South Korea IT Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

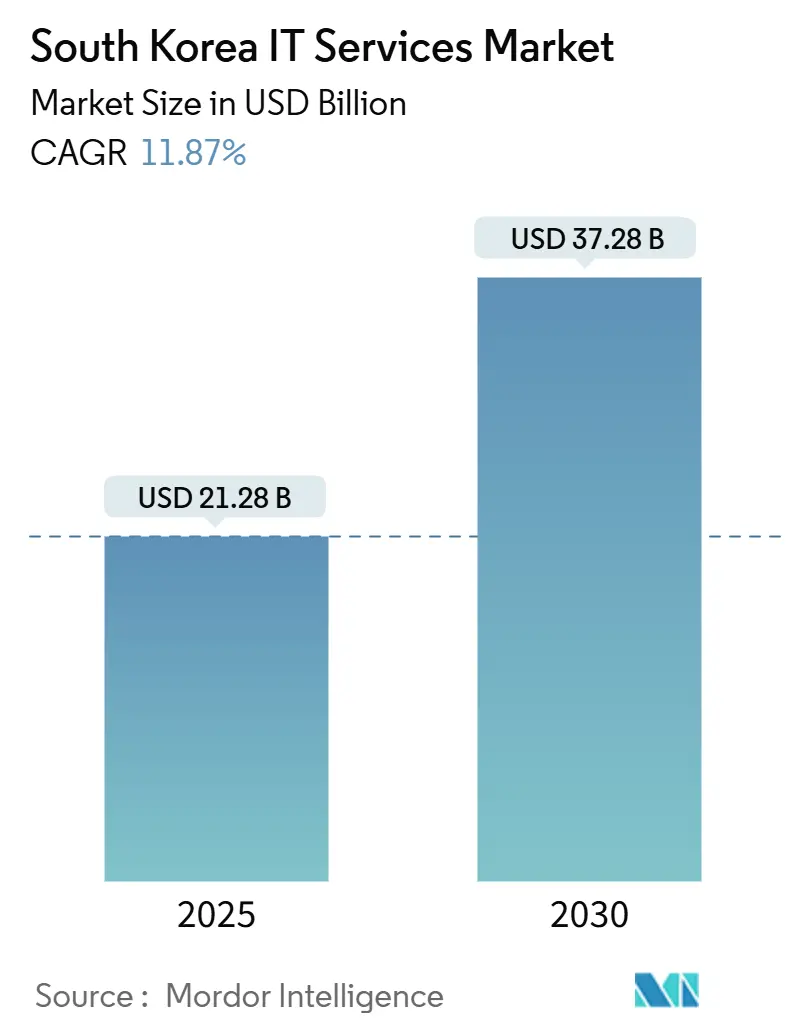

| Market Size (2025) | USD 21.28 Billion |

| Market Size (2030) | USD 37.28 Billion |

| Growth Rate (2025 - 2030) | 11.87% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea IT Services Market Analysis by Mordor Intelligence

South Korea IT services market size stands at USD 29.92 billion in 2025 and is projected to grow at a 12.38% CAGR to USD 53.63 billion by 2030. Robust government digital-platform strategy, sustained 5G-AI investment, and hyperscaler entry underpin this strong trajectory. Policy-driven cloud migration validates security standards and accelerates private-sector adoption. Rapid expansion of edge and private-5G use cases stimulates demand for low-latency platforms, while data-sovereignty rules elevate managed security revenues. Rising offshore delivery offsets local talent shortages and supports cost competitiveness across the South Korea IT services market. Competitive intensity increases as AWS, Microsoft, and Google obtain domestic certifications and target regulated workloads, prompting chaebol subsidiaries to deepen AI and industry-vertical expertise.[1]Ministry of the Interior and Safety, “Guidelines on Cloud Computing Service Use and Security,” mois.go.kr

Key Report Takeaways

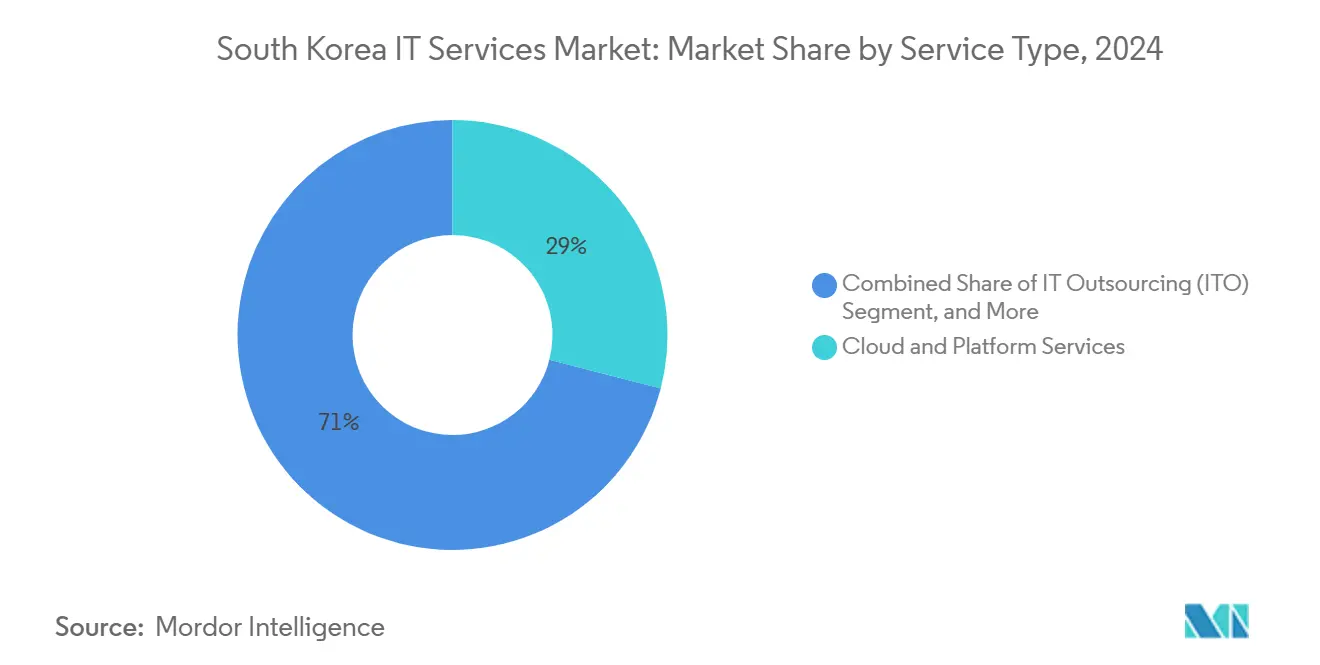

- By service type, cloud and platform services led with 29% revenue share in 2024; managed security services are advancing at a 16.9% CAGR through 2030.

- By enterprise size, large enterprises held 61% of the South Korea IT services market share in 2024, while SMEs are forecast to expand at a 15.2% CAGR to 2030.

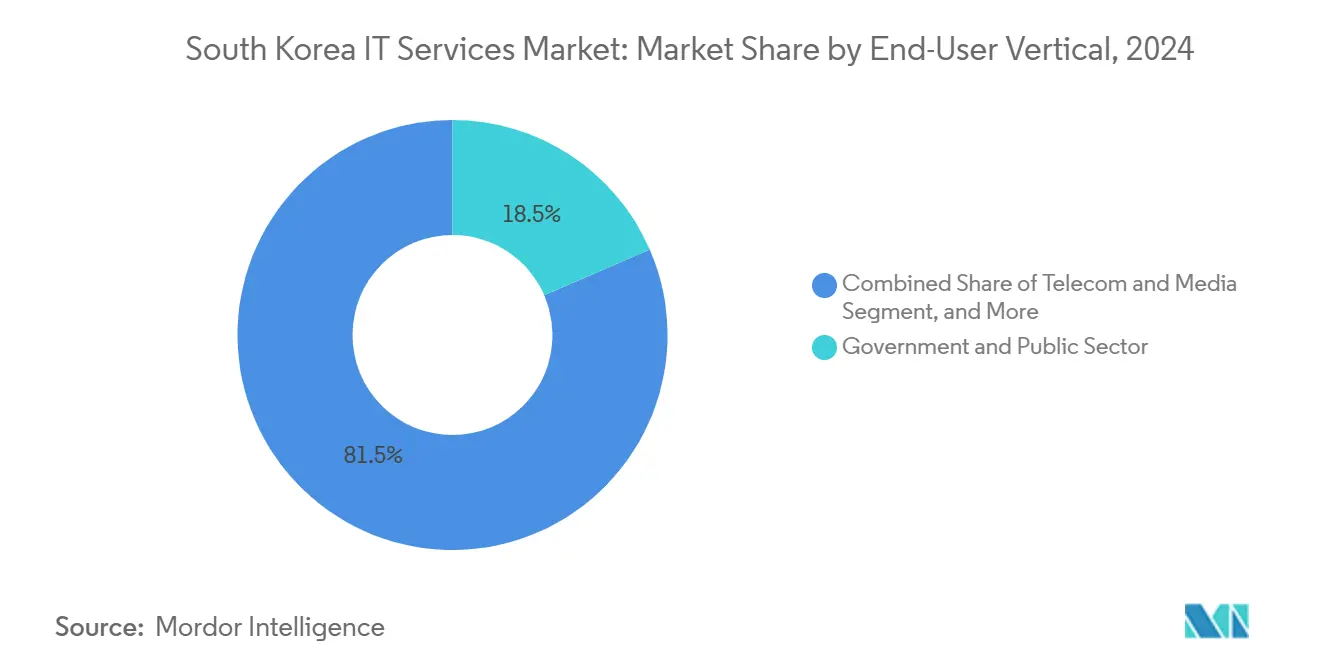

- By end-user vertical, government and public sector captured 18.5% share of the South Korea IT services market size in 2024; healthcare and life sciences are projected to grow at 15.74% CAGR through 2030.

- By deployment model, onshore delivery accounted for 54% share of the South Korea IT services market size in 2024, whereas offshore delivery is projected to rise at a 15.94% CAGR between 2025-2030.

South Korea IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Public-sector "Digital Platform Government" cloud-first policy | +3.20% | National, concentrated in Seoul metropolitan area | Medium term (2-4 years) |

| 5G/AI convergence projects from MSIT RandD budget surge | +2.80% | National, with early deployment in Busan, Incheon smart cities | Long term (≥ 4 years) |

| SME digital-innovation subsidies and tax credits | +2.10% | National, strongest uptake in Gyeonggi, Daegu manufacturing hubs | Short term (≤ 2 years) |

| Generative-AI localisation race among hyperscalers and chaebol | +1.90% | Seoul-Incheon corridor, expanding to Sejong administrative city | Medium term (2-4 years) |

| Semiconductor supply-chain re-shoring demanding local IT expertise | +1.60% | Gyeonggi Province, Chungcheongnam-do industrial zones | Long term (≥ 4 years) |

| Data-sovereignty compliance boosting managed security services | +1.40% | National, with regulatory oversight from Seoul | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Public-sector Digital-Platform Cloud-First Policy

Mandated migration of 10,000 public information systems to cloud-native architecture by 2030 secures multiyear demand for system integration and managed services.[2]Digital Platform Government Committee, “Public-Sector Large-Scale AI Introduction Guide,” dpg.go.kr KRW 430 billion earmarked for 2025 alone accelerates procurement cycles. Samsung SDS won high-visibility contracts for the National Assembly big-data platform and local-administration common system, boosting its 2024 cloud revenue to KRW 2.32 trillion. Public-sector security frameworks quickly become de facto standards for private firms, compressing evaluation timelines and stimulating broader adoption across the South Korea IT services market. FedRAMP-style certification paths enable faster vendor onboarding, while visibility of cloud migration KPIs influences provincial IT spending plans.

5G-AI Convergence from MSIT R&D Surge

MSIT’s KRW 625.3 billion K-Network 2030 program funds next-generation 6G research and immediate 5G-AI pilots.[3]Ministry of Science and ICT, “K-Network 2030 Strategy,” msit.go.kr KT’s alliance with Microsoft integrates private-5G slices and Azure AI for smart-factory control, showcasing low-latency orchestration. Nokia and Megazone Cloud demonstrate AWS-based industrial-edge solutions that reduce cycle time for machine-vision analytics to sub-25 milliseconds. Naver Cloud adds data-center capacity to address growing inference workloads, while chip-level optimizations lower power consumption by 18%. These converged projects cultivate specialized demand for edge consulting, site-survey services, and carrier-grade security across the South Korea IT services market.

SME Digital-Innovation Subsidies

The Ministry of SMEs and Startups earmarks KRW 15.2 trillion to underwrite cloud and AI adoption, including grants of up to KRW 50 million per firm. Subsidy guidelines prioritize manufacturing, logistics, and healthcare SMEs, easing upfront migration costs. LG Electronics positions its smart-factory solutions portfolio to capture KRW 1 trillion in revenue by 2030. Naver Cloud reports that 68% of CSAP-certified SMEs operate on its platform, reflecting infrastructure cost support averaging KRW 5 million per deployment. Accelerated procurement cycles among SMEs add breadth to the South Korea IT services market and mitigate historical over-reliance on enterprise contracts.

Generative-AI Localisation Race

Naver’s HyperCLOVA X attains break-even status and secures Bank of Korea’s finance-specialized AI platform contract. In response, AWS allocates KRW 7.9 trillion for data-center expansion, while Microsoft and Google introduce Korean-language foundation models. Domestic telcos form sovereign-cloud alliances to address compliance concerns. These moves expand infrastructure footprints, reduce model latency, and diversify AI vendor options. Localized generative-AI cores facilitate use cases ranging from underwriting to clinical decision support, strengthening domestic IP and anchoring new revenue pools inside the South Korea IT services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute shortage of senior cloud and cyber-talent | -2.30% | National, most severe in Seoul tech corridor | Long term (≥ 4 years) |

| Margin squeeze from hyperscaler price wars | -1.80% | National, affecting all service providers | Medium term (2-4 years) |

| Regulatory ambiguity in forthcoming AI Framework Act | -1.20% | National, with regulatory oversight from Seoul | Short term (≤ 2 years) |

| Liability-risk concerns in outcome-based managed-service contracts | -0.90% | National, concentrated in large enterprise segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Acute Shortage of Senior Cloud and Cyber Talent

Korea Development Institute projects a deficit of more than 50,000 advanced IT professionals within five years, with only 618 PhD engineers specialized in AI fields. FPT Software’s Korean unit boosted domestic revenue by 65% between 2022-2023 by supplying nearshore talent priced 70% below local averages. Naver raises developer compensation packages, while Mobile C&C launches Cambodian delivery hubs to secure cost-effective staff. Prolonged scarcity inflates wage bills and dilutes project margins across the South Korea IT services market.

Margin Squeeze from Hyperscaler Price Wars

CSAP certification enables AWS, Microsoft, and Google to bid for public workloads, forcing domestic providers to discount infrastructure services up to 40%. Kakao and SK Telecom respond with aggressive promotions, eroding profitability for commodity hosting. Independent MSPs pivot to value-added DevOps and FinOps advisory yet rising cloud credits and rebate structures keep gross margins thin. Sustained price pressure risks deferring capital investment and moderating near-term revenue growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Cloud Platforms Drive Digital Transformation

Cloud and platform services generated 29% of 2024 revenue, underscoring the structural pivot toward scalable infrastructure within the South Korea IT services market size. Managed security services, although smaller, recorded 16.9% CAGR and benefit from wave-on-wave demand tied to zero-trust frameworks. Samsung SDS reported cloud sales of KRW 2.32 trillion, up 23.5%, while LG CNS booked KRW 3.35 trillion from cloud and AI solutions, equal to 56% of revenue. Regulatory CSAP renewals lengthen engagement cycles, anchoring multiyear service contracts. Mid-tier providers secure niche opportunities through Kubernetes migration, data-mesh design, and observability tooling, enriching the service-mix across the South Korea IT services market.

Growth in managed security aligns with evolving threat landscapes and data-localization statutes. MSSPs integrate AI-driven threat hunting and OT-security modules, capturing cross-sell opportunities in manufacturing and energy. Compliance consulting expands as KISA updates multi-cloud inspection criteria. Collectively, service-type dynamics accelerate cloud-first modernization and reinforce digital-platform adoption nationwide.

By Enterprise Size: SME Digitalization Accelerates

Large enterprises contributed 61% of 2024 spending, yet SMEs deliver a superior 15.2% CAGR through 2030, widening addressable scope for the South Korea IT services market. Government grants offset migration costs and shorten ROI periods, unlocking latent demand among factories and wholesalers. Naver Cloud’s SME portfolio now hosts 68% of CSAP-certified customers, reflecting subsidy-driven uptake.

Large enterprises pursue complex integrations, typified by HD Hyundai’s maritime digital twin built on HyperCLOVA X, which ingests over 200 million data points. SMEs gravitate toward SaaS and managed cloud bundles, with Samsung Smart-Factory Academy reporting 25% throughput gains for participants. Rising SME adoption diffuses regional demand and diversifies revenue streams across the South Korea IT services industry.

By End-User Vertical: Healthcare Innovation Leads Growth

Government and public sector held 18.5% of 2024 revenue, benefiting from the Digital-Platform rollout, whereas healthcare and life sciences is forecast to grow at 15.74% CAGR, the fastest vertical in the South Korea IT services market. Samsung Medical Center achieved HIMSS Stage 7 and deployed RPA that cut document issuance time to five minutes with zero errors. The Dr. Answer 2.0 consortium mobilizes 30 hospitals and 19 ICT firms to build AI medical devices under MSIT grants.

Manufacturing remains pivotal through smart-factory reforms, with LG Electronics targeting KRW 1 trillion in solutions revenue and POSCO DX embedding AI into steel production. BFSI vertical introduces private LLMs, as K-Bank rolls out KT and Upstage models for risk analysis. Vertical diversification enhances resilience and keeps the South Korea IT services market aligned with national industrial priorities.

By Deployment Model: Offshore Growth Amid Talent Constraints

Onshore delivery retained 54% share in 2024 due to data-sovereignty and compliance prerequisites, but offshore delivery is set to expand at a 15.94% CAGR to 2030. FPT Software’s Korean sales climbed to KRW 32.9 billion in 2023, illustrating cost-arbitrage momentum. Vietnamese and Cambodian centers deliver competitive code quality, complemented by Korean-fluent project managers to ensure cultural alignment. Nearshore alliances, such as Naver Cloud’s collaboration with Singapore-based StarHub, support regional multicloud rollouts.

Hybrid models combine local oversight with overseas execution, satisfying KISA security checks while alleviating staffing shortages. Providers invest in secure VPN gateways, encrypted code repositories, and joint-training programs, reinforcing quality assurance and sustaining offshore scalability within the South Korea IT services industry.

Geography Analysis

Seoul-Incheon corridor concentrates 54% of domestic demand, powered by hyperscale data centers, ministries, and headquarters of conglomerates. Continuous metro-edge upgrades slash latency for AI workloads, catalyzing further spending across the South Korea IT services market. Gyeonggi Province anchors manufacturing digitalization, hosting LG smart-factory rollouts and POSCO DX AI installations that optimize steel throughput. Busan and Incheon act as live 5G-AI testbeds funded under K-Network 2030, enabling smart-port and logistics pilots.

Sejong administrative city hosts core Digital-Platform Government operations, creating a budding public-cloud cluster. Chungcheongnam-do semiconductor parks adopt advanced process-control systems, stimulating niche MES and industrial-IoT services. Daegu’s machinery hubs and Ulsan’s automotive plants implement software-defined robotics, leveraging grants to bridge skills gaps. Internationally, Naver Cloud extends southeast via Intel and StarHub partnerships, exporting Korean compliance templates to neighbouring markets. Geography-specific demand underscores balanced regional growth within the South Korea IT services market.

Competitive Landscape

South Korea IT services market exhibits moderate concentration as global hyperscalers challenge domestic incumbents. Samsung SDS leads managed cloud and ranks second in public cloud, reporting 2024 revenue of KRW 13.83 trillion with cloud contributing KRW 2.32 trillion, up 23.5%. LG CNS posted KRW 5.98 trillion and raised USD 827 million in its 2025 IPO to fund AI expansion. Naver Cloud, profitable on HyperCLOVA X, secured Bank of Korea’s generative-AI contract, enhancing sovereign-cloud credibility.[4]Bank of Korea, “Generative AI Platform Contract,” bok.or.kr

SK Shieldus dominates MSS with tier-3 SOC coverage, while KT integrates Microsoft Azure stacks to exploit private-5G demand. CJ OliveNetworks attained AWS DevOps competency and partners with Naver Cloud to double MSP revenue. Foreign players obtain CSAP certifications-Microsoft first, followed by Google and AWS-eroding historical barriers and triggering price compression. Competitive dynamics now revolve around vertical AI accelerators, compliance tooling, and sovereign-data options, sharpening service differentiation within the South Korea IT services market.

South Korea IT Services Industry Leaders

Samsung SDS Co., Ltd.

LG CNS Co., Ltd.

SK Inc. C&C

KT Corporation (KT Cloud & Security)

Naver Cloud Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: LG CNS completed successful IPO on KOSPI, raising USD 827 million at USD 4.1 billion valuation, enabling global AI and cloud expansion.

- January 2025: Samsung SDS announced KRW 13.83 trillion 2024 revenue, with cloud services rising 23.5% to KRW 2.32 trillion.

- December 2024: Korean National Assembly passed AI Framework Act, effective Jan 2026, establishing governance mandates for enterprise AI adoption.

- September 2024: KT and Microsoft unveiled multibillion-dollar AI partnership integrating 5G networks and Azure services.

South Korea IT Services Market Report Scope

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-User Verticals |

| Onshore Delivery |

| Nearshore Delivery |

| Offshore Delivery |

| By Service Type | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By End-User Vertical | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| Healthcare and Life-Sciences | |

| Retail and Consumer Goods | |

| Telecom and Media | |

| Logistics and Transport | |

| Energy and Utilities | |

| Other End-User Verticals | |

| By Deployment Model | Onshore Delivery |

| Nearshore Delivery | |

| Offshore Delivery |

Key Questions Answered in the Report

What is the forecast value of the South Korea IT services market in 2030?

The market is projected to reach USD 53.63 billion by 2030, growing at a 12.38% CAGR.

Which service category leads spending in South Korean IT services?

Cloud and platform services lead, accounting for 29% of 2024 revenue.

Why are managed security services growing faster than other segments?

Data-sovereignty rules and zero-trust mandates are driving a 16.9% CAGR for managed security services.

How do government policies influence market demand?

The Digital-Platform Government cloud-first mandate allocates KRW 430 billion for 2025 migrations, directly fueling integration and managed-service contracts.

What is the main challenge limiting market growth?

A shortage of senior cloud and cyber professionals, projected at 50,000 by 2030, constrains delivery capacity and raises labor costs.

Which vertical shows the highest growth potential?

Healthcare and life sciences is poised to expand at a 15.74% CAGR as smart-hospital and AI diagnostic projects scale nationally.

Page last updated on: