Veterinary Pain Management Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 1.85 Billion |

| Market Size (2031) | USD 2.46 Billion |

| Growth Rate (2026 - 2031) | 5.84% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Pain Management Market Analysis by Mordor Intelligence

The veterinary pain management market size was valued at USD 1.75 billion in 2025 and estimated to grow from USD 1.85 billion in 2026 to reach USD 2.46 billion by 2031, at a CAGR of 5.84% during the forecast period (2026-2031). Growing pet humanization, tightening livestock welfare rules, and sustained product launches underpin this trajectory. Drug-based modalities still dominate value contribution, but device therapies are moving rapidly from adjunct to mainstream status as adverse-event scrutiny pushes veterinarians toward non-pharmaceutical tools. Monoclonal antibodies, AI-enabled pain-scoring platforms, and cannabinoid candidates illustrate a pipeline that is broadening beyond legacy NSAIDs and opioids. Simultaneously, mandatory multimodal analgesia protocols in the United States and the European Union are fostering demand for combination regimens that lower opioid exposure while sustaining efficacy.

Key Report Takeaways

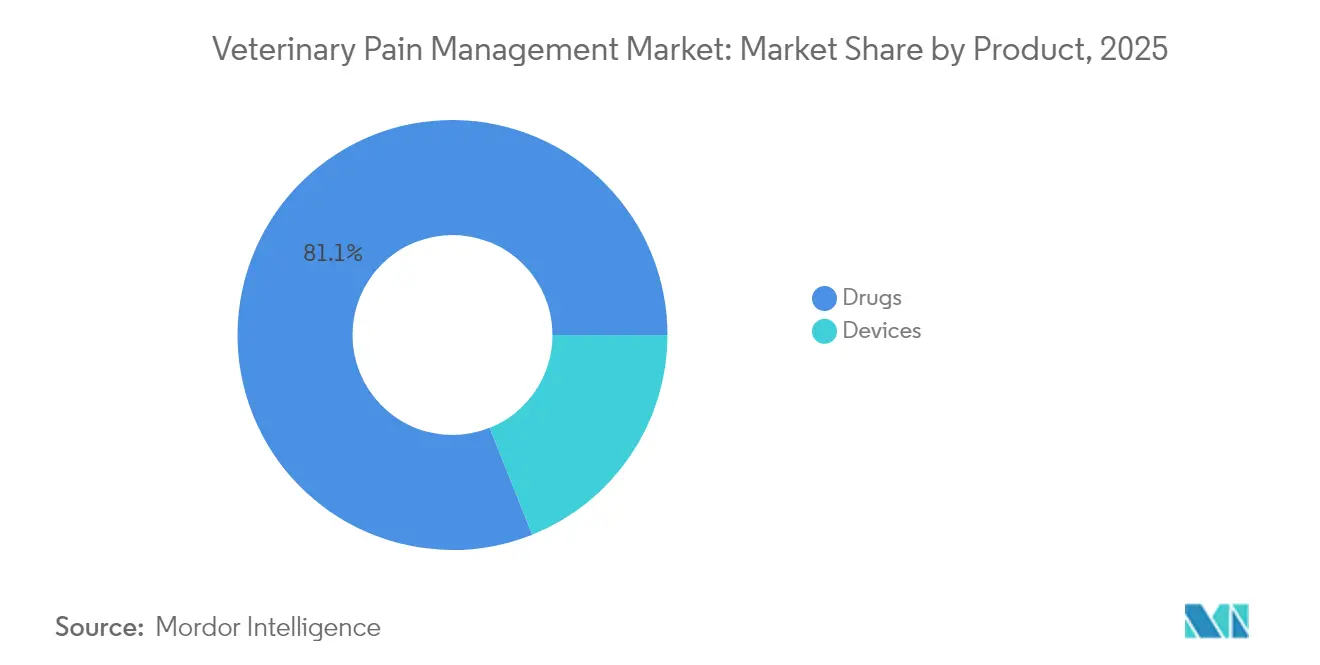

- By product category, pharmaceuticals commanded an 81.05% revenue share in 2025 while devices are projected to expand at a 6.03% CAGR through 2031, marking the fastest trajectory in the portfolio.

- By animal type, livestock retained 55.31% of the veterinary pain management market share in 2025, yet companion animal treatments are poised to grow at 6.78% CAGR to 2031 on the back of discretionary pet-care spending.

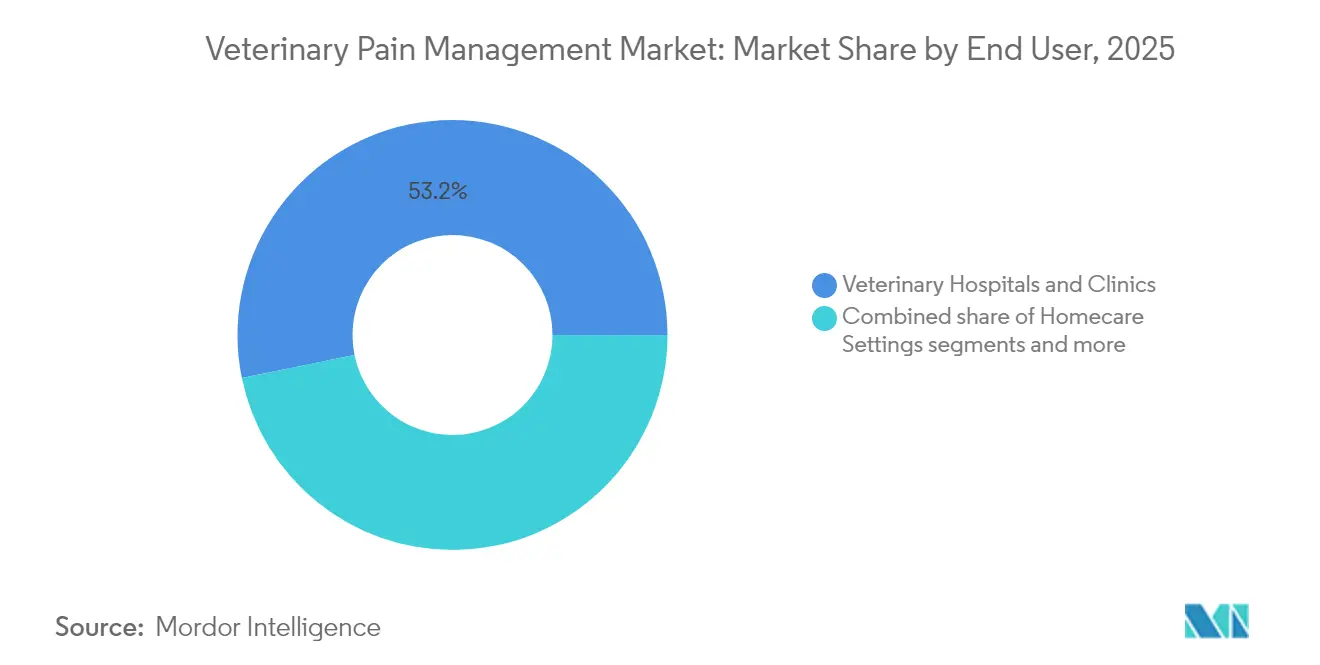

- By end user, veterinary hospitals and clinics held 53.21% of the veterinary pain management market size in 2025; home-care settings lead growth with a 6.46% CAGR thanks to telemedicine and owner-administered products.

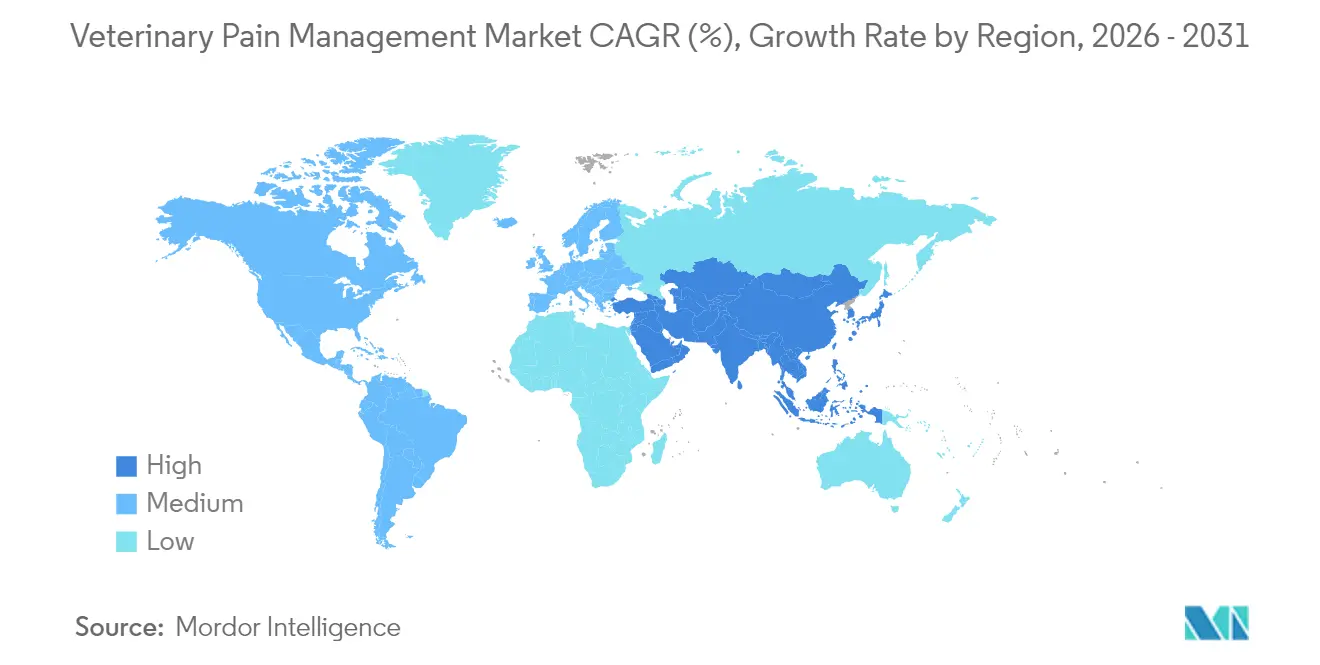

- By geography, North America accounted for 41.78% revenue in 2025, whereas Asia-Pacific is advancing at a 7.18% CAGR supported by rising incomes and evolving welfare standards.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Pain Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pet ownership & humanization | +1.2% | Global, strongest in North America & Europe | Medium term (2-4 years) |

| Growing osteoarthritis & post-operative pain incidence | +0.8% | Global, aging pet populations in developed markets | Long term (≥ 4 years) |

| Expansion of livestock welfare regulations | +0.9% | EU, North America, expanding to APAC | Short term (≤ 2 years) |

| Mandatory multimodal analgesia protocols (EU, US) | +0.7% | EU, US, with spillover to other developed markets | Medium term (2-4 years) |

| Commercialization of cannabinoid-based vet therapeutics | +0.6% | North America, selective EU markets | Long term (≥ 4 years) |

| AI-powered pain-scoring tools boosting early treatment | +0.5% | Global, led by North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Pet Ownership & Humanization

Pet owners increasingly expect human-level clinical standards, prompting premium adoption of innovations such as Zoetis’ bedinvetmab injections. The American Animal Hospital Association’s 2024 guidelines codify multimodal regimens, legitimizing antibody use alongside NSAIDs. Retailers of welfare-certified livestock products likewise seek credible analgesia claims to justify price premiums, widening overall demand.

Growing Osteoarthritis & Post-Operative Pain Incidence

Osteoarthritis affects 20% of dogs older than one year and nearly 90% of cats above 12 years. FDA approval of bedinvetmab established biologics as viable long-term solutions, with trial success rates of 43.5% versus 16.9% for placebo. Long-acting bupivacaine formulations such as Elanco’s Nocita deliver 72-hour coverage, curbing readmission rates and owner burden. Productivity losses in untreated livestock further amplify the economic argument for effective analgesia.

Expansion of Livestock Welfare Regulations

The European Union’s 2024 rules oblige analgesia during dehorning, castration, and tail docking, with fines for non-compliance. The United States Department of Agriculture increased inspection frequencies 40% since 2023, pressuring producers to adopt label-approved drugs over off-label low-cost options. Such mandates convert compliance costs into recurring revenue streams for suppliers.

Mandatory Multimodal Analgesia Protocols (EU, US)

European Medicines Agency guidance insists veterinarians justify high-dose monotherapies, nudging clinics toward combination approaches and device adjuncts. Companies possessing both drug and device assets can therefore bundle solutions, whereas single-product firms must forge partnerships or broaden their pipelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse-event profile of NSAIDs & opioids | -0.4% | Global, particularly in geriatric populations | Short term (≤ 2 years) |

| Stringent regulatory approval timelines | -0.3% | Global, most restrictive in EU & US | Long term (≥ 4 years) |

| Shortage of veterinary anesthesiologists | -0.2% | North America, expanding to other regions | Medium term (2-4 years) |

| AMR-linked scrutiny curbing NSAID usage | -0.1% | Global, led by EU regulatory initiatives | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adverse-Event Profile of NSAIDs & Opioids

Veterinarians weigh renal, hepatic, and gastrointestinal risks when prescribing NSAIDs, and diversion concerns complicate opioid dispensing. Post-marketing surveillance of bedinvetmab documented 17,162 adverse reports from 18 million doses, reminding clinicians that even innovative biologics carry safety obligations. FDA approval of suzetrigine for human use underscores momentum toward non-opioid classes that may cross into veterinary care.

Stringent Regulatory Approval Timelines

Average review cycles exceed five years, and combination products require parallel device and drug dossiers, lifting costs above USD 10 million. VICH streamlining efforts have yielded uneven national adoption, compelling companies to fund multiple submissions or delay market entry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Devices Gain Ground Despite Drug Dominance

The pharmaceutical segment captured 81.05% of the veterinary pain management market size in 2025, anchored by NSAIDs such as meloxicam, yet device revenues are growing at a 6.03% CAGR. NSAIDs persist as first-line therapy because of cost efficiency, whereas opioid use retreats under diversion scrutiny. Long-acting local anesthetics like Nocita extend analgesia to 72 hours and mitigate readmission. Alpha-2 agonists retain niche roles in large animal sedation. Early cannabinoid entrants address chronic pain that resists conventional classes, despite regulatory headwinds.

Portable diode-laser units, PEMF mats, and shockwave systems are carving out space as stand-alone or adjunct solutions. Clinics promote these technologies for geriatric pets intolerant of NSAIDs, while equine practitioners leverage PEMF for musculoskeletal recovery. Manufacturers now bundle software analytics that log session parameters, enabling veterinarians to document compliance with multimodal mandates. The device trajectory signals that the veterinary pain management market will increasingly balance pharmacology with non-pharmacologic modalities.

By Animal Type: Companion Animals Drive Future Growth

Livestock held 55.31% of the veterinary pain management market share in 2025, reflecting mandatory compliance across large herds. Nevertheless, the companion segment is projected to expand at 6.78% CAGR, lifted by a global pet economy valued at USD 261 billion. Livestock buyers emphasize cost-per-head and withdrawal periods, favoring proven molecules in bulk packaging. Conversely, dog and cat owners fund antibody injections and laser packages that prioritize quality of life over minimum viable care.

Breakthrough NGF-targeting antibodies Librela and Solensia showcase pet-owner willingness to pay USD 75–115 monthly, pushing lifetime value per patient higher than typical NSAID regimes. Livestock producers are integrating automated dosing units to comply with welfare audits without inflating labor costs, indicating an efficiency-driven adoption model separate from the emotionally motivated companion sector.

By End User: Homecare Settings Emerge as Growth Driver

Hospitals and clinics accounted for 53.21% of revenue in 2025, yet homecare channels are accelerating at a 6.46% CAGR. Teleconsult platforms permit real-time video triage, and courier services deliver refill packs within hours. Transdermal buprenorphine (ZORBIUM) and chewable NSAIDs create regimens owners can administer without clinic visits. Monitoring apps link wearable activity trackers to veterinarian dashboards, flagging deviations that may indicate breakthrough pain. For chronic conditions, subscription models bundle monthly antibody injections, AI-powered pain-scoring assessments, and periodic telecheckups. Clinics retain a supervisory role but shift toward consultancy rather than direct administration, realigning revenue from procedure fees to service packages.

Academic and research institutes, while modest in revenue, furnish critical validation for new modalities. Universities refine feline grimace scales via machine learning and map cannabinoid pharmacokinetics in species-specific studies. Collaborative grants between universities and manufacturers fast-track concept-to-clinic timelines, reducing commercial risk.

Geography Analysis

North America contributed 41.78% of global revenue in 2025, underpinned by high pet insurance penetration and a regulatory climate that enables rapid first-to-market approvals. Monoclonal antibody pioneers capitalized on FDA review efficiencies, securing early brand recognition. Canada’s cautious stance on controlled substances has, however, catalyzed investment in non-opioid drugs and cannabinoid research pipelines.

Europe follows closely, shaped by some of the world’s strictest welfare legislation. Mandatory multimodal analgesia elevates demand for diverse product kits, pushing suppliers to hold broader formularies. Antimicrobial stewardship programs restrain NSAID courses, indirectly prompting uptake of laser and electromagnetic therapy devices. The United Kingdom’s post-Brexit regulatory autonomy is allowing accelerated pathways for niche products, giving smaller firms an entry door ahead of pan-EU approvals.

Asia-Pacific is the fastest-expanding region with a projected 7.18% CAGR. Urban pet ownership in China rose sharply after pandemic-era lifestyle shifts, while Japan’s aging pet cohort parallels that of Western markets. South Korea’s reform of its Animal Protection Act stipulates pain relief during cosmetic surgery and disease treatment, creating new baseline demand. Emerging Southeast Asian economies deploy welfare upgrades to align with export certification criteria, translating policy into accessible market volume for globally established brands.

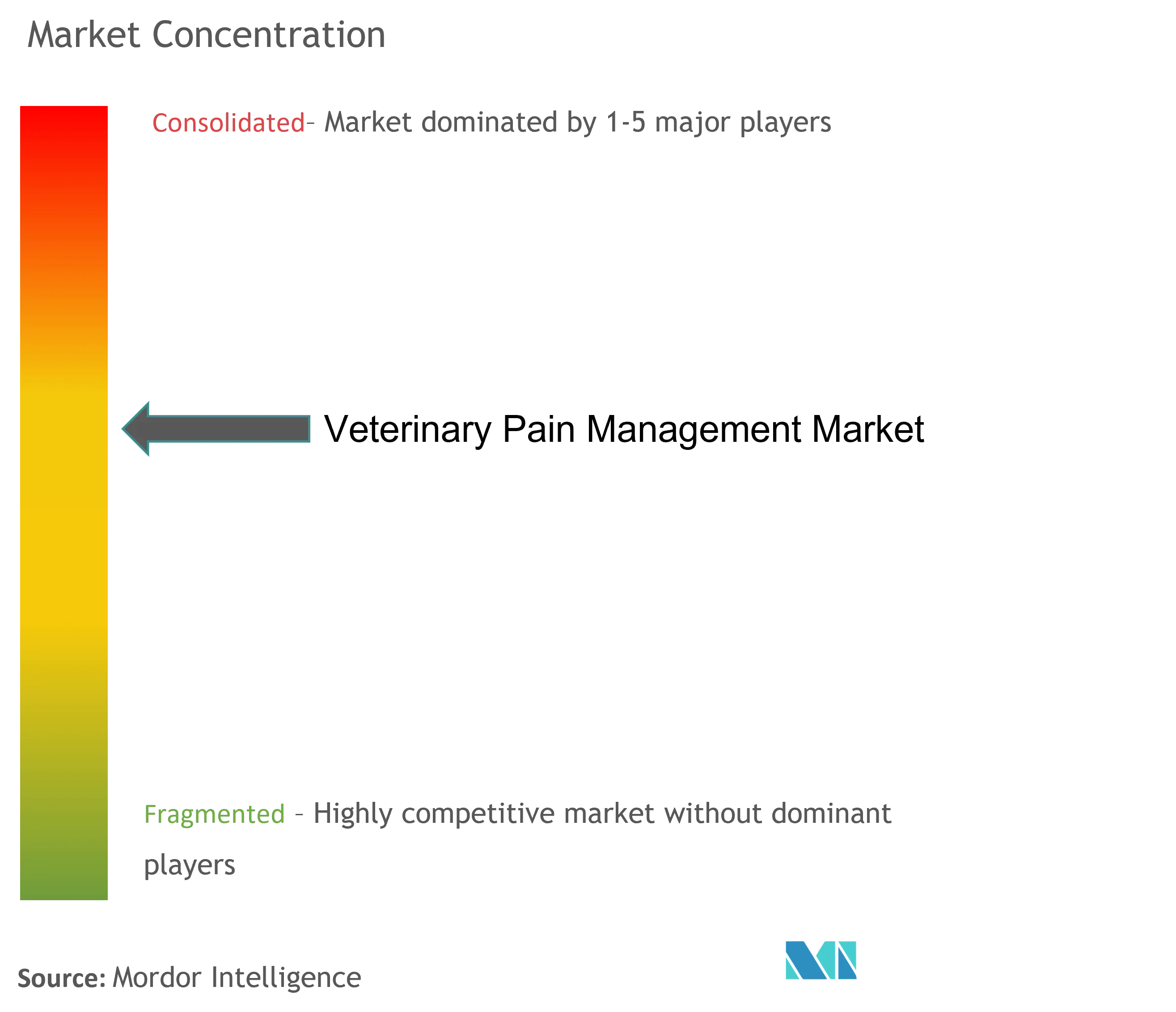

Competitive Landscape

The veterinary pain management market hosts a moderately fragmented set of players. Zoetis, Boehringer Ingelheim, and Elanco command significant prescription volume through wide distribution footprints and robust in-house R&D, yet device specialists such as LiteCure and PulseVet Technologies carve defensible niches in non-pharmacologic therapy. Consolidation pressures are rising; acquisitions like Boehringer Ingelheim’s 2024 purchase of Saiba Animal Health illustrate intent to diversify beyond small-molecule franchises.

Technology convergence is a distinguishing factor. Zoetis links antibody treatments with AI diagnostics that triage cases eligible for biologics, thereby maximizing uptake. Device makers embed Bluetooth connectivity, enabling clinics to track at-home session compliance and justify package renewals. Biotechnology startups pioneering veterinary cannabinoids find licensing agreements with larger incumbents attractive to offset regulatory cost hurdles.

Price competition persists among generic NSAID suppliers, but innovation is gravitating toward differentiated modalities that support premium positioning. Manufacturers also develop veterinary-specific delivery formats—long-acting injectables, single-dose otic suspensions, and extended-release chewables—that simplify compliance and add value beyond active ingredient parity. Collectively, these strategic pivots position the veterinary pain management market for sustained product life-cycle innovation.

Veterinary Pain Management Industry Leaders

Ceva Sante Animale

Elanco Animal Health Incorporated

Zoetis Inc.

Vetoquinol SA

Boehringer Ingelheim International Gmbh

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2022: Zoetis launched Solensia to manage feline osteoarthritis pain in the United States.

- July 2024: Clinical validation of AI-powered feline pain assessment technology achieved breakthrough with CatsMe! application demonstrating over 95% accuracy in pain state identification, downloaded by over 200,000 users globally for owner-based monitoring

Global Veterinary Pain Management Market Report Scope

Veterinary pain management refers to a medical approach toward the prevention, diagnosis, and treatment of pain caused by several factors, such as physical trauma, internal organ problems, surgical procedures, brain and spine problems, slipped discs, arthritis, and joint damage.

The veterinary pain management market is segmented by product (drugs and devices), application (osteoarthritis and joint pain, postoperative pain, cancer, and other applications), animal type (companion and livestock), end user (hospitals and clinics, retail outlets, and other end users), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 different countries. The report offers the value (in USD million) for the above segments.

| Drugs | NSAIDs |

| Opioids | |

| Local Anesthetics | |

| Alpha-2 Agonists | |

| Cannabinoid-based Therapeutics | |

| Devices | Laser Therapy |

| Electromagnetic Therapy |

| Companion Animals |

| Livestock |

| Veterinary Hospitals & Clinics |

| Homecare Settings |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product (Value) | Drugs | NSAIDs |

| Opioids | ||

| Local Anesthetics | ||

| Alpha-2 Agonists | ||

| Cannabinoid-based Therapeutics | ||

| Devices | Laser Therapy | |

| Electromagnetic Therapy | ||

| By Animal Type (Value) | Companion Animals | |

| Livestock | ||

| By End User (Value) | Veterinary Hospitals & Clinics | |

| Homecare Settings | ||

| Academic & Research Institutes | ||

| By Region (Value) | North America | United States |

| Canada | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global veterinary pain management market in 2026?

The market is valued at USD 1.85 billion in 2026 and is projected to reach USD 2.46 billion by 2031 at a 5.84% CAGR.

Which treatment category is expanding fastest?

Device-based therapies, including laser and PEMF systems, are expected to grow at 6.03% CAGR through 2031 as clinics seek non-pharmaceutical options.

What regional market is growing most quickly?

Asia-Pacific leads in growth with a 7.18% CAGR, supported by rising incomes and evolving animal welfare mandates.

How are regulatory changes affecting product demand?

EU and US multimodal analgesia protocols create obligatory demand for bundled solutions while stricter welfare laws in livestock farming increase baseline analgesic usage.

Which companies dominate new product launches?

Zoetis, Boehringer Ingelheim, Elanco, Merck Animal Health, and Dechra are introducing monoclonal antibodies, AI diagnostics, long-acting injectables, and antibiotic-free therapies.

What alternatives are emerging to NSAIDs and opioids?

Monoclonal antibodies, cannabinoids in development, long-acting local anesthetics, and device-based modalities deliver pain control with reduced systemic risk profiles.

Page last updated on: