Indonesia Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

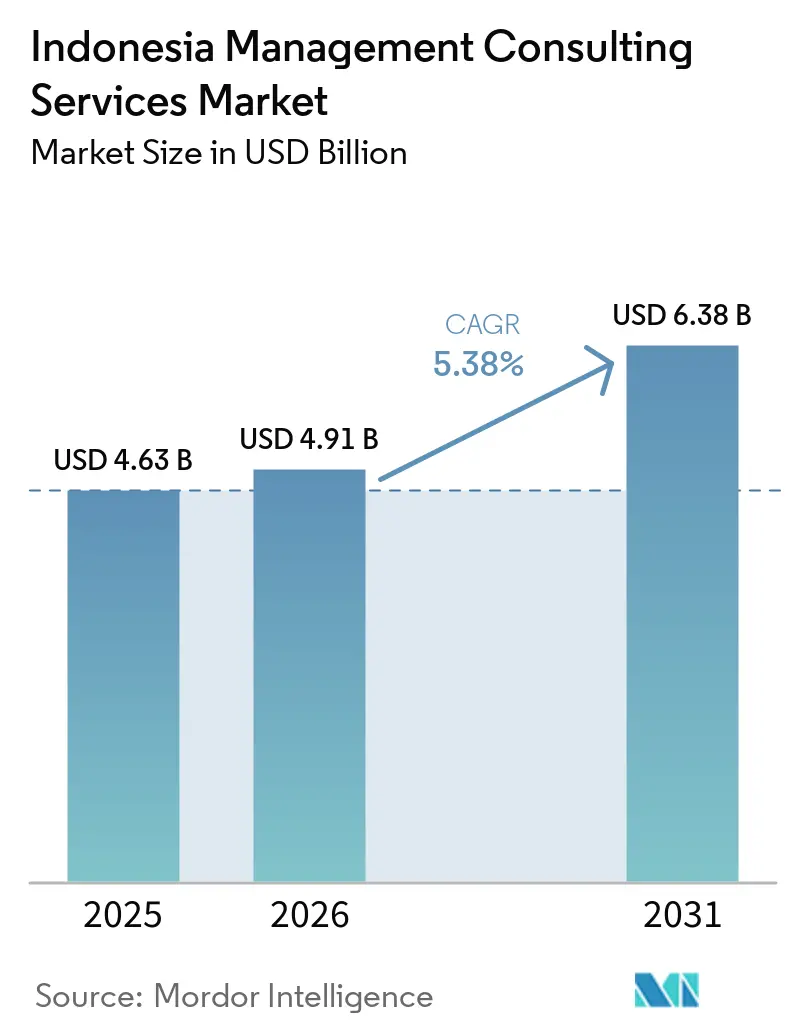

| Base Year Market Size (2025) | USD 4.63 Billion |

| Market Size (2026) | USD 4.91 Billion |

| Market Size (2031) | USD 6.38 Billion |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Management Consulting Services Market Analysis by Mordor Intelligence

The Indonesia management consulting services market size is expected to increase from USD 4.63 billion in 2025 to USD 4.91 billion in 2026 and reach USD 6.38 billion by 2031, growing at a CAGR of 5.38% over 2026-2031. Heightened infrastructure build-out around the new capital, sweeping digital-government programs, and binding climate-finance obligations are expanding advisory pipelines. The relocation to Nusantara alone has unlocked more than IDR 130 trillion (USD 8.1 billion) in public-private partnership mandates, while a national push for AI governance is accelerating readiness assessments across ministries and state-owned enterprises. At the same time, mandatory risk-taxonomy rules for banks and insurers are reshaping compliance priorities, and healthcare reform is driving actuarial redesign and provider-network optimization. Competition is intense but fragmented, with the Big Four accounting networks and three global strategy houses capturing about one-third of revenue, leaving ample room for mid-tier boutiques and local specialists.

Key Report Takeaways

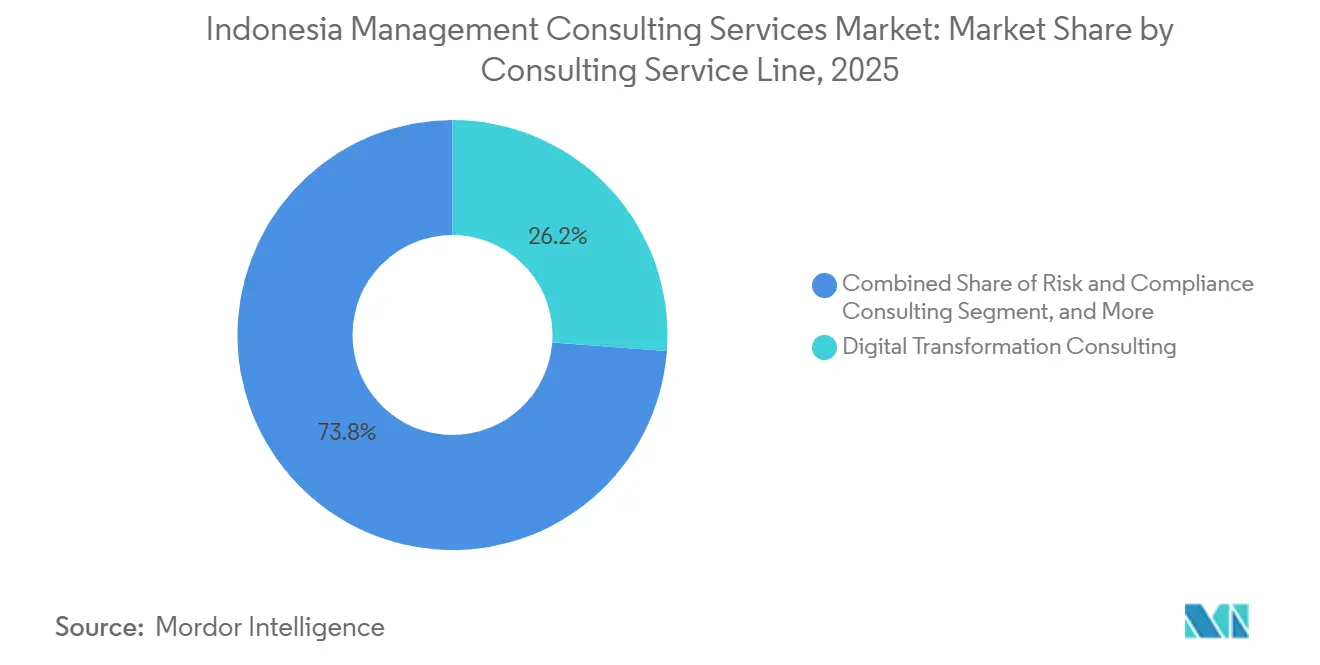

- By consulting service line, Digital Transformation Consulting commanded 26.19% of revenue in 2025, whereas Risk and Compliance Consulting recorded the highest projected CAGR at 5.71% through 2031.

- By organization size, large enterprises accounted for 64.37% of 2025 engagements, yet small and medium-sized enterprises are projected to grow fastest at a 5.47% CAGR over 2026-2031.

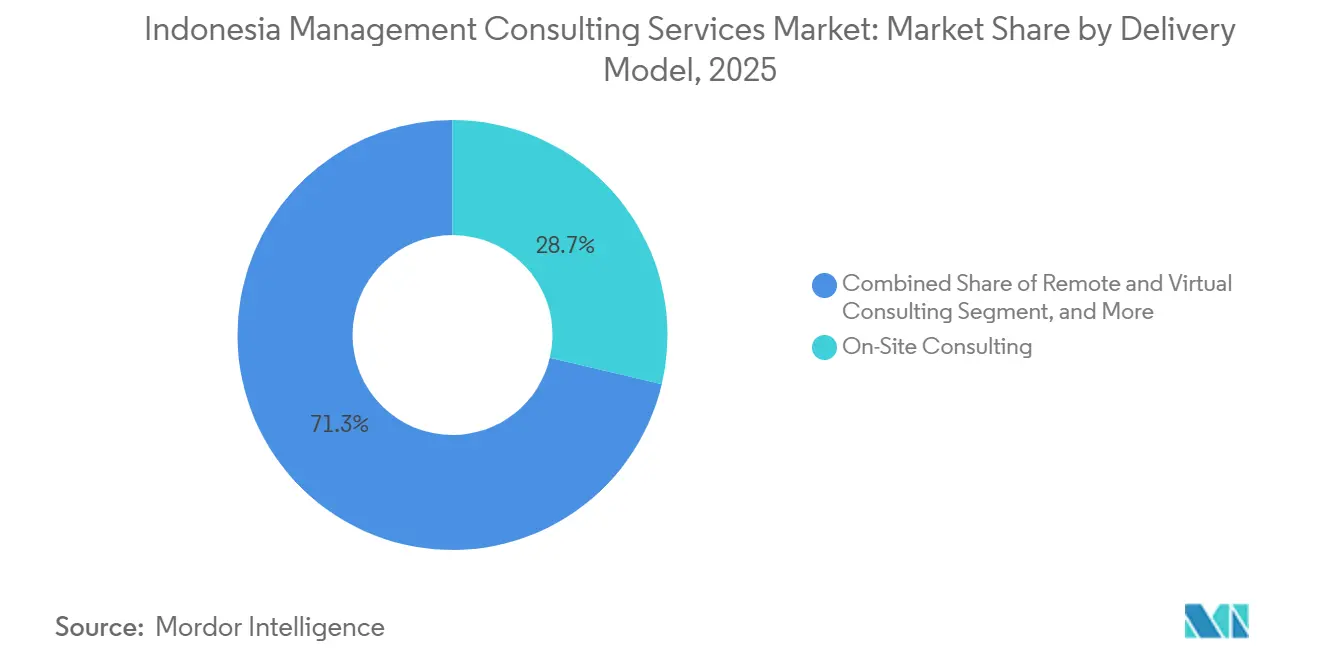

- By delivery model, on-site consulting held 28.67% share in 2025, while hybrid consulting is projected to expand at 5.83% CAGR between 2026-2031.

- By end-user industry, banking and insurance captured 18.48% revenue share in 2025; healthcare is forecast to advance at a 5.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Indonesia Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-First Transformation Programs | +1.2% | National, Jakarta-Surabaya-Nusantara corridor | Medium term (2-4 years) |

| Infrastructure and New-Capital (IKN) Advisory Demand | +1.0% | Java-Kalimantan corridor | Long term (≥4 years) |

| Carbon-Market and ESG Compliance Push | +0.8% | National, early adoption in energy, mining, palm oil | Medium term (2-4 years) |

| AI Governance Readiness Projects | +0.7% | National, ministries and financial institutions | Short term (≤2 years) |

| SME Formalization and Funding Wave | +0.6% | Java, Sumatra, Bali | Medium term (2-4 years) |

| Family-Owned Conglomerate Succession Planning Boom | +0.5% | National, top-100 groups | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Digital-First Transformation Programs

Indonesia’s National Digital Government Masterplan 2025-2045 mandates interoperable platforms across 34 provinces and 514 districts, triggering multi-year demand for enterprise-architecture, change-management, and cybersecurity advisory.[1]Ministry of Communication and Informatics, “National Digital Government Masterplan 2025-2045,” kominfo.go.id A 2025 tender from the Ministry of Communication and Informatics signaled systematic rollouts, while large private groups, such as Orang Tua, began six-month ERP migrations requiring extensive process reengineering. The Personal Data Protection Law, effective October 2024, adds urgency by obligating data-localization impact studies, consent-management workflows, and breach-notification protocols, services that most organizations outsource.

Infrastructure and New-Capital (IKN) Advisory Demand

The IKN Nusantara Authority’s pipeline of IDR 130 trillion (USD 8.1 billion) spans smart-city utilities, social facilities, and logistics backbones, each needing financial modeling, risk allocation, and stakeholder-engagement guidance.[2]IKN Nusantara Authority, “Infrastructure Projects,” ikn.go.id USTDA awarded a USD 2.49 million grant in 2025 for digital-backbone feasibility studies, and international advisors, including Roland Berger, are steering financing structures for parallel Jakarta MRT upgrades. Persistent logistics costs of 23-24% of GDP underscore opportunities for consultancies that can quantify life-cycle savings and embed digital twins into asset-management frameworks.

Carbon-Market and ESG Compliance Push

Presidential Regulation 110/2025 operationalized the National Carbon Registry, setting sectoral emissions baselines that require third-party verification and offset-project certification.[3]Ministry of Energy and Mineral Resources, “Energy Transition Roadmap,” esdm.go.id OJK’s Sustainable Finance Roadmap obliges banks to disclose financed emissions and align lending portfolios with net-zero pathways, prompting a surge in climate-risk modeling engagements.[4]Financial Services Authority, “Regulations and Circulars,” ojk.go.id Pertamina’s Gundih carbon-capture initiative illustrates how industrial actors rely on feasibility consultants for geological storage assessments and UNFCCC compliance.

AI Governance Readiness Projects

A draft presidential regulation crafted with Boston Consulting Group defines risk-tiering and algorithmic-transparency requirements, motivating ministries, SOEs, and banks to commission readiness assessments. UNESCO’s 2025 audit exposed gaps in technical standards and procurement guidelines, accelerating adoption of ISO 42001 as a de facto benchmark. A 2026 BCG-Google Cloud report highlighted measurable value from generative-AI pilots, yet most institutions remain in proof-of-concept mode, sustaining advisory demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight Senior-Consultant Talent Pool | -0.9% | Jakarta, Surabaya, Bali | Short term (≤2 years) |

| High Fee-Sensitivity of SME Clients | -0.7% | Tier-2 cities, outer islands | Medium term (2-4 years) |

| Foreign-Ownership Caps and Licensing Hurdles | -0.4% | National | Long term (≥4 years) |

| Client Insourcing of Digital Capabilities | -0.3% | Large enterprises, SOEs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tight Senior-Consultant Talent Pool

Up to 95% of senior consultants classify as passive job-seekers, and 78% express willingness to relocate abroad, shrinking the domestic talent reservoir. Typical Jakarta salaries range from IDR 136 million to IDR 256 million (USD 8,500 to USD 16,000), but 57% of candidates expect 20% raises when changing firms, compressing margins for providers lacking automation or offshore centers.[5]JobStreet, “Indonesia Salary Guide,” jobstreet.co.id Sector-specific shortages, CISOs in finance, RSPO auditors in palm oil, compound the issue, triggering proprietary academies and equity incentives that inflate fixed costs.

High Fee-Sensitivity of SME Clients

Roughly half of Indonesia’s 62 million micro and small enterprises remained unregistered in 2024, and only 27% of formal SMEs accessed loans, signaling tight cash flow for advisory spend. Local specialists such as InCorp Indonesia offer modular compliance packages below USD 5,000, undercutting international firms whose cost structures rely on retainers. Delivery expenses escalate outside Java, forcing consultancies to balance geographic reach against profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Digital and Risk Engagements Dominate

Digital Transformation Consulting captured the largest slice of Indonesia management consulting services market share in 2025, and demand is forecast to grow at 5.38% through 2031. Projects cover ERP migrations, cloud-native architectures, and customer-experience redesign, exemplified by the AI-powered YonBIP roll-out for manufacturing clients. Risk and Compliance Consulting, propelled by OJK Regulation 30/2025, is expanding even faster as banks implement early-warning systems and cyber-risk assessments. The Indonesia management consulting services market size for these two lines is benefiting from mandatory regulatory deadlines that compress decision cycles. Strategy, operations, and HR consulting continue to serve niche transitions such as family business succession and lean manufacturing, but lack the same structural tailwinds.

The Indonesia management consulting services market is also experiencing rising demand for ISO 27001 and ISO 42001 readiness work, which consultancies now bundle into digital and risk engagements. Firms with proprietary accelerators can cross-sell audit-preparation services, creating recurring income streams. Sustainability advisory, innovation management, and organizational design collectively hold less than 3% of Indonesia management consulting services market share, suggesting room for consolidation among specialists willing to invest in thought leadership.

By Organization Size: Enterprise Spend Steady, SME Momentum Builds

Large enterprises accounted for 64.37% of Indonesia management consulting services market revenue in 2025, fueled by state-owned utilities, family conglomerates, and multinational subsidiaries executing multi-year transformation roadmaps. Succession planning across major business groups remains a prominent workstream as 60% still lack formal governance structures. In parallel, small and medium-sized enterprises are advancing at a 5.47% CAGR, supported by formalization programs and improved credit access. The Indonesia management consulting services market size attached to SMEs is smaller today yet expanding rapidly. Consultancies targeting this cohort must optimize pricing below USD 10,000 per engagement, rely on digital intake workflows, and partner with fintech lenders to embed advisory into loan origination.

The bifurcation of engagement models is widening. Enterprises favor retainers and multi-phase diagnostics, while SMEs demand productized, outcome-linked services. Firms unable to reconcile both models are specializing, either doubling down on C-suite relationships or scaling low-touch SME platforms.

By Delivery Model: Hybrid Approaches Gain Traction

On-site work retained 28.67% of Indonesia management consulting services market share in 2025 because infrastructure projects and change-management initiatives still require physical presence. However, hybrid delivery, combining remote analysis with periodic site visits, is growing at 5.83% CAGR, enabled by collaboration platforms and regional micro-offices such as PwC’s new Yogyakarta hub. The Indonesia management consulting services market size attached to hybrid engagements is expanding as clients seek cost efficiency without sacrificing face-to-face workshops.

Remote-only consulting remains constrained by patchy connectivity outside Java, and data-localization rules under the Personal Data Protection Law raise hosting costs. Consequently, most providers now design engagement plans that allocate discovery and analytical tasks to virtual teams, reserving travel for stakeholder alignment and training.

By End User Industry: Financial Institutions Lead, Healthcare Outpaces

Banking and insurance clients generated 18.48% of Indonesia management consulting services market revenue in 2025, with regulatory deadlines for risk-taxonomy and cyber-security controls sustaining advisory pipelines. BI-FAST adoption, open-API initiatives, and digital bank licensing are layering technology and compliance mandates atop core-system upgrades. Healthcare exhibits the highest growth, with a 5.56% projected CAGR driven by universal coverage targets and BPJS Kesehatan’s deficit-reduction roadmap. The Indonesia management consulting services market size linked to provider digitalization includes SIMRS roll-outs, telemedicine platforms, and supply-chain redesigns.

Manufacturing engagements focus on Industry 4.0 lean transformations, while energy clients seek decarbonization roadmaps to meet a 75 GW renewable-capacity goal. Public-sector demand is tied to IKN master planning and digital-government platforms, although budget cycles dictate timing. IT and telecommunications firms look for 5G architecture advice and data-center site selection to serve hyperscale entrants.

Geography Analysis

Java captures roughly 70% of Indonesia management consulting services market activity, anchored by Jakarta’s concentration of headquarters and regulators. Surabaya adds manufacturing and logistics engagements, with its port handling 40% of national container throughput. The forthcoming move to IKN Nusantara is beginning to redirect advisory work toward Kalimantan, especially around master planning, smart-city utilities, and public-private contracting.

Outer islands, Sumatra, Sulawesi, and Papua, represent 30% of current revenue, yet are expanding at an estimated 6.2% CAGR. Medan’s agro-processing cluster requires RSPO and ISPO certification consultants to meet European import rules, while Makassar’s seafood exporters engage HACCP advisors. Bali’s hospitality rebound is fueling demand for digital revenue-management systems and sustainability certifications.

Regulation still flows through Jakarta. BKPM Regulation 5/2025 lowered capital thresholds but kept a 12-month lock-up, discouraging foreign boutiques from opening regional offices. The Online Single Submission platform has simplified licensing, yet sector-specific risk scores mean legal and compliance consultants remain vital navigators.

Competitive Landscape

The Indonesia management consulting services market features moderate fragmentation. The Big Four and three global strategy houses hold about 35% of revenue, while mid-tier firms such as Roland Berger and Kearney, plus local technology specialists like Telkomsigma and Metrodata, compete on sector depth and price. KPMG’s IDR 150 billion (USD 9.8 million), five-year investment is earmarked for cybersecurity, data science, and sustainability practices. PwC’s Yogyakarta office recruits Central Java talent to feed hybrid delivery models and reduce travel costs. Metrodata’s March 2026 capital injection of IDR 150 billion into its consulting arm illustrates how ecosystem leverage can fund rapid scaling.

White-space niches persist. SME formalization remains under-served, healthcare consulting is fragmented despite systemic deficits, and carbon-market verification lacks dominant players. Technology is the leading differentiator, with Telkomsigma’s Digipactum platform embedding contract management and risk analytics into governance advisory. ISO 37001 and ISO 27001 certifications are now prerequisites for many SOE tenders, favoring firms that bundle audit-readiness into transformation programs.

Indonesia Management Consulting Services Industry Leaders

Deloitte Indonesia (PT Deloitte Konsultan Indonesia)

PwC Indonesia Advisory (PT PricewaterhouseCoopers Consulting Indonesia)

Accenture Indonesia

Ernst and Young Indonesia (PT Ernst and Young Advisory Indonesia)

KPMG Indonesia Advisory (PT KPMG Advisory Indonesia)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Boston Consulting Group released “Leading in the Age of Messaging,” detailing AI-enabled customer communication opportunities in Indonesia’s financial sector.

- March 2026: Metrodata injected IDR 150 billion (USD 9.4 million) into PT Mitra Integrasi Informatika to scale cloud, AI, and cybersecurity consulting capabilities.

- February 2026: Boston Consulting Group and Google Cloud published a joint study showing measurable lifetime-value gains from generative-AI pilots in Indonesian banking.

- January 2026: Orang Tua Group completed a six-month YonBIP ERP roll-out supported by Yonyou and Wilmar Consultancy Services.

- October 2025: PwC Indonesia inaugurated its Yogyakarta office inside Universitas Gadjah Mada’s innovation center, targeting regional digital-talent pools.

Indonesia Management Consulting Services Market Report Scope

The Indonesia Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current Indonesia management consulting services market size and its expected growth rate?

The market stands at USD 4.91 billion in 2026 and is projected to reach USD 6.38 billion by 2031, growing at a CAGR of 5.38%.

Which consulting service line is expanding fastest through 2031?

Risk and Compliance Consulting leads with a projected 5.71% CAGR, propelled by OJK mandates for new risk classifications and early-warning systems.

How is the relocation to IKN Nusantara influencing demand for advisory services?

IKN's IDR 130 trillion (USD 8.1 billion) public-private pipeline is driving sustained need for feasibility studies, financial modeling, and smart-city implementation guidance.

Why are hybrid consulting models gaining popularity in Indonesia?

Clients seek cost savings and flexibility, leveraging remote diagnostics for data analysis and reserving site visits for stakeholder workshops, driving a 5.83% CAGR in hybrid delivery.

Which end-user sectors will offer the strongest growth opportunities by 2031?

Healthcare is forecast to expand at 5.56% CAGR due to universal coverage targets and hospital digitalization, while banking continues to invest heavily in compliance and digital channels.

What factors limit foreign boutique consultancies from entering regional Indonesian markets?

Although capital requirements were lowered, the 12-month lock-up and total-investment thresholds under BKPM Regulation 5/2025, coupled with talent scarcity outside Java, restrict new entrants.

Page last updated on: