Indonesia Two Wheeler Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

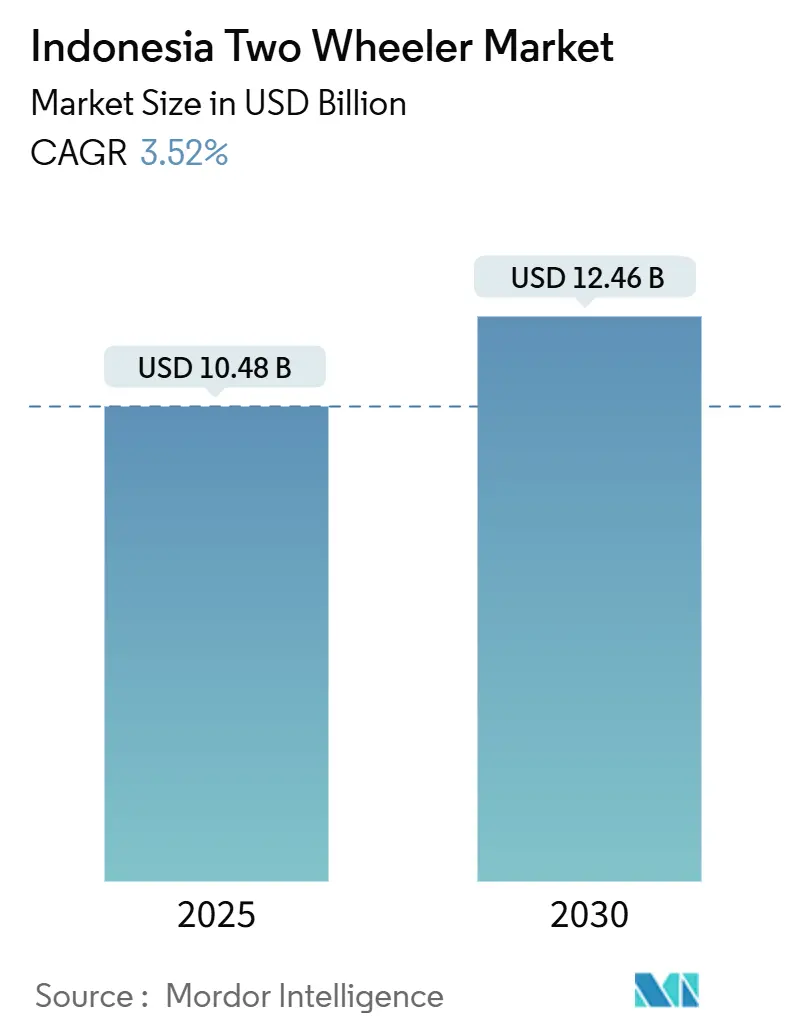

| Market Size (2025) | USD 10.48 Billion |

| Market Size (2030) | USD 12.46 Billion |

| Growth Rate (2025 - 2030) | 3.52% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Two Wheeler Market Analysis by Mordor Intelligence

The Indonesian two-wheeler market size is valued at USD 10.48 billion in 2025 and is projected to reach USD 12.46 billion by 2030, advancing at a 3.52% CAGR during the forecast period. Robust household purchasing power, rising urbanisation, and dependable retail financing underpin steady demand, while early-stage electrification introduces fresh competitive dynamics. Internal-combustion models still anchor sales volumes, but electric scooters enjoy double-digit growth as government incentives and air-quality concerns encourage adoption. Regional performance remains uneven: Java dominates unit sales thanks to its dense population and deep dealer footprint. Kalimantan records the fastest expansion due to infrastructure projects and mining-led income gains. Established Japanese OEMs defend their share with broad lineups and far-reaching service networks, yet local electric specialists and cost-focused Indian brands intensify price and technology rivalry.

Key Report Takeaways

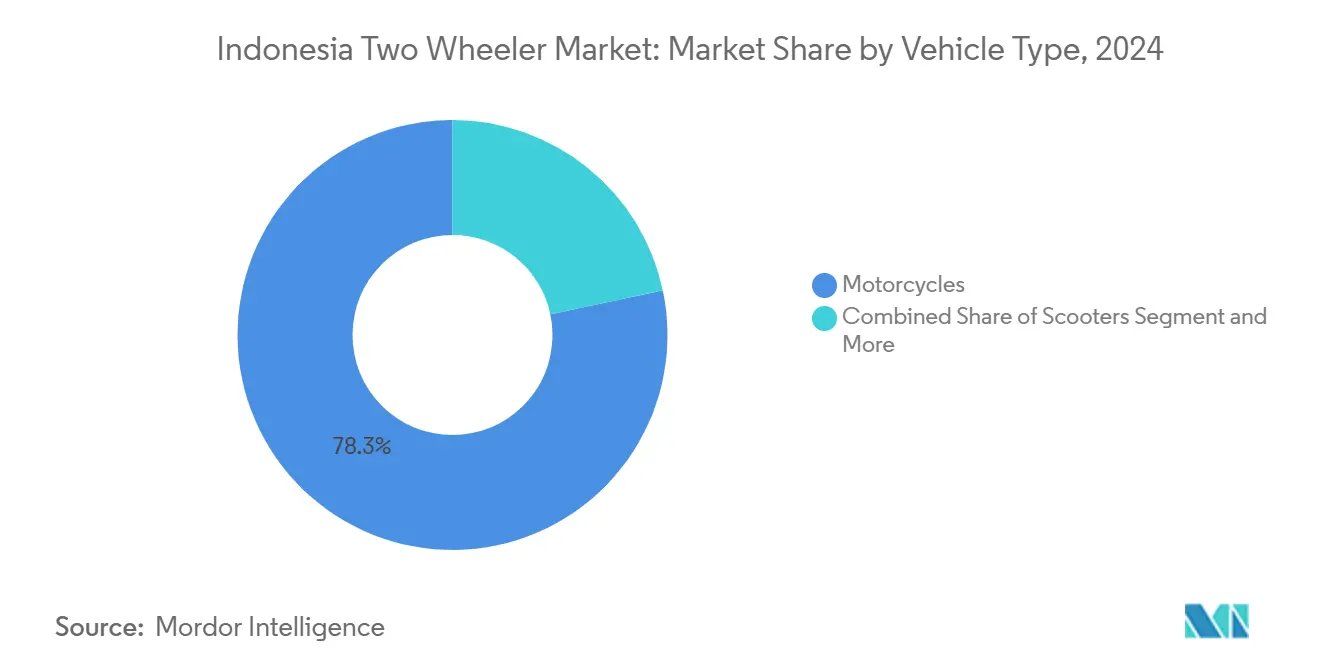

- By vehicle type, motorcycles commanded 78.32% of the Indonesian two-wheeler market share in 2024; scooters are projected to grow at a 5.16% CAGR through 2030.

- By propulsion type, internal-combustion engines held 89.17% of the Indonesian two-wheeler market share in 2024, while electric two-wheelers are forecast to advance at a 13.41% CAGR through 2030.

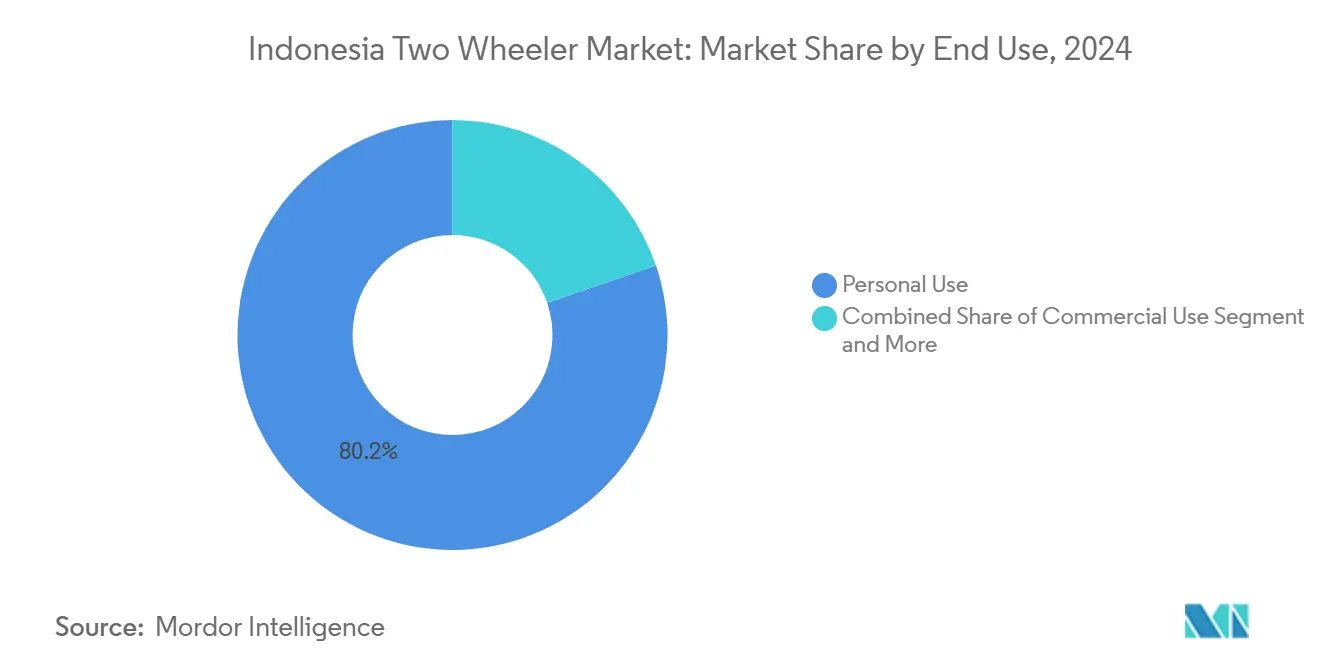

- By end use, personal ownership represented 80.23% of the Indonesian two-wheeler market share in 2024; delivery and fleet applications are expected to climb at a 9.22% CAGR during the same horizon.

- By sales channel, offline dealerships captured 84.41% of the Indonesian two-wheeler market share in 2024; online platforms are anticipated to rise at an 8.17% CAGR through 2030.

- By geography, Java contributed 59.28% of Indonesia's two-wheeler market share in 2024; Kalimantan is poised to expand at a 7.26% CAGR to 2030.

Indonesia Two Wheeler Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government E-Mobility Roadmap and Incentives | +1.2% | National, with concentration in Java and Bali | Short term (≤ 2 years) |

| Abundant Nickel Reserves Attracting Battery and E2W Investment | +0.9% | National, with manufacturing clusters in Java | Long term (≥ 4 years) |

| Rising Disposable Income and Rapid Urbanization | +0.8% | Java, Sumatra, major metropolitan areas | Medium term (2-4 years) |

| Gig-Economy Delivery Boom in Tier-2/3 Cities | +0.7% | Tier-2/3 cities across all regions | Medium term (2-4 years) |

| Growth in Retail Financing and Leasing Options | +0.6% | National, stronger penetration in tier-2/3 cities | Medium term (2-4 years) |

| Shift Toward Affordable Personal Mobility Post-COVID | +0.4% | Urban centers across Java, Sumatra, Kalimantan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government E-Mobility Roadmap and Incentives

Presidential Regulation 55/2019 targets 13 million electric motorcycles by 2030 and provides IDR 7 million (USD 466) purchase subsidies, import-duty relief on battery components, and VAT discounts [1]“Government Disburses Electric Motorcycle Subsidies,”, Tempo, tempo.co. The Ministry of Industry distributed 63,146 subsidised units in 2024 and plans a VAT-relief model in 2025 to streamline disbursement. Local-content rules (TKDN) push manufacturers to assemble battery packs domestically, spurring investment in module plants around Karawang and Surabaya. While subsidy uptake lags headline targets, the policy mix narrows the total-cost-of-ownership gap between electric and gasoline models, particularly in Jakarta and Bali, where emissions regulations tighten first.

Abundant Nickel Reserves Attracting Battery and E2W Investment

Indonesia holds around 40% of global nickel resources and seeks to capture more value by moving up the battery supply chain [2]“Nickel Reserves and Battery Roadmap,”, CNN Indonesia, cnnindonesia.com. Joint ventures between Japanese, Korean, and local firms plan cathode and cell facilities in Java and Sulawesi, integrating raw-material supply with final-pack assembly. Successful commissioning could lower electric scooter battery costs by trimming logistics expenses and import duties, improving price parity with 110-125 cc gasoline scooters. Longer term, local recycling plants would close the loop, addressing sustainability concerns and stabilizing raw-material pricing.

Rising Disposable Income and Rapid Urbanization

Accelerating migration into Greater Jakarta, Surabaya, Medan, and an expanding roster of tier-2 cities elevates the importance of affordable personal mobility. World Bank data shows sustained urban population growth that stresses mass-transit capacity, making two-wheelers the practical alternative [3]“Indonesia Urban Population Data,”, World Bank, worldbank.org. Improving wages enables households to trade basic motorcycles for premium scooters that offer automatic transmissions, better fuel economy, and additional storage. Beyond Java, fast-growing cities such as Makassar and Balikpapan replicate this pattern, widening the geographic footprint of demand. OEMs respond with broader colour palettes, connectivity features, and instalment plans to convert first-time buyers.

Gig-Economy Delivery Boom in Tier-2/3 Cities

Grab and Gojek extend delivery services into Bandung, Semarang, and Denpasar, generating an incremental need for cargo-optimised two-wheelers. University research from Surabaya finds that drivers rank fuel efficiency and resale value as top purchase criteria, channelling demand toward models from brands with dense service networks. OEMs introduce factory-fitted rear carriers, reinforced suspensions, and service packages that include scheduled maintenance and accident coverage to appeal to this commercial customer set. The segment’s growth diversifies revenue away from crowded metropolitan arenas.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aspirational Shift to Entry-Level Cars | -0.5% | Java urban centers, emerging middle-class areas | Medium term (2-4 years) |

| Weak Domestic Battery Supply Chain | -0.4% | National, affecting electric segment growth | Medium term (2-4 years) |

| Inner-City Traffic Restrictions on Two-Wheelers | -0.3% | Major urban centers, particularly Jakarta and Bali | Short term (≤ 2 years) |

| Seasonal Flooding Driving Up Insurance Costs | -0.2% | Java, Sumatra, coastal regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aspirational Shift to Entry-Level Cars

Gaikindo data shows stable demand for compact cars such as the Toyota Agya as rising middle-class consumers equate four-wheel ownership with social ascent. Competitive financing narrows monthly payment gaps between top-tier scooters and low-cost cars, siphoning prospective buyers—especially dual-income households—from the Indonesian two-wheeler market. Manufacturers counter by adding smartphone-linked dashboards and larger under-seat storage to scooters, positioning them as ‘second cars’ rather than budget options.

Weak Domestic Battery Supply Chain

Despite abundant nickel, most battery cells still arrive from overseas; only pack assembly occurs locally. Import dependence inflates costs and exposes electric scooter pricing to currency swings. The absence of a national recycling policy also clouds residual-value calculations, slowing fleet-operator procurement decisions. Local firms such as Gesits search for technology partners to accelerate cell production but face intellectual-property barriers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type – motorcycles dominate while scooter adoption accelerates

Motorcycles generated 78.32% of 2024 shipments within the Indonesian two-wheeler market, reflecting their versatility across urban alleys and rural roads. In contrast, with a forecast 5.16% CAGR, scooters attract commuters seeking automatic transmissions and cleaner styling. The Indonesian two-wheeler market size for scooters is set to widen steadily as more women riders and first-time owners choose low-seat models.

OEM strategies illustrate this divergence: Kawasaki commenced local production of the W175L to supply value-oriented enthusiasts, and simultaneously launched the Z900 for performance seekers. Such moves reinforce motorcycle loyalty across varied displacement bands while scooters thrive in metropolitan showrooms displaying Honda’s EM1 e: and Yamaha’s Fazzio hybrids. Ongoing urban densification and better road quality continue to expand scooter addressability without eroding the core motorcycle customer base.

By Propulsion Type – ICE retains scale as electrification gains momentum

Internal-combustion units held 89.17% of 2024 deliveries, but electric models are climbing at 13.41% CAGR, redrawing long-term competitive lines. The Indonesian two-wheeler market size for electric variants should exceed USD 1 billion by 2030, provided subsidy frameworks remain intact. Smaller 101-125 cc gasoline bikes still dominate cost-sensitive rural pockets, whereas Jakarta consumers increasingly cross-shop premium electric scooters with smartphone-controlled features.

TVS plans local assembly of the iQube in 2025 to meet TKDN rules and price the model below IDR 50 million (USD 3,004). Government targets of 13 million e-motorcycles create a large theoretical headroom, yet infrastructural gaps persist. OEMs, therefore, pair home chargers with dealership-based fast-charging to overcome range anxiety until public networks mature.

By Drive Type – chain drive leads, belt technology gains favor

Chain systems captured a 75.27% share in 2024, thanks to affordability and ease of roadside servicing across the archipelago. Belt drives, expanding at 7.88% CAGR, resonate with urban riders looking for quieter, lower-maintenance ownership. The Indonesian two-wheeler market share of belt drive scooters is expected to widen as electric powertrains, which naturally pair with belt systems, proliferate.

Honda’s EM1 e: exemplifies this transition by coupling an electric motor with a belt transmission to emphasise silent running and minimal upkeep. Shaft drives remain a niche confined to high-end tourers, where long-distance reliability offsets higher upfront costs. Over the forecast window, belt technology penetration will track rising disposable incomes and consumer willingness to pay for convenience.

By End Use – personal transportation rules as delivery fleets surge

Personal riding generated 80.23% of unit demand in 2024, underscoring the motorcycle’s role as the primary household vehicle across Indonesia. Delivery and dedicated fleet usage, advancing at 9.22% CAGR, benefit from e-commerce expansion and the geographic push of on-demand platforms into secondary towns. The Indonesian two-wheeler market size for last-mile delivery could double by 2030 if platform rider enrollment continues at the current velocity.

Grab and Gojek collaborate with OEMs on fleet-negotiated pricing and bundled maintenance contracts, signalling rising professionalism among gig drivers. Manufacturers introduce heavy-duty clutches, reinforced frames, and cargo-box mounting points to tailor offerings for high-utilisation cycles. In parallel, financing firms create mileage-based repayment schemes that match delivery income variability, sustaining fleet uptake even during off-peak seasons.

By Sales Channel – brick-and-mortar keeps edge while e-commerce supplements reach

Offline dealerships controlled 84.41% of 2024 purchases within the Indonesian two-wheeler market, reinforcing the importance of test rides, warranty discussions, and after-sales service in the buyer journey. Online channels, though smaller, are set to grow 8.17% CAGR as digital-native shoppers configure models and secure loan pre-approvals before visiting a showroom.

Gesits exemplifies an omnichannel approach, running dealerships and service centres that fulfil orders initiated via social-media campaigns. OEMs invest in virtual showrooms and augmented-reality apps to preview colour options and accessories, yet they still rely on physical outlets for final document processing and unit delivery. Over time, the line between online and offline blurs into a single integrated path to purchase.

Geography Analysis

Java generated 59.28% of Indonesia's two-wheeler market revenue in 2024, anchored by dense population clusters, concentrated manufacturing, and broad service coverage. Jakarta consumers gravitate toward technology-rich scooters, while rural Central Java favours low-cc commuter bikes. Dealer footprints in Surabaya and Bandung support rapid spare-parts availability, limiting downtime and reinforcing brand loyalty. Market maturity forces OEMs to deploy loyalty programs and insurance tie-ups to defend share in these saturated zones.

Kalimantan posts the fastest regional growth at 7.26% CAGR through 2030, buoyed by commodity-driven incomes and limited public-transport alternatives. Mining towns around Balikpapan and Samarinda exhibit above-average penetration of mid-displacement motorcycles that endure rough haul roads. OEMs establish satellite workshops capable of on-site servicing to minimise rider travel distances, addressing geographic isolation. Infrastructure projects tied to the new national capital in East Kalimantan promise additional demand catalysts.

Sumatra sustains mid-single-digit expansion as the plantation and petrochemical sectors underpin steady cash flows. Medan and Palembang hubs channel inventory across provincial borders, while seasonal palm-oil earnings influence purchasing timetables. Sulawesi benefits from nickel-processing investments that raise local salaries and upgrade preferences toward belt-drive scooters. Bali and Nusa Tenggara balance tourist-led demand with regulatory limits on motorcycle access near heritage sites, incentivizing electric adoption through preferential parking and entry rules. Lesser-served islands such as Maluku and Papua remain nascent, yet improving ferry links and road paving gradually lift motorcycle affordability and availability.

Competitive Landscape

The Indonesian two-wheeler market is moderately concentrated; Honda leverages its Karawang engine plant to localise high-volume components, while Yamaha pilots battery-swapping kiosks with utility firms to build infrastructure moats. Suzuki refreshes styling and connectivity across its underbone lineup to remain relevant among younger riders.

Home-grown Gesits pursues urban e-scooter niches through a direct-sales model complemented by value-added services such as bundled insurance and ride-share partnerships. TVS Motor Company Indonesia positions the iQube below premium Japanese electric offerings by tapping Indian cost synergies and meeting local-content thresholds through a forthcoming battery pack line. Chinese entrants test the waters via distributorships that import CKD kits, but face tariff headwinds and brand-trust gaps.

Strategic playbooks increasingly revolve around electrification readiness, with OEMs committing capex to battery labs, charging alliances, and software integration. Dealer networks evolve into mobility hubs that sell accessories, insurance, and financing rather than merely vehicles. As subsidies taper, competitive focus will shift from headline pricing toward total cost of ownership, durability, and residual value assurance.

Indonesia Two Wheeler Industry Leaders

PT Astra Honda Motor.

PT. Yamaha Indonesia Motor Manufacturing

Suzuki Indonesia

Kawasaki Motor Indonesia

GESITS MOTOR NUSANTARA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: PT TVS Motor Company Indonesia has announced the local assembly of the TVS iQube electric scooter at its East Karawang plant. This move highlights the company's commitment to expanding its presence in the Indonesian electric vehicle market and catering to the growing demand for sustainable mobility solutions.

- May 2025: Harley-Davidson makes a triumphant return to Indonesia, unveiling seven brand-new motorcycles for Model Year 2025, highlighted by the eagerly awaited comeback of its prestigious CVO (Custom Vehicle Operations) Special Edition.

Indonesia Two Wheeler Market Report Scope

| Motorcycles |

| Scooters |

| Mopeds |

| Internal Combustion Engine (ICE) | Below 100 cc |

| 101-125 cc | |

| 126-250 cc | |

| Above 250 cc | |

| Electric Two-Wheelers (E2W) | Below 1 kW |

| 1-3 kW | |

| 3-7.5 kW | |

| Above 7.5 kW | |

| Others (CNG/LPG) |

| Chain Drive |

| Belt Drive |

| Shaft Drive |

| Personal Use |

| Commercial Use |

| Delivery & Fleet Services |

| Online |

| Offline |

| Java |

| Sumatra |

| Kalimantan |

| Sulawesi |

| Bali & Nusa Tenggara |

| Other Islands |

| By Vehicle Type | Motorcycles | |

| Scooters | ||

| Mopeds | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | Below 100 cc |

| 101-125 cc | ||

| 126-250 cc | ||

| Above 250 cc | ||

| Electric Two-Wheelers (E2W) | Below 1 kW | |

| 1-3 kW | ||

| 3-7.5 kW | ||

| Above 7.5 kW | ||

| Others (CNG/LPG) | ||

| By Drive Type | Chain Drive | |

| Belt Drive | ||

| Shaft Drive | ||

| By End-Use | Personal Use | |

| Commercial Use | ||

| Delivery & Fleet Services | ||

| By Sales Channel | Online | |

| Offline | ||

| By Region | Java | |

| Sumatra | ||

| Kalimantan | ||

| Sulawesi | ||

| Bali & Nusa Tenggara | ||

| Other Islands | ||

Key Questions Answered in the Report

How large is the Indonesia two-wheeler market in 2025?

The Indonesia two-wheeler market size stands at USD 10.48 billion in 2025.

What is the growth outlook for electric two-wheelers?

Electric models are projected to grow at a 13.41% CAGR through 2030, supported by subsidies and improving charging access.

Which region is expanding fastest for motorcycle sales?

Kalimantan leads regional growth with a 7.26% CAGR forecast to 2030.

What financing options support motorcycle purchases?

Multifinance firms such as FIF and Adira Finance offer installment plans, while fintech platforms provide instant approvals for underserved borrowers.

How are government incentives changing in 2025?

Direct cash subsidies for electric motorcycles will transition to value-added-tax discounts to widen access and reduce fiscal burden.

Page last updated on: