Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

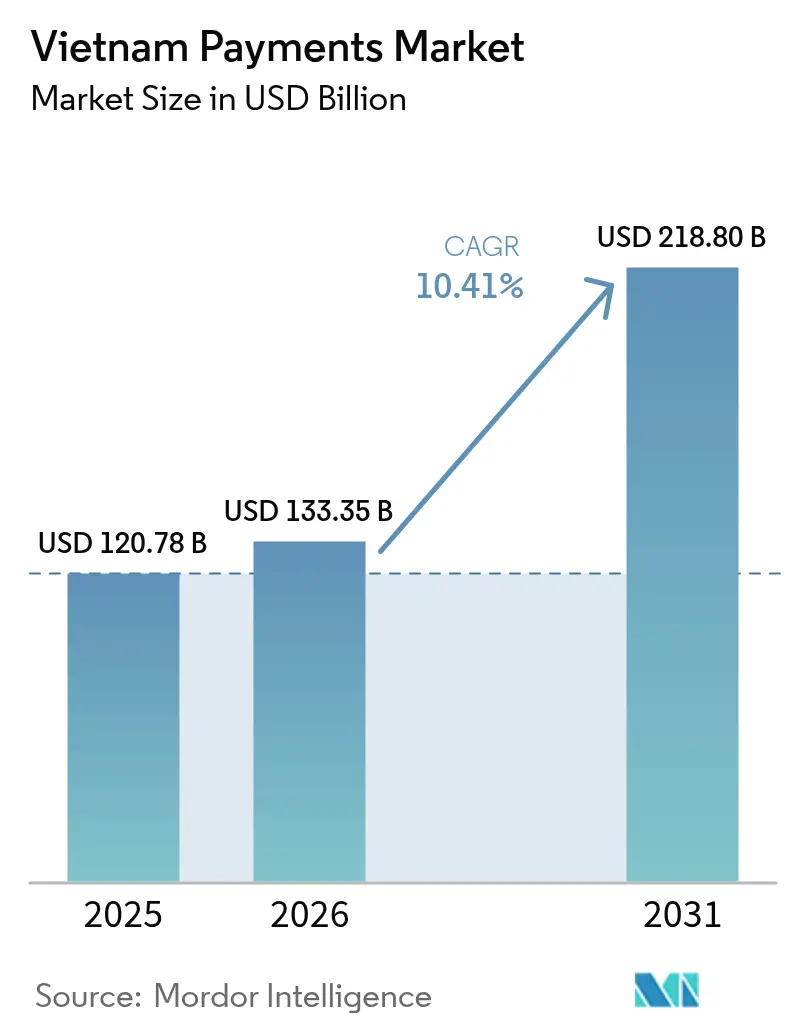

| Base Year Market Size (2025) | USD 120.78 Billion |

| Market Size (2026) | USD 133.35 Billion |

| Market Size (2031) | USD 218.8 Billion |

| Growth Rate (2026 - 2031) | 10.41% CAGR |

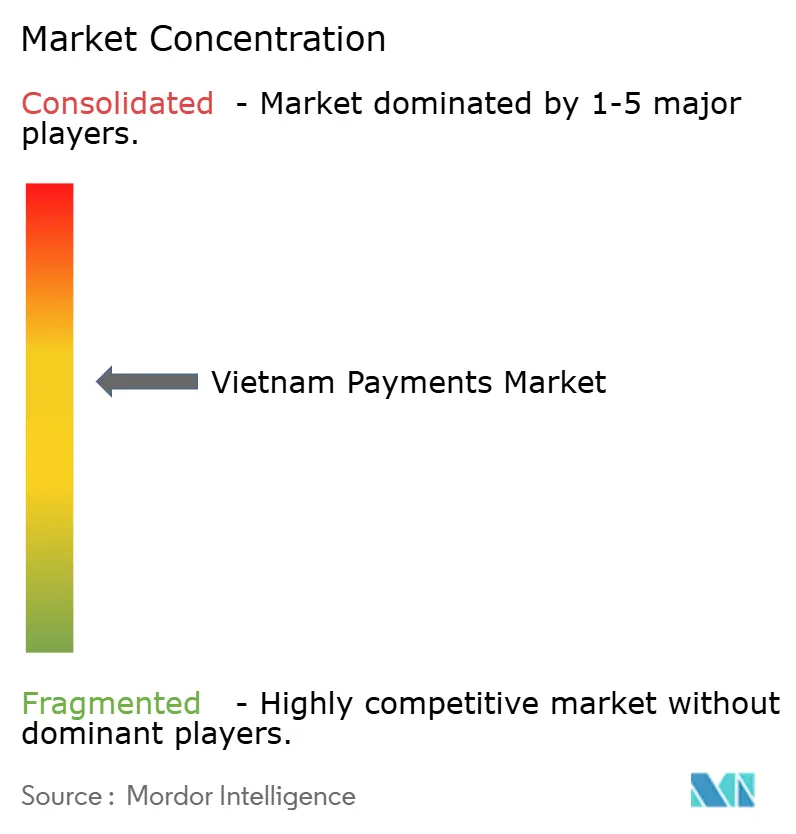

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Payments Market Analysis by Mordor Intelligence

The Vietnam payment market size is expected to grow from USD 120.78 billion in 2025 to USD 133.35 billion in 2026 and is forecast to reach USD 218.8 billion by 2031 at 10.41% CAGR over 2026-2031. Robust e-commerce growth, proliferating real-time rails, and a sustained push from the State Bank of Vietnam (SBV) to achieve 80% cashless transactions by 2030 continue to accelerate adoption. Digital wallets still command the largest share yet account-to-account (A2A) transfers now post the quickest gains as consumers migrate toward VietQR-enabled instant payments. Retail remains the biggest end-user group, but healthcare is growing faster thanks to electronic medical record mandates that embed digital payments into patient workflows. Policy clarity and open-API rules lower entry barriers, intensifying rivalry among local wallets, universal banks, and global card networks. Taken together, these forces position the Vietnam payment market to outpace every other major economy in Southeast Asia through 2030.

Key Report Takeaways

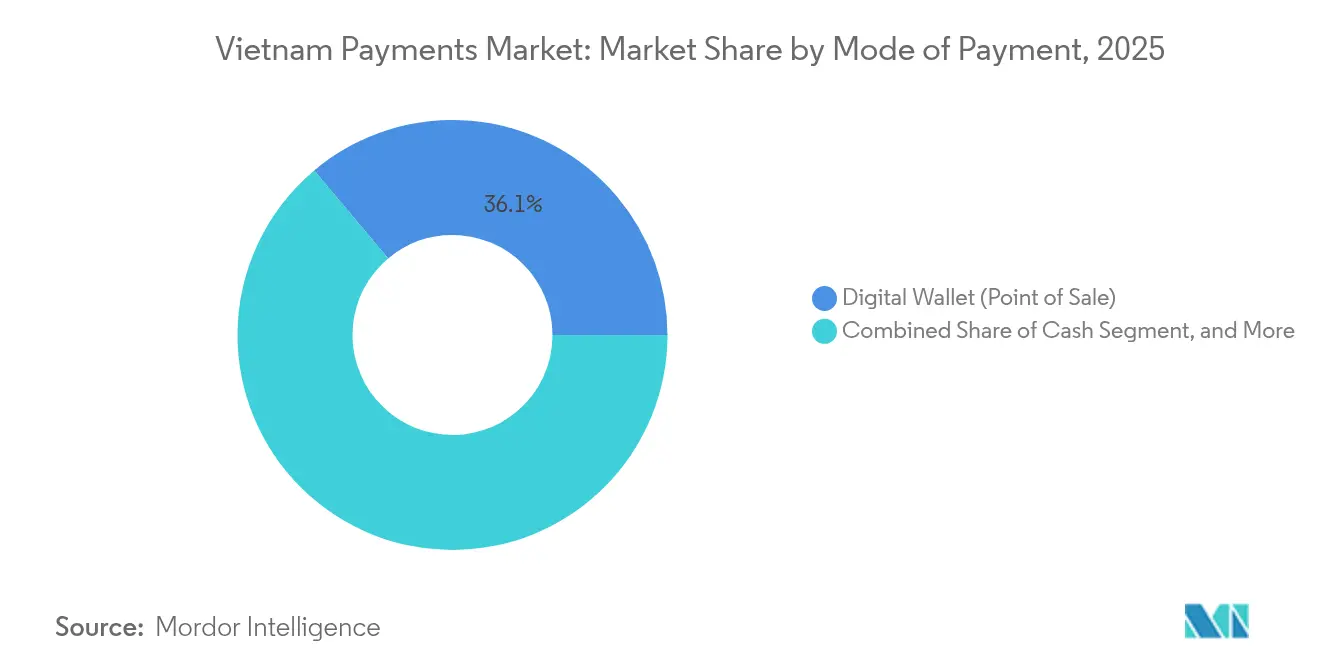

- By mode of payment, digital wallets led with 36.12% of Vietnam payment market share in 2025, while A2A transfers are advancing at an 11.64% CAGR through 2031.

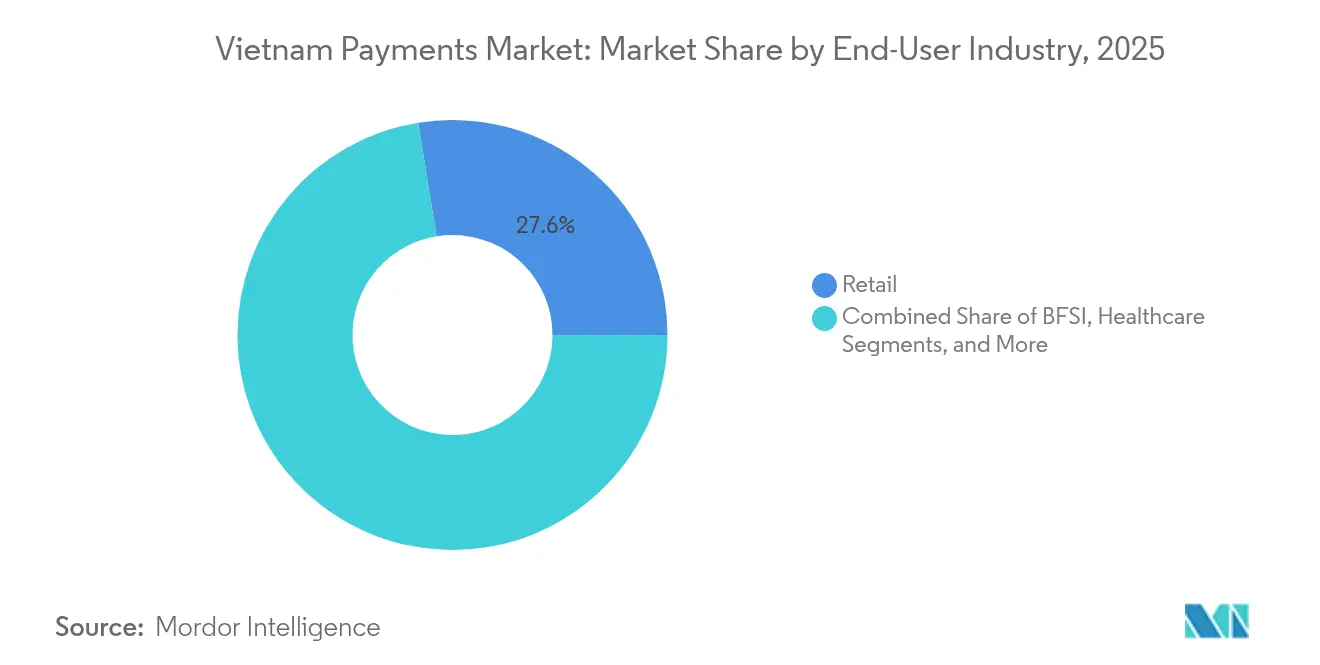

- By end-user industry, retail held 27.55% of Vietnam payment market size in 2025; healthcare is projected to post the fastest 11.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising e-commerce and m-commerce penetration | +2.8% | National, with concentration in Ho Chi Minh City, Hanoi, Da Nang | Medium term (2-4 years) |

| Government cashless-economy programmes | +3.2% | National, with rural focus through Mobile Money initiatives | Long term (≥ 4 years) |

| Expansion of real-time payment rails (Napas 247, VNPay QR) | +2.1% | National infrastructure with urban-first deployment | Short term (≤ 2 years) |

| Social-commerce payments via Zalo/Meta ecosystems | +1.9% | National, with higher penetration in Tier 2-3 cities | Medium term (2-4 years) |

| Embedded finance in super-apps (Grab, Gojek) | +1.7% | Urban centers and major metropolitan areas | Medium term (2-4 years) |

| SME supply-chain digitisation and B2B e-invoicing | +1.5% | National, with focus on enterprises >VND 200 billion revenue | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-commerce and M-commerce Penetration

Vietnamese consumers have shifted decisively toward mobile shopping, with app-based checkouts accounting for a majority of online transactions in 2025. Social-commerce storefronts embedded inside Zalo, Facebook, and TikTok simplify one-click purchasing, reducing reliance on browser redirects.[1]ZaloPay, “Developer API Documentation,” ZALOPAY.Payment providers therefore prioritize API-first architectures that slot easily into these platforms, ensuring high authorization rates and frictionless consumer journeys. Companies such as ZaloPay now bundle seller dashboards, logistics booking, and BNPL options to defend transaction share from cash-on-delivery. As smartphone ownership exceeds 80% in major urban clusters, the Vietnam payment market embeds directly into daily social media use, closing the gap between browsing and buying.

Government Cashless-Economy Programs

The SBV’s National Payment Strategy aims for 80% cashless transactions by 2030, buttressed by Decree 52/2024 that standardizes security, data localization, and interoperability.[2]State Bank of Vietnam, “National Payment Strategy and Regulatory Framework,” SBV.GOV.VN Mobile Money pilots, capped at VND 10 million balances, enrolled 8.8 million users in 2024—72% located in rural provinces underserved by brick-and-mortar banks. These pilots demonstrate that simplified KYC tied to mobile phone numbers can unlock latent demand outside the top cities. By requiring ISO 20022 messaging for all new rails and mandating open APIs, regulators align Vietnam with wider ASEAN standards and give domestic firms a springboard for cross-border scale.

Expansion of Real-time Payment Rails

NAPAS 247 handled 8.9 billion instant transfers in 2024, up 33.8% year on year, making Vietnam a regional leader in 24/7 settlement.[3]National Payment Corporation of Vietnam, “NAPAS 247 Transaction Statistics,” NAPAS.COM.VN Merchant VietQR acceptance has reached 85%, enabling shoppers to scan a single interoperable code regardless of their bank or wallet. Real-time rails now support government fee collection, utility bills, and payroll, widening beyond retail P2M flows. Because the network is ISO 20022-native, Vietnamese providers are technically ready for ASEAN QR linkage, which commenced with Thailand in 2024 and will add Cambodia and Laos next. This infrastructure means the Vietnam payment market can offer cross-border instant transfers at materially lower cost than legacy correspondent banking.

Social-commerce Payments via Zalo/Meta Ecosystems

Livestream sales inside Facebook, Instagram, and Zalo bypass traditional e-commerce checkout pages, creating demand for embedded payment APIs that confirm orders in chat threads. ZaloPay’s Shopify connector extends this embedded approach to global storefront platforms, letting Vietnamese SMEs collect international cards while settling domestically. Larger average order values in livestream sessions encourage wallets to layer financing tools such as pay-later, protecting share from card issuers. As Decree 52/2024 compels stronger customer authentication, entrenched social platforms enjoy scale advantages in fraud prevention, raising entry thresholds for niche wallets and new-to-market fintechs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Entrenched cash culture in rural provinces | -1.4% | Rural provinces, particularly Mekong Delta and Northern mountains | Long term (≥ 4 years) |

| Limited e-wallet and QR code interoperability | -0.8% | National, with higher impact in competitive urban markets | Medium term (2-4 years) |

| Escalating A2A payment fraud and regulatory throttling | -1.1% | National, with concentration in high-volume urban transactions | Short term (≤ 2 years) |

| Data-sovereignty hurdles for foreign PSPs | -0.6% | National, affecting international payment service providers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Entrenched Cash Culture in Rural Provinces

Cash remains dominant in remote areas where patchy network coverage and low smartphone adoption hamper digital migration. Agricultural households in the Mekong Delta favor tangible currency that aligns with irregular harvest income, and many merchants resist transaction fees that accompany card or wallet acceptance. SBV-driven digital literacy programs and telecom rollouts aim to narrow the gap, yet cultural preferences and concerns over data privacy slow progress. Even so, Mobile Money’s rapid uptake hints that low-friction, phone-number-based services can gradually displace cash if reinforced by agent networks and bill-payment use cases.

Limited E-wallet and QR Code Interoperability

While VietQR unites the banking sector, proprietary wallet codes still fragment acceptance, forcing small merchants to juggle multiple stickers and settlement dashboards. MoMo’s deep user base and ZaloPay’s social graph both lock consumers into walled gardens that complicate universal acceptance. The forthcoming Open-API circular, slated for 2026, will oblige licensees to open transfer and balance endpoints, but implementation remains two years away. Until then, merchants incur duplicate integration costs that weigh heavier on micro-SMEs, and consumers face inconsistent cashback and fee structures that sometimes nudge them back to cash.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: Digital Wallets Lead While A2A Transfers Accelerate

Digital wallets captured 36.12% of Vietnam payment market share in 2025 on the back of MoMo’s 69% and ZaloPay’s 44% user penetration. However, A2A payments are forecast to grow at an 11.64% CAGR, buoyed by VietQR’s 85% merchant reach and NAPAS 247’s 8.9 billion annual transactions. This migration toward real-time bank transfers reduces top-up friction and merchant MDRs, making wallets compete on value-added services instead of closed-loop balance storage. Vietnam payment market size for A2A flows is projected to more than double by 2031 as consumers trust direct bank connections and enjoy instant refunds and charge-back parity.

POS card usage still accounts for significant volume, with debit acceptance at 95% of stores, but credit still lags because prudential capital rules deter aggressive card issuance. Cash-on-delivery retains around 30% share of rural e-commerce checkouts, though this proportion erodes each year as Mobile Money expands. Decree 52/2024’s enhanced authentication rules play to the strengths of established banks that already comply with multifactor protocols, accelerating wallet-to-bank substitution. By 2030, analysts expect wallets to act primarily as orchestration layers, routing payments to real-time rails beneath rather than holding user deposits.

By End-User Industry: Healthcare Digitization Outpaces Retail Growth

Retail commanded 27.55% of Vietnam payment market size in 2025, sustained by high QR acceptance at convenience stores and supermarkets. Yet healthcare is on track for an 11.17% CAGR thanks to government mandates that 71% of hospitals now satisfy. Direct bank connections support 31.4% of hospitals, while alternative channels such as kiosks linked to Mobile Money cover a further 15.4%. These integrations shrink checkout times and cut administrative overhead, giving hospital managers a clear ROI.

Entertainment and hospitality rebound alongside inbound tourism and now incorporate tokenized card-on-file models that travelers trust. Visa’s 2024 consumer survey found 48% of outbound Vietnamese tourists plan cashless trips, encouraging hotels and airlines to integrate multiple wallets. Transport continues its steady climb, with ride-hailing operators embedding MoMo and ZaloPay to secure frictionless hand-offs between ordering, navigation, and payment. Finally, government e-invoicing thresholds push B2B corporates into automated accounts-payable flows, broadening revenue streams for treasury-focused fintechs beyond consumer retail.

Geography Analysis

Ho Chi Minh City and Hanoi together generate 60% of Vietnam payment market transaction value while hosting only 25% of the population. Urban merchants post 95% digital acceptance, backed by fiber networks and dense banking footprints. Conversely, Mobile Money’s 8.8 million users skew 72% rural, demonstrating that simplified, SIM-based accounts thrive where smartphones and bank branches are scarce.

Cross-border ties push the Vietnam payment market beyond domestic confines. 2024’s QR interoperability with Thailand enables tourists to scan VietQR codes overseas and vice versa, and ASEAN working groups plan Cambodian and Lao links next. Digital remittances into Vietnam reached USD 15.9 billion in 2024, 6.2% of GDP, underscoring the economy’s integration into migrant labor corridors.

Decree 52/2024 imposes uniform technical standards nationwide, but readiness varies. Tier-2 cities such as Da Nang, Can Tho, and Hai Phong now exhibit adoption curves that mirror Hanoi’s 2019 baseline, helped by public-private fiber projects and SBV subsidies for merchant POS kits. Meanwhile, the Mekong Delta lags as cash crops and fragmented logistics inhibit digital uptake. Government telecom build-outs scheduled through 2027 aim to close this gap, pairing 4G coverage with payments training at community banks.

Competitive Landscape

The Vietnam payment market displays moderate concentration: the top five providers control a combined share near 60%, balancing wallet scale against bank incumbency. MoMo’s 69% active wallet penetration leads, followed by ZaloPay’s 44%, while VNPay leverages a bank consortium model to retain merchant QR share. Domestic banks, VietinBank, Agribank, BIDV, still settle the lion’s share of salary, loan, and utility transactions, wielding capital heft and regulatory familiarity.

2024 saw Visa ink three-way deals with MoMo, VNPay, and ZaloPay that extend card tokenization into wallet apps and enable outbound cross-border QR scanning. These alliances blur the lines between cards and wallets, positioning Visa as an embedded infrastructure layer rather than a standalone scheme. NAPAS, for its part, speeds up API rollouts that allow smaller fintechs to build payroll or subscription services without deep core-bank links.

White-space niches persist. B2B payment automation remains under-served, with only 15% of large corporates using integrated payables engines. Healthcare kiosks, rural agent networks, and export-oriented SMEs also sit on the product roadmap of both banks and fintechs. The forthcoming open-API framework is expected to compress onboarding times from months to days, lowering barriers for cloud-native entrants eager to specialize in vertical niches.

Vietnam Payments Industry Leaders

VietinBank Group

Vietnam Bank for Agriculture and Rural Development

Bank for Investment and Development of Vietnam

PayPal Holdings Inc.

M Service JSC (MoMo)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: HDBank extended MediPay kiosks to 150 hospitals, automating payment capture and record retrieval.

- November 2024: ZaloPay integrated with Shopify, letting Vietnamese merchants collect foreign cards and settle locally.

- October 2024: VNPay launched B2B payables tools to aid firms affected by mandatory e-invoice rules.

- September 2024: Grab deepened wallet ties with MoMo and ZaloPay, unifying mobility checkout across super-app channels.

Vietnam Payments Market Report Scope

The Vietnam Payments Market is Segmented by Mode of Payment (Point of Sale (Card Payments, Digital Wallet, Cash), Online Sale (Card Payments, Digital Wallet)), and by End-user Industries (Retail, Entertainment, Healthcare, Hospitality). or POS, all transactions made on physical sales are within the market range of credit or debit card payments. This includes all face-to-face transactions, not just traditional in-store transactions, regardless of location. In both cases, cash payments are also an option for e-commerce sales.

By Mode of Payment

| Point of Sale | Debit Card Payments |

| Credit Card Payments | |

| Account-to-Account (A2A) Payments | |

| Digital Wallet | |

| Cash | |

| Other PoS Modes | |

| Online Sale | Debit Card Payments |

| Credit Card Payments | |

| Account-to-Account (A2A) Payments | |

| Digital Wallet | |

| Cash-on-Delivery | |

| Other Online Modes |

By End-User Industry

| Retail |

| Entertainment |

| Hospitality |

| Healthcare |

| Transport and Logistics |

| Other Industries |

| By Mode of Payment | Point of Sale | Debit Card Payments |

| Credit Card Payments | ||

| Account-to-Account (A2A) Payments | ||

| Digital Wallet | ||

| Cash | ||

| Other PoS Modes | ||

| Online Sale | Debit Card Payments | |

| Credit Card Payments | ||

| Account-to-Account (A2A) Payments | ||

| Digital Wallet | ||

| Cash-on-Delivery | ||

| Other Online Modes | ||

| By End-User Industry | Retail | |

| Entertainment | ||

| Hospitality | ||

| Healthcare | ||

| Transport and Logistics | ||

| Other Industries | ||

Key Questions Answered in the Report

What is the 2026 size of the Vietnam payment market?

It stands at USD 133.35 billion, rising toward USD 218.8 billion by 2031.

Which payment method is growing fastest in Vietnam?

Account-to-account (A2A) transfers, projected to expand at an 11.64% CAGR through 2031.

Why is healthcare a high-growth payment vertical?

Regulatory mandates require electronic medical records and digital payments in 71% of hospitals, driving an 11.17% CAGR.

How are regulators fostering cashless adoption?

Through Decree 52/2024, open-API standards, and Mobile Money pilots targeting 80% cashless transactions by 2030.

Which cities lead digital payment volume?

Ho Chi Minh City and Hanoi generate 60% of transaction value thanks to near-universal merchant acceptance.

Page last updated on: