Asia Pacific Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

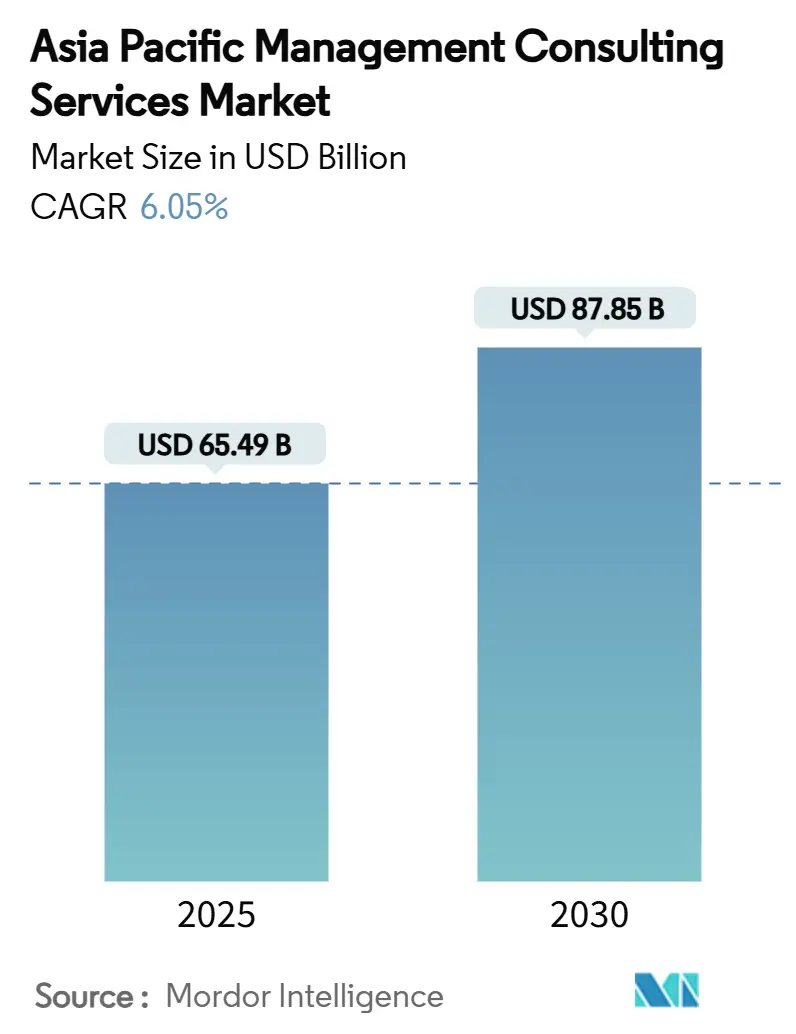

| Market Size (2025) | USD 65.49 Billion |

| Market Size (2030) | USD 87.85 Billion |

| Growth Rate (2025 - 2030) | 6.05% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia Pacific Management Consulting Services Market Analysis by Mordor Intelligence

The Asia Pacific management consulting services market size stands at USD 65.49 billion in 2025 and is projected to reach USD 87.85 billion by 2030, translating into a 6.05% CAGR over the forecast period. Strong enterprise appetite for digital transformation, rising regulatory complexity, and an expanding base of small and mid-sized clients collectively sustain momentum across the region. Government-backed e-government and industry 4.0 programs anchor demand for implementation expertise, while boardroom focus on operational resilience and net-zero supply chains enlarges the advisory addressable base. The financial services sector sets a high bar for compliance consulting, and AI-driven productivity mandates among large enterprises propel technology consulting uptake. In parallel, skill shortages and wage inflation temper near-term expansion, yet hybrid delivery models soften margin pressure by widening access to cross-border talent pools.

Key Report Takeaways

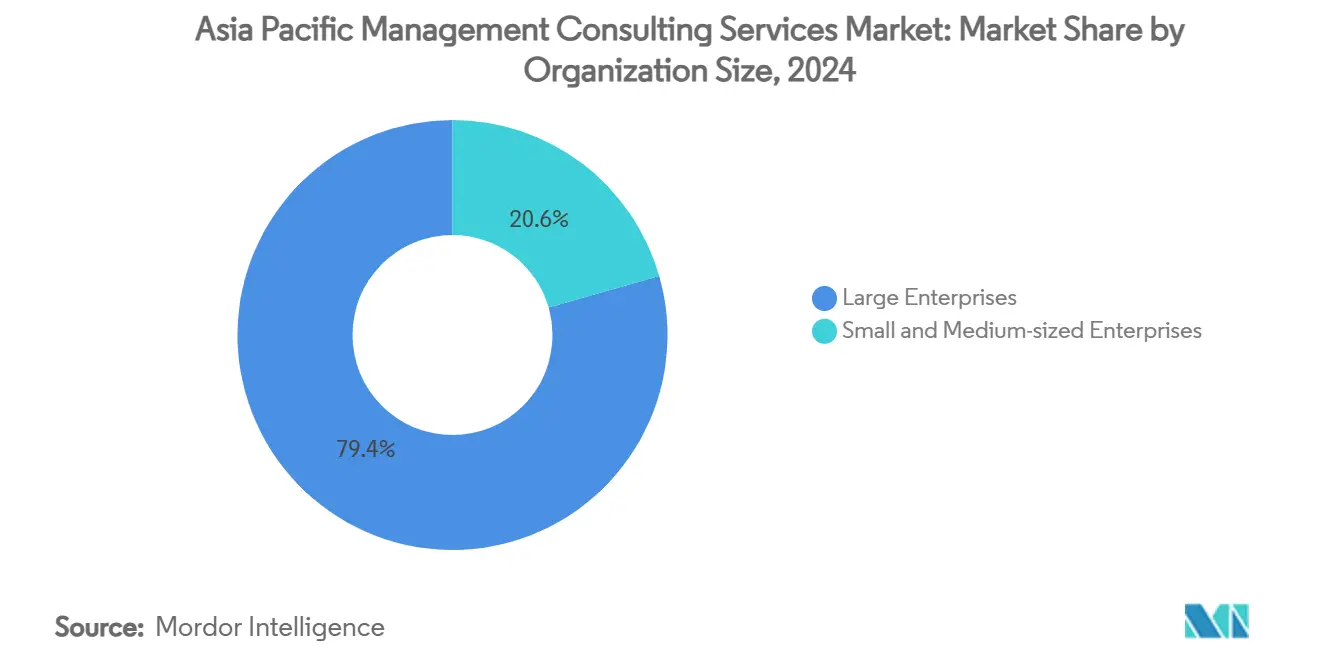

- By organization size, large enterprises held 79.44% revenue share of the Asia Pacific management consulting services market size in 2024, while small and medium-sized enterprises expanded at a 7.83% CAGR through 2030.

- By service type, operations consulting led with 34.85% revenue share in 2024; technology consulting is forecast to advance at a 9.14% CAGR to 2030, underscoring the shift toward AI and cybersecurity mandates.

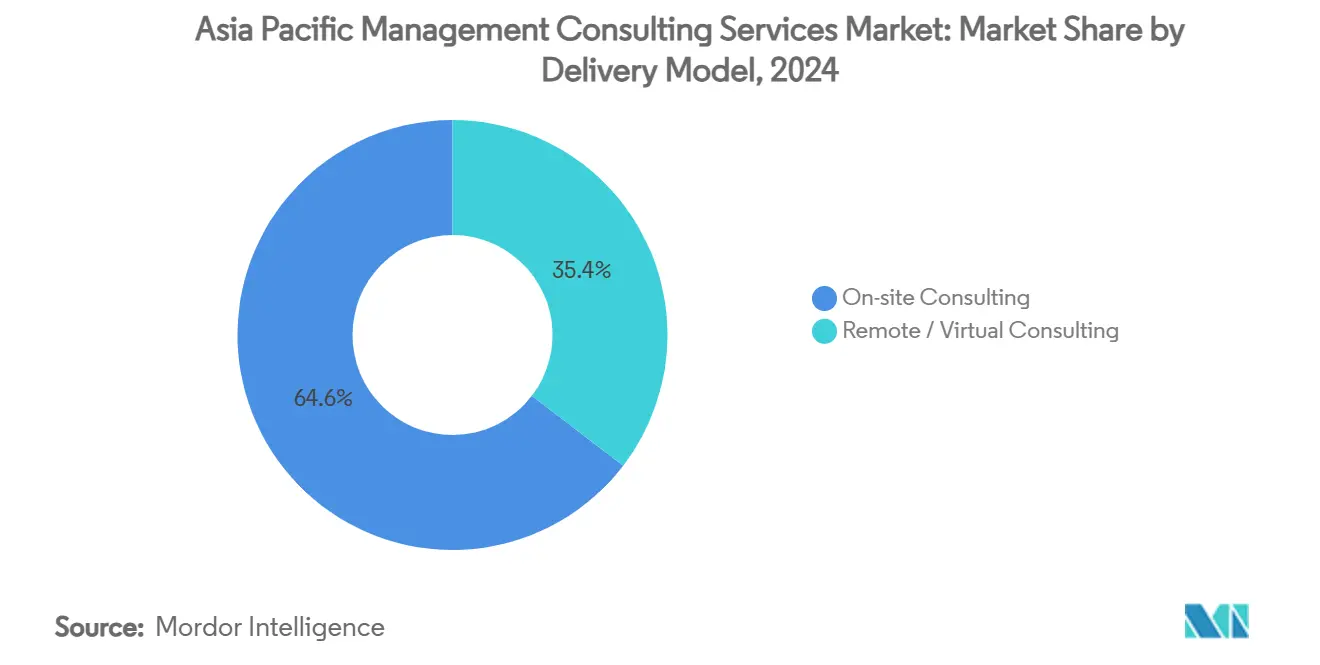

- By delivery model, on-site consulting accounted for 64.59% of the Asia Pacific management consulting services market share in 2024 and remote and virtual consulting is projected to progress at a 7.18% CAGR through 2030.

- By end-user industry, financial services captured 26.59% market share in 2024, while healthcare and life sciences is anticipated to grow at a 10.65% CAGR through 2030 on the back of nationwide digital-health programs.

- By geography, China commanded 33.88% revenue share in 2024 and India is poised to grow at a 10.18% CAGR between 2025-2030, powered by rising exports of consulting services and large-scale public digital initiatives.

Asia Pacific Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-transformation spending boom | +1.8% | Global, with concentration in China, India, Japan | Medium term (2-4 years) |

| Rising demand for post-pandemic operational resilience solutions | +1.2% | APAC core, spill-over to emerging markets | Short term (≤ 2 years) |

| Accelerated compliance pressures across BFSI and fintech | +0.9% | Singapore, Hong Kong, Australia, with expansion to Vietnam | Medium term (2-4 years) |

| AI-driven productivity mandates in large enterprises | +1.5% | Japan, South Korea, Australia, spreading to China and India | Long term (≥ 4 years) |

| Net-zero supply-chain consulting pull from exporters | +0.7% | Export-heavy economies: China, Vietnam, Thailand | Long term (≥ 4 years) |

| Cross-border M&A surge among mid-cap Asian firms | +0.5% | Regional hubs: Singapore, Hong Kong, with activity in India, Vietnam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital-Transformation Spending Boom

Over 70% of Philippine government services moved online by 2024, catalyzing widespread demand for implementation consulting across the public and private sectors.[1]Department of Information and Communications Technology, “e-Government Master Plan Progress,” dict.gov.ph Enterprises consequently seek advisory support for system integration, process re-engineering and change management to align with new digital infrastructure. Japan exemplifies the trend: 56% of surveyed companies plan to enlarge professional-services headcount in 2025, the highest intention rate among Asian markets. Consulting engagements now extend beyond technology roll-outs into business-model redesign for incumbents confronting digital-native challengers.

Rising Demand for Post-Pandemic Operational Resilience Solutions

Supply-chain shocks prompted firms to reprioritize risk management over pure cost optimization. Vietnam’s GDP is set to grow 6% in 2024 and 6.5% in 2025, while FDI rose 9.8% during early 2024, underscoring investor confidence in diversified production bases. Industrial clients therefore contract consultants for sourcing diversification, scenario planning and contingency architecture. The advisory scope increasingly features agile operating-model design to maintain service levels under volatility.

Accelerated Compliance Pressures Across BFSI and Fintech

Financial institutions juggling multiple supervisory regimes in Singapore, Hong Kong and emerging Southeast Asian jurisdictions increase spending on regulatory technology and governance consulting. The boom in digital payments and crypto-assets multiplies reporting obligations, encouraging banks to outsource process re-design to specialists. Firms versed in anti-money-laundering automation and prudential capital modelling enjoy elevated win rates as cross-border players strive for harmonized compliance frameworks.

AI-Driven Productivity Mandates in Large Enterprises

Worker-level AI usage in Japan rose from 5.8% to 8.3% in one year, yielding 15.1% task-efficiency gains and a 0.5-0.6% increase in macro labor productivity.[2]Takuro Morikawa, "The Impact of Artificial Intelligence on Macroeconomic Productivity," Research Institute of Economy, Trade and Industry, rieti.go.jp Corporates translate these gains into board-approved AI strategies that require external expertise for architecture design, data-governance policy, and workforce reskilling. Healthcare digitization under India's Ayushman Bharat Digital Mission further exemplifies how AI deployment pulls in niche consultants for patient-record automation and telehealth optimization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent retention crunch and wage inflation | -1.3% | Japan, Singapore, Australia, spreading to emerging markets | Short term (≤ 2 years) |

| Client budget tightening amid macro volatility | -0.8% | Global, with particular impact in China and export-dependent economies | Medium term (2-4 years) |

| Local data-sovereignty rules hindering remote delivery | -0.6% | China, India, Vietnam, with regulatory variations across APAC | Medium term (2-4 years) |

| Rising DIY analytics platforms reducing advisory spend | -0.4% | Advanced markets: Japan, South Korea, Australia, expanding to China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Talent Retention Crunch and Wage Inflation

Across six major Asia Pacific markets, 62% of consulting employers report moderate to acute skill shortages, with Malaysia witnessing equivalent proportions of professionals actively pursuing job changes. High demand for AI, cybersecurity, and compliance expertise pushes wages upward, compressing firm margins and extending project timelines. Hybrid work expectations from 68% of regional employees further complicate engagement, delivery, and culture retention, making talent strategy a board-level risk.

Client Budget Tightening Amid Macro Volatility

World Bank forecasts show East Asia Pacific growth easing from 4.8% in 2024 to 4.2% in 2025 and 4.1% in 2026.[3]World Bank Prospects Group, “Global Economic Prospects—East Asia and Pacific Highlights,” worldbank.org In response, enterprises triage discretionary consulting outlays, concentrating spend on compliance and quick cash-release initiatives. The squeeze is acute for SMEs, prompting advisors to design modular, outcome-based offerings and cultivate digital collaboration to reduce project cost and duration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: Enterprise Dominance Drives Market Scale

Large corporates commanded 79.44% of 2024 engagement value, reflecting their extensive transformation roadmaps and regulatory footprints that demand multiyear advisory support. These clients commission enterprise-wide AI programs, cross-border M&A integration, and sustainability reporting, driving high fee density per mandate. The Asia Pacific management consulting services market size sourced from small and medium-sized enterprises is smaller today, yet is expanding at a 7.83% CAGR as modular cloud platforms and public incentives lower entry barriers.

Australia’s professional-services workforce is forecast to expand by 409,800 roles by May 2029, with more than 90% requiring post-secondary credentials, signaling enduring demand for advisory capabilities across firm sizes. SMEs increasingly capitalize on government digitization grants and rely on outsourced consulting to bridge capability gaps.

By Service Type: Technology Consulting Gains Momentum

Operations consulting retained a 34.85% share in 2024, anchored in lean process redesign and supply-chain resilience. Nonetheless, technology consulting is projected to grow at 9.14% CAGR to 2030, outpacing all other categories as clients migrate core systems to the cloud and embed AI into workflows. Japan’s evidence of 0.5-0.6% economy-wide productivity lift from AI usage validates the business case and fuels boardroom urgency.

Strategy and HR consulting remain pillars for C-suite decision support and talent transformation. Yet cross-cutting digital agendas increasingly blur category boundaries, encouraging firms to bundle strategy, technology and change-management competences in integrated value propositions.

By Delivery Model: Remote Services Expand Market Reach

On-site projects accounted for 64.59% of 2024 billings, a testament to the preference for high-touch delivery in complex transformations and sensitive compliance engagements. Even so, remote and virtual consulting revenue is rising at 7.18% CAGR, powered by cost containment priorities and reliable collaboration software. Cross-border online work grew 30% during the past cycle as countries like India, Pakistan and Bangladesh scaled remote IT and analytics talent pools.

Hybrid models now dominate technology implementation, where discovery workshops occur onsite but configuration, testing and knowledge transfer run virtually. The mix widens consultant access to scarce specialists while enabling clients to shorten project kick-off times.

By End-User Industry: Healthcare Drives Sectoral Growth

Financial services captured 26.59% of 2024 demand thanks to stringent regulatory needs, omnichannel banking upgrades and continuous cyber-threat vigilance. Yet healthcare and life sciences is the fastest climber, heading for a 10.65% CAGR through 2030. India’s Ayushman Bharat Digital Mission alone mandates sweeping patient-record digitization, interoperability and data-security frameworks, widening the advisory remit for technology and change-management experts.

Manufacturing retains steady advisory spend for supply-chain diversification and industry 4.0 retrofits, while energy, telecom and government verticals engage consultants for grid modernization, 5G rollout and e-government platforms.

Geography Analysis

China led with a 33.88% share in 2024, driven by extensive industrial digitalization and the emergence of home-grown consulting champions. Growth steadies as major corporates mature in transformation cycles, yet AI adoption mandates and supply-chain re-risking sustain advisory demand. India, forecasted to grow at a 10.18% CAGR to 2030, benefits from USD 36.95 billion in consulting exports in FY 2021-22 and USD 1.05 billion in FDI into consultancy services.

Japan, South Korea, Vietnam, and Australia/New Zealand form the next tier. Japan posts the region’s highest professional services hiring intentions, with 56% of employers planning expansions in 2025. Vietnam’s 6-6.5% GDP growth outlook and 9.8% FDI increase create fresh mandates for operational improvement and market-entry advisory services. Australia’s services economy relies on a continual inflow of professional skills, while South Korea’s investment climate reforms stimulate strategic and compliance consulting.

Competitive Landscape

The Asia Pacific management consulting services market exhibits moderate concentration. Global majors deploy broad industry coverage, deep bench strength, and proprietary frameworks to service cross-border mandates. Regional champions and specialist boutiques capture high-growth niches in digital health, ESG reporting, and regulatory technology. Competition intensifies within technology consulting as legacy strategy houses acquire system-integration assets and tech vendors add advisory units.

Firms differentiate via AI-enabled delivery accelerators, sector-specific playbooks, and outcome-based fee models that align billing with client value realization. Talent scarcity pressures providers to establish distributed centers of excellence and invest in continuous learning paths for consultants. In parallel, alliances are proliferating between consulting firms and cloud hyperscalers to co-develop solutions, exemplified by CAC Holdings and FPT IS creating a Japan-focused joint venture that combines technology platforms with consulting expertise.

White-space opportunities emerge among mid-cap multinationals pursuing cross-border M&A, where transaction advisory, synergy capture and post-merger integration remain underserved, and among SMEs embarking on first-time digital transitions. Firms that package modular diagnostics, remote workshops, and templated accelerators are well-positioned to win price-conscious clients without eroding margins.

Asia Pacific Management Consulting Services Industry Leaders

-

Accenture PLC

-

Deloitte Touche Tohmatsu Limited (DTTL)

-

PricewaterhouseCoopers (PWC)

-

McKinsey & Company, Inc.

-

Ernst & Young Global Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: CAC Holdings and FPT IS agreed to form a joint venture targeting infrastructure management and localization of FPT products for the Japanese market, aiming to accelerate regional consulting-technology synergies.

- April 2025: Glosperity Corporation was selected as a partner in Kobe’s “KOBE Overseas Biz Assistance” program to guide local firms through international expansion.

- December 2024: SCSK detailed a plan to invest ¥100 billion (USD 680 million) over three years, expand cloud solutions and open new ASEAN bases, targeting ¥500 billion (USD 3.4 billion) in FY 2025 net sales.

- March 2024: Arthur D. Little analyzed India’s digital-health transformation challenges linked to Ayushman Bharat, signaling advisory opportunities in interoperability and security .

Asia Pacific Management Consulting Services Market Report Scope

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Technology Consulting |

| Other Service Types (Implementation, Function-specific, Industry-specific) |

| On-site Consulting |

| Remote / Virtual Consulting |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Financial Services (BFSI) |

| Manufacturing and Industrial |

| Energy and Utilities |

| Government and Public Sector |

| Real Estate and Construction |

| Retail and Consumer Goods |

| Media, Entertainment and Sports |

| Hospitality and Travel |

| Other Industries (Education, Transportation and Logistics, Agriculture and Agribusiness, among others) |

| Japan |

| India |

| China |

| South Korea |

| Vietnam |

| Australia and New Zealand |

| Rest of Asia-Pacific |

| By Organization Size | Large Enterprises |

| Small and Medium-sized Enterprises | |

| By Service Type | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Technology Consulting | |

| Other Service Types (Implementation, Function-specific, Industry-specific) | |

| By Delivery Model | On-site Consulting |

| Remote / Virtual Consulting | |

| By End-user Industry | IT and Telecommunications |

| Healthcare and Life Sciences | |

| Financial Services (BFSI) | |

| Manufacturing and Industrial | |

| Energy and Utilities | |

| Government and Public Sector | |

| Real Estate and Construction | |

| Retail and Consumer Goods | |

| Media, Entertainment and Sports | |

| Hospitality and Travel | |

| Other Industries (Education, Transportation and Logistics, Agriculture and Agribusiness, among others) | |

| By Geography | Japan |

| India | |

| China | |

| South Korea | |

| Vietnam | |

| Australia and New Zealand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current size of the Asia Pacific management consulting services market?

The Asia Pacific management consulting services market size is USD 65.49 billion in 2025 and is projected to reach USD 87.85 billion by 2030.

Which service category is growing fastest?

Technology consulting is the fastest-expanding category, forecast to post a 9.14% CAGR through 2030 as firms adopt AI, cloud and cybersecurity solutions.

Why is India the fastest-growing geography?

India benefits from government digital programs, rising foreign investment and USD 36.95 billion in consulting exports, supporting a 10.18% CAGR through 2030.

How are delivery models changing?

Remote and virtual engagements are growing at a 7.18% CAGR as clients seek cost efficiency and access to global talent while retaining on-site interactions for complex work.

What is the main challenge facing consulting firms in the region?

A talent retention crunch—where 62% of employers report skill shortages—drives wage inflation and threatens timely project delivery.

Which end-user industry offers the strongest growth outlook?

Healthcare and life sciences lead with a 10.65% CAGR, propelled by large-scale digital-health initiatives such as India’s Ayushman Bharat Digital Mission.

Page last updated on: