Vietnam Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

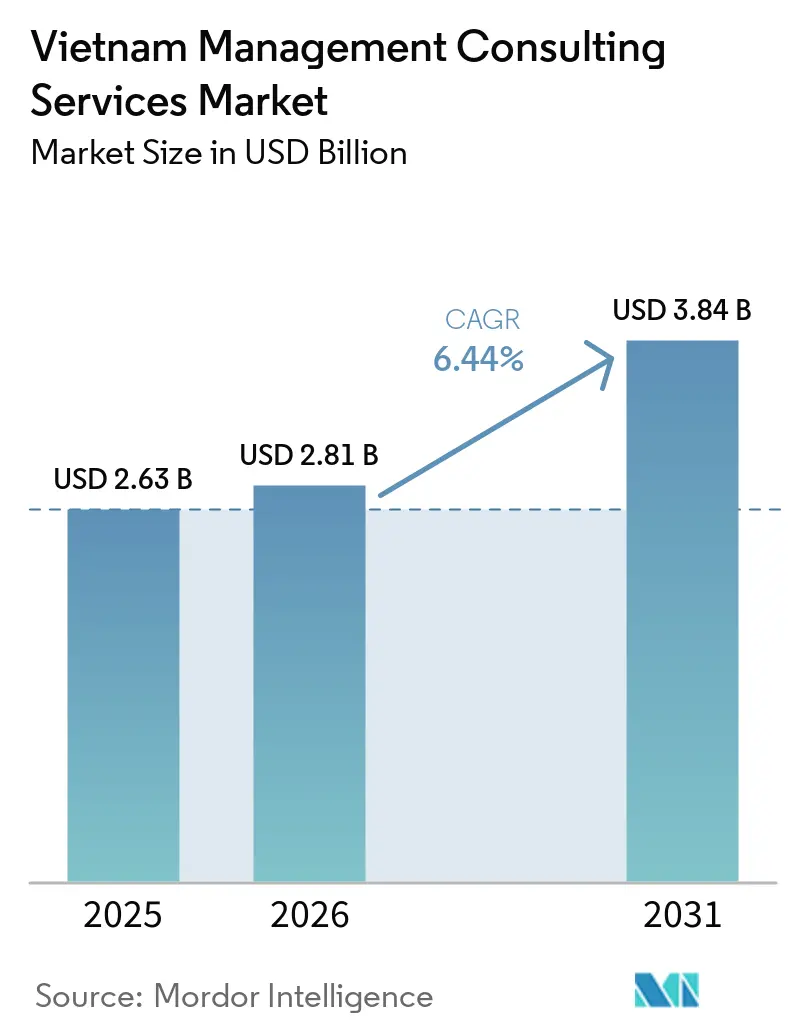

| Base Year Market Size (2025) | USD 2.63 Billion |

| Market Size (2026) | USD 2.81 Billion |

| Market Size (2031) | USD 3.84 Billion |

| Growth Rate (2026 - 2031) | 6.44% CAGR |

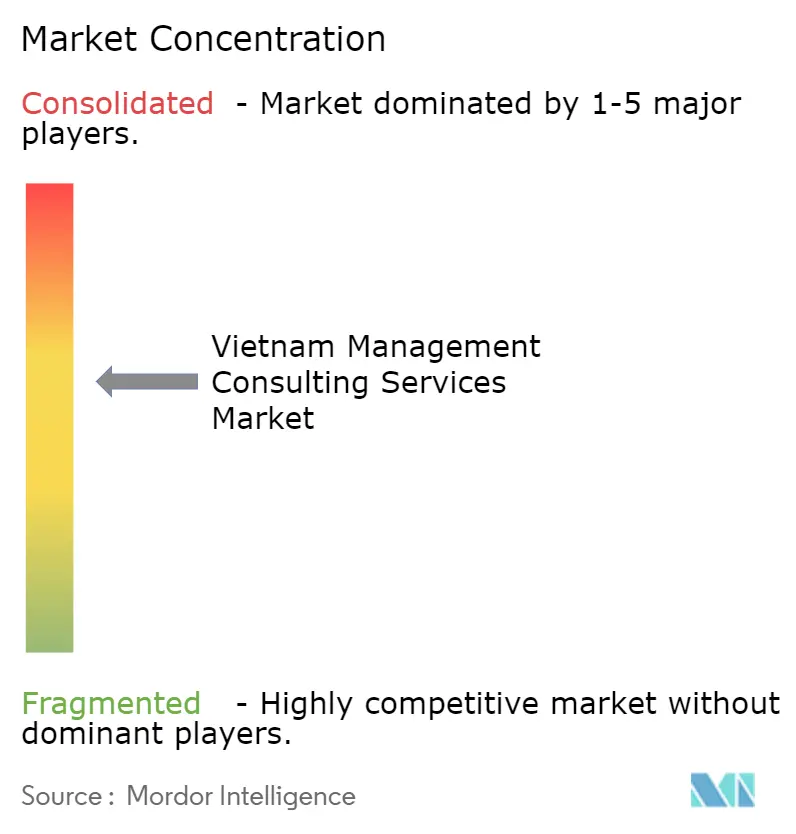

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Management Consulting Services Market Analysis by Mordor Intelligence

The Vietnam management consulting services market size was valued at USD 2.63 billion in 2025 and is estimated to grow from USD 2.81 billion in 2026 to reach USD 3.84 billion by 2031, at a CAGR of 6.44% during the forecast period (2026-2031). A surge in high-quality foreign direct investment, the government’s aggressive 10% GDP growth ambition for 2026 and an expanding digital-savvy domestic enterprise base are jointly driving demand for specialized advisory. Manufacturing captured more than 70% of first-quarter 2026 FDI capital, channeling immediate opportunities toward operations optimization, factory relocation planning and compliance services. Decision 433/QD-TTg is accelerating digital transformation funding for half a million small and medium enterprises, while newly enforced data-residency rules are reshaping technology stack choices and creating fertile ground for in-country advisory on privacy, cybersecurity and data governance. Collectively, these factors reinforce a positive growth outlook for the Vietnam management consulting services market as clients shift from single-function projects to integrated strategy, technology and compliance engagements.

Key Report Takeaways

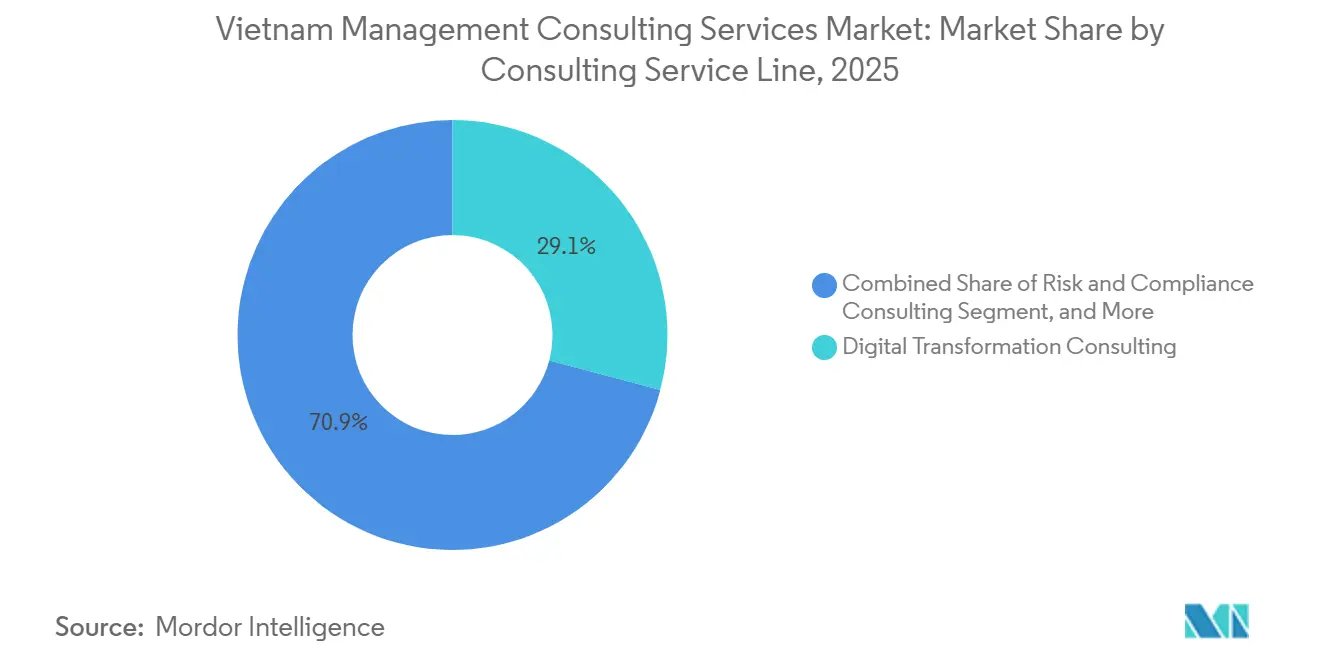

- By consulting service line, digital transformation consulting led with 29.12% of Vietnam management consulting services market share in 2025, while risk and compliance consulting is projected to record the fastest 6.78% CAGR through 2031.

- By organization size, large enterprises accounted for 62.87% of the Vietnam management consulting services market in 2025, whereas the small and medium-sized enterprise segment is forecast to expand at a 6.51% CAGR between 2026-2031.

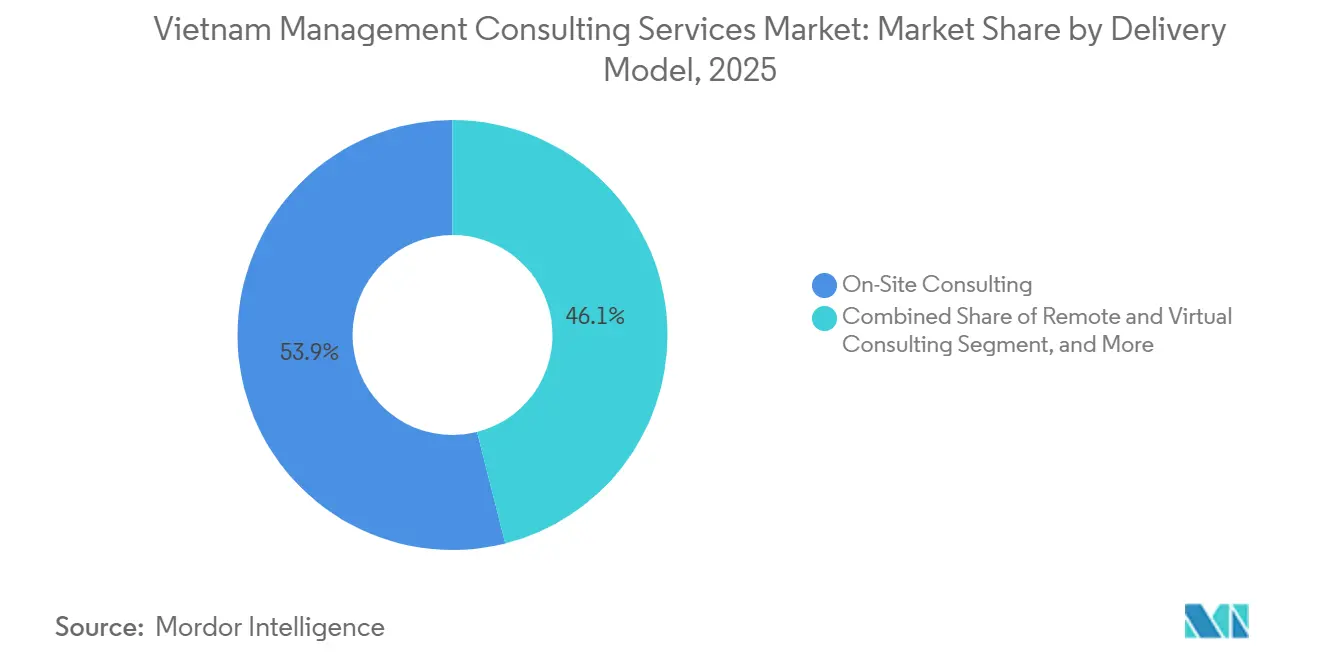

- By delivery model, on-site consulting commanded 53.94% revenue share in 2025, yet the hybrid model is poised to advance at the highest 6.83% CAGR during the same period.

- By end-user industry, manufacturing secured a 21.48% slice of the Vietnam management consulting services market size in 2025 and healthcare is expected to achieve the quickest 6.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Transformation Agenda Among Vietnamese Enterprises | +1.2% | Nationwide, strongest in Ho Chi Minh City, Hanoi, Da Nang | Medium term (2-4 years) |

| Growing Foreign Direct Investment Requiring Strategic Advisory | +1.1% | Red River Delta and Southeast Region | Short term (≤ 2 years) |

| Regional Semiconductor Supply-Chain Incentives Driving Advisory Demand | +0.8% | High-tech zones in Thu Duc, Bac Ninh, Hai Phong | Long term (≥ 4 years) |

| Mandatory ESG Reporting Under Vietnam Stock Exchange Sustainability Guidelines | +0.7% | Listed firms in Hanoi and Ho Chi Minh City | Medium term (2-4 years) |

| Government Reforms and SOE Privatization Initiatives | +0.6% | Energy, telecom and infrastructure sectors nationwide | Medium term (2-4 years) |

| Rapid Expansion of Vietnam's Manufacturing Export Base | +0.9% | Southeast Region, Red River Delta, North Central Coast | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Digital Transformation Agenda Among Vietnamese Enterprises

Decision 433/QD-TTg approved in March 2026 earmarks co-financing that covers up to 50% of eligible technology spending, stimulating a subsidized pipeline of advisory engagements. Standardized digital maturity criteria released in June 2025 now anchor consulting scopes to measurable outcomes, boosting demand for structured readiness assessments and change-management roadmaps. A national survey conducted mid-2025 found 69% of firms at only basic digital adoption, revealing a vast addressable market for consultants that can integrate artificial intelligence, cloud and analytics solutions. Early movers that align service offerings with the government’s 25 industry-group framework are winning preferred-vendor status and locking in multi-year contracts. The policy’s emphasis on skills transfer and local capacity building also encourages blended delivery teams, widening participation for domestic specialists alongside global firms.[1]Điện tử và Ứng dụng, “Phê duyệt Đề án chuyển đổi số,” dientungaynay.vn

Growing Foreign Direct Investment Requiring Strategic Advisory

Registered FDI capital surged 42.9% year-on-year in Q1 2026 to USD 15.2 billion, with manufacturing attracting more than 70% of inflows.[2]Vietnam Investment Review, “FDI inflows surge 42.9% in Q1 2026,” vir.com.vn Resolution 306/NQ-CP reorganizes Vietnam into six socio-economic regions and prioritizes high-tech, environmentally aligned projects, obliging investors to seek counsel on industrial-park selection, ESG compliance and incentives qualification. Streamlined licensing under the 2025 Investment Law allows 100% foreign-owned consulting entities, yet niche service lines such as construction advisory still require local practicing certificates, creating demand for regulatory-navigation specialists. State-affiliated players such as Vietnam Post Logistics are bundling legal, customs and site-selection support, intensifying competition and raising the bar on integrated, one-stop service propositions. Consultants versed in supply-chain localization and green permitting are positioned to capture premium FDI-linked assignments over the next two years.

Regional Semiconductor Supply-Chain Incentives Driving Advisory Demand

Corporate income tax concessions as low as 5% for up to 37 years, extensive land-rent exemptions and fast-tracked licensing are turning Vietnam into a preferred assembly, testing and packaging base for semiconductors. The January 2026 joint venture between FPT and Viettel to build the country’s first semiconductor testing plant underscores a new wave of complex, capital-intensive projects that rely on consultants for feasibility studies, workforce planning and factory layout optimization. Decrees under Resolution 57 grant high-tech zones in Thu Duc, Bac Ninh and Hai Phong priority access to infrastructure funding, yet complicated multi-agency approvals and severe engineering talent shortages necessitate end-to-end project-management advisory. International quality benchmarks such as IATF 16949 and ISO 9001 further raise the need for niche process-engineering expertise, anchoring multi-stage consulting relationships that can span well beyond the initial build-out phase.[3]Vietnam Investment Review, “Vietnam semiconductor incentives 2025,” vir.com.vn

Mandatory ESG Reporting Under Vietnam Stock Exchange Sustainability Guidelines

Vietnam’s evolving ESG disclosure regime now requires listed companies to report on greenhouse gas emissions, labor standards, board diversity and anti-corruption practices. Many issuers lack systems to collect and verify the necessary data, creating opportunities for consultants specializing in materiality assessments, data analytics and assurance readiness. The parallel growth of green bonds and sustainability-linked loans heightens the importance of accurate, third-party-verified metrics, enabling advisory firms to bundle ESG strategy with capital-market access services. Privatizing state-owned enterprises, under scrutiny from strategic buyers, are mandated to demonstrate governance improvements, further enlarging the advisory pool. Integration of ESG with digital dashboards and automated reporting tools distinguishes firms able to cross-sell compliance, risk and technology services in one engagement.[4]Baker McKenzie, “Vietnam ESG reporting requirements,” bakermckenzie.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Senior Consulting Talent Locally | -0.9% | Hanoi, Ho Chi Minh City, Da Nang | Short term (≤ 2 years) |

| New 2025 Data-Residency Rules Increasing Compliance Costs | -0.6% | Nationwide, heavier on multinational firms | Medium term (2-4 years) |

| Price Sensitivity Among SMEs | -0.4% | Rural and lower-tier cities | Medium term (2-4 years) |

| Cultural Preference for In-House Solutions in Family-Owned Firms | -0.3% | Traditional manufacturing and retail sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Senior Consulting Talent Locally

Attrition levels of 24-28% in outsourcing hubs and a 94-day average to fill senior roles constrain the scale-up capacity of both domestic and global firms. A 43% salary gap between local and multinational employers spurs talent migration to regional financial centers, hollowing out leadership benches in Hanoi and Ho Chi Minh City. Government ambitions to certify 1,000 digital advisors and train 50,000 semiconductor engineers will help, but pipeline maturation takes time, forcing firms to invest in rapid upskilling and retention incentives. Hybrid delivery models pairing junior local analysts with offshore experts mitigate shortages yet risk weakening client intimacy and contextual insight. Scarcity is most acute in semiconductor process engineering, clinical-trials regulatory affairs and advanced cybersecurity, extending project timelines and elevating labor costs.[5]World Bank, “Vietnam Development Report 2024,” worldbank.org

New 2025 Data-Residency Rules Increasing Compliance Costs

The Law on Data and Personal Data Protection Law require that certain data sets be stored on servers located within Vietnam, impose steep penalties for violations and mandate a local representative for data-protection matters.[6]Baker McKenzie, “Vietnam data law compliance guide,” bakermckenzie.com Multinational consultancies reliant on global cloud platforms must therefore fund localized infrastructure, conduct data-flow audits and hire compliance staff, eroding margins on smaller assignments. Domestic firms with in-country data centers, most notably FPT Digital and Viettel Consulting, leverage this regulation to market compliance-ready solutions, gaining a competitive tilt in public-sector and state-owned enterprise bids. Ambiguity in defining “important” versus “personal” data breeds legal risk that clients shift back to external advisors through broader indemnity clauses, prolonging sales cycles. Over the medium term, higher operational costs could temper foreign entrants’ appetite for aggressive expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Digital Leads While Compliance Gains Pace

Digital transformation engagements held 29.12% of Vietnam management consulting services market share in 2025, underpinned by the state-subsidized push to onboard 500,000 small and medium enterprises onto digital platforms. That ceiling is far from reached, and demand remains buoyant as only 10% of companies have integrated artificial intelligence into core workflows. Risk and compliance consulting, although smaller today, is projected to chart a 6.78% CAGR through 2031, fueled by anti-money laundering regulations and heightened stress-testing mandates in banking. Strategy consulting continues to attract large state-owned enterprises exploring privatization pathways, and operations consulting supports electronics and textile exporters striving for yield optimization in a cost-sensitive landscape. Meanwhile, human-capital advisory gains relevance as Decree 335/2025 imposes competency-based performance evaluation, prompting firms like VietEZ to roll out KPI platforms across public-sector units.

A pivot toward bundled offerings is reshaping competitive positions. KPMG’s “Vietnam 2026 Outlook” report, for instance, packages macroeconomic forecasts with sector-specific digital roadmaps, signaling that multidomain service suites resonate with clients navigating synchronized challenges. Sustainability advisory, once peripheral, is gaining traction as listed corporations prepare for stricter ESG disclosure, while semiconductor project sponsors increasingly demand factory-readiness blueprints that blend engineering standards, workforce planning and supplier qualification. Collectively, these factors sustain a robust pipeline for cross-disciplinary engagements and reinforce the ascendancy of digital and compliance-centric practices within the Vietnam management consulting services market.

By Organization Size: Corporate Heavyweights Dominate, SMEs Gather Momentum

Large enterprises retained 62.87% share of the Vietnam management consulting services market in 2025, anchored by multinational manufacturers relocating capacity to Vietnam’s industrial parks and state-owned giants restructuring under Decree 57/2026. They command multiphase engagements, from carve-out modeling to post-merger integration and large ERP upgrades that consume extensive consulting hours. Small and medium-sized enterprises, however, are projected to register a 6.51% CAGR, catalyzed by cost-sharing programs that reimburse up to half of qualified digital investments. Although price sensitivity hampers adoption, modular advisory products, subscription CRM deployments, phased analytics rollouts, lower entry thresholds and improve retention.

Retention, nevertheless, remains a challenge. A World Bank study shows that SME consulting usage drops from 80% in the first project year to 35% after 18 months, primarily due to limited absorptive capacity and cash-flow constraints. To offset this churn, advisory firms are piloting freemium diagnostics and micro-engagements that prove value before scaling. Family-owned businesses, which dominate Vietnam’s economy, reveal significant governance gaps, 81% report intra-family conflict, unleashing demand for succession planning, yet cultural preference for keeping matters in-house tempers uptake. Advancements in cloud-based software-as-a-service further democratize access, letting consultants bundle technology licenses with advisory retainers, strategically positioning the Vietnam management consulting services market for wider SME penetration.

By Delivery Model: Hybrid Consulting Surges in a Flexible Work Era

On-site delivery accounted for 53.94% of Vietnam management consulting services market revenue in 2025, reflecting enduring client expectations for face-to-face collaboration on intricate transformations such as factory relocation and regulatory audits. Yet hybrid consulting is forecast to escalate at a 6.83% CAGR as enterprises embrace distributed work, illustrated by Sacombank’s nationwide hybrid workplace model launched in March 2026. Remote collaboration platforms now facilitate virtual workshops, real-time data sharing and digital-twin simulations, enabling consultants to conduct supply-chain diagnostics without stepping onto factory floors.

Data-residency regulations, enforced from 2025-2026, inadvertently reinforce hybrid uptake by compelling foreign firms to establish local infrastructure that supports secure, in-country processing for virtual engagements. Industries dealing with sensitive data, banking, insurance and healthcare, still insist on selective on-site presence for critical phases, maintaining a baseline demand for physical interaction. Global networks take advantage by pairing senior offshore partners with teams of local analysts, reducing travel expense but necessitating disciplined knowledge-transfer protocols to uphold client intimacy. The mix of convenience, cost reduction and compliance obligations positions hybrid delivery as a structural growth driver for the Vietnam management consulting services market.

By End-User Industry: Manufacturing Anchors, Healthcare Accelerates

Manufacturing represented 21.48% of Vietnam management consulting services market size in 2025, mirroring Vietnam’s ascent as a regional assembly hub across electronics, textiles and consumer goods. The sector’s appetite for lean implementation, yield improvement and reshoring analysis keeps operations and supply-chain advisory pipelines full. Concurrently, healthcare is on track for the fastest 6.72% CAGR as clinical-trials expansion and telemedicine growth demand help navigating regulatory changes, data security and hospital IT modernization. Banks and insurers are another major consulting consumer as Circular 83/2025 compels Three Lines of Defense frameworks and advanced stress testing, spurring a rush for risk, compliance and capital-adequacy expertise.

Energy and resources operators, particularly in the Mekong Delta, seek project-finance structuring for wind and solar installations and must address stringent environmental-impact assessments, broadening the advisory canvas. Public-sector bodies leverage consultants to execute widescale digital initiatives, such as Electricity Corporation of Vietnam’s overhaul of internal governance, customer service and data management. Retail and logistics clients, riding urbanization and e-commerce waves, turn to omnichannel strategy and supply-chain optimization services. The upshot is a balanced demand spectrum that cushions the Vietnam management consulting services market against cyclicality in any one vertical.

Geography Analysis

Ho Chi Minh City and the wider Southeast Region remain the commercial heartland of the Vietnam management consulting services market, with the city’s digital economy contributing 22% of gross regional domestic product and catalyzing advisory needs in smart-logistics, ecological industrial-park development and public-private partnership design. Boston Consulting Group’s long-standing Ho Chi Minh City base and Bain’s 2023 office opening attest to sustained client concentration in the south. Hanoi and the broader Red River Delta captured 49.2% of FDI capital in the first eight months of 2025, driving strong uptake for supply-chain integration, supplier upgrading and ESG compliance services as automotive and electronics clusters scale up.

Secondary hubs are gathering mass. Da Nang, Nghi Son and Vung Ang leverage deep-water ports and low-cost talent pools to attract logistics and foundational-industry projects, though consultant capacity is curtailed by higher attrition. The Mekong Delta shapes a niche consulting market for renewable energy feasibility, agro-processing optimization and climate-resilience planning aligned with government green-growth priorities. Central Highlands provinces, rich in hydropower and minerals, represent smaller but rising demand centers focused on high-tech agriculture and disaster-risk mitigation.

Real-estate dynamics provide further impetus. Grade-A central business district office rents in Ho Chi Minh City averaged USD 62.09 per square meter per month in Q2 2025, encouraging tenants to migrate to fringe locations at USD 40.70. Over 287,000 square meters of fresh Grade-A supply slated for 2025-2027 opens opportunities for workplace strategy, lease-renegotiation and smart-building integration advisory. Overall, revenue dispersion will continue to mirror FDI flows, infrastructure rollout and digital-policy implementation, ensuring that the Vietnam management consulting services market retains a two-tier geographical structure where Hanoi and Ho Chi Minh City dominate but emerging corridors steadily enlarge their share.

Competitive Landscape

The Vietnam management consulting services market is moderately concentrated. Global strategy houses, McKinsey, Boston Consulting Group and Bain, along with Big Four networks command the premium segment, supported by brand credibility and deep sectoral playbooks. Local champions such as FPT Digital and Viettel Consulting leverage proximity, language advantages and in-country data centers to win mid-market and government contracts. Bain’s 2023 Ho Chi Minh City launch and Boston Consulting Group’s 2024 Hanoi office signal unwavering confidence in Vietnam’s growth trajectory, while KPMG’s appointment of a new Head of Deal Advisory underlines a strategic pivot toward transaction-driven mandates.

Technology is the new battleground. Firms embed artificial-intelligence-powered analytics into supply-chain optimization, demand forecasting and risk modeling, differentiating service depth. State-affiliated Vietnam Post Logistics bundles legal, customs and supply-chain advice in a one-stop format, challenging traditional consultants on price and speed. Domestic providers benefit from data-residency regulations that complicate foreign firms’ centralized platform usage, enhancing their competitive position in sensitive government and state-owned enterprise work.

Consolidation remains measured. CSTS Enterprises’ acquisition and rebrand to Conduca in February 2026 is one of the few notable deals, suggesting that organic growth and alliances outpace mergers in shaping the competitive map. Niches such as semiconductor process engineering, clinical-trials regulatory navigation and climate-risk advisory exhibit undersupply, offering white-space for specialists willing to invest in talent and certifications. The collective market behavior yields a concentration score of 6, reflecting that the top five consultancies control slightly more than 60% of sector revenue while numerous mid-size and boutique firms thrive in specialized pockets.

Vietnam Management Consulting Services Industry Leaders

McKinsey and Company Vietnam Company Limited

Boston Consulting Group Vietnam Company Limited

Bain and Company (Asia) Pte. Ltd. – Vietnam

Deloitte Consulting (Vietnam) Co., Ltd.

PwC Vietnam Consulting Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Andersen Consulting and Kyanon Consulting formed a strategic alliance to deliver digital-transformation advisory aimed at small and medium enterprises.

- February 2026: CSTS Enterprises integrated HN Consulting and rebranded as Conduca to expand capacity in public-sector digital-transformation and ESG engagements.

- February 2026: VietBank partnered with KPMG Vietnam to establish a transaction-management office supporting its digital roadmap and Circular 83/2025 compliance.

- February 2026: CETA Consulting joined the Leaders for Growth programme to strengthen SME governance and market-access advisory services.

Vietnam Management Consulting Services Market Report Scope

The Vietnam Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current Vietnam management consulting services market size and expected growth?

The market stood at USD 2.63 billion in 2025 and is projected to reach USD 3.84 billion by 2031, reflecting a 6.44% CAGR over 2026-2031.

Which consulting service line is largest in Vietnam?

Digital transformation consulting led with 29.12% market share in 2025 due to government-backed subsidies and standardized maturity frameworks.

Why is risk and compliance consulting growing quickly?

Circular 27/2025 and Circular 83/2025 tighten anti-money laundering controls and mandate stress testing, pushing banks and corporates to seek specialized advisors.

How are data-residency rules affecting foreign consultancies?

Laws effective from 2025-2026 require in-country data storage, increasing infrastructure costs for multinationals but favoring domestic firms with local data centers.

Which regions generate the most consulting demand in Vietnam?

Ho Chi Minh City and the Red River Delta dominate due to high FDI inflows, large corporate headquarters and expansive infrastructure pipelines.

What delivery model is growing fastest?

Hybrid consulting is forecast to advance at a 6.83% CAGR as enterprises adopt flexible work setups supported by secure virtual-collaboration platforms.

Page last updated on: