Animal Ortho-Prosthetics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

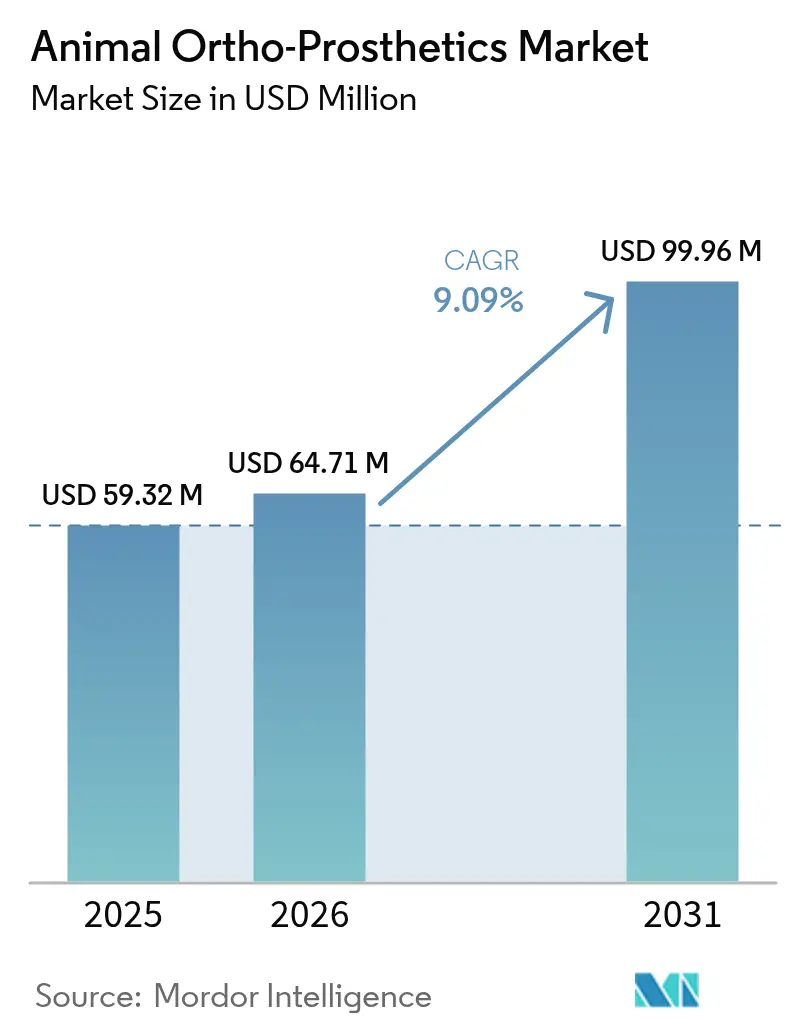

| Market Size (2026) | USD 64.71 Million |

| Market Size (2031) | USD 99.96 Million |

| Growth Rate (2026 - 2031) | 9.09% CAGR |

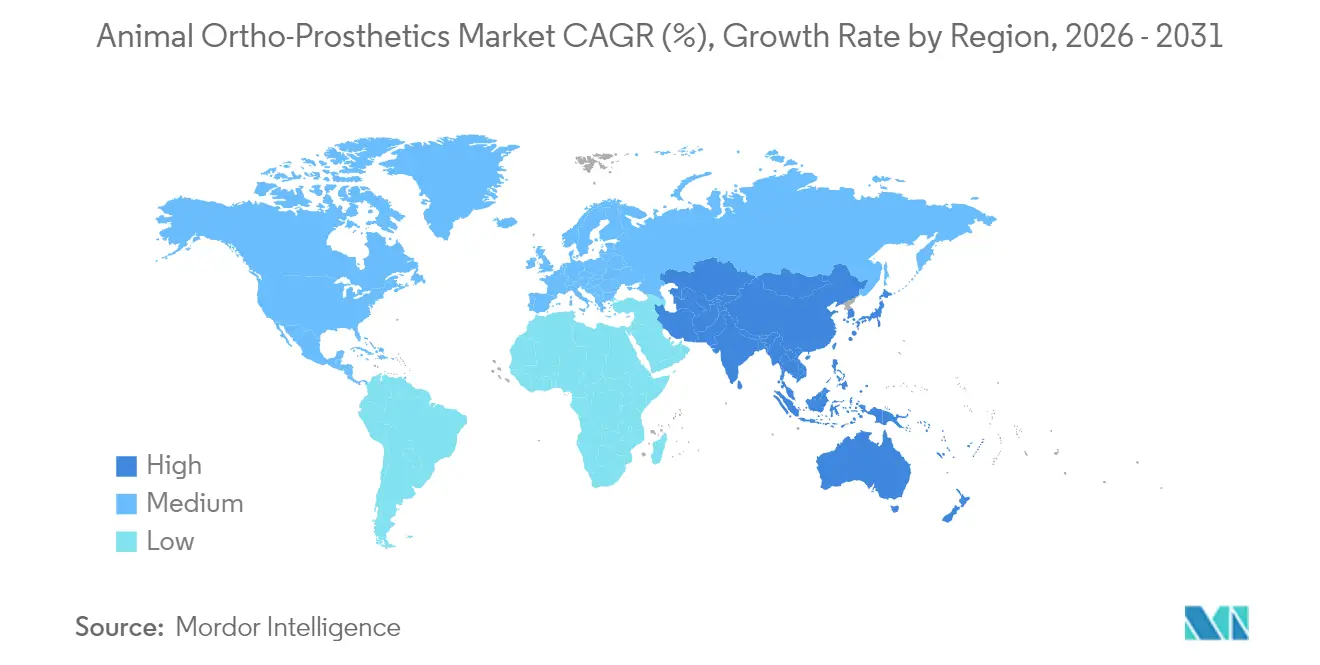

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Animal Ortho-Prosthetics Market Analysis by Mordor Intelligence

The animal ortho-prosthetics market size is expected to grow from USD 59.32 million in 2025 to USD 64.71 million in 2026 and is forecast to reach USD 99.96 million by 2031 at 9.09% CAGR over 2026-2031. Demand for custom limbs, braces, and mobility carts is rising as pet owners look beyond amputation toward solutions that preserve activity and comfort. Three trends sustain the expansion: widespread pet humanization, rapid gains in 3-D printing that shorten production cycles, and evolving clinical guidelines that promote limb-sparing care over surgical removal. Competition remains fragmented because every patient requires a made-to-order device, yet scale advantages flow to firms that blend veterinary partnerships with digital design workflows. Emerging markets add a second growth engine; local clinics prefer lower-cost conventional fabrication, so both advanced and traditional technologies grow in parallel.

Key Report Takeaways

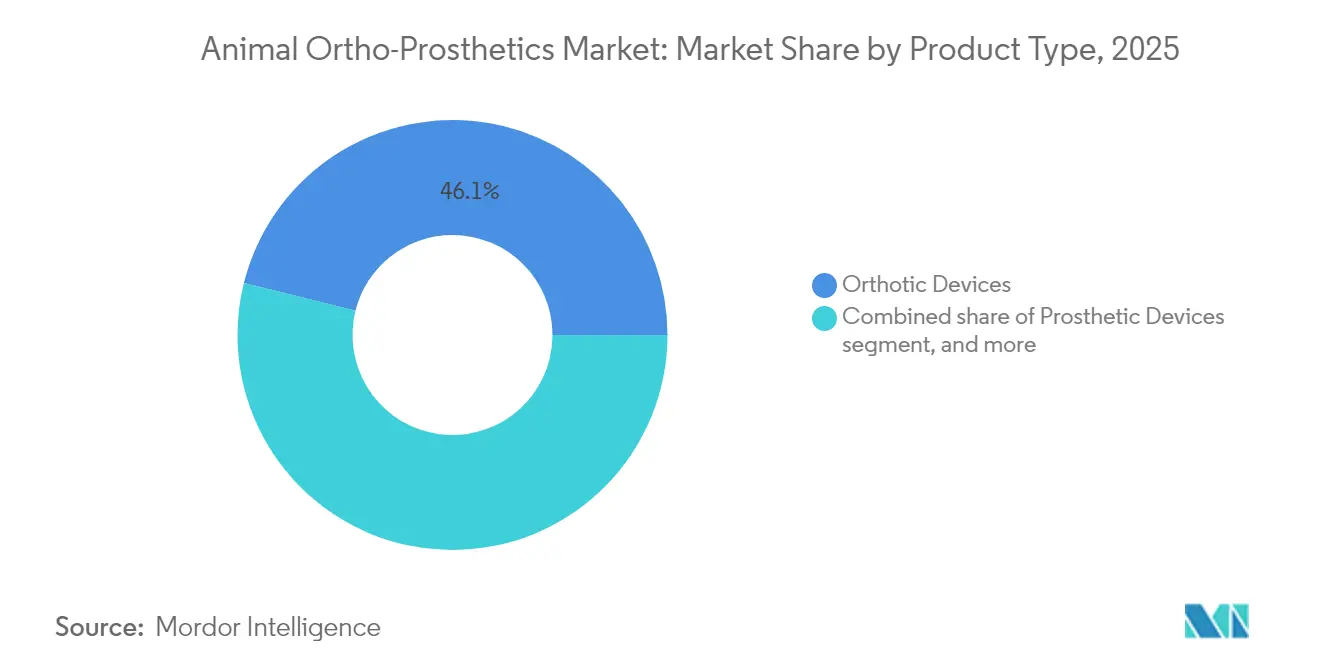

- By product type, orthotic devices held 46.12% of animal ortho-prosthetics market share in 2025 while mobility aids are projected to advance at an 11.52% CAGR through 2031.

- By technology, 3-D printing captured 57.94% share of the animal ortho-prosthetics market in 2025, whereas conventional manufacturing is forecast to post a 11.88% CAGR to 2031.

- By animal type, canine cases accounted for 67.63% of the animal ortho-prosthetics market size in 2025, and the equine segment is set to grow at a 12.06% CAGR to 2031.

- By end user, veterinary hospitals and clinics controlled 58.98% share in 2025, while rehabilitation centers are on track for a 12.69% CAGR to 2031.

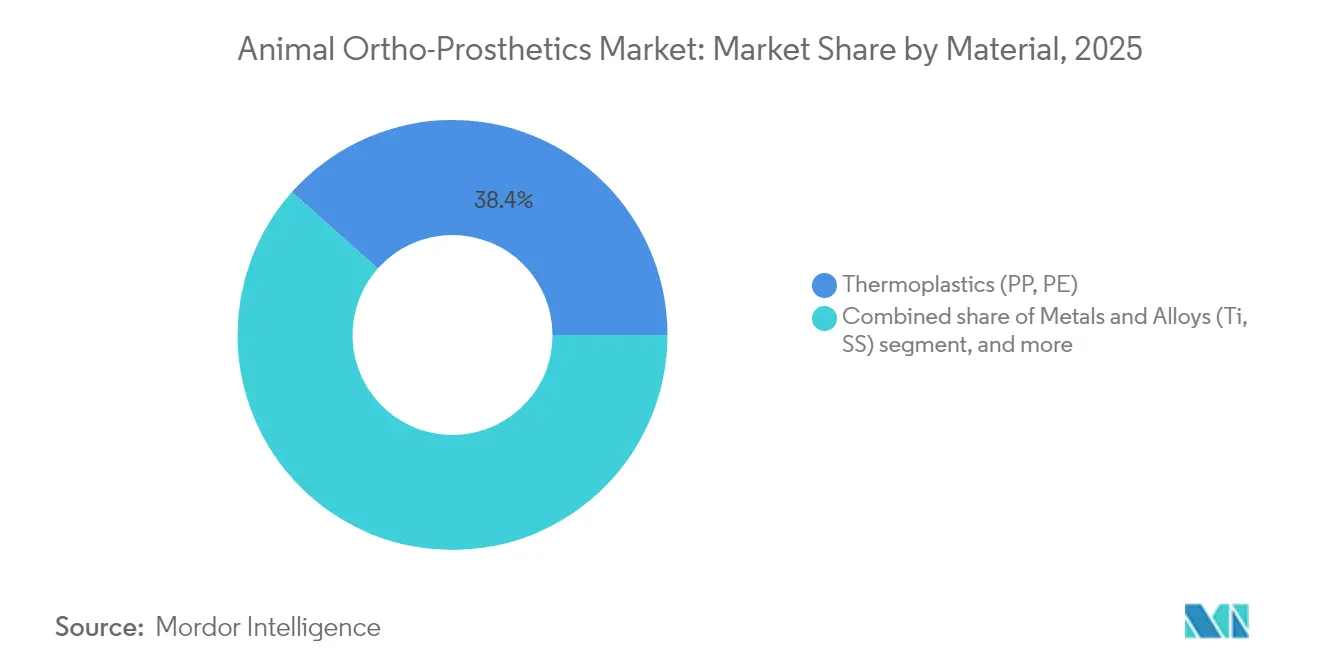

- By material, thermoplastics commanded 38.42% share in 2025, and metals and alloys will register an 11.78% CAGR during the forecast window.

- By geography, North America led with 41.95% revenue share in 2025; Asia-Pacific shows the fastest expansion at a 10.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Animal Ortho-Prosthetics Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global pet expenditure | +2.8% | North America, Europe, key urban centers in Asia-Pacific | Medium term (2-4 years) |

| Technological innovations in veterinary orthopedics | +2.1% | North America and European Union leading; adoption accelerating in Asia-Pacific | Long term (≥4 years) |

| Increasing prevalence of animal musculoskeletal disorders | +1.6% | Mature pet economies with aging populations | Medium term (2-4 years) |

| Expanding veterinary care infrastructure and insurance penetration | +1.4% | Asia-Pacific core, spill-over to Middle East & Africa and Latin America | Long term (≥4 years) |

| Growing awareness of animal mobility solutions | +0.9% | Global, strongest in large urban markets | Short term (≤2 years) |

| Adoption of tele-rehabilitation and remote fitting platforms | +0.5% | North America, Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Pet Expenditure

Pet spending continues to swell as millennial and Gen Z owners treat animals as family members; surveys show U.S. outlays could move from USD 121 billion in 2023 to USD 279 billion by 2030[1]American Pet Products Association, “Pet Industry Expenditure Dashboard,” americanpetproducts.org. The budget shift makes prosthetic costs between USD 1,000 and USD 2,000 tolerable, positioning devices as essential healthcare, not luxuries. Demand proves resilient during downturns because owners rarely cut pet health expenses first. Premium brands therefore focus on quality-of-life outcomes rather than price, reinforcing value perceptions. Insurers are slowly broadening coverage, which further cushions household budgets and widens adoption.

Technological Innovations in Veterinary Orthopedics

Titanium and carbon-fiber parts produced on high-resolution 3-D printers now replicate precise limb geometry, promoting bone integration and weight savings. Hospital networks such as VCA opened dedicated additive labs in 2024, trimming fabrication lead times from several weeks to a few days. Computer-aided modeling lets engineers balance strength and flexibility, reducing stress shielding that once triggered revision surgery. As scanning, software, and printing operate on one digital thread, clinics can iterate designs quickly and deliver superior fit, a clear edge over manual plaster casting.

Increasing Prevalence of Animal Musculoskeletal Disorders

Longer life expectancy means more pets present with osteoarthritis, cruciate tears, and congenital deformities that once ended active lifestyles. In 2024, 95% of veterinarians surveyed called for standardized canine osteoarthritis protocols. Studies also note that 91.66% of prosthetic recipients regain the ability to stand, and 87.5% resume walking after device acclimatization[2]Veterinary Evidence, “Systematic Review: Outcomes of Prosthetic Use in Small Animals,” veterinaryevidence.org. With outcomes documented, clinicians now recommend limb-sparing treatments earlier, generating predictable demand for off-the-shelf braces and bespoke implants.

Expanding Veterinary Infrastructure and Insurance Penetration

Asia-Pacific governments are investing in modern clinics, imaging suites, and postgraduate training that bring advanced orthopedic care closer to pet owners[3]RAPS, “Asia-Pacific Veterinary Device Regulations,” raps.org. Parallel growth in pet insurance, especially in China and South Korea, lowers out-of-pocket hurdles. Tele-consultation platforms allow specialists in urban centers to guide fittings in rural regions, boosting reach without heavy capital outlay. Harmonization of device approval pathways, although incomplete, signals future regulatory clarity that should unlock cross-border scale economies.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of custom prosthetic solutions | -1.8% | Global, particularly acute in emerging economies | Medium term (2-4 years) |

| Limited skilled workforce in veterinary orthopedics | -1.2% | Global shortage, most severe in rural and developing regions | Long term (≥4 years) |

| Lack of standardized regulatory framework | -0.9% | Fragmented across Asia-Pacific, Latin America, and parts of Europe | Long term (≥4 years) |

| Limited market penetration in emerging economies | -0.7% | Asia-Pacific tier-2 cities, Middle East & Africa, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Custom Prosthetic Solutions

A full limb device from market leader OrthoPets ranges from USD 1,265 to USD 2,125 before clinic fees double the bill. Limited production batches and premium materials block economies of scale and keep price elasticities high. Insurers often cap payouts or exclude mobility aids, leaving owners to carry residual costs. When ongoing adjustments, padding replacements, and refurbishment are factored in, lifetime expenses climb further, dampening demand outside affluent households.

Limited Skilled Workforce in Veterinary Orthopedics

Specialists need training that blends anatomical insight with material science and digital design, yet only a few universities offer integrated programs. A regional workforce study highlighted a shortfall of more than 1,000 veterinarians in New England alone by 2024, with orthopedics among the scarcest disciplines. Without fitters, cases in secondary cities wait or travel long distances, lengthening lead times and hurting outcomes. Skills shortages also limit manufacturer expansion because every clinic partnership hinges on practitioner confidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mobility Solutions Gain Speed

Orthotic braces generated the largest revenue in 2024, yet carts and wheelchairs deliver the highest forecast growth. Orthotics appeal because they avoid surgery, offering immediate stability for ligament injuries. However, complete limb loss cases now receive custom carts that restore gait with minimal rehabilitation time. The animal ortho-prosthetics market size for mobility aids is projected to reach USD 27.33 million by 2031, a 6-year jump underpinned by lightweight aluminum frames and quick-release harness systems. Orthotics remain indispensable for partial weight bearing, but manufacturers are bundling braces with wheels and ramps, selling integrated mobility kits rather than single parts. This bundling strategy unlocks cross-sell revenue and strengthens clinic relationships.

Prosthetic limbs occupy a smaller volume niche yet command higher unit prices because of titanium pylons, silicone liners, and detailed finishing. Accessory lines—replacement straps, paw covers, and joint locks—are gaining recognition as recurring revenue streams. Clinics often sign annual supply contracts to ensure patients receive timely consumables, anchoring aftermarket sales. Providers that master both durable goods and consumables diversify risk and build loyalty in the animal ortho-prosthetics market.

By Animal Type: Equine Potential Accelerates

Companion dogs dominate procedure counts as owners prioritize pets’ welfare, but working horses generate rising traction. The animal ortho-prosthetics market share for canine applications was 67.63% in 2025, yet targeted programs for sport and police horses are forecast to post a 12.06% CAGR. Gait analysis tools such as inertial sensors now objectify lameness metrics, letting farriers and veterinarians decide when a brace can defer euthanasia. Breeding operations see direct financial returns when a high-value stallion resumes service sooner, supporting premium price points.

Cats index lower because device acceptance is hindered by grooming behavior and stature. Exotic mammals and livestock remain marginal but strategic; zoos and dairies commission high-margin one-off builds when an animal has significant conservation or economic value. These cases spark media coverage that lifts public perception of the animal ortho-prosthetics market and indirectly boosts adoption among mainstream pet owners.

By End User: Rehabilitation Centers Scale Up

Hospitals and clinics are primary distributors because they diagnose injuries and conduct surgery when required. In 2025 these facilities processed 58.98% of orders and acted as formal payers for some insured cases. Rehabilitation centers, often operated by physiotherapists with canine hydrotherapy pools, are expanding networks quickly; their 12.69% CAGR reflects strong owner demand for post-operative exercise and device tuning. The animal ortho-prosthetics market size recorded from this channel is set to double by 2030 as centers integrate treadmills, laser therapy, and online coaching.

Home-based usage lags because fittings must account for muscle atrophy and stump swelling that change weekly. Tele-rehabilitation apps partly bridge gaps by guiding owners through video sessions and alerting clinics when symmetry or pressure metrics deviate. Companies now ship adjustment kits with extra liners, wrenches, and adhesive pads so minor tweaks happen on site, easing the support burden on busy clinics.

By Material: High-Performance Alloys Gain Momentum

Thermoplastics remain cost-effective for braces that need periodic heating and shaping. Yet weight-bearing implants increasingly rely on Ti-Nb-Zr alloys that align modulus with cortical bone, cutting implant loosening risk. Metals and alloys show an 11.78% CAGR, the fastest within materials, as practitioners trust corrosion resistance for long-term service. Carbon-fiber shells shield hardware and distribute load while preserving agility; these shells extend brace life and permit color personalization, an underrated factor in owner satisfaction. Antimicrobial nanosilver coatings debut in 2025 product lines, answering infection concerns stated by clinicians.

Silicone interfaces reduce chafing at socket edges, improving compliance. Suppliers partner with chemical companies to co-develop medical-grade elastomers that endure outdoor conditions. Collectively, diversified materials broaden indications and support device crossover from orthotics into prosthetics, deepening penetration of the animal ortho-prosthetics market.

By Technology: Dual Paths to Scale

Additive manufacturing captured 57.94% of revenue in 2025 by delivering near-perfect anatomical fit. Yet conventional milling, vacuum forming, and hand lamination still win orders in cost-sensitive settings, climbing at 11.88% CAGR. Clinics in India and Brazil favor polypropylene sheets thermo-formed over casts because printers and titanium powder are scarce. Hybrid workflows emerge: a limb is scanned digitally, but the mold is milled from polyurethane foam and finished manually to save on metal powder. The animal ortho-prosthetics market benefits when both methods coexist, giving providers pricing flexibility. Regulatory milestones—such as China’s 2025 approval of a laser-printed knee—signal broader acceptance and should normalize additive implants in animals next.

Geography Analysis

North America leads the animal ortho-prosthetics market with a 41.95% share because owners allocate premium budgets, insurers reimburse partial costs, and device makers cluster around academic veterinary hubs. The region shows steady single-digit unit growth while mix shifts toward high ticket prosthetics. Clinics in Colorado, Texas, and Ontario pioneer osseointegrated fixation, positioning the continent for early adoption of load-bearing implant lines. Regulatory guidance from the U.S. Food and Drug Administration on veterinary devices reduces ambiguity and keeps compliance costs manageable.

Asia-Pacific records the highest forecast CAGR at 10.18% as urban households acquire pedigree pets and treat them as family. China’s acceptance of a 3-D printed knee in 2025 demonstrates state endorsement of advanced orthopedics. However, inter-regional disparity persists: tier-one cities host specialist hospitals, while provincial clinics lack imaging and fabrication labs. Government investment and insurer entry should narrow gaps, though pricing must align with middle-income affordability. Conventional fabrication remains dominant today, creating scope for local manufacturing hubs that leverage lower labor costs.

Europe ranks third in value terms and enjoys harmonized product standards under CE marking. Universities in Germany, the Netherlands, and the United Kingdom perform biomechanics research that feeds into design enhancements, while small enterprises craft bespoke solutions for equine sports medicine. The Middle East and Africa plus South America form a long-tail opportunity curve. Affluent Gulf households import devices, but broader uptake waits for wider veterinary coverage. In Brazil, rehabilitation chains add hydrotherapy pools, indicating momentum despite economic volatility. Across these regions, distributors that bundle fitting, after-care, and remote support win contracts because clinics seek turnkey offerings.

Competitive Landscape

The animal ortho-prosthetics market remains moderately concentrated, with no single vendor exceeding a 15% revenue share. OrthoPets, Bionic Pets, and several regional specialists anchor the field, each focusing on specific species or device classes. Money flows into vertical integration: OrthoPets operates scanning, design, production, and after-care under one roof, shortening cycle times and locking in clinical referrals. Bionic Pets invests heavily in social media storytelling, turning successful recoveries into viral marketing that widens consumer pull.

Digital tooling constitutes a sharp competitive wedge. Companies that own cloud-based design software let clinics upload scans, approve renderings in hours, and receive shipments in under one week. Those without such systems face churn as veterinarians favor faster partners. Materials know-how is the second wedge: suppliers with proprietary titanium or composite blends achieve lighter builds that can justify 20% price premiums and command loyalty among athletic dog owners.

Strategic moves signal impending consolidation. Orthopedic groups serving humans, such as OrthoPediatrics, bought brace specialists in 2024, hinting at cross-species synergies in supply chains and R&D. Venture funds allocated USD 35 million to pet health in 2024, targeting niche disruptors developing tele-rehab platforms and AI-based gait analysis. As investment scales up, smaller craftsman outfits may partner or sell to broaden distribution. Still, regulatory diversity and custom fabrication complexity will likely keep the animal ortho-prosthetics industry moderately fragmented over the next decade.

Animal Ortho-Prosthetics Industry Leaders

OrthoPets LLC

Animal OrthoCare

Bionic Pets

Walkin’ Pets By HandicappedPets

Össur Veterinary

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Naton Biotechnology secured Chinese approval for the first laser 3-D printed total knee, paving a pathway for load-bearing implants in animals.

- February 2025: American Regent Animal Health released a clinical guide to standardize canine osteoarthritis management, indirectly supporting earlier brace adoption.

- July 2024: Ani.VC launched a USD 35 million pet health fund targeting mobility innovation.

- August 2024: ELIAS Animal Health began a limb-sparing osteosarcoma trial combining surgery with adoptive T-cell therapy.

- February 2024: VCA Animal Hospitals opened a 3-D printing lab to create custom surgical guides and implants for pets

- January 2024: OrthoPediatrics acquired Boston Orthotics & Prosthetics, underscoring consolidation momentum across orthopedic device lines.

Global Animal Ortho-Prosthetics Market Report Scope

As per the scope of the report, the animal ortho-prosthetics products are associated with orthopedic devices designed to assist injured animals, to provide position, immobilize, align, support, prevent deformity, improve functioning, and are coupled with prosthetic devices for compensating for the missing leg segment. The Animal Ortho-Prosthetics Market is Segmented by Product Type (Braces, Prosthetics, and Other Product Types), End-User (Veterinary Hospitals and Clinics, and Rehabilitation Centers), and Geography (North America, Europe, Asia-Pacific, Rest of the World). The report offers the value (in USD million) for the above segments.

| Orthotic Devices |

| Prosthetic Devices |

| Mobility Aids (Carts, Wheel-chairs) |

| Components & Accessories |

| Canine |

| Feline |

| Equine |

| Other Animal Types |

| Veterinary Hospitals & Clinics |

| Rehabilitation & Physiotherapy Centers |

| Home-Care (Pet Owners) |

| Thermoplastics (PP, PE) |

| Metals & Alloys (Ti, SS) |

| Carbon-Fiber Composites |

| Silicone & Others |

| 3-D Printing / Additive Manufacturing |

| Conventional Manufacturing |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Orthotic Devices | |

| Prosthetic Devices | ||

| Mobility Aids (Carts, Wheel-chairs) | ||

| Components & Accessories | ||

| By Animal Type | Canine | |

| Feline | ||

| Equine | ||

| Other Animal Types | ||

| By End-User | Veterinary Hospitals & Clinics | |

| Rehabilitation & Physiotherapy Centers | ||

| Home-Care (Pet Owners) | ||

| By Material | Thermoplastics (PP, PE) | |

| Metals & Alloys (Ti, SS) | ||

| Carbon-Fiber Composites | ||

| Silicone & Others | ||

| By Technology | 3-D Printing / Additive Manufacturing | |

| Conventional Manufacturing | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the animal ortho-prosthetics market in 2026?

The animal ortho-prosthetics market size is USD 64.71 million in 2026.

What is the projected growth rate for the market?

Revenue is forecast to rise at a 9.09% CAGR over 2026-2031, hitting USD 99.96 million by 2031.

Which product segment is growing fastest?

Mobility carts and wheelchairs are expected to expand at an 11.52% CAGR through 2031.

Why is Asia-Pacific the fastest-growing region?

Rapid urban pet ownership, new veterinary hospitals, and supportive regulators push regional demand at a 10.18% CAGR.

Who are the key market players?

Specialists such as OrthoPets, Bionic Pets, and several regional manufacturers lead through custom design, advanced materials, and clinic partnerships.

What limits wider adoption of animal prosthetics?

High customization costs and shortages of skilled veterinary orthopedists remain the main barriers despite growing owner interest.

Page last updated on: