CINV Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

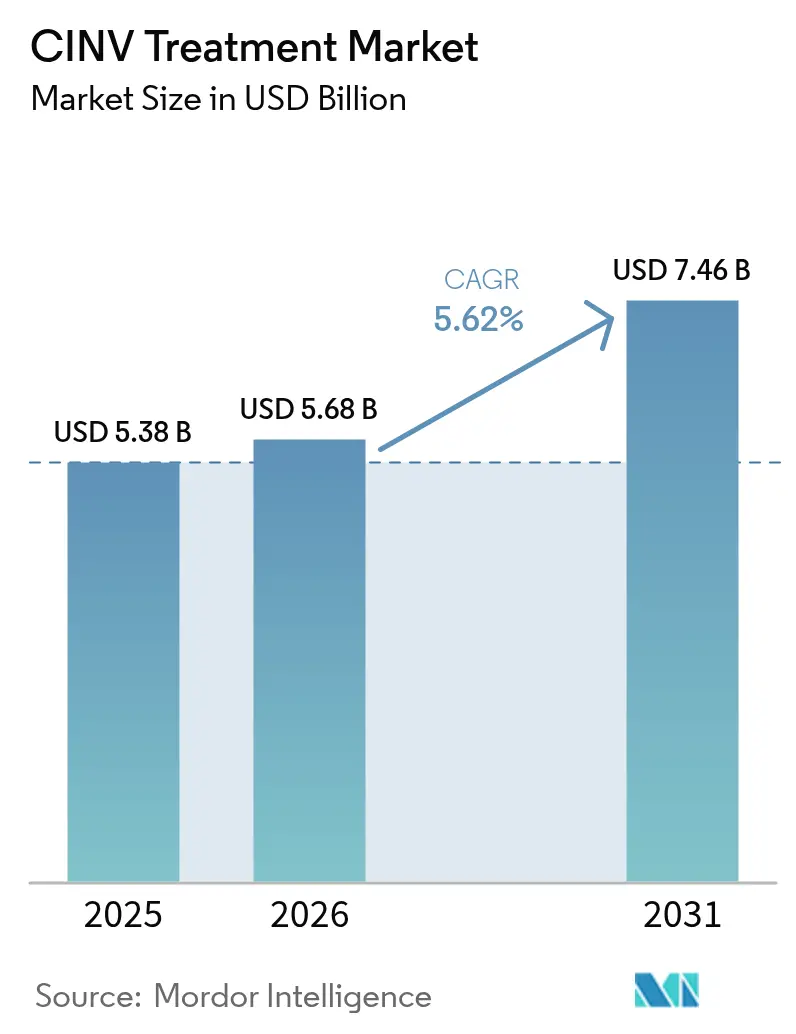

| Market Size (2026) | USD 5.68 Billion |

| Market Size (2031) | USD 7.46 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

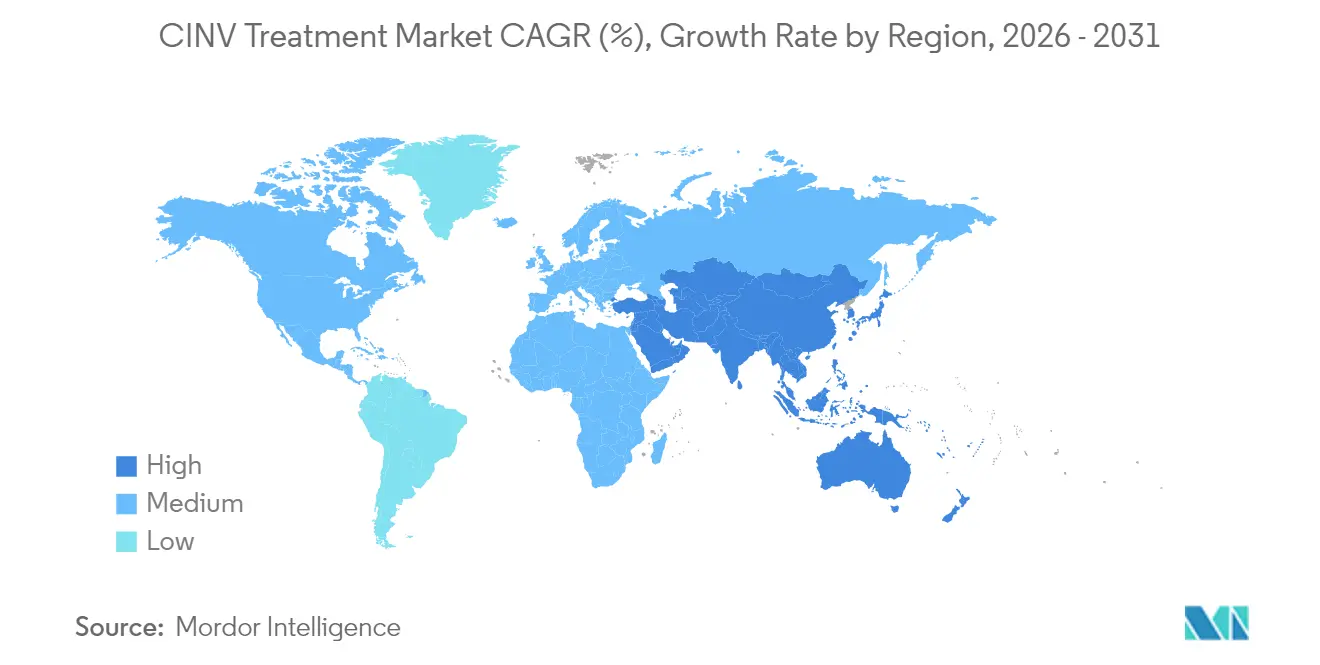

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CINV Treatment Market Analysis by Mordor Intelligence

The CINV Treatment Market size is expected to grow from USD 5.38 billion in 2025 to USD 5.68 billion in 2026 and is forecast to reach USD 7.46 billion by 2031 at 5.62% CAGR over 2026-2031.

Sustained demand arises from expanding cancer prevalence, wider use of highly-emetogenic chemotherapy, and the steady migration of care toward outpatient and home-based settings. Oral and extended-release formulations gain traction because they fit decentralized care pathways and improve adherence, a shift that tempers the historical dominance of injectables. Patent expiries for key brands place near-term pressure on prices, yet they also open space for differentiated products that emphasize convenience, fixed-dose combinations, and personalized dosing. Asia-Pacific’s regulatory harmonization and rising oncology caseload drive the fastest regional growth, while North America leverages reimbursement depth and clinical trial infrastructure to remain the largest contributor to CINV treatment market revenue.

Key Report Takeaways

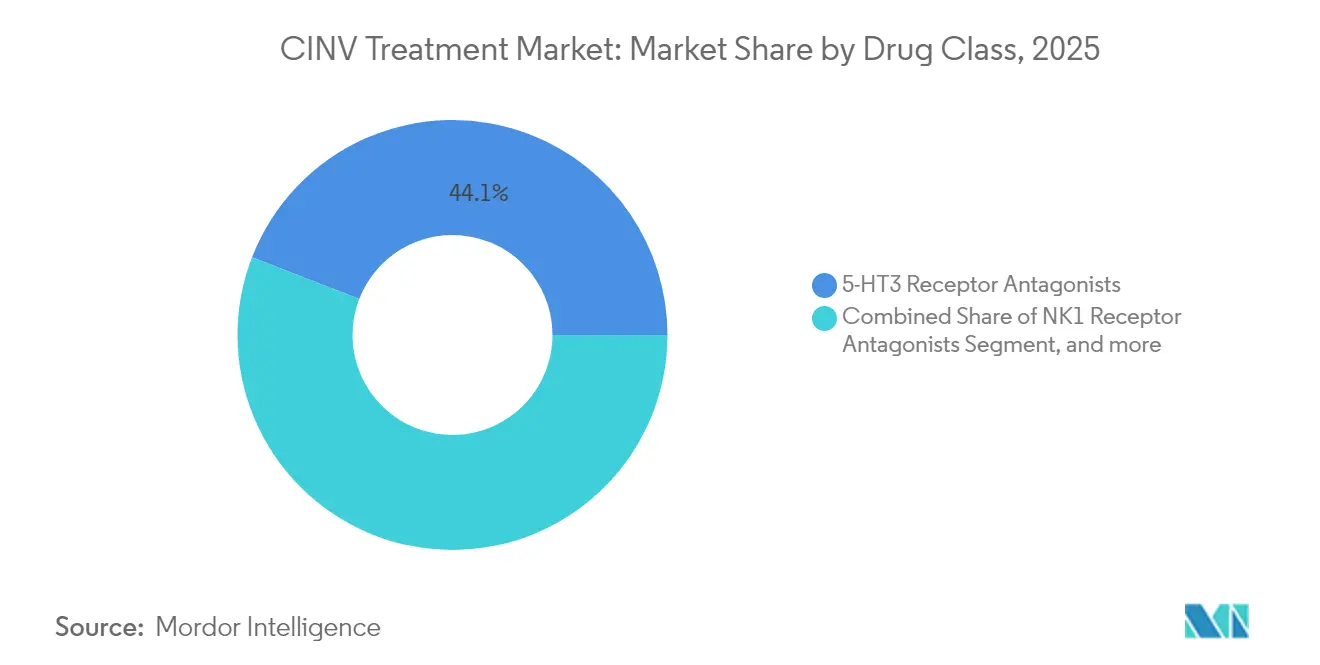

- By drug class, 5-HT3 receptor antagonists led with 44.12% of CINV treatment market share in 2025; NK1 receptor antagonists are projected to expand at a 6.42% CAGR through 2031.

- By formulation, injectables commanded 55.32% share of the CINV treatment market size in 2025, whereas oral formulations are growing at 7.08% CAGR to 2031.

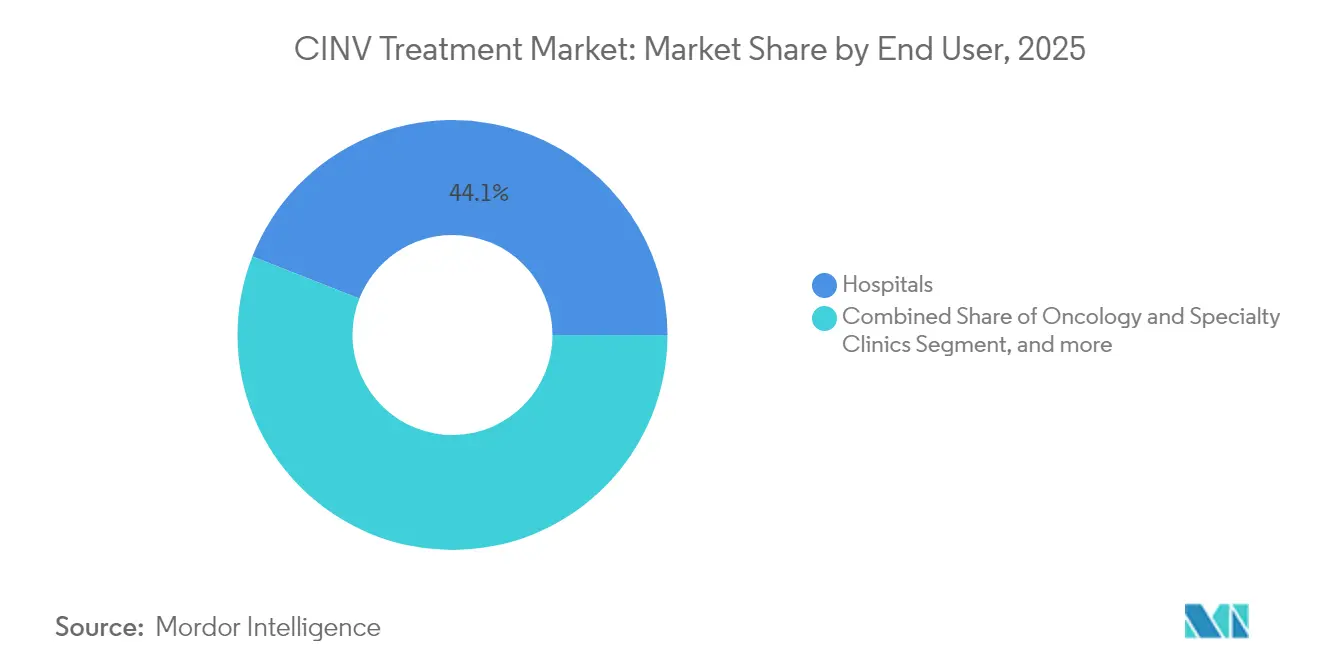

- By end user, hospitals held 44.05% of the CINV treatment market in 2025, and homecare & ambulatory surgery centers are forecast to rise at an 7.84% CAGR through 2031.

- By geography, North America accounted for 37.20% of CINV treatment market revenue in 2025, while Asia-Pacific records the highest projected CAGR at 6.78% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global CINV Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of cancer | +1.2% | Global | Long term (≥ 4 years) |

| Adoption of highly-emetogenic chemotherapy | +0.9% | North America & EU | Medium term (2-4 years) |

| Guideline-driven uptake of triple therapy | +0.8% | Global | Short term (≤ 2 years) |

| Fixed-dose combos & extended-release formats | +0.7% | North America & EU | Medium term (2-4 years) |

| Oral oncolytics boosting oral antiemetics | +0.6% | Asia-Pacific, spill-over to MEA | Long term (≥ 4 years) |

| Pharmacogenomics-based personalization | +0.4% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Cancer

Breakthrough oncology drugs cleared by the FDA in 2024 widened the treated patient pool, intensifying demand for supportive care antiemetics. Longer survival times among older populations further lengthen exposure to chemotherapy and related nausea risks, ensuring that antiemetic use scales alongside oncology advances. The demographic shift toward aging populations in developed markets compounds this trend, as older patients typically require more aggressive chemotherapy protocols with higher emetogenic potential. Additionally, improved cancer screening programs detect malignancies at earlier stages, leading to longer treatment durations and cumulative antiemetic exposure per patient.

Adoption of Highly-Emetogenic Chemotherapy Regimens

Clinical protocols incorporating anthracycline-based or platinum-dense regimens hinge on robust antiemetic prophylaxis, steering prescribers toward premium NK1 antagonists. A study showed 94.7% complete response when olanzapine, palonosetron, and fosaprepitant were combined for high-risk patients.[1]M. Benson, “Olanzapine Combinations Improve CINV Control in High-Risk Patients,” JCO Global Oncology, ascopubs.orgThe trend accelerates as precision oncology identifies patient subgroups requiring intensified treatment approaches, creating sustained demand for advanced antiemetic solutions. Furthermore, the integration of immunotherapy with traditional chemotherapy creates novel emetogenic profiles that require specialized management strategies.

Guideline-Driven Uptake of Triple Antiemetic Therapy

Updated MASCC-ESMO guidelines standardize triple-agent prophylaxis for moderate-to-high emetogenic therapy, reducing practice variability and cementing routine use of NK1-5-HT3-dexamethasone combinations.[2]Multinational Association of Supportive Care in Cancer, “2023 MASCC/ESMO Antiemetic Guidelines,” esmo.orgThe consensus-driven approach builds confidence among healthcare providers, particularly in resource-constrained settings where treatment decisions require strong evidence support. Additionally, guideline adherence becomes increasingly important for reimbursement approval, creating economic incentives for compliance with recommended antiemetic protocols.

Fixed-Dose Combos & Extended-Release Formulations

Products such as Sustol deliver ≥ 5-day coverage, easing delayed-phase nausea control and discouraging off-schedule rescue dosing.[3]A. Smith, “Granisetron ER Shows Non-Inferiority to Palonosetron,” American Health & Drug Benefits, ahdbonline.com Formulation innovation offers life-cycle extension benefits for manufacturers facing generic erosion on immediate-release versions. Fixed-dose combinations like AKYNZEO (netupitant/palonosetron) eliminate dosing complexity and reduce medication errors, particularly important in outpatient settings where nursing supervision is limited. These formulation advances also create differentiation opportunities for pharmaceutical companies facing generic competition on traditional immediate-release products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent expiries driving price erosion | -1.1% | Global | Short term (≤ 2 years) |

| Side-effect profile limiting adherence | -0.6% | Global | Medium term (2-4 years) |

| Oncologist under-estimation of emetogenicity | -0.4% | Global | Medium term (2-4 years) |

| Restricted reimbursement in emerging markets | -0.3% | Asia-Pacific, spill-over to MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Patent Expiries Driving Price Erosion

Loss of exclusivity for brands such as Sancuso intensifies generic entry, compressing average selling prices and challenging R&D reinvestment models for incumbents, particularly in regions where payers prioritize least-cost alternatives. Companies respond through defensive strategies including authorized generics, value-based contracting, and lifecycle management initiatives, but these approaches typically delay rather than prevent revenue erosion. The pricing pressure intensifies in emerging markets where healthcare systems prioritize cost-effectiveness over brand preference, accelerating generic adoption rates.

Side-Effect Profile Limiting Adherence

Sedation, constipation, and rare seizure-like events associated with NK1 agents complicate chronic use, prompting dose adjustments or switches that can compromise prophylactic consistency. The challenge intensifies as treatment durations extend and patients receive multiple chemotherapy cycles, creating cumulative exposure risks that require careful monitoring and potential dose modifications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: NK1 Antagonists Gain Momentum

5-HT3 receptor antagonists retained a 44.12% CINV treatment market share in 2025, a position built on long-standing clinical familiarity. Yet the segment grows modestly as clinicians increasingly adopt NK1 agents for delayed-phase protection. The CINV treatment market size tied to NK1 antagonists is on track to rise at 6.42% CAGR thanks to guideline endorsements and new once-daily formulations. Robust clinical evidence underpins NK1 uptake, and brands such as CINVANTI extend protection through 2035 patents, giving innovators pricing latitude.

Complementary roles for dopamine antagonists and corticosteroids persist, while cannabinoids remain a niche option for refractory cases. Evidence supporting olanzapine’s multi-receptor blockade is altering rescue therapy preferences, especially for breakthrough nausea where single-mechanism drugs show gaps. As combination regimens become standard, manufacturers that integrate NK1 components with 5-HT3 or corticosteroids in a single capsule or infusion capture workflow efficiencies that resonate with oncology clinics.

By Formulation: Oral Delivery Accelerates

Injectables maintained 55.32% of 2025 revenue, benefiting from controlled inpatient settings and immediate bioavailability requirements during initial chemotherapy cycles. Hospitals and infusion centers continue to rely on IV fosaprepitant and palonosetron for day-one coverage. However, the oral sub-segment is expanding at a 7.08% CAGR, led by once-per-cycle extended-release tablets that align with home-based oncology regimens. Oral formulations also reduce nursing time and syringe disposal costs, creating tangible operational savings that appeal to value-based procurement teams.

Transdermal and sublingual formats address swallowing difficulties or persistent nausea preventing oral intake, yet their uptake remains incremental. Manufacturers are refining polymer matrices to extend transdermal release, a strategy expected to unlock future gains beyond 2030. The rise of single-tablet triple therapies illustrates how formulation innovation can circumvent generic-driven price wars, preserving brand differentiation inside an increasingly crowded CINV treatment market.

By End User: Decentralized Care Gains Traction

Hospitals held 44.05% of 2025 revenue because most first-cycle chemotherapies and acute toxicity emergencies still unfold in tertiary centers. Multidrug IV protocols and reimbursement bundling favor inpatient settings, ensuring hospitals remain a critical channel for the CINV treatment market. Oncology clinics deliver personalized dosing adjustments and rapid follow-up, reinforcing their relevance even as payers push infusions to lower-cost venues.

Homecare and ambulatory surgery centers are posting an 7.84% CAGR as payers recognize 20-40% cost reductions versus hospital delivery. Growth in wearable infusion pumps and oral targeted therapies reduces the need for chair time, enabling stable patients to shift antiemetic management to home. Manufacturers that design patient-friendly packaging, digital adherence reminders, and easy-to-open blister packs stand to gain loyalty within this rising care segment of the CINV treatment market.

Geography Analysis

North America generated 37.20% of global revenue in 2025 owing to established clinical guideline enforcement, rapid FDA approvals, and extensive insurance coverage for supportive oncology drugs. The region’s clinicians readily adopt extended-release innovations despite higher acquisition costs when data show reduced rescue medication use. Patent expiries are expected to temper annual price growth, but volume expansion from rising cancer incidence and broader use of immuno-chemotherapy combinations sustains overall market value. Value-based care models are nudging hospital systems toward longer-acting antiemetics that cut infusion chair occupancy and readmissions.

Asia-Pacific is projected to grow at 6.78% CAGR through 2031 as China, India, and Southeast Asian countries expand oncology infrastructure and harmonize regulatory pathways. China’s National Medical Products Administration cleared 228 NDAs in 2024, 37% for antineoplastic agents, catalyzing supportive-care demand. Domestic manufacturers introduce cost-competitive NK1 generics, while multinational firms leverage accelerated pathways to launch fixed-dose combos. Pharmacovigilance capacity is rising, making data-driven formulary inclusion more feasible across public hospitals.

Europe maintains consistent demand anchored by harmonized EMA approvals and robust health technology assessments that balance innovation with cost containment. National reimbursement boards emphasize real-world effectiveness data, favoring products that document reduced rescue therapy and hospital re-visits. Emerging regions in MEA and South America remain nascent contributors yet represent strategic expansions for companies willing to localize production and navigate fragmented regulatory landscapes.

Competitive Landscape

The CINV treatment market is moderately concentrated, with innovators relying on intellectual property to defend premium NK1 and combo products. Heron Therapeutics, for instance, extended CINVANTI exclusivity to 2035, enabling its 2024 revenue to climb to USD 100.1 million despite intensifying generic competition in 5-HT3 and corticosteroid classes. Market players increasingly allocate R&D toward delivery innovation rather than novel targets, reflecting clinical consensus around multi-receptor blockade.

Strategic alliances facilitate penetration in high-growth Asia-Pacific markets where domestic distribution and tender experience accelerate uptake. Daiichi Sankyo’s purchase of ramosetron rights illustrates outbound licensing to strengthen regional portfolios. Midsize firms prioritize lifecycle management, including authorized generics and extended-release line extensions, to offset erosion following patent cliffs. Digital adherence tools bundled with therapy packs are emerging differentiators, linking symptom diaries to tele-oncology platforms and reinforcing brand loyalty.

M&A momentum persists as large pharmas seek to round out oncology supportive-care offerings. GSK’s USD 1.15 billion acquisition of IDRx in January 2025 exemplifies this trend, augmenting pipeline breadth and heightening competitive stakes. While barriers to entry for novel mechanisms remain high, formulation innovators and specialty generics firms continue to challenge incumbents, ensuring ongoing price rationalization within the CINV treatment market.

CINV Treatment Industry Leaders

Merck & Co., Inc.

GlaxoSmithKline plc

Heron Therapeutics, Inc.

Helsinn Group

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Novartis announced positive Phase III PSMAddition trial results for Pluvicto in metastatic hormone-sensitive prostate cancer, demonstrating statistically significant radiographic progression-free survival benefits that may expand treatment paradigms and increase patient populations requiring CINV management.

- February 2025: Heron Therapeutics reported full-year 2024 financial results with CINVANTI revenue reaching USD 100.1 million, representing 5.5% growth and demonstrating sustained market demand for premium NK1 receptor antagonist.

- January 2025: GSK completed its USD 1.15 billion acquisition of IDRx, gaining access to IDRX-42 for gastrointestinal stromal tumors and strengthening its oncology portfolio with potential implications for supportive care product development.

- October 2024: FDA issued draft guidance for postoperative nausea and vomiting drug development, providing regulatory framework that may accelerate clinical development for PONV indications and expand market opportunities.

Global CINV Treatment Market Report Scope

As per the scope of the report nausea and vomiting are the two most common side effects coupled with cancer chemotherapy and are described to as chemotherapy-induced nausea and vomiting. This report is segmented by Drug Type, by End-User, and by Geography.

| 5-HT3 Receptor Antagonists |

| NK1 Receptor Antagonists |

| Dopamine Antagonists |

| Cannabinoid Antagonists |

| Corticosteroids |

| Other Classes (Benzodiazepines, Antihistamines) |

| Oral |

| Injectable |

| Transdermal |

| Sublingual |

| Hospitals |

| Oncology & Specialty Clinics |

| Homecare Settings & ASCs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | 5-HT3 Receptor Antagonists | |

| NK1 Receptor Antagonists | ||

| Dopamine Antagonists | ||

| Cannabinoid Antagonists | ||

| Corticosteroids | ||

| Other Classes (Benzodiazepines, Antihistamines) | ||

| By Formulation | Oral | |

| Injectable | ||

| Transdermal | ||

| Sublingual | ||

| By End User | Hospitals | |

| Oncology & Specialty Clinics | ||

| Homecare Settings & ASCs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the CINV treatment market?

The CINV treatment market size is USD 5.68 billion in 2026 and is forecast to reach USD 7.46 billion by 2031.

Which drug class is expanding fastest?

NK1 receptor antagonists are the fastest-growing class, advancing at a 6.42% CAGR through 2031.

Why are oral formulations gaining popularity?

Oral extended-release formulations support outpatient and home-based chemotherapy models, achieving a 7.08% CAGR as they improve convenience and adherence.

Which region offers the highest growth potential?

Asia-Pacific records the highest regional CAGR at 6.78% owing to regulatory harmonization and rising cancer incidence.

How are patent expiries impacting the market?

Expiring patents for brands such as Sancuso invite generic competition, eroding prices in the short term but encouraging innovators to differentiate through novel delivery technologies.

What role do clinical guidelines play in market expansion?

MASCC-ESMO guidelines standardize triple therapy for moderate and highly emetogenic chemotherapy, driving consistent global uptake of multi-agent antiemetic regimens.

Page last updated on: