Veterinary Emergency Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 22.17 Billion |

| Market Size (2031) | USD 29.67 Billion |

| Growth Rate (2026 - 2031) | 5.99% CAGR |

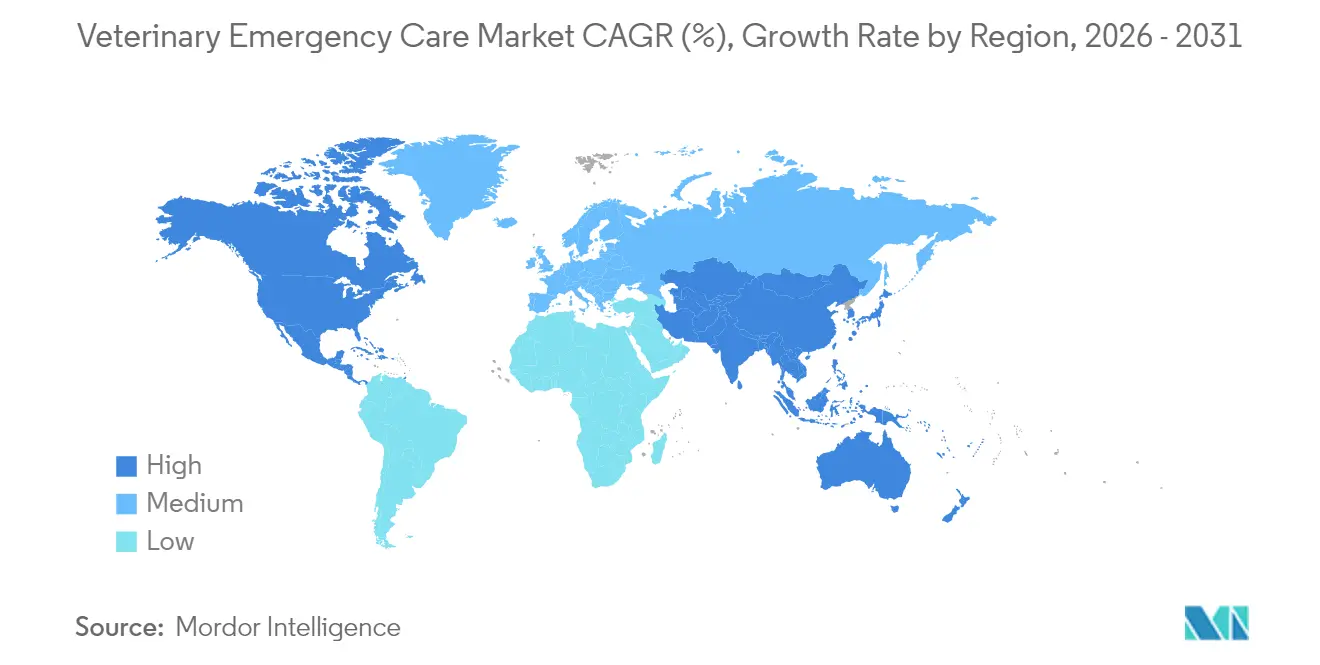

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

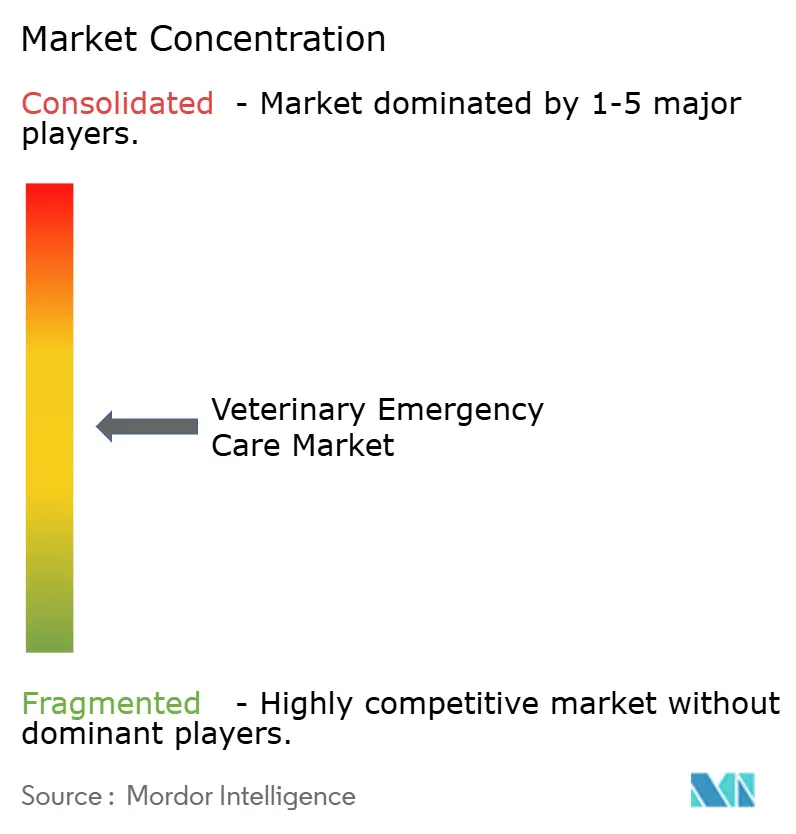

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Emergency Care Market Analysis by Mordor Intelligence

The veterinary emergency care market size in 2026 is estimated at USD 22.17 billion, growing from 2025 value of USD 20.92 billion with 2031 projections showing USD 29.67 billion, growing at 5.99% CAGR over 2026-2031. Robust household pet ownership, greater insurance coverage, and rapid technology adoption are widening access to critical interventions. North America remains the largest revenue contributor, while Asia-Pacific records the fastest unit growth as disposable incomes climb and specialty clinics multiply. Private equity consolidation accelerates as corporate chains buy independent hospitals, and AI-enabled diagnostics shorten triage times, improving clinical outcomes. Workforce shortages persist, spurring mobile units and telehealth to fill appointment gaps and keep the veterinary emergency care market expanding.

Key Report Takeaways

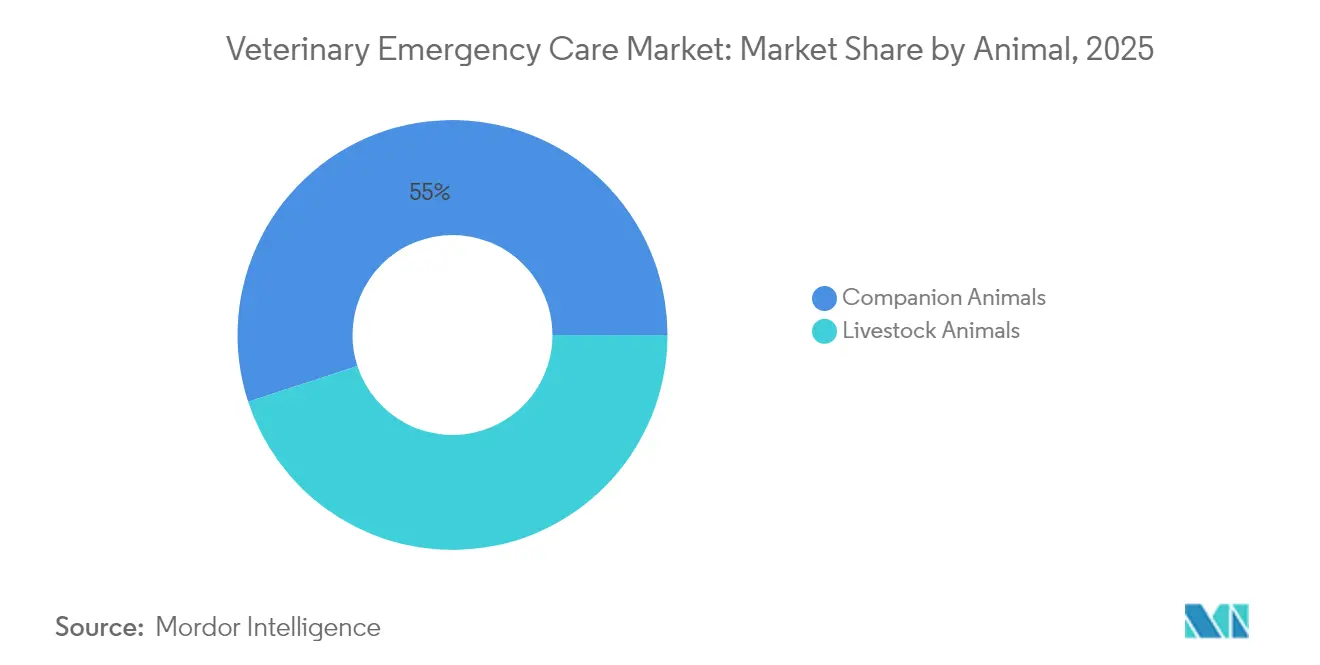

- By animal type, companion animals held 55.02% of the veterinary emergency care market share in 2025, while livestock animals are projected to grow at an 8.42% CAGR through 2031.

- By application, accidental ingestion represented 28.12% of the veterinary emergency care market size in 2025, whereas respiratory distress is on track for a 9.21% CAGR to 2031.

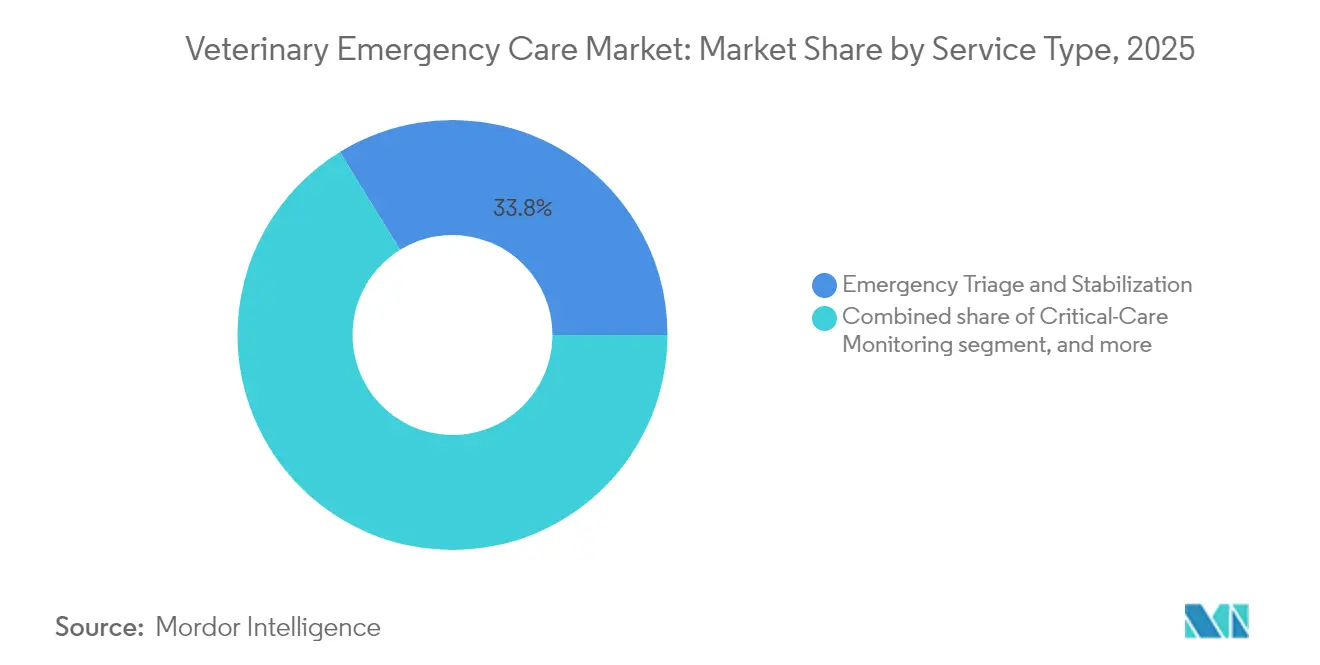

- By service type, emergency triage and stabilization led with 33.78% revenue share in 2025, while critical-care monitoring is forecast to post an 8.51% CAGR by 2031.

- By care setting, hospital-based emergency centers commanded 56.92% share in 2025, and mobile or on-call services are slated for a 9.31% CAGR through 2031.

- By geography, North America captured 42.35% share of the veterinary emergency care market in 2025; Asia-Pacific is predicted to expand at a 7.31% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Emergency Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding companion animal population | +1.2% | Global, concentrated in North America and Asia-Pacific | Long term (≥ 4 years) |

| Rising pet insurance penetration | +0.9% | North America and Europe, expanding in Asia-Pacific | Medium term (2-4 years) |

| Increasing household spend on veterinary care | +0.8% | Global, led by developed markets | Medium term (2-4 years) |

| Adoption of AI-enabled triage platforms | +0.7% | North America and Europe, Asia-Pacific uptake accelerating | Short term (≤ 2 years) |

| Growth of mobile emergency veterinary units | +0.6% | North America and Australia, expanding globally | Medium term (2-4 years) |

| Climate-driven surge in disaster cases | +0.5% | Global, highest in disaster-prone regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Companion Animal Population

Millennials and Gen Z households now drive pet adoptions, lifting U.S. dog numbers to 89.7 million in 2024 and pushing pet ownership to 66% of households. This younger cohort readily pursues specialist interventions during emergencies, reinforcing the veterinary emergency care market. Rising lifespans for cats and dogs inflate the geriatric pet cohort that often needs cardiac, renal, or orthopedic stabilization. Similar patterns are visible in China and India where urban families adopt small-breed dogs for companionship. The resulting demand swell anchors long-run growth for clinics, mobile units, and teleconsultation platforms.

Rising Pet Insurance Penetration

Premiums more than doubled between 2019 and 2024 and are projected to reach USD 4.5 billion in 2024, removing price friction at the point of care. In Sweden, 83% of dogs carry policies, offering a benchmark for other developed markets. When insurance covers intensive care, clinicians deploy advanced imaging, continuous telemetry, and multi-disciplinary teams without delay, boosting average invoice values. Consolidation among insurers under large investment groups could standardize reimbursement pathways and further expand the veterinary emergency care market[1]North American Pet Health Insurance Association, “State of the Industry Report 2024,” naphia.org.

Increasing Household Spend on Veterinary Care

American pet parents spent nearly USD 147 billion on pet products and services in 2023 with veterinary fees absorbing one-third of the total. Emergency invoices often range from USD 200 to USD 10,000, and owners continue to prioritize treatment despite economic cycles. Higher disposable incomes in emerging Asia add a new tier of affluent clients seeking 24/7 critical care. Premium services such as CT scans, minimally invasive surgery, and intensive pain control support stronger revenue per visit and sustain the veterinary emergency care market.

Adoption of AI-Enabled Triage Platforms

About 83.8% of clinicians report familiarity with artificial intelligence tools that support cytology, radiology, and workflow documentation. Systems such as Zoetis Vetscan Imagyst now deliver in-clinic CBCs with reference-grade precision in minutes. AI-driven scribes generate clinical notes, slashing administrative time and freeing doctors for patient care. Cardiac monitors using impedance cardiography show 14.71% gains in treated heartworm cases, underscoring the clinical promise. Faster, data-rich triage tightens treatment cycles and lifts throughput across emergency rooms.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High emergency care costs | -1.8% | Global, most acute in emerging markets | Medium term (2-4 years) |

| Shortage of emergency veterinarians | -1.4% | Global, pronounced in North America & Europe | Long term (≥ 4 years) |

| Professional burnout and attrition | -1.1% | Global, sector-wide | Long term (≥ 4 years) |

| Limited critical-care infrastructure in emerging markets | -0.9% | Latin America, Africa, parts of Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Emergency Care Costs

Prices for emergency surgery continue to rise; European data record 27% annual price jumps for pyometra corrections. Roughly 37% of U.S. households lack funds to pay a USD 500 bill, causing delayed visits that can worsen prognoses. Corporate clinics often set higher fee schedules than independents, widening affordability gaps. Some owners migrate to tele-advice or crowdfunding to offset expenses, yet cost sensitivity still trims visits in low-income segments. Policy initiatives that allow health-savings-account withdrawals for pet care could ease financial strain and protect future growth.

Shortage of Emergency Veterinarians

The U.S. is projected to fall short by more than 70,000 veterinarians by 2032, with 18 job openings per practitioner recorded in 2021. Demanding overnight shifts and compassion fatigue deter graduates from emergency specialties. Burnout carries an estimated USD 1-2 billion annual cost due to high turnover. Corporations such as Mars have earmarked USD 500 million for wage floors and student-debt relief to widen the talent pool. Apprenticeship programs like BluePearl EmERge are scaling but will take years to balance supply, restraining the veterinary emergency care market[2]Association of American Veterinary Medical Colleges, “Workforce Projections through 2032,” aavmc.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal: Companion Animals Lead Demand Growth

Companion animals contributed 55.02% to the veterinary emergency care market in 2025, supported by rising dog and cat ownership and insurance coverage expansion. Dogs typically incur higher per-case fees than cats because surgical and monitoring requirements can be more complex. Cats still drive volumes for obstructive uropathy and toxin exposure. Exotic pets—rabbits, birds, reptiles—show double-digit growth from a low base as specialist capabilities spread.

Livestock animals post the fastest expansion at an 8.42% CAGR through 2031, propelled by climate-linked disease outbreaks such as H5N1 in dairy herds. Rapid response teams apply herd-level triage, ultrasound screening, and on-site vaccinations. Regulatory pressure to prevent zoonotic spread makes emergency infrastructure essential. Overall, this segment enlarges the veterinary emergency care market size for farm owners seeking protective care.

By Application: Respiratory Distress Rising Fast

Accidental ingestion dominated with a 28.12% share in 2025, reflecting frequent chocolate, xylitol, and foreign-body incidents. Treatments often combine emetics, endoscopy, and activated charcoal, generating high invoice values and underpinning the veterinary emergency care market.

Respiratory distress is the fastest-growing application with a 9.21% CAGR. Brachycephalic breeds, wildfire smoke, and urban air pollution raise case volumes. Critical-care units deploy ventilators and oxygen cages, and new FDA-approved therapeutics for pulmonary edema broaden survival odds. Expansion in this segment lifts the overall veterinary emergency care market size.

By Service Type: Monitoring Technologies Advance

Emergency triage and stabilization brought 33.78% revenue in 2025 as every critical case begins with airway, breathing, and circulation checks. Clinics now embed AI algorithms that weigh vitals to color-code urgency and direct staff.

Critical-care monitoring is primed for an 8.51% CAGR. Non-invasive impedance cardiography, continuous glucose sensors, and telemetric ECGs allow minute-by-minute adjustments that cut mortality. These advances unlock premium billing, increasing the veterinary emergency care market share for specialty hospitals.

By Care Setting: Mobile Model Gains Momentum

Hospital-based emergency centers retained 56.92% of 2025 revenue due to comprehensive operating theaters and ICUs. Consolidators keep investing in 24/7 hubs that support referral cases and training programs.

Mobile and on-call services will grow fastest at 9.31% through 2031. Vans equipped with ultrasound, laboratory cartridges, and oxygen delivery reach homes and farms, meeting demand in underserved areas and relieving urban caseloads. The convenience factor draws price-sensitive owners while sustaining the veterinary emergency care market.

Geography Analysis

North America accounted for 42.35% of 2025 revenue, buoyed by high pet insurance penetration and corporate investments such as Mars Inc.’s USD 500 million workforce program. The FDA’s streamlined approval pathway for veterinary medicines also accelerates adoption of cutting-edge therapies. Workforce shortages remain the chief bottleneck, yet telehealth and mobile units soften the impact.

Asia-Pacific records the fastest 7.31% CAGR through 2031. China’s pet medical sector already exceeds USD 14 billion and urban clinics continue to proliferate. India follows with strong dog population growth that demands more emergency capacity. Consolidation is low, so private equity funds are injecting capital to build regional platforms.

Europe shows steady expansion as high insurance penetration reduces out-of-pocket shocks. Corporate ownership now covers 16% of veterinarians, and pan-European chains harmonize protocols. Spain, the UK, and Scandinavia see the swiftest practice roll-ups, improving resource availability while triggering fee debates. Overall, diversified growth across developed and emerging countries supports the veterinary emergency care market.

Competitive Landscape

The field remains moderately consolidated; the top five groups collectively own about 45% of clinics worldwide. Mars Inc. leads with roughly 3,000 hospitals after its VCA buyout and continues both acquisition and greenfield strategies. National Veterinary Associates split operations into Ethos specialty hospitals and NVA general practices to sharpen focus ahead of a potential IPO.

Private equity continues to merge regional networks; Mission Veterinary Partners and Southern Veterinary Partners plan a 730-clinic combination that could reshape U.S. competition subject to antitrust review. Technology differentiation is rising: Zoetis offers cartridge-based hematology analyzers with AI, while start-ups such as Airvet deliver 24-hour tele-triage. Mobile practices see higher profitability due to low fixed costs. These dynamics underline a competitive yet opportunity-rich veterinary emergency care market.

Veterinary Emergency Care Industry Leaders

BluePearl Specialty & Emergency Pet Hospital

VCA Animal Hospitals

Ethos Veterinary Health

MedVet

National Veterinary Associates (NVA)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: FDA conditionally approved Felycin-CA1 for subclinical hypertrophic cardiomyopathy in cats, the first drug addressing this condition.

- February 2025: Elanco and Medgene partnered to commercialize an H5N1 vaccine for dairy cattle; USDA conditional licensing is in final review.

- February 2025: PANOQUELL-CA1 became available in the U.S. to manage acute canine pancreatitis symptoms.

- January 2025: Mars Veterinary Health allotted USD 500 million to wages, education pathways, and debt relief, impacting more than 55,000 employees.

- January 2025: National Veterinary Associates reorganized into Ethos Veterinary Health and NVA to accelerate strategic growth.

- September 2024: Zoetis launched Vetscan OptiCell, the first AI-powered cartridge hematology analyzer.

Global Veterinary Emergency Care Market Report Scope

As per the scope of the report, veterinary emergency care is used to address the immediate medical needs of companion and livestock animals.

The veterinary emergency care market is segmented by animal, application, and geography. By animal, the market is segmented into companion animals and livestock animals. By application, the market is segmented into accidental ingestion, respiratory distress, gastrointestinal disease, seizures, accidents, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Companion Animals | Dogs |

| Cats | |

| Other Companion Animals | |

| Livestock Animals | Poultry |

| Cattle | |

| Sheep | |

| Other Livestock Animals |

| Accidental Ingestion |

| Respiratory Distress |

| Gastrointestinal Disease |

| Seizures |

| Accidents |

| Other Applications |

| Emergency Triage & Stabilization |

| Surgery |

| Critical-Care Monitoring |

| Diagnostic Imaging |

| Laboratory & Blood-Bank Services |

| Hospital-Based Emergency Centers |

| Standalone Emergency Clinics |

| Mobile / On-Call Services |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Animal | Companion Animals | Dogs |

| Cats | ||

| Other Companion Animals | ||

| Livestock Animals | Poultry | |

| Cattle | ||

| Sheep | ||

| Other Livestock Animals | ||

| By Application | Accidental Ingestion | |

| Respiratory Distress | ||

| Gastrointestinal Disease | ||

| Seizures | ||

| Accidents | ||

| Other Applications | ||

| By Service Type | Emergency Triage & Stabilization | |

| Surgery | ||

| Critical-Care Monitoring | ||

| Diagnostic Imaging | ||

| Laboratory & Blood-Bank Services | ||

| By Care Setting | Hospital-Based Emergency Centers | |

| Standalone Emergency Clinics | ||

| Mobile / On-Call Services | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the veterinary emergency care market by 2031?

The sector is expected to reach USD 29.67 billion by 2031, growing at a 5.99% CAGR.

Which animal segment is expanding fastest in emergency services?

Livestock cases are rising at an 8.42% CAGR due to outbreaks such as H5N1.

Why are mobile units gaining popularity?

Mobile teams cut overhead, reach rural owners, and relieve staffing shortages while growing revenue at a 9.31% CAGR.

How does insurance affect emergency treatment decisions?

Rising insurance penetration reduces out-of-pocket costs, letting clinicians choose optimal therapies without financial delays.

Which geography offers the quickest growth opportunity?

Asia-Pacific leads with a 7.31% CAGR as pet ownership and disposable incomes advance.

What technology trend is reshaping clinical workflows?

AI-enabled diagnostics and documentation solutions improve triage accuracy and free veterinarian time for patient care.

Page last updated on: