Vietnam HVAC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

| Market Size (2026) | USD 3.91 Billion |

| Market Size (2031) | USD 5.48 Billion |

| Growth Rate (2026 - 2031) | 6.96% CAGR |

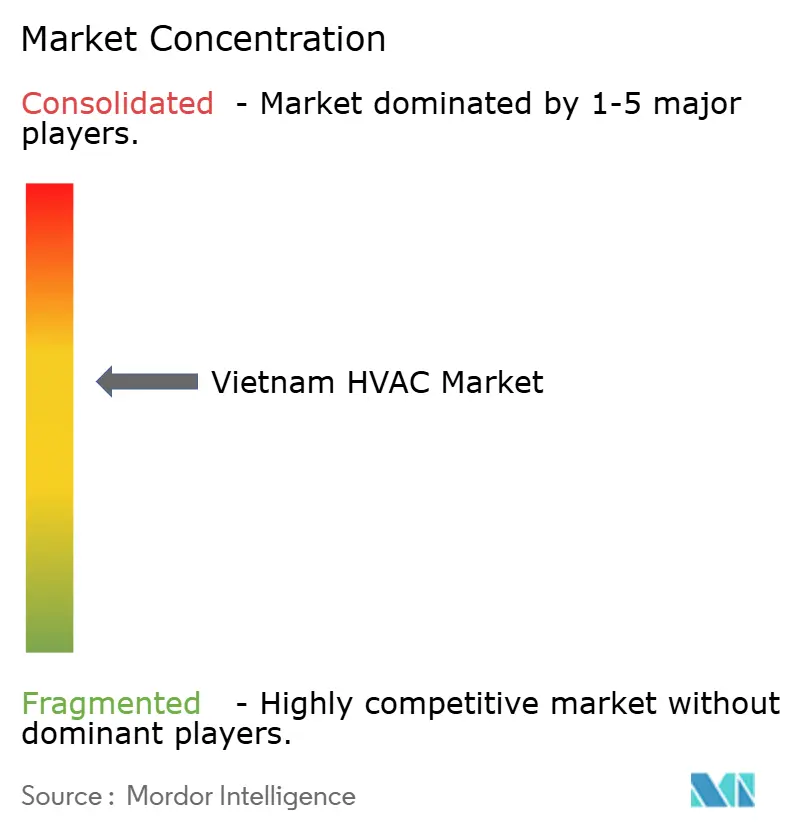

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam HVAC Market Analysis by Mordor Intelligence

The Vietnam HVAC market size stood at USD 3.91 billion in 2026 and is projected to reach USD 5.48 billion by 2031, advancing at a 6.96% CAGR over the forecast period. Robust GDP growth, accelerating urbanization, and a steady pipeline of mixed-use construction are enlarging the Vietnam HVAC market by broadening the customer base across residential, commercial, and industrial applications. Foreign direct investment into electronics assembly and semiconductor packaging is spurring demand for precision cleanroom air-handling, while the hospitality sector’s post-pandemic rebound is boosting requirements for centralized chillers and low-noise guest-room systems. Government energy-efficiency incentives, together with mandatory performance standards for non-ducted air conditioners that took effect in 2025, are tilting preferences toward inverter-driven equipment and variable refrigerant flow platforms, reshaping competitive positioning in the Vietnam HVAC market. At the same time, tighter refrigerant regulations and district-cooling pilots are creating white-space opportunities for suppliers of low-GWP refrigerants, integrated controls, and performance-based service contracts.

Key Report Takeaways

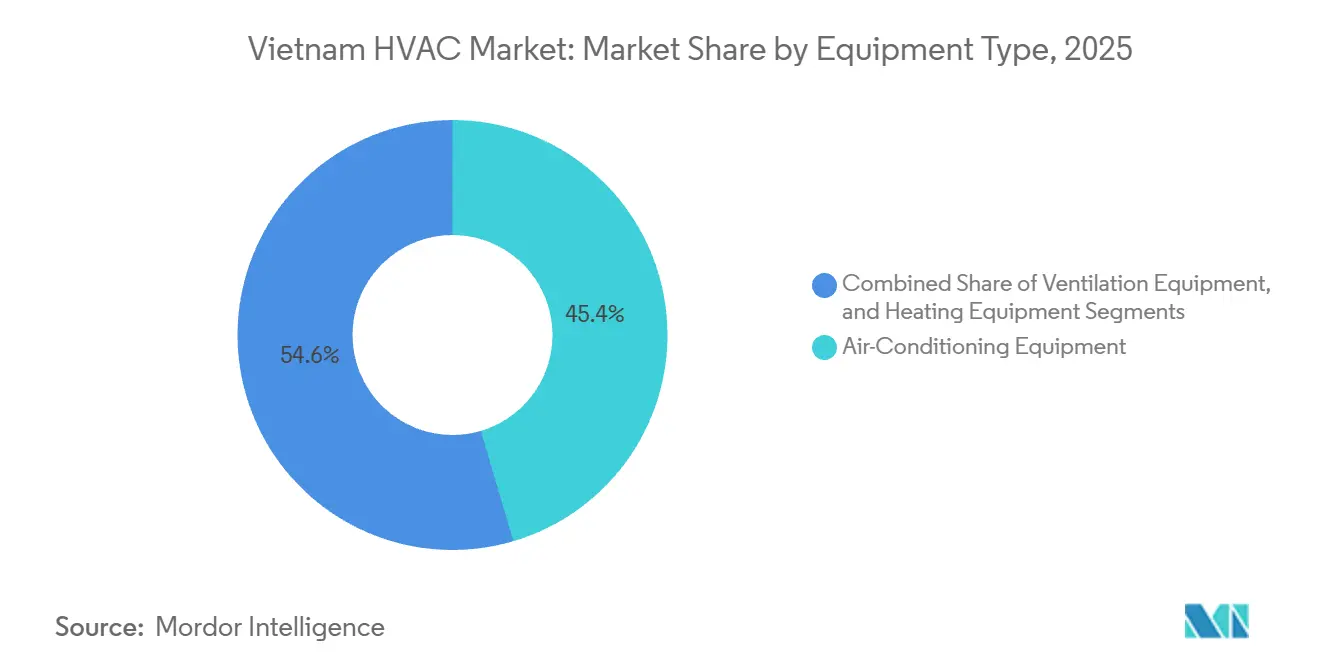

- By equipment type, air-conditioning equipment accounted for 45.43% of the Vietnam HVAC market revenue in 2025, and is forecast to expand at a 7.43% CAGR through 2031.

- By installation type, retrofit and replacement accounted for 61.64% of the Vietnam HVAC market in 2025, whereas new construction is projected to log the fastest 7.89% CAGR to 2031.

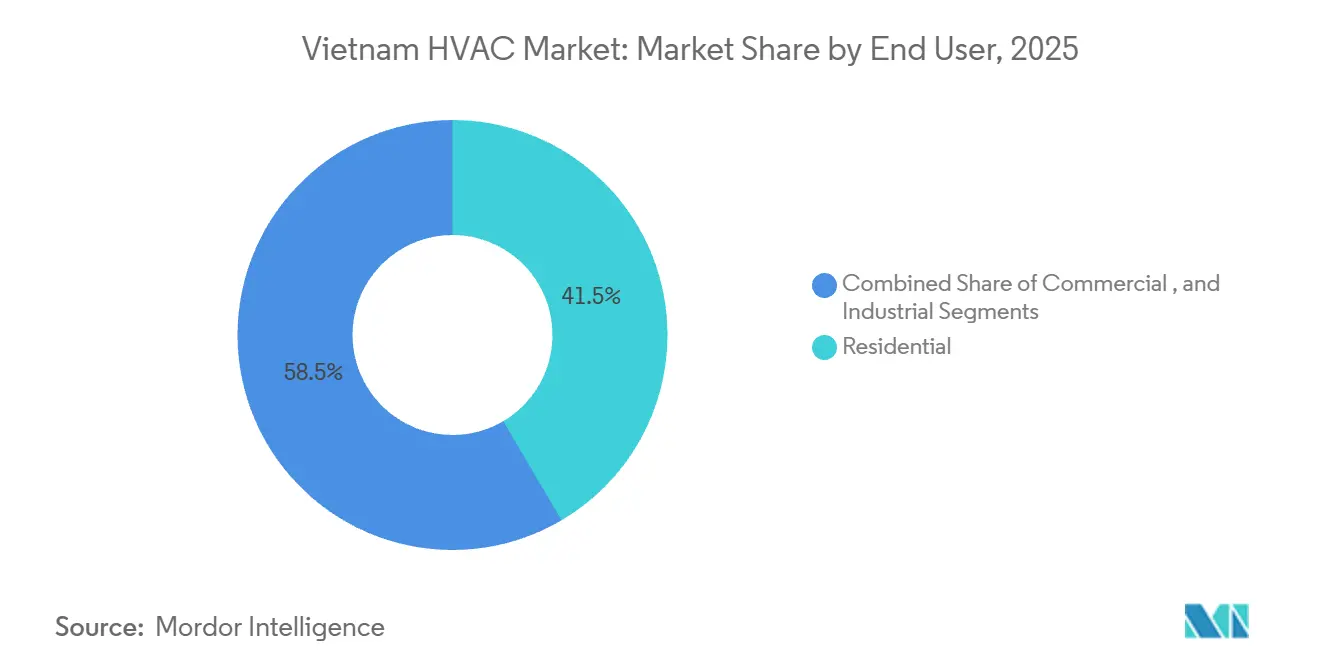

- By end user, residential systems accounted for 41.53% of the Vietnam HVAC market in 2025, while commercial applications are expected to post the highest 7.68% CAGR during the outlook period.

- By building type within commercial facilities, office buildings held 34.23% of the Vietnam HVAC market share in 2025, whereas data centers are forecast to grow at an 8.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam HVAC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Tourism and Hospitality Sector | +1.20% | National, concentration in Ho Chi Minh City, Hanoi, Da Nang, Phu Quoc | Medium term (2-4 years) |

| Rising Disposable Income and Urbanization | +1.50% | National, accelerated gains in Ho Chi Minh City, Hanoi, Can Tho | Long term (≥ 4 years) |

| Government Incentives for Energy-Efficient Buildings | +0.90% | National, early adoption in Hanoi, Ho Chi Minh City, Thu Duc City | Medium term (2-4 years) |

| Rapid Growth of Commercial Real-Estate Construction | +1.30% | Ho Chi Minh City, Hanoi, Thu Duc City, Binh Duong Province | Short term (≤ 2 years) |

| Adoption of District Cooling in Smart-City Projects | +0.60% | Thu Thiem, Dong Anh, Can Tho pilot zones | Long term (≥ 4 years) |

| Expansion of Foreign-Invested Cleanroom Manufacturing Plants | +1.10% | Bac Ninh, Bac Giang, Hai Phong, Ho Chi Minh City | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Tourism And Hospitality Sector

Visitor arrivals are rebounding toward the 25 million target set for 2025, and the national hotel pipeline now tops 49,800 rooms concentrated in Ho Chi Minh City, Hanoi, Da Nang, and Phu Quoc.[1]United Nations Environment Programme, “Harmonizing of Energy-Efficiency Standards for Room Air Conditioners in Southeast Asia,” unep.org Hotels are specifying centralized chillers, VRF systems, and low-noise ductless units that meet QCVN 09:2017/BXD efficiency benchmarks, pushing contractors to incorporate inverter compressors and R-32 refrigerant. International brands require compliance with ASHRAE 55 thermal-comfort standards and ISO 7730 metrics, prompting the integration of building management systems to reduce peak electrical demand during high-occupancy periods. Wellness amenities and spa zones require precise humidity control, driving demand for high-efficiency air-handling units. The sector’s focus on life-cycle cost savings is accelerating the shift toward energy-recovery ventilators and performance-based maintenance contracts.

Rising Disposable Income And Urbanization

Urbanization is near 45%, and metropolitan populations in Hanoi and Ho Chi Minh City are growing 3-4% annually, extending the Vietnam HVAC market across mid-rise condominiums and high-rise apartments. Rising household incomes enable middle-class buyers to upgrade from window units to multi-zone inverter mini-splits, while luxury projects increasingly pre-install VRF systems. TCVN 7830:2021 minimum performance thresholds, mandatory since January 2025, are phasing out fixed-speed models and reinforcing demand for variable-speed platforms. Developers align with green-building labels to attract buyers, using high CSPF scores as marketing levers. Localized production by LG, Daikin, and Mitsubishi Electric reduces lead times and supports after-sales service networks that are critical to residential purchase decisions.[2]LG Electronics, “LG Expands HVAC Business With New Global South Facility,” lgcorp.com

Rapid Growth Of Commercial Real-Estate Construction

Office building and mixed-use development cycles in Ho Chi Minh City, Hanoi, and Binh Duong are shortening as foreign tenants seek modern, Grade A space. Projects such as the USD 2.2 billion Lotte Eco Smart City in Thu Thiem require large-capacity chillers, vertical distribution risers, and smart controls that optimize energy use across hotels, retail, and condominiums. VRF systems are the preferred choice for mid-rise offices because they reduce ductwork and mechanical-room footprints and provide simultaneous heating and cooling with refrigerant heat recovery. QCVN 04:2019/BXD mandates higher fresh-air rates and smoke-extraction capability, lifting demand for dedicated outdoor-air systems and energy-recovery ventilators. Developers increasingly adopt digital twins during design to select equipment and predict life-cycle energy consumption.

Expansion Of Foreign-Invested Cleanroom Manufacturing Plants

Greenfield electronics, display, and semiconductor factories in Bac Ninh, Bac Giang, Hai Phong, and Ho Chi Minh City are driving rapid adoption of ISO 14644-class cleanroom HVAC systems. Precision air-handling units with HEPA filtration, positive-pressure cascades, and tight temperature-humidity tolerances underpin yields in system-in-package assembly and display manufacturing. Multinationals stipulate NEBB testing and ASHRAE cleanroom standards, creating opportunities for Vietnamese contractors that can deliver end-to-end design and validation. Large projects often specify liquid-cooling or desiccant dehumidification to control latent loads and meet energy budgets. Local component fabrication shortens lead times for terminal HEPA housings and stainless-steel ductwork, supporting further cost optimization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Installation and Maintenance Costs | -0.80% | National, more acute in rural and secondary cities | Medium term (2-4 years) |

| Volatile Electricity Tariffs Increasing Operating Costs | -0.70% | National, high sensitivity in commercial and industrial segments | Short term (≤ 2 years) |

| Skilled Labor Shortage Inflating Installation Lead Times | -0.50% | Hanoi, Ho Chi Minh City, Bac Ninh, Hai Phong | Medium term (2-4 years) |

| Limited Domestic Production of Low-GWP Refrigerants | -0.40% | National, import-dependent supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Installation And Maintenance Costs

Centralized chillers, VRF platforms, and cleanroom air-handling units require specialized engineering, ductwork fabrication, and structural adaptations that can add 20-30% to project capital outlays, restricting adoption among SMEs and budget-sensitive developers. Lifecycle service costs are elevated by periodic refrigerant handling, filter replacement, and digital controls calibration, all of which demand certified technicians. A shortage of HVAC professionals trained to QCVN 21:2015/BLĐTBXH and ASHRAE standards pushes wages upward and extends downtime when failures occur. Smaller residential customers in secondary cities gravitate toward fixed-speed units that cost less despite higher energy bills. Limited access to concessional financing further slows the uptake of high-efficiency retrofits.

Volatile Electricity Tariffs Increasing Operating Costs

EVN implemented two successive 4.8% tariff hikes in 2024 and 2025, raising operating expenses for building owners and lengthening payback periods for efficiency upgrades.[3]Vietnam Electricity, “Average Retail Electricity Tariff Adjustment 2025,” evn.com.vn HVAC loads represent 30-50% of electricity consumption in typical commercial buildings and up to 60% in data centers, making tariff uncertainty a material budgeting risk. While higher prices encourage investment in variable-speed drives, free-cooling economizers, and thermal-storage systems, many facility managers defer replacement until tariffs stabilize. PDP8’s shift toward renewable generation introduces grid-balancing costs that may prompt further rate adjustments. Residential consumers delay replacing inefficient window units, slowing penetration of inverter mini-splits that align with national energy-saving goals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Air-Conditioning Sustainability Redefines Demand

Air-conditioning equipment captured 45.43% of the Vietnam HVAC market revenue share in 2025, and the segment is poised to grow at a 7.43% CAGR through 2031. In the Vietnam HVAC market, ductless mini-splits dominate residential applications because they can be wired to single-phase power and require minimal structural work. Commercial buyers favor variable refrigerant flow systems that provide zone independence and recover waste heat, improving part-load efficiency across open-plan offices and co-working spaces. Chiller demand is stable in hotels, hospitals, and high-rise offices where plant capacities exceed 500 TR, with screw and centrifugal compressors preferred for high COPs at both full and part load. The shift toward R-32 refrigerant and microchannel condensers is reducing charge volumes and improving heat-transfer coefficients. Packaged rooftop units and terminal air conditioners remain staples in small retail and stand-alone classrooms owing to their plug-and-play serviceability.

Heating equipment remains a niche because tropical temperatures seldom drop below 18 °C, but heat-pump water heaters are gaining traction in resorts and hospitals that value energy recovered from condenser waste heat. Ventilation products, including dedicated outdoor-air systems, energy-recovery ventilators, and smart CO₂-based demand control, are registering steady gains as QCVN 04:2019/BXD tightens fresh-air and smoke-extraction mandates. In cleanrooms and healthcare isolation wards, fan-filter units with EC motors and ULPA filters meet stricter particulate and pathogen thresholds. Suppliers that bundle air-conditioning and ventilation equipment with unified controls can differentiate on commissioning speed and data analytics capabilities.

By Installation Type: Retrofit Dominance Meets New-Build Momentum

Retrofit and replacement accounted for 61.64% of the Vietnam HVAC market in 2025, as buildings erected before QCVN 09:2017/BXD seek energy-efficiency upgrades and digital controls. Owners of pre-2010 offices, hotels, and retail centers frequently replace fixed-speed chillers and pneumatic controls with inverter-driven systems and building management systems, cutting annual electricity bills by as much as 30%. VNEEP audit mandates for facilities surpassing 1,000 TOE per year unlock concessional loans and tax incentives that shorten payback to fewer than five years, expanding the Vietnam HVAC market size for retrofit services. Residential demand is driven by mid-income households upgrading to quieter, Wi-Fi-enabled mini-splits that integrate with smart-home ecosystems.

New-build installations are projected to grow at a 7.89% CAGR, powered by mega-projects such as Thu Thiem’s Lotte Eco Smart City and Dong Anh Smart City near Hanoi. Integrated design teams employ BIM and prefabricated MEP modules to accelerate schedules and minimize material waste. District-cooling feasibility studies in Thu Thiem and Can Tho favor high-efficiency chillers, thermal storage tanks, and tertiary loops serving mixed-use clusters. Greenfield factories in northern industrial hubs install ISO-compliant cleanrooms and high-static-pressure air-handling units during the shell-and-core stage to avoid costly retrofits. As construction shifts toward green certification, first-cost premiums for high-efficiency HVAC are increasingly justified by lower operational expenditure and tenant attraction.

By End User: Commercial Momentum Strengthens Despite Residential Base

The residential sector accounted for 41.53% of Vietnam's HVAC market share in 2025, anchored by widespread use of inverter mini-splits priced between USD 300 and USD 800 per 9,000-18,000 BTU capacity. Branded warranty programs and service availability are deciding factors for middle-class buyers, spurring manufacturers to localize assembly and expand parts depots. Nevertheless, rising electricity tariffs make entry-level buyers reluctant to replace legacy units, and low-income segments in rural areas continue to opt for fixed-speed window models. Developers of luxury apartments pre-install VRF or centralized systems to differentiate projects and command higher unit prices.

Commercial demand is forecast to outpace residential at a 7.68% CAGR through 2031. Offices are moving toward variable-air-volume boxes with CO₂ sensors and digital twins, enabling real-time energy monitoring. Data centers, benefiting from regulatory data-localization rules, require precision cooling with N+1 redundancy and are pioneering liquid-cooling deployments for AI workloads. Hospitals are adopting HEPA-filtered, positive-pressure operating suites and negative-pressure isolation rooms to meet infection-control benchmarks, thereby stimulating demand for dual-fan, variable-speed air-handling units. Retail centers favor packaged rooftop units combined with demand-response algorithms that modulate supply fans according to foot-traffic analytics. Manufacturing plants install evaporative coolers and large destratification fans to mitigate heat-stress risks, complementing spot cooling at sensitive production lines.

By Building Type (Commercial): Data Centers Set The Pace For Innovation

Office towers accounted for 34.23% of commercial HVAC installations in 2025, cementing their status as the largest user group in the Vietnam HVAC market. Grade A landlords are retrofitting chilled-beam systems and underfloor air distribution that lower static pressure and improve occupant comfort. Smart leases allocate energy savings between owners and tenants, encouraging early adoption of predictive maintenance and AI-driven controls.

Data centers are projected to log the fastest CAGR of 8.24% as global hyperscalers, domestic telecoms, and colocation providers ramp up capacity to serve Vietnam’s booming digital economy. High-density racks exceeding 10 kW require in-row cooling, rear-door heat exchangers, or direct-to-chip liquid loops capable of handling 30 kW per rack while maintaining 18-27 °C inlet temperatures and 40-60% relative humidity. The ASHRAE Vietnam Chapter’s 2025 workshop spotlighted liquid cooling’s potential to improve thermal performance by up to 3,500-fold, underscoring its relevance to next-generation facilities. Hotels, resorts, and entertainment venues continue to prioritize low-noise operations and heat recovery for domestic hot water, while healthcare projects demand 100% outdoor air and stringent pressurization controls to meet ASHRAE 170 guidelines.

Geography Analysis

Southern Vietnam, led by Ho Chi Minh City and neighboring provinces such as Binh Duong and Dong Nai, delivers the highest density of installations thanks to a year-round hot-humid climate, a deep inventory of commercial real estate, and proximity to ports that streamline equipment imports. The region’s thriving logistics parks and export-oriented manufacturing complexes also sustain demand for large air-handling units and cleanroom HVAC systems, cementing its position as the principal growth engine of the Vietnam HVAC market.

Northern Vietnam, anchored by Hanoi and Bac Ninh, Bac Giang, and Hai Phong, ranks second in market size, as government offices, electronics assembly clusters, and a growing middle class spur demand for both residential mini-splits and industrial cleanroom solutions. Northern winters create periodic heating loads, creating a niche for reversible heat-pump systems in hotels and healthcare facilities. High-tech industrial parks in Bac Ninh and Hai Phong specify ISO-class cleanrooms and precision humidity control, attracting specialized contractors capable of NEBB-certified balancing and commissioning.

The central region, notably Da Nang and Quang Nam, is emerging as a secondary growth pole supported by tourism, port upgrades, and smart-city initiatives. Da Nang’s beachfront resorts require centralized chillers and low-noise guest-room units, while the city’s designation as a smart-city pilot stimulates interest in district cooling and IoT-enabled building controls. The Mekong Delta, with Can Tho at its core, lags in penetration because of lower income levels and extensive reliance on natural ventilation; however, urban-cooling action plans and climate-resilience funding are beginning to introduce high-efficiency fans, passive shading, and affordable air-conditioners that expand the reachable Vietnam HVAC market across smaller cities.

Vietnam’s participation in ASEAN harmonization initiatives, including adoption of ISO 5151:2010 test methods for room air conditioners, is facilitating cross-border trade and enabling manufacturers to serve multiple Southeast Asian markets with standardized platforms. The elevation of ASHRAE Vietnam to Chapter status in 2025 and the establishment of technical working groups on cleanrooms, indoor air quality, and net-zero buildings signal deeper integration with international standards bodies and professional networks, catalyzing technology transfer and capacity building.

Competitive Landscape

The Vietnam HVAC market is moderately fragmented, featuring multinational equipment manufacturers, regional distributors, and local mechanical-electrical contractors. Japanese and South Korean brands Daikin, Mitsubishi Electric, LG Electronics, Panasonic, and Samsung command strong recognition in residential and light-commercial channels through localized assembly plants and dense service networks. Daikin’s VRV and Mitsubishi Electric’s City Multi platforms dominate VRF applications across offices and hotels, while LG and Samsung leverage consumer-electronics retail footprints to push Wi-Fi-enabled mini-splits into tier-two cities.

Western suppliers such as Carrier, Johnson Controls (York), and Trane Technologies focus on centralized chillers, building automation systems, and long-term operations and maintenance contracts for high-rise complexes, hospitals, and data centers. They frequently partner with Vietnamese EPC firms to navigate permitting, local content rules, and project finance structures. District-cooling pilots and large-scale mixed-use developments are creating new turf where global and local players collaborate on chilled-water infrastructure, thermal-storage integration, and performance-based service models.

Domestic companies are climbing the value chain. REE Corporation has evolved into an end-to-end cleanroom and HVAC integrator over 15 years of R&D, delivering NEBB-certified facilities for electronics and pharmaceutical clients. Intech Group’s local fabrication of terminal HEPA housings and stainless ductwork reduces costs and lead times, strengthening its competitive stance. University-industry collaborations, such as Panasonic’s 2025 donation of an HVAC Solutions Laboratory to Ho Chi Minh City University of Technology, are cultivating the next generation of engineers versed in ASHRAE, ISO, and QCVN standards, further enhancing local capacity.

Vietnam HVAC Industry Leaders

Samsung Electronics Co., Ltd.

Panasonic Holdings Corporation

Daikin Industries Ltd.

Mitsubishi Electric Corporation

LG Electronics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: LG Electronics began operating a 32,000 m² partner-run air-conditioner plant in Bekasi, Indonesia, with year-one output of 700,000 indoor and outdoor units, reinforcing regional supply for the Vietnam HVAC market.

- October 2025: Lotte Group reversed its decision to cancel the USD 2.2 billion Lotte Eco Smart City project after securing revised land-use fee terms, restarting HVAC design and procurement for 11 towers in Ho Chi Minh City.

- June 2025: ASHRAE upgraded its Vietnam Section to Chapter status, inaugurating the body in Ho Chi Minh City and broadening local access to ASHRAE standards, publications, and professional training.

- January 2025: Panasonic Air-Conditioning Vietnam transferred an HVAC Solutions Laboratory to Ho Chi Minh City University of Technology to enhance research capabilities and address the skilled-labor gap.

- November 2024: LG committed an additional USD 1 billion investment to expand production capacity in Vietnam, bolstering local availability of inverter mini-splits and VRF systems.

Vietnam HVAC Market Report Scope

HVAC systems ensure indoor comfort in residential, commercial, and industrial spaces. Heating warms interiors during cold weather using furnaces, heat pumps, and radiant systems, distributing heat evenly for comfort and safety. Ventilation exchanges indoor and outdoor air, ensuring circulation, pollutant removal, humidity control, and air quality. It uses mechanical and natural methods to introduce fresh air and prevent harmful gas buildup and moisture issues. Air conditioning cools and dehumidifies spaces during warm weather. Modern systems, including central units and ductless mini-splits, use refrigeration cycles for precise temperature control. Together, heating, ventilation, and air conditioning adapt to weather changes and occupant needs.

The study tracks the revenue accrued through the sale of HVAC product types by various players in Vietnam. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of macroeconomic factors on the market. The report's scope encompasses market sizing and forecasts for the various market segments.

The Vietnam HVAC Market Report is Segmented by Equipment Type (Air-Conditioning Equipment, Heating Equipment, and Ventilation Equipment), Installation Type (New Construction, and Retrofit and Replacement), End User (Residential, Commercial, and Industrial), and Building Type (Office Buildings, Data Centers, Hospitality and Leisure, Healthcare, Retail Stores and Malls, Educational Institutions, and Others). The Market Forecasts are Provided in Terms of Value (USD).

| Heating Equipment | Boilers and Furnaces | |

| Heat Pumps | ||

| Unitary Heaters | ||

| Ventilation Equipment | Air Handling Units (AHUs) | |

| Air Filters | ||

| Fan Coil Units | ||

| Humidifiers and Dehumidifiers | ||

| Air-Conditioning Equipment | Unitary Air Conditioners | Ducted Splits |

| Ductless Mini-Splits | ||

| Packaged Rooftops | ||

| Variable Refrigerant Flow (VRF) Systems | ||

| Room Air Conditioners | ||

| Packaged Terminal Air Conditioners | ||

| Chillers | ||

| New Construction |

| Retrofit / Replacement |

| Residential |

| Commercial |

| Industrial |

| Office Buildings |

| Healthcare Facilities |

| Hospitality and Leisure |

| Retail Stores and Malls |

| Educational Institutions |

| Data Centers |

| By Equipment Type | Heating Equipment | Boilers and Furnaces | |

| Heat Pumps | |||

| Unitary Heaters | |||

| Ventilation Equipment | Air Handling Units (AHUs) | ||

| Air Filters | |||

| Fan Coil Units | |||

| Humidifiers and Dehumidifiers | |||

| Air-Conditioning Equipment | Unitary Air Conditioners | Ducted Splits | |

| Ductless Mini-Splits | |||

| Packaged Rooftops | |||

| Variable Refrigerant Flow (VRF) Systems | |||

| Room Air Conditioners | |||

| Packaged Terminal Air Conditioners | |||

| Chillers | |||

| By Installation Type | New Construction | ||

| Retrofit / Replacement | |||

| By End User | Residential | ||

| Commercial | |||

| Industrial | |||

| By Building Type (Commercial) | Office Buildings | ||

| Healthcare Facilities | |||

| Hospitality and Leisure | |||

| Retail Stores and Malls | |||

| Educational Institutions | |||

| Data Centers | |||

Key Questions Answered in the Report

What is the current value of the Vietnam HVAC market?

The Vietnam HVAC market size reached USD 3.91 billion in 2026.

How fast is the market expected to grow over the next five years?

The market is forecast to expand at a 6.96% CAGR from 2026 to 2031.

Which equipment category dominates sales?

Air-conditioning equipment holds the largest revenue share at 45.43% and remains the fastest-growing category.

Why are data centers important to future HVAC demand?

Data centers are projected to grow at an 8.24% CAGR as cloud and AI workloads increase cooling intensity and drive adoption of precision and liquid-cooling technologies.

How do electricity tariffs affect HVAC purchasing decisions?

Recent tariff hikes raise operating costs and lengthen payback periods, prompting facility managers to favor high-efficiency, variable-speed systems yet delaying some replacement cycles amid price uncertainty.

What role do government policies play in market expansion?

Mandatory efficiency standards, energy audits, and green-building incentives under VNEEP and QCVN regulations push adoption of inverter mini-splits, VRF platforms, and advanced controls across new and existing buildings.

Page last updated on: