myriota HyperPulse enabling sensor backhaul from any latitude. Bluetooth LE and Wi-Fi retain roles in wearables and home-automation hubs.

Hybrid modems combining cellular and LoRaWAN ensure redundancy for mission-critical sites. Private LPWAN deployments give enterprises autonomy over data flows and encryption keys, addressing sovereignty concerns. As roaming fees fall and roaming agreements widen, cross-border asset tracking becomes more feasible, further broadening the telemetric devices market.

Geography Analysis

North America captured 37.46% of telemetric devices market share in 2025, propelled by mandatory real-time tracking in aviation and energy. The Space Development Agency’s USD 4.3 billion allocation to next-generation satellites underpins domestic demand for secure telemetry. Honeywell’s joint initiative with Verizon embeds 5G links into smart meters, illustrating public-utility modernization. The FCC’s new 6 GHz VLP rules accommodate additional device classes, stimulating innovation. Robust healthcare infrastructure fosters rapid adoption of implantable cardiac monitors, strengthening the region’s lead.

Asia Pacific is forecast to grow at 17.18% CAGR to 2031. China’s NB-IoT base alone is expected to reach 1.9 billion connections, driven by state subsidies and manufacturing scale. Japan’s Sinto Corporation fields on-premise monitoring to counter factory labor shortages. India’s smart-city programs mandate sensor deployments for traffic, water, and air-quality management. Local chip fabrication along with supportive telecom policies, allow regional firms to price hardware aggressively, broadening domestic adoption and positioning the area as a supply-chain hub for the telemetric devices market.

Europe maintains steady expansion on the back of smart-grid rollouts and climate-action regulations. Smart-meter penetration reached 60% for electricity and 45% for gas by 2023, providing a platform for grid-edge telemetry. Siemens generated EUR 75.9 billion in 2024 revenue with digitalization cited as a growth engine. Strict GDPR compliance rules shape design choices, pushing vendors toward stronger encryption and regional data centers. Environmental monitoring networks measure CO₂ and methane at industrial sites, supporting the EU’s Green Deal objectives and creating new telemetric devices market demand.

Competitive Landscape

Competition is moderately fragmented. Traditional medical-device makers extend into industrial telemetry, while software firms add hardware to own the full stack. Siemens invested EUR 6.3 billion in R&D during 2024, underscoring the capital required to stay ahead.[4]Siemens AG Annual Report 2024, siemens.comPlatform Science’s purchase of Trimble’s transportation-telematics units, worth USD 300 million in annual revenue, shows ongoing consolidation. L3Harris won a USD 919 million satellite-payload contract, illustrating defense influence on advanced telemetry features.

White-space opportunities abound in ultra-low-power segments such as wildlife tracking and structural-health monitoring. Vendors differentiate through analytics sophistication and cross-platform interoperability rather than hardware alone. Proprietary ecosystems still lock in some customers, but RESTful APIs and Matter-compliant frameworks continue to erode barriers. The balance of power is tilting toward companies that fuse AI, edge computing, and multi-bearer connectivity into seamless services for the telemetric devices market.

Telemetric Devices Industry Leaders

Siemens AG

GE Healthcare

Philips Healthcare

Schlumberger Limited.

Schneider Electric

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Medtronic posted USD 33.5 billion revenue, up 3.6%, propelled by BrainSense™ Adaptive DBS telemetry innovations.

- April 2025: Boston Scientific recorded 20.9% net-sales growth to USD 4.663 billion and began FARAFLEX pulsed-field ablation trials.

- March 2025: Honeywell joined Verizon to embed 5G into smart meters for real-time grid telemetry.

- February 2025: Myriota and Viasat launched HyperPulse, the first 5G NTN service dedicated to remote IoT.

Global Telemetric Devices Market Report Scope

With the growing requirement of remote monitoring, the applications of telemetric devices have become ample. These devices are used for measuring and collecting data via wireless transmission from remote sources. The devices have applications in various end-user verticles such as connected devices, healthcare, industrial, oil & gas, and many more.

| Wearable Telemetric Sensors |

| Implantable Telemetric Devices |

| Ingestible Telemetry Capsules |

| Remote Fixed-site Modules |

| Sensors and Transducers |

| Telemetry Communication Module |

| Antennas and Power Management |

| Software / Analytics Platform |

| Healthcare and Life Sciences |

| Industrial and Manufacturing |

| Oil and Gas (Upstream and Midstream) |

| Aerospace and Defense |

| Transportation and Logistics |

| Utilities and Smart Grid |

| Cellular (3G/4G/5G) |

| Satellite |

| LPWAN (NB-IoT, LoRa, Sigfox) |

| Bluetooth / Wi-Fi |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Device Type | Wearable Telemetric Sensors | ||

| Implantable Telemetric Devices | |||

| Ingestible Telemetry Capsules | |||

| Remote Fixed-site Modules | |||

| By Component | Sensors and Transducers | ||

| Telemetry Communication Module | |||

| Antennas and Power Management | |||

| Software / Analytics Platform | |||

| By End-User Vertical | Healthcare and Life Sciences | ||

| Industrial and Manufacturing | |||

| Oil and Gas (Upstream and Midstream) | |||

| Aerospace and Defense | |||

| Transportation and Logistics | |||

| Utilities and Smart Grid | |||

| By Communication Technology | Cellular (3G/4G/5G) | ||

| Satellite | |||

| LPWAN (NB-IoT, LoRa, Sigfox) | |||

| Bluetooth / Wi-Fi | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the telemetric devices market?

The market is worth USD 252.73 billion in 2026 and is projected to reach USD 529.18 billion by 2031 at a 15.92% CAGR.

Which device type is growing the fastest?

Ingestible capsules lead growth with an 18.41% CAGR through 2031, reflecting rising demand for internal monitoring solutions.

Why are LPWAN protocols gaining traction over cellular?

LPWAN offers multi-year battery life and lower connectivity costs, driving a 18.86% CAGR even though cellular still holds 47.88% market share.

Which region will expand the most by 2031?

Asia Pacific shows the highest regional CAGR at 17.18% due to industrial IoT adoption and large-scale smart-city projects.

How are regulators influencing telemetric device adoption?

Mandates for real-time asset tracking in sectors such as aviation, oil, and gas, along with new cybersecurity rules for medical devices, are accelerating deployment across multiple industries.

What factors currently restrain market growth?

High upfront integration costs, cybersecurity concerns, and spectrum congestion in sub-GHz bands are the primary brakes on wider adoption.

Page last updated on: