Thailand Two Wheeler Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

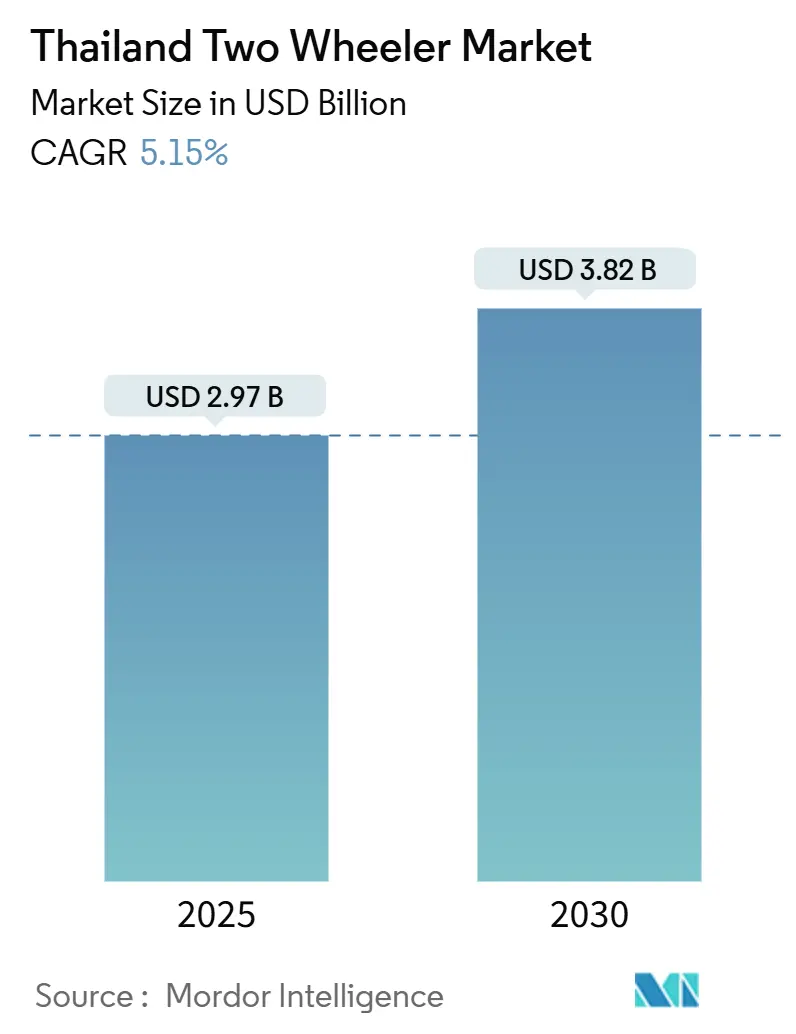

| Market Size (2025) | USD 2.97 Billion |

| Market Size (2030) | USD 3.82 Billion |

| Growth Rate (2025 - 2030) | 5.15% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Two Wheeler Market Analysis by Mordor Intelligence

The Thailand two-wheeler market size stands at USD 2.97 billion in 2025 and is forecast to reach USD 3.82 billion by 2030, translating to a 5.15% CAGR through the period. Thailand is strengthening its status as Southeast Asia's premier motorcycle production hub, buoyed by steadfast government incentives for electrification and a surging demand for adaptable urban mobility solutions. In response, manufacturers are ramping up capacity and output, even as domestic retail demand grapples with challenges from stringent lending conditions and high household debt. Yet, strategic investments in the Eastern Economic Corridor are bolstering component localization and export capabilities, aiding producers in navigating the ups and downs of domestic sales. The e-commerce boom is reshaping mobility demands, driving a heightened appetite for scooters to facilitate last-mile deliveries. On another front, government subsidies are bridging the cost divide between electric and gasoline models, setting the stage for a sustained push towards electrification, despite short-term sales variances. However, the landscape is not without its hurdles: credit availability poses a significant constraint, thrusting financing innovation into the spotlight as a pivotal element of future growth strategies, and steering the evolution of Thailand's two-wheeler market.

Key Report Takeaways

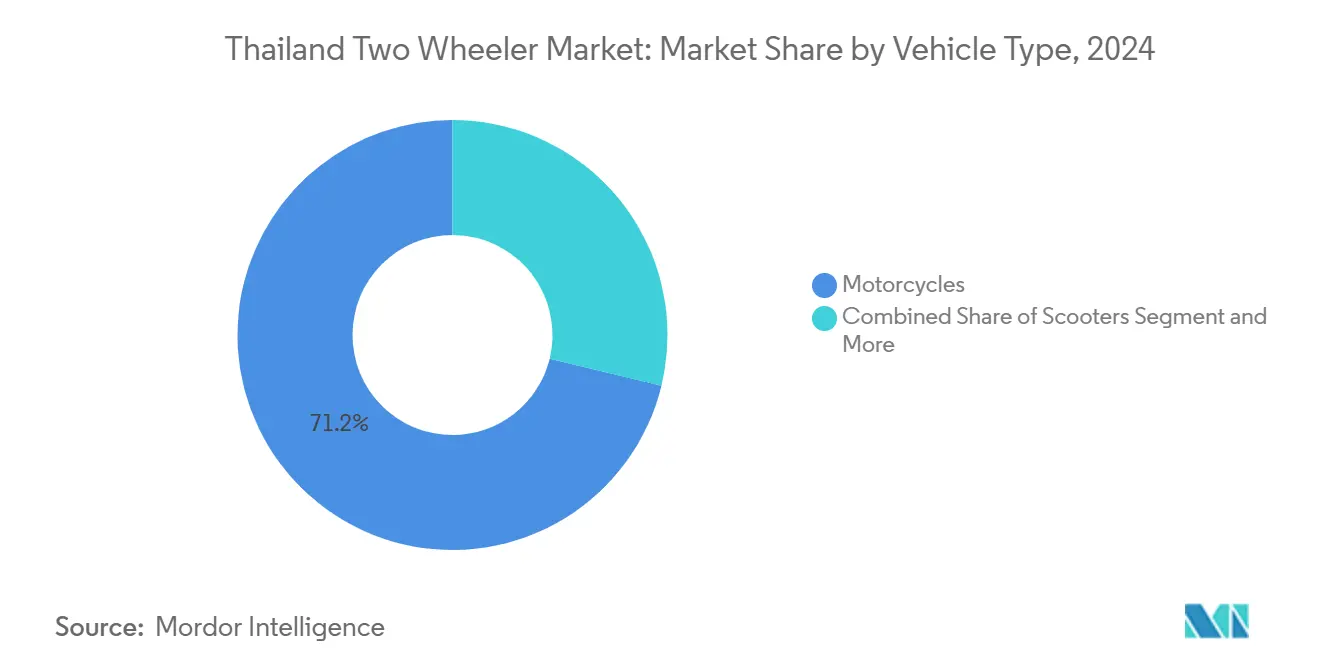

- By vehicle type, motorcycles accounted for 71.28% Thailand's two-wheeler market share in 2024, while scooters, though smaller at 7.52% CAGR, represented the quickest-advancing subsegment to 2030.

- By propulsion, internal combustion engines dominated with an 89.71% of the Thailand two-wheeler market share in 2024, whereas electric two-wheelers, at 12.62% CAGR, recorded the most accelerated uptake among powertrains to 2030.

- By drive system, chain drives led with 75.39% of the Thailand two-wheeler market share in 2024; belt drives, with a 7.88% CAGR, posted the fastest relative expansion to 2030.

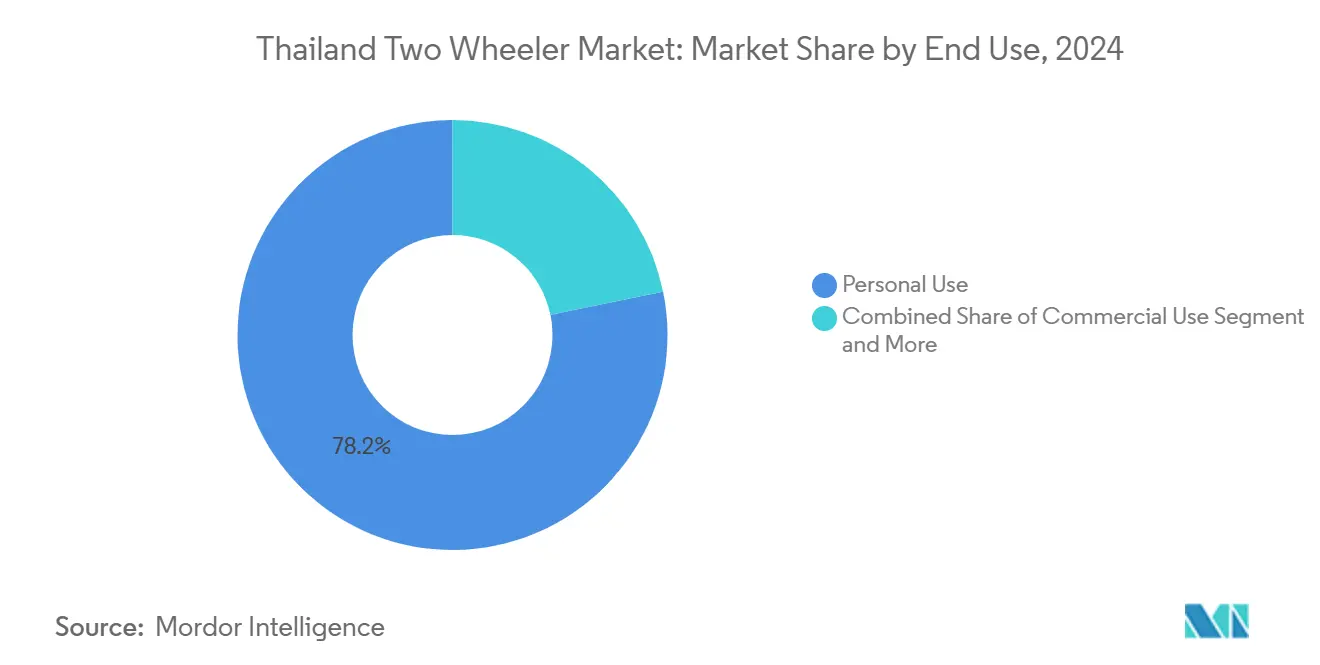

- By end use, personal ownership dominated, with 78.23% of the Thailand two-wheeler market share in 2024, while delivery and fleet applications, with 9.66% CAGR, showed the sharpest growth trajectory to 2030.

- By sales channel, offline dealerships captured 84.41% of the Thailand two-wheeler market share in 2024, yet online platforms, with an 8.87% CAGR, achieved the highest growth pace.

- By region, Bangkok and Central Thailand commanded 36.21% of demand in 2024, while the Eastern Economic Corridor, at 7.65%, emerged as the fastest-growing regional market.

Thailand Two Wheeler Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Last-Mile Delivery Bikes | +1.2% | Bangkok and Central Thailand, EEC | Short term (≤ 2 years) |

| Government EV Subsidy Scheme | +0.8% | National; early gains in Bangkok, Chonburi, Rayong | Medium term (2-4 years) |

| Digital Motorcycle Financing Via Mobile Apps | +0.7% | National, urban concentration | Short term (≤ 2 years) |

| Expansion of Battery-Swap Networks | +0.6% | Bangkok and Central Thailand; major provinces | Medium term (2-4 years) |

| Tourism Rebound and Rental Demand | +0.5% | Southern and Northern resort provinces | Short term (≤ 2 years) |

| Subscription-Based Leasing for Millennials | +0.4% | Bangkok and Central Thailand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Last-mile Delivery Motorcycles

Thailand’s e-commerce boom reshapes two-wheeler usage patterns as food-delivery and parcel platforms expand fleet requirements. Bangkok alone records tens of thousands of riders who now log higher daily mileage than private users, prompting gig workers to favor automatic scooters with integrated cargo space. App-based aggregators continually cut delivery lead times, creating a positive utilization loop that boosts replacement cycles and keeps the Thailand two-wheeler market in motion. Safety concerns tied to shift length and time pressure are prompting regulators to review labor provisions, signaling eventual compliance costs but also pushing demand for purpose-built delivery variants that meet stricter standards. Component suppliers benefit from rising demand for reinforced suspensions, larger luggage racks, and telematics modules that monitor fleet performance.

Government EV Subsidy Scheme Reducing Upfront Cost of E2Ws

The EV 3.5 program pares electric motorcycle prices by up to THB 10,000 and cuts excise tax from 8% to 2%, narrowing parity with gasoline models and encouraging early adopters. Local content rules requiring two domestically produced units for every imported bike by 2027 will attract battery makers and drivetrain firms to Thai industrial zones, further anchoring jobs and technology. Certification through the Thailand Automotive Institute ensures quality thresholds, giving consumers greater confidence in long-term durability. While electric two-wheeler registrations slipped in 2024, the policy’s four-year runway clarifies OEM business plans and dealer network adaptation.

Emergence of Subscription-based Motorcycle Leasing for Urban Millennials

Start-ups pilot monthly subscription plans bundling insurance, maintenance, and swap batteries, appealing to riders who prize flexibility over ownership. The approach suits electric scooters whose residual values and battery warranties remain uncertain. Dealers also view subscriptions as an avenue to lift lifetime customer value—each renewal resets the customer journey, moving repairs and parts into predictable revenue streams.

Tourism Rebound Boosting Rental Motorcycle Demand

International arrivals are back to near-pre-pandemic levels in island and mountain provinces, re-energizing rental fleets that favor 125-150 cc scooters for short-haul leisure trips. Seasonal surges push rental companies to rotate inventory frequently, lifting wholesale demand. Provincial authorities increasingly require helmet use and liability coverage, incentivizing rental operators to modernize fleets with ABS-equipped models and cleaner engines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Hire-Purchase Credit Approval Criteria | -1.8% | Nationwide, deeper effect in rural districts | Short term (≤ 2 years) |

| Sparse Fast-Charging Outside Urban Cores | -0.9% | Northern, Northeastern, rural Southern Thailand | Medium term (2-4 years) |

| Domestic Li-Ion Cell Supply Gap | -0.7% | National, with cost pressure greatest on EEC assemblers | Medium term (2-4 years) |

| High Motorcycle Fatality Rate and Stricter Rules | -0.6% | National; concentrated enforcement in Bangkok and other large cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Public Fast-Charging Infrastructure Outside Urban Cores

In Thailand, the rollout of electric vehicle infrastructure shows a pronounced geographic imbalance. Most charging units are clustered in Bangkok and its neighboring provinces, leaving vast regions in the North and Northeast without adequate service. National utilities have ambitious plans to significantly expand this network by decade's end, aiming to introduce thousands of car chargers and battery-swap stations for electric motorcycles. Yet, despite these plans, coverage gaps pose challenges to widespread EV adoption. Several key barriers, including grid limitations, complexities in land acquisition, and uncertain investment returns, deter private sector involvement. This is especially true in areas where usage might remain low for an extended period. To counter these hurdles, consultancies are pushing for targeted tax incentives and blended-finance models to mitigate risks and draw in capital. Yet, the pace of infrastructure deployment is inconsistent. Without more inclusive planning and innovative financing solutions, Thailand's shift to electric mobility may not achieve its desired breadth and depth.

High Motorcycle Fatality Rate Prompting Stricter Safety Regulations

Thailand’s traffic-fatality rate ranks among the highest globally, with motorcycles involved in most incidents. Road-safety agencies are tightening helmet checks, enforcing ABS mandates for new models, and considering graduated licensing. Compliance costs rise for OEMs and importers alike, squeezing entry-level vehicle margins. Awareness campaigns and insurance reforms will improve outcomes over time but could temporarily slow low-budget sales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Motorcycles Remain Core While Scooters Gain Traction

Motorcycles anchored the Thailand two-wheeler market with a 71.28% share in 2024, underpinned by dense dealer footprints and low running costs. Commuter-class 110-125 cc models dominate daily mobility within this segment, yet adventure and 250 cc-plus categories sustain enthusiast niches and export contracts. Scooters are closing the gap by addressing urban congestion and stop-start delivery routes. The fastest-growing 7.52% CAGR is propelled by automatic transmissions that suit riders facing frequent traffic lights and narrow alleyways. As app-based gig work multiplies, fleet managers specify under-seat storage and flat-floor designs that streamline parcel handling, further buoying scooter demand. In rental hotspots like Phuket, scooters claim near-total dominance among tourists, reinforcing cyclical replenishment cycles that support volume.

A moped sub-segment persists in dense city cores where regulatory benefits such as reduced licensing thresholds and insurance premiums appeal to price-sensitive customers. Emissions compliance looms, with Euro 6-equivalent standards effective 2025. OEMs are phasing in electronic-fuel-injection and after-treatment upgrades that add unit cost but reduce maintenance intervals—an attractive trade-off for high-mileage users.

By Propulsion Type: ICE Still Dominant but Electric Momentum Builds

Internal combustion engines controlled 89.71% of the Thailand two-wheeler market share in 2024, thanks to vast fueling infrastructure and rider familiarity. Segment leaders break ICE demand into four displacement bands: sub-100 cc for entry-level, 101-125 cc mainstream, 126-250 cc performance, and above-250 cc premium export. Each tier now faces Euro 6 calibration work, pushing OEMs toward enhanced fuel injection, three-way catalysts, and lean-burn strategies. Even so, escalating fuel prices and urban emission controls gradually raise the total cost of ownership, opening space for electric penetration.

Electric bikes chart a 12.62% CAGR to 2030, catalyzed by EV 3.5 cash incentives and public-sector fleet pilots. Classification by power output—below 1 kW commuter, 1-3 kW mainstream, 3-7.5 kW sporty, and over 7.5 kW premium—lets manufacturers fine-tune subsidy eligibility and price points. Battery-swap programs mitigate range anxiety, and leasing models unbundle battery ownership from chassis price, slicing upfront costs further. Meanwhile, alternative gaseous fuels (CNG/LPG) capture fractionally small niches, primarily among institutional fleets looking for bridging solutions to the nation’s net-zero pathway.

By Drive Type: Chain Prevails as Belt Technology Advances

Chain systems delivered 75.39% of 2024 shipments, prized for durability under Thailand’s humid, dusty, and sometimes flood-prone environment. Low parts cost and ubiquitous mechanic know-how keep chains entrenched, especially in rural districts where self-service repairs are common. At the same time, belt drives gain pace at 7.88% CAGR as urban scooter sales mount. Riders appreciate cleaner operation and quietness, while fleet operators value the extended maintenance intervals that trim downtime. Electric scooter OEMs routinely specify belts to align with low-noise branding, reinforcing the shift.

Shaft drives remain the domain of heavyweight touring and police motorcycles. Although virtually maintenance-free, shafts carry higher initial expense and weight penalties, limiting their presence to niche buyers. Ongoing industrial-estate investments in the EEC could one day localize more belt-production capacity, shortening supply chains and narrowing unit-cost differentials, but chains will hold price leadership into the medium term.

By End Use: Personal Mobility Maintains Lead yet Commercial Demand Accelerates

Household transportation needs kept personal riders at a 78.23% share in 2024. Bikes bridge the last mile to jobs, clinics, and schools in towns where buses run infrequently and rail coverage is thin. Financing promotions and factory warranties make new units accessible, though credit headwinds test uptake. In parallel, delivery and fleet requirements climb at a 9.66% CAGR as online grocery, parcel, and ride-hailing ecosystems scale. Fleet operators increasingly negotiate bulk purchase contracts and preventive-maintenance agreements, magnifying bargaining power over OEMs.

Commercial sub-segments include motorcycle-taxi cooperatives, rental outfits serving tourism corridors, and corporate couriers. High utilization prompts quick depreciation; thus, operators prioritize robust engines, fuel efficiency, and low parts downtime. Several fleet players pilot battery-swap scooters engineered for 100-plus km daily duty, suggesting that the total cost of electric ownership could outcompete gasoline sooner in fleets than in private garages.

By Sales Channel: Omnichannel Blurs Online-Offline Divide

Brick-and-mortar dealerships accounted for 84.41% of 2024 volume, a testament to Thai buyers’ preference for in-person inspection, test rides, and spot-credit processing. Multi-brand showrooms and provincial fairs connect rural customers to finance firms, enabling same-day delivery of ride-ready units. Yet online research and reservation tools reshape the path to purchase. With a 8.87% CAGR to 2030, virtual storefronts no longer stop at price comparison; they host 360-degree model tours, push trade-in quotes, and sync with e-wallets for deposits.

Digital financing APIs feed consumers real-time approval status, shortening the buyers’ journey. Post-purchase, apps schedule service appointments and deliver loyalty offers—functions that keep dealerships in the loop while elevating overall experience. Independent marketplaces carve revenue by bundling insurance, accessories, and loan origination, hinting that future competition may revolve less around vehicle supply and more around data-driven customer retention.

Geography Analysis

Bangkok and its Central Thailand satellite provinces represent the single largest regional slice of the Thailand two-wheeler market with a 36.21% share in 2024. They benefit from metropolitan density, disposable incomes, and a multimodal transport fabric that still leaves short-range gaps filled by motorcycles. Metro policies have introduced contactless fare systems and expanded bike lanes, yet public transport overcrowding during peak hours keeps powered two-wheelers in heavy rotation[1]“Contactless Urban Mobility Insights,”, Visa Thailand, visa.co.th. Dealer density ensures ready access to after-sales service, and pervasive e-commerce warehousing underpins gig-economy rider demand. Charging infrastructure is most advanced here, with state utilities clustering stations along arterial roads, positioning Bangkok as the bellwether for electric adoption.

The Eastern Economic Corridor posts the fastest growth through 2030 with a 7.65% CAGR. Industrial estates in Chonburi, Rayong, and Chachoengsao welcome automakers pivoting to electrification; Triumph’s new plant, Harley-Davidson’s model shift, and Sunwoda’s cell factory exemplify the ecosystem in motion[2]“Triumph Plant 4 Ground-Breaking,”, Amata Corporation, amata.com. Modern ports and dual-track rail streamline logistics, making the EEC an export springboard. Worker commuting needs, supplier shuttle fleets, and testing tracks all feed two-wheeler demand. At the same time, local authorities fast-track permits for EV charging and swap stations to showcase smart-city credentials.

Northern Thailand leverages tourism and cross-border trade with Laos and Myanmar. Scenic routes draw touring clubs who favor mid-capacity adventure bikes, boosting premium garages in Chiang Mai. Agricultural cycles swing personal purchases, with bumper harvests translating into down-payments. Due to sparse public transit, northeastern (Isan) provinces rely on motorcycles for everyday transport, but credit risk is higher, so loan approvals lag the national average. Subsidized community-bank schemes partially offset barriers, yet ICE models remain dominant until charging grids extend eastward.

Southern Thailand’s resort economies—Phuket, Krabi, Surat Thani—generate brisk rental turnover. Tourist-oriented dealers purchase fleet stock in bulk ahead of high season, driving localized spikes in wholesale demand. Rubber and palm-oil exporters provide steady income flows, enabling private ownership, though seasonal rainfall influences riding patterns. Infrastructure expansion continues around airports and seaports, promising a gradual lift to electric prospects as swap kiosks piggy-back on fuel stations along coastal highways.

Competitive Landscape

Thailand's motorcycle industry boasts a competitive structure that's moderately concentrated. This concentration offers scale advantages, boosts operational efficiency, and leaves space for challengers and niche players to stake their claim. Aiming to defend its leadership, Honda is consolidating its assembly operations into a single, high-efficiency site. However, it keeps component plants active to cater to regional demand across ASEAN. Yamaha boldly invests in hybrid-ready engine lines, underscoring its commitment to electrification and urban mobility. Kawasaki is honing in on niche sports segments, leveraging its brand strength and specialized products to stay relevant. On the other hand, Suzuki is pivoting. While it's stepping back from automobile production in Thailand, it's doubling down on motorcycles, channeling resources into affordable commuter models that align with shifting regulatory standards. These maneuvers highlight a broader industry trend, with manufacturers pivoting towards efficiency, electrification, and nuanced market segmentation in response to evolving consumer preferences and policy shifts.

New entrants are capitalizing on electrification and trade-zone incentives. Royal Enfield's CKD operation in Samut Prakan is trimming tariffs and allowing for spec customization tailored to Thai riders[3]“Royal Enfield CKD Factory Overview,”, KiWAV Motor, kiwav.com. Harley-Davidson is strategically relocating three models, enhancing utilization at its Rayong plant, and setting its sights on regional free-trade corridors. Domestic energy giants are making waves in the mobility sector: PTT's Arun Plus is rolling out On-Ion swap stations, and Bangchak is throwing its weight behind Winnonie's subscription scooters. This move signifies a budding vertical integration between energy retail and vehicle services. Meanwhile, component heavyweights like Thai Stanley and AAPICO are forging alliances with battery pack and charger suppliers, highlighting the merging lanes of the automotive and electronics value chains.

Price wars are kept at bay, thanks to a mix of differentiated warranties, enticing financing bundles, and the weight of brand heritage. However, the rise of online marketplaces is leveling the playing field, pushing OEMs to adopt transparent pricing and standardized service costs. The realm of accessories—from helmets to smart dashcams—has emerged as a crucial battleground for cultivating rider loyalty. Looking to the future, corporate fleet tenders for delivery bikes could shift the bargaining power dynamics, especially in the electrified segment, where total cost of ownership is becoming the key decision-making factor.

Thailand Two Wheeler Industry Leaders

Honda Motor Co., Ltd.

Yamaha Motor Co., Ltd.

GPX Thailand

Suzuki Motor Corporation

Kawasaki Motors, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Mile Green, an electric vehicle (EV) company, announced plans to develop Thailand's EV infrastructure. The company, with headquarters in Hong Kong and Thailand, aims to expand the country's EV charging network.

- December 2024: Royal Enfield has inaugurated its first CKD (completely knocked down) assembly facility outside India in Samut Prakan, Bangkok. The facility, fully owned and operated by Royal Enfield, demonstrates the motorcycle manufacturer's focus on the Thai market and the broader Asia-Pacific (APAC) region.

Thailand Two Wheeler Market Report Scope

| Motorcycles |

| Scooters |

| Mopeds |

| Internal Combustion Engine (ICE) | Below 100 cc |

| 101-125 cc | |

| 126-250 cc | |

| Above 250 cc | |

| Electric Two-Wheelers (E2W) | Below 1 kW |

| 1 kW - 3 kW | |

| 3 kW - 7.5 kW | |

| Above 7.5 kW | |

| Other Alternative Fuels | CNG/LPG |

| Chain Drive |

| Belt Drive |

| Shaft Drive |

| Personal Use |

| Commercial Use |

| Delivery and Fleet Services |

| Online |

| Offline |

| Bangkok and Central Thailand |

| Eastern Economic Corridor |

| Northern Thailand |

| Northeastern Thailand |

| Southern Thailand |

| By Vehicle Type | Motorcycles | |

| Scooters | ||

| Mopeds | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | Below 100 cc |

| 101-125 cc | ||

| 126-250 cc | ||

| Above 250 cc | ||

| Electric Two-Wheelers (E2W) | Below 1 kW | |

| 1 kW - 3 kW | ||

| 3 kW - 7.5 kW | ||

| Above 7.5 kW | ||

| Other Alternative Fuels | CNG/LPG | |

| By Drive Type | Chain Drive | |

| Belt Drive | ||

| Shaft Drive | ||

| By End Use | Personal Use | |

| Commercial Use | ||

| Delivery and Fleet Services | ||

| By Sales Channel | Online | |

| Offline | ||

| By Region | Bangkok and Central Thailand | |

| Eastern Economic Corridor | ||

| Northern Thailand | ||

| Northeastern Thailand | ||

| Southern Thailand | ||

Key Questions Answered in the Report

What is the current value of the Thailand two-wheeler market?

It is valued at USD 2.97 billion in 2025, with a projected rise to USD 3.82 billion by 2030.

Which segment is growing fastest within Thai two-wheelers?

Electric two-wheelers lead growth with a 12.62% CAGR forecast for 2025-2030, propelled by subsidies and swap-station rollouts.

How big is scooter demand compared with motorcycles?

Motorcycles still rule at 71.28% share in 2024, but scooters post the quickest segment growth at 7.52% CAGR to 2030.

Which companies recently invested in Thai two-wheeler manufacturing?

Royal Enfield opened a 30,000-unit CKD facility in 2025, while Harley-Davidson will shift production of three models to its Rayong plant from 2025 onward.

Page last updated on: