Voice Cloning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.02 Billion |

| Market Size (2031) | USD 9.53 Billion |

| Growth Rate (2026 - 2031) | 25.84% CAGR |

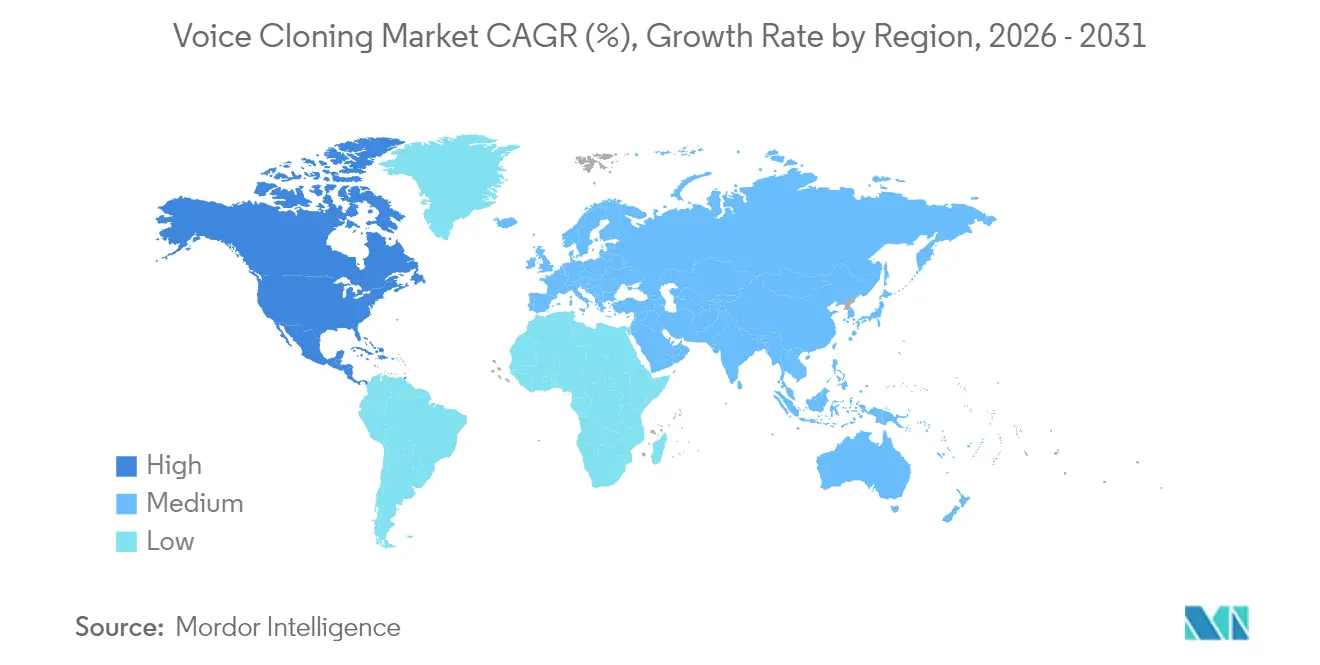

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

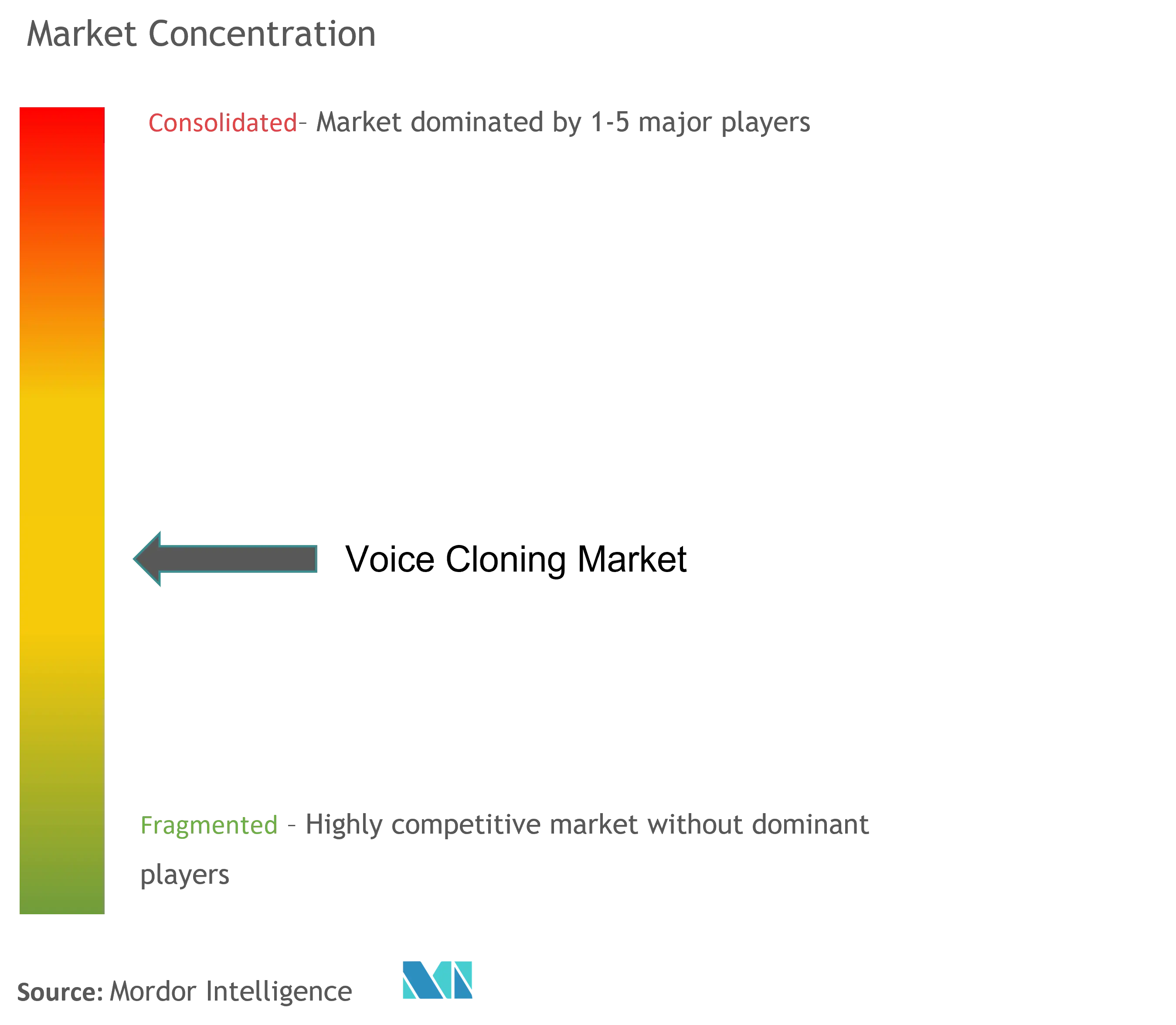

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Voice Cloning Market Analysis by Mordor Intelligence

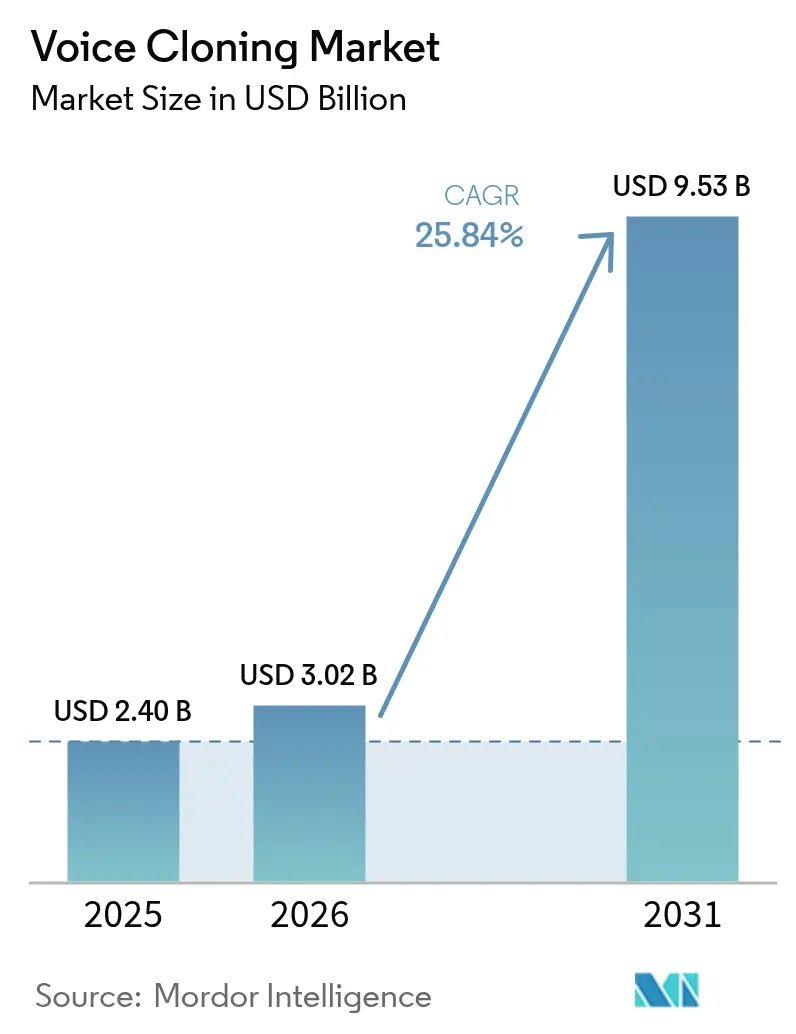

The Voice Cloning Market size was valued at USD 2.40 billion in 2025 and estimated to grow from USD 3.02 billion in 2026 to reach USD 9.53 billion by 2031, at a CAGR of 25.84% during the forecast period (2026-2031).

Strong demand for hyper-personalized customer engagement, rapid neural network innovation, and falling API pricing are pushing the voice cloning market into mainstream enterprise budgets. North America remains the center of gravity, yet Asia Pacific’s mobile-first commerce culture is steering the fastest regional gains. Neural text-to-speech now delivers near-human naturalness, creating new revenue streams in media, gaming, healthcare, and assistive communication. At the same time, regulators are tightening guardrails, prompting vendors to ship watermarking and consent management functions as standard controls rather than premium add-ons.

Key Report Takeaways

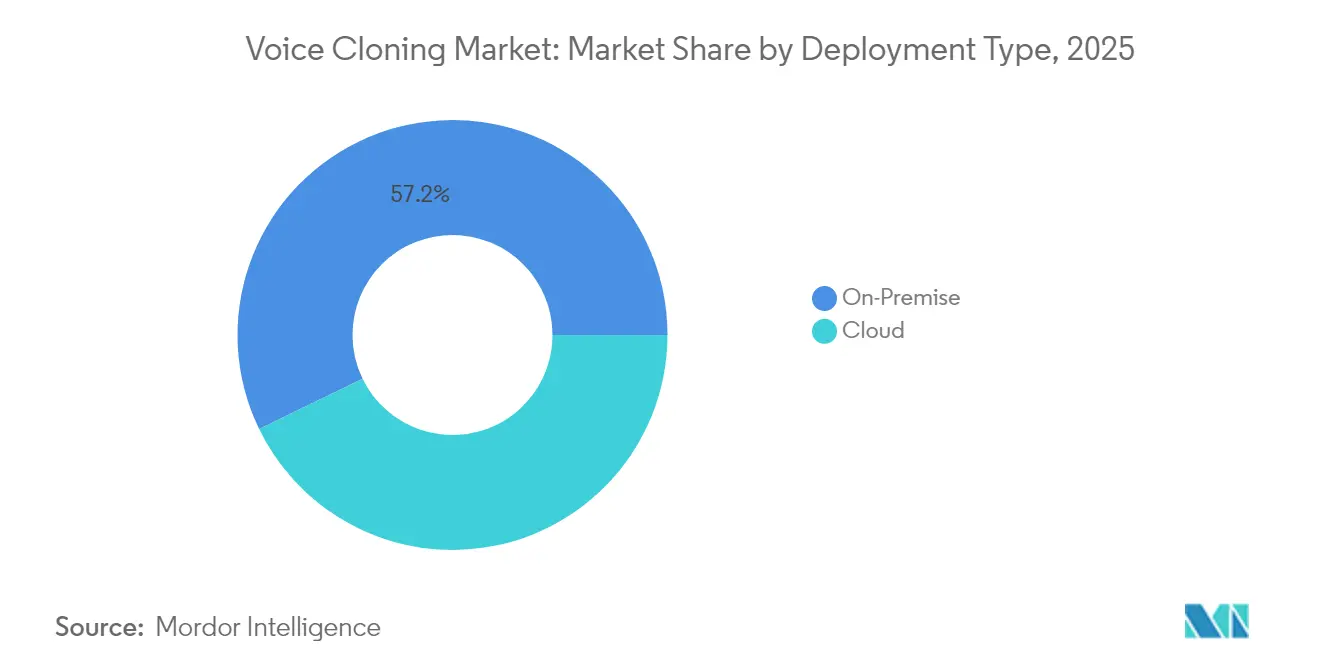

- By deployment type, cloud deployments captured 42.80% revenue share in 2025, while the segment is expanding at a 29.82% CAGR through 2031.

- By component, solutions held 71.10% of the voice cloning market share in 2025, whereas services are projected to advance at a 28.93% CAGR to 2031.

- By voice-cloning method, neural and deep-learning approaches lead with 64.40% share in 2025 and are anticipated to grow at a 34.95% CAGR.

- By application, chatbots and voice assistants represented 33.50% of the voice cloning market size in 2025, yet interactive games are tracking a 32.88% CAGR over 2026-2031.

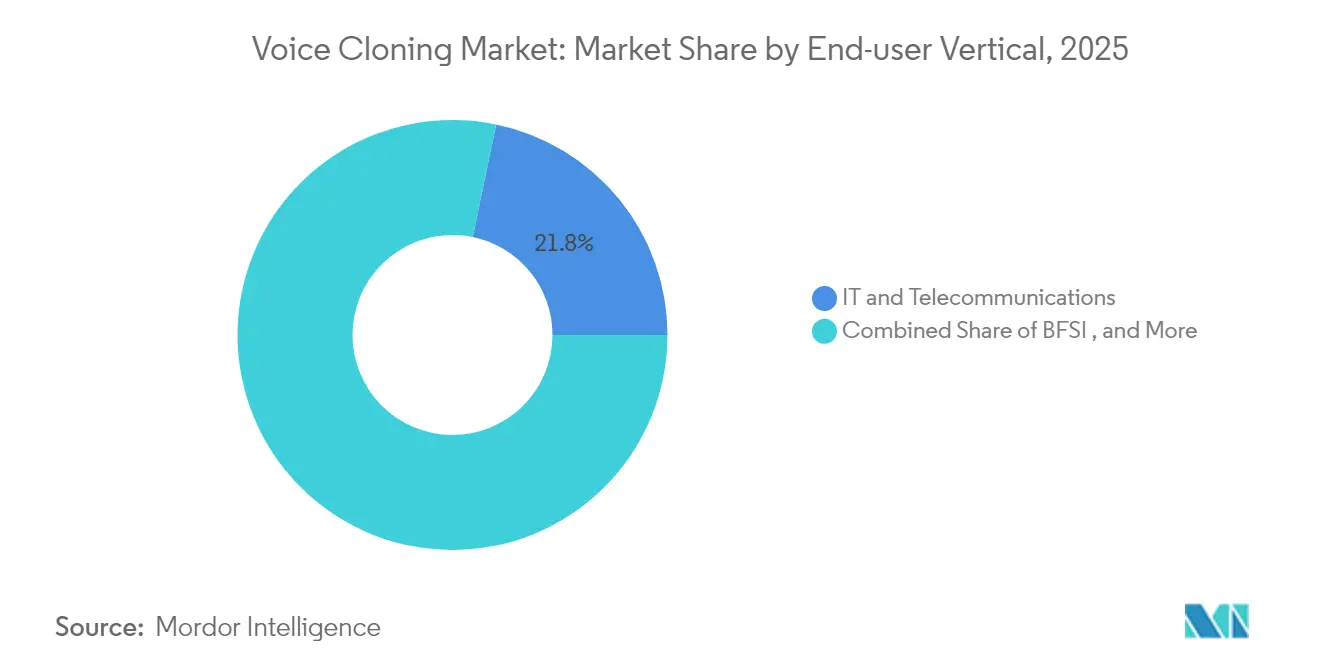

- By end-user vertical, IT & telecommunications accounted for 21.75% share in 2025, while healthcare & life sciences are on course for a 30.78% CAGR to 2031.

- By geography, North America commanded 38.70% of 2025 revenue, and Asia Pacific is forecast to rise at a 27.42% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Voice Cloning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of AI-generated personal voices for media localization | +7.80% | North America, Europe | Medium term (2-4 years) |

| Rapid integration in conversational commerce | +6.50% | Asia Pacific | Short term (≤ 2 years) |

| Accessibility mandates in public digital services | +5.20% | Europe | Medium term (2-4 years) |

| SaaS Voice-API monetization | +4.30% | Global | Short term (≤ 2 years) |

| Multilingual digital advertising | +3.60% | Global | Short term (≤ 2 years) |

| Digital avatars for the metaverse | +3.10% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adoption of AI-generated Personal Voices for Media Localization by North-American Streaming Platforms

Major streaming studios now release multi-language premieres simultaneously by rendering localized dialogue with neural voice clones that preserve the original actor’s vocal fingerprint. Production teams report 40% cost savings and 60% faster dubbing cycles after switching from traditional voice-over workflows. The new economics allow smaller catalog titles to secure high-quality localization, widening global reach. As international viewers contributed more than 60% of new subscriptions in 2024, investing in premium yet scalable voice workflows became a board-level priority. Competitive pressure is forcing late adopters to modernize rapidly, sustaining double-digit momentum in the voice cloning market.

Rapid Integration of Voice Cloning in Conversational Commerce across Asian Retail

Chinese, Japanese, and Korean retailers embed branded voice personalities inside shopping apps to guide purchasing journeys. Pilot projects boosted conversion rates by 23% on flagship e-commerce platforms. Voice cloning restores the advisory element of brick-and-mortar retail, yet scales to millions of concurrent sessions. Mobile shoppers benefit from hands-free navigation, reducing friction on small screens. With Asia Pacific already accounting for more than 60% of global mobile commerce revenue, conversational voice is evolving from novelty to necessity. This regional lead will ripple outward as global brands mimic proven templates.

Accessibility Mandates Driving Synthetic Speech in European Public Digital Services

The European Accessibility Act sets a 2025 deadline for equal digital experiences, prompting rapid public-sector spending on high-quality synthetic speech. Implementation counts surged 64% in 2024 as ministries adopted voice cloning for websites, call centers, and transport announcements. Government tenders now specify neural speech quality and watermarking to deter misuse. Vendors equipped with compliance toolkits enjoy an early-mover advantage. Because public-service contracts often span multiple years, this driver creates predictable demand streams that cushion the voice cloning market against cyclical private-sector swings.

SaaS Voice-API Monetization Accelerating Cloud Deployments Worldwide

Consumption-based Voice-as-a-Service pricing eliminates heavy upfront licensing, inviting mid-market firms into the voice cloning market. Cloud APIs achieve sub-100 ms latency and 99.9% uptime, clearing the bar for customer-facing workloads. Integrators can embed speech in days using SDKs and no-code dashboards. Variable usage tiers align costs with campaign surges or seasonal training bursts, strengthening ROI arguments for finance teams. The cloud trajectory also unlocks global reach, where local GPU shortages previously throttled adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Deepfake voice fraud costs in BFSI | -3.20% | Global | Medium term (2-4 years) |

| High GPU compute costs for SMEs | -2.10% | Global | Short term (≤ 2 years) |

| Fragmented regulation | -1.80% | Global | Medium term (2-4 years) |

| Ethical consent hurdles | -1.40% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Deepfake Voice Fraud Escalating KYC Compliance Costs for BFS

Voice fraud attempts surged 138% in 2024, exposing gaps in first-generation voice biometric systems used by banks and insurers. Financial institutions now layer liveness checks, behavioral analytics, and stepped-up manual reviews onto every high-risk call. These countermeasures raise per-transaction verification costs and prolong customer wait times, eroding some of the efficiency gains that voice cloning promised. Regulators in the United States and Europe have responded by updating KYC guidelines to include explicit controls for synthetic speech, adding more compliance tasks. Several global banks report that voice-specific security upgrades have lifted overall compliance spending by 27% in the past year. Until detection and watermarking tools mature, many firms will defer or limit new voice cloning deployments in customer-facing workflows.

High GPU Compute Costs Hindering SME Adoption of Real-time Neural Synthesis

Real-time neural voice models demand 4-8× more compute than batch TTS engines, pushing workload costs beyond typical SME budgets. Cloud credits help, but still leave a recurring fee that scales linearly with every second of synthesized speech. Latency-sensitive use cases, such as live customer support, force smaller firms to rent premium low-latency GPU instances, compounding expense. Emerging quantization and model-distillation techniques cut inference loads, yet they rarely match the naturalness of full-size models. Consequently, many SMEs restrict voice cloning to low-traffic tasks or settle for lower-fidelity parametric voices that run on CPUs. Broader adoption will depend on further efficiency gains or new pricing schemes that decouple quality from raw GPU consumption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud Accelerates Enterprise Integration

Cloud-hosted platforms represented USD 1.03 billion of the voice cloning market size in 2025, equal to 42.80% revenue share, and are advancing at a 29.82% CAGR to 2031 Flexible resource scaling, global edge nodes, and pay-as-you-go billing make cloud the default choice for new pilots. Vendor roadmaps now prioritize real-time streaming quality at sub-100 ms round-trip, dissolving historical latency concerns. Service level agreements offer 99.9% uptime, reassuring critical use cases in contact centers and live broadcasts. Cloud ecosystems also simplify access to adjacent AI services like translation and sentiment analysis, lowering integration friction for product managers. On-premise installations still command 57.20% revenue share owing to data residency mandates in financial services and healthcare. These buyers require airtight control of biometric data and often pair internal GPU clusters with hybrid orchestration to tap burst cloud capacity for peak demand. Leading suppliers are shipping Docker-ready voice engines and Kubernetes Helm charts, letting DevOps teams integrate voice cloning into existing CI/CD workflows. Edge computing further blurs boundaries by placing inference modules on customer-owned gateways for latency-sensitive tasks while centralizing training in the cloud. As privacy preserving federated learning matures, migration paths from strictly on-premise to hybrid footprints will continue, shrinking pure on-prem holdings over time within the voice cloning market.

By Component: Services Growth Outpaces Solutions

Solutions captured 71.10% of 2025 revenue, yet services are climbing at 28.93% CAGR versus 22.61% for software licences Enterprises now emphasize deployment governance, model fine-tuning, and compliance policy design, all of which demand specialized consulting. Implementation partners staff multidisciplinary teams of linguists, ethicists, and DevSecOps engineers to align voice cloning strategies with brand and legal requirements. New service offerings include voice DNA audits that catalog speaker rights for future disputes. Meanwhile, platform vendors keep pushing the envelope on neural fidelity. Transformer-based engines can build a viable clone from under 30 s of reference audio, streamlining onboarding for talent agencies and medical use cases. Low-bit-rate codec optimization cuts bandwidth by 60% without clipping harmonic detail, enabling over-the-air delivery in automotive infotainment. Governance modules now log every synthesis request with cryptographic hashes, creating immutable trails that satisfy emerging AI audit laws. These advances reinforce the solutions segment’s revenue floor even as service billings expand, maintaining balance inside the voice cloning market.

By Voice-Cloning Method: Neural and Deep-Learning Dominates Innovation

Neural architectures held 64.40% revenue share in 2025, posting a 34.95% CAGR outlook that invalidates earlier concatenative paradigms. Transformer and diffusion models now restore micro-prosody, sibilance, and breathiness once lost in statistical approaches. Training data demands keep falling through unsupervised pretext tasks and speaker adaptation layers, pushing entry costs lower. GPU inference optimizations slash per-request compute by 45%, widening profit margins for SaaS providers. Concatenative systems still power select safety messaging in aviation and public transport, where absolutist phoneme consistency trumps expressive naturalness. Parametric engines remain in niche IVR menus for budget projects, yet their relevance fades as neural licensing costs compress. Research energy now flows into cross-lingual zero-shot synthesis and emotional controllability knobs. These capabilities will cement neural dominance and reinforce buyers’ perception that state-of-the-art equals neural inside the voice cloning market.

By Application: Games Drive Innovation Beyond Assistants

Chatbots and voice assistants accounted for 33.50% revenue share in 2025, cementing their role as baseline cash generators. Banks, airlines, and telcos depend on cloned brand voices to maintain tonal consistency across IVR, smart speakers, and mobile apps. Response libraries stretch into tens of thousands of prompts, demanding scalable synthesis pipelines. However, game studios are the new R&D vanguard, with spend growing at a 32.88% CAGR. Dynamic storytelling engines now generate bespoke dialogue that adapts to player actions without the budget nightmare of recording every branch.Accessibility solutions also ride the growth wave. Personalized prosthetic voices restore identity to patients with degenerative conditions. Hospitals bundle cloning into pre-operative protocols, letting patients bank speech before high-risk procedures. Dubbing and localization further scale as OTT publishers court non-English audiences. Customer service use cases are shifting from rigid scripts toward empathetic, sentiment-aware responses tuned in real time. The breadth of needs means application suppliers can specialize while still tapping core platform APIs, ensuring steady diversification across the voice cloning market.

By End-user Vertical: Healthcare Adoption Accelerates

IT & telecommunications led with 21.75% revenue share in 2025, harnessing cloned voices to reduce average call handling time and improve brand recall. Telcos route millions of monthly IVR calls to virtual agents that speak in regionally nuanced tones. Yet, healthcare & life sciences is the breakout story, tracking a 30.78% CAGR as hospitals modernize patient engagement. Personalized discharge instructions voiced in a familiar accent boost adherence to medication schedules, improving outcomes.Media & entertainment remains the quality trend-setter: blockbuster franchises now localize simultaneously across 40+ languages. Education providers deploy consistent instructor voices across vast course libraries, increasing learner satisfaction. BFSI spending is uneven; fraud concerns slowed rollouts, yet pilot programs mixing voice cloning with liveness detection hint at future mainstreaming once security modules mature. Retail & e-commerce voices unify store, app, and smart-speaker personas, smoothing omnichannel journeys. Government agencies prioritize multilingual outreach and emergency broadcasting, underscoring the public value of robust voice technology. Collectively, these verticals guarantee multi-threaded demand inside the voice cloning market.

Geography Analysis

North America commanded 38.70% of 2025 revenue, anchored by Silicon Valley research clusters and Hollywood media demand. Streaming platforms standardize neural dubbing workflows, setting de facto quality bars that ripple through global production houses. Regulatory scrutiny is palpable: the Federal Trade Commission’s Voice Cloning Challenge invites technologists to propose content authentication solutions, a move that pressures vendors to embed watermarking natively.Despite tighter oversight, venture funding remains buoyant, sustaining a vibrant startup pipeline that feeds enterprise procurement pipelines. Asia Pacific is the growth engine, posting a 27.42% CAGR through 2031. China spearheads multilingual cloning research, driven by its vast e-commerce ecosystems, which require dialect agility. Japanese health-tech firms are deploying synthetic voices tailored for senior citizens, addressing the communication gaps of an aging population. South Korean game publishers experiment with real-time character voice morphing, spotlighting new engagement mechanics. India presents a fertile, linguistically complex market where regional language support can unlock hundreds of millions of new users. Together, these dynamics position Asia Pacific as the fastest-advancing region in the voice cloning market. Europe’s narrative centers on governance and accessibility. The EU AI Act introduces transparency clauses that obligate disclosures when synthetic voices are used, compelling vendors to ship audit dashboards. The European Accessibility Act further entrenches demand within public digital services. Germany’s industrial sector explores voice-enabled robotics on factory floors, while the United Kingdom pilots cloned-voice customer reps across leading banks. Although compliance hurdles extend sales cycles, they ultimately elevate trust, ensuring sustained uptake across continental markets.

Regulatory Landscape

Global governance for voice cloning is shifting from broad consumer-protection enforcement toward explicit synthetic-media transparency and digital-replica rights. In the European Union, the EU AI Act (Regulation (EU) 2024/1689) introduces Article 50 transparency obligations for providers and deployers of deepfakes, requiring synthetic audio to be marked in a machine-readable, detectable way from August 2, 2026, which raises the compliance bar for vendors distributing or operating in the EU.

In the United States, policymakers are converging on a federal framework for unauthorized digital replicas: a revised bipartisan NO FAKES Act was introduced in May 2026 and advanced by the Senate Judiciary Committee on June 18, 2026, proposing liability tied to distribution of unauthorized voice and likeness replicas and outlining procedural mechanisms such as counter-notice. In China, the Cyberspace Administration of China has moved toward mandatory labeling and disclosure in AI-human interaction services, with interim measures referenced as taking effect in mid-2026, reinforcing a multi-jurisdiction compliance reality for global deployments.

Value Chain Analysis

The value chain begins with data acquisition and rights management (voice talent consent, speaker releases, and audio collection), then moves into model development and training by foundational AI labs and platform providers (including Microsoft and other large AI developers). From there, enterprise voice platforms and developer-facing APIs package cloning, text-to-speech, and real-time streaming as production services, feeding into integration layers such as contact-center stacks, conversational AI orchestration, SDKs, and DevSecOps pipelines that operationalize governance through audit logs, watermarking/provenance signals, and consent controls.

Downstream, deployments run on cloud and hybrid infrastructure, distributed via app platforms and enterprise channels, and monetized through usage-based Voice-as-a-Service pricing, professional services, and verticalized workflows (media localization, customer service, and assistive communication). Key bottlenecks concentrate around GPU inference cost for real-time synthesis, multilingual quality assurance, and compliance engineering as rules converge on labeling and disclosure (for example, EU AI Act Article 50 effective August 2026). Vendor strategies increasingly package end-to-end, lower-latency systems to reduce stitching across multi-vendor chains, which shows up in enterprise launches such as Yellow.ai Nexus Vox in May 2026 and platform integrations such as Microsoft Foundry voice capabilities.

Competitive Landscape

Competition is fragmented yet intense. Hyperscale clouds such as Microsoft Azure, Amazon Web Services, Google Cloud, and IBM watsonx exploit global infrastructure and bundled AI suites to lock in enterprise accounts. They differentiate via regional data centers, SOC-2 compliance, and integration with broader AI workflows. Conversely, specialists including ElevenLabs, Resemble AI, and Descript prioritize voice quality, API ergonomics, and creative control. Their nimbleness lets them debut features like emotion sliders and real-time style transfer ahead of larger rivals, forcing incumbents to fast-follow.

Strategic alliances proliferate. ElevenLabs joined forces with Reality Defender to fuse synthesis and detection, delivering end-to-end solutions against deepfake misuse. Resemble AI partners with post-production studios to streamline film dubbing pipelines. Open-source projects democratize access but still lack enterprise-grade observability and SLA guarantees, so commercial offerings preserve monetization headroom. Patent filings reveal Microsoft targeting affective computing, aiming to retain subtler cues like sarcasm and awe in synthetic delivery. Such moves signal a shift from raw intelligibility toward emotional richness as the new competitive differentiator within the voice cloning market.

Pricing pressure intensifies. Amazon’s Nova models claim 75% lower operational costs versus peers, threatening to compress margins market-wide. To stay viable, pure-play vendors bundle workflow orchestration, talent rights management, and compliance dashboards, elevating from point API providers to holistic platforms. M&A rumblings suggest larger clouds may acquire niche innovators to fast-track capability gaps, pointing to continued consolidation.

Voice Cloning Industry Leaders

IBM Corporation

Microsoft Corporation

Smartbox Assistive Technology Ltd

Descript, Inc.

CereProc Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Enterprise voice automation is a near-term whitespace where buyers are moving from experimental assistants to brand-governed, multilingual voice agents with embedded compliance controls. Product moves in 2026 reflect this shift toward integrated, enterprise-ready stacks: Yellow.ai launched Nexus Vox in May 2026, positioned around rapid voice cloning and broad language coverage, and Microsoft introduced MAI-Voice-2 in Microsoft Foundry in June 2026, adding system-level consent enforcement and tying voice capabilities into enterprise workflows such as Dynamics 365 Contact Center, which expands the implementation base beyond standalone TTS APIs.

Rights-cleared voice licensing and professional media localization also offer a monetization path that aligns with tightening rules on unauthorized replicas. ElevenLabs partnership activity around licensed voice and likeness (for example, the Stan Lee Universe licensing deal announced in May 2026) highlights a commercial model centered on consented, contractable voice assets rather than ad hoc cloning. In parallel, regulatory anchors are turning into product requirements: the EU AI Act Article 50 marking obligations from August 2, 2026 and US legislative momentum around the NO FAKES Act support demand for watermarking, disclosure tooling, and auditable consent management, giving providers that can operationalize compliance across regions a clearer differentiation.

Recent Industry Developments

- July 2026: Omilia launched Lexis, a generative text-to-speech model for enterprise contact centers that includes native voice cloning within its cloud platform. The announcement emphasized enterprise compliance alignment (including frameworks used in regulated environments), reinforcing the shift toward end-to-end voice stacks inside contact-center perimeters rather than stitched third-party voice APIs.

- May 2026: OpenAI confirmed the acquisition of voice cloning startup Weights.gg and integrated its team and technology internally. The acquisition signals ongoing consolidation of specialized voice cloning capabilities into broader AI platforms, affecting competitive dynamics for standalone voice vendors and developer ecosystems.

- April 2024: The US Federal Trade Commission published guidance and policy considerations on approaches to address AI-enabled voice cloning risks, highlighting consumer protection and fraud concerns tied to synthetic voice. This visibility from a major regulator has pushed vendors and deployers to formalize consent, disclosure, and authentication controls earlier in procurement cycles.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenue earned from voice cloning solutions and related services that create a synthetic voice from recorded speech, and then generate new speech for business and consumer use cases.

Scope exclusions: We exclude general speech-to-text transcription, generic text-to-speech that is not trained to match a specific speaker, and pure hardware sales where voice cloning software is not bundled.

Segmentation Overview

- By Deployment Type

- On-Premise

- Cloud

- By Component

- Solution

- Service

- By Voice-Cloning Method

- Concatenative TTS

- Parametric/Statistical TTS

- NeuralandDeep-Learning-based TTS

- By Application

- ChatbotsandVoice Assistants

- AccessibilityandAssistive Technologies

- DigitalandInteractive Games

- DubbingandLocalization

- Customer ServiceandIVR

- Voice ProstheticsandPersonalized Speech

- By End-user Vertical

- ITandTelecommunications

- BFSI

- HealthcareandLife Sciences

- MediaandEntertainment

- Education

- TravelandTourism

- RetailandE-commerce

- GovernmentandDefense

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

We start by mapping the value chain and the normal buying path, since voice cloning is typically sold as software, cloud usage, and services rather than as one standardized unit. Public sources are used to frame adoption and constraints, including NIST publications on speech technology evaluation, U.S. Federal Trade Commission consumer guidance on impersonation fraud, OECD work on AI policy, and official AI governance updates from the European Union.

Next, we use evidence that helps set realistic demand signals and pricing direction, such as IT spend and digital economy indicators from the World Bank and OECD, plus selected filings, investor presentations, product documentation, and reputable press coverage for shipment-like proxies (for example, active customers, usage tiers, and partnership announcements). Where needed, analyst access to paid company financials and news intelligence, patent databases, and global contracts and tenders databases is used to standardize company revenue footprints and cross-check commercialization intensity. The desk sources listed above are illustrative only, and many other public references were also used for validation and clarification.

Primary Interviews and Surveys

Our primary work focuses on confirming what gets counted as voice cloning revenue in practice, and how pricing usually scales as usage grows in real deployments. We speak with product and go-to-market leaders, solution architects, and managers across major regions to validate adoption by industry, typical contract structures, and the split between software, cloud usage, and services.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 15% | APAC: 47% |

| Mid tier: 44% | Functional/Unit leaders: 33% | EMEA: 31% |

| Smaller Players: 17% | Managers: 52% | Americas: 22% |

Market-Sizing & Forecasting

The core sizing is built using a top-down approach where the spend pool is reconstructed by tracking adoption of synthetic voice in customer-facing automation, media localization, accessibility, and security-aware deployments, and then allocating only the portion that is truly voice cloning. To keep the totals realistic, we corroborate them with selective bottom-up approximations such as sampled vendor revenue bands, channel checks with implementers, and an ASP times volume view using typical license or usage tiers.

Inputs that meaningfully move the model include the mix of cloud versus on-premise deployments, average contract values by enterprise size, usage growth patterns (for example, minutes generated or seats covered), the share of spending tied to regulated or high-risk use cases, and the shift from generic TTS toward neural cloning methods that change unit economics. Forecasts are shaped using scenario analysis supported by expert views on governance tightening, fraud mitigation spending, and enterprise AI rollout pace, and then consolidated into a base case that reflects what buyers can implement at scale. Where company disclosures are limited, gaps are handled by using conservative revenue ranges, applying peer comparisons, and then checking for over-counting across solutions, services, and bundled offers.

Data Validation & Update Cycle

We run multi-step checks so totals do not drift away from observable market signals, and so regional splits stay consistent with known adoption patterns. Outliers are investigated through variance checks across pricing, deployment mix, and end-use demand, and then reviewed by another analyst before sign-off.

Reports refresh annually, and interim updates are made when material events occur, such as major policy changes, sharp currency moves, or a step-change in pricing models. Before delivery, a fresh pass is done to align assumptions to the latest public disclosures and primary re-checks, so clients receive an updated view.

Mordor Intelligence's Voice Cloning Market Sizing Compared With Other Published Estimates

Different publishers can land on different market values even when they cover the same technology, because they often lock the model on different timing, pricing, and scope boundaries. In voice cloning, the gap typically comes from how fast ASP is assumed to fall as models commoditize, what currency timing is used for global revenue conversion, and whether fraud-related spend is counted within voice cloning or treated as an adjacent category.

In our refresh-led workflow, assumptions are re-checked when pricing shifts from fixed licenses to usage-based tiers, and currency conversion is aligned to the same year that company financials and contract signals are validated, which is why the 2026 value published by Mordor Intelligence can sit apart from estimates that rely on older pricing snapshots or a different cut of service revenue.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.02 B (2026) | |

| Industry Report Publisher A | USD 3.50 B (2024) | Uses an earlier base year and applies an aggressive growth path without clearly separating voice cloning from broader synthetic speech and adjacent conversational AI revenues, which can inflate the starting point. |

| Press Release B | USD 2.43 B (2024) | Relies on a press release style estimate with limited visibility on pricing mechanics and service attachment, and the currency timing and conversion approach is not transparent, which can shift global totals. |

The spread in the table is mainly explained by base-year choice, what is counted as voice cloning versus nearby synthetic voice categories, and how pricing is updated as usage-based plans expand. By tying the model to repeatable inputs like deployment mix, contract value bands, and validated conversion timing, the final number stays traceable and easier to reconcile across years.

Key Questions Answered in the Report

What is the current size of the Voice Cloning Market?

The Voice Cloning Market size is USD 3.02 billion in 2026, with revenue forecast to hit USD 9.53 billion by 2031 at a 25.84% CAGR.

Which deployment model is growing fastest?

Cloud deployments are expanding at 29.82% CAGR because pay-as-you-go APIs and global edge nodes simplify adoption for enterprises and SMEs alike.

Why are healthcare organizations adopting voice cloning?

Hospitals use personalized synthetic voices for patient education and voice prosthetics, driving a 30.78% CAGR in the healthcare & life sciences vertical.

How big is North America’s role in the market?

North America holds 38.70% of 2025 revenue thanks to early media, telecom, and AI research leadership, although Asia Pacific is now growing quicker.

What are the main security concerns?

Deepfake voice fraud has pushed BFSI compliance costs up by 27% and is the top restraint, prompting development of watermarking and detection tools.

Which application segment shows the highest growth?

Interactive games lead with a 32.88% CAGR as studios integrate real-time voice cloning to generate adaptive dialogue that deepens player immersion.

Page last updated on: