Uveitis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

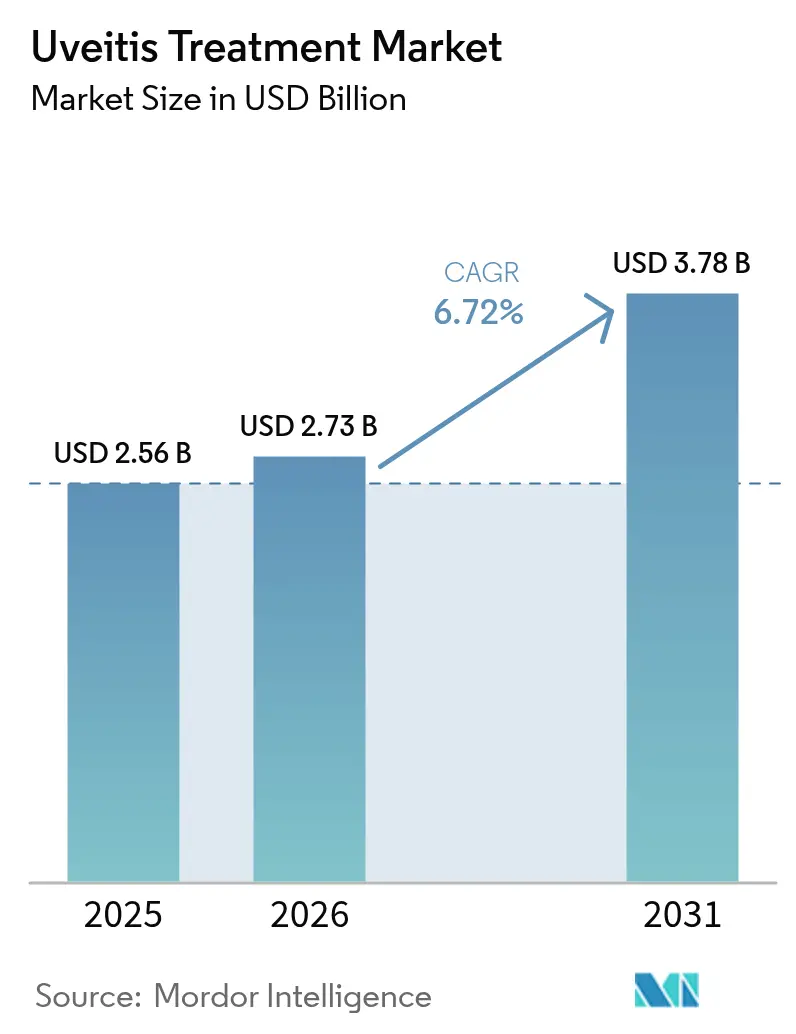

| Market Size (2026) | USD 2.73 Billion |

| Market Size (2031) | USD 3.78 Billion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Uveitis Treatment Market Analysis by Mordor Intelligence

The uveitis treatment market size was valued at USD 2.56 billion in 2025 and estimated to grow from USD 2.73 billion in 2026 to reach USD 3.78 billion by 2031, at a CAGR of 6.72% during the forecast period (2026-2031). Heightened recognition of uveitis as a leading cause of preventable blindness, combined with rising autoimmune disease prevalence, underpins this growth trajectory. North America remains the revenue anchor, driven by early biologic adoption and advanced reimbursement frameworks, while Asia-Pacific posts the fastest expansion as large underserved populations gain access to specialist ophthalmology services. Shifts toward precision immunomodulation and sustained-release ocular implants continue to tilt prescribing away from traditional corticosteroids toward premium biologics and biosimilars. Supply chain disruptions for key corticosteroids and an uneven global ophthalmology workforce present short-term constraints yet simultaneously spur innovation in alternative delivery platforms.

Key Report Takeaways

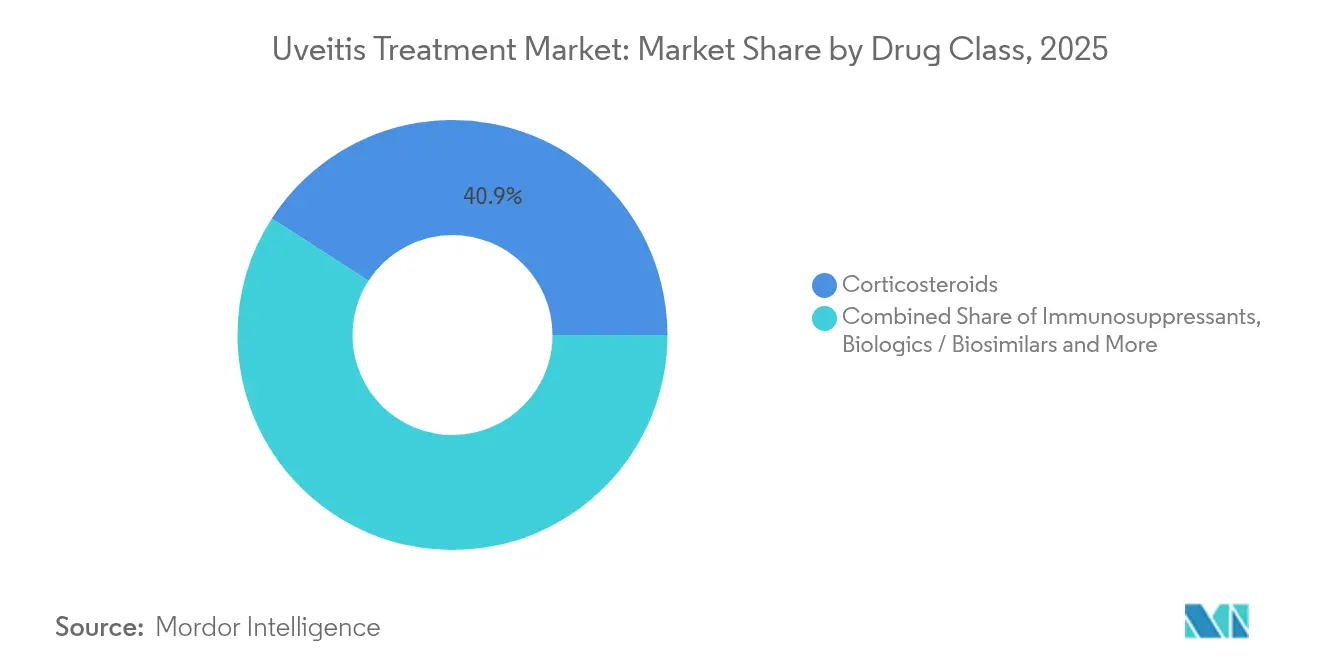

- By drug class, corticosteroids led with 40.89% of uveitis treatment market share in 2025, while biologics and biosimilars logged the highest projected CAGR at 9.11% through 2031.

- By disease type, anterior uveitis accounted for 43.76% of the uveitis treatment market size in 2025; posterior uveitis is set to expand at an 8.72% CAGR to 2031.

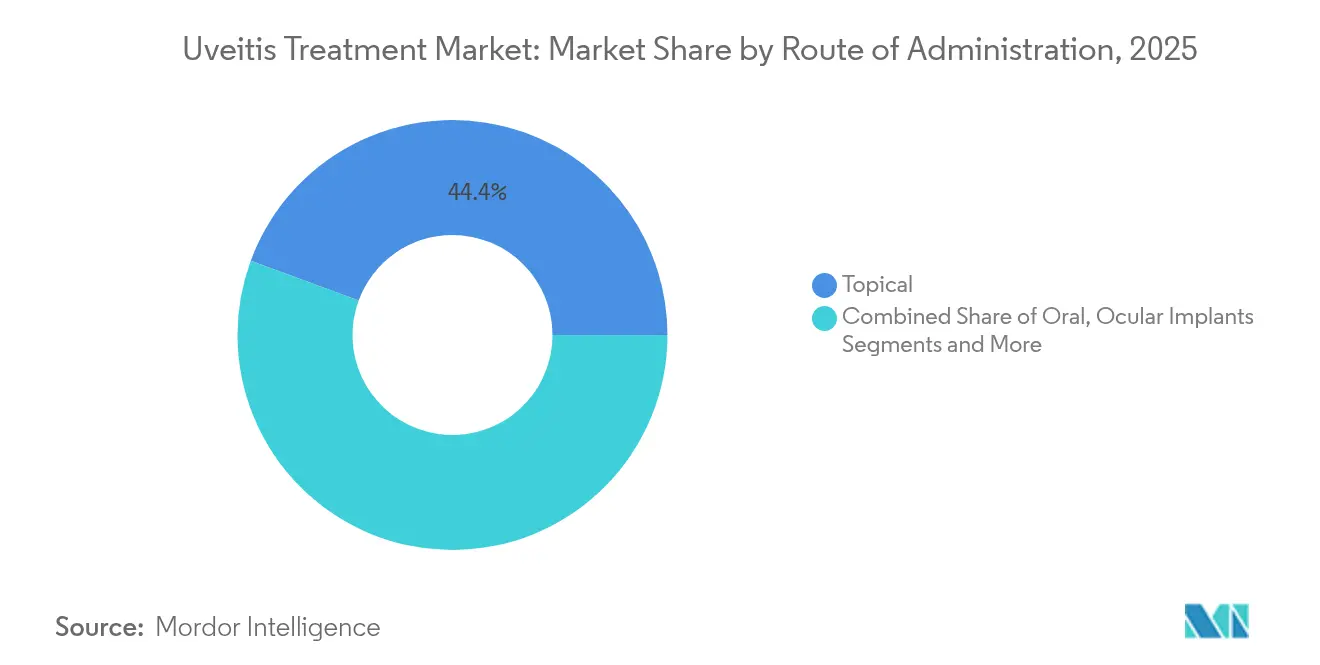

- By route of administration, topical therapies commanded 44.38% of revenue in 2025, whereas ocular implants and inserts are forecast to grow at a 10.12% CAGR.

- By distribution channel, hospital pharmacies maintained a 39.02% share in 2025, yet online pharmacies are projected to record a 10.05% CAGR.

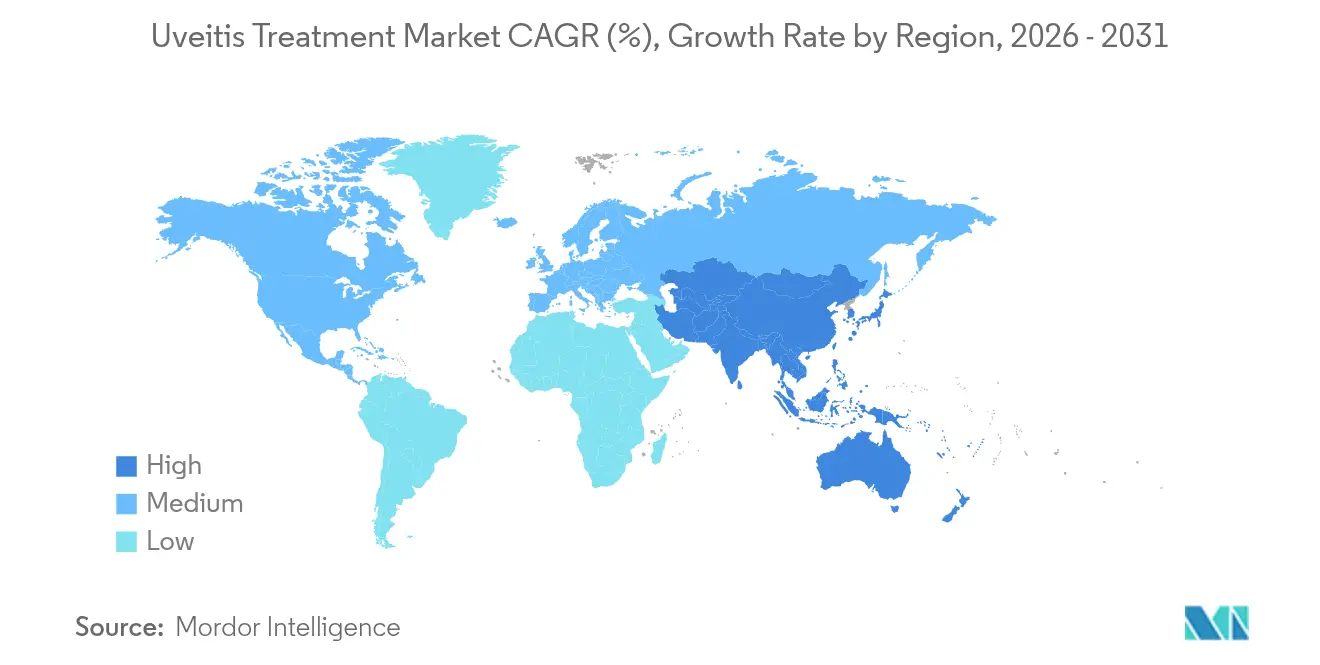

- By geography, North America captured 38.11% of global revenue in 2025; Asia-Pacific is expected to grow at an 8.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Uveitis Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of uveitis and vision-threatening complications | +1.2% | North America, Europe | Long term (≥ 4 years) |

| Growing R&D spend on novel biologics and implants | +1.8% | North America, Europe, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Expanding access to ophthalmic care in emerging economies | +1.1% | Asia-Pacific core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Increasing adoption of biosimilar adalimumab and infliximab | +0.9% | Global, with early gains in Europe and emerging markets | Short term (≤ 2 years) |

| AI-enabled retinal imaging for early diagnosis | +0.7% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Venture funding for sustained-release ocular delivery start-ups | +0.5% | North America core, Europe and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence Of Uveitis & Vision-Threatening Complications

The cumulative incidence of uveitis reached 60 per 100,000 and prevalence hit 285 per 100,000 in the United States by 2023, yet anterior cases remain under-diagnosed in primary care. Systemic autoimmune disease comorbidities such as ankylosing spondylitis amplify detection rates as rheumatology referrals rise. Posterior and intermediate forms now represent about 55% of presentations and require costlier biologics or implants to avert irreversible vision loss, thereby boosting per-patient spend. Epidemiologic shifts toward more severe phenotypes elevate therapy duration and complexity, expanding the uveitis treatment market beyond headline patient numbers. Premium implant platforms that deliver drugs for months from a single procedure gain traction as clinicians seek durable inflammation control with fewer systemic risks.

Growing R&D Spend On Novel Biologics & Implants

Merck’s USD 1.3 billion purchase of EyeBio for its tetravalent antibody program underscored industry appetite for multi-target biologics that address both inflammation and retinal repair. FDA approval of Roche’s Susvimo, offering nine-month refill intervals, validated sustained-release implants as commercially viable. Non-viral gene therapy start-ups attracted fresh venture capital, signalling a pivot toward potentially curative approaches that could lower lifetime treatment costs while reshaping competitive dynamics. These developments collectively expand therapeutic choice, compress injection frequency, and raise barriers to entry for conventional corticosteroids.

Expanding Access To Ophthalmic Care In Emerging Economies

China accepted an NDA for ARCATUS, the first suprachoroidal therapy submitted for uveitic macular edema, reflecting regulatory momentum in Asia-Pacific[1]Clearside Biomedical, “NDA acceptance for ARCATUS in China,” clearsidebio.com. Community-based eye-care models in Kenya illustrate scalable pathways to reach underserved populations through social enterprises and tele-ophthalmology. These initiatives mitigate workforce shortages by extending specialist oversight through remote imaging and AI triage. As reimbursement frameworks mature, emerging markets become fertile ground for biosimilars that offer 15-30% price reductions compared with originators, accelerating volume growth for the uveitis treatment market.

Increasing Adoption Of Biosimilar Adalimumab & Infliximab

The first interchangeable aflibercept biosimilar won FDA clearance in early 2025, allowing pharmacy-level substitution without prescriber approval. Registry data confirm comparable efficacy and safety of biosimilar adalimumab in paediatric non-infectious uveitis while enabling glucocorticoid sparing[2]AIDA Network Investigators, “Biosimilar adalimumab in paediatric uveitis,” ncbi.nlm.nih.gov. Broader biosimilar adoption helps relieve budget pressure in price-sensitive regions and encourages insurers in mature markets to widen access criteria, expanding patient pools eligible for biologic therapy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost and systemic side-effects of current therapies | -1.4% | Global, most acute in emerging economies | Medium term (2-4 years) |

| Limited ophthalmology specialist workforce in low-income regions | -1.1% | Sub-Saharan Africa, rural Asia-Pacific, parts of South America | Long term (≥ 4 years) |

| Regulatory lag for intravitreal or suprachoroidal devices | -0.8% | Varies by jurisdiction | Short term (≤ 2 years) |

| Intermittent API shortages for corticosteroids | -0.6% | North America, Europe with global ripple effects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost & Systemic Side-Effects Of Current Therapies

Annual systemic adalimumab therapy can surpass USD 60,000 per patient, whereas long-acting implants such as YUTIQ demand high upfront outlays despite three-year durability. TNF-alpha inhibitors also impose infection monitoring costs that inflate total expenditure by up to 30%. Business-driven trial discontinuations, exemplified by the HUMBOLDT study ending despite favourable filgotinib data, highlight how commercial viability shapes the therapy landscape. High costs therefore restrict uptake, particularly in markets with low per-capita healthcare spend.

Limited Ophthalmology Specialist Workforce In Low-Income Regions

Global modelling forecasts a 30% shortfall in ophthalmology FTEs by 2035, with rural areas shouldering the greatest deficit. Concurrent API shortages for generic corticosteroids compound access barriers, as 91% of ophthalmic prescriptions rely on generics vulnerable to supply disruptions. These intertwined issues slow diffusion of advanced therapies and place downward pressure on uveitis treatment market growth in high-need geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Biologics Drive Premium Growth

Corticosteroids retained 40.89% revenue share in 2025, yet biologics and biosimilars expanded at a 9.11% CAGR, reflecting clinician migration toward targeted agents that avoid cataract formation and intraocular pressure spikes. The recent six-month shortage of triamcinolone acetonide highlighted supply chain fragility and encouraged pivoting to sustained-release implants. The uveitis treatment market size for biologics is projected to advance faster than any other drug class through 2031 as pipeline JAK inhibitors progress into Phase 3. Immunosuppressants remain vital bridge therapies, and anti-infectives support the smaller infectious subset, maintaining a balanced but shifting drug-class landscape.

Second-generation biologics diversify mechanisms to include bispecific antibodies and Wnt pathway modulators, intensifying competition yet widening choice. Biosimilar launches create tiered price points that broaden patient access while preserving manufacturer margins through volume. The uveitis treatment industry therefore faces accelerating product proliferation alongside consolidation of legacy corticosteroid lines.

By Disease Type: Posterior Complexity Drives Value

Anterior uveitis led revenue with 43.76% share in 2025 because of high incidence and topical therapy reliance, but posterior uveitis is forecast to be the fastest-growing category at an 8.72% CAGR on account of specialised delivery needs such as suprachoroidal injections. The uveitis treatment market share for posterior forms is poised to expand as clinicians adopt implants that reduce retreatment frequency. New data showing faricimab efficacy in uveitic macular edema open further premium therapy avenues. Intermediate uveitis shows steady but moderate growth, while panuveitis remains the highest acuity segment with persistent unmet needs.

Adoption of diagnostic imaging advances, including wide-field OCT and AI algorithms, improves posterior disease detection and supports earlier intervention. This contributes to sustained revenue gains even as payer scrutiny rises. Consequently, the uveitis treatment market continues to shift toward segments involving complex pathophysiology and expensive interventions.

By Route of Administration: Sustained Release Transforms Care

Topical drops generated 44.38% of revenue in 2025, yet ocular implants and inserts show the highest trajectory at a 10.12% CAGR through 2031. The uveitis treatment market size for implantable products is projected to rise sharply as technologies such as the Port Delivery Platform prove commercial viability. Intravitreal and suprachoroidal injections remain critical interim modalities, driving procedure volumes in hospital settings. Systemic delivery persists for bilateral or refractory cases but faces increasing scrutiny around adverse events and monitoring costs.

Non-invasive sustained-release concepts, including drug-eluting soft contact lenses, are entering early-stage trials and may democratise premium therapy access by obviating invasive procedures. Regulatory reclassification of ultrasound cyclodestructive devices to Class II indicates a broader FDA willingness to streamline approvals for novel delivery solutions.

By Distribution Channel: Digital Transformation Accelerates

Hospital pharmacies controlled 39.02% of distribution in 2025 as biologic initiation and implant procedures remain hospital-centric. Online pharmacies, however, are expected to grow at 10.05% CAGR, buoyed by consumer preference for home delivery and transparent pricing. Specialty pharmacy tie-ins ensure cold-chain integrity for biologics, strengthening the digital channel’s credibility. Retail outlets maintain relevance for chronic topical therapy refills, while drug-store clinics integrate tele-ophthalmology follow-ups to capture value without requiring full ophthalmologist visits. Hybrid hub-and-spoke models extend specialist oversight to rural zones and support overall uveitis treatment market expansion.

Geography Analysis

North America generated 38.11% of global revenue in 2025, underpinned by widespread insurance coverage, early biologic uptake, and a robust clinical trial ecosystem. The region’s CAGR is expected to moderate as the market matures, although shortages of prednisolone acetate and difluprednate highlight supply-chain vulnerabilities that could redirect prescriptions toward alternative formulations. Workforce adequacy remains a looming challenge, with a projected 30% deficit by 2035 that may cap procedure volumes despite strong therapy demand.

Asia-Pacific posts the fastest-growing trajectory at an 8.74% CAGR as large patient backlogs meet rising healthcare expenditure. China’s Phase 3 success with ARCATUS, showing a 38.5% rate of 15+ ETDRS letter gains, exemplifies regional progress toward premium therapy adoption. Japan continues to pioneer extended-interval anti-VEGF regimens, and Australia often serves as a regulatory gateway for multinational launches. Nevertheless, ophthalmologist density remains uneven, with certain countries reporting zero specialists per million population compared with Japan’s 114 per million.

Europe maintains balanced growth as biosimilar-friendly policies sustain biologic uptake. EMA procedures offer predictable timelines, and Germany, France, and the United Kingdom anchor demand for sustained-release implants. Middle East and Africa show nascent but rising adoption as Gulf Cooperation Council health systems modernise; however, broader continental growth is hampered by limited specialist capacity. South America records moderate expansion led by Brazil’s sizeable population and improving reimbursement structures, though currency volatility and budget constraints temper premium biologic penetration.

Competitive Landscape

The uveitis treatment market features moderate fragmentation, with AbbVie, Novartis, and Bausch + Lomb sharing the biologic and small-molecule space alongside focused ophthalmology firms like EyePoint Pharmaceuticals and Clearside Biomedical. Consolidation gained pace when ANI Pharmaceuticals purchased Alimera Sciences for USD 105 million, uniting ILUVIEN and YUTIQ to form a rare-disease implant powerhouse. Strategic alliances proliferate; AbbVie’s agreement with Ripple Therapeutics provides an option to license biodegradable implants in a deal that could reach USD 290 million in value. AI-driven imaging firms collaborate with drug developers to integrate diagnostic algorithms that personalise therapy schedules, while gene therapy start-ups such as PulseSight Therapeutics pursue curative modalities that could disrupt chronic immunosuppression paradigms. White-space opportunities persist in paediatric-specific formulations and combination products that merge anti-inflammatory and anti-VEGF mechanisms.

Uveitis Treatment Industry Leaders

AbbVie Inc.

Novartis AG

Bausch + Lomb

EyePoint Pharmaceuticals

Alimera Sciences

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Clearside Biomedical’s Asia-Pacific partner Arctic Vision secured Chinese NDA acceptance for ARCATUS, the first suprachoroidal therapy filed for uveitic macular edema.

- September 2024: Priovant Therapeutics commenced the CLARITY Phase 3 brepocitinib trial in non-anterior non-infectious uveitis with a 300-patient global cohort.

Global Uveitis Treatment Market Report Scope

As per the scope of this report uveitis treatment refers to various remedies for treating inflammation in the uvea and surrounding tissues. The disease is characterized by blurred vision, dark or floating spots in the vision, redness of the eye, and sensitivity to light. The Uveitis Treatment Market is segmented By Treatment (Corticosteroids, Antibiotics, Antivirals, Antifungal, Analgesics, and Others), By Disease (Anterior Uveitis, Posterior Uveitis, Intermediate Uveitis, and Panuveitis), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The report offers the value (in USD billion) for the above segments.

| Corticosteroids |

| Immunosuppressants |

| Biologics / Biosimilars |

| Antimicrobials (Antibiotics, Antivirals, Antifungals) |

| NSAIDs & Analgesics |

| Others |

| Anterior Uveitis |

| Posterior Uveitis |

| Intermediate Uveitis |

| Panuveitis |

| Topical (Eye Drops & Ointments) |

| Oral / Systemic |

| Local Ocular Injections (Intravitreal, Suprachoroidal, Periocular) |

| Ocular Implants & Inserts |

| Hospital Pharmacies |

| Retail Pharmacies & Drug Stores |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Corticosteroids | |

| Immunosuppressants | ||

| Biologics / Biosimilars | ||

| Antimicrobials (Antibiotics, Antivirals, Antifungals) | ||

| NSAIDs & Analgesics | ||

| Others | ||

| By Disease Type | Anterior Uveitis | |

| Posterior Uveitis | ||

| Intermediate Uveitis | ||

| Panuveitis | ||

| By Route of Administration | Topical (Eye Drops & Ointments) | |

| Oral / Systemic | ||

| Local Ocular Injections (Intravitreal, Suprachoroidal, Periocular) | ||

| Ocular Implants & Inserts | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies & Drug Stores | ||

| Online Pharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the uveitis treatment market?

The market is valued at USD 2.73 billion in 2026 and is projected to reach USD 3.78 billion by 2031.

Which region leads the uveitis treatment market?

North America holds the largest share at 38.11% in 2025 owing to advanced biologic uptake and robust reimbursement systems.

Which drug class is growing the fastest?

Biologics and biosimilars are forecast to grow at a 9.11% CAGR through 2031 as clinicians pivot toward targeted immunomodulation.

Why are ocular implants gaining traction?

Implants such as ILUVIEN and YUTIQ provide sustained drug release for months to years, reducing injection frequency and improving adherence.

What restrains market growth in emerging economies?

High therapy costs, limited specialist availability, and intermittent corticosteroid shortages curtail patient access to premium treatments.

Page last updated on: