Vietnam Electric Vehicle Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

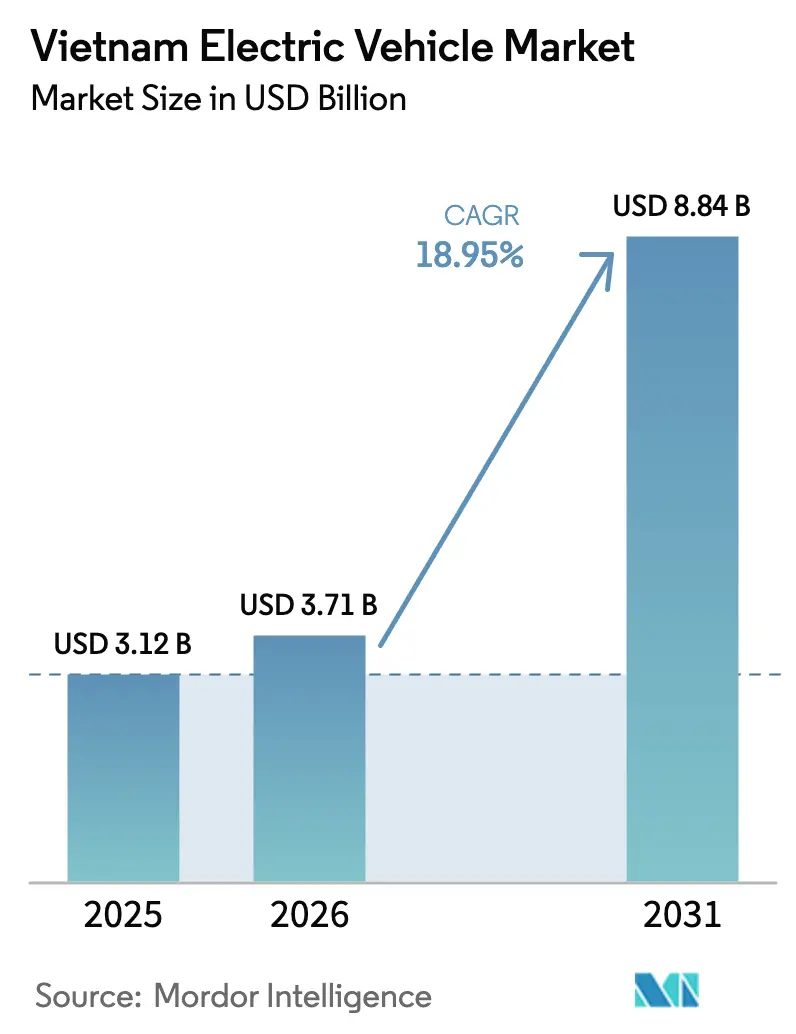

| Base Year Market Size (2025) | USD 3.12 Billion |

| Market Size (2026) | USD 3.71 Billion |

| Market Size (2031) | USD 8.84 Billion |

| Growth Rate (2026 - 2031) | 18.95% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vietnam Electric Vehicle Market Analysis by Mordor Intelligence

The Vietnam electric vehicle market size in 2026 is estimated at USD 3.71 billion, growing from 2025 value of USD 3.12 billion with 2031 projections showing USD 8.84 billion, growing at 18.95% CAGR over 2026-2031. Demand is propelled by firm government targets that mandate 50% EV penetration in urban areas by 2030 and net-zero emissions by 2050[1]Hang Nguyen Thanh, "Viet Nam Accelerates Plans to Phase Out Fossil Fuel Vehicles by 2050", Changing Transport, changing-transport.org. VinFast’s localization drive, foreign OEM factory commitments, and preferential electricity tariffs collectively reduce the total cost of ownership, amplifying adoption. Rapid two-wheeler electrification creates consumer familiarity and shared charging infrastructure that spills over to four-wheelers, while falling battery pack prices allow LFP technology to dominate value-conscious segments. Competition remains moderate because VinFast’s dominance deters price wars, yet Chinese brands and global mass-market OEMs are entering with cost-competitive models, nudging the ecosystem toward wider model variety and lower pricing.

Key Report Takeaways

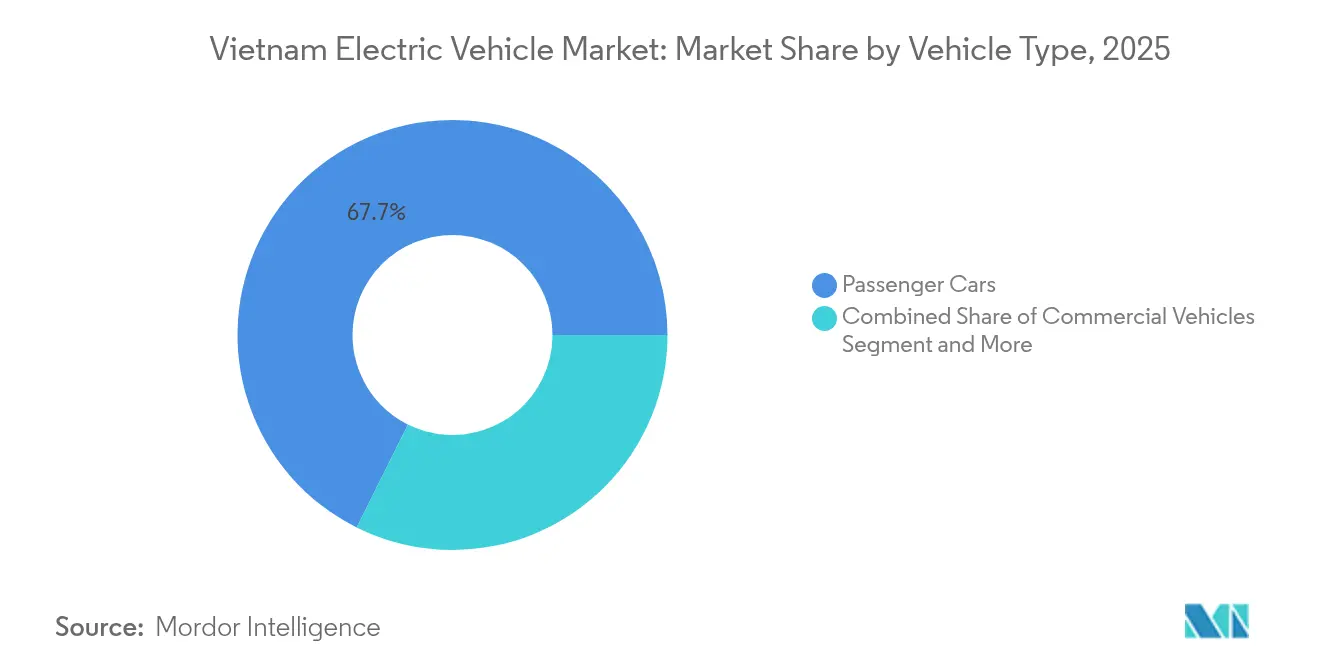

- By vehicle type, passenger cars led with 67.65% revenue share in 2025, whereas buses are forecast to expand at a 33.11% CAGR through 2031.

- By propulsion, battery electric vehicles held 70.82% of the Vietnam electric vehicle market share in 2025 and are projected to grow at 27.85% CAGR to 2031.

- By driving range, below-200 km models accounted for 53.72% share of the Vietnam electric vehicle market size in 2025; above-400 km models show the highest 29.10% CAGR to 2031.

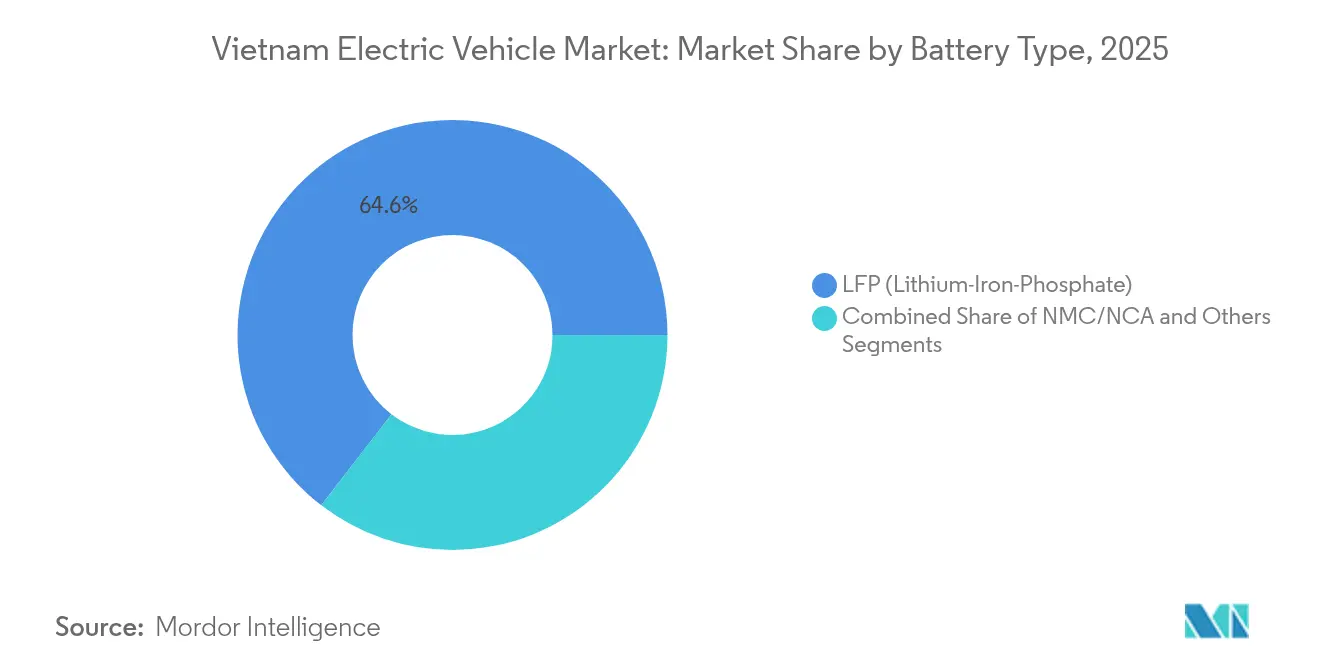

- By battery type, LFP technology captured 64.55% share in 2025, while solid-state batteries post the fastest 36.50% CAGR through 2031.

- By end user, private ownership commanded 77.55% revenue in 2025; commercial fleet and ride-hailing is the quickest-expanding group at 31.10% CAGR to 2031.

- By region, Southern Vietnam retained 45.21% revenue share in 2025; Northern Vietnam is advancing at a 28.40% CAGR, the swiftest nationwide.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Electric Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Domestic Manufacturing Scale-Up | +4.8% | Southern Vietnam, Northern Vietnam industrial zones | Medium term (2-4 years) |

| Government Incentives and Tax Rebates | +4.2% | All provinces with registration fee exemptions | Short term (≤ 2 years) |

| Rising Environmental Awareness and Net-Zero Targets | +3.3% | Urban centers in Ho Chi Minh City, Hanoi, Da Nang | Long term (≥ 4 years) |

| Electric Two-Wheeler Ecosystem Spill-Over | +2.9% | Ho Chi Minh City, Hanoi metropolitan areas | Medium term (2-4 years) |

| Falling Battery Pack Prices | +2.1% | Manufacturing hubs in Northern Vietnam, Central Vietnam | Medium term (2-4 years) |

| Preferential EV-Charging Tariff Structure | +1.3% | All provinces with established charging infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Domestic Manufacturing Scale-up

VinFast aims for 80% domestic content by 2026, with a goal to produce 500,000 vehicles by 2027 and reach 1 million vehicles annually by 2030, a scale that compresses component costs and mitigates exchange-rate exposure. Complementary commitments from Chery and Geely reinforce Vietnam’s standing as a regional assembly hub, yet sophisticated electronics and battery management systems remain import-reliant. Guaranteed offtake contracts from VinFast give local suppliers demand visibility, prompting new capital investment that accelerates localisation.

Government Incentives and Tax Rebates

The incentive package waives registration fees for EVs until February 2027 and keeps import duties at zero on ASEAN-built cars, trimming purchase prices by more than VND 100 million per unit. Preferential charging tariffs of 2,204 VND/kWh further tilt the total cost of ownership in favor of electric models. Provincial add-ons, such as Ho Chi Minh City’s proposed tax holidays and soft loans for its 400,000-unit motorcycle conversion program, underscore multi-tier policy coordination[2]"HCMC wants only electric motorbikes for ride-hailing by 2030", VnExpress, e.vnexpress.net. Continuity beyond 2027 depends on reaching cost parity, exposing the market to fiscal-policy rollover risk.

Rising Environmental Awareness and Net-zero Targets

Vietnam’s 2050 net-zero pledge instituted binding milestones: all new urban buses must be green by 2025 and 50% of urban vehicles electric by 2030, creating regulatory demand that bypasses discretionary consumer choice. Worsening air-quality indices in Ho Chi Minh City and Hanoi galvanize public opinion, particularly among 25-44-year-olds who exhibit higher EV preference. Further, fuel-import savings projections by 2050 offer fiscal validation for the aggressive roadmap.

Electric Two-wheeler Ecosystem Spill-over

Surging sales of electric motorcycles are expanding charging-port density to over 150,000 nationwide, ports that service both bikes and cars. The ease of battery-swap familiarity and positive user experience shorten four-wheeler adoption cycles. Ho Chi Minh City’s ride-hailing initiative, converting 400,000 motorcycles by 2026, creates a living advertisement for electric mobility, shrinking skepticism and accelerating cross-segment diffusion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sparse Public Charging Infrastructure | -4.2% | Rural provinces, Central Vietnam coastal areas | Medium term (2-4 years) |

| High Up-Front Vehicle Cost Vs Average Income | -3.1% | Lower-income provinces, rural Northern Vietnam | Short term (≤ 2 years) |

| Limited Mid-Range Model Availability | -2.4% | All provinces with limited dealer networks | Short term (≤ 2 years) |

| Grid Capacity Constraints at Peak Hours | -1.8% | Northern Vietnam industrial zones, Southern Vietnam urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sparse Public Charging Infrastructure

Although dense in tier-one cities, the network thins rapidly in rural corridors, restricting inter-city travel and segment growth beyond sub-200 km models. V-Green has earmarked USD 404 million to deploy additional stations, yet lead times mean near-term bottlenecks persist. Grid stress surfaces during high-demand months, prompting government directives that prioritize power supply resilience.

High Up-front Vehicle Cost vs Average Income

VinFast’s VF3, priced at USD 9,200, remains aspirational for large swathes of the population despite fee waivers and battery-subscription schemes. The affordability gap concentrates adoption among upper-middle-income urbanites, limiting economies of scale. Wider domestic parts localisation and LFP battery dominance are expected to narrow the gap, but meaningful mass-market access still hinges on sustained subsidy frameworks or breakthrough cost declines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Drive Electrification

Passenger cars contributed 67.65% of overall revenue in 2025, while buses registered the quickest expansion at a 33.11% CAGR. The Vietnam electric vehicle market size for buses is projected to double between 2025 and 2028 as provincial mandates trigger large tender volumes. Private car buyers account for much of today’s stock, yet commercial fleets tip the growth curve; Ho Chi Minh City’s 37-route electric bus roll-out and Hanoi’s 100% core-area bus electrification agenda inject predictable bulk demand.

Intense fleet utilisation magnifies total-cost benefits, making commercial buyers early adopters of newer battery chemistries and fast-charging solutions. Conversely, two-wheelers retain vitality through rural-urban commuter demand, indirectly bolstering charging-hub economics that benefit four-wheeler deployment. Over the forecast horizon, passenger-car share will erode modestly even as volumes rise, because buses and vans gain policy-driven ground in public transit and last-mile logistics.

By Propulsion: Battery Electric Dominance

Battery electric vehicles captured 70.82% of the Vietnam electric vehicle market share in 2025, eclipsing hybrid and plug-in alternatives. That dominance deepens as BEV volumes compound at 27.85% CAGR, propelled by a government strategy that leapfrogs transitional powertrains. Hybrids hold niche appeal for peri-urban commuters needing range flexibility, but a lack of tax parity with BEVs caps growth. Fuel-cell vehicles remain experimental due to infrastructure voids.

VinFast’s single-minded BEV product map shapes consumer perception, while nationwide charging subsidies reinforce the pure-electric narrative. Foreign OEMs may inject plug-in variants to hedge range anxiety, yet policy signals keep BEVs on the mainstream trajectory. In tandem, battery advancements shorten charging times, shaving practical limitations that once justified hybrid premiums. Altogether, the Vietnam electric vehicle industry stays on a direct-to-BEV path, avoiding the incremental hybrid detour seen in developed markets.

By Driving Range: Urban-Optimised Solutions Lead

Sub-200 km models occupied 53.72% of 2025 shipments because urban mobility dominates daily travel. Nonetheless, the long-range (over 400 km) sub-segment outpaces all peers at 29.10% CAGR, its gains contingent on highway-corridor charger build-out.

CATL’s announced 1,500 km pack with five-minute top-ups, illustrates technological headroom, but cost parity remains the swing factor. Mainstream buyers will continue opting for practical urban ranges while using public transport or rental alternatives for longer journeys. Over time, rising living standards and inter-city business travel will feed demand for mid- and long-range variants, diversifying OEM line-ups.

By Battery Type: LFP Technology Leads Cost Optimisation

LFP chemistry governed 64.55% sales in 2025 and will retain the majority share owing to raw-material cost advantages and benign thermal properties. In value models, safety credentials and lifecycle longevity outshine modest energy-density trade-offs. Solid-state batteries, currently negligible, are forecast to grow 36.50% CAGR as VinFast and technology partner ProLogium finalise pilot production lines.

NMC and NCA chemistries linger in high-performance and export-oriented trims, but relative cost pressure makes them less viable domestically. Government recycling guidelines in progress will also influence chemistry choice by capping end-of-life liabilities, favouring solutions with established reuse channels. Battery diversification thus follows a cost-to-performance spectrum where LFP remains the mass-volume backbone.

By End User: Private Ownership Drives Market Growth

Private buyers delivered 77.55% of the 2025 volume, underscoring Vietnam’s personal-mobility culture. Yet commercial fleet orders post a compelling 31.10% CAGR as service operators chase fuel and maintenance savings. Government and public transport maintain steady growth through policy mandates requiring electric bus transitions across provincial networks.

Household demand benefits from the well-trodden path of motorcycle electrification: familiarity with home charging and battery leases lowers psychological barriers. Government fleet procurement, though smaller, wields outsized signalling power, ensuring model diversity via bulk tenders. Over the outlook period, a gradually narrowing price gap and greater financing options will keep private buyers atop volume rankings even as fleet adoption accelerates.

Geography Analysis

Southern Vietnam’s dominates with 45.21% Vietnam electric vehicle market share due to springs from economic heft and proactive city governance. The 37-route electric bus launch in July 2025 alone adds 256 zero-emission buses and signals a multi-modal commitment. High urban density maximises fleet utilisation, providing strong payback periods even at today’s tariff levels. Power-supply challenges persist during summer peaks, prompting coordinated generation and demand-response plans to safeguard reliability.

Northern Vietnam benefits from geographic proximity to component supply chains and concerted efforts to foster an EV-industry cluster allowing to grow at 28.40% CAGR by 2031. Factory investments by VinFast and foreign OEMs scale the region’s output while seeding localised tier-2 supplier networks. Hanoi’s target of 100% electric buses in central districts by 2030 generates predictable order books, stimulating ancillary investments in depots and fast-charging hubs. Yet cold-weather battery-range degradation and peak-load pressures require technology adaptations and grid reinforcement.

Central Vietnam leverages its tourism orientation to experiment with niche deployments such as coastal shuttle fleets and airport circulators. Policy innovations include interest-rate subsidies for operators purchasing electric coaches servicing heritage sites. While volumes remain modest, the region acts as a proving ground for renewable-energy-linked charging clusters that integrate solar and wind capacity, potentially exporting this template nationwide.

Competitive Landscape

VinFast’s vertically integrated model covers production, charging (via V-Green), and mobility services (Xanh SM), sustaining a market share that confers economies of scale and brand ubiquity. Its domestic focus yields agility in adapting products to local tastes, such as compact VF3s tailored for first-time buyers. Hyundai and Toyota deploy hybrid portfolios to hedge policy shifts but currently lack comparable charging ecosystems.

Strategic activity centres on capacity additions and network alliances. VinFast’s battery-supplier conference in April 2025 locked in long-term offtake agreements, de-risking raw-material volatility. Foreign OEMs balance local content mandates with global platform sharing to preserve margins. Infrastructure spend acts as the new battleground: V-Green’s 42-point fast-charge hub in Hanoi raises the bar, pushing rivals to co-invest in interoperable standards. Software ecosystems remain nascent; telematics and OTA updates offer differentiators but have not yet influenced buyer decisions as strongly as price and charging convenience.

Market entry barriers remain moderate. While license requirements are transparent, achieving a charge-point footprint and financing consumer credit portfolios pose new-entrant hurdles. Local-content incentives tilt in favour of early movers that have domestic supplier networks. Over the medium term, intensified competition is expected once factory build-outs by global brands come online, placing downward pressure on prices and accelerating technology migration.

Vietnam Electric Vehicle Industry Leaders

-

Vinfast Auto Ltd.

-

Hyundai Motor Company

-

SAIC–GM–Wuling Automobile Co., Ltd.

-

Toyota Motor Corporation

-

BYD Auto Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: V-Green inaugurated Hanoi’s largest fast-charging station with 42 points, capable of serving 84 vehicles concurrently, reinforcing capital-city network density.

- March 2025: VinFast introduced the VF3 mini-EV at USD 9,200, targeting annual domestic sales of 20,000 units and expansion toward regional export markets.

- March 2025: Start-up Move committed USD 13 million to build 120,000 affordable EVs per year, targeting underserved budgets with 150-200 km-range models.

Vietnam Electric Vehicle Market Report Scope

An electric vehicle is powered by one or more electric motors that use energy stored in batteries. It doesn't rely on any liquid fuel components or have a tailpipe. \

The Vietnamese electric vehicle market is segmented by vehicle type and propulsion. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By propulsion, the market is segmented into battery electric vehicles, plug-in hybrid electric vehicles, hybrid electric vehicles, and fuel cell electric vehicles. For each segment, the market sizing and forecast have been done based on the value (USD).

| Passenger Cars |

| Commercial Vehicles |

| Two-Wheelers |

| Buses |

| Battery Electric Vehicles (BEV) |

| Plug-in Hybrid Electric Vehicles (PHEV) |

| Hybrid Electric Vehicles (HEV) |

| Fuel-Cell Electric Vehicles (FCEV) |

| Below 200 km |

| 200 to 400 km |

| Above 400 km |

| LFP |

| NMC/NCA |

| Others |

| Private Ownership |

| Commercial Fleet/Ride-Hailing |

| Government and Public Transport |

| Northern Vietnam |

| Central Vietnam |

| Southern Vietnam |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| Two-Wheelers | |

| Buses | |

| By Propulsion | Battery Electric Vehicles (BEV) |

| Plug-in Hybrid Electric Vehicles (PHEV) | |

| Hybrid Electric Vehicles (HEV) | |

| Fuel-Cell Electric Vehicles (FCEV) | |

| By Driving Range | Below 200 km |

| 200 to 400 km | |

| Above 400 km | |

| By Battery Type | LFP |

| NMC/NCA | |

| Others | |

| By End User | Private Ownership |

| Commercial Fleet/Ride-Hailing | |

| Government and Public Transport | |

| By Region | Northern Vietnam |

| Central Vietnam | |

| Southern Vietnam |

Key Questions Answered in the Report

What is the current size of the Vietnam electric vehicle market?

The market stands at USD 3.71 billion in 2026 and is forecast to reach USD 8.84 billion by 2031.

Which segment is growing the fastest?

Buses exhibit the highest growth, advancing at a 33.11% CAGR as provincial mandates drive public-transport electrification.

Why do battery electric vehicles dominate Vietnam’s propulsion mix?

Government incentives focus on pure electric models, and VinFast’s BEV-only line-up makes them readily available and cost-competitive versus hybrids.

How is charging infrastructure keeping pace with demand?

Urban fast-charging hubs are expanding quickly—Hanoi’s new 42-point station exemplifies high-capacity roll-outs—yet rural corridors still face coverage gaps.

What is the biggest barrier to wider EV adoption?

High upfront purchase costs relative to average income remain a chief obstacle despite fee waivers and battery-lease programs.

Which regions lead EV adoption?

Southern Vietnam holds the largest share in 2025 at 45.21% owing to Ho Chi Minh City’s initiatives, while Northern Vietnam is growing fastest at a 28.40% CAGR through 2031 thanks to industrial investment and supportive local policies.

Page last updated on: