Vietnam Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

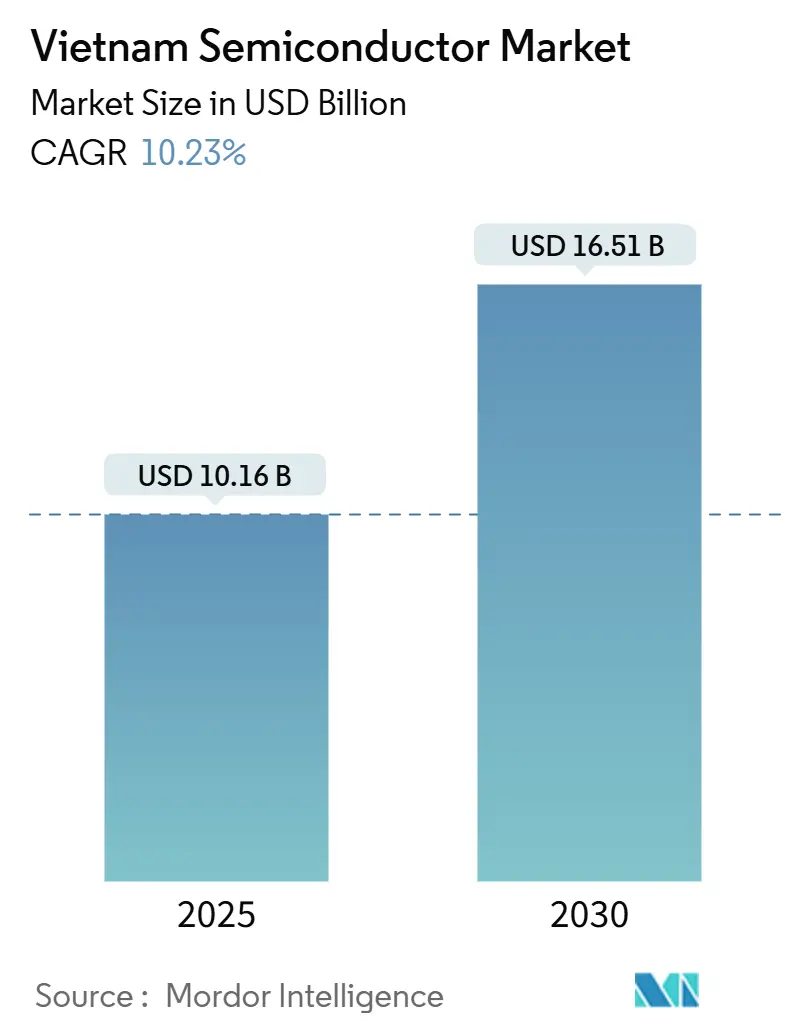

| Market Size (2025) | USD 10.16 Billion |

| Market Size (2030) | USD 16.51 Billion |

| Growth Rate (2025 - 2030) | 10.23% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Semiconductor Market Analysis by Mordor Intelligence

Vietnam semiconductor market size stands at USD 10.16 billion in 2025 and is forecast to reach USD 16.51 billion by 2030, progressing at a 10.23% CAGR. This robust trajectory positions the Vietnam semiconductor market as the pivotal alternative manufacturing hub for companies recalibrating China-centric supply chains. Foreign direct investment from Intel, Samsung, and Amkor anchors advanced assembly and test capacity, while rising demand from smartphones, IoT, and AI applications sustains long-term volume growth. Government incentives under the National Semiconductor Strategy 2024-2030 and preferential trade ties with the United States further accelerate localization across device packaging and design. Persistent upstream gaps such as reliance on imported ultra-high-purity gases remain, yet rare-earth mineral reserves create a strategic hedge that few competitors can match.[1]Community Intel, “Get to Know Intel Sites: Vietnam,” Intel, intel.com

Key Report Takeaways

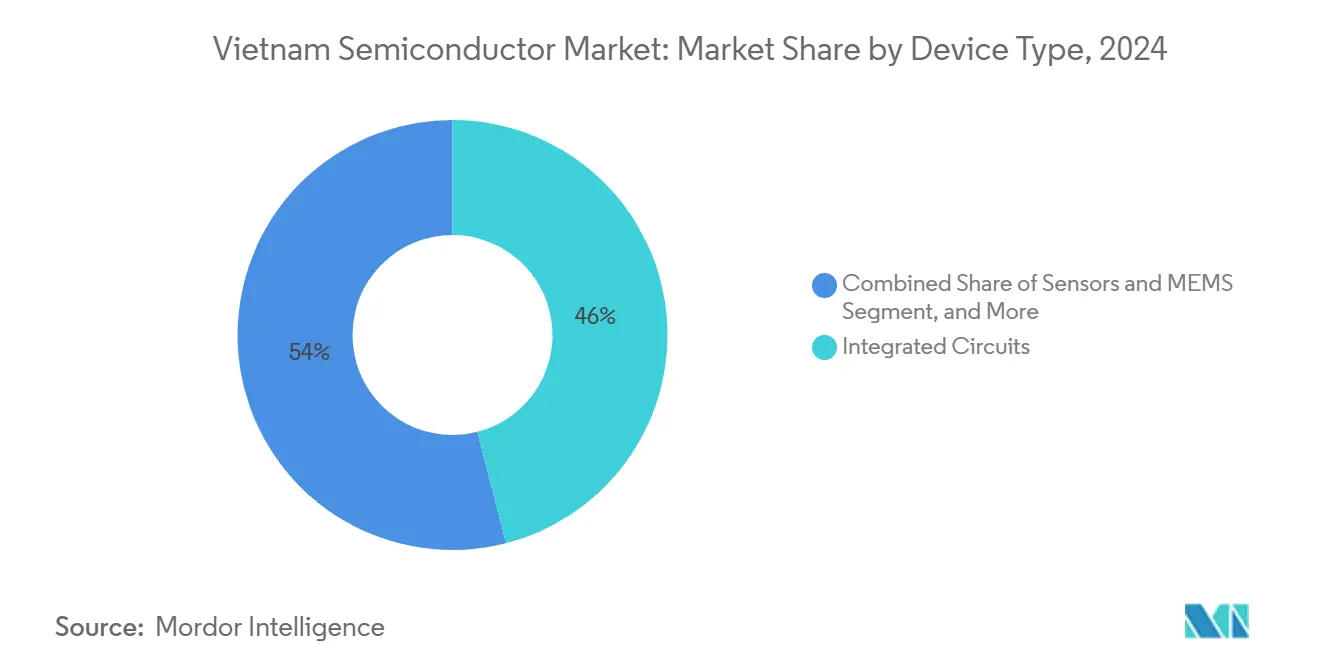

- By device type, integrated circuits led with 46% revenue share in 2024; sensors and MEMS are projected to advance at a 13.21% CAGR through 2030.

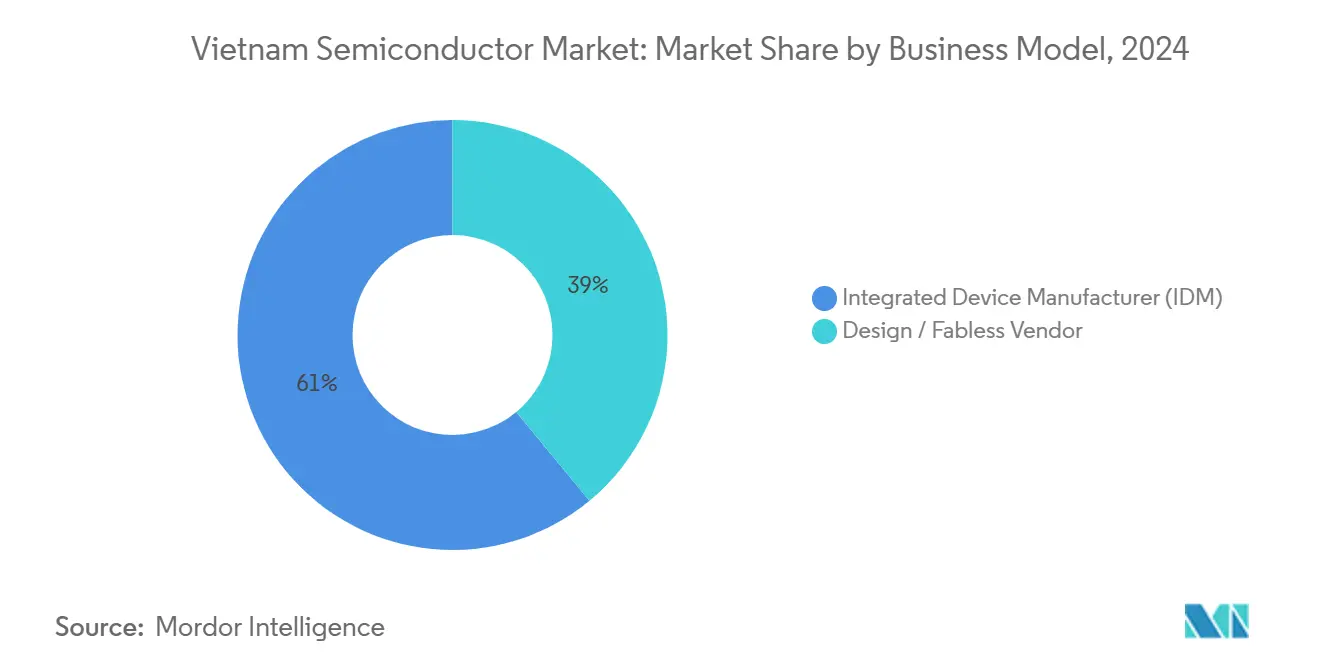

- By business model, IDM operations held 61% of the Vietnam semiconductor market size in 2024; the fabless segment is forecast to expand at a 12.88% CAGR to 2030.

- By end-user industry, communication applications captured 29% share of the Vietnam semiconductor market size in 2024; artificial intelligence applications are set to grow at a 13.89% CAGR over the same horizon.

Vietnam Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising FDI from Intel, Samsung and Amkor facilities | +2.10% | Northern Vietnam (Bac Ninh, Thai Nguyen) | Medium term (2-4 years) |

| Government "National Semiconductor Strategy 2024-2030" tax incentives | +1.80% | National, concentrated in Ho Chi Minh City, Hanoi | Long term (≥ 4 years) |

| Expansion of Vietnam's electronics export base (smartphones/IoT) | +1.50% | Global export markets, primarily US and EU | Short term (≤ 2 years) |

| Rare-earth mineral deposits enabling local upstream materials | +1.20% | Northern provinces with mining operations | Long term (≥ 4 years) |

| 1,000 imported chip-IP licences lowering design entry barriers | +0.90% | National, with concentration in tech hubs | Medium term (2-4 years) |

| Public-private talent pipeline (50,000 engineers by 2030) | +1.40% | National, early gains in Ho Chi Minh City, Hanoi, Da Nang | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising FDI from Intel, Samsung and Amkor Facilities

Large-scale investments by Intel, Samsung and Amkor deliver advanced System-in-Package capacity and create regional centers for next-generation packaging essential for AI and 5G devices. Intel’s site processes one-half of the company’s global packaging and test volume. Samsung’s continued USD 1 billion annual outlay and Amkor’s USD 1.6 billion Bac Ninh plant add scale and technology transfer that elevate the Vietnam semiconductor market in value-chain sophistication.[2]“Amkor’s Newest Factory Set to Open in Vietnam,” Amkor Technology, amkor.com Spillover effects include supplier localization and workforce upskilling across northern industrial zones.

Government “National Semiconductor Strategy 2024-2030” Tax Incentives

The government grants four years of full income-tax exemption followed by a nine-year 50% rate, yielding a fiscal edge over regional peers.[3]“Toàn văn Nghị định 205/2025-NĐ-CP sửa đổi…,” Government of Vietnam, chinhphu.vn A steering committee chaired by the Prime Minister coordinates ministries to ensure coherent policy delivery that anchors long-horizon investments. Ambitions go beyond assembly to embrace design and eventual fabrication, reinforcing the Vietnam semiconductor industry’s path up the value curve.

Expansion of Vietnam’s Electronics Export Base

Electronics exports reached USD 142 billion in 2023, locking in downstream demand for chips used in smartphones, IoT sensors and 5G infrastructure. Samsung’s smartphone output and MediaTek’s “Make in Vietnam” Wi-Fi 6/7 chipset program illustrate the virtuous feedback loop between contract manufacturing and domestic chip design. A larger export platform protects fab utilization rates and justifies continued capital inflows.

Rare-Earth Mineral Deposits Enabling Local Upstream Materials

Vietnam holds the world’s second-largest rare-earth reserves, giving the Vietnam semiconductor market a unique upstream hedge as the United States prioritizes critical-material security. Government plans to develop sustainable mining and processing link directly to semiconductor chemical inputs, differentiating the country from Malaysia and Thailand where comparable reserves are absent.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Absence of sub-28 nm wafer fabs in-country | -1.70% | National, affecting advanced node production | Long term (≥ 4 years) |

| Engineer shortfall versus annual demand | -1.30% | National, acute in Ho Chi Minh City and Hanoi | Short term (≤ 2 years) |

| Grid-instability risks for power-hungry fabs in South and Central VN | -0.80% | Southern and Central Vietnam | Medium term (2-4 years) |

| Dependence on imported ultra-high-purity gases and chemicals | -0.60% | National, affecting all manufacturing operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Absence of Sub-28 nm Wafer Fabs in-Country

Vietnam lacks advanced-node fabs, leaving high-margin AI processors and leading-edge mobile chips dependent on imports. Capital intensity upward of USD 10 billion and acute utility needs hinder local buildouts. Without sub-28 nm capability, the Vietnam semiconductor market forfeits the highest value pool in the supply chain, although government-brokered partnerships with Taiwanese foundries could bridge this gap over a longer horizon.

Engineer Shortfall Versus Demand

Current engineering output meets roughly 40-50% of the 150,000 annual requirement, forcing firms to import talent or slow expansion. Salary inflation erodes labour-cost advantages, particularly in design where Vietnam currently employs about 7,000 engineers, well below Taiwan’s bench strength. Accelerated academic programs are ramping but will take several cycles to close the gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated Circuits Anchor Advanced Packaging Scale

Integrated circuits held 46% of the Vietnam semiconductor market share in 2024, underscoring their central role in sustaining assembly and test volumes. Intel, Samsung and Amkor specialize in advanced wafer-level fan-out and SiP technologies, aligning with surging demand for AI accelerators and 5G RF modules. Sensors and MEMS, although a smaller slice, post the highest segment CAGR at 13.21% as automotive and IoT adoption climbs. The upcoming USD 1.8 billion Da Nang fab-lab will raise total Vietnam semiconductor market size for integrated-circuit packaging capacity by an additional 10 million units annually, alleviating global bottlenecks in advanced module production.

Vietnam’s discrete power devices and optoelectronics maintain stable demand from handset and LED lighting lines, while niche analog-to-digital converters such as CT Group’s CTDA200M show accelerated design cycle compression. Access to 1,000 imported IP blocks further shortens verification loops, raising design wins among local fabless outfits.

By Business Model: IDM Footprint Provides Production Backbone

IDM operations accounted for 61% of Vietnam semiconductor market size in 2024 on the back of Intel’s end-to-end packaging portfolio and Samsung’s vertically integrated memory and logic stack. This dominance guarantees predictable capacity utilization and guides supplier clustering in northern provinces, cutting logistics cost. The fabless model is nevertheless the fastest growing at 12.88% CAGR, led by FPT Semiconductor, Viettel High Tech and Marvell’s forthcoming Ho Chi Minh City design hub. Government incentives to waive IP import duties and streamline IC tape-out approvals further tilt new entrants toward fabless economics, foreshadowing a more balanced structure by 2030.

Fab-light strategies gain traction as local firms outsource wafer production to Taiwan while retaining verification and packaging in-country. This hybrid approach limits capital exposure and elevates local value capture, consistent with National Strategy goals.

By End-User Industry: Communication Base Spurs AI Momentum

Communication devices, chiefly smartphones and telecom base-stations commanded 29% share of Vietnam semiconductor market size in 2024. Samsung’s multi-plant complex remains the world’s second-largest handset producer and thus a steady consumer of PMICs, RF front ends and image sensors. Artificial intelligence workloads represent the swiftest expansion at 13.89% CAGR, driven by packaging demand for high-bandwidth memory and chiplets tailored to data-center inference. FPT’s AI R&D center in Da Nang and VinAI’s edge-AI collaborations with Qualcomm illustrate how the Vietnam semiconductor market now influences not just follows emerging compute architectures.

Automotive electronics gains steam as VinFast’s EV roadmap matures and Tier-1 suppliers localize ADAS modules. Consumer electronics, industrial automation and government security projects round out diversified demand, buffering cyclical swings in any single vertical.

Geography Analysis

Northern Vietnam anchors large-scale production. Bac Ninh hosts Amkor’s flagship 200,000 m² SiP plant and Samsung’s memory line, while Thai Nguyen packs smartphones and ICs for export. Together these provinces account for an estimated 65% of Vietnam semiconductor market size in assembly and packaging output. Ho Chi Minh City leads design and software integration with over 50 fabless entities and multinational R&D centers. Marvell’s expansion and FPT’s chip-design academies make the southern hub the prime talent magnet.

Da Nang forms a nascent third pole centered on the USD 1.8 billion advanced packaging fab lab. Central placement shortens logistics between north-south supply lines and relieves concentration risk. Infrastructure programs such as Long Thanh airport and power-grid upgrades increase resilience critical for power-intensive process flows. Free-trade pacts with the United States, Japan and South Korea widen market access and streamline dual-use technology approvals.

Competition from Malaysia and Singapore remains intense, yet the Vietnam semiconductor market maintains a labour-cost discount coupled with deep electronics manufacturing ecosystems. Decree 205/2025 further eases land-lease and customs procedures, speeding line qualification and equipment imports. These structural advantages drive the projected 10.23% CAGR despite external headwinds.[4]“Will American ‘giant’ Marvell open the world’s leading semiconductor design center in Tan Thuan EPZ?” Tan Thuan Corporation, tanthuan.com.vn

Competitive Landscape

Roughly 50 design companies and 15 packaging houses create a moderately concentrated field. Intel, Samsung and Amkor dominate high-volume production, while local champions such as FPT Semiconductor, Viettel High Tech and VNPT Technology expand into PMICs, RF transceivers and LED drivers. Vertical integration emerges as a common theme. FPT’s “FPT Chip Inside” ecosystem bundles IP, training and software support, encouraging domestic OEMs to specify local dies. MediaTek’s joint lab with Viettel and FPT enables co-tape-outs on Wi-Fi 7 chipsets, an early sign of co-creation models.

Technology leadership centers on advanced fan-out packaging, chiplet interposers and AI-infused EDA tools. The acquisition of large-scale ARM and Cadence licenses accelerates verification cycles, narrowing the gap with Taiwan design houses. Quality compliance to ISO 26262 and emerging AI governance standards becomes a differentiator as automotive and defense customers demand traceable design provenance.

While engineer shortages and imported material reliance cap upside in the near term, substantial committed capital exceeding USD 4 billion signals that strategic investors view Vietnam as a durable node in global supply-chain diversification plans.

Vietnam Semiconductor Industry Leaders

Samsung Electronics Vietnam Thai Nguyen Co., Ltd.

Intel Products Vietnam Co., Ltd.

Amkor Technology Vietnam Limited Company

Hana Micron Vina Co., Ltd.

FPT Semiconductor Joint Stock Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Coherent Corporation inaugurated a USD 127 million plant in Dong Nai for Silicon Carbide substrates and optical equipment.

- July 2025: CT Group unveiled the CTDA200M 12-bit 200 MSPS ADC, designed in six months and slated for TSMC fabrication.

- July 2025: Deputy Prime Minister Nguyen Chi Dung agreed with Taiwan’s Sustainable Economic Development Association to station 16 experts for semiconductor R&D transfer.

- May 2025: FPT showcased its “FPT Chip Inside” ecosystem at SEMICON Southeast Asia and pledged to train 10,000 professionals.

Vietnam Semiconductor Market Report Scope

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By Integrated Circuit Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | Less than 3nm | ||

| 3nm | |||

| 5nm | |||

| 7nm | |||

| 16nm | |||

| 28nm | |||

| 28nm | |||

| Integrated Device Manufacturer (IDM) |

| Design / Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing / Data Storage |

| Data Center |

| Artificial Intelligence |

| Government (Aerospace and Defense) |

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Devices | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Device Types | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Others | ||||

| Integrated Circuits | By Integrated Circuit Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (Shipment Volume Not Applicable) | Less than 3nm | |||

| 3nm | ||||

| 5nm | ||||

| 7nm | ||||

| 16nm | ||||

| 28nm | ||||

| 28nm | ||||

| By Business Model | Integrated Device Manufacturer (IDM) | |||

| Design / Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing / Data Storage | ||||

| Data Center | ||||

| Artificial Intelligence | ||||

| Government (Aerospace and Defense) | ||||

Key Questions Answered in the Report

How large is the Vietnam semiconductor market today?

The Vietnam semiconductor market size is USD 10.16 billion in 2025 and is projected to reach USD 16.51 billion by 2030.

What is the growth rate forecast for Vietnam's chip sector?

The market is expected to grow at a 10.23% CAGR between 2025 and 2030 thanks to sustained FDI and government incentives.

Which device category holds the largest revenue share?

Integrated circuits command 46% of market revenue due to robust packaging and test demand from global OEMs.

Which business model is expanding fastest?

The fabless model is slated to advance at a 12.88% CAGR as local firms leverage imported IP and outsourced wafer production.

Why is Vietnam attractive for semiconductor investors?

Competitive tax holidays, low labor costs, rare-earth resources and proximity to established electronics manufacturing clusters draw multinational capital.

What are the main challenges facing local chipmakers?

Key hurdles include the absence of sub-28 nm fabs, engineer shortages, power-grid instabilities and dependence on imported specialty gases and chemicals.

Page last updated on: