China Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

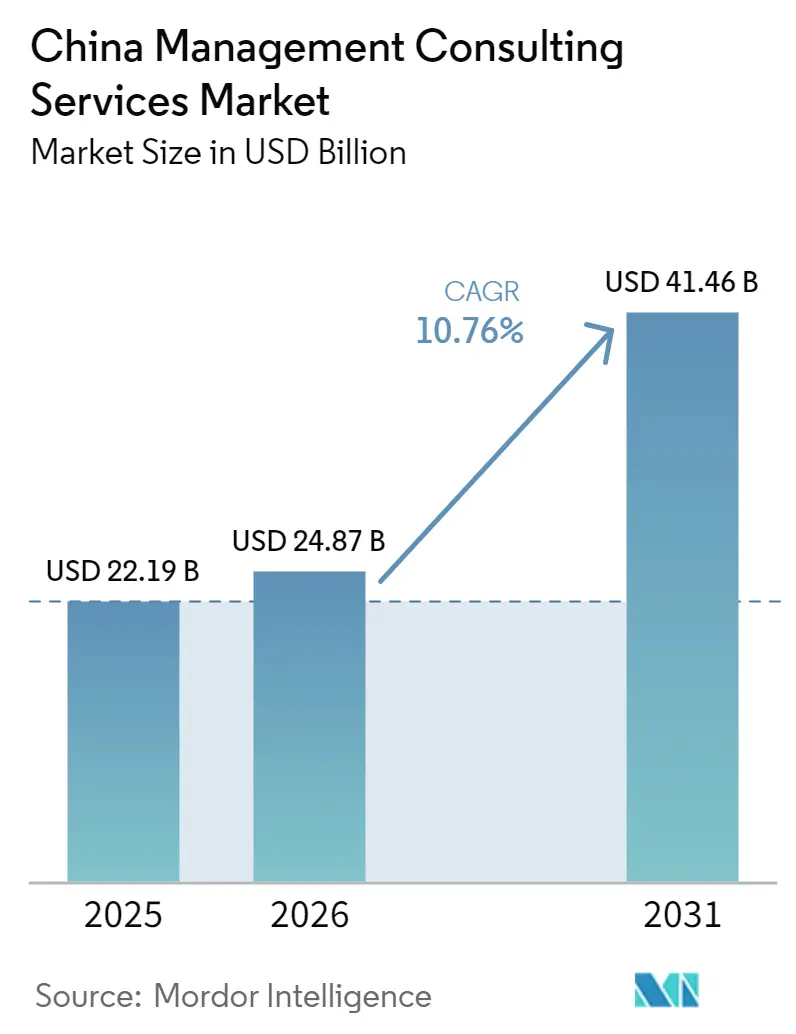

| Base Year Market Size (2025) | USD 22.19 Billion |

| Market Size (2026) | USD 24.87 Billion |

| Market Size (2031) | USD 41.46 Billion |

| Growth Rate (2026 - 2031) | 10.76% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Management Consulting Services Market Analysis by Mordor Intelligence

The China management consulting services market size is projected to be USD 22.19 billion in 2025, USD 24.87 billion in 2026, and reach USD 41.46 billion by 2031, growing at a CAGR of 10.76% from 2026 to 2031. State-led industrial upgrading, tighter environmental rules, and rapid adoption of generative AI are widening the advisory mandate across strategy, operations, and technology. The China management consulting services market is also benefiting from SOE digital-first directives in the 15th Five-Year Plan, while private enterprises turn to AI-enabled consulting to offset margin pressure. Belt and Road outbound activity sustains cross-border engagements even as foreign firms adjust to stringent data-security enforcement. Hybrid delivery models that blend on-site workshops with remote analytics are expanding the China management consulting services market footprint beyond tier-1 cities, lowering cost-to-serve and unlocking demand in emerging regional clusters.

Key Report Takeaways

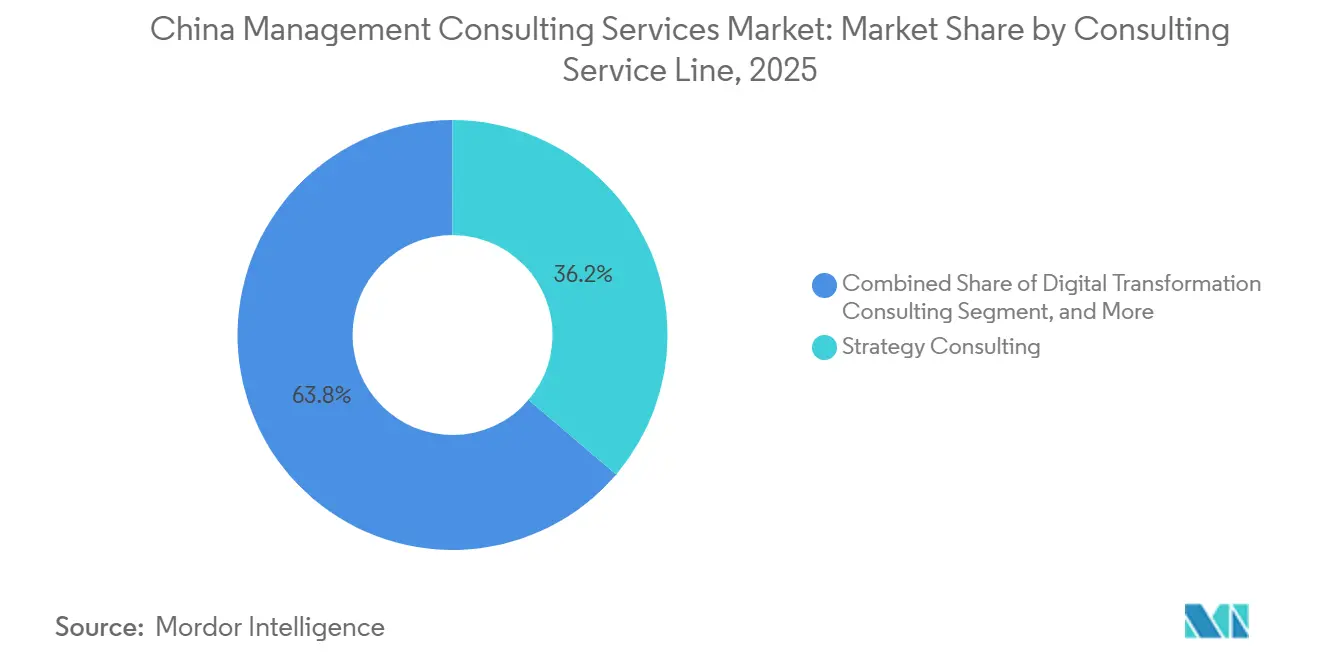

- By consulting service line, strategy consulting led with 36.23% of the China management consulting services market share in 2025, while Digital Transformation Consulting is advancing at an 11.08% CAGR to 2031.

- By organization size, large enterprises held 64.32% of the China management consulting services market size in 2025 and SMEs are projected to grow at a 10.91% CAGR between 2026-2031.

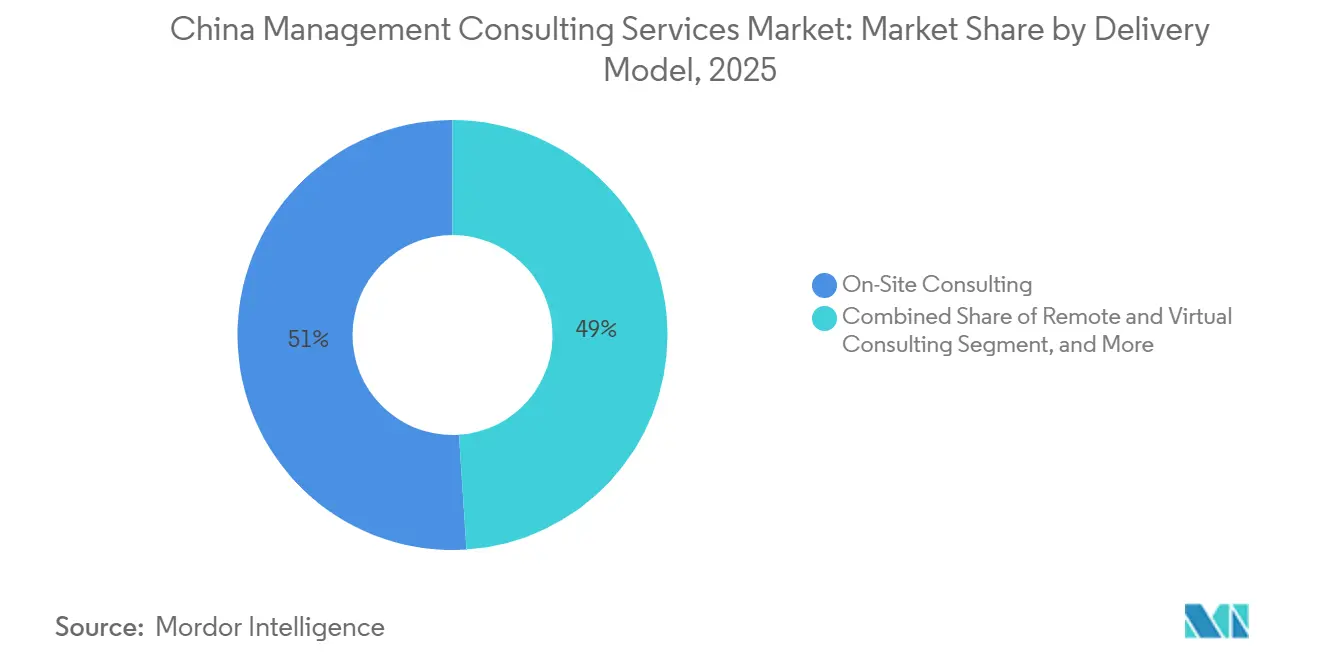

- By delivery model, on-site consulting accounted for 51.04% of 2025 revenue, whereas Remote and Virtual Consulting is rising at a 12.16% CAGR through 2031.

- By end user, manufacturing commanded 34.13% spending in 2025 and Healthcare is forecast to expand at 11.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-First Transformation Mandates From SOEs and Private Giants | +2.8% | National, concentrated in Beijing, Shanghai, Guangdong, Jiangsu | Medium term (2-4 years) |

| Regulatory Push for Carbon-Neutral Transition Roadmaps | +2.3% | National, early gains in Shanxi, Inner Mongolia, Hebei | Long term (≥ 4 years) |

| Accelerated Demand for Gen-AI-Enabled Productivity Consulting | +2.1% | National, early adoption in Beijing, Shanghai, Shenzhen, Hangzhou | Short term (≤ 2 years) |

| Belt-and-Road Outbound Projects Requiring Advisory Support | +1.4% | National with spillover to Southeast Asia, Central Asia, Middle East and Africa | Medium term (2-4 years) |

| Compliance Advisory Surge From State-Guided Industrial Funds | +1.2% | National, focus on semiconductors, new energy, biotech | Medium term (2-4 years) |

| Wave of Mid-Cap CFO Turnover Driving Finance-Transformation Projects | +0.9% | National, concentrated in manufacturing and consumer sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Digital-First Transformation Mandates from SOEs and Private Giants

State-owned enterprises are executing digital mandates set in the 15th Five-Year Plan that call for industrial digitalization, intelligent manufacturing, and data-driven decision making.[1]Ministry of Industry and Information Technology, “Industrial Digital Transformation Blueprint,” miit.gov.cn Over 2,000 digital workshops and smart factories were completed by the end of the 14th plan period, creating a lasting pipeline for ERP modernization, supply-chain optimization, and operations consulting. Private groups mirror this effort to relieve margin stress; Shanghai Huayi Group realized 33% productivity gain, 20% cost reduction, and 31% energy savings after rolling out 28 Industry 4.0 use cases. Consulting demand therefore spans strategic road-mapping, systems integration, and workforce upskilling. Because many SOEs now tie executive incentives to digital KPIs, budgets for advisory support are ring-fenced against cyclical downturns. The China management consulting services market gains durable revenue visibility from these multi-year programs.

Regulatory Push for Carbon-Neutral Transition Roadmaps

China’s pledge to peak carbon emissions by 2030 and reach neutrality in 2060 compels every energy-intensive sector to draft transition playbooks. Consulting firms offer ESG diagnostics, carbon accounting, and climate-risk disclosure frameworks that comply with guidelines issued by the National Development and Reform Commission and the Ministry of Ecology and Environment. Financial institutions alone must align portfolios with the People’s Bank of China’s taxonomy; the domestic green-finance market surpassed RMB 30 trillion (USD 4.23 trillion) in 2025.[2]Green Finance Development Center, “China Green Finance Market Report 2025,” greenfinance.org.cn KPMG China joined the Partnership for Carbon Accounting Financials in December 2025, signaling wider market focus on financed-emission measurement.[3]KPMG China, “Joining Partnership for Carbon Accounting Financials,” kpmg.com Provincial governments also procure transition-planning advice to distribute emission quotas, broadening the China management consulting services market across public and private sectors.

Accelerated Demand for Gen-AI-Enabled Productivity Consulting

Chinese enterprises are deploying large language models to automate customer service, product design, and knowledge management. Consulting firms, often in tandem with domestic cloud providers, guide clients through rapid prototyping and controlled scaling. The Ministry of Industry and Information Technology’s AI Plus Manufacturing roadmaptargets USD 70 billion in core AI revenue by 2025 and USD 140 billion by 2030, framing a sizeable advisory gap.[4]Accenture, “Generative AI Deployment Playbook,” accenture.com Early projects focus on measurable gains like automated inquiry handling and demand forecasting, delivering quick ROI that justifies further spend. Concerns about data sovereignty and algorithmic bias position consultants as neutral arbiters who can craft governance policies and oversee change management. Consequently, the China management consulting services market sees growing retainer-based AI engagements.

Belt-and-Road Outbound Projects Requiring Advisory Support

Outbound investment reached USD 174.4 billion in 2025, with cross-border mergers and acquisitions climbing 40% to USD 43.6 billion. Infrastructure, energy, and healthcare projects across Southeast Asia, Central Asia, and the Middle East and Africa demand due diligence, regulatory navigation, and post-merger integration advisory. Consulting firms also help clients comply with host-country environmental and local-content rules while mitigating geopolitical risks.[5]Fidinam, “Belt and Road Advisory Analysis,” fidinam.com The resulting multi-layered service mix enlarges the China management consulting services market beyond domestic boundaries, especially for firms with multilingual, on-the-ground teams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Economic Soft Patch Squeezing Discretionary Consulting Spend | -1.6% | National, pressure in consumer, real estate, export-dependent sectors | Short term (≤ 2 years) |

| Tighter Data-Security Rules Limiting Foreign Firms’ Access | -1.3% | National, heightened enforcement in Beijing, Shanghai, Shenzhen | Medium term (2-4 years) |

| AI Chatbots Cannibalizing Entry-Level Consulting Revenues | -0.8% | National, early impact in tier-1 cities and technology sectors | Short term (≤ 2 years) |

| National-Security Scrutiny Delaying Foreign Engagements | -0.7% | National, focus on technology, defense, critical infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Economic Soft Patch Squeezing Discretionary Consulting Spend

Household consumption growth lags GDP amid weak property sentiment and elevated youth unemployment, so private clients trim non-essential advisory budgets.[6]International Monetary Fund, “China Consumption Trends,” imf.org Retailers and real estate developers delay brand-strategy or expansion projects, favoring cost-reduction and turnaround assignments. KPMG’s 2025 survey showed 83% of multinationals in China shifting focus toward localization and efficiency, compressing scope for growth-oriented consulting. Consulting firms respond by bundling outcome-linked pricing and targeting counter-cyclical demand such as regulatory compliance. Although the drag is temporary, it moderates revenue velocity in the China management consulting services market through 2027.

Tighter Data-Security Rules Limiting Foreign Firms’ Access

The Personal Information Protection Law and companion cybersecurity statutes restrict cross-border data transfers and mandate onshore storage.[7]China Briefing, “Understanding the PIPL,” china-briefing.com Foreign consultancies must secure explicit client consent and run local data centers, raising cost and slowing project kick-off. High-profile raids on consultancies in 2023 amplified caution, with some firms declining sensitive SOE engagements to avoid scrutiny. Domestic competitors exploit regulatory proximity to win market share, particularly in sectors where data sensitivity is acute. Over time, these frictions reallocate portions of the China management consulting services market to local players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Strategy Still Dominates While Digital Transformation Accelerates

Strategy Consulting generated the largest slice of 2025 revenue, supplying 36.23% of the China management consulting services market share through SOE restructuring and carbon-transition mandates. Digital Transformation Consulting, however, is forecast to expand at 11.08% CAGR, becoming the fastest moving segment within the China management consulting services market size between 2026-2031. Clients now seek integrated offerings that embed AI, cloud, and analytics into core workflows, shifting spend from high-level road-mapping toward execution. Operations Consulting rides the smart-manufacturing wave, illustrated by Shanghai Huayi Group’s double-digit productivity lift after 28 Industry 4.0 projects. Meanwhile, HR and Financial Advisory lines capture opportunity from CFO turnover and rising cross-border M&A volumes. Risk and Compliance services continue to escalate as data-security statutes tighten. Collectively, these shifts rebalance wallet share across service lines without dislodging Strategy’s primacy.

Consultancies differentiate by packaging rapid-prototype sprints, proprietary AI governance frameworks, and pay-for-performance clauses. This model aligns with enterprises’ emphasis on measurable outcomes and cost certainty. As Digital Transformation engagements scale, firms weave in change management and workforce reskilling, generating follow-on opportunities. The resulting blend of strategy visioning and technology enablement keeps the China management consulting services market vibrant while elevating execution-heavy fees.

By Organization Size: Large Enterprises Prevail Yet SMEs Gain Momentum

Large Enterprises represented 64.32% of 2025 billings, reflecting their appetite for multi-year ERP, finance-transformation, and carbon-neutrality programs that anchor recurring advisory needs. Government-backed lenders and capital-market access allow blue-chip clients to sustain consulting budgets even during macro headwinds, preserving the base of the China management consulting services market. SMEs, however, are poised for 10.91% CAGR growth through 2031 as the Ministry of Industry and Information Technology’s April 2026 cultivation measures free funding for 17,600 “little giant” innovators and more than 600,000 tech-oriented SMEs. These companies seek modular compliance and innovation packages that fit leaner operating models, inviting consultants to deploy remote delivery and templated toolkits.

SME industrial output rose 6.9% in 2025, while profit at computer, communication, and electronics SMEs jumped 49.1%, underscoring paying capacity for targeted advisory. Municipal rules, such as Shanghai’s 2025 SME governance code, further stimulate demand for environmental audits, labor-standard alignment, and financial controls. Consequently, the China management consulting services market is broadening its client mix, with many firms launching separate SME practices that balance volume with streamlined scope.

By Delivery Model: On-Site Prevails While Remote Surges

On-Site Consulting generated 51.04% of 2025 revenue, confirming that face-to-face workshops remain the default for high-stakes projects such as SOE restructuring and carbon-transition planning within the China management consulting services market. Clients view in-person engagement as essential for executive alignment, data-room access, and confidential discussions, so most large-ticket mandates still budget travel and accommodation for core teams. Even so, hybrid approaches now thread virtual analytics into on-site sprints, compressing timelines and lowering billable hours without sacrificing quality. Deloitte China institutionalized its pandemic-era remote tool kit into standard offerings that let partners oversee multiple provinces in parallel. YCP Group’s hybrid structure blends local market teams with off-site analysts to cut costs for multinational clients seeking regional scale. These examples show how vendors protect pricing power by packaging efficiency gains rather than discounting day rates.

Remote and Virtual Consulting is forecast to grow at a 12.16% CAGR through 2031, the fastest rate among delivery modes inside the China management consulting services market. Generative-AI collaboration suites now automate first-draft research, storyboard generation, and progress dashboards, enabling junior staff to support more engagements simultaneously. Domestic suppliers leverage these tools to reach tier-2 and tier-3 cities without opening permanent offices, expanding geographic coverage at marginal cost. Clients accept screen-share diagnostics and asynchronous workshops when the brief centers on data modeling, compliance checklists, or training roll-outs. Over time, remote models will penetrate complex mandates as trust in cloud security rises and regulators allow encrypted video for sensitive discussions. That trend enlarges the total addressable pool of price-sensitive SMEs even while on-site remains entrenched for transformation programs at state-owned conglomerates.

By End-User Industry: Manufacturing Leads While Healthcare Accelerates

Manufacturing captured 34.13% of 2025 consulting spend, reflecting its push to install about 2,000 smart workshops and intelligent factories during the 14th Five-Year Plan. Digital-thread projects covering MES, predictive maintenance, and supply-chain synchronization dominate statements of work, so the China management consulting services market continues to book multi-year backlogs from petrochemicals, equipment, and electronics plants. Consultants translate national guidelines into site-level blueprints, benchmark energy intensity, and manage vendor tenders, then cycle into change-management and worker-upskilling phases. This repeatable pattern secures sticky revenue and anchors the China management consulting services market size for operations and technology practices. Demand also benefits from export clients adopting EU carbon-border rules, which inject advisory needs around product life-cycle audits and green-label certification.

Healthcare is forecast to grow at 11.42% CAGR through 2031, making it the quickest industry mover inside the China management consulting services market. Public hospital reforms, DRG and DIP payment pilots across more than 130 and 110 cities respectively, and the Healthy China 2030 plan are pushing administrators to redesign billing, clinical pathways, and digital health platforms. Consultants assist with activity-based costing, supply-chain sterilization, and AI-driven radiology, generating high-value road maps that stretch over several budget cycles. Medical-tourism volumes reached 1.28 million visits in 2025, triggering projects on patient experience and international accreditation. As provincial governments subsidize elder-care and chronic-disease management pilots, niche firms specializing in facility workflow and regulatory submissions are scaling quickly, further diversifying the China management consulting services market share across end users.

Geography Analysis

Tier-1 cities, Beijing, Shanghai, Guangzhou, and Shenzhen, continue to account for the bulk of fees as they host most SOE headquarters, multinational Asia-Pacific hubs, and venture-backed tech unicorns. Beijing’s 2025 work report targeted 5% GDP growth with a heavy tilt toward digital-economy and green-finance pillars, reinforcing advisory demand for cloud migration, ESG disclosure, and innovation-ecosystem design. Shanghai set an RMB 4.7 trillion (USD 0.66 trillion) GDP goal for 2025, emphasizing advanced manufacturing and cross-border trade facilitation; consultants therefore secure mandates on supply-chain rerouting, trade-compliance automation, and international tax structuring. Guangzhou and Shenzhen channel spend into semiconductor, electric-vehicle, and biotech strategy engagements, as local authorities compete to anchor emerging clusters, keeping the China management consulting services market firmly rooted in the Pearl River Delta.

Tier-2 and tier-3 cities are delivering the fastest incremental growth because hybrid delivery allows reputable firms to advise without maintaining costly physical offices. Jiangsu, Shandong, Anhui, Hubei, Hunan, and inland hubs like Chengdu now host smart-factory pilots funded from central subsidies, each requiring readiness assessments and vendor-selection support. Regional integration initiatives such as the Yangtze River Delta and the Greater Bay Area create cross-jurisdiction supply-chain questions that reward consultants able to model tax incentives and logistics nodes across multiple provinces. Labor-market frictions differ by tier, so HR consulting related to attrition in new-economy firms rises outside of Beijing and Shanghai. These projects expand the geographic diversity of the China management consulting services market size and help large partnerships move beyond saturated coastal metros.

Provincial governments themselves constitute a growing client base. Shanxi, Inner Mongolia, and Hebei need carbon-transition road maps that reconcile national emission caps with local employment targets, leading to procurement of scenario models and stakeholder workshops. The Belt and Road Initiative also introduces outbound assignments where consultants coordinate between Chinese municipal investors and host-country agencies in Southeast Asia or Central Asia. Because local-currency contracts can now be settled through cross-border digital RMB pilots, smaller coastal cities experiment with international project-management offices, a trend expected to widen consulting penetration. Cumulatively, the broadening footprint strengthens the resilience of the China management consulting services market against single-region slowdowns.

Competitive Landscape

The China management consulting services market remains fragmented, as the Big Four and MBB hold notable yet non-dominant shares alongside domestic specialists such as CITIC Consulting, China Insights Consultancy, and KMIND Consulting. Data-security regulation has become a competitive separator; foreign brands form joint ventures with local cloud providers and open onshore data centers to maintain eligibility for public-sector bids. KPMG China’s late-2025 entry into the Partnership for Carbon Accounting Financials illustrates how established players reposition toward ESG and financed-emission metrics, carving out a defensible niche. Deloitte’s Joint Innovation Center with Digital China integrates generative-AI modules that automate due diligence and slide production, freeing senior talent for C-suite advisory.

Domestic challengers exploit speed and regulatory familiarity. China Insights Consultancy leverages its one-million-member expert network to validate market sizing within 48 hours, winning bids where incumbents once relied on lengthy interviews. KMIND Consulting boasted a 100% client-renewal rate in 2024 and topped Vault’s APAC innovation chart, signaling buyer willingness to trust agile boutiques. AI-native upstarts further erode entry-level margins by offering subscription dashboards that replace manual benchmarking, pressuring traditional firms to climb the value chain. Still, large partnerships defend share through integrated tax, audit, and consulting bundles that align with SOE procurement frameworks. The resulting dynamic keeps pricing rational yet forces steady capability refresh across the China management consulting services market.

Competition also intensifies in the SME arena. Advisory packages tuned for “little giant” firms combine compliance checklists, grant-application playbooks, and templated digital-transformation sprints priced at a fraction of enterprise engagements. Foreign entrants often hesitate because deal sizes are smaller and require local credit-risk underwriting, so domestic firms command the field. Nevertheless, multi-nationals with scalable IP may white-label toolkits through city-level incubators, capturing royalty streams without front-line delivery. Overall, rivalry pivots on speed, localized IP, and regulatory fluency rather than raw headcount, shaping a moderately concentrated yet fluid China management consulting services market share structure.

China Management Consulting Services Industry Leaders

Accenture plc

Deloitte Touche Tohmatsu Limited (Deloitte Consulting)

PricewaterhouseCoopers Advisory Services Ltd.

Ernst & Young Advisory Ltd.

McKinsey & Company, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The Ministry of Industry and Information Technology’s revised SME cultivation measures took effect, activating new consulting budgets for 17,600 “little giant” firms and over 600,000 tech-focused SMEs.

- February 2026: EY Greater China published its outbound-investment overview showing 2025 ODI at USD 174.4 billion, with cross-border M&A up 40% to USD 43.6 billion.

- February 2026: President Xi Jinping visited a technology innovation park, underscoring national commitment to self-reliance and R&D acceleration.

- December 2025: KPMG China joined the Partnership for Carbon Accounting Financials, aligning its advisory with financed-emission disclosure needs.

China Management Consulting Services Market Report Scope

The China Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the projected value of the China management consulting services market by 2031?

The China management consulting services market is forecast to reach USD 41.46 billion by 2031.

Which consulting service line is growing fastest through 2031?

Digital Transformation Consulting is expected to rise at an 11.08% CAGR as enterprises embed generative AI, cloud, and analytics capabilities.

Why are SMEs becoming an important client segment for consultants in China?

Revised cultivation measures effective Apr 2026 unlock advisory budgets for 17,600 "little giant" firms and hundreds of thousands of tech-oriented SMEs, lifting compliance and innovation demand.

How are data-security regulations reshaping competition among consulting firms?

The Personal Information Protection Law requires onshore data storage and explicit consent, favoring domestic consultancies and joint-venture models while adding cost for foreign entrants.

Which end-user industry shows the highest growth potential for consulting spend?

Healthcare is projected to expand at an 11.42% CAGR through 2031, driven by hospital payment reforms and digital-health adoption.

What delivery model trend is most pronounced in China's consulting scene?

Remote and virtual engagements are growing at a 12.16% CAGR as AI-powered collaboration tools let firms serve tier-2 and tier-3 cities without large travel budgets.

Page last updated on: