Taiwan Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

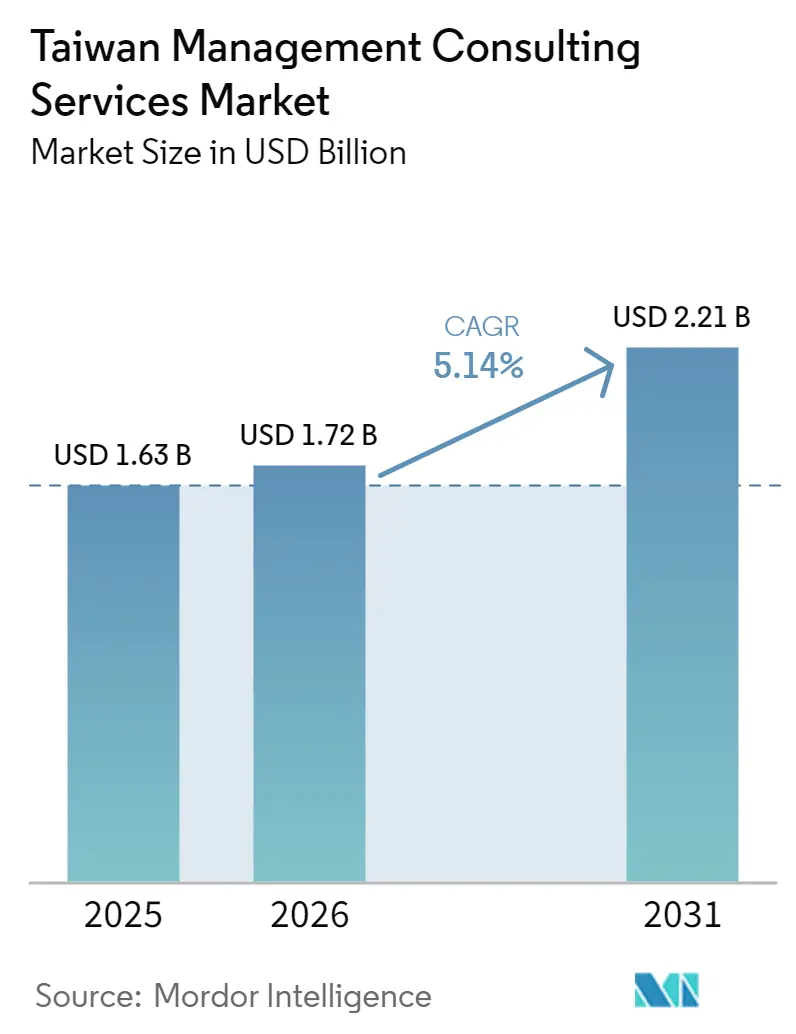

| Base Year Market Size (2025) | USD 1.63 Billion |

| Market Size (2026) | USD 1.72 Billion |

| Market Size (2031) | USD 2.21 Billion |

| Growth Rate (2026 - 2031) | 5.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Taiwan Management Consulting Services Market Analysis by Mordor Intelligence

The Taiwan management consulting services market size is expected to increase from USD 1.63 billion in 2025 to USD 1.72 billion in 2026 and reach USD 2.21 billion by 2031, growing at a CAGR of 5.14% over 2026-2031. Digital-first public-sector mandates, fast-scaling semiconductor near-shoring projects, and a coordinated push toward a 2050 net-zero economy are redirecting enterprise spending from pure hardware upgrades to consulting-led transformation programs. Demand is strongest where operational bottlenecks converge with new regulatory benchmarks, especially in AI-governance, carbon accounting, and supply-chain cybersecurity. Consulting firms that blend sector know-how with bilingual delivery enjoy a first-mover edge, yet experience sustained cost pressure as small and medium-sized enterprises (SMEs) negotiate outcome-based contracts. Fragmented talent pools and a growing preference for hybrid engagement models moderate growth but do not derail the structural uptrend.

Key Report Takeaways

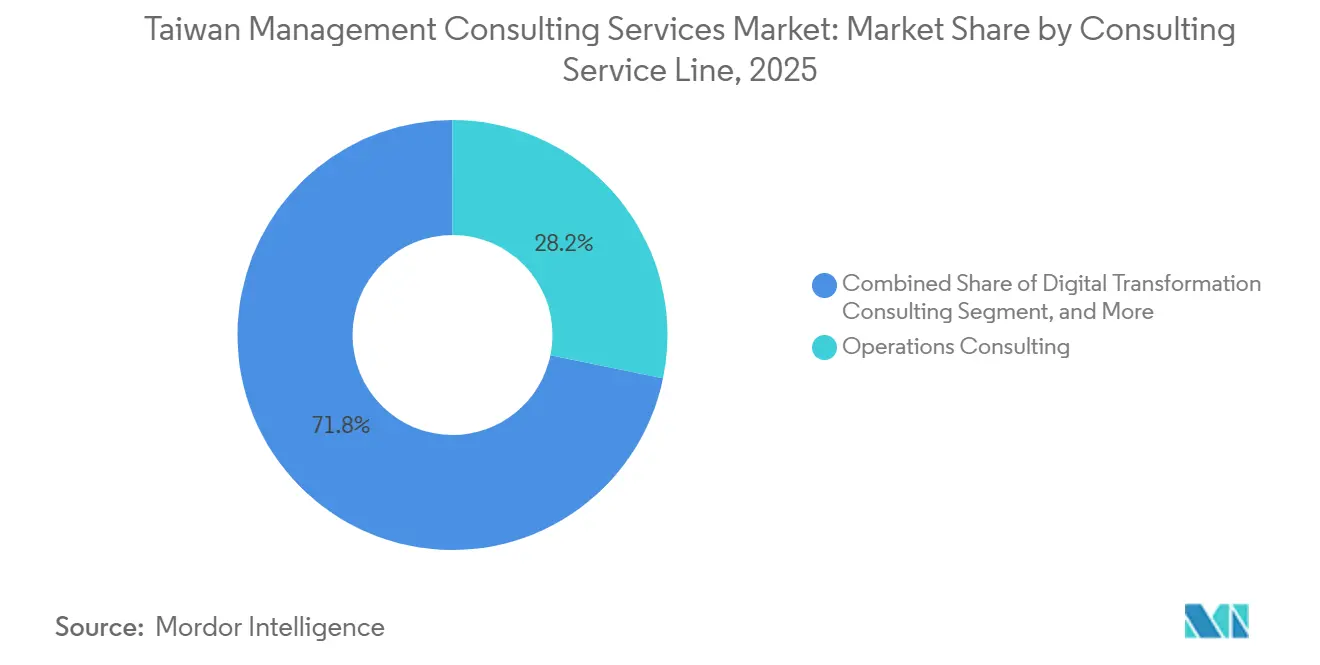

- By consulting service line, Operations Consulting led with 28.23% of 2025 spending, while Digital Transformation Consulting is projected to expand at a 5.89% CAGR through 2031.

- By organization size, Large Enterprises commanded 70.79% of 2025 expenditure, whereas SMEs are forecast to grow at 5.67% and progressively narrow the gap by 2029.

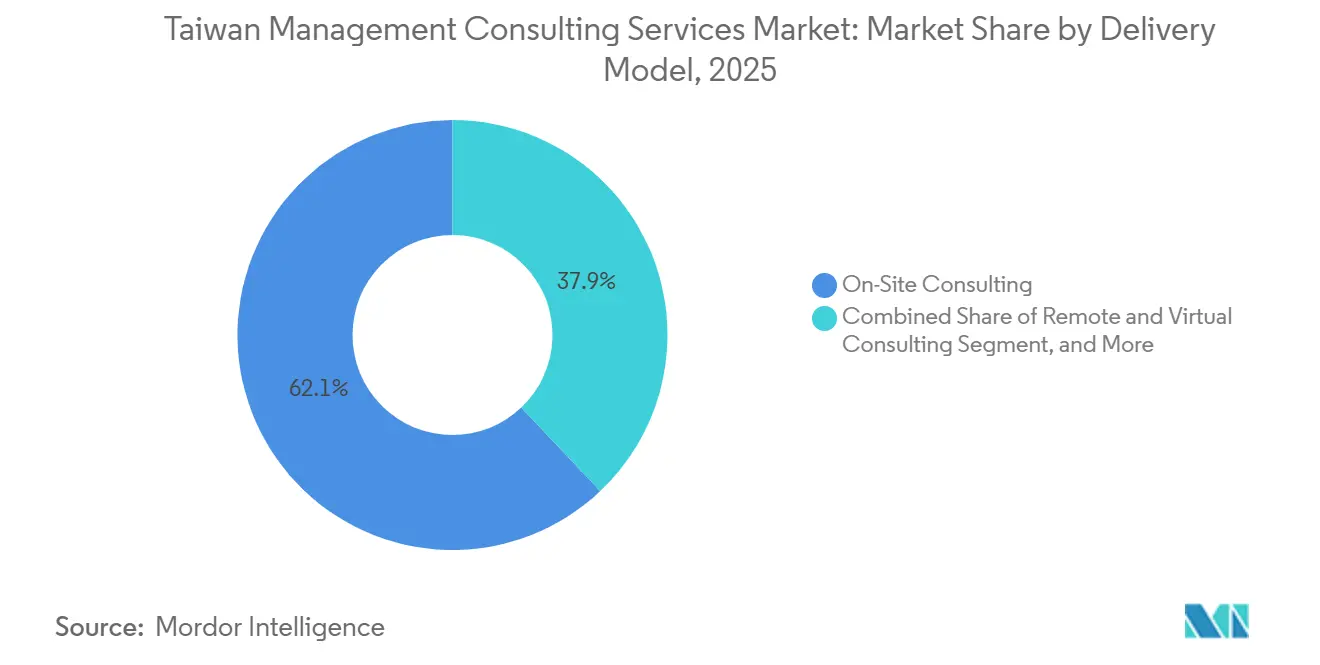

- By delivery model, On-Site Consulting captured 62.07% in 2025, yet Remote and Virtual Consulting is advancing at 5.76% as hybrid work practices normalize.

- By end user industry, Banking and Insurance held 22.13% of 2025 demand, while Healthcare is expected to accelerate at a 5.92% CAGR on the back of the national AI-health program.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Taiwan Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-Transformation Acceleration Across Taiwanese Enterprises | +1.4% | Taipei, Hsinchu, Taichung | Medium term (2-4 years) |

| Government Smart Taiwan 2030 and Net-Zero Road-Map Incentives | +1.2% | Taipei, New Taipei, Taoyuan, Kaohsiung | Long term (≥ 4 years) |

| Cross-Border M and A and Regional Expansion by Local Conglomerates | +0.9% | National, spill-over to ASEAN and North America | Medium term (2-4 years) |

| Semiconductor Near-Shoring Creating Niche Consulting Demand | +0.8% | Hsinchu, Tainan, with links to Arizona and Kumamoto | Long term (≥ 4 years) |

| Urgent Cyber-Resilience Requirements From Global Clients | +0.5% | National electronics supply chains | Short term (≤ 2 years) |

| AI-Powered Manufacturing Upgrades in SME Cluster Parks | +0.4% | Taichung, Tainan, Kaohsiung | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital-Transformation Acceleration Across Taiwanese Enterprises

Taiwan’s 1.71 million SMEs and its flagship electronics manufacturers are migrating toward cloud-native architectures and edge-AI applications, shifting budgets from license renewals to consulting-driven redesign. The Ministry of Digital Affairs’ MyData project, which onboarded 83 agencies and processed more than 55,000 open datasets by late 2025, illustrates how policy sets de-facto technical standards that private firms must meet. Chunghwa Telecom earmarked NTD 31.91 billion (USD 1.03 billion) for 5G-Advanced in 2026, creating new advisory work in network optimization.[1]Chunghwa Telecom, “2026 Capital Expenditure Guidance,” cht.com.tw Regulated industries follow suit: E.SUN Financial adopted IBM watsonx.governance in 2025, outsourcing model-risk controls to external experts. Industrial Development Administration (IDA) programs assisted 126 manufacturers in 2025, with 70% prioritizing efficiency upgrades.[2]Industrial Development Administration, “Assistance Programs for Manufacturers,” moeaidb.gov.tw Together, these moves sustain above-trend demand for operations and digital-transformation consulting through 2028.

Government Smart Taiwan 2030 and Net-Zero Road-Map Incentives

Smart Taiwan 2030 aligns artificial intelligence, healthcare modernization, and clean-energy targets under a single policy umbrella, generating multi-year pipelines for strategy and compliance consulting. The Ministry of Health and Welfare’s NTD 10 billion (USD 322 million) AI-health program with Google aims to deploy predictive diagnostics across regional hospitals by 2027. A national cybersecurity budget of NTD 8.8 billion (USD 301 million) mandates SEMI E187 and ISO 27001 adherence, pushing risk-management engagements into the semiconductor and public-sector domains. Monthly mitigation of over 1.3 billion cyberattacks signals an urgent need for sovereign-tech architectures consultancies can later export.[3]Ministry of Digital Affairs, “Three Arrows Policy and MyData Platform,” moda.gov.tw Offshore wind and green-hydrogen roadmaps expand sustainability advisory work, with peak influence expected between 2027 and 2030.

Cross-Border M&A and Regional Expansion by Local Conglomerates

Taiwanese conglomerates accelerate acquisitions in ASEAN and North America to derisk supply chains and capture demand close to end markets. National M and A value hit USD 12.8 billion in 2024, with sub-USD 50 million bolt-on deals up 24% year-over-year. Delta Electronics bought Vivotek for NTD 3.73 billion (USD 119 million) in December 2025, integrating IP-surveillance capabilities. Micron’s January 2026 purchase of PSMC’s P5 fab for USD 1.8 billion exemplifies foreign direct investment that requires navigation of Taiwan’s export-control regime.[4]Micron, “PSMC P5 Fab Acquisition,” micron.com Baker McKenzie’s 2025 forums underscore continued appetite for cross-border legal and strategic counsel. As friend-shoring strategies intensify, multi-jurisdictional consultancies gain share through 2029.

Semiconductor Near-Shoring Creating Niche Consulting Demand

A USD 500 billion US-Taiwan framework and TSMC’s USD 165 billion capex plan through 2032 spur parallel fab builds in Arizona, Kumamoto, and Dresden, all requiring localization playbooks. SEMI E187 raises the bar for cybersecurity audits in equipment supply chains.[5]SEMI, “SEMI E187 Cybersecurity Standard,” semi.org TSMC’s Arizona site, moving into volume production in 2025, forces consultancies to translate Taiwanese process rigor into US environmental and labor codes. ITRI’s NTD 25.5 billion (USD 822 million) annual budget and 2035 technology roadmap provide R&D touchpoints for advisory projects on chiplets and heterogeneous integration. High-margin niche engagements remain lucrative until knowledge playbooks commoditize after 2032.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Bilingual Domain-Specialist Consultants | -0.6% | Hsinchu, Tainan, Taichung | Short term (≤ 2 years) |

| Intensifying Competition From Global Tier-1 Consultancies | -0.5% | Taipei | Medium term (2-4 years) |

| High Price Sensitivity of SMEs Facing Post-Pandemic Margin Pressure | -0.3% | Traditional manufacturing clusters | Short term (≤ 2 years) |

| Brain Drain to Emerging In-House Digital COEs Within Tech Giants | -0.2% | Hsinchu Science Park, Taipei | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Bilingual Domain-Specialist Consultants

Universities graduate fewer than 500 engineers a year who can pair Mandarin-English fluency with deep semiconductor or carbon-accounting knowledge, limiting project staffing flexibility. The Taichung Precision Machinery Park, home to 1,000-plus machine-tool firms, reports acute shortages of automation engineers ready for AI-enabled predictive maintenance McKinsey, TSMC, and MediaTek compete for the same talent pool, inflating compensation and elongating delivery timelines.[6]McKinsey, “Taiwan Office Focus Areas,” mckinsey.com Parallel demand for NIST-aligned cybersecurity skills further stretches resources. Relief is unlikely before 2027, when university-industry pipelines begin to mature.

Intensifying Competition from Global Tier-1 Consultancies

Deloitte’s Asia-Pacific Agentic AI Center (2025), EY-Parthenon’s 2026 expansion, and KPMG’s Greater South offices (2025) raise service benchmarks and compress price points. PwC’s Taiwan-US platform showcases multi-jurisdiction delivery that local boutiques cannot match. BCG and McKinsey leverage two-decade footprints to lock in cross-border mandates. Niche research-advisory hybrids must differentiate on sector depth rather than pricing. Margin pressure is most acute between 2026 and 2028 as global players finish Taiwan buildouts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Digital Transformation Surges Past Operations

Operations Consulting accounted for the largest 2025 spending slice, yet Digital Transformation engagements headline growth through 2031. Enterprises modernize legacy enterprise-resource-planning stacks, deploy AI-driven maintenance, and interconnect data lakes, creating double-digit project pipelines. Taiwan management consulting services market size for Digital Transformation is projected to widen its lead as cloud migration and real-time analytics become standard procurement checklists. Risk and compliance consulting grows in parallel as SEMI E187 and ISO 27001 audits migrate from ad-hoc to mandatory. Telecom operators such as Chunghwa Telecom illustrate crossover demand, outsourcing spectrum planning to consultancies versed in both network physics and cloud economics. Overall, digital mandates are reshaping staffing profiles toward data engineers and industry-certified cybersecurity analysts.

Continued demand for strategy work rides the M&A wave, while HR consulting captures reskilling agendas aimed at retaining semiconductor engineering talent. Financial advisory retains relevance around Taiwan management consulting services market share for transactional activity, yet pricing remains tied to deal volumes. Emerging sustainability advisory practices monetize the net-zero legislative push, integrating carbon baselining with supply-chain redesign. Collectively, the service-line portfolio underscores how digital narratives increasingly anchor value propositions.

By Organization Size: SMEs Close the Distance

Large Enterprises still anchor the Taiwan management consulting services market, spending heavily on cross-border due diligence, multi-cloud governance, and ESG compliance. The scale of TSMC’s USD 165 billion capex plan alone sustains multi-year engagements. However, SMEs stand out as the fastest-growing client cohort, booking modular projects around e-commerce enablement and low-code analytics. Subsidy programs from the IDA reduce adoption friction, while fixed-fee packages mitigate budget uncertainty. Taiwan management consulting services market size for the SME segment benefits from self-service digital-advisory portals that lower entry thresholds.

Hybrid delivery further levels the field, allowing smaller manufacturers in Kaohsiung and Tainan to access Big Four toolkits without the travel overhead. KPMG’s Greater South Asset Innovation Platform exemplifies regional go-to-market innovation, offering dashboards, ESG templates, and supply-chain optimizers via subscription. As SMEs internalize digital capabilities, consultants must pivot toward continuous-improvement retainers rather than one-off transformation projects.

By Delivery Model: Hybrid Engagements Redefine Norms

On-Site Consulting remains dominant where process mapping on semiconductor fab floors or bank compliance walk-throughs cannot be virtualized. Yet a multiyear shift toward Remote and Virtual Consulting gains traction as clients normalize hybrid workforces. Taiwan management consulting services market share linked to virtual engagements is underpinned by cloud-native workspaces and secure video pipelines. Multinational campaigns, like PwC’s Taiwan-US corridor, run discovery sessions onshore, while execution shifts to distributed teams to compress timelines and travel spend.

Hybrid models, blending kickoff workshops with remote sprint cycles, are quickly standardizing. They balance the cultural emphasis on face-to-face trust with post-pandemic cost discipline. Consultancies refine playbooks for document co-authoring, digital white-boarding, and asynchronous stand-ups, targeting a high-touch yet low-travel equilibrium. Forecasts suggest the virtual component levels off near 25% of all billable hours by 2031, with hybrid formats soaking up incremental demand.

By End User Industry: Healthcare Accelerates, Banking Holds Scale

Banks and insurers stay the single largest client base thanks to stringent Financial Supervisory Commission rules on AI-model governance and open-banking security. Yet healthcare outpaces every other vertical, powered by the NTD 10 billion (USD 322 million) AI-health rollout. Taiwan management consulting services market size for healthcare projects spans clinical-workflow redesign, privacy-by-design data lakes, and precision-medicine reimbursement models. Hospitals require consultants to align predictive algorithms with patient consent and data-localization statutes.

Manufacturing continues as a core revenue pillar, driven by predictive maintenance and smart factory retrofits in IDA-supported industrial parks. Telecom operators extend consulting pipelines with 5G-Advanced network slicing and IoT backhaul tuning. Clean-energy developers tap advisory support on offshore wind bid structuring and hydrogen supply-chain economics, reflecting the policy-driven shift toward renewables. Public-sector digitalization remains an evergreen segment as ministries scale MyData use cases across citizen services.

Geography Analysis

Northern Taiwan anchored by Taipei and Hsinchu Science Park continues to command the dominant portion of consulting revenue. Headquarters density, semiconductor R&D clusters, and regulatory agencies keep project pipelines full, ensuring a steady mid-single-digit CAGR for the region through 2031. The Taiwan management consulting services market size related to northern clients expands as cross-border mandates and compliance programs cluster around capital city decision makers. On-site engagements in Hsinchu fabs and fintech sandboxes in Taipei account for many of the highest margin projects. Proximity to venture capital and bilingual talent further cements the region’s lead over other parts of the island.

Central Taiwan, led by Taichung Precision Machinery Park, shows rising demand in AI-enabled machine-tool upgrades and lean-manufacturing rollouts. Consulting firms adopt hybrid delivery to service scattered industrial townships, allowing mid-sized manufacturers to access Big Four toolkits without major travel costs. Uptake of predictive maintenance and cloud-based MES drives a healthy expansion rate that slightly outpaces the wider Taiwan management consulting services market. As more SMEs enroll in Industrial Development Administration subsidy programs, the area’s Taiwan management consulting services market share is expected to improve steadily through 2029.

Southern metros Kaohsiung and Tainan represent the fastest growing geography on the back of green-energy cluster investments and semiconductor back-end expansion. KPMG’s Greater South Asset Innovation Platform and similar initiatives from Deloitte position the region as a proving ground for outcome-based consulting subscriptions. Offshore wind staging ports, hydrogen pilots, and advanced-packaging facilities attract specialized advisory work in ESG strategy, supply-chain localization, and workforce reskilling. Cross-regional collaboration allows teams in the south to tap expertise from Taipei while delivering local execution, creating a balanced national footprint for the sector.

Competitive Landscape

The competitive field remains bifurcated between global networks and local specialists. Deloitte, PwC, EY, and KPMG secure large-enterprise mandates that require multi-jurisdiction tax, audit, and M&A support. Accenture, McKinsey, BCG, and Bain strengthen technology advisory depth through alliances with hyperscalers and semiconductor equipment vendors. These firms leverage offshore shared service centers to deliver analytics and code generation at scale, compressing project cycles and raising entry barriers for mid-tier rivals. Their collective hold on regulated-industry accounts underpins roughly 60% of billings, highlighting moderate concentration.

Local research-advisory hybrids such as TrendForce, DIGITIMES Research, and ITRI’s Industrial Economics and Knowledge Center win assignments where granular semiconductor intelligence is critical. They differentiate by providing proprietary wafer-price trackers, equipment lead-time dashboards, and technician reskilling curricula that large networks rarely productize. Boutique process-optimization shops in Taichung and Hsinchu pair domain depth with Mandarin-only delivery, commanding loyalty among SMEs that prize cultural affinity over brand scale. However ongoing wage inflation and limited succession planning expose smaller players to acquisition overtures from regional mid caps looking to build scale fast.

Competitive tactics now center on sector-specific centers of excellence, subscription-based SME portals, and generative-AI tooling that automates research and draft deliverables. Deloitte’s Agentic AI hub in Taipei, EY’s Parthenon analytics pods, and KPMG’s Greater South office exemplify location-anchored talent plays that feed larger Asia Pacific delivery chains. Outcome-based pricing gains traction in energy-transition and carbon-accounting engagements, rewarding firms able to quantify avoided emissions or throughput gains. With global players finalizing Taiwan buildouts by 2028, market-share battles are set to peak then taper as mid-tier consolidation gradually raises the market concentration score.

Taiwan Management Consulting Services Industry Leaders

Deloitte Touche Tohmatsu Limited

PricewaterhouseCoopers (PwC)

Ernst & Young (EY)

KPMG

Accenture Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Chunghwa Telecom signed an MoU with Nokia to co-develop 5G-Advanced and pre-6G technologies, opening advisory opportunities in spectrum optimization and IoT integration.

- March 2026: EY-Parthenon expanded its Taiwan presence to capture rising M&A advisory demand stemming from supply-chain diversification.

- January 2026: Micron acquired PSMC’s P5 fab for USD 1.8 billion, underscoring the role of consultants in foreign-investment approval and tech-export compliance.

- December 2025: Delta Electronics completed its NTD 3.73 billion (USD 119 million) purchase of Vivotek, boosting demand for valuation and post-merger integration services.

Taiwan Management Consulting Services Market Report Scope

The Taiwan Management Consulting Services Market Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current size of the Taiwan management consulting services market?

The market stands at USD 1.72 billion in 2026 and is projected to reach USD 2.21 billion by 2031.

How fast is the market expected to grow over 2026-2031?

It is forecast to expand at a 5.14% CAGR during the 2026-2031 period.

Which consulting service line is expanding the fastest in Taiwan?

Digital Transformation Consulting leads growth with a projected 5.89% CAGR through 2031.

Why are SMEs becoming an important client segment for consultancies?

Government incentives, modular service packages, and lower hybrid-delivery costs enable 1.71 million SMEs to invest steadily in digital transformation.

Which end user industry is projected to be the fastest growing?

Healthcare shows the highest momentum, supported by a NTD 10 billion (USD 322 million) AI-health initiative targeting predictive diagnostics by 2027.

How are hybrid consulting models influencing project delivery?

Hybrid engagements blend on-site kickoffs with remote execution, trimming travel costs and allowing firms to serve geographically dispersed clients more efficiently.

Page last updated on: