Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

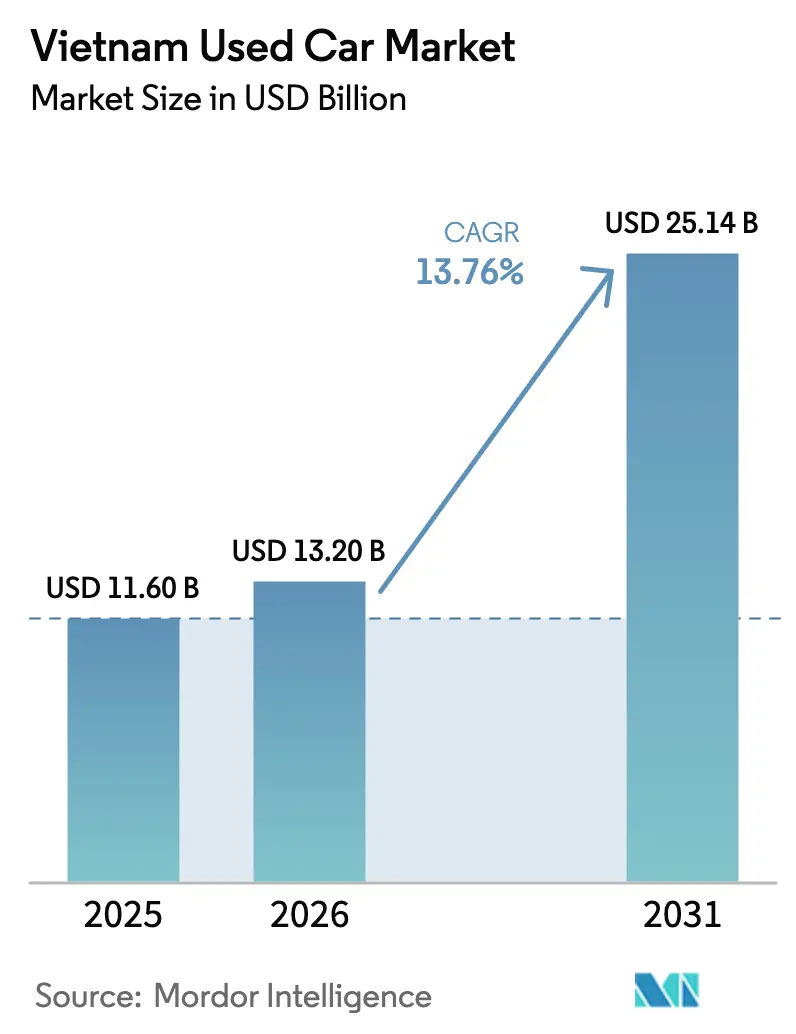

| Base Year Market Size (2025) | USD 11.60 Billion |

| Market Size (2026) | USD 13.20 Billion |

| Market Size (2031) | USD 25.14 Billion |

| Growth Rate (2026 - 2031) | 13.76% CAGR |

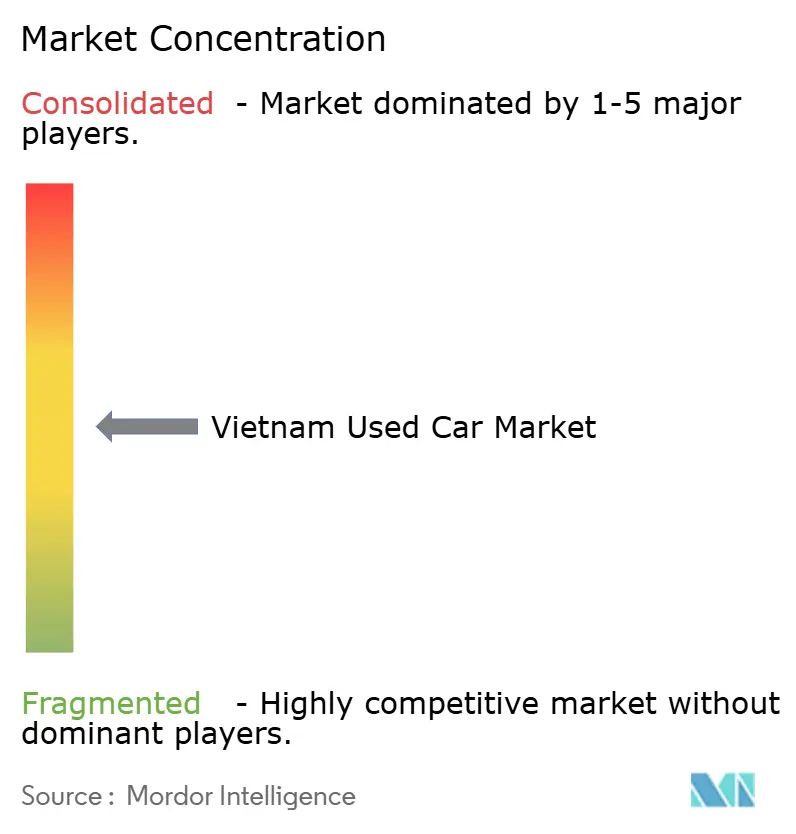

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Used Car Market Analysis by Mordor Intelligence

The Vietnam used-car market size is expected to grow from USD 11.60 billion in 2025 to USD 13.20 billion in 2026 and is forecast to reach USD 25.14 billion, growing at a CAGR of 13.76% during the forecast period (2026-2031). Rising disposable incomes, widening price gaps between new and used vehicles, and tightening emissions rules are accelerating used-vehicle adoption nationwide. Online marketplaces already guide most purchase journeys, while certified dealerships extend professional retail standards beyond core metros. Vehicle financing at loan-to-value ratios above 80% broadens access for first-time buyers, even as looming Euro-5 import rules steer demand toward younger, cleaner inventory. These forces together position the Vietnamese used car market among Southeast Asia’s fastest-growing mobility ecosystems.

Key Report Takeaways

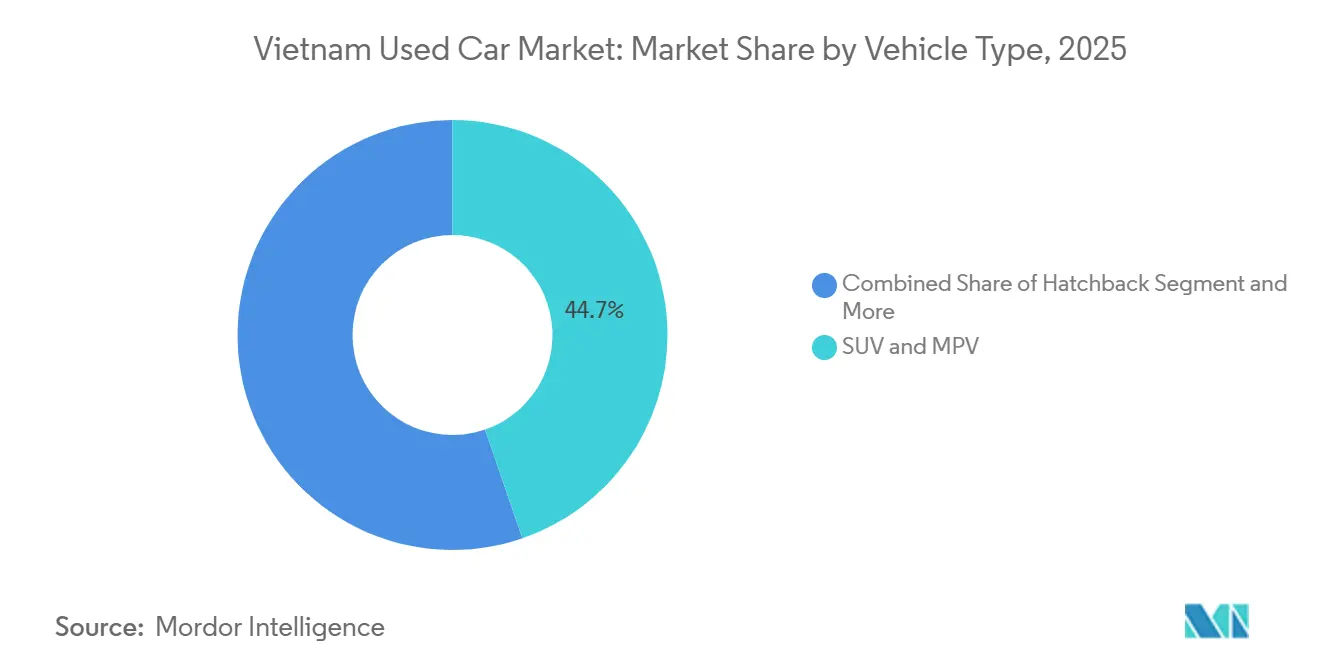

- By vehicle type, SUVs and MPVs led the Vietnam used-car market with 44.72% market share in 2025, and the same segment is forecast to post a 14.12% CAGR through 2031.

- By fuel type, petrol vehicles held 84.63% of the Vietnam used-car market share in 2025; battery-electric vehicles are projected to post an 18.28% CAGR through 2031.

- By sales channel, online marketplaces captured 58.55% of the Vietnam used car market share in 2025 and are poised to expand at a 14.45% CAGR through 2031.

- By vehicle age, the 3-5-year band held 46.91% of the Vietnam used-car market share in 2025, while cars less than 3 years old are expected to grow at a 15.52% CAGR through 2031.

- By price band, the USD 7-15 k tier commanded 38.74% of the Vietnam used car market share in 2025; the USD 15-30 k inventory should accelerate at a 15.86% CAGR through 2031.

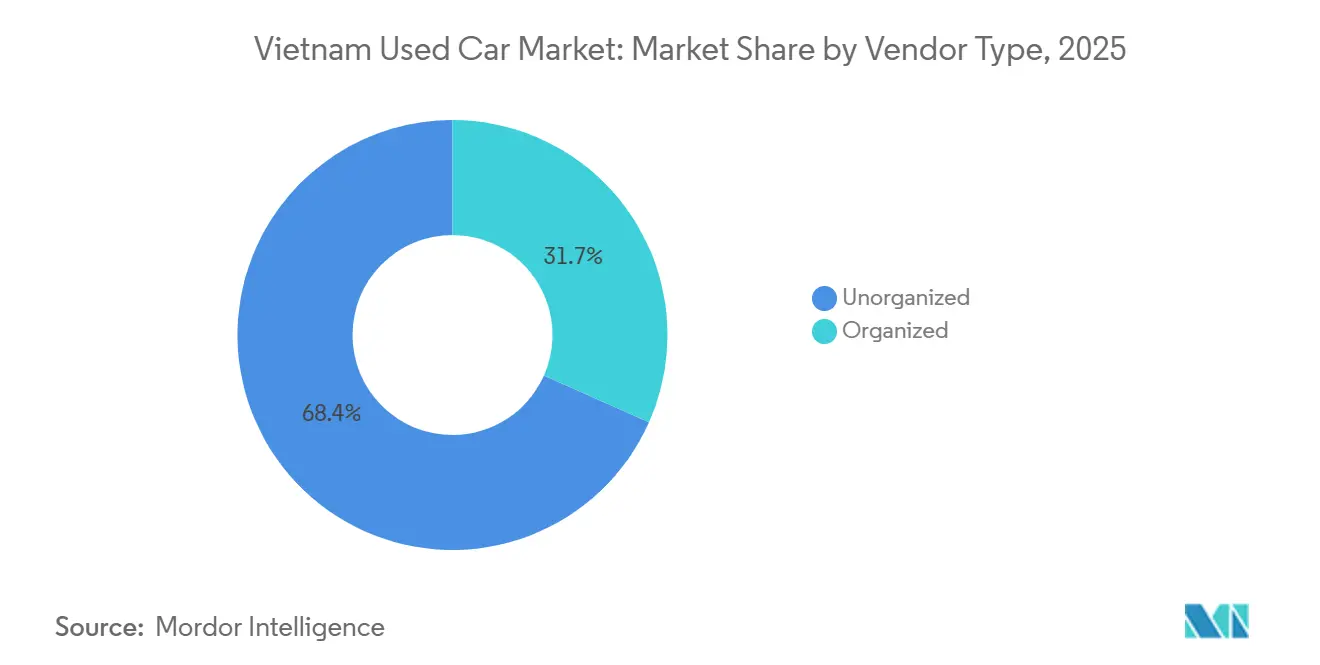

- By vendor type, the unorganized segment held 68.35% of the Vietnam used-car market share in 2025, while organized vendors will witness the fastest growth, with a 16.86% CAGR by 2031.

- By mileage, cars under 20,001 km and 50,000 km commanded 47.56% market share in 2025, while the below 20,000 km segment is projected to grow at a CAGR of 16.41% through 2031.

- By region, South Vietnam accounted for 48.20% of the Vietnam used-car market share in 2025, whereas Central Vietnam is projected to grow at a 15.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Price Delta | +3.2% | HCMC and Hanoi | Medium term (2-4 years) |

| Vehicle Financing Above 80% LTV | +2.8% | Urban centers | Short term (≤2 years) |

| Digital Marketplaces Expand City Reach | +2.4% | Central and North secondary cities | Short term (≤2 years) |

| OEM-Backed Pre-Owned Programs | +2.1% | South and Central Vietnam | Medium term (2-4 years) |

| Fleet Off-Loads Drive Supply | +1.9% | Major logistics hubs | Long term (≥4 years) |

| Grey-Import Clamp-Downs Redirect Supply | +1.3% | Port cities nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Price Delta Between New and Used Cars

In Vietnam, rising import duties, currency fluctuations, higher logistics costs, and the introduction of premium features in newer car models have led to higher new-car sticker prices. Concurrently, steep depreciation during the initial three years of ownership has expanded the affordability gap between new and lightly used vehicles. For widely recognized models such as the Toyota Vios and Honda City, the price disparity between a new unit and a three-year-old model has remained substantial since 2022. This price differential enhances the attractiveness of three to five-year-old vehicles, which offer modern safety systems, advanced infotainment, and improved fuel efficiency at significantly lower purchase prices. Domestic income levels and cautious consumer spending patterns continue to anchor demand in the used-vehicle market. Fleet operators and small businesses leverage this price gap to refresh their assets without overextending their capital budgets. By opting for late-model used vehicles, buyers achieve optimized total cost of ownership while accessing relatively modern specifications. As new vehicle prices remain elevated relative to income growth, this widening price gap is expected to sustain growth in Vietnam's used-car market over the forecast period.

Growing Availability of Vehicle-Financing at Above 80% LTV

Local banks in Vietnam have increased loan-to-value ratios for used cars up to seven years old, reflecting a shift from stricter eligibility criteria observed in previous years[1]. The adoption of advanced data-driven valuation tools and partnerships with digital marketplaces has reduced underwriting risks and expedited loan approval processes. Enhanced financing coverage is driving demand among younger consumers, who prefer structured monthly repayments to upfront cash purchases. Several lenders are introducing tailored financial products for certified used vehicles, often incorporating extended warranty coverage to strengthen buyer confidence. As competition among banks and financial institutions intensifies, financing penetration is projected to rise, supporting transaction growth in the Vietnamese used car market.

Digital Marketplaces’ Expansion Into Tier-2 and Tier-3 Cities

Rising smartphone penetration and the rapid expansion of e-commerce infrastructure are enabling used-car platforms in Vietnam to expand beyond Ho Chi Minh City and Hanoi into secondary cities such as Da Nang and Can Tho. Localized mobile applications, integrated cashless payment systems, and doorstep vehicle inspection services are narrowing the information gap between urban and semi-urban markets. Sellers in smaller provinces can now access nationwide demand, improving inventory turnover and enhancing price transparency. At the same time, buyers outside major metropolitan areas gain access to a wider selection of models without the need for long-distance travel. This broader digital reach expands the total addressable market for the Vietnamese used car industry and gradually reduces dependence on informal roadside transactions.

OEM-Backed Certified-Pre-Owned Programs Ramp-Up

Automakers in Vietnam are accelerating certified used vehicle programs to compete with the fragmented independent resale market. Brands such as Toyota, Ford, and Hyundai are strengthening structured inspection protocols, verified service histories, and extended warranty coverage to justify price premiums over non-certified listings. These programs enhance transparency and reduce buyer concerns related to vehicle condition and ownership records. Some players are also integrating digital maintenance-tracking systems to improve traceability and reduce risks, such as odometer manipulation. Through certified schemes, dealers secure more reliable pipelines of lease returns and trade-ins, while OEMs deepen customer engagement and generate additional after-sales revenue. As consumer preferences shift toward greater assurance and structured transactions, certified inventory is expected to increase the business-to-consumer share in the Vietnamese used-car market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Looming Euro-5 Emissions Mandate | -2.4% | HCMC and Hanoi first | Medium term (2-4 years) |

| Low Odometer Data Transparency | -2.1% | Informal markets nationwide | Short term (≤2 years) |

| Prospective Carbon Tax on Old Vehicles | -1.9% | Urban enforcement zones | Long term (≥4 years) |

| Patchy Warranty After-Sales Ecosystem | -1.8% | Rural and tier-3 areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Looming Euro-5 Emissions Adoption for Imports (2027)

Beginning in 2027, imported light vehicles in Vietnam will be required to comply with Euro 5 emission standards, with major cities such as Hanoi and Ho Chi Minh City evaluating the possibility of stricter or earlier enforcement to address air quality concerns. Anticipation of tighter regulatory compliance has already influenced buyer sentiment, particularly toward older imported models manufactured between 2010 and 2017. As consumers factor in potential inspection hurdles and higher compliance-related costs, resale values for these older units have shown early signs of softening. Dealers carrying non-compliant inventory, therefore, face heightened depreciation risk and potential margin compression. However, the regulation is expected to reshape demand rather than contract the market overall, as buyers pivot toward three to five-year-old vehicles that meet newer emission standards. This transition supports healthier turnover of relatively modern stock and gradually improves the overall fleet composition in the Vietnamese used-car market.

Low Odometer-Data Transparency and Tampering

A significant number of consumer complaints have been lodged over vehicle-history misrepresentation, with odometer rollbacks topping the list. Independent inspection stations lack interconnected databases, leaving room for mileage fraud that erodes trust and depresses prices in higher-value segments. Marketplaces now pilot third-party verification and AI-driven photo forensics, yet loopholes persist. Until a centralized VIN registry materializes, transparency shortfalls will weigh on buyer confidence and temper the growth pace of the Vietnam used car market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: SUVs and MPVs Outpace Sedans

SUVs and MPVs accounted for 44.72% of the Vietnam used car market share in 2025, reflecting consumer preference for high ground clearance and family-oriented versatility. The Vietnam used-car market, driven by SUVs and MPVs, is projected to expand at a 14.12% CAGR through 2031, buoyed by fleet disposals from ride-hailing firms favoring utility vehicles for cabin comfort. Domestic maker VinFast captures this sentiment with tiered SUV offerings spanning entry to premium segments. Sedans retained relevance among cost-focused commuters but ceded momentum to more spacious formats.

Growing road-trip culture and investments in highway networks sustain SUV resale values, reinforcing a positive feedback loop for first-time buyers. Meanwhile, hatchbacks serve a niche market in inner-city corridors, where parking constraints dominate purchase decisions. Collectively, these trends indicate a structural tilt toward utility body styles that will continue to shape inventory availability and pricing dynamics in the Vietnam used-car industry.

By Fuel Type: Electric Momentum Builds

Although petrol cars accounted for 84.63% of the Vietnam used-car market share in 2025, battery-electric units posted the fastest clip at an 18.28% CAGR, underscoring early electrification undercurrents. VinFast delivered over 87,000 EVs in 2024 across the Vietnamese market, ensuring a sizeable future secondary inventory[2]“EV Sales Cross 87,000,” Thanh Niên Auto Desk, thanhnien.vn. The Vietnam used-car market for EVs will surge once the first-wave lease terms conclude in 2026. Diesel retains a foothold in commercial use but faces unfavorable tax treatment, prompting operators to switch to hybrid or newer petrol options to comply.

Charging infrastructure gaps persist, yet many prospective buyers are open to an EV in their next purchase. Government registration-fee waivers until 2027 keep the total cost of ownership attractive. As a result, battery-electric supply and demand trajectories will likely intersect sooner than infrastructure skeptics forecast, granting EVs an outsized influence on future Vietnam used-car market share.

By Sales Channel: Online Takes Center Stage

Online platforms accounted for 58.55% of the Vietnamese used-car market share in 2025, mirroring broader e-commerce uptake across consumer categories. The Vietnam used-car market, transacted digitally, is forecast to grow 14.45% per year through 2031 as mobile-first interfaces streamline everything from search to financing. Peer-to-peer uploads still dominate rural listings, but verified dealer storefronts within the same apps now handle financing and warranty upsells that attract urban millennials.

Offline dealers pivot toward hybrid models, offering virtual tours and test-drive delivery at the customer’s doorstep. This convergence blurs channel boundaries yet reinforces the overarching digital ethos. Ultimately, seamless online discovery, paired with structured after-sales, will remain the cornerstone of value creation across the Vietnam used-car industry.

By Vehicle Age: Younger Cars Emerge

Inventory aged 3-5 years captured 46.91% of the Vietnam used car market share in 2025, balancing affordability with modern tech features. Yet the less than 3-year cohort is on track for a 15.52% CAGR, fed by ride-hailing fleet turnover and swift consumer upgrade cycles. The Vietnam used car market share of these near-new units is expected to rise as warranty transfers and certified status lower perceived risk.

Conversely, cars older than 8 years face margin pressure from possible carbon taxation and stricter inspections. Financial institutions now price loan risk based on projected regulatory costs, tightening credit for aging units. The resulting age shift aligns Vietnam with trajectories observed in mature auto economies, where policy nudges push fleets toward younger vehicles.

By Price Band: Mid-Tier Sweet Spot Broadens

Vehicles priced between USD 7k and USD 15k held 38.74% of the Vietnam used car market share in 2025, matching middle-income budgets. The USD 15k-30k tranche is set to expand 15.86% annually, fueled by stronger financing access and aspirational demand for premium badges. Luxury cars above USD 30k stay niche yet stable, supported by high-net-worth business owners seeking prestige without new-car depreciation.

Price-band migration mirrors Vietnam’s rise in GDP per capita and evolving consumer expectations. As warranty programs lengthen and digital auctions expose previously opaque premium inventory, upward mobility within price tiers will remain central to Vietnam's used car market development.

By Vendor Type: Organized Channels Gain Ground

Unorganized vendors accounted for 68.35% of transactions in the Vietnam used-car market in 2025, reflecting a long-standing reliance on individual sellers and informal lots. Organized outlets, although smaller, are projected to log a 16.86% CAGR through 2031 as buyers increasingly favor transparency, certified inspections, and bundled warranties. Banks also prefer lending through these structured dealers, which supply reliable documentation and repossession support, thereby lowering credit risk.

Organized vendors deploy standardized 150-point checks, extended warranty packages, and digital price-discovery tools that justify premiums while nurturing repeat business. Compliance with evolving consumer-protection rules further differentiates them from informal traders who struggle to meet documentation and odometer-verification requirements. As regulatory scrutiny tightens and online platforms raise listing standards, organized channels are set to capture incremental market share in Vietnam's used-car market, carving durable moats against lower-overhead but lower-trust independents.

By Mileage: Low-Mileage Premium Expands

Cars driven between 20,001 km and 50,000 km accounted for 47.56% of 2025 turnover, offering buyers a sweet spot of manageable depreciation and proven reliability. Yet vehicles showing below 20,000 km on the odometer are expected to rise at a 16.41% CAGR, buoyed by corporate fleet replacements and early adopters upgrading quickly for the latest tech.

Lease returns supply a steady pipeline of low-mileage inventory complete with digital service logs, making them attractive to lenders and warranty providers. As financing spreads and residual-value protection gains weight in purchase decisions, high-mileage units face diminishing appeal. Digital marketplaces now spotlight verified mileage badges, enhancing transparency in the Vietnam used-car market and steering demand toward low-wear vehicles that promise lower long-term ownership costs.

Geography Analysis

South Vietnam remains the largest pocket of demand with 48.20% share, underpinned by Ho Chi Minh City’s robust economic output, mature financing channels, and extensive service infrastructure. Port access eases inbound flows for new imports and dealer trade-ins, ensuring consistent inventory turnover. The region’s dense population and urban lifestyles fuel appetite for compact crossovers and certified sedans, sustaining liquidity across price points.

Central Vietnam shows the fastest trajectory at 15.16% CAGR. Government-backed industrial parks widen employment and lift disposable income in Da Nang, Hue, and Vinh. New expressways shorten delivery timelines, encouraging dealers to set up satellite lots. Smartphone penetration supports online browsing, giving buyers transparent price benchmarks previously available only in HCMC or Hanoi listings.

North Vietnam delivers steady volumes hinged on Hanoi’s administrative and corporate fleets. Earlier rollouts of emission-testing regimes have prompted accelerated replacement of aging government sedans with Euro-5-compliant units. Cross-border logistics with China also feed vehicle demand, although stricter customs oversight narrows grey-import arbitrage. These regional currents fortify nationwide resilience in the Vietnamese used car market.

Competitive Landscape

Competition spans digital platforms, franchise dealerships, and small independents. Oto.com and Chợ Tốt Xe rank among the top websites by web traffic due to AI-based price suggestions and escrow payment options that reduce transaction friction[3]. Toyota-affiliated dealers counter with nationwide certified lots and 10-year powertrain warranties that reduce residual-value anxiety. VinFast Automalls, meanwhile, blend online configurators with 4,000 m² urban showrooms to showcase trade-ins with warranty-rich terms.

Strategic moves in 2024-2025 illustrate escalating stakes. Ford Vietnam extended certified coverage to a decade for gasoline models, boosting dealer footfall and service revenue. VinFast exited specific taxi-fleet contracts to preserve resale values on consumer channels, thereby tightening near-new supply and defending brand equity. Start-ups like Vietwheels entered the scene with curated multi-brand listings and comparison engines, signaling ongoing fragmentation yet higher overall professionalism.

Technology is the new battleground. Blockchain-backed maintenance logs, 360-degree inspection kiosks, and instant loan-approval APIs redefine user expectations. Scale players invest in tier-2 city rollouts to capture incremental demand, while independents forge alliances for shared logistics and warranty pools. As transparency and convenience converge, the Vietnamese used-car market tilts toward players able to merge digital reach with tangible after-sales support.

Vietnam Used Car Industry Leaders

Oto.com.vn

Chợ Tốt Xe

Bonbanh.com

Carmudi Vietnam

Viet Han Used Cars

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Vucar, an AI-driven platform, is set to revolutionize car transactions in Vietnam, emphasizing cutting-edge technology, transparency, and innovation.

- February 2025: In 2025, government incentives supporting the purchase of new vehicles and electric cars began influencing Vietnam’s pre-owned vehicle market. Policies such as tax incentives and reduced registration fees for domestically manufactured vehicles make new cars more financially attractive, potentially diverting demand from used vehicles.

Vietnam Used Car Market Report Scope

A used car, also known as a pre-owned or secondhand car, is a vehicle that has had one or more previous retail owners. These cars can be purchased from various sources, including franchise and independent car dealerships, rental car companies, buy-here-pay-here dealerships, leasing offices, auctions, and private party sales.

The Vietnamese used car market is segmented by vehicle type, fuel type, booking type, and vehicle age. By vehicle type, the market is segmented into hatchbacks, sedans, sports utility vehicles (SUVs), and multi-purpose vehicles (MPVs). By fuel type, the market is segmented into ICE and electric. By booking type, the market is segmented into online and offline. By vehicle age, the market is segmented into up to 5 years and above 5 years. For each segment, market sizing and forecast have been done based on value (USD).

By Vehicle Type

| Hatchback |

| Sedan |

| SUV and MPV |

By Fuel Type

| Gasoline |

| Diesel |

| Hybrid |

| Battery Electric |

| Other Alternative Fuels |

By Sales Channel

| Online Marketplace |

| Certified Offline Dealership |

By Vehicle Age

| Less than 3 Years |

| 3-5 Years |

| 5-8 Years |

| Above 8 Years |

By Price Band

| Below USD 7 k |

| USD 7-15 k |

| USD 15-30 k |

| Above USD 30 k |

By Vendor Type

| Organized |

| Unorganized |

By Mileage

| Below 20,000 km |

| 20,001-50,000 km |

| Above 50,000 km |

By Region

| North Vietnam |

| Central Vietnam |

| South Vietnam |

| By Vehicle Type | Hatchback |

| Sedan | |

| SUV and MPV | |

| By Fuel Type | Gasoline |

| Diesel | |

| Hybrid | |

| Battery Electric | |

| Other Alternative Fuels | |

| By Sales Channel | Online Marketplace |

| Certified Offline Dealership | |

| By Vehicle Age | Less than 3 Years |

| 3-5 Years | |

| 5-8 Years | |

| Above 8 Years | |

| By Price Band | Below USD 7 k |

| USD 7-15 k | |

| USD 15-30 k | |

| Above USD 30 k | |

| By Vendor Type | Organized |

| Unorganized | |

| By Mileage | Below 20,000 km |

| 20,001-50,000 km | |

| Above 50,000 km | |

| By Region | North Vietnam |

| Central Vietnam | |

| South Vietnam |

Key Questions Answered in the Report

How large is the Vietnam used car market in 2026?

The Vietnam used car market size is USD 13.2 billion in 2026.

What CAGR is expected for used-car sales through 2031?

Sales are projected to expand at a 13.76% CAGR during 2026-2031.

Which vehicle type dominates resale activity?

SUVs and MPVs held 44.72% of 2025 transactions, the highest among body styles.

Are electric used cars becoming popular?

Yes, battery electric units are forecast to grow at an 18.28% CAGR as VinFast lease returns enter the secondary market and government fee waivers remain in place.

Page last updated on: