Thailand Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

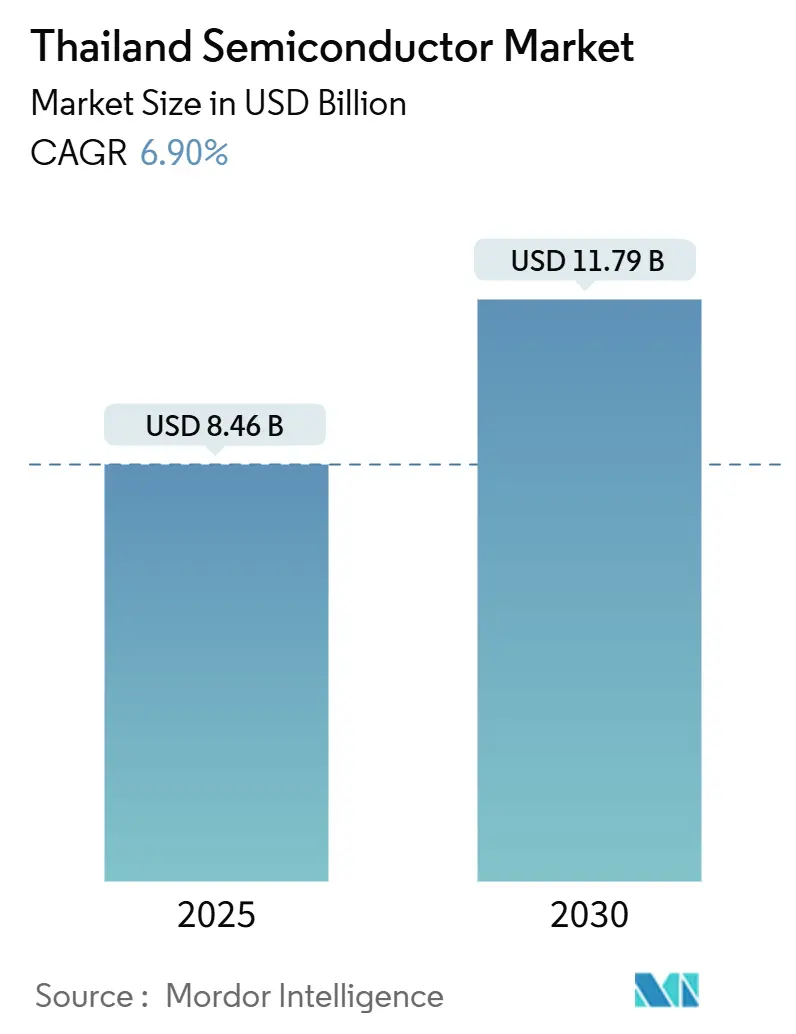

| Market Size (2025) | USD 8.46 Billion |

| Market Size (2030) | USD 11.79 Billion |

| Growth Rate (2025 - 2030) | 6.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Semiconductor Market Analysis by Mordor Intelligence

The Thailand semiconductor market size stands at USD 8.46 billion in 2025 and is projected to reach USD 11.79 billion by 2030, advancing at a 6.90% CAGR during the period. Government incentives, robust foreign direct investment, and a decisive shift toward electric vehicles (EVs), artificial intelligence (AI), and Internet of Things (IoT) devices are steering this progress. Integrated device manufacturers (IDMs) continue to dominate, yet Thailand’s growing network of fabless design houses is steadily capturing value in high-growth niches. A maturing Eastern Economic Corridor (EEC) is attracting large-scale green- and brownfield plants, while the confluence of automotive evolution and power-semiconductor innovation reinforces local demand. Ongoing energy-price challenges and engineering-talent shortages, however, temper Thailand’s ambitions to compete at sub-16 nm nodes.[1]Board of Investment of Thailand, “Thailand’s Advantages,” boi.go.th

Key Report Takeaways

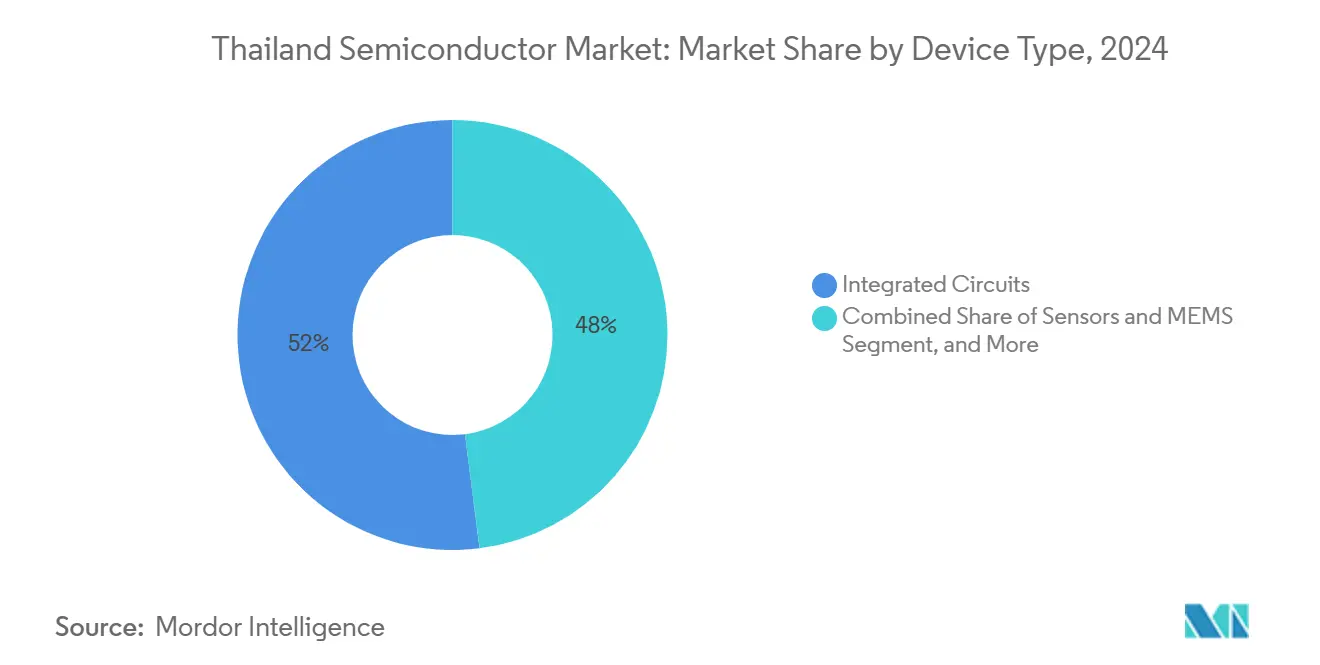

- By device type, integrated circuits led with a 52% Thailand semiconductor market share in 2024; sensors and MEMS are forecast to expand at a 10.93% CAGR through 2030.

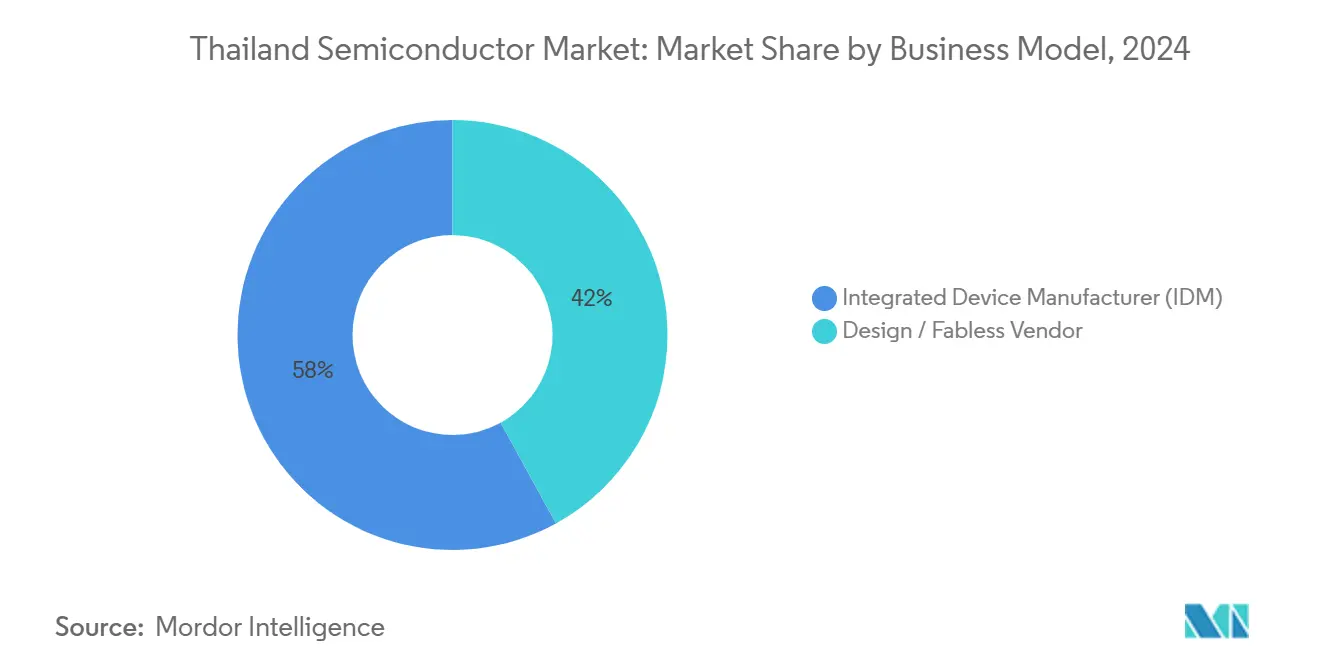

- By business model, IDMs held 58% of the Thailand semiconductor market share in 2024, while design/fabless vendors recorded the highest projected CAGR at 0.48% through 2030.

- By end-user industry, automotive captured 26% of the Thailand semiconductor market size in 2024; AI applications are set to accelerate at an 11.26% CAGR to 2030.

Thailand Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government incentives under Thailand 4.0 and Eastern Economic Corridor | +1.80% | National, concentrated in Chachoengsao, Chonburi, Rayong provinces | Medium term (2-4 years) |

| Rapid expansion of EV and battery manufacturing clusters | +1.50% | Eastern Economic Corridor, with spillover to Greater Bangkok | Short term (≤ 2 years) |

| Rising domestic demand for IoT and smart-home devices | +1.20% | National, urban centers leading adoption | Medium term (2-4 years) |

| Growing foreign direct investment seeking China+1 supply-chain diversification | +1.00% | National, EEC priority zones | Long term (≥ 4 years) |

| Niche demand for wide-bandgap power electronics from utility-scale renewables | +0.80% | National, solar-rich provinces in Northeast and Central regions | Long term (≥ 4 years) |

| Emergence of specialized medical-electronics design houses for ageing-care devices | +0.50% | Bangkok metropolitan area, medical device clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV Manufacturing Clusters Accelerate Power-Semiconductor Demand

Thailand targets 600,000 EVs per year by 2026 under EV 3.0 and EV 3.5 policies. The Hana Microelectronics–PTT joint venture is building the country’s first silicon-carbide wafer facility (THB 11.5 billion), directly supporting high-voltage traction inverters and fast chargers.[2]DIGITIMES Asia, “Thailand to Build First SiC Facility,” digitimes.com Delta Electronics and other Tier 1 suppliers have co-located new power-module lines in Samut Prakan, tightening the automotive–semiconductor value loop.

IoT and Smart-Device Proliferation Drives Sensor Integration

National IoT spending is forecast to top USD 2.19 billion by 2030, underpinned by 5G mmWave deployments at industrial parks, smart-city pilots, and hospital automation. MEMS pressure, accelerometer, and temperature sensors therefore outpace other categories. Alliances brokered by the Digital Economy Promotion Agency between domestic OEMs and leading cloud providers expedite edge-compute adoption.[3]Bangkok Post, “Ministry Allots B5bn to Upgrade Workforce,” bangkokpost.com

China+1 Diversification Strategies Reshape Investment Flows

Approved FDI pledges reached THB 1.14 trillion in 2024, with semiconductors the largest recipient as firms pursue geographic hedging. Western Digital, Sony, and Analog Devices are raising Thai capacity to safeguard against single-country exposure. BOI roadshows in the United States and Japan reinforce the pipeline of assembly, test, and advanced-packaging projects.

Government Incentives Drive Strategic Semiconductor Positioning

Thailand’s Board of Investment offers corporate income-tax holidays of up to 15 years and accelerated depreciation for advanced fabs. The EEC adds land-ownership privileges and fast-track visas, accelerating landmark investments such as Infineon’s USD 350 million backend fab and a TSMC-affiliated packaging plant. A parallel THB 5 billion program to train 17,500 semiconductor workers over five years addresses critical talent gaps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of advanced-node engineering talent | -1.20% | National, acute in Bangkok and EEC zones | Short term (≤ 2 years) |

| High electricity prices versus regional peers | -0.80% | National, manufacturing-intensive provinces | Medium term (2-4 years) |

| Chronic water-stress risks around industrial zones | -0.60% | Eastern provinces, industrial estates | Long term (≥ 4 years) |

| Fragmented local ecosystem hampers adoption below 16 nm | -0.40% | National, technology development centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated Circuits Lead Value Creation

Integrated circuits held a 52% Thailand semiconductor market share in 2024, anchored by mature back-end assembly capacity. Sensors and MEMS, propelled by EV traction inverters and smart-factory rollouts, will log the fastest 10.93% CAGR to 2030. The upcoming silicon-carbide wafer line marks Thailand’s first move beyond 28 nm mainstream nodes into wide-bandgap territory. Industrial power discrete for solar inverters and EV chargers maintain a stable niche.

Steady diversification continues as optoelectronics underpin LED auto-lighting exports, while discrete transistors support motor drives in appliance factories. Domestic design houses now co-develop MEMS pressure and inertial sensors with the Thai Microelectronics Center, injecting higher local value capture. Although advanced logic remains absent, the Thailand semiconductor market size for IC assembly is projected to rise in step with global outsourcing cycles.

By Business Model: IDM Dominance Faces Fabless Pressure

IDMs controlled 58% of the Thailand semiconductor market share in 2024 as companies such as Western Digital and Texas Instruments leverage scale economies in back-end lines. Fabless and design-service firms grow at a restrained 0.48% CAGR yet signal a structural pivot toward R&D-led revenue. Stars Microelectronics’ cross-border OSAT venture exemplifies this outward shift.

Local policy now diverts R&D grants to tape-out subsidies, encouraging small design houses to partner with regional foundries while using Thai prototyping labs for MEMS and RF modules. As learning curves mature, the Thailand semiconductor market size attributable to design royalty streams is expected to broaden, even if manufacturing-centric IDMs dominate absolute output volumes.

By End-User Industry: Automotive Leadership Meets AI Acceleration

Automotive retained 26% of the Thailand semiconductor market size in 2024, reflecting the country’s role as ASEAN’s EV hub. Government targets of 600,000 EVs annually shore up demand for traction inverters, battery-management ICs, and advanced driver-assistance sensors. AI edge devices for predictive maintenance, computer vision in smart factories, and speech recognition in consumer appliances are set to climb at an 11.26% CAGR to 2030.

Communication infrastructure builds, alongside 5G small cells, support incremental growth, while industrial automation sustains steady sensor and MCU pull-through. Datacenter and storage demand hinges on Western Digital’s HDD expansions. Government and aerospace niches gain strategic importance through satellite component programs that involve Thai–Taiwan co-development contracts.

Geography Analysis

The EEC covering Chachoengsao, Chonburi, and Rayong hosts more than 70% of new semiconductor investment pledges, benefiting from purpose-built utilities, seaport connectivity at Laem Chabang, and preferential BOI privileges. Map Ta Phut industrial estates now integrate chemical supply chains crucial for photoresists and wet-process gases. Greater Bangkok emerges as the design nucleus, sheltering Silicon Craft Technology and the Thai Microelectronics Center, where tape-out support and MEMS prototyping occur.

Northern Lamphun province diversifies geographic risk; Murata’s USD 1.7 billion multilayer-ceramic-capacitor (MLCC) expansion underscores the trend. Such dispersion supports supply-chain resilience and harnesses lower labour costs. Energy-rich northeastern provinces also court power-semiconductor plants that can co-locate with utility-scale solar farms, aligning corporate decarbonization targets with the National Energy Plan’s 51% renewables objective.[4]Asian Development Bank, “ASEAN and Global Value Chains,” adb.org

Regional trade pacts such as the ASEAN Free Trade Area and the Indo-Pacific Economic Framework strengthen Thailand’s position as a China+1 alternative. Efficient road–rail corridors linking the EEC to Laos and Vietnam improve lead times to customers in neighbouring electronics clusters. Collectively, these factors allow the Thailand semiconductor market to serve both domestic assembly plants and wider ASEAN export channels.

Competitive Landscape

Thailand’s semiconductor ecosystem demonstrates moderate concentration as domestic champions coexist with global majors. Hana Microelectronics, Stars Microelectronics, and Delta Electronics exploit labour and cost efficiencies in packaging and power-module assembly. Infineon, Texas Instruments, and ON Semiconductor enlarge Thai footprints to balance global supply chains.

Competition centers on back-end excellence, time-to-yield, and ISO-certified quality. Western Digital’s HDD complex, employing more than 28,000 staff, illustrates economies of scale in volume manufacturing. New entrants bet on advanced packaging fan-out wafer-level and heterogeneous integration and wide-bandgap power devices. Government incentive tiers favour ventures bringing novel process steps or establishing R&D affiliations with Thai universities.

Talent development partnerships, green-energy procurement commitments, and local-content rules shape competitive positioning. Firms aligning with BOI sustainability metrics gain expedited permitting, while those investing in workforce skilling access salary-subsidy programs. As advanced-packaging capacity scales, rivalry is likely to intensify in test-services specialization, reinforcing Thailand’s role in regional semiconductor supply chains.

Thailand Semiconductor Industry Leaders

Hana Microelectronics PLC

Western Digital (Thailand) Co., Ltd.

Silicon Craft Technology PLC

Stars Microelectronics (Thailand) PLC

ROHM Integrated Systems (Thailand) Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Thailand BOI set a THB 500 billion semiconductor-investment target and commissioned a national industry roadmap.

- January 2025: Infineon began construction of a new backend fab in Samut Prakan, aiming for first output in early 2026.

- December 2024: Murata approved THB 62 billion for an advanced capacitor plant in Lamphun.

- December 2024: A TSMC subsidiary secured incentives for a Thai chip-assembly plant.

Thailand Semiconductor Market Report Scope

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By Integrated Circuit Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | Less than 3nm | ||

| 3nm | |||

| 5nm | |||

| 7nm | |||

| 16nm | |||

| 28nm | |||

| 28nm | |||

| Integrated Device Manufacturer (IDM) |

| Design / Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing / Data Storage |

| Data Center |

| AI |

| Government (Aerospace and Defense) |

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Devices | ||||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Device Types | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Others | ||||

| Integrated Circuits | By Integrated Circuit Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (Shipment Volume Not Applicable) | Less than 3nm | |||

| 3nm | ||||

| 5nm | ||||

| 7nm | ||||

| 16nm | ||||

| 28nm | ||||

| 28nm | ||||

| By Business Model | Integrated Device Manufacturer (IDM) | |||

| Design / Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing / Data Storage | ||||

| Data Center | ||||

| AI | ||||

| Government (Aerospace and Defense) | ||||

Key Questions Answered in the Report

What is the value of the Thailand semiconductor market in 2025 and its forecast for 2030?

It is valued at USD 8.46 billion in 2025 and is expected to reach USD 11.79 billion by 2030.

Which segment leads by device type in Thailand?

Integrated circuits hold a 52% share, the largest among device categories.

How fast is the sensors and MEMS segment growing?

Sensors and MEMS are projected to expand at a 10.93% CAGR through 2030.

What share do IDMs hold in Thailand?

IDMs accounted for 58% of packaged-chip revenue in 2024.

Which end-user sector drives the most demand?

Automotive leads with 26% of semiconductor consumption.

What is the main geographic hub for chip manufacturing in Thailand?

The Eastern Economic Corridor concentrates the majority of new semiconductor investments.

Page last updated on: