Vietnam Data Center Server Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

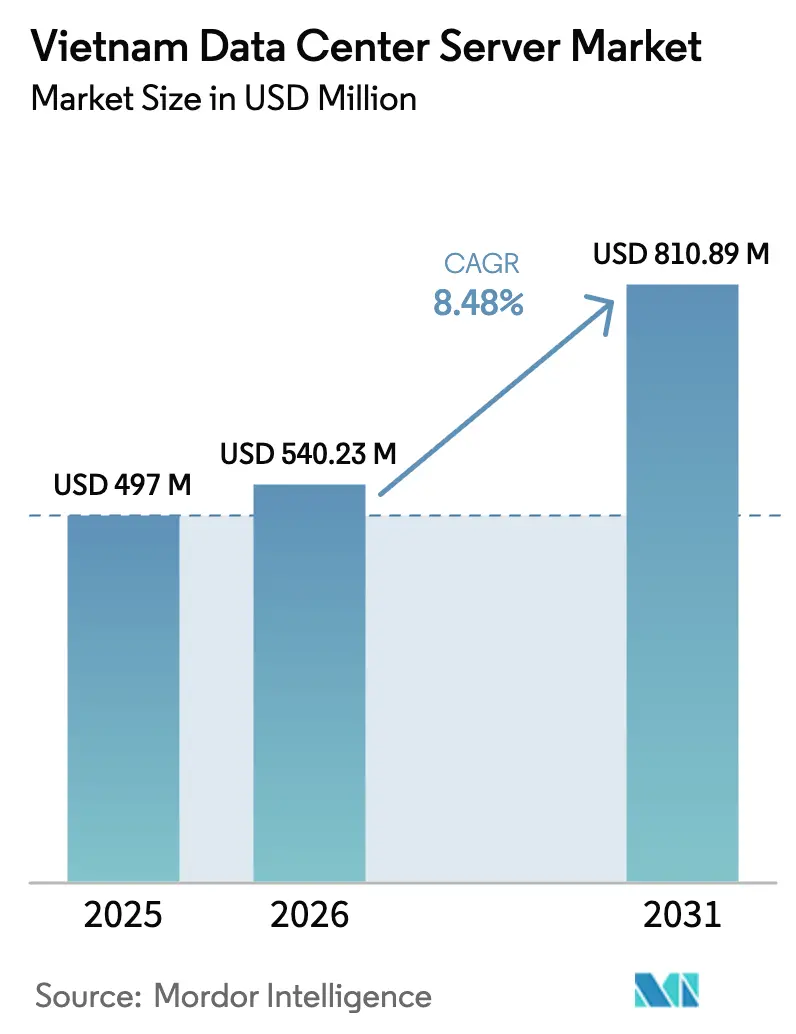

| Base Year Market Size (2025) | USD 497 Million |

| Market Size (2026) | USD 540.23 Million |

| Market Size (2031) | USD 810.89 Million |

| Growth Rate (2026 - 2031) | 8.48% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Data Center Server Market Analysis by Mordor Intelligence

The Vietnam data center server market size is expected to grow from USD 497 million in 2025 to USD 540.23 million in 2026 and is forecast to reach USD 810.89 million by 2031 at 8.48% CAGR over 2026-2031. Robust fiscal incentives for digital infrastructure, ongoing power-sector upgrades and the removal of foreign ownership limits are accelerating capital inflows into new server capacity. Tier 3 facilities dominate deployments, yet Tier 4 builds are rising quickly as hyperscalers demand concurrent maintainability for AI clusters. Half-height blades remain the preferred form factor, though quarter-height and micro-blade systems are growing as operators pursue rack-level density gains. Edge nodes in second-tier cities, direct power-purchase agreements and the China + 1 manufacturing pivot continue to reinforce Vietnam’s status as a strategic Southeast Asian hub.

Key Report Takeaways

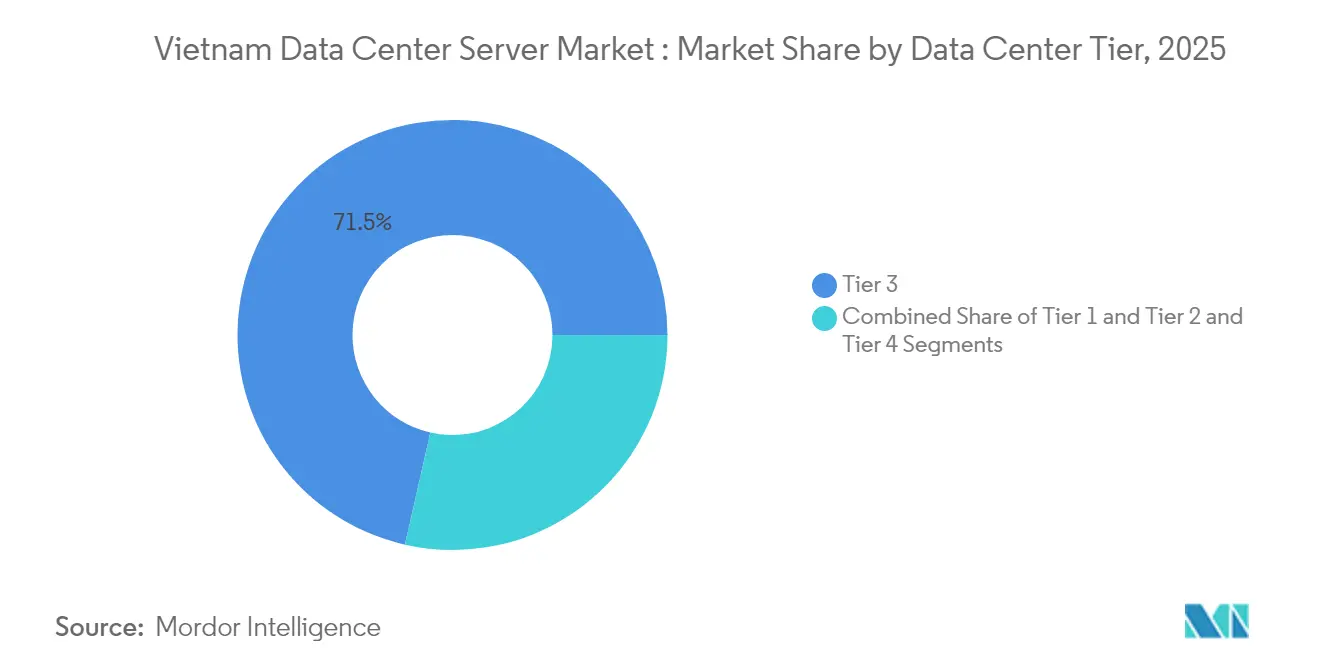

- By data-center tier, Tier 3 facilities led with 71.45% of Vietnam data center server market share in 2025; Tier 4 is forecast to expand at 16.08% CAGR through 2031.

- By form factor, half-height blade servers accounted for 47.98% of Vietnam data center server market size in 2025, while quarter-height and micro-blade systems record the highest projected CAGR at 14.87% between 2026-2031.

- By application, virtualization and private cloud held 38.74% share of the Vietnam data center server market size in 2025; AI / ML workloads are advancing at 17.05% CAGR through 2031.

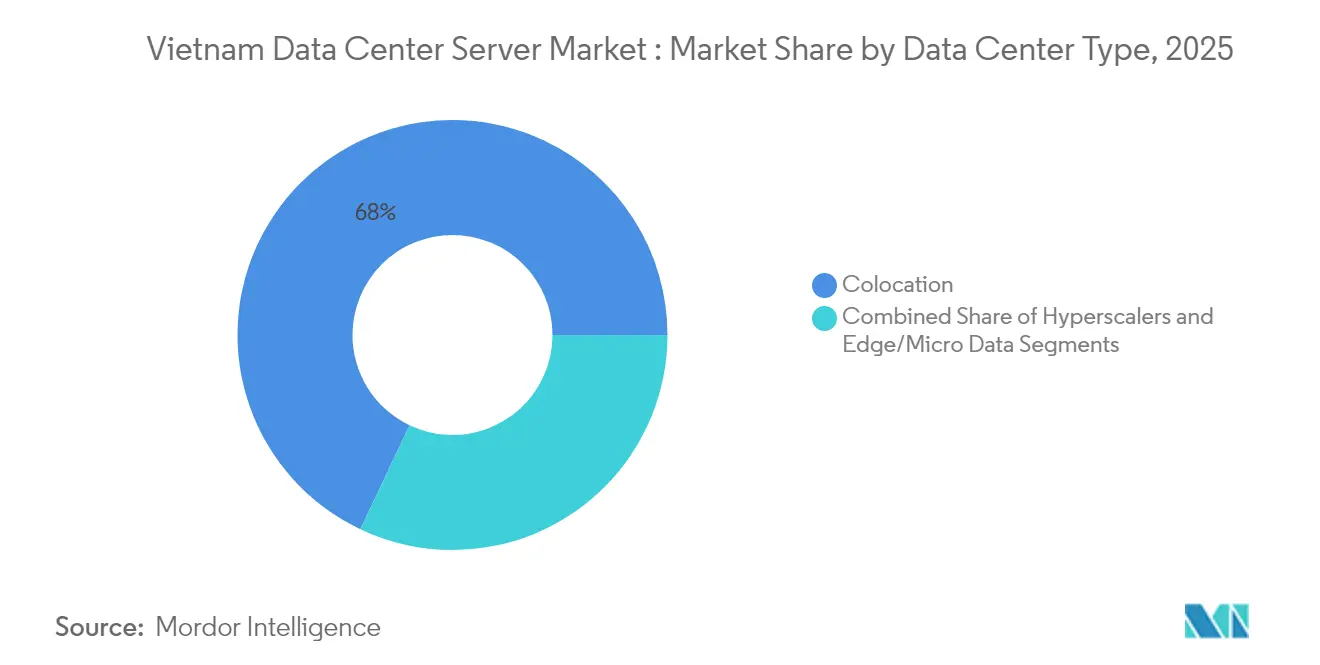

- By data-center type, colocation sites commanded 67.95% of Vietnam data center server market size in 2025; hyperscaler facilities are growing at 14.76% CAGR to 2031.

- By end-use industry, IT & telecommunications captured 25.93% of Vietnam data center server market share in 2025; government deployments are the fastest climber at 12.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam contributes to a system defined not by any single country or region but by the interaction of many. The global data center server market data by Mordor Intelligence represents that combined structure.

Vietnam Data Center Server Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in construction of new data centers and internet infrastructure | +2.8% | National, concentrated in HCMC and Hanoi | Medium term (2-4 years) |

| Increasing adoption of cloud and IoT services | + 2.1% | National, with enterprise focus in major cities | Short term (≤ 2 years) |

| Government data-localization and digital-economy mandates | +1.9% | National, affecting all sectors | Long term (≥ 4 years) |

| China + 1 shift catalyzing server assembly in Vietnam | +1.2% | Northern provinces, Bac Giang and Binh Duong | Medium term (2-4 years) |

| Emergence of AI/GPU clusters for Vietnamese LLMs | +0.6% | HCMC and Hanoi tech corridors | Long term (≥ 4 years) |

| Tier-2 city tax abatements attracting second-wave data-center builds | +0.6% | National, with early gains Tier 2 areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increase in construction of new data centers and internet infrastructure

Vietnam’s construction boom is redefining server demand. Viettel’s 140 MW Ho Chi Minh City campus is the first domestic site to break the 100 MW threshold, prompting bespoke blade configurations optimized for tropical airflow and renewable-ready power systems.[1]Datacenter Dynamics, “Viettel breaks ground on Ho Chi Minh City’s first 140 MW data center,” datacenterdynamics.com Secondary-city edge sites are multiplying to support 5G backhaul and latency-sensitive workloads. Foreign investors such as Saigon Asset Management have committed USD 1.5 billion for a 150 MW campus in Binh Duong Province, intensifying requirements for local assembly partnerships that shorten delivery cycles.

Increasing adoption of cloud and IoT services

A USD 45 billion digital-economy target for 2025 stimulates enterprise cloud migration. Manufacturing zones in Tan Thuan deploy ruggedized edge servers for predictive-maintenance analytics, while Foxconn’s Lighthouse Factory in Bac Giang runs GPU-enabled digital-twin workloads that drive premium server demand. Healthcare digitization adds further momentum as Bach Mai Hospital scales electronic medical records across a nationwide care network.[2]Light Reading, “SAM plans USD 1.5B data-center campus in Binh Duong,” lightreading.com

Government data-localization and digital-economy mandates

The Law on Data, effective January 2025, obliges sensitive data to reside onshore, compelling global clouds to build domestic server farms rather than service Vietnam remotely. Banks such as An Binh deploy secure, Fortinet-hardened architectures to comply with sovereignty rules, while the National Data Center’s August 2025 launch will standardize procurement of certified, tamper-resistant servers.

China + 1 shift catalyzing server assembly in Vietnam

Quanta Computer’s USD 50 million factory and Taiwanese OEM expansions illustrate the pivot of server assembly to Vietnam’s northern corridor. Tariff advantages on U.S. exports and skilled labor pools enable local customization that addresses high-humidity conditions and local compliance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capex for data-center construction | -1.4% | National, particularly affecting SME deployments | Short term (≤ 2 years) |

| Limited grid reliability and rising electricity tariffs | -1.1% | Ho Chi Minh City and industrial zones | Medium term (2-4 years) |

| Shortage of certified data-center engineers | -0.8% | National, acute in tier-2 cities | Long term (≥ 4 years) |

| Fragmented local supply chain for advanced components | -0.5% | Northern manufacturing corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High initial capex for data-center construction

Even at USD 6.9 million per MW, financing hurdles constrain small-to-mid-size firms. Electrical systems absorb a disproportionate share of budgets, steering buyers to standardized rack-mount servers that maximize watt-per-compute ratios. Asset-management funds are emerging to defray capex, yet procurement teams still favor lifecycle-cost optimization over raw performance.

Limited grid reliability and rising electricity tariffs

Vietnam needs USD 128.3 billion in grid investments through 2030, and periodic shortages in Ho Chi Minh City elevate operational risk.[3]International Trade Administration, “Vietnam Power Development Plan VIII overview,” trade.gov Operators lock in renewable supply via direct power-purchase agreements, compelling server OEMs to certify low-power silicon and liquid cooling for racks exceeding 30 kW BCLP.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data-Center Tier: Enterprise-Grade Infrastructure Dominates

Tier 3 facilities held 71.45% share of the Vietnam data center server market in 2025, mirroring enterprise tolerance for cost-balanced redundancy. This tier underpins banking, telecom and public-sector workloads that stipulate 99.982% availability. Operators specify dual-power blades, hot-swappable drives and battery-assisted modules to control Mean-Time-To-Repair. Tier 4 sites, growing 16.08% CAGR, are propelled by hyperscalers building AI clusters that require concurrent maintainability.

Vietnam data center server market size within Tier 4 is projected to expand sharply as GPU-dense racks demand fault-tolerant cooling. Tier 1 and Tier 2 venues remain viable for distributed edge nodes, housing cost-optimized 1U and 2U servers. NTT’s 6 MW Ho Chi Minh City 1 facility exemplifies how foreign entrants target Tier 3 specifications for regional cloud tenancy. AI-ready blueprinting accelerates Tier 4 adoption, with facilities provisioning 100 kW per rack for Blackwell-class GPUs.

By Form Factor: Density Optimization Drives Micro-Blade Adoption

Half-height blades retained 47.98% share in 2025, delivering a sweet spot of density versus thermal headroom. Enterprises leverage integrated chassis management to streamline firmware updates and power budgeting. Quarter-height and micro-blade platforms rise at 14.87% CAGR, reflecting edge-site constraints where floor space and power feeds are limited.

Vietnam data center server market size for micro-blade deployments benefits from telecom 5G rollouts that embed compute at radio access points. Full-height blades serve HPC clusters in research institutes funded under the Vietnam National University program. Telecommunications players, notably Viettel, standardize micro-blades to minimize heat per RU, aiding operations in 35 °C ambient climates.

By Application/Workload: AI Transformation Accelerates Beyond Virtualization

Virtualization and private cloud workloads delivered 38.74% of revenue in 2025. Enterprises continue to collapse legacy x86 footprints onto VMware- and KVM-based clusters. AI / ML server shipments, however, surge 17.05% CAGR. Telecommunications firms employ GPU farms for natural-language chatbots and anti-fraud analytics under Korea Telecom’s USD 94.6 million pact with Viettel.

Vietnam data center server market size tied to AI applications will eclipse virtualization in large sites by 2028. HPC workloads remain niche, servicing seismic modeling and pharmaceutical research. Storage-centric builds fulfill regulatory backup mandates, while IoT gateway servers proliferate in Industry 4.0 plants such as Samsung’s smart-factory program.

By Data-Center Type: Hyperscaler Expansion Challenges Colocation Dominance

Colocation facilities accounted for 67.95% of capacity in 2025 as enterprises prefer OPEX models over building proprietary halls. Viettel IDC alone manages 49% of domestic colocation racks, bundling connectivity with managed services. Hyperscaler investment, now climbing at 14.76% CAGR, is reshaping the Vietnam data center server market as foreign clouds deploy dedicated campuses.

Vietnam data center server market share for hyperscalers is fueled by policy liberalization removing equity caps on foreign investors in July 2024 VietnamBriefing. Google’s site-selection studies and Amazon’s regional roadmaps signal further divergence toward 200 MW-plus campuses. Edge and enterprise micro-centers persist for low-latency workloads where data sovereignty or process-control loops preclude public cloud.

By End-Use Industry: Government Digitization Outpaces Traditional Leaders

IT & telecommunications absorbed 25.93% of server shipments in 2025, sustaining network-core modernization and 5G RAN upgrades with Qualcomm-enabled massive-MIMO servers, LightReading. Yet government programs log the steepest growth at 12.74% CAGR, energised by the National Data Center and mandatory digital-process initiatives.

Vietnam data center server industry participants serve BFSI clients evolving digital-banking stacks, such as Cake Digital Bank’s AI-driven risk engines hosted on GPU servers, Google Cloud. Healthcare adoption rises with electronic health-record rollouts, while energy utilities deploy hardened servers for smart-grid telemetry along transmission corridors.

Geography Analysis

Ho Chi Minh City and Hanoi concentrate nearly 80% of installed server racks because they couple submarine-cable gateways with dense enterprise clusters. Ho Chi Minh City’s Saigon Hi-Tech Park supports hyperscale builds such as Viettel’s 140 MW campus, benefitting from proximity to AAE-1 and APG cable landings. Hanoi’s political role secures federal workloads and disaster-recovery preferring geographic dispersion from the south.

Secondary nodes such as Da Nang emerge as edge aggregation points; its IDC facility offers latency under 20 milliseconds to both major hubs DevelopingTelecoms. Northern provinces, led by Bac Giang, evolve into server-assembly hotbeds under the China + 1 strategy, leveraging road links to Shenzhen suppliers. Foxconn’s Lighthouse Factory illustrates deep-tier integration supporting custom tropical server SKUs SloveniaTimes.

Vietnam data center server market size grows in Binh Duong and Long An as power projects under PDP VIII unlock loads above 100 MW backed by solar farms. Grid-reliability upgrades and direct PPAs entice investors like Saigon Asset Management to place USD 1.5 billion campuses close to major industrial parks LightReading. Coastal fiber-landing expansions widen resilience for east-west traffic, enhancing appeal for multi-region replicas.

The data center server market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Americas, Europe, and Asia. This is complemented by country-specific insights for Indonesia, India, Brazil, Sweden, Hong Kong, and France, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

Domestic telecom heavyweights retain significant sway. Viettel Group, integrating fiber, mobile and IDC footprints, operates 230,000 servers across 14 sites and captures almost half of national colocation revenue TheInvestor. VNPT and FPT follow with nationwide fiber rings and government contract pipelines. International OEMs compete through alliance models; Dell Technologies partners with FPT Information System to bundle PowerEdge platforms with local compliance services, while HPE collaborates with FPT for AI factory offerings FPTSoftware.

Competition pivots on AI-optimized designs and energy efficiency. NVIDIA’s forthcoming R&D center will seed ecosystem demand for Blackwell GPU blades and liquid-cool racks NVIDIA. White-space opportunities persist in Tier 2-city edge deployments where local SI integrators such as CMC Telecom deliver ruggedized, environmental-grade servers.

Foreign ownership liberalization heightens rivalry. Google and Microsoft scout sites for first-party campuses, raising supply-chain award stakes for ODMs assembling in Bac Ninh. Market entrants must differentiate via renewable integration, advanced cooling and sovereign-cloud certifications to win public-sector and regulated-industry bids.

Vietnam Data Center Server Industry Leaders

Dell Inc.

Hewlett Packard Enterprise

Cisco Systems Inc.

Huawei Technologies Co. Ltd.

Inspur Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Korea Telecom and Viettel signed a USD 94.6 million AI technology partnership targeting GPU farms for Vietnamese-language virtual assistants and anti-fraud analytics

- May 2025: Dell Technologies introduced PowerEdge XE9780/XE9785 servers supporting 192 NVIDIA Blackwell Ultra GPUs for AI training workloads.

- April 2025: Viettel broke ground on a 140 MW Ho Chi Minh City data center, the first domestic facility to exceed 100 MW

- March 2025: Saigon Asset Management unveiled a USD 1.5 billion 150 MW campus in Binh Duong and a USD 300 million Vietnam Data Center Fund

- February 2025: Dell launched its Open Telecom Transformation Program to accelerate cloud-native networks for telecom operators.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Vietnam data center server market as all new rack, blade, and micro-blade servers that are installed inside purpose-built or retrofit data centers across the country and delivered through OEM or system-integrator channels. These servers power enterprise, colocation, edge, and hyperscale workloads, and the market value is tracked in USD at factory gate prices, net of installation.

Scope exclusion: we do not count refurbished units or servers embedded in consumer-grade micro facilities.

Segmentation Overview

- By Data-Center Tier

- Tier 1 and 2

- Tier 3

- Tier 4

- By Form Factor

- Half-height Blades

- Full-height Blades

- Quarter-height / Micro-blades

- By Application / Workload

- Virtualisation and Private Cloud

- High-Performance Computing (HPC)

- Artificial Intelligence/Machine Learning and Data Analytics

- Storage-centric

- Edge / IoT Gateways

- By Data Center Type

- Hyperscalers/Cloud Service Provider

- Colocation Facilities

- Enterprise and Edge

- By End-use Industry

- BFSI

- IT and Telecom

- Healthcare and Life-Sciences

- Manufacturing and Industry 4.0

- Energy and Utilities

- Government and Defence

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed server OEM product managers, Vietnam-based colocation operators, and cloud architects in Ho Chi Minh City, Hanoi, and Da Nang. The conversations validated power-density assumptions, typical discount curves on high-volume deals, and the share of AI accelerators in 2024 purchase orders, thereby refining shipment-to-revenue conversions.

Desk Research

We began with public data sets from the General Statistics Office of Vietnam, EVN power-tariff filings, and customs import codes 8471.50.x for computing equipment, which clarified shipment baselines. Trade-association white papers from the Vietnam Internet Association and the Asia Cloud Computing Association provided density factors for rack utilization. Academic papers indexed in IEEE Xplore detailed emerging AI server thermal profiles, while patent families pulled through Questel helped gauge future liquid-cooling penetration. Finally, company 10-Ks and press releases gave server ASP trends. These illustrative sources sit alongside information drawn from paid databases such as D&B Hoovers and Dow Jones Factiva for company revenue splits. The list above is not exhaustive; many other open datasets and periodicals were consulted to cross-check figures and fill gaps.

Market-Sizing & Forecasting

We anchored 2025 demand using a top-down reconstruction of server imports and domestic assembly, which are then aligned with data-center floor-space additions and average rack counts. Select bottom-up checks sampled hyperscaler purchase orders and channel inventory roll-ups, which tempered over-reporting risks. Key drivers in our model include 5G site build-outs, data-localization deadlines, average rack power (kW), server ASP trajectories, and SME cloud-migration ratios. A multivariate regression relates these variables to annual server revenue, while scenario analysis tests grid-tariff shocks. Where channel data were patchy, shipment gaps were bridged with three-year moving averages confirmed during expert calls.

Data Validation & Update Cycle

Outputs move through peer review, anomaly scans against independent metrics like IT load MW additions, and senior analyst sign-off. Reports refresh annually, and interim updates trigger when tariff hikes, policy changes, or ≥5 MW hyperscale announcements alter the baseline.

Why Mordor's Vietnam Data Center Server Baseline Commands Reliability

Published estimates differ because firms choose divergent scopes, discount treatments, and refresh cadences. We trace every value back to transparent shipment, power, and pricing variables before applying consistent currency and tax assumptions.

Key gap drivers with other studies include Mordor's inclusion of micro-blade edge deployments, annual FX resets, and live tariff pass-throughs, whereas peers often freeze exchange rates or exclude edge nodes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 497.99 M (2025) | Mordor Intelligence | - |

| USD 403 M (2023) | Regional Consultancy A | excludes edge sites and applies static 1.9 kW/rack density |

| USD 210 M (2024) | Global Consultancy B | omits colocation purchases and uses 2019 ASP benchmark |

| USD 100 M (2024) | Industry Journal C | tracks only tier-1 OEM shipments, ignoring white-box volume |

Taken together, the comparison shows that Mordor's disciplined blend of public shipments, primary validations, and timely refreshes offers decision-makers a balanced, reproducible baseline tied to clearly observable market fingerprints.

Key Questions Answered in the Report

What is the current size of the Vietnam data center server market?

The Vietnam data center server market generates USD 540.23 million in 2026 revenue and is forecast to reach USD 810.89 million by 2031.

Which data-center tier holds the largest share?

Tier 3 facilities command 71.45% of deployments, offering enterprises a balance of high availability and manageable costs.

How fast is the AI server segment expanding?

AI / machine-learning workloads are increasing at a 17.05% CAGR, outpacing all other application segments through 2031.

Why are hyperscalers investing in Vietnam?

Liberalized foreign-ownership rules, low construction costs of USD 6.9 million per MW and data-localization laws make Vietnam an attractive location for hyperscale campuses.

Page last updated on: