Malaysia Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

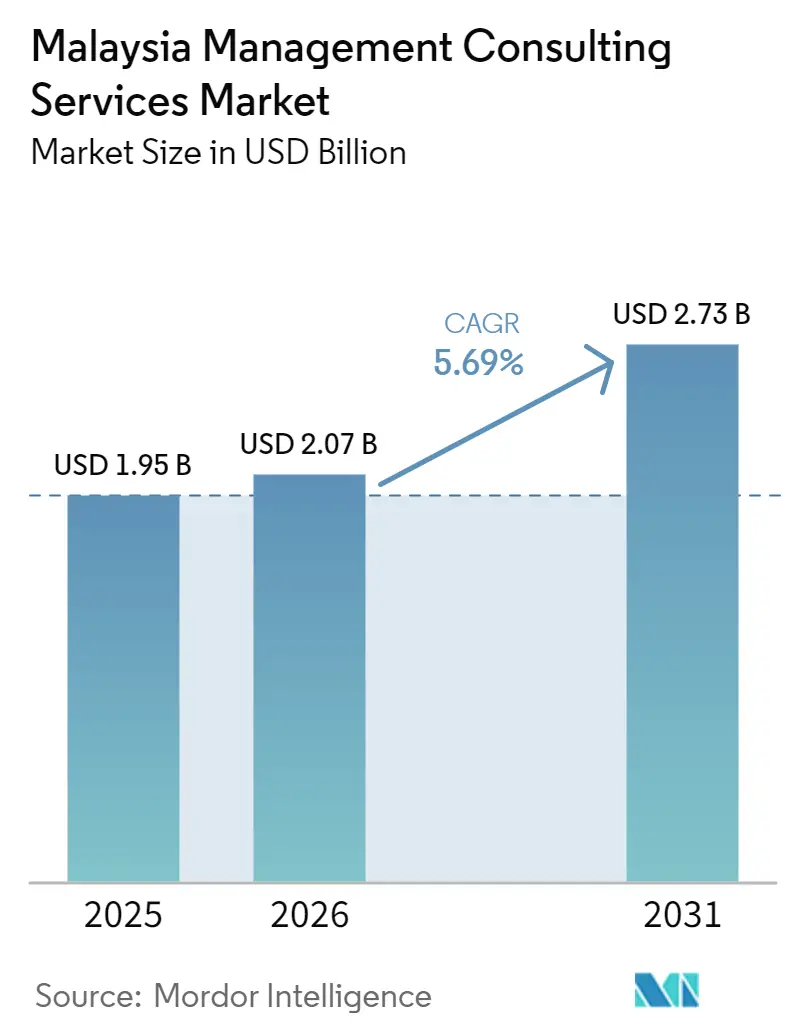

| Base Year Market Size (2025) | USD 1.95 Billion |

| Market Size (2026) | USD 2.07 Billion |

| Market Size (2031) | USD 2.73 Billion |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Management Consulting Services Market Analysis by Mordor Intelligence

The Malaysia management consulting services market size is projected to expand from USD 2.07 billion in 2026 to USD 2.73 billion by 2031, registering a CAGR of 5.69% over 2026-2031. Demand is scaling on the back of government-led digital transformation mandates, accelerated Industry 4.0 adoption in manufacturing, and new data-governance regulations that elevate consulting from discretionary spend to core strategic input. Budget 2026 funding for a sovereign AI cloud, enterprise cloud migrations exemplified by the MAR 1.0 billion (USD 226 million) Maybank-Microsoft partnership, and mandatory e-invoicing for SMEs in 2026 jointly reinforce the advisory pipeline. Consulting firms are increasingly packaging hybrid delivery models to contain project costs while accelerating talent deployment, an approach that also helps offset the sector’s chronic skills shortage. Competition is intensifying as global firms acquire niche local specialists and technology service providers scale workforces to capture large-scale digital programs.

Key Report Takeaways

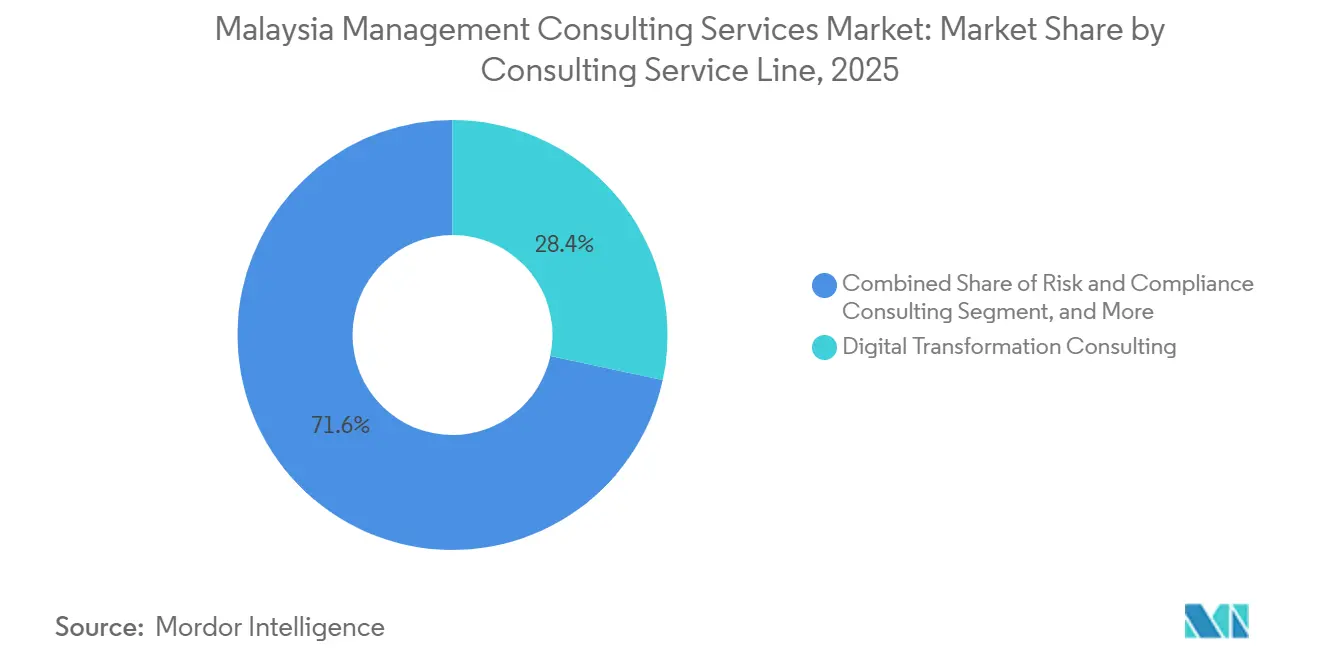

- By consulting service line, digital transformation captured 28.36% revenue share in 2025, whereas risk and compliance is forecast to grow at the fastest 6.71% CAGR through 2031.

- By organization size, large enterprises held 61.87% of spending in 2025, while SMEs are projected to expand at a 5.84% CAGR over 2026-2031.

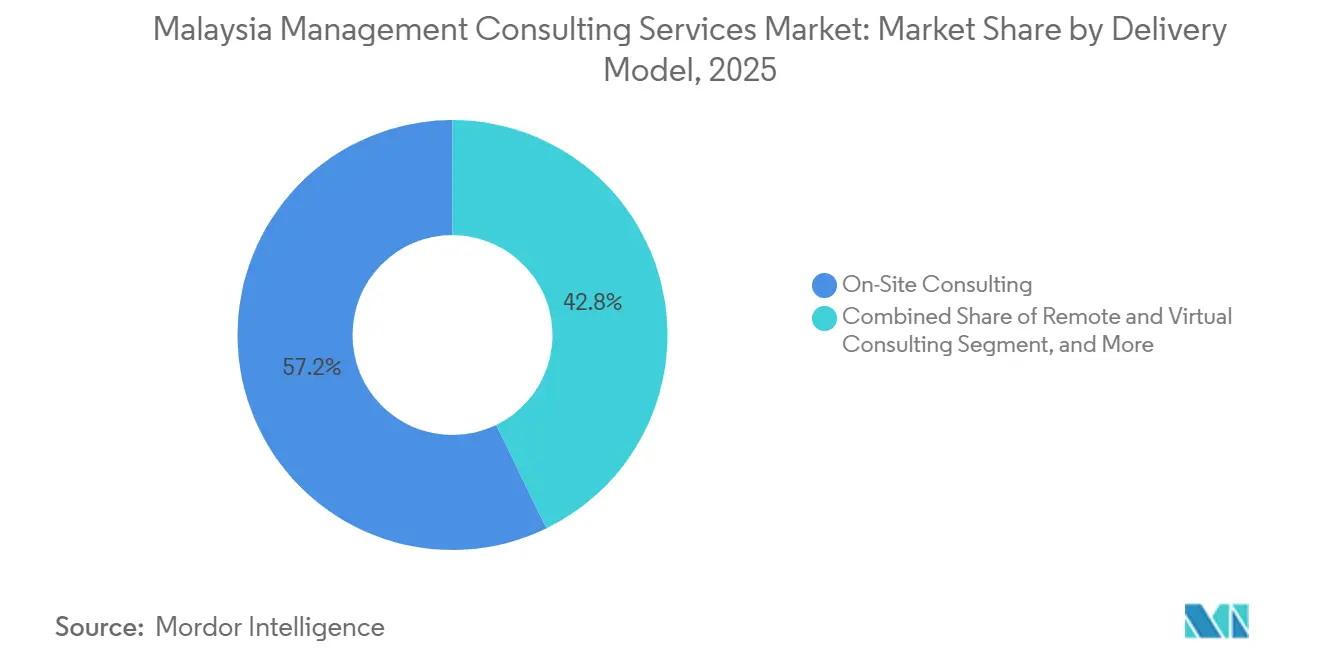

- By delivery model, on-site engagements led with 57.21% share in 2025, yet remote and virtual consulting is advancing at a 6.23% CAGR to 2031.

- By end-user industry, banking and insurance commanded 19.83% share in 2025; energy and resources is expected to post the highest 5.97% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Malaysia Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-Transformation Push Under MyDIGITAL Blueprint | +1.8% | National, with concentration in Klang Valley, Penang, Johor | Medium term (2-4 years) |

| Industry4WRD Incentives Accelerating Manufacturing Consulting Demand | +1.2% | Peninsular Malaysia manufacturing hubs | Short term (≤ 2 years) |

| Regulatory and Compliance Changes Boosting Risk Advisory | +1.5% | National, particularly financial services and data-intensive sectors | Short term (≤ 2 years) |

| Cloud-First and Cybersecurity Spending by Enterprises | +1.0% | National, led by banking, telecommunications, public sector | Medium term (2-4 years) |

| Rising ESG and Shariah-Compliant Advisory Opportunities | +0.4% | National, with strength in Islamic finance hubs (Kuala Lumpur) | Long term (≥ 4 years) |

| Generative-AI Adoption Creating New Advisory Niches | +0.6% | National, early adoption in financial services, retail, manufacturing | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital-Transformation Push Under MyDIGITAL Blueprint

MyDIGITAL Corporation coordinates 48 national initiatives that compel federal agencies to migrate 80% of data to hybrid cloud and digitize most citizen-facing services. The program assigns clear funding lines, including a sovereign AI cloud budget, so ministries release tenders that bundle program management, vendor selection, and change-management workstreams. Private companies align their roadmaps with sectoral incentives to qualify for tax breaks, which places consultants at the center of application design and compliance verification. Deliverables now extend beyond strategy decks to architecture blueprints, data-governance playbooks, and workforce-upskilling plans. The pipeline therefore contains large, multi-year engagements that reinforce steady revenue visibility for firms active in Kuala Lumpur, Penang, and Johor.[1]Ming En Liew, “Behind Malaysia's MyDIGITAL Corporation,” GovInsider, govinsider.asia

Industry4WRD Incentives Accelerating Manufacturing Consulting Demand

The Industry4WRD Intervention Fund reimburses up to 70% of approved project costs, capped at MAR 500,000 (USD 113,000), after an SME completes a government-funded readiness assessment. Eligible line items span automation, analytics, and digital-twin implementations, so consultants often design both the assessment and the follow-on solution. Upfront disbursement of 30% of the government share lowers cash-flow barriers and accelerates project kickoff. Firms that master claim documentation and milestone scheduling reduce reimbursement risk for clients and themselves. This subsidy loop positions manufacturing SMEs as a durable growth pocket within the overall advisory market.[2]Malaysian Investment Development Authority, “Industry4WRD Intervention Fund,” mida.gov.my

Regulatory and Compliance Changes Boosting Risk Advisory

The Personal Data Protection Amendment Act 2024 introduces 72-hour breach notifications, mandatory Data Protection Officers, and new data-portability rights. Bank Negara Malaysia’s draft guidance on AI model governance requires banks and insurers to document explainability controls and continuous monitoring. Overlapping rules create demand for integrated compliance roadmaps that cut across cyber, privacy, and operational-risk domains. Consulting scopes now include maturity assessments, policy redesign, and simulation drills that test incident-response readiness. Institutions prefer external advisors that can map regulatory dependencies and embed controls into in-flight digital programs.[3]Pertama Partners, “Malaysia PDPA 2025 & AI Governance,” pertamapartners.com

Cloud-First and Cybersecurity Spending by Enterprises

Malaysia’s cloud-computing policy ties data-sovereignty rules to sectoral risk standards, compelling banks to justify any cross-border data transfer. Maybank’s five-year MAR 1.0 billion (USD 226 million) Azure adoption underscores the scale of current migrations and the breadth of work spanning architecture, DevSecOps, and change-management tracks. Similar deals in telecom and public sector follow a pattern of phased workload moves paired with zero-trust redesigns. Consultants differentiate by offering reference controls that satisfy both the cloud policy and Bank Negara technology-risk guidance. The result is a rising share of multicloud security, resilience testing, and workforce-upskilling services in enterprise statements of work.[4]Maybank, “Maybank Forges Strategic Partnership with Microsoft,” maybank.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of Specialized Consulting Talent and High Staff Churn | -0.9% | National, acute in Kuala Lumpur, Penang | Short term (≤ 2 years) |

| Price Sensitivity Among SMEs Limiting Consulting Spend | -0.7% | National, especially outside Klang Valley | Medium term (2-4 years) |

| Growth of Independent Freelance Platforms Eroding Traditional Firm Revenues | -0.3% | National, digital and IT consulting | Medium term (2-4 years) |

| Data-Sovereignty Concerns Restricting Remote Engagements | -0.2% | National, public sector and finance | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarcity of Specialized Consulting Talent and High Staff Churn

More than 61,000 Malaysians left the country in five years, and 39% of those working in Singapore are classified as skilled, shrinking the domestic talent pool available to firms. Surveys show 35% of chief executives now rank skills shortages ahead of cyber and inflation risks, a reversal from regional peers. Replacement costs rise when mid-project departures force knowledge transfer and client-relationship rebuilding. Firms respond by embedding formal upskilling modules into engagements and by certifying client staff to offload routine tasks. Even so, wage gaps with neighboring hubs continue to pull specialists abroad, capping delivery capacity in high-growth domains such as AI engineering.[5]Online Bureau, “Malaysia Risks Talent Loss,” hrsea.economictimes.indiatimes.com

Price Sensitivity Among SMEs Limiting Consulting Spend

Half of MSMEs cite cash-flow stress as their top challenge, and 70% hold less than six months of reserves. Grants that cap at MAR 5,000 (USD 1.130) cover only diagnostic work, leaving little budget for full implementations. Rising minimum wages and new foreign-worker levies further squeeze operating margins, so owners delay or scale back advisory engagements. Consultants now unbundle scopes into quick-win modules linked to measurable revenue or cost outcomes and coordinate claim paperwork for available subsidies. Uptake improves when firms can match payment milestones to grant disbursements, yet overall project scale remains modest relative to enterprise programs.[6]Ainin Wan Salleh, “SME Groups Urge Digitalisation Support,” freemalaysiatoday.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Digital Transformation Leads Risk and Compliance Surges

Digital transformation captured the largest 28.36% share of the Malaysia management consulting services market in 2025. Enterprise cloud adoption, generative-AI pilots, and core-system modernization are expected to preserve momentum, while risk and compliance workstreams will likely outpace with a 6.71% CAGR as institutions grapple with new data-protection and cyber-resilience mandates. Strategy and operations remain foundational, often embedded as phases within larger digital programs. Generative-AI advisory is emerging as a differentiator, with projects focused on productivity gains and new revenue models for banks and retailers.

Demand for risk and compliance advisory is expanding fastest because multiple regulators now require evidence of AI model governance and breach-notification rigor. Consultants that integrate privacy, operational resilience, and cyber frameworks into cloud-migration playbooks gain competitive advantage. Sustainability and Shariah-compliant advisory niches are widening as green sukuk issuance accelerates and Bursa Malaysia tightens ESG reporting.

By Organization Size: Large Enterprises Dominate SMEs Accelerate

Large enterprises delivered 61.87% of 2025 revenue for the Malaysia management consulting services market, fueled by multi-year transformations and enterprise-wide compliance programs. They favor retainer arrangements that secure continuous access to specialist skills and program management. SMEs, though smaller in absolute spend, represent the highest growth at 5.84% CAGR as Industry4WRD grants and mandatory e-invoicing deadlines push them to digitize.

SMEs procure outcome-linked micro-engagements focused on quick ROI, often co-funded by matching grants. Consulting firms are tailoring modular playbooks, bundling grant-application support, and deploying hybrid delivery teams to trim travel and onsite expenses. The Malaysia management consulting services market size captured from SMEs is therefore projected to widen steadily through 2031.

By Delivery Model: Hybrid Takes Hold

On-site work remained dominant at 57.21% in 2025 but hybrid models combining limited face-to-face workshops with remote execution are rising fastest at a 6.23% CAGR. Data-sovereignty clauses in financial-services and public-sector contracts require consultants to evidence that client data never leaves Malaysia, shaping secure remote-access architectures and favoring local cloud nodes. Firms that invest in regional delivery centers and sovereign-cloud credentials are best positioned to win.

Remote engagements reduce cost and accelerate staffing across Peninsular Malaysia, Sabah, and Sarawak. However, data-residency audits and vendor-lock-in concerns mean that Malaysia management consulting services market share for fully virtual delivery remains capped in regulated sectors.

By End-User Industry: Banking Leads Energy Transition Accelerates

Banking and insurance accounted for the largest 19.83% slice of the Malaysia management consulting services market in 2025, propelled by core-banking modernization and AI-driven customer analytics. Digital banks now serve more than 2.4 million customers, expanding demand for credit-risk modeling and open-API architecture advice.

Energy and resources is forecast to record the fastest 5.97% CAGR as the National Energy Transition Roadmap channels USD 47 billion into renewables by 2030. Consultants deliver feasibility studies, workforce reskilling, and power-purchase-agreement structuring. Manufacturing consulting is buoyed by Industry4WRD subsidies, whereas public-sector engagements revolve around creating interoperable data exchanges and super-app health platforms.

Geography Analysis

Klang Valley remains the epicenter of the Malaysia management consulting services market, hosting federal ministries, regulators, and the headquarters of most multinationals. Penang and Johor contribute sizable volumes on account of semiconductor clusters, cross-border trade with Singapore, and data-center corridors anchored by hyperscaler investments. These three regions jointly attract the majority of cloud-migration, Industry4WRD, and compliance-consulting contracts.

Sabah and Sarawak trail in consulting spend but enjoy double-digit growth opportunities as Budget 2026 earmarks MAR 9.3 billion (USD 2.1 billion) for rural connectivity and Jendela aims for nationwide fiber coverage. Projects here focus on digital-inclusion roadmaps, supply-chain digitization in palm-oil and logging sectors, and public-service delivery transformation.

Special economic zones such as the Johor-Singapore SEZ and Kedah-Thailand border zone are emerging hotspots. Consulting scopes span cross-border regulatory alignment, logistics automation, and renewable-energy integration into ASEAN grids, leveraging Malaysia’s 70% renewable target by 2050.

Competitive Landscape

Global full-service firms, Accenture, Deloitte, PwC, EY, and KPMG, compete against technology consultancies like IBM, Capgemini, and Cognizant plus local boutiques ZICO Consulting and RSM Malaysia. Market share battles increasingly hinge on sector-specific depth and onshore delivery scale. Accenture’s 2025 purchase of Aristal inserted 30 banking-transformation experts, expanding its core-banking footprint. Cognizant is tripling headcount to 5,000 by 2026, establishing a Centre of Excellence and seventeen offshore development centers to support cloud and AI programs.

Technology partnerships anchor new revenue pools. The MAR 1.0 billion (USD 226 million) Maybank-Microsoft agreement pulls advisory volume toward firms with Azure and Copilot certifications. EY’s Digital Augmented Resources model fuses delivery with upskilling, differentiating on talent-transfer metrics.

White-space opportunity lies in sustainability and AI governance. Bursa Malaysia’s upcoming Scope 1 and 2 assurance rules and the National AI Office’s framework development are prompting engagements around ESG reporting systems and responsible-AI operating models. Niche specialists such as Foray Advisory and AI Labs are carving share with generative-AI proof-of-concepts for mid-caps.

Malaysia Management Consulting Services Industry Leaders

Accenture plc

PwC (PricewaterhouseCoopers)

Deloitte Touche Tohmatsu Limited

KPMG International Limited

Ernst & Young Global Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: NexG Bhd won a six-year MAR 732.72 million (USD 165 million) contract to supply next-generation national identity cards.

- February 2026: The Digital Ministry expanded the Malaysian Government Central Data Exchange, which processed more than 23 million API transactions YTD.

- January 2026: A MAR 87.45 million (USD 19.8 million), 36-month tender was issued for MySejahtera super-app maintenance and expansion.

- December 2025: The Energy Commission relaxed Corporate Renewable Energy Supply Scheme guidelines to accelerate project approvals.

Malaysia Management Consulting Services Market Report Scope

The Malaysia Management Consulting Services Market Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current size of the Malaysia management consulting services market?

The market stands at USD 2.07 billion in 2026 and is projected to reach USD 2.73 billion by 2031.

Which consulting service line is growing fastest?

Risk and compliance consulting is expected to grow at a 6.71% CAGR through 2031, outpacing other service lines.

Why are SMEs important to consulting demand in Malaysia?

SMEs are the fastest-growing client segment, expanding at 5.84% CAGR as Industry4WRD grants and mandatory e-invoicing drive digital adoption.

How are data-sovereignty rules affecting delivery models?

Sovereignty mandates require local data residency, so firms blend on-site security workshops with remote execution over Malaysian cloud nodes.

Which geographic areas outside Klang Valley offer strong growth?

Penang's semiconductor corridor, Johor's SEZ, and connectivity upgrades in Sabah and Sarawak are creating new advisory opportunities.

What strategic moves are leading firms making?

Moves include Accenture's acquisition of Aristal for banking depth and Cognizant's plan to treble its Malaysia workforce and open a Centre of Excellence.

Page last updated on: