Singapore Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

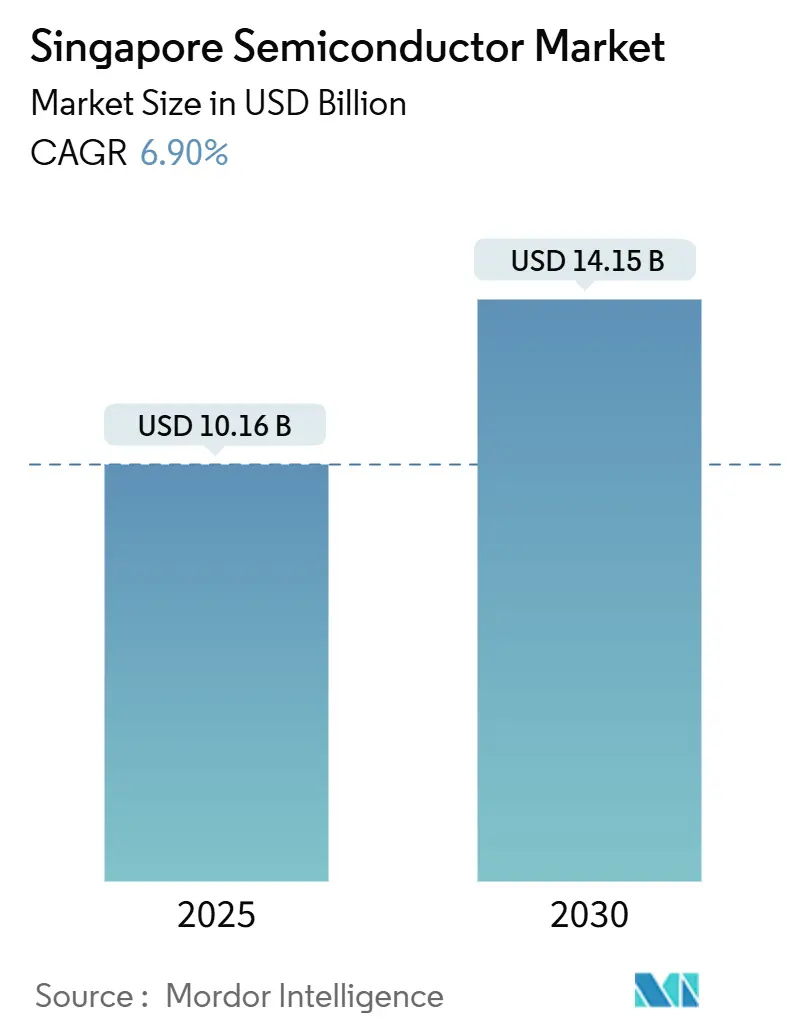

| Market Size (2025) | USD 10.16 Billion |

| Market Size (2030) | USD 14.15 Billion |

| Growth Rate (2025 - 2030) | 6.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Semiconductor Market Analysis by Mordor Intelligence

The Singapore semiconductor market reached a market size of USD 10.16 billion in 2025 and is forecast to climb to USD 14.15 billion by 2030, posting a 6.9% CAGR that underscores Singapore’s role as a global chip manufacturing hub.[1]Ministry of Finance Singapore, “Budget 2025 Factsheet: Advancing Manufacturing,” mof.gov.sg Government funding, AI-optimized production lines, and deep-water investments in advanced packaging attract multinational corporations while nurturing local design activity. Modern fabs leverage renewable power and smart-factory automation to offset high operating costs. Strategic public-private R&D programs supply cleanroom space and industry-grade tools, accelerating device prototyping cycles. At the same time, data-center buildouts in Jurong and Changi funnel demand for high-bandwidth memory, logic, and power devices that serve AI workloads.

Key Report Takeaways

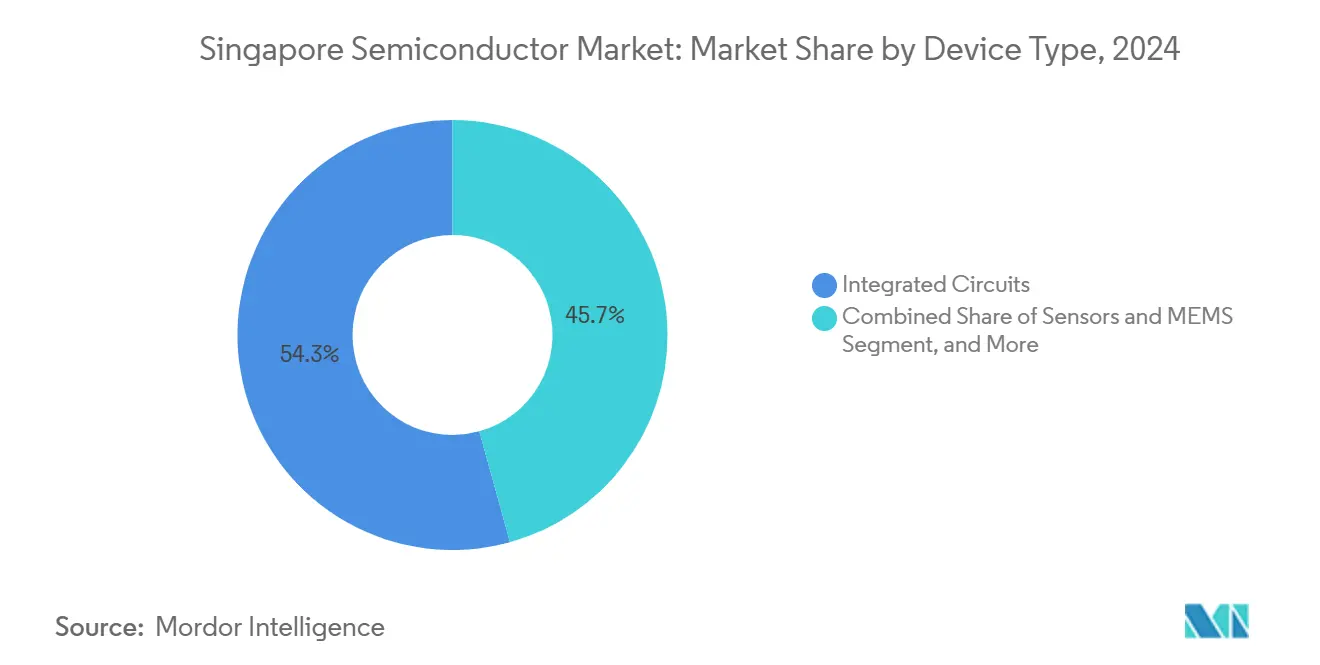

- By device type, Integrated Circuits led with 54.3% revenue share in 2024; Sensors & MEMS are projected to expand at a 10.41% CAGR through 2030.

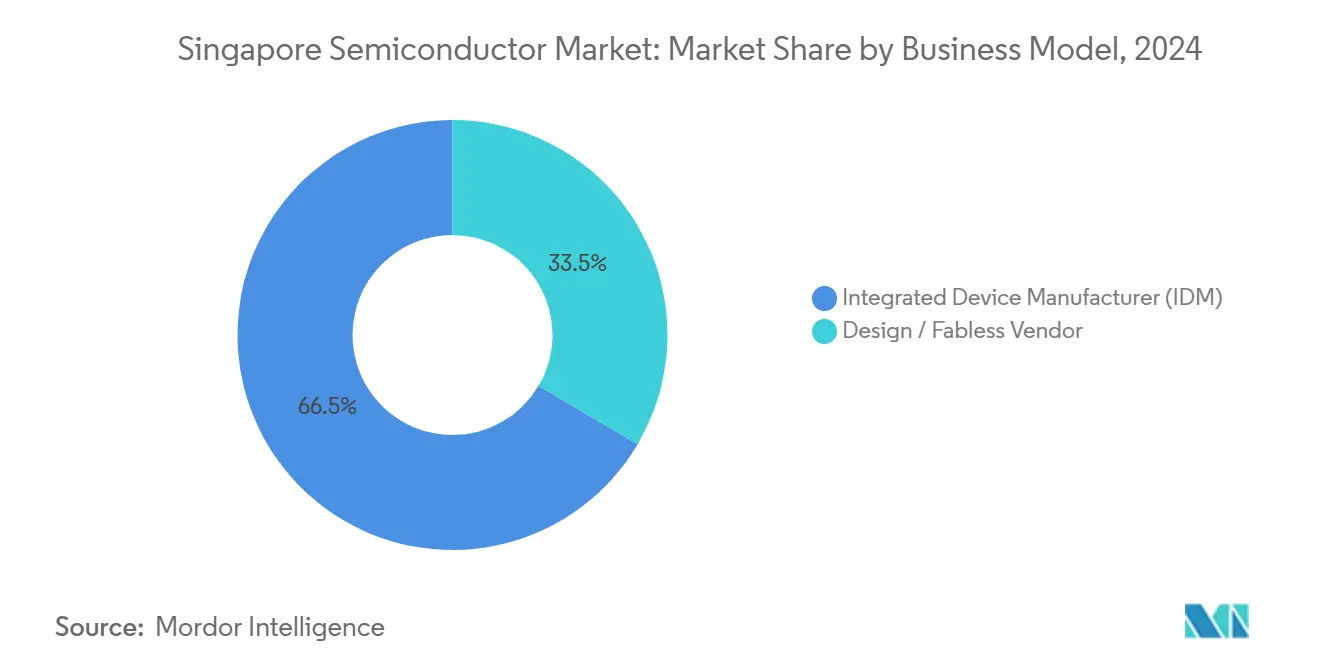

- By business model, the IDM segment held a 66.5% share of the Singapore semiconductor market size in 2024, while the Design/Fabless segment is forecast to grow at a 9.88% CAGR to 2030.

- By end-user industry, Communication applications commanded 27% of the Singapore semiconductor market share in 2024; AI-focused applications register the fastest growth at an 11.03% CAGR through 2030.

Singapore Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust government incentives for advanced-node fabs | +1.20% | Singapore, with spillover to APAC | Medium term (2-4 years) |

| Surge in automotive-grade semiconductor testing demand | +1.80% | Global, with concentration in Singapore testing hubs | Long term (≥ 4 years) |

| Expansion of data-center build-outs in Jurong and Changi | +1.50% | Singapore, supporting regional cloud infrastructure | Short term (≤ 2 years) |

| Increased 3D-NAND output by Micron's Singapore mega-fab | +0.90% | Singapore, serving global memory markets | Medium term (2-4 years) |

| National AI compute roadmap catalyzing local chip design | +0.80% | Singapore, with regional AI ecosystem benefits | Long term (≥ 4 years) |

| Rising interest in silicon photonics for maritime 5G/6G | +0.40% | Singapore ports, with maritime industry applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Government Incentives for Advanced-Node Fabs

Budget 2025 added S$3 billion to the National Productivity Fund and earmarked S$1 billion for semiconductor infrastructure, enabling the S$500 million National Semiconductor Translation and Innovation Centre that offers shared cleanrooms and state-of-the-art tools. Tax breaks let firms convert up to S$100,000 of qualifying R&D outlays into cash at a 20% ratio while enjoying 400% deductions on approved projects through 2028.[2]Inland Revenue Authority of Singapore, “Enterprise Innovation Scheme,” iras.gov.sg These incentives reduce capital barriers for advanced packaging and chiplet integration. The Economic Development Board secured S$13.5 billion in fixed-asset pledges during 2024, S$11.1 billion of which targeted manufacturing, signalling investor confidence in Singapore’s pro-semiconductor stance. Stable policy, efficient customs, and strong IP protection round out an environment that de-risks multibillion-dollar fab projects.

Surge in Automotive-Grade Semiconductor Testing Demand

Electric vehicles now integrate more than 3,000 chips valued up to USD 6,000 per unit, driving unprecedented test complexity for safety-critical and high-temperature conditions.[3]The Straits Times, “EV Microchips Boom Spurs Singapore Test Demand,” straitstimes.com Singapore’s system-level test providers deploy AI-enabled “Test 2.0” platforms that lift throughput and slash false-fail rates. AEM Holdings upgrades capacity to address silicon carbide power devices used in traction inverters while meeting ISO 26262 functional-safety mandates. Automotive original-equipment manufacturers increasingly redirect overflow test volumes from China and Malaysia to Singapore to secure faster cycle times and robust intellectual-property safeguards. Growing vehicle electrification across Southeast Asia amplifies demand for advanced validation services anchored in Singapore.

Expansion of Data-Center Buildouts in Jurong and Changi

Singapore’s Green Data Centre Roadmap unlocks at least 300 MW of new capacity, with 200 MW earmarked for operators using renewables. High-bandwidth memory, server-grade logic, and AI accelerators underpin this infrastructure wave, aligning with Micron’s USD 7 billion HBM packaging plant launching in 2026. Data-center operators adopt immersion cooling, prompting specialized power-management semiconductors from Infineon and STMicroelectronics. The close physical link between fabs and cloud facilities trims component lead times and logistics risk. Singapore’s 5G+ rollout boosts connectivity, reinforcing a virtuous cycle between telecom infrastructure and semiconductor uptake.

Increased 3D-NAND Output by Micron’s Singapore Mega-Fab

Micron’s ninth-generation TLC NAND achieves 3.6 GB/s transfer speeds and rolls out on lines powered by 100% renewable electricity, after an 11% drop in greenhouse emissions relative to 2020 baselines. The plant’s 128 GB DDR5 RDIMM boosts bit density by 45% and energy efficiency by 22% over peers, catering to AI servers that demand high-throughput, low-latency storage. Co-located HBM assembly will let Micron flex capacity between NAND and stacked-memory products, guarding against price cycles. Workforce-development programs and proximity to Asia-Pacific hyperscale’s cut prototype-to-production timelines, ensuring quick revenue ramp for next-generation memory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying utility-cost inflation vs. regional peers | -0.80% | Singapore, with competitive pressure from Malaysia | Short term (≤ 2 years) |

| Tight local engineering talent pipeline | -1.20% | Singapore, affecting regional expansion plans | Medium term (2-4 years) |

| Global inventory correction in consumer electronics | -0.60% | Global, impacting Singapore's export-oriented production | Short term (≤ 2 years) |

| Geopolitical export-control uncertainty on EUV tools | -0.90% | Singapore, affecting advanced node development | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Utility-Cost Inflation vs. Regional Peers

Electricity tariffs outpace regional averages while heat-stress forecasts warn of USD 1.5 billion in productivity losses by 2035. Semiconductor fabs reliant on ultra-pure water and power must either pay premiums or commit to on-site renewables and advanced cooling. STMicroelectronics inked long-term solar-energy contracts for its Malaysian operations, illustrating cost-management strategies that Singapore plants may emulate. Efficiency retrofits cushion margins but raise capital budgets, influencing site-selection for new advanced-node projects. Policymakers weigh subsidies or grid-fee rebates to preserve cost competitiveness versus Malaysia and Thailand.

Tight Local Engineering Talent Pipeline

Regional chipmakers report shortages totalling 34,000 engineers, with Singapore graduate output lagging demand. Salaries escalate as firms lure talent from neighbouring Malaysia, India, and Taiwan. The Economic Development Board partnered with local universities to tailor semiconductor curricula and fund mid-career conversion programs. Companies sponsor overseas scholarships in return for service bonds, yet the lead time to produce seasoned process engineers stretches expansion schedules. Wage inflation pressures profitability for high-mix, lower-volume specialty nodes common in Singapore.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated Circuits Anchor AI Infrastructure

Integrated Circuits accounted for 54.3% of 2024 revenue, mirroring capacity expansions that feed AI server demand and regional 5G rollouts. United Microelectronics Corporation’s Fab 12i will add 22 nm capability by 2026, broadening logic supply for automotive and IoT platforms. Memory makers deliver high-bandwidth modules that dovetail with Micron’s HBM roadmap. Analog ICs address power management for industrial drives and EV chargers, while discrete devices such as silicon carbide MOSFETs support traction inverters. Optoelectronics ride the surge in data-center optical links and nascent silicon-photonics projects at Tuas Port.

Sensors & MEMS hold the fastest trajectory with a 10.41% CAGR through 2030 as EVs add radar, LiDAR, and inertial sensors requiring high-precision packaging. The Lab-in-Fab program between STMicroelectronics and A*STAR develops piezoelectric MEMS, enhancing automotive safety and industrial robotics. Singapore’s foundries run mature 28 nm and 40 nm nodes suited for sensing solutions, while the National Semiconductor Translation and Innovation Centre explores heterogeneous integration that blends sensors, logic, and RF in single packages. The Singapore semiconductor market benefits when local test houses validate these multisensory modules under harsh automotive standards, shortening time-to-qualification.

By Business Model: IDM Scale Meets Fabless Agility

IDM players retained 66.51% of 2024 revenue thanks to vertically integrated control of design through assembly, vital for automotive reliability and aerospace certification. GlobalFoundries and STMicroelectronics leverage close coupling of R&D and manufacturing inside Singapore sites to speed design spins and process tweaks. Advanced-packaging roadmaps hinge on co-development between design and fab teams, favouring integrated models. Stable policy and IP safeguards further justify IDMs’ capital intensity.

Fabless and design-only firms expand at a 9.88% CAGR as the National Semiconductor Translation and Innovation Centre grants shared access to advanced-node prototyping and packaging. NXP and Vanguard’s USD 7.8 billion joint fab embodies hybrid collaboration in which design expertise merges with foundry efficiency. Startups tap low-volume pilot lines before scaling in regional foundries, accelerating commercialization. Equipment-maker Applied Materials positions Singapore as its Asia-Pacific process-development hub, bolstering both IDM and fabless ecosystems.

By End-User Industry: Communication Leads, AI Climbs Fast

Communication networks absorbed 27% of 2024 sales as operators rolled out 5G across Southeast Asia. Singtel’s 5G+ service covers more than 1.5 million users, spurring demand for RF front-end modules and base-station ASICs. Port-automation projects at Tuas integrate maritime 5G/6G links and silicon-photonics transceivers, creating new pull for optical components. Automotive applications strengthen with Infineon’s power devices and STMicroelectronics’ microcontrollers supporting EV drivetrains.

AI-centric workloads post an 11.03% CAGR through 2030, underpinned by Micron’s HBM and DDR5 rollouts that supply regional hyperscale cloud operators. Enterprise adoption of generative-AI platforms boosts accelerator card shipments, while ROHM’s EcoGaN power stages improve energy efficiency in AI servers. Industrial automation modernizes Singapore’s legacy electronics plants, upgrading to smart-factory sensors and edge-AI controllers. Consumer-device demand stabilizes following an inventory correction, though premium smartphones still adopt advanced SoCs produced locally.

Geography Analysis

Singapore commands the lion’s share of regional revenue, supplying 10% of global chip output and about 20% of semiconductor equipment while holding an estimated 82% share of the Southeast Asia Singapore semiconductor market size in 2025. Export-oriented fabs cluster near coastal logistics nodes, enabling two-day shipping to 80% of Asian customers. Public-private R&D hubs in Tampines and one-stop customs clearance at Changi Airfreight Centre keep cycle times low and quality yields high. Robust intellectual-property enforcement further anchors value capture inside the city-state. As a result, the local ecosystem retains advanced-node production even when neighbouring countries compete mainly on cost.

Malaysia complements Singapore through volume backend work, exemplified by Infineon’s Kulim silicon-carbide plant that feeds power devices back to Singapore for final test and packaging.[4]Infineon Technologies AG, “Kulim SiC Fab Grand Opening,” infineon.com The Johor–Singapore Special Economic Zone shortens cross-border trucking hops to under two hours, trimming inventory buffers and boosting the Singapore semiconductor market supply resilience. Thailand hosts Infineon’s new Samut Prakan assembly line, diversifying risk from single-site dependency while funnelling high-margin engineering change orders to Singapore labs. Vietnam and the Philippines continue to add labour-intensive assembly and test capacity, freeing Singapore engineers to focus on AI-centric design and heterogeneous integration.

Partnership deals widen Singapore’s reach beyond ASEAN. An India–Singapore cooperation pact opens joint training pipelines and IP sharing that ease the local engineering crunch. Taiwan’s foundries collaborate with Singapore packaging houses on chiplet ecosystems that target AI accelerators, giving the Singapore semiconductor market faster time-to-commercialization for sub-10 nm devices. Multinationals also use Singapore as a neutral export base to navigate U.S.–China trade frictions while staying compliant with evolving export-control regimes. This networked model keeps Singapore at the center of design wins even as manufacturing footprints become more distributed across Asia.

Competitive Landscape

GlobalFoundries, Micron, and STMicroelectronics remain the three largest revenue generators, together accounting for close to 45% of the Singapore semiconductor market in 2024. Each firm invests in smart-factory automation that cuts process-tool downtime by as much as 18%, keeping yields high despite rising node complexity. Micron’s USD 7 billion HBM line, operational in 2026, adds 45 thousand wafer-starts-per-month and converts to 100% renewable electricity by 2028, improving energy intensity metrics that matter to hyperscale customers.

Joint-venture activity intensifies. The USD 7.8 billion NXP–Vanguard fab slated for 2027 marries Dutch automotive MCU design with Taiwanese 300 mm manufacturing know-how, expanding Singapore semiconductor market capacity for mature-node power and analog devices. United Microelectronics Corporation’s 22 nm expansion at Fab 12i positions the company to court IoT and 5G baseband clients that need cost-competitive wafers without sacrificing reliability. Equipment suppliers such as Applied Materials and KLA deepen local footprints through joint labs that accelerate deposition, etch, and metrology tool iterations, shortening fab ramp-up schedules for every wafer producer in the cluster.

Competition now hinges on advanced packaging and export-control compliance. AEM Holdings’ AI-driven “Test 2.0” platform boosts tester utilization to 93%, saving customers up to USD 0.40 per device while winning share in the Singapore semiconductor market high-performance computing segment. Firms that document robust due-diligence workflows for dual-use items gain smoother customs clearances, an edge amplified as global rules on EUV scanners and gallium nitride power devices tighten. Overall, rivalry remains vigorous but guided collaboration via consortia and shared-fabrication programs keeps switching costs high and pricing discipline intact.

Singapore Semiconductor Industry Leaders

GlobalFoundries Singapore Pte. Ltd.

Micron Semiconductor Asia Pte. Ltd.

STMicroelectronics Asia Pacific Pte. Ltd.

Infineon Technologies Asia Pacific Pte. Ltd.

Systems on Silicon Manufacturing Co. Pte. Ltd. (SSMC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: onsemi reported first-quarter 2025 revenue of USD 1,445.7 million with 72% year-over-year free-cash-flow growth, highlighting strong design wins across automotive and industrial segments while trimming costs through portfolio rationalization.

- June 2025: TSMC affiliate VIS accelerated the production timeline for its USD 7.8 billion Singapore fab, targeting a late-2026 start instead of 1H 2027.

- June 2025: Renesas Electronics delayed its USD 20 billion revenue goal from 2030 to 2035 and shifted focus from silicon-carbide to gallium-nitride devices amid EV market turbulence.

- May 2025: STMicroelectronics expanded its “Lab-in-Fab” partnership with A*STAR and National University of Singapore to advance piezoelectric MEMS technology.

Singapore Semiconductor Market Report Scope

| Discrete Semiconductors | Diodes | |

| Transistors | ||

| Power Transistors | ||

| Rectifier and Thyristor | ||

| Other Discrete Devices | ||

| Optoelectronics | Light-Emitting Diodes (LEDs) | |

| Laser Diodes | ||

| Image Sensors | ||

| Optocouplers | ||

| Other Device Types | ||

| Sensors and MEMS | Pressure | |

| Magnetic Field | ||

| Actuators | ||

| Acceleration and Yaw Rate | ||

| Temperature and Others | ||

| Integrated Circuits | By Integrated Circuit Type | Analog |

| Micro | ||

| Logic | ||

| Memory | ||

| By Technology Node (Shipment Volume Not Applicable) | Less than 3nm | |

| 3nm | ||

| 5nm | ||

| 7nm | ||

| 16nm | ||

| 28nm | ||

| 28nm | ||

| Integrated Device Manufacturer (IDM) |

| Design / Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing / Data Storage |

| Data Center |

| AI |

| Government (Aerospace and Defense) |

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | |

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | Light-Emitting Diodes (LEDs) | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By Integrated Circuit Type | Analog | |

| Micro | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | Less than 3nm | ||

| 3nm | |||

| 5nm | |||

| 7nm | |||

| 16nm | |||

| 28nm | |||

| 28nm | |||

| By Business Model | Integrated Device Manufacturer (IDM) | ||

| Design / Fabless Vendor | |||

| By End-user Industry | Automotive | ||

| Communication (Wired and Wireless) | |||

| Consumer | |||

| Industrial | |||

| Computing / Data Storage | |||

| Data Center | |||

| AI | |||

| Government (Aerospace and Defense) | |||

Key Questions Answered in the Report

How large is the Singapore semiconductor market in 2025?

The singapore semiconductor market size stands at USD 10.16 billion in 2025, on track for USD 14.15 billion by 2030 at a 6.9% CAGR.

Which segment grows fastest through 2030?

Sensors & MEMS post the highest growth, advancing at a 10.41% CAGR as electric vehicles and industrial automation demand more embedded sensing.

Who are the key players?

GlobalFoundries, Micron, STMicroelectronics, and joint ventures like NXP-Vanguard dominate revenue while AEM Holdings leads advanced test services.

What drives near-term demand?

Government incentives, expanding data-center capacity, and AI server upgrades lift orders for high-bandwidth memory, advanced logic, and power devices.

What restrains expansion?

Rising utility costs and a tight engineering talent pool trim margins and could slow fab ramp-ups over the next two to four years.

How does Singapore differ from regional peers?

Singapore specializes in advanced packaging, R&D, and high-value test, while nearby Malaysia and Thailand focus on cost-effective volume assembly.

Page last updated on: