Vietnam Two Wheeler Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

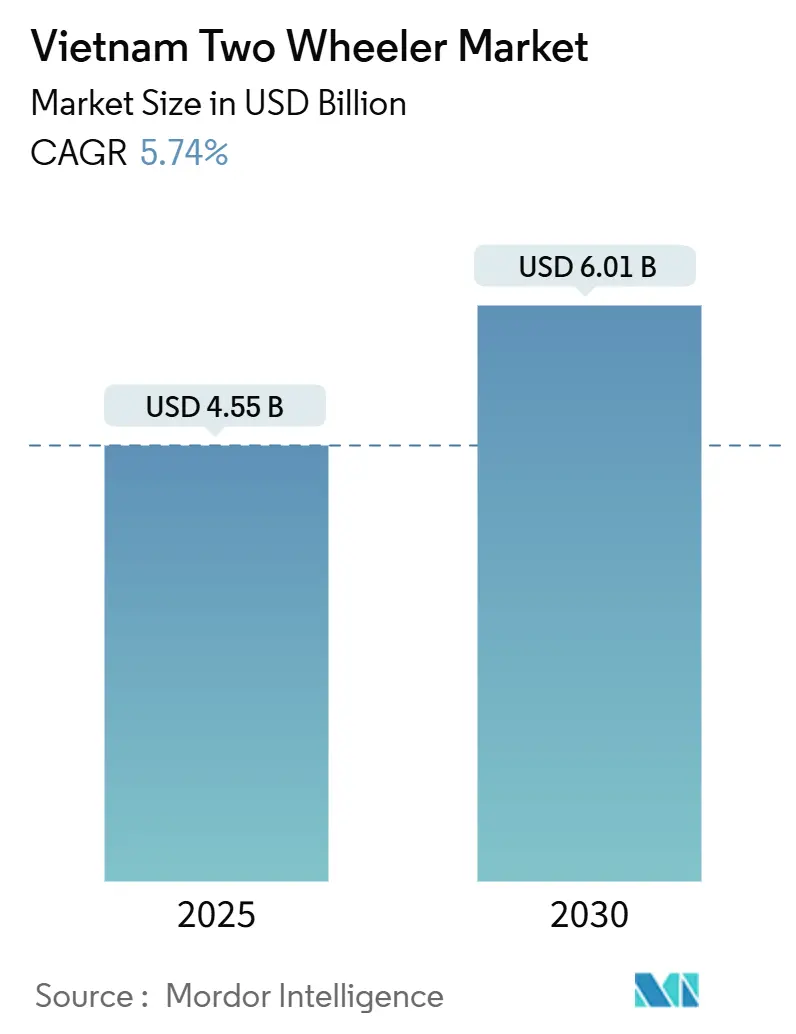

| Market Size (2025) | USD 4.55 Billion |

| Market Size (2030) | USD 6.01 Billion |

| Growth Rate (2025 - 2030) | 5.74% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Two Wheeler Market Analysis by Mordor Intelligence

The Vietnam two-wheeler market size stands at USD 4.55 billion in 2025 and is projected to reach USD 6.01 billion by 2030, expanding at a 5.74% CAGR during the forecast period. Strong urban dependence on motorcycles, persistent traffic congestion, and the rapid scale-up of e-commerce delivery fleets keep demand resilient. Scooters are winning share as urban riders favour automatic transmissions, while electric models accelerate on the back of tax breaks, zero-interest loans, and a fast-growing battery-swap network. The market benefits from extensive local supply chain integration, which reduces production costs and maintains profit margins while enabling competitive pricing. Digital sales channels are expanding gradually, providing new ways to reach consumers. The increasing adoption of electric motorcycles aligns with changes in urban transportation preferences, environmental consciousness, and technological advancement in Vietnam's two-wheeler market.

Key Report Takeaways

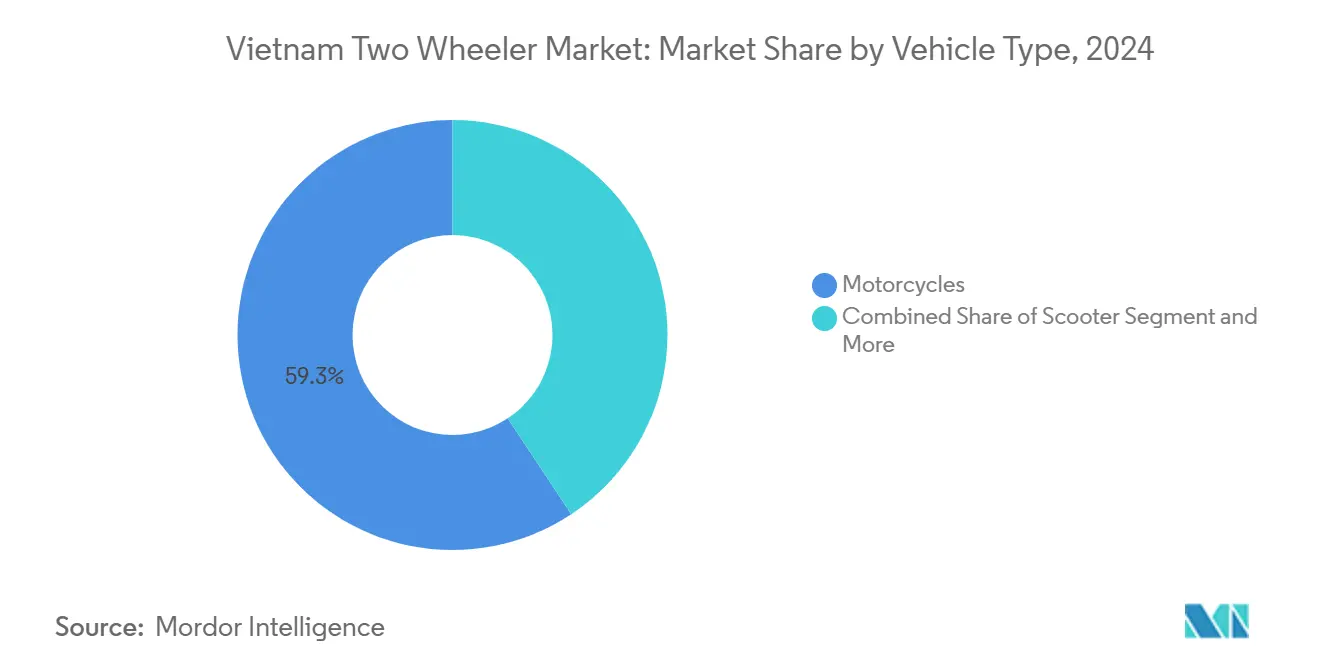

- By vehicle type, motorcycles led with 59.32% of the Vietnam two-wheeler market share in 2024, while scooters posted the fastest expansion at a 7.63% CAGR through 2030.

- By propulsion type, internal-combustion engines account for 86.17% of the Vietnam two-wheeler market size in 2024, yet electric two-wheelers are forecast to rise at an 11.41% CAGR by 2030.

- By drive type, chain drives captured 84.41% of the Vietnam two-wheeler market size in 2024; belt drives are advancing at a 7.88% CAGR through 2030.

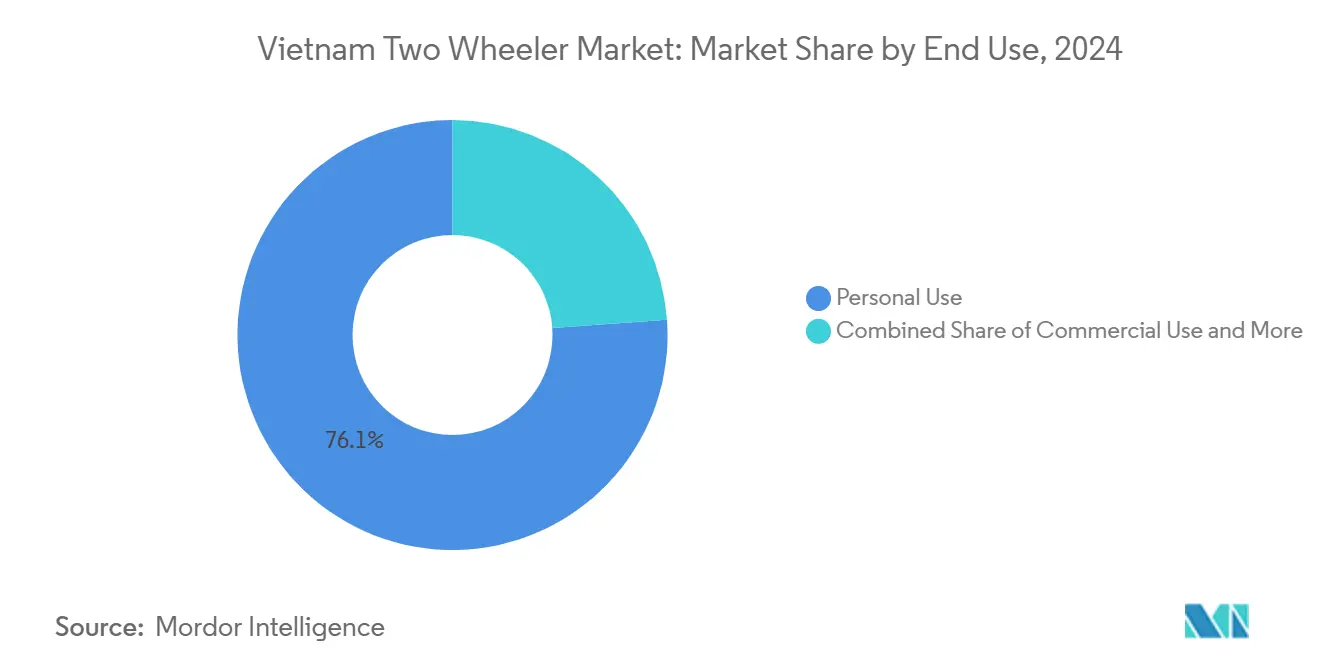

- By end use, personal use represented 76.13% of the Vietnam two-wheeler market share in 2024, while delivery and fleet services will log the highest 9.65% CAGR to 2030.

- By sales channel, offline dealers retained 84.41% of the Vietnam two-wheeler market share in 2024, although online sales are set to climb at an 8.17% CAGR to 2030.

- By Geography, Northern Vietnam held 46.28% of the Vietnam two-wheeler market size in 2024; Southern Vietnam is projected to grow fastest at a 7.82% CAGR through 2030.

Vietnam Two Wheeler Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Delivery and Last-Mile Logistics Surge | +1.8% | Nationwide | Medium term (2-4 years) |

| Urban Traffic Congestion | +1.2% | Hanoi, Ho Chi Minh City | Long term (≥ 4 years) |

| Government EV Incentives and Zero-Interest Loans | +0.9% | Nationwide | Medium term (2-4 years) |

| Expansion of Battery-Swap Networks | +0.7% | Major cities | Long term (≥ 4 years) |

| Domestic Localization Over 90% | +0.6% | Nationwide | Short term (≤ 2 years) |

| Premium Chinese Imports | +0.4% | North and South regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urban Traffic Congestion Sustaining Two-Wheeler Preference

Chronic congestion in Hanoi and Ho Chi Minh City results in annual economic losses, prompting commuters to rely on motorcycles and scooters for predictable travel times. Even affluent households keep at least one two-wheeler because car use is hampered by limited parking and narrow streets. Metro projects remain unfinished, so mass transit cannot absorb rising mobility demand. City policies restricting car entry in downtown corridors while maintaining dedicated motorcycle lanes further entrench two-wheeler use. The outcome is a feedback loop in which congestion sustains high two-wheeler ownership, thereby shaping vehicle design around manoeuvrability and low operating costs.

Government EV Incentives and Zero-Interest E-Bike Loans

Registration-fee exemptions, charging-station electricity subsidies, and zero-interest loans cut lifetime ownership costs of electric scooters. Consistent policy signals tied to Vietnam’s Net Zero 2050 pledge reassure consumers and financiers. Banks extend three-year zero-interest plans for certified e-bikes, reducing monthly payments to a level comparable with mid-range ICE models. Effectiveness hinges on charging coverage; VinFast’s plan to install 150,000 battery swapping stations across all 63 provinces exemplifies how OEM-led ecosystems can magnify government support.

Domestic Localization above 90% Lowering Unit Costs

Local content surpassing 90% in frames, plastics, and wiring harnesses allows assemblers to hedge currency risk and compress lead times. Suppliers clustered around Hanoi and Vinh Phuc benefit from scale and knowledge spillovers, enabling mid-range models to retain acceptable margins. In turn, OEMs reinvest savings into R&D for connectivity features and ABS upgrades, further differentiating the Vietnam two-wheeler market.

Chinese Limited-Edition Imports Stimulating Premium-Scooter Upgrades

Limited-run Chinese maxi-scooters priced above VND 80 million (USD 3,080) trigger aspirational purchases among urban professionals in Hanoi and Ho Chi Minh City. Parallel importers report sell-outs within weeks, prompting local dealers to stock higher-trim Honda SH and Yamaha Grande variants. The halo effect pushes average transaction values upward and encourages manufacturers to release colour-customisation programs and finance bundles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban ICE Restrictions in Hanoi/HCMC | -0.8% | Inner districts | Medium term (2-4 years) |

| Surplus Dealer Inventory | -0.6% | Nationwide | Short term (≤ 2 years) |

| Fragmented After-Sales for Low-Cost E-Mopeds | -0.4% | Rural & peri-urban areas | Medium term (2-4 years) |

| Rising Entry-Level Car Affordability | -0.7% | Tier-1 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Looming Urban ICE Restrictions in Hanoi/HCMC

Hanoi plans to curtail motorcycle use in 12 inner districts by 2030, layering mandatory emission tests on pre-2010 models. Owners face new compliance fees and potential fines, spurring earlier replacement cycles. While the policy nudges buyers toward electric scooters, phased rollouts risk shifting congestion to adjacent boroughs and could suppress near-term sales if investors await clearer guidelines. OEMs hedge by front-loading electric launches and lobbying for grace periods on cargo-bike exemptions.

Rising Entry-Level Car Affordability Diverting Aspirational Buyers

Domestic automakers discount hatchbacks below VND 350 million (USD 14,400) as factory capacity outstrips demand, drawing upper-middle-income families away from premium scooters. Car loans stretch up to seven years, making monthly payments competitive with high-end two-wheelers. As a result, the premium share of the Vietnam two-wheeler market could compress, forcing brands to highlight parking ease, fuel savings, and expedited commuting to justify premium scooter pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Scooter Growth Outpaces Traditional Dominance

Motorcycles controlled 59.32% of Vietnam's two-wheeler market share 2024, reflecting long-standing rider familiarity and rugged adaptability. Scooters, however, are forecast to post a 7.63% CAGR. The scooter boom aligns with female workforce participation and aging demographics, valuing step-through frames and automatic gearboxes. Honda’s ICON e: and CUV e: electric scooters launched in 2025 strategically capture this urban cohort. Meanwhile, Piaggio’s Liberty 2025 redesign uses a 5-inch LCD and ergonomic tweaks to tempt style-conscious professionals. Off-road and rural riders still favor motorcycles for torque and payload, so OEMs maintain extensive 110-125 cc petrol lineups.

Rugged mopeds remain essential in mountainous provinces, yet their volume stabilizes as stricter safety standards raise costs. The Vietnam two-wheeler market, therefore, bifurcates: scooters dominate high-density cities, while motorcycles anchor rural transport and commercial tasks. Portfolio balance lets manufacturers cross-subsidize innovation, helping finance ABS and IoT upgrades for scooters without forsaking entry-level motorcycle affordability.

By Propulsion Type: Electric Acceleration Amid ICE Dominance

Internal combustion engines retained an 86.17% share of the Vietnam two-wheeler market in 2024, but their share declines to roughly 70% by 2030 under baseline policy assumptions. Electric deliveries climb at an 11.41% CAGR, catalysed by fee exemptions and battery-swap ecosystems. VinFast moved 70,977 e-bikes in 2024 despite isolated corrosion complaints on the Quantum line[1]“Quantum Frame Investigation,”, Thanh Niên, thanhnien.vn. The sweet spot sits in the 1-3 kW power band, combining 120 km real-world range with sub-five-hour full charges, meeting most urban commutes.

Gasoline motorcycles in the 101-125 cc bracket remain critical, balancing performance and fuel economy at roughly 55 km per litre. Above-250 cc segments cater to enthusiasts but remain niche. CNG or LPG alternatives stay marginal owing to sparse refuelling points. As charging networks densify, fleet buyers expect total operating costs for e-bikes to undercut ICE equivalents within three years, accelerating the shift.

By Drive Type: Belt Drive Innovation Challenges Chain Supremacy

Chain drives dominated the Vietnam two-wheeler market, with an 84.41% share in 2024, thanks to low acquisition costs and ubiquitous roadside servicing. Belt drives grow 7.88% annually on the promise of lower maintenance, less vibration, and cleaner operation—attributes prized by office commuters in white attire. Electric scooters capitalise on belt or hub-motor layouts to remove chain lubrication tasks altogether. Honda upgrades its future 125 cc scooters with Kevlar-reinforced belts, signalling confidence in longevity claims.

Shaft drives stay confined to high-end touring motorcycles, given added weight and cost, though small logistics fleets see value in their durability over 100,000 km duty cycles. As electrification progresses, hub motors may bypass traditional drive systems altogether, reshaping supplier relationships and maintenance workshops

By End Use: Commercial Surge Transforms Personal Transport Market

Personal riders represented 76.13% of total volume in 2024, yet delivery and fleet applications' 9.65% CAGR outpaced all other segments. Fleet operators now demand telematics, extended warranties, and bulk procurement financing.

Ride-hailing’s flexible asset utilisation blurs boundaries between personal and commercial categories. Owners list personal motorcycles on apps outside office hours, unlocking supplemental income, which raises wear-and-tear considerations and accelerates replacement cycles. Manufacturers respond with commercial-spec variants offering reinforced frames, dual disc brakes, and ride-tracker compatibility.

By Sales Channel: Digital Transformation Accelerates Offline Dominance

Brick-and-mortar dealerships still control 84.41% of sales, underpinned by test-rides, immediate delivery, and in-house financing. Nevertheless, online direct-to-consumer sales are growing 8.17% annually as Gen-Z buyers trust virtual reviews and unboxing videos. Dat Bike’s Singapore-registered entity leverages social media and bundled subscription servicing to close digital orders, though it must roll out mobile service vans to address rural after-sales gaps[2]“Corporate Restructuring Filing,”, Dat Bike, cafef.vn.

Legacy dealers counter by offering online reservations, video consultations, and home delivery while retaining profit-rich maintenance revenue. OEMs integrate QR-coded owner manuals and app-based maintenance reminders, nurturing customer stickiness irrespective of channel.

Geography Analysis

Northern Vietnam accounted for 46.28% of Vietnam's two-wheeler market size in 2024 as decades of FDI channelled assembly plants and parts clusters to Hanoi, Haiphong, and Vinh Phuc. The region’s higher per-capita income supports premium scooter adoption, while proximity to Chinese suppliers lets dealers roll out new SKUs rapidly. Hanoi’s planned restrictions on inner-district gasoline bikes compel early electric conversion, turning the capital into a live testbed for emission-compliant models. Localisation policies and a skilled workforce keep production footprints sticky, although rising wages spur investment in robotics and MES (manufacturing execution systems).

Though the smallest market, Central Vietnam forms a logistical bridge between north and south. Improved highways shorten lead times, enabling Da Nang-based distributors to serve Central Highlands provinces within 24 hours. Tourism-heavy cities demand rental-ready scooters with easy-maintenance belt drives, while coffee-growing hinterlands require rugged motorcycles capable of 200 kg payloads during harvest season. Government incentives for Quang Ngai and Quang Nam component plants aim to broaden the regional supply base and raise local income, indirectly fueling two-wheeler purchases.

Southern Vietnam is the fastest-growing region, registering a 7.82% CAGR to 2030. Ho Chi Minh City’s entrepreneurial ecosystem spawns courier start-ups, ride-hailing pilots, and fintech-backed micro-leasing schemes that lower entry barriers for riders. Selex Motors positions Ho Chi Minh City as its Southeast Asian export hub, capitalizing on the deep-water port of Cat Lai for Indonesia-bound shipments. Industrial zones in Binh Duong and Dong Nai attract young migrant workers who purchase entry-level motorcycles through payroll deduction, enlarging the buyer pool. Persistent congestion and limited metro coverage reinforce the necessity of two-wheeler use, sustaining double-digit scooter growth.

Competitive Landscape

VinFast, Dat Bike, and imported Chinese electric vehicles chip away at this dominance by leveraging tax breaks, over-the-air updates, and lifestyle branding. Honda’s ICON e: launch marks a strategic shift, but supply is constrained by imported battery packs, underscoring supply-chain vulnerabilities[3]“ICON e: Product Briefing,”, Honda Vietnam, tnck.vn. Yamaha, SYM, and Piaggio pursue premium urban niches, each releasing ABS-equipped 150 cc scooters to fend off Chinese maxi-scooter incursions.

VinFast’s vertically integrated model combines V-Green charging, Xanh SM ride-hailing, and V-Finance consumer loans. This ecosystem approach raises switching costs and yields data insights on battery degradation, informing warranty provisions. Chinese brands pursue flash-sale tactics, shipping container-sized lots to parallel importers who undercut MSRP, pressuring local assemblers to accelerate facelifts and financing promotions.

Technological differentiation intensifies as IoT units track vibration, route patterns, and battery health. OEMs monetise data through predictive maintenance subscriptions sold to fleet managers, adding an annuity layer to unit sales. Cyber-secure OTA platforms become gatekeepers of long-term brand loyalty. The Vietnam two-wheeler market is migrating from product competition to ecosystem rivalry, where hardware, software, and infrastructure converge.

Vietnam Two Wheeler Industry Leaders

Honda Vietnam

Yamaha Motor Vietnam

VinFast Auto Ltd.

Piaggio Vietnam Co. Ltd.

SYM Vietnam

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Piaggio Vietnam introduced the new generation Piaggio Liberty 2025 scooter in three variants: Liberty Standard, Liberty S, and Liberty Z. The Liberty Z variant is designed exclusively for the Vietnamese market.

- December 2024: V-GREEN Global Charging Station Development Joint Stock Company and Fast+ Charging Station Joint Stock Company signed a franchise agreement to install 5,000 charging stations for VinFast vehicles across the country. The charging stations will have power capacities ranging from 7.4 KW to 150 KW.

Vietnam Two Wheeler Market Report Scope

| Motorcycles |

| Scooters |

| Mopeds |

| Internal Combustion Engine (ICE) | Below 100 cc |

| 101-125 cc | |

| 126-250 cc | |

| Above 250 cc | |

| Electric Two-Wheelers (E2W) | Below 1 kW |

| 1 kW - 3 kW | |

| 3 kW - 7.5 kW | |

| Above 7.5 kW | |

| Others (CNG/LPG) |

| Chain Drive |

| Belt Drive |

| Shaft Drive |

| Personal Use |

| Commercial Use |

| Delivery and Fleet Services |

| Online |

| Offline |

| Northern Vietnam |

| Central Vietnam |

| Southern Vietnam |

| By Vehicle Type | Motorcycles | |

| Scooters | ||

| Mopeds | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | Below 100 cc |

| 101-125 cc | ||

| 126-250 cc | ||

| Above 250 cc | ||

| Electric Two-Wheelers (E2W) | Below 1 kW | |

| 1 kW - 3 kW | ||

| 3 kW - 7.5 kW | ||

| Above 7.5 kW | ||

| Others (CNG/LPG) | ||

| By Drive Type | Chain Drive | |

| Belt Drive | ||

| Shaft Drive | ||

| By End Use | Personal Use | |

| Commercial Use | ||

| Delivery and Fleet Services | ||

| By Sales Channel | Online | |

| Offline | ||

| By Region | Northern Vietnam | |

| Central Vietnam | ||

| Southern Vietnam | ||

Key Questions Answered in the Report

What is the current value of the Vietnam two-wheeler market?

The market is valued at USD 4.55 billion in 2025 and is expected to reach USD 6.01 billion by 2030.

How fast are electric two-wheelers growing?

Electric models are forecast to expand at an 11.41% CAGR between 2025 and 2030, the fastest among propulsion types.

Which region is growing quickest for two-wheelers in Vietnam?

Southern Vietnam, led by Ho Chi Minh City, is projected to grow at a 7.82% CAGR through 2030.

What share do offline dealers hold?

Physical dealerships accounted for 84.41% of total two-wheeler sales in 2024.

Why are scooters gaining share?

Urban congestion, automatic transmissions, and rising female ridership drive scooters to a 7.63% CAGR through 2030.

Page last updated on: