Singapore IT Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

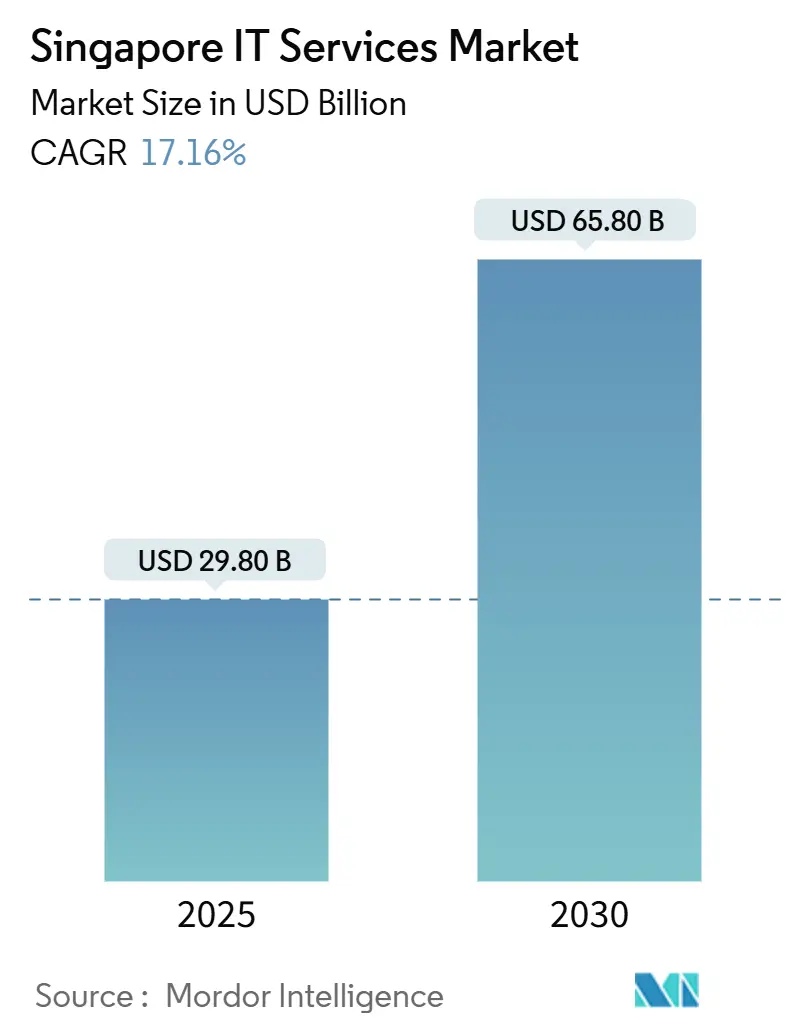

| Market Size (2025) | USD 29.80 Billion |

| Market Size (2030) | USD 65.80 Billion |

| Growth Rate (2025 - 2030) | 17.16% CAGR |

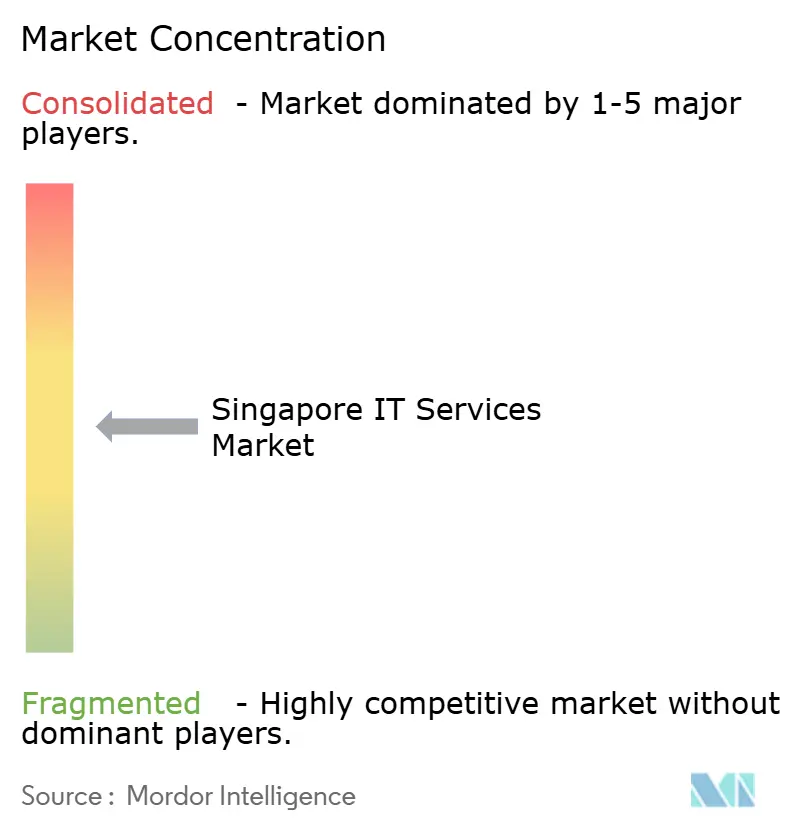

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore IT Services Market Analysis by Mordor Intelligence

The Singapore IT services market size stood at USD 29.80 billion in 2025 and is forecast to climb to USD 65.80 billion by 2030, translating into a 17.16% CAGR. A cloud-first public-sector mandate that has already migrated more than 80% of eligible systems, annual government ICT spending above USD 3 billion, and Smart Nation 2.0 investments continue to anchor this growth trajectory. Multinational corporations using Singapore as their Asia-Pacific headquarters demand sophisticated cross-border integration services, while 5G network-slicing opens new outsourcing use cases in manufacturing, healthcare, and logistics. At the same time, a widening cyber-skills gap pushes enterprises toward managed security, and rising nearshore capacity in Malaysia and the Philippines reshapes cost–quality considerations without eroding Singapore’s premium value proposition.

Key Report Takeaways

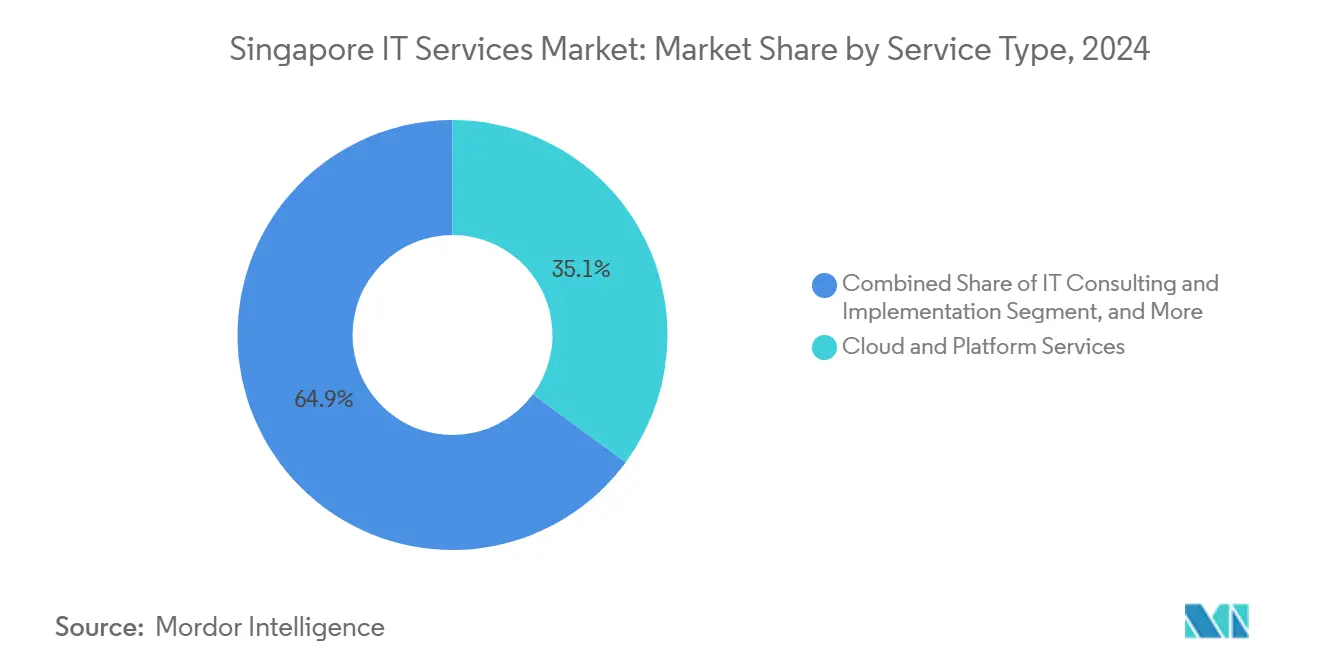

- By service type, Cloud and Platform Services led with 35.1% of the Singapore IT services market share in 2024; Managed Security Services is projected to expand at a 20.3% CAGR through 2030.

- By enterprise size, Large Enterprises held 62.3% of the Singapore IT services market size in 2024, while Small and Medium Enterprises are advancing at an 18.8% CAGR over 2025-2030.

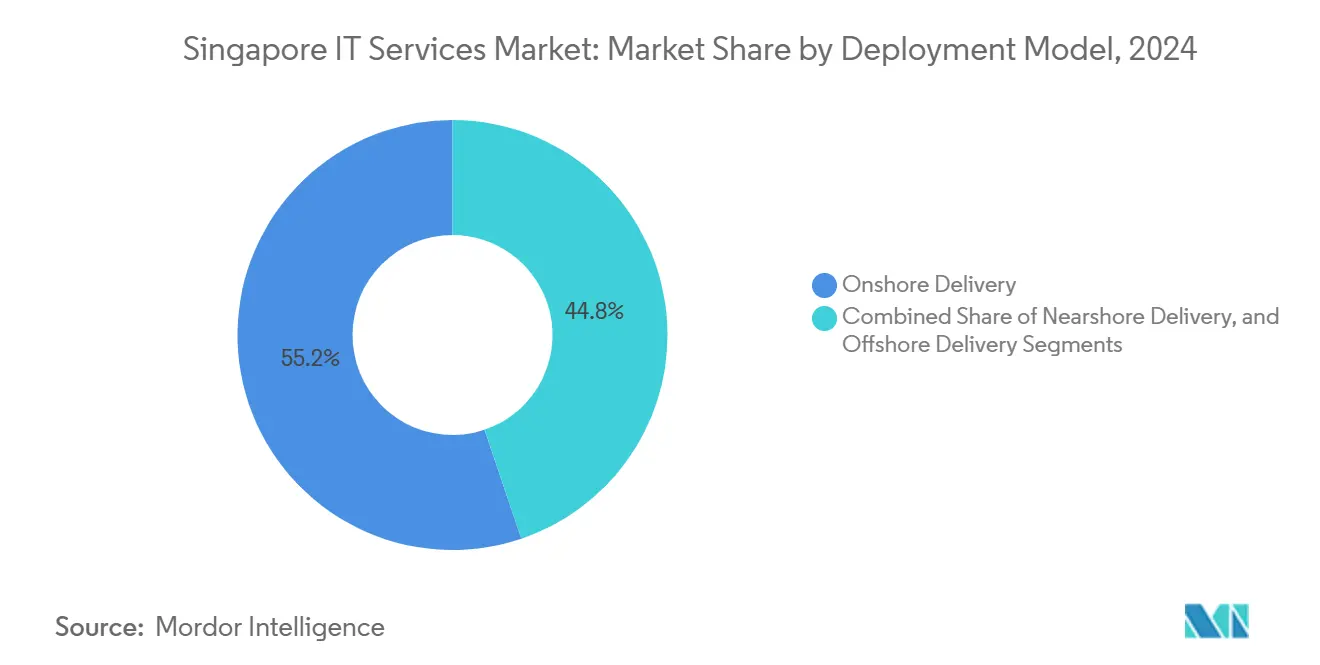

- By deployment model, Onshore Delivery accounted for 55.2% of the Singapore IT services market share in 2024, and Near/Offshore Delivery is rising at a 19.5% CAGR to 2030.

- By vertical, BFSI captured 30.7% of the Singapore IT services market size in 2024; Healthcare and Life-Sciences are expanding at a 19.2% CAGR through 2030.

Singapore IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart Nation 2030 ICT investment acceleration | +4.2% | National, with concentrated benefits in urban centers | Medium term (2-4 years) |

| Government cloud-first procurement mandate | +3.8% | National government agencies, spillover to GLCs | Short term (≤ 2 years) |

| SME GenAI adoption incentives via IMDA Sandbox | +2.9% | National SME ecosystem, early gains in fintech and healthcare | Medium term (2-4 years) |

| Cyber-skills shortage boosting MSS demand | +3.5% | Global enterprises with Singapore operations | Short term (≤ 2 years) |

| Singapore as Asia-Pacific HQ and near-/offshore hub | +4.1% | Regional MNC operations, ASEAN connectivity | Long term (≥ 4 years) |

| 5G network-slicing enabled outsourcing use-cases | +2.7% | Enterprise clients, public sector early adopters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Smart Nation 2030 ICT Investment Acceleration

Annual public spending above USD 3.3 billion, 45% of it earmarked for co-developed projects, underpins an ecosystem where bulk-buy contracting and “Tender Lite” categories accelerate procurement cycles.[1]Government Technology Agency, “FY24: Government To Spend More Than $3B To Modernise ICT Infrastructure And Develop Digital Services,” tech.gov.sg Over USD 2.1 billion is routed toward cybersecurity and public-trust initiatives, creating a strong pull for integrators that can certify to government benchmark standards. As these frameworks spill over to government-linked companies, vendors able to map solutions to Smart Nation reference architectures gain priority access to a multi-year pipeline of transformation projects. The resulting halo effect prompts private-sector adoption, magnifying total addressable demand for cloud migrations, data-governance tooling, and AI-enabled citizen services.

Government Cloud-First Procurement Mandate

Surpassing its initial 70% target, the state migrated more than 80% of eligible workloads to commercial cloud by 2024, under standardized GCC and GCC+ pathways. GovTech’s central enablement team provides shared training, templates, and security baselines, compressing lead times for new deployments. Relaxed rules now allow unclassified workloads on public clouds, unlocking fresh demand from agencies once constrained by data-residency interpretations. Vendors proficient in FedRAMP-equivalent controls are well-positioned to capture ongoing modernization budgets across ministries, statutory boards, and quasi-government entities.

SME GenAI Adoption Incentives via IMDA Sandbox

Through the GenAI Sandbox program, more than 150 SMEs have tested generative-AI prototypes; 82% retained active deployments post-pilot.[2]Infocomm Media Development Authority, “IMDA Scales Efforts To Level Up Singapore's Tech Talent,” imda.gov.sg Subsidies that cover up to 70% of project costs lower entry barriers, while a curated marketplace of pre-approved vendors speeds solution selection. Early traction appears strongest in fintech customer-service bots and healthcare triage assistants, signaling rapid demand for domain-specific data-engineering services. This groundswell propels revenue diversification beyond large-enterprise accounts and stimulates packaged offerings tailored to resource-constrained clients.

Cyber-Skills Shortage Boosting MSS Demand

An estimated 10,000 cybersecurity up-skilling slots over the next three years will narrow but not close the talent gap. Local MSPs report 98% urgency to expand AI competencies and 82% client pressure for AI-infused defenses. The CSA’s CISO-as-a-Service program offers up to 70% cost offsets, bringing enterprise-grade protection within SME budgets. Consequently, MSS providers that integrate threat intelligence, SOC automation, and compliance consultancy capture rising annuity streams amid escalating attack sophistication.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High manpower costs vs. regional peers | -2.8% | National labor market, acute in specialized roles | Short term (≤ 2 years) |

| Stricter PDPA compliance burden | -1.9% | All data processing entities, cross-border operations | Medium term (2-4 years) |

| Domestic market saturation | -2.1% | Local enterprise segment, government contracts | Long term (≥ 4 years) |

| Data-centre carbon limits and reporting rules | -1.6% | Data center operators, cloud service providers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Manpower Costs vs Regional Peers

Annual software-engineer salaries ranging SGD 60,000-360,000 (USD 44,000-267,000) dwarf equivalents in Malaysia, the Philippines, and Vietnam, where hourly rates run USD 25-59 compared with Singapore’s USD 55-65. Workspace leasing averages SGD 6,023 per seat annually, lifting total cost-of-service delivery above regional alternatives. To defend margins, providers are expanding nearshore pods for commoditized activities, while reserving higher-value architecture and governance tasks for the Singapore hub.

Stricter PDPA Compliance Burden

Amendments to the Personal Data Protection Act require mandatory breach notifications and tighten cross-border transfer controls, raising compliance costs for service operators.[3]Steptoe and Johnson LLP, “Singapore Data Protection: Considerations For Data Driven Compliance Activities,” steptoe.com Although new “legitimate interests” exemptions offer limited flexibility, ongoing interpretive updates force continual policy realignment. Vendors must embed robust audit trails, encryption, and consent-management modules to navigate evolving obligations, increasing operating overhead, yet opening advisory revenue streams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Cloud Dominance Accelerates Digital Transformation

Singapore IT services market size for Cloud and Platform Services registered 35.1% of total spend in 2024. Widespread public-sector migrations and enterprise pursuit of scalable architectures anchor this leadership. Managed Security Services follow as the fastest mover, propelled by a 20.3% CAGR and growing reliance on outsourced SOC capabilities that alleviate talent shortages.

Singapore IT services market share distribution reveals steady demand for IT Consulting and Implementation, which guides complex hybrid-cloud rollouts amid MAS compliance mandates. Business Process Outsourcing maintains relevance by embedding RPA and analytics into customer-care workflows, while pure IT Outsourcing shows moderated growth as automation substitutes for labor arbitrage. Collectively, these patterns position Singapore as a high-value digital services hub rather than a volume-based outsourcing location.

By End-User Enterprise Size: SME Acceleration Transforms Market Dynamics

Large Enterprises generated 62.3% of the Singapore IT services market size in 2024. They continue to drive complex multi-cloud orchestration, zero-trust architectures, and regional compliance harmonization. Yet SMEs are expanding at 18.8% CAGR, backed by grants that subsidize up to 70% of qualifying tech costs and sandbox programs that de-risk GenAI pilots.

The convergence of enterprise needs induces providers to create modular service tiers: fractional CTO engagements, pay-as-you-go cybersecurity bundles, and verticalized SaaS accelerators. As SMEs surpass the 90% digital-tool adoption mark, vendors that can bundle governance, cloud infrastructure, and business-process optimization capture recurring revenue while enlarging the total addressable market.

By Deployment Model: Onshore Preference Balances Cost and Control

Onshore Delivery retained 55.2 of % Singapore IT services market share in 2024, reflecting the premium placed on regulatory compliance, data sovereignty, and responsiveness for mission-critical workloads. Nonetheless, Offshore Delivery’s 19.5% CAGR highlights growing acceptance of distributed agile squads that leverage regional wage differentials.

Hybrid blueprints are now common: strategic design and governance remain onshore, while coding and L1 support flow to nearshore centers in Johor, Manila, and Ho Chi Minh City. Improved collaboration tooling and stringent service-level dashboards sustain quality, ensuring that cost savings do not compromise MAS or PDPA compliance obligations.

By End-User Vertical: BFSI Leadership Meets Healthcare Innovation

BFSI contributed 30.7% of 2024 revenue, underpinned by digitized core banking, real-time payments, and regulatory reporting engines. Regulatory sandboxes encourage continual fintech experimentation, driving demand for secure API gateways and DevSecOps consulting.

Healthcare and Life-Sciences, advancing at 19.2% CAGR, is propelled by a USD 200 million Health Innovation Fund that champions AI-diagnostic pilots and predictive care systems. Manufacturing leverages 5G network-slicing for process automation; Logistics depends on data-driven route optimization; and Energy utilities deploy smart-grid analytics to meet carbon-reporting mandates. Providers that master vertical nuances secure premium margins and longer contract tenures.

Geography Analysis

Singapore’s domestic market is geographically compact yet commercially dense, representing 100% of addressable national demand and acting as the launchpad for wider ASEAN engagements. In 2024, the digital economy contributed SGD 106 billion (USD 78 billion) or 17.3% of GDP, growing at more than twice the overall economy. Over 4,000 tech startups cluster around 70+ data-center facilities with 1.4 GW operational capacity, delivering latency under two milliseconds for most intra-city transactions.[4]Cushman and Wakefield, “Singapore, Hong Kong Rank Third And Fourth In Global Data Centre Market Comparison,” cushmanwakefield.com

Sixteen subsea cables connect Singapore to North America, Europe, and neighboring ASEAN states, ensuring that cloud workloads can burst across regions with minimal jitter. The Bridge Alliance GPU-as-a-Service offering further extends computational elasticity into Thailand, Malaysia, and Indonesia, cementing Singapore’s role as the region’s digital nerve center.

Integration with Johor via the new Special Economic Zone primes hybrid delivery patterns where compute-intensive tasks are processed in Malaysia while governance, orchestration, and customer-facing services remain onshore. As data-localization debates intensify across ASEAN, Singapore’s balanced stance—advocating open data flows alongside robust privacy protections—positions it as the regulatory blueprint for neighboring markets.

Competitive Landscape

The Singapore IT services market hosts a competitive mix of telco-anchored incumbents, global consultancies, and niche domain specialists. Singtel’s NCS leverages deep government ties and a USD 260 million SG6 data-center expansion to secure public-sector and AI-workload contracts. Accenture and IBM differentiate through region-wide delivery networks, while StarHub teams with ServiceNow to automate telecom service-management lifecycles.

Global cloud hyperscalers are doubling down: Google has invested USD 5 billion in data-center infrastructure since 2018, Oracle opened a second cloud region, and NTT DATA is partnering with CSIT to bolster national cyber-defense capabilities. Providers are now judged on AI-readiness, zero-carbon credentials, and the breadth of compliance attestation.

Cost pressures from regional wage gaps spur a flurry of strategic alliances. Singtel and Hitachi are co-developing GPU cloud nodes, while Fortinet’s collaboration with CSA embeds threat-intelligence feeds into national critical information infrastructures. Market share remains fluid, with emergent deep-tech startups securing funding rounds—DiMuto, Aprisium, and Decagon among them—injecting innovation into supply-chain transparency and AI-powered customer support.

Singapore IT Services Industry Leaders

NCS Pte Ltd

Singapore Telecommunications Ltd (Singtel)

Accenture Pte Ltd

IBM Singapore Pte Ltd

StarHub Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Equinix committed USD 260 million to its sixth Singapore data center (SG6) to support high-density AI workloads.

- October 2024: Google completed a campus expansion that lifts its Singapore investment tally to USD 5 billion.

- October 2024: NTT DATA and CSIT signed an MoU to bolster national cyber-defense capabilities.

- August 2024: Singtel and Hitachi partnered to build next-generation GPU cloud infrastructure across the Asia Pacific.

Singapore IT Services Market Report Scope

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Onshore Delivery |

| Nearshore Delivery |

| Offshore Delivery |

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-User Verticals |

| By Service Type | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By Deployment Model | Onshore Delivery |

| Nearshore Delivery | |

| Offshore Delivery | |

| By End-User Vertical | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| Healthcare and Life-Sciences | |

| Retail and Consumer Goods | |

| Telecom and Media | |

| Logistics and Transport | |

| Energy and Utilities | |

| Other End-User Verticals |

Key Questions Answered in the Report

How big is the Singapore IT services market in 2025?

It stands at USD 29.80 billion and is projected to grow to USD 65.80 billion by 2030.

Which service line leads spending?

Cloud and Platform Services hold a 35.1% share, reflecting sustained migrations and Smart Nation mandates.

What segment is expanding fastest?

Managed Security Services is advancing at a 20.3% CAGR through 2030 due to acute cyber-skills shortages.

Why are SMEs important to providers?

Adoption grants covering up to 70% of project costs are driving an 18.8% CAGR among SMEs, enlarging the addressable base.

How are delivery models evolving?

Hybrid approaches place strategic oversight onshore while routing development and support to near/offshore hubs, balancing cost and compliance.

Page last updated on: