ASEAN Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

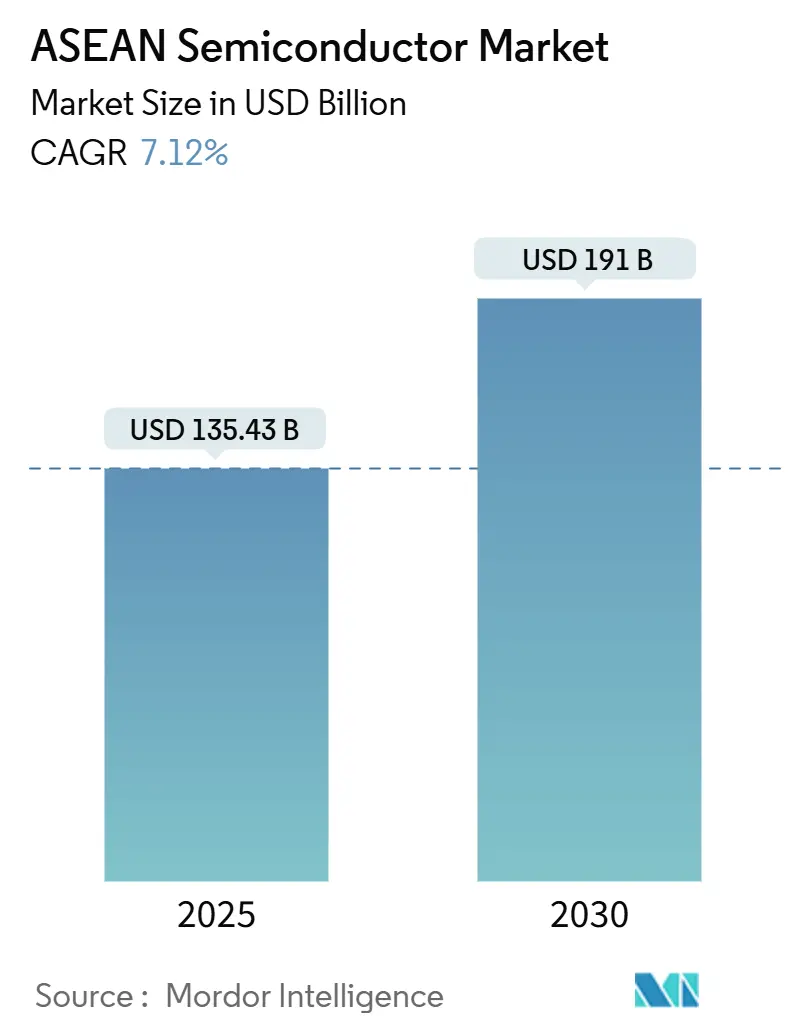

| Market Size (2025) | USD 135.43 Billion |

| Market Size (2030) | USD 191 Billion |

| Growth Rate (2025 - 2030) | 7.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Semiconductor Market Analysis by Mordor Intelligence

The ASEAN semiconductor market size stood at USD 135.43 billion in 2025 and is forecast to reach USD 191 billion by 2030, delivering a 7.12% CAGR. This expansion reflects the region’s role as a key diversification node in global supply chains amid geopolitics, and it is propelled by surging demand from electric vehicles, AI infrastructure, and 5G deployments. Government incentives, mature‐node capacity shifts from China, and rapid build-out of chiplet-ready packaging lines reinforce momentum. Multinational foundries deepen footprints across Malaysia, Singapore, and Vietnam to hedge risk and secure cost-effective production. At the same time, rising energy prices and engineering-talent shortages temper the speed at which local firms can move from back-end assembly into design and advanced fabrication.

Key Report Takeaways

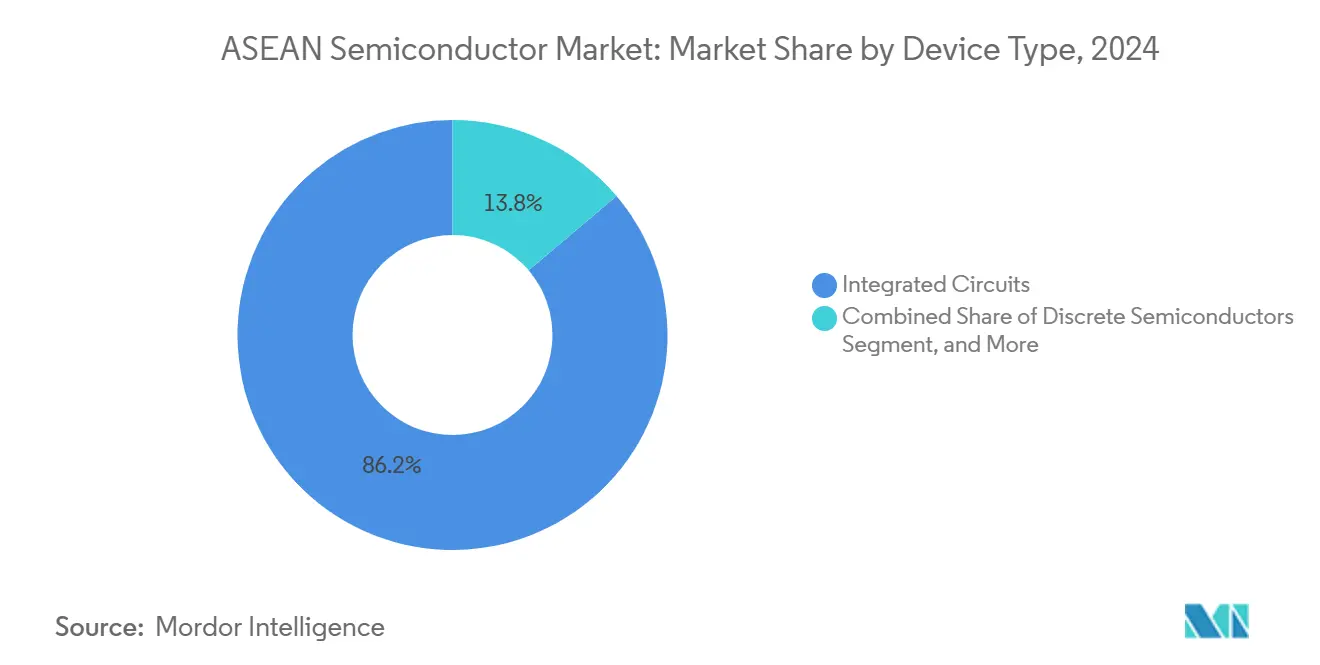

- By device type, integrated circuits held 86.2% of the ASEAN semiconductor market share in 2024; sensors and MEMS posted the fastest growth at 7.8% CAGR to 2030.

- By business model, the design/fabless segment commanded 68.1% share of the ASEAN semiconductor market size in 2024 and is projected to expand at a 7.5% CAGR between 2025–2030.

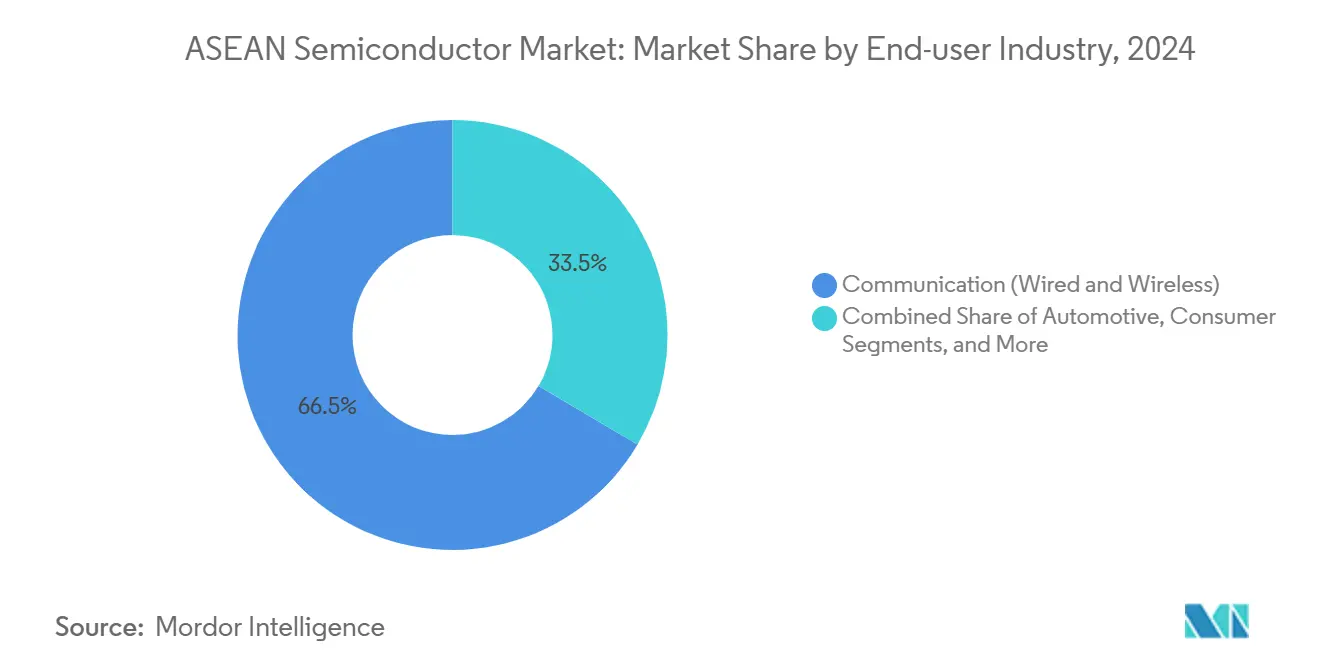

- By end-user, communication applications led with 66.5% revenue share in 2024, while AI workloads are advancing at a 9.9% CAGR through 2030.

- By country, Malaysia accounted for 47.6% of 2024 revenue, whereas Vietnam is forecast to post the fastest 8.2% CAGR to 2030.

ASEAN Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in EV and ADAS semiconductor demand | +1.8% | Malaysia, Thailand, and Vietnam core markets | Medium term (2-4 years) |

| Expansion of AI-enabled data-centres | +1.5% | Singapore, Malaysia, and Indonesia primary hubs | Short term (≤ 2 years) |

| Roll-out of 5G infrastructure | +1.2% | Global ASEAN coverage, Singapore leading | Medium term (2-4 years) |

| Government FDI incentives and subsidy schemes | +0.9% | Vietnam, Thailand, and Indonesia focus areas | Long term (≥ 4 years) |

| Mature-node capacity shift from China to ASEAN | +1.1% | Malaysia, Vietnam, Thailand beneficiaries | Medium term (2-4 years) |

| Emergence of chiplet-ready advanced packaging hubs | +0.7% | Singapore, Malaysia have advanced facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in EV and ADAS Semiconductor Demand

Thailand targets 30% EV output by 2030, drawing Chinese automakers that now source ISO 26262-compliant power and sensor chips from nearby Malaysian and Vietnamese packaging partners. Infineon is enlarging its Kulim line to produce silicon-carbide devices for EV inverters, while Qualcomm’s Snapdragon Ride platform ships from regional OSATs for Toyota and FAW programs.[1]Stephanie Findlay, “Qualcomm Lands Autonomous Driving Projects with Toyota and FAW’s Hongqi,” KrASIA, kr-asia.com Indonesia leverages nickel reserves to attract battery and power-semiconductor projects, further amplifying automotive chip demand.

Expansion of AI-enabled Data Centers

Hyperscale firms anchor new cloud regions in Singapore’s tech corridor and Malaysia’s Johor district, each requiring AI accelerators and high-bandwidth memory that pass through ASEAN’s advanced packaging chain. Nvidia-backed design pilots in Ho Chi Minh City aim to localize chiplet layouts for AI training clusters, while renewable-power constraints prompt custom power-management IC development for tropical data-center thermals.

Roll-out of 5G Infrastructure

Singapore achieved national 5G coverage in 2025, and Malaysia targets 80% population to reach the same year, triggering bulk orders for RF front-end modules and baseband ASICs assembled in Penang and Batam. Thailand’s Eastern Economic Corridor is integrating 5G to enable smart-factory IoT, lifting demand for industrial microcontrollers, while Vietnamese carriers issue long-term frameworks that guide predictable semiconductor procurement.

Government FDI Incentives and Subsidy Schemes

Vietnam grants up to 15-year tax holidays for high-tech fabs, Malaysia earmarks USD 5 billion for its National Semiconductor Strategy, and Indonesia’s sovereign wealth fund channels capital toward back-end clusters. Cross-border coordination lets companies splice design labs in Singapore with mass packaging in Vietnam, maximizing incentives while retaining ASEAN market access.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of advanced-node engineering talent | -1.4% | Singapore, Malaysia primary impact | Long term (≥ 4 years) |

| Geopolitical raw-material supply risks | -0.8% | Global ASEAN exposure, Vietnam critical minerals focus | Medium term (2-4 years) |

| Energy-intensity vs decarbonisation targets | -0.6% | Malaysia, Thailand are manufacturing hubs | Long term (≥ 4 years) |

| Weak local IP-protection deterring fabless growth | -0.5% | Vietnam, Indonesia are developing frameworks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Advanced-node Engineering Talent

ASEAN universities expand wafer-process curricula, yet the region competes with Taiwan and the United States for veteran 7 nm and below engineers. Corporate rotation programs bring expertise to greenfield fabs, but long learning curves constrain design-start velocity, limiting how fast ASEAN companies can lock in intellectual-property revenue.

Geopolitical Raw-material Supply Risks

China still refines most specialty gases and rare earths, leaving ASEAN fabs exposed to export-control shocks. Vietnam’s tenfold jump in rare-earth output offers diversification, yet processing plants remain under construction, and Malaysia’s Lynas refinery faces stringent environmental reviews.[2]“China Is King of These Critical Metals,” Channel News Asia, channelnewsasia.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated Circuits Sustain Packaging-led Growth

Integrated circuits commanded 86.2% revenue in 2024 and are growing at a 7.8% CAGR, keeping the ASEAN semiconductor market size heavily tilted toward system-on-chip and chiplet modules for AI and mobile workloads. Discrete power devices trail but receive a lift from EV chargers and renewable inverters.

Advanced packaging hubs in Singapore and Malaysia now laminate logic, memory, and I/O dies into single substrates, monetizing the thermal-management know-how needed for 3 DIC AI accelerators. Optoelectronics centers in Vietnamese handset lines sustain steady sensor demand, while MEMS suppliers pivot to industrial pressure and inertial units for smart-factory rollouts.

By Business Model: Fabless Surge Reallocates Value

Design-centric companies represented 68.1% of 2024 revenue, signaling how intellectual property creation reshapes the ASEAN semiconductor market. Fabless startups in Ho Chi Minh City tap subsidized EDA seats to draft RISC-V cores that later enter the OSAT flow in Penang, capturing higher gross margins than legacy assembly contracts.

IDMs still maintain capacity backstops—GlobalFoundries Singapore and UMC’s Malaysian line secure mature-node supply—yet increasingly outsource 2.5 D package builds to regional consortium partners. Strengthened IP-protection laws and cross-border R&D grants aim to keep tape-outs local and slow brain drain.

By End-user Industry: AI Drives Demand Transformation

Communication electronics kept a 66.5% share in 2024, but AI servers now post the fastest 9.9% CAGR, shifting the ASEAN semiconductor market share toward high-performance computing dies that require advanced interposers. Industrial IoT rollouts around 5G factories drive resilient microcontroller uptake, while EV expansion lifts automotive ADAS SOCs that meet ISO 26262.

Consumer-device flows remain robust as Vietnam and Malaysia churn out smartphones and laptops, yet replacement cycles lengthen, steering suppliers to diversify into mixed-signal ASICs for edge AI peripherals.

Geography Analysis

Malaysia held 47.6% revenue in 2024 owing to its decades-old OSAT cluster, but Vietnam’s 8.2% CAGR raises prospects of eroding that gap before 2030. Singapore retains a crucial 10% slot for R&D-heavy wafer and equipment output.

Malaysia’s entrenched supplier networks, USD 5 billion state aid, and rare-earth refining keep its foundries full and margins healthy despite energy-cost pressure. Penang’s “Silicon Island” continues to host ASE Group and STATS ChipPAC expansions, reinforcing Malaysia’s position at the center of the ASEAN semiconductor market.

Vietnam’s aggressive tax holidays, 16 free-trade pacts, and Intel’s flagship test-and-assembly plant have set a high bar for speed of capacity additions. Da Nang’s USD 75 million Fab-Lab anchors advanced packaging skills, while mandatory local-chip rules effective 2027 deepen domestic design pools.[3]“Đà Nẵng đầu tư mạnh cho ngành công nghiệp bán dẫn,” Vietnamplus.vn

Singapore pairs world-class IP frameworks with a USD 2 billion Silicon Box investment that brings chiplet-ready substrates to scale. Though labor costs outrank peers, its predictable regulation and proximity to global capital continue to pull in HQ and R&D mandates. Thailand and Indonesia complete the picture: Bangkok’s Eastern Economic Corridor incentivizes automotive chips; Jakarta banks on battery supply-chain adjacency to cultivate power-device fabs.

Competitive Landscape

The ASEAN semiconductor market supports a mosaic of multinationals and home-grown challengers. GlobalFoundries’ 300 mm fab in Woodlands anchors 0.13 µm to 22 nm demand, while UMC’s Malaysian site shores up overflow. Micron presses ahead with DRAM stacking lines in Singapore to feed AI servers.

Regional disruptors include Vietnamese design houses drafting AI inference cores for cloud clients, and Malaysian IP boutiques co-developing RISC-V extensions with Arm partnerships. OSAT majors ASE Group and Amkor broaden package portfolios to 2.5D and fan-out, capturing chiplet business away from Northeast Asia.

Government local-content mandates tilt bidding toward suppliers with indigenous capacity, prompting multinationals to form joint ventures or build “copy-exact” modules inside ASEAN borders. Patent filings for humidity-tolerant passivation layers and low-latency chiplet interconnects underline a maturing innovation fabric.[4]“BoS Semiconductors joins UCIe Consortium…,” Design-reuse.com

ASEAN Semiconductor Industry Leaders

GlobalFoundries Singapore Pte. Ltd.

Micron Semiconductor Asia Operations Pte. Ltd.

United Microelectronics Corporation (Singapore)

Infineon Technologies Asia Pacific Pte. Ltd.

Silicon Box Pte. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Vietnam’s prime minister mandates domestic chip design and manufacturing capabilities by 2027 to deepen the value chain.

- August 2025: Da Nang launches a USD 75 million Fab-Lab to accelerate advanced packaging skill development.

- July 2025: Samsung clinches Tesla AI-chip contract, signaling ASEAN production’s rising stature in high-performance segments.

- May 2025: Vietnam’s finance minister and Samsung discuss VAT incentives, raising total Samsung investment to USD 23.2 billion.

ASEAN Semiconductor Market Report Scope

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By Integrated-Circuit Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | ||

| 3 nm | |||

| 5 nm | |||

| 7 nm | |||

| 16 nm | |||

| 28 nm | |||

| > 28 nm | |||

| IDM |

| Design / Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing / Data Storage |

| Data Centre |

| AI |

| Government (Aerospace and Defence) |

| Singapore |

| Malaysia |

| Thailand |

| Vietnam |

| Indonesia |

| Rest of ASEAN countries |

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Devices | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Device Types | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Others | ||||

| Integrated Circuits | By Integrated-Circuit Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (Shipment Volume Not Applicable) | < 3 nm | |||

| 3 nm | ||||

| 5 nm | ||||

| 7 nm | ||||

| 16 nm | ||||

| 28 nm | ||||

| > 28 nm | ||||

| By Business Model | IDM | |||

| Design / Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing / Data Storage | ||||

| Data Centre | ||||

| AI | ||||

| Government (Aerospace and Defence) | ||||

| By Country | Singapore | |||

| Malaysia | ||||

| Thailand | ||||

| Vietnam | ||||

| Indonesia | ||||

| Rest of ASEAN countries | ||||

Key Questions Answered in the Report

How large is the ASEAN semiconductor market in 2025?

It is valued at USD 135.43 billion and is projected to record a 7.12% CAGR to 2030.

Which country leads ASEAN semiconductor production?

Malaysia holds 47.6% of 2024 revenue thanks to its mature assembly and test ecosystem.

What drives future chip demand in Southeast Asia?

EV adoption, AI data-center build-outs and 5G rollouts supply the strongest multi-year pull.

Why are companies shifting mature-node capacity to ASEAN?

Cost benefits, geopolitical risk diversification and generous FDI incentives encourage migration from China.

What is the fastest-growing end-use for chips in the region?

AI workloads, particularly data-center accelerators, are expanding at 9.9% CAGR through 2030.

Page last updated on: