Thailand Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

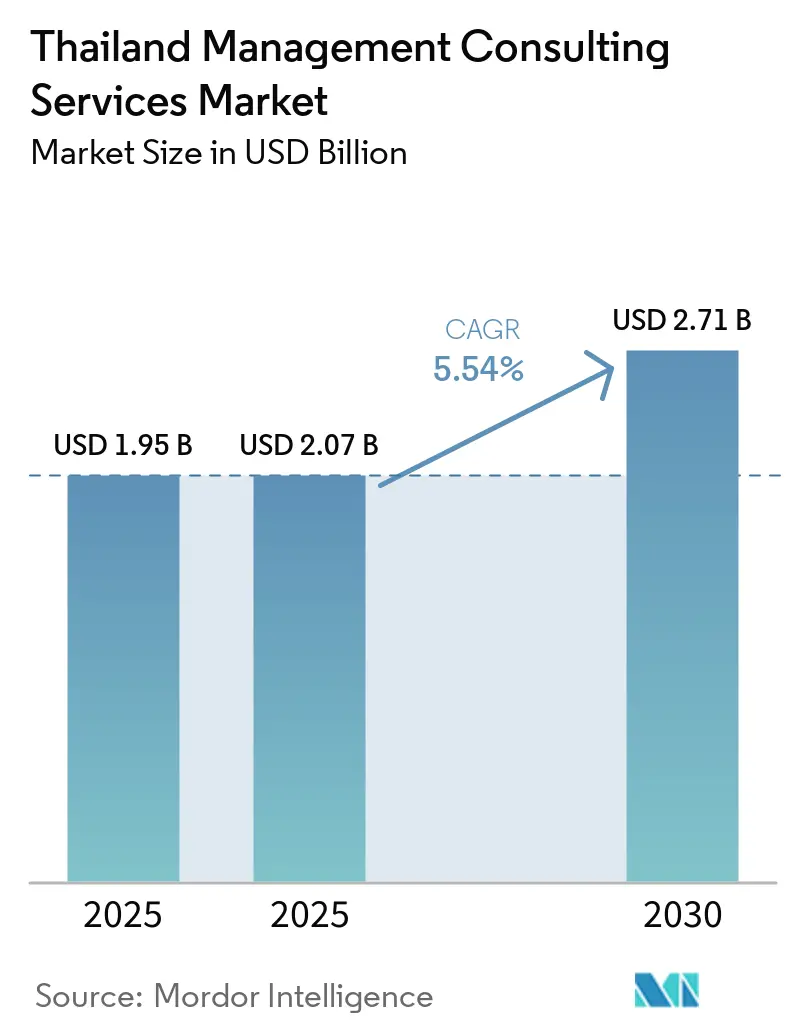

| Base Year Market Size (2025) | USD 1.95 Billion |

| Market Size (2025) | USD 2.07 Billion |

| Market Size (2030) | USD 2.71 Billion |

| Growth Rate (2026 - 2031) | 5.54% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Management Consulting Services Market Analysis by Mordor Intelligence

The Thailand management consulting services market size was valued at USD 1.95 billion in 2025 and estimated to grow from USD 2.07 billion in 2026 to reach USD 2.71 billion by 2031, at a CAGR of 5.54% during the forecast period (2026-2031). Private-sector digital transformation programs, rapid cloud and AI datacenter build-outs, and Bangkok’s emergence as an ASEAN headquarters hub continue to offset periodic freezes in public-sector spending. Multinational cloud providers have announced multi-billion-dollar capital expenditure that funnels implementation, change-management, and cybersecurity work to advisors, while the Board of Investment’s incentives accelerate inflows of regional operations that require regulatory and talent-strategy support. Consulting demand rises further as Thai conglomerates professionalize ESG reporting ahead of phased ISSB and TCFD rules, creating a pipeline of risk, compliance, and sustainability engagements. At the same time, caretaker-government rules that halt new infrastructure approvals can suppress short-term revenue visibility, yet large enterprises maintain transformation budgets that shield the Thailand management consulting services market from sharper cyclicality.

Key Report Takeaways

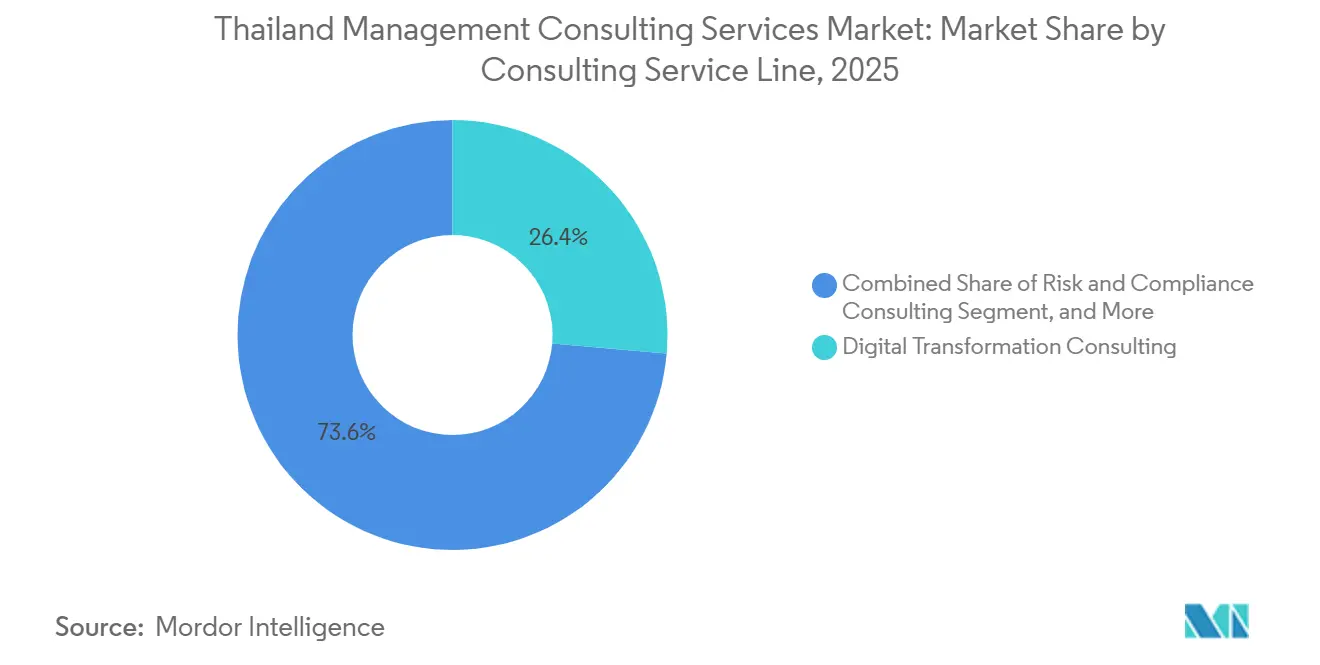

- By consulting service line, Digital Transformation Consulting led with 26.37% revenue share in 2025, whereas Risk and Compliance Consulting is projected to post the fastest 5.82% CAGR through 2031.

- By organization size, Large Enterprises accounted for 63.28% of 2025 revenue, while Small and Medium-Sized Enterprises are on track for a 5.61% CAGR over 2026-2031.

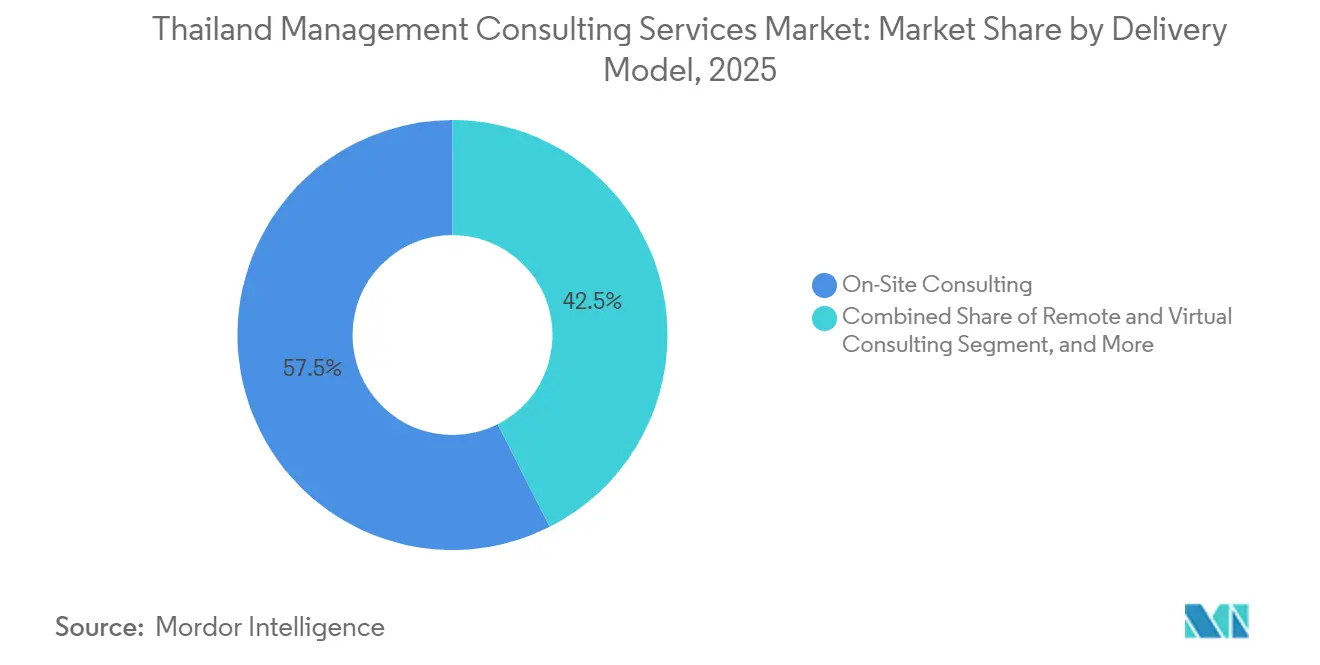

- By delivery model, On-Site Consulting commanded 57.46% share in 2025, yet Remote and Virtual Consulting is forecast to advance at the highest 5.88% CAGR to 2031.

- By end-user industry, Banking and Insurance contributed 18.32% of 2025 spending and Healthcare is expected to register a 5.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Thailand Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government "Thailand 4.0" Digital-Economy Push | +1.2% | National, Bangkok and Eastern Economic Corridor | Medium term (2-4 years) |

| Rapid Enterprise Digital Transformation and Cloud Uptake | +1.0% | National, early adoption in Bangkok and Chiang Mai | Short term (≤ 2 years) |

| Surge in ESG and Sustainability Advisory Demand | +0.8% | National, especially Bangkok-listed corporates | Medium term (2-4 years) |

| ASEAN Regional-HQ Relocations to Bangkok | +0.6% | Bangkok, with spillover to Phuket and Chiang Mai | Long term (≥ 4 years) |

| IPO-Ready Family-Owned Mid-Caps Professionalizing | +0.4% | National manufacturing hubs | Medium term (2-4 years) |

| Secondary-City Corridor and SEZ Build-Outs | +0.5% | Chonburi, Rayong, Chiang Mai, Phuket, Khon Kaen | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government "Thailand 4.0" Digital-Economy Push

Tax holidays and import-duty exemptions for AI hardware remain in force until 2026, and THB 500 billion (USD 14.7 billion) of digital-government outlays earmarked for 2026 underpin sustained demand for enterprise architecture, cybersecurity, and change-management advisory.[1]Digital Economy Promotion Agency, “depa Operational Plan 2026,” depa.or.th The National AI Action Plan targets 50 government pilots by 2027, opening work in data governance and algorithmic transparency. Microsoft’s USD 1 billion datacenter build and AWS’s USD 5 billion regional infrastructure expansion translate directly into migration and managed-services mandates. In the Eastern Economic Corridor, the THB 74.4 billion (USD 2.2 billion) EECiti smart-city project due in 2026 drives advisory needs in urban planning and IoT integration. Yet infrastructure gaps highlighted by the Asian Development Bank’s climate-resilient connectivity loan introduce scheduling risk that can defer consulting revenue.

Rapid Enterprise Digital Transformation and Cloud Uptake

Thai enterprises spent more than THB 120 billion (USD 3.5 billion) on cloud migration and digital-core projects in 2025, with banks, manufacturers, and retailers leading adoption. PwC Thailand upskilled 1,200 staff in generative AI and cloud analytics in early 2025, illustrating the race to expand delivery capacity. Industry 4.0 showcases, such as Bosch’s smart factory in Rayong, have shifted consulting focus from strategy to implementation. Core-banking replacements triggered by virtual bank licenses issued in 2026 create multi-year demand for regulatory compliance and customer-experience design. The trend reinforces the Thailand management consulting services market as enterprises seek vendor selection, change leadership, and cybersecurity frameworks.

Surge in ESG and Sustainability Advisory Demand

The Securities and Exchange Commission’s phased ISSB roadmap obliges climate-first reporting from 2027 and full TCFD assurance by 2031, spurring advisory on carbon accounting and assurance readiness. The Thailand Green Taxonomy guides sector-specific thresholds for green financing, intensifying demand for classification and impact-measurement consulting.[2]Bank of Thailand, “Thailand Taxonomy,” bot.or.th Thai conglomerates such as SCG have introduced internal carbon prices and circular-economy targets, widening opportunities in renewable procurement, waste-to-energy feasibility, and biodiversity impact assessments. M&A due-diligence now embeds ESG risk analysis, adding incremental scopes to financial advisory mandates. Collectively, these shifts boost the Thailand management consulting services market by expanding compliance advisory spend beyond financial reporting.

ASEAN Regional-HQ Relocations to Bangkok

Incentives under the International Business Center scheme, including eight-year corporate-tax exemptions and facilitated visas, attracted 47 regional headquarters in 2025. ONE Championship’s 2024 relocation to Bangkok underscores momentum in creative and media enterprises.[3]Board of Investment Thailand, “Demographic,” boi.go.th, ONE Championship, “ONE Championship Moves Regional HQ to Bangkok,” onefc.com Cloud-platform build-outs further entice tech multinationals to base ASEAN operations locally, driving advisory around data residency, partner-ecosystem strategy, and talent acquisition. Yet uncertainty around the THB 65 billion (USD 1.9 billion) Direct Power Purchase Agreement program, now on hold, demonstrates how policy pauses can delay planned relocations and dampen near-term consulting scopes. Long-run headquarters clustering nonetheless cements Bangkok’s role as a launchpad for advisors covering wider Southeast Asian markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Political Uncertainty and Stop-Start Public Budgets | -0.7% | National, acute in public procurement | Short term (≤ 2 years) |

| Shortage of Bilingual Digital-Savvy Consultants | -0.6% | Bangkok and Chiang Mai | Medium term (2-4 years) |

| Foreign-Ownership Caps on Professional Services | -0.3% | National | Long term (≥ 4 years) |

| Price-Sensitive SME Segment | -0.4% | Secondary cities and rural provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Political Uncertainty and Stop-Start Public Budgets

Parliament’s December 2025 dissolution froze more than THB 1.4 trillion (USD 41 billion) of infrastructure approvals, including the Don Mueang-Suvarnabhumi-U-Tapao high-speed rail, abruptly postponing engagements in procurement, PPP structuring, and stakeholder management. Ratings downgrades tied to contested tax-reform timelines have further clouded multi-year consulting visibility. Cabinet sign-off delays on water-resource megaprojects underscore how caretaker constraints paralyze new scopes.[4]Thailand Construction and Engineering News, “Thailand’s Trillion Infrastructure Pipeline Frozen,” thailand-construction.com Budget enactment slippages similar to 2023 could again compress fiscal-2027 disbursements, weakening public-sector advisory pipelines. Such volatility can momentarily temper the Thailand management consulting services market trajectory despite solid private-sector demand.

Shortage of Bilingual Digital-Savvy Consultants

Roland Berger estimates that only 18% of Thai professionals possess advanced digital skills, pushing wage inflation for senior cloud-architect consultants to 25% year-on-year.[5]he Nation, “Fitch Flags Political Hurdles to Thailand’s Deficit-Cut Plan,” nationthailand.com PwC Thailand’s THB 9 million (USD 265,000) upskilling effort typifies the costly reskilling race. Local systems integrator G-Able has formed university partnerships to widen the talent funnel, yet the Foreign Business Act’s four-Thai-to-one-expatriate ratio strains foreign firms’ staffing models. Chiang Mai recruiting platform KiTalent reports that senior bilingual AI specialists command a 30-40% premium over 2024 rates Talent scarcity therefore adds cost pressure across the Thailand management consulting services market and caps near-term delivery capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Digital Transformation Leads, Risk and Compliance Accelerates

Digital Transformation Consulting accounted for 26.37% of the Thailand management consulting services market share in 2025, reflecting the scale of cloud migrations, omnichannel commerce rollouts, and AI pilot programs among large Thai conglomerates. The National AI Action Plan and hyperscale datacenter investments continue to fuel engagements in architecture design, cybersecurity, and change management. Over the forecast horizon, Risk and Compliance Consulting is poised for a 5.82% CAGR as ISSB and TCFD mandates tighten disclosure obligations. Consulting spend expands into carbon accounting, biodiversity impact assessments, and climate scenario planning. Strategy Consulting remains the domain of global firms guiding M&A and portfolio optimization, while Operations Consulting captures Industry 4.0 work such as lean manufacturing and predictive maintenance. HR Consulting supports large-scale reskilling programs, and Financial Advisory Consulting assists IPO-ready family businesses with valuation and governance upgrades. Collectively, these service lines reinforce recurring demand, anchoring the Thailand management consulting services market at both enterprise and mid-market levels.

The Thailand management consulting services market size tied to Digital Transformation engagements is projected to expand steadily as public-cloud spending scales through 2028. Niche practices in supply-chain resilience and customer experience design gain traction when manufacturers deploy smart-factory solutions and retailers integrate online and offline channels. Automotive electrification in the Eastern Economic Corridor pulls battery-chain advisory into focus, amplified by Roland Berger’s acquisition of Alexec Consulting. As specialized workloads rise, advisors with deep technical know-how and regulatory fluency outperform generic strategy peers.

By Organization Size: Large Enterprises Dominate while SMEs Drive Momentum

Large Enterprises commanded 63.28% of Thailand management consulting services market revenue in 2025, leveraging sizable budgets to fund end-to-end digital programs, ESG frameworks, and overseas expansion. Framework agreements with global consultancies secure preferential access to top talent and proprietary accelerators. Conversely, Small and Medium-Sized Enterprises exhibit the fastest 5.61% CAGR, underpinned by government subsidies for ERP adoption and IPO-driven governance upgrades. Grant Thornton’s Q1 2025 survey showed that 62% of mid-market executives intended to raise technology investment despite macro-risk.

Credit tightness and high household debt tempered optimism in late 2025, but Bank of Thailand rate cuts to 1.25% and a potential 1.00% floor in early 2026 aim to revive access to growth capital. SMEs often favor local firms such as G-Able that provide Thai-language delivery and cost structures 30-40% below global peers. Scaling advisory to this segment remains sensitive to price; hybrid remote models and modular project scopes therefore gain popularity, broadening the Thailand management consulting services industry footprint without eroding profitability.

By Delivery Model: On-Site Retains Primacy as Remote Gains Pace

On-Site delivery held 57.46% of revenue in 2025, reflecting client trust in face-to-face workshops for complex transformations and regulatory projects. Yet Remote and Virtual Consulting advances at a 5.88% CAGR as hybrid work formalizes. Cloud-based collaboration suites enable distributed teams to support implementation and analytics remotely, shrinking travel costs for both advisor and client. The Destination Thailand Visa and Long-Term Resident visa broaden the legal pathway for foreign digital nomads, expanding the pool of specialized talent available for virtual projects.

Advisory tied to ESG assurance and public-sector security requirements still mandates onsite verification, slowing virtual uptake in those niches. Nonetheless, offshore delivery hubs rise, exemplified by ABeam Consulting’s India capability center that supports Thai clients in SAP and AI rollouts. The Thailand management consulting services market size allocated to hybrid models is expected to compound steadily as clients balance cost, speed, and compliance obligations.

By End-User Industry: Banking Leads while Healthcare Surges

Banking and Insurance represented 18.32% of 2025 spending, sustained by virtual-bank licensing rounds and incumbent core-bank modernizations. Use cases span API-first architectures, digital-channel redesign, and Basel-aligned risk modeling. Healthcare is projected to deliver the highest 5.73% CAGR through 2031 as the Mor Prom digital-health platform scales to underserved provinces. Industrial manufacturing follows close behind, with automotive suppliers deploying AI-driven predictive maintenance and smart-factory analytics.

Energy and resources clients seek carbon accounting and circular-economy advisory to meet internal carbon-price thresholds, while retail conglomerates integrate online and physical channels through data-platform rollouts. Public-sector demand remains uneven, tied to budget enactment delays, but when released, it can trigger large scopes in e-government, infrastructure PPP structuring, and stimulus-program design. The diversified end-user base therefore underpins resilience in the Thailand management consulting services market, enabling advisors to reallocate capacity as sector cycles rotate.

Geography Analysis

Bangkok continues to generate the largest share of Thailand management consulting services market revenue, underpinned by its concentration of corporate headquarters, financial institutions, and government ministries. Digital Government Complex modernization and multi-tenant hyperscale datacenters concentrate advisory work in Nonthaburi and neighboring districts. The Eastern Economic Corridor (EEC) encompassing Chonburi, Rayong, and Chachoengsao is the fastest-growing region by consulting spend, catalyzed by THB 74.4 billion (USD 2.2 billion) smart-city projects and EV supply-chain investments. Firms provide urban planning, PPP structuring, and sustainability advisory as EECiti infrastructure comes online by 2026.

Secondary corridors such as Chiang Mai, Phuket, and Khon Kaen rise as remote-work and tech-startup magnets, attracting ecosystem-building and talent-strategy engagements. The Destination Thailand Visa fuels a growing consultant population that delivers services from co-working hubs, bolstering local ecosystems. Northern provinces also tap consultants for agritech and tourism digitalization projects aimed at diversifying income beyond traditional agriculture.

Cross-border mandates emanate from Bangkok-based ASEAN headquarters that supervise expansion into Vietnam, Cambodia, and Lao PDR. Advisors craft regulatory roadmaps and supply-chain strategies that knit Thai production bases to Indochina consumer growth. The geographic diversification of engagements ensures that the Thailand management consulting services market can navigate localized political or budgetary shocks while sustaining national-scale momentum.

Competitive Landscape

Global firms, Accenture, Deloitte, PwC, EY, KPMG, McKinsey, BCG, and Bain, collectively capture an estimated 55-60% of Thailand management consulting services market revenue, anchored by long-standing relationships with conglomerates and public agencies. Roland Berger’s March 2026 purchase of battery specialist Alexec Consulting highlights the premium on deep technical skills to serve EV and battery-cell factory investments. Japanese-heritage ABeam Consulting doubled down on SAP and AI implementation by appointing a Thailand Managing Director in April 2026 and securing multiple 2026 SAP Partner Awards.

Local systems integrators such as G-Able leverage Thai-language delivery and 30-40% lower fee structures to win mid-market digital transformation and cybersecurity projects. Recognition through IBM’s 2025 AI Innovation Award in February 2026 and Veeam accolades in March 2026 reinforces their credentials. Partnerships with AWS and Veeam allow bundling of migration, backup, and security services, posing credible competition to the multinational tier.

Regulatory barriers under the Foreign Business Act still require foreign consultancies to secure licenses and maintain Thai-to-expatriate employment ratios, limiting greenfield entrants. Proposed amendments that could relax restrictions for future industries may intensify rivalry if enacted. Corporate venture arms such as SCG’s AddVentures embed innovation-studio services directly into industrial clients, blurring lines between consulting, incubator, and integrator models. Overall, moderate fragmentation persists as niche specialists coexist with global multipractice leaders, preserving pricing discipline yet promoting innovation in delivery models.

Thailand Management Consulting Services Industry Leaders

Accenture plc

Deloitte Touche Tohmatsu Limited

PricewaterhouseCoopers International Limited

Ernst & Young Global Limited

KPMG International Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ABeam Consulting appointed Supreeda Jirawongsri as Thailand Managing Director, tasking her with scaling SAP, AI, and digital transformation services for local conglomerates and Japanese subsidiaries.

- March 2026: Roland Berger acquired Alexec Consulting to deepen battery and EV value-chain expertise for automotive electrification projects in the Eastern Economic Corridor.

- March 2026: G-Able hosted the Cloud Trust Alliance event that drew over 300 executives and showcased cloud governance and AI trust frameworks.

- February 2026: ABeam Consulting expanded its India capability center to support offshore delivery for Thai and ASEAN clients, enhancing cost-effective remote advisory.

Thailand Management Consulting Services Market Report Scope

The Thailand Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current size of the Thailand management consulting services market?

The Thailand management consulting services market size stood at USD 1.95 billion in 2025 and is projected to reach USD 2.71 billion by 2031.

Which service line contributes the most revenue?

Digital Transformation Consulting led with 26.37% market share in 2025 due to cloud migration and AI adoption.

Which end-user sector is expanding the fastest?

Healthcare consulting is expected to grow at a 5.73% CAGR through 2031, supported by telemedicine scale-up and digital-health platforms.

How is remote consulting adoption evolving?

Remote and Virtual Consulting is forecast to rise at a 5.88% CAGR as hybrid work, collaboration tools, and visa programs enable distributed delivery.

What key factor restrains short-term public-sector engagements?

Political transitions that freeze new infrastructure approvals can delay THB-scale projects and compress near-term advisory revenue.

Why is sustainability consulting in high demand?

Mandatory ISSB and TCFD disclosure timelines beginning 2027 require listed firms to upgrade carbon accounting, scenario analysis, and assurance processes.

Page last updated on: