Veterinary Electrosurgery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

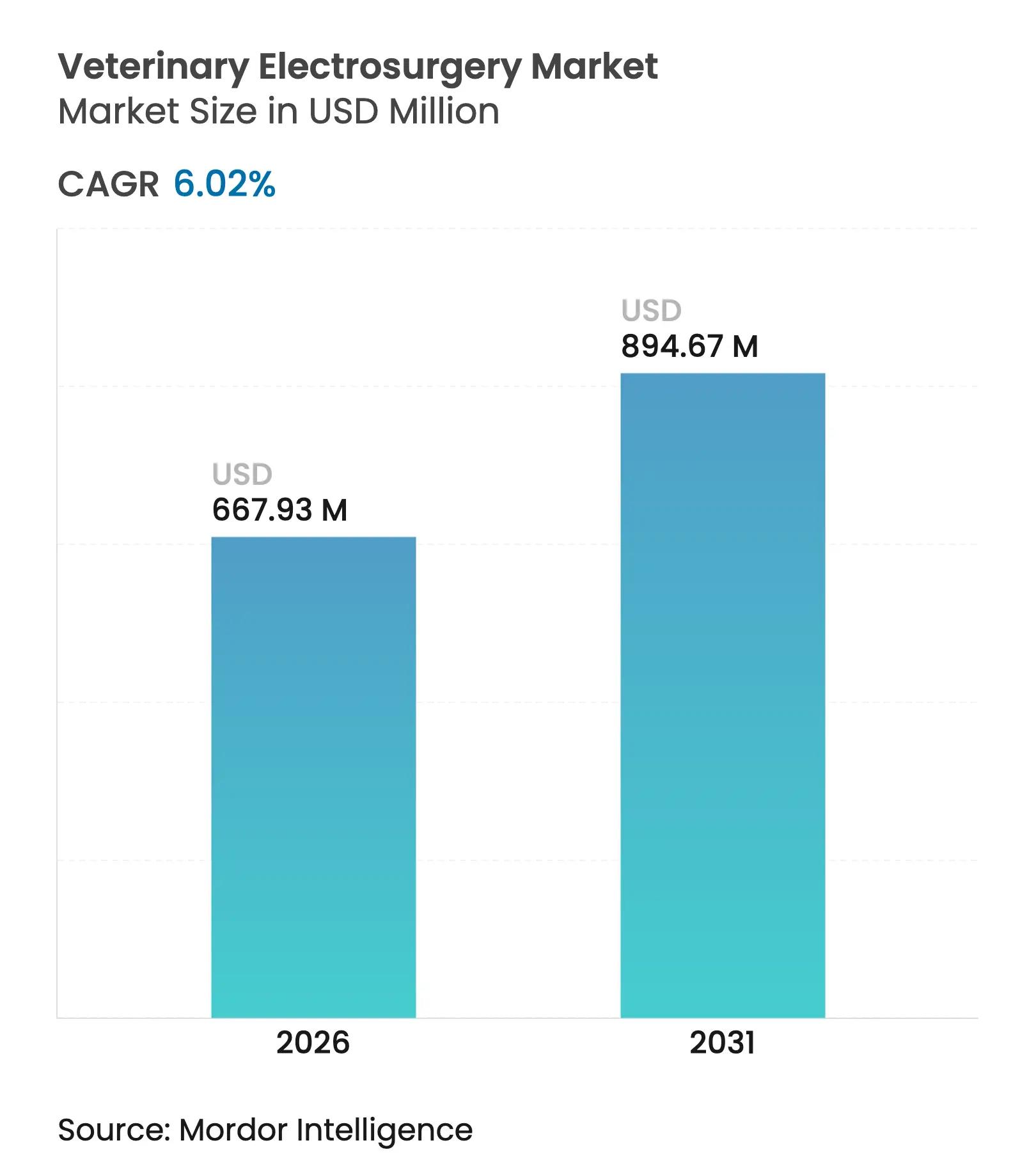

| Market Size (2026) | USD 667.93 Million |

| Market Size (2031) | USD 894.67 Million |

| Growth Rate (2026 - 2031) | 6.02 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Veterinary Electrosurgery Market Analysis by Mordor Intelligence

The veterinary electrosurgery market size in 2026 is estimated at USD 667.93 million, growing from 2025 value of USD 630.01 million with 2031 projections showing USD 894.67 million, growing at 6.02% CAGR over 2026-2031. Growth stems from steady pet healthcare spending, widespread adoption of minimally invasive surgery, and a rising number of specialty referral centers that house advanced surgical suites. Monopolar systems held the leading 45.9% revenue share in 2024, yet bipolar instruments are tracking a brisk 9.9% CAGR to 2030 as clinicians favor their tighter thermal control. Small-animal procedures dominate demand, and manufacturers with human-health portfolios continue to repurpose proven energy platforms for veterinary use. Capital spending by hospitals that treat insured pets, coupled with regulatory clarity in North America and Europe, reinforces a favorable investment climate for energy-based surgical tools.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Veterinary Electrosurgery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Pet health-insurance uptake Pet health-insurance uptake | +1.20% | North America & Europe; emerging in APAC | Medium term (2–4 years) | (~) % Impact on CAGR Forecast:+1.20% | Geographic Relevance:North America & Europe; emerging in APAC | Impact Timeline:Medium term (2–4 years) |

Growth in companion-animal population Growth in companion-animal population | +1.80% | Global urban centers | Long term (≥ 4 years) | |||

Uptake of minimally invasive surgeries Uptake of minimally invasive surgeries | +1.50% | North America & EU; early APAC adoption | Medium term (2–4 years) | |||

Rise of elective wellness procedures Rise of elective wellness procedures | +0.90% | Developed markets; spreading to emerging economies | Long term (≥ 4 years) | |||

AI-guided intra-operative energy modulation AI-guided intra-operative energy modulation | +0.70% | Tech hubs in North America, EU, select APAC cities | Short term (≤ 2 years) | |||

Expansion of specialty referral hospitals Expansion of specialty referral hospitals | +1.10% | Global; fastest in APAC and Latin America | Medium term (2–4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Demand for Pet Health Insurance

Insurance has lowered presurgical euthanasia by 41% in complex gastric dilatation–volvulus cases, allowing clinics to schedule advanced electrosurgical interventions that once faced cost barriers.[1]Jennifer J. Risselada et al., “Pet Insurance Impact on Surgical Decision-Making,” Frontiers in Veterinary Science, frontiersin.org The resulting financial predictability encourages practices to purchase premium generators and vessel sealers. Reimbursement policies that classify electrosurgery as standard care further accelerate adoption, especially in North America and parts of Europe where penetration tops 30% of pets insured.

Growth in Companion-Animal Population

Seventy percent of U.S. households owned at least one pet in 2024, the highest level ever recorded by the American Pet Products Association.[2]American Pet Products Association, “2024–2025 National Pet Owners Survey,” americanpetproducts.org Comparable trends in Western Europe and urban Asia signal rising caseloads for spay-neuter, tumor removal, and orthopedic procedures that depend on reliable electrosurgical energy. Urban millennials and Gen Z owners show a strong preference for tools that shorten anesthesia time and recovery periods, thereby reinforcing demand for bipolar and advanced sealing modalities.

Increasing Adoption of Minimally Invasive Surgeries

Laparoscopic and thoracoscopic techniques cut tissue trauma and pain, a fact supported by 2024 clinical data showing electrosurgery lowered canine celiotomy blood loss from 3.0 mL to 0.7 mL. Veterinary teaching hospitals equipped with integrated OR platforms and virtual-reality simulators continue to scale surgeon proficiency, accelerating the shift toward energy-based laparoscopy.

Shift Toward Elective Wellness Procedures

Regular dental cleanings, early tumor excisions, and preventive orthopedic corrections now sit on fixed wellness calendars, ensuring predictable use of electrosurgical handpieces. Dental applications grow fastest as owners recognize systemic links between periodontal disease and cardiac health. Clinics capitalize by standardizing cordless micro-seal pens that limit collateral heat during delicate gingival resections.

Drivers Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Pet-Care Costs Rising Pet-Care Costs | -1.40% | Global, with acute impact in price-sensitive emerging markets | Medium term (2-4 years) | % Impact on CAGR Forecast:-1.40% | Geographic Relevance:Global, with acute impact in price-sensitive emerging markets | Impact Timeline:Medium term (2-4 years) |

Device-Related Thermal Injury Concerns & Litigation Device-Related Thermal Injury Concerns & Litigation | -0.80% | Primarily North America & EU with established legal frameworks | Short term (≤ 2 years) | |||

Supply-Chain Dependence On Limited RF Component Vendors Supply-Chain Dependence On Limited RF Component Vendors | -0.90% | Global, with concentrated impact in Asia Pacific manufacturing hubs | Medium term (2-4 years) | |||

Shortage Of Board-Certified Veterinary Surgeons In Developing Regions Shortage Of Board-Certified Veterinary Surgeons In Developing Regions | -0.60% | APAC, MEA, and Latin America with limited veterinary education infrastructure | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Pet-Care Costs

Inflation lifted surgical fees 8% year-over-year in 2024, prompting mid-income owners to defer optional interventions. Clinics in emerging markets sometimes choose budget generators over premium systems to keep pricing within reach, slowing high-end device adoption even as pet insurance coverage expands.

Device-Related Thermal Injury Concerns & Litigation

A Veterinary Record case report documented electrically induced ventricular fibrillation during thoracoscopic surgery, spotlighting the risk when energy settings are misapplied. Heightened liability pushes practitioners toward devices with automatic shutoffs or AI feedback loops, but training and capital expense can impede rapid replacement of legacy generators.[3]M. Oberkircher et al., “Electrically Induced Ventricular Fibrillation During Thoracoscopy,” Veterinary Record Case Reports, bvajournals.com

Segment Analysis

By Product: Monopolar Versatility Sustains Leadership While Bipolar Gains Ground

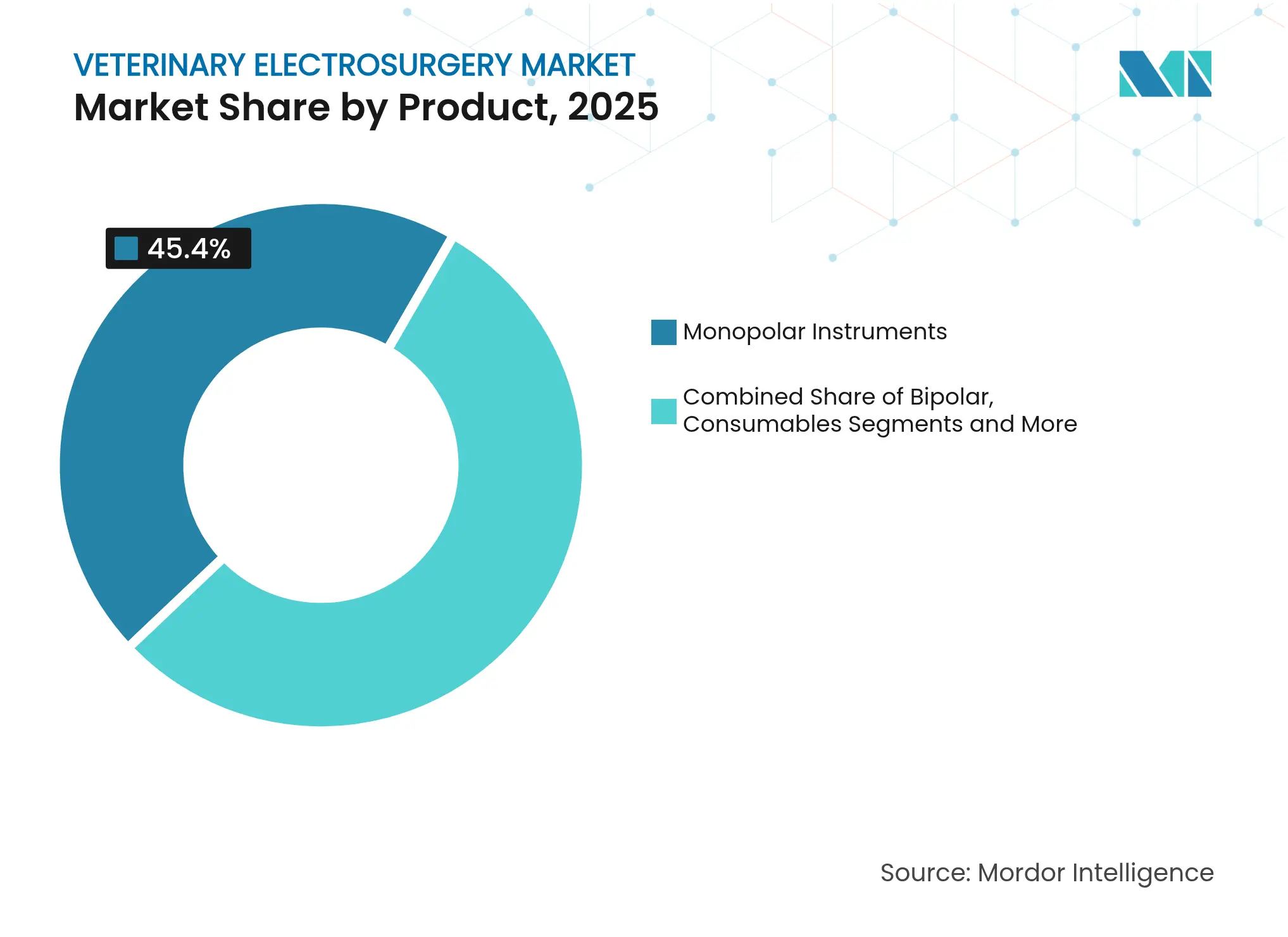

Monopolar instruments retained a 45.40% revenue share in 2025, benefiting from dual cutting–coagulation capability, universal accessory compatibility, and lower entry pricing. Their ubiquity in general practice means consumables such as grounding pads and blade electrodes form a steady aftermarket revenue stream. The veterinary electrosurgery market gained a wave of replacements in 2025 as clinics retired aging units, fueling short-term demand.

Bipolar systems, however, display the sharpest growth trajectory. Their 9.48% CAGR reflects surgeon preference for smaller thermal footprints when operating near neurovascular bundles or delicate oral tissues. Vessels up to 7 mm can now be sealed reliably in less than two seconds, reducing ligature time and intra-operative blood loss by 70% in randomized canine trials. Integration of impedance sensing in new bipolar handpieces makes them a centerpiece of training curricula at veterinary teaching hospitals.

Note: Segment shares of all individual segments available upon report purchase

By Application: General Surgery Remains Core While Dentistry Accelerates

General surgery delivered 35.40% of 2025 revenue, underpinning equipment utilization across spay-neuter, soft-tissue oncology, and emergency trauma repairs. The segment’s durability allows clinics to amortize high-end generators over broad case mixes, especially where rapid coagulation shortens anesthesia duration. Laparoscopic ovariectomy, for instance, posts lower complication rates and shorter incisions when energy-based vessel sealers replace sutures.

Dental surgery is forecast to record a 10.05% CAGR through 2031, the highest among all applications. Rising awareness of periodontal disease’s link to systemic illness drives owners to authorize ultrasonic bone contouring and gingivectomy procedures that depend on precise energy control. Manufacturers respond with micro-bipolar probes that navigate tight oral fields while maintaining sub-100 °C tip temperatures, reducing adjacent tissue desiccation.

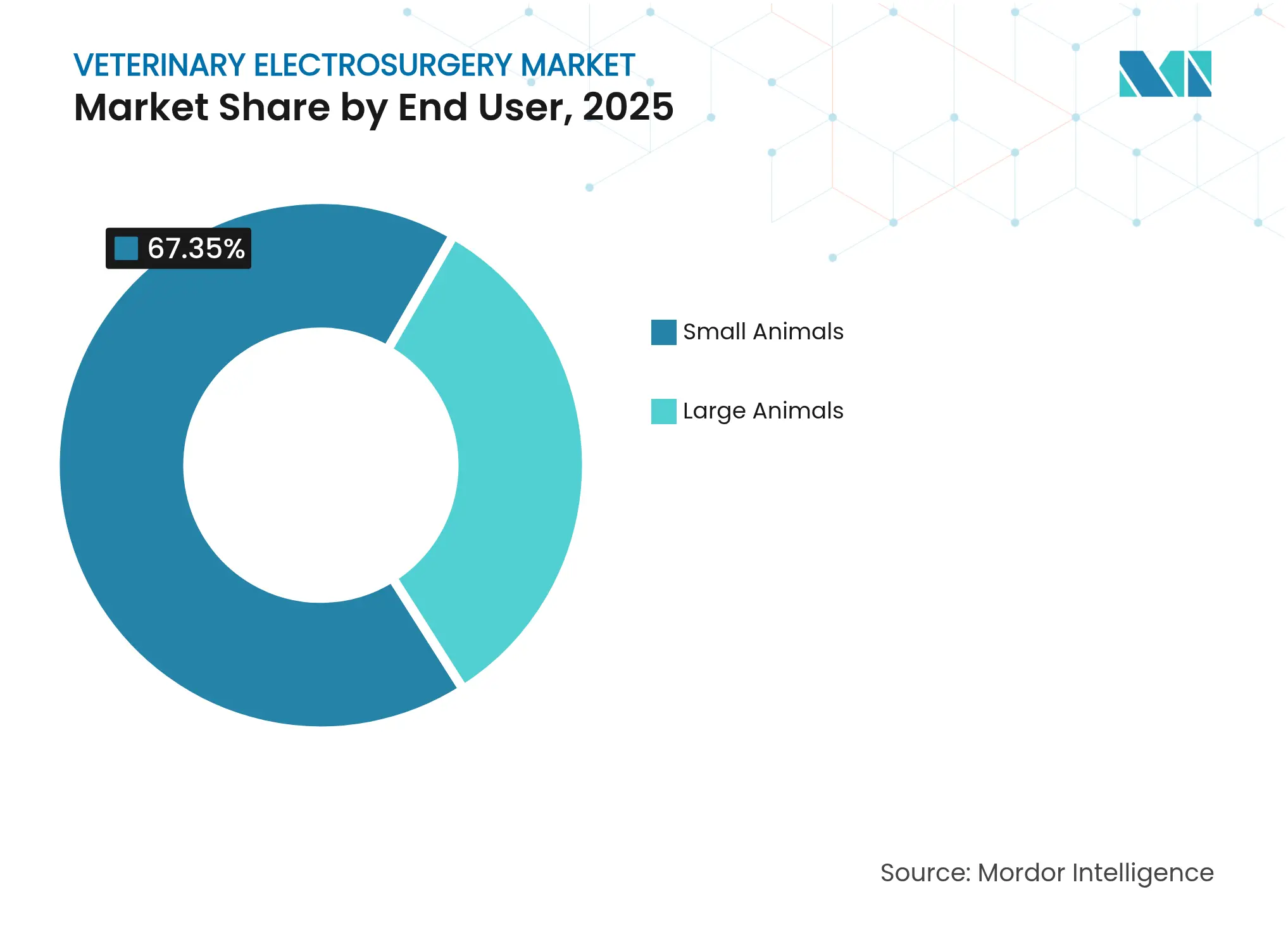

By Animal Type: Small-Animal Dominance Fuels Innovation

Small animals contributed 67.35% of 2025 revenue, and the veterinary electrosurgery market size for this segment is projected to climb at an 8.35% CAGR to 2031. Canine and feline procedures demand smaller handpieces and finely tuned power curves, pushing suppliers to miniaturize generators without sacrificing wattage.

Large-animal use cases remain niche but stable. Equine referral centers favor portable generators capable of sealing vessels during field castrations or fracture repairs. Mobile operating theaters have proven viable for high-value horses, expanding the veterinary electrosurgery market into new service models.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By End User: Hospitals Drive High-End Purchases, Clinics Emphasize Versatility

Veterinary hospitals anchor roughly 60% of revenue and adopt integrated OR ecosystems that link electrosurgical generators with imaging, smoke evacuation, and data capture. According to multi-center data collected in 2024, such configurations cut turnover time by 12% per procedure. Specialty centers further magnify demand for premium bipolar sealers and AI-guided platforms.

Clinics, especially those in suburban areas, prefer multifunction carts that toggle between monopolar and bipolar modes. Vendor service contracts and e-commerce consumable subscriptions have become decisive purchase factors, underpinning Patterson Companies’ 2024–2025 acquisition spree aimed at bolstering last-mile distribution.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

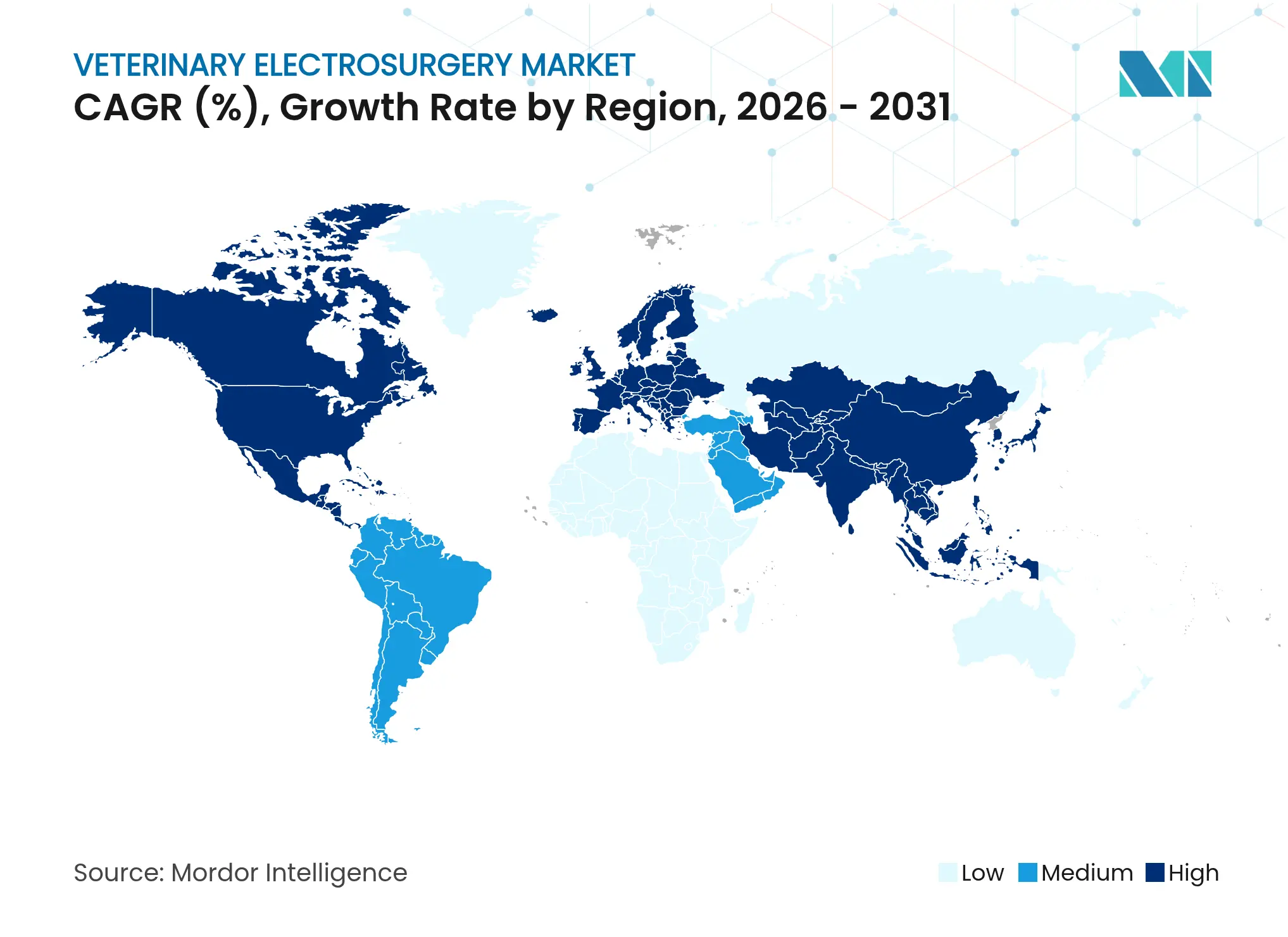

North America leads global revenue owing to dense pet-insurance coverage, a mature referral network, and FDA pathways that streamline device clearance for animal use. The United States alone accounted for roughly 39.60% of 2025 sales, buoyed by higher procedure rates per veterinarian than any other region. Training symposiums sponsored by device makers at AVMA and AAHA meetings reinforce early adoption of next-generation generators.

Europe follows as the second-largest market and is poised for steady mid-single-digit growth as harmonized EU standards remove national registration hurdles. Veterinary schools in Germany, the Netherlands, and the Nordic countries have integrated laparoscopic simulation labs, ensuring a pipeline of surgeons fluent in electrosurgical techniques. EU welfare directives that prioritize pain minimization increase demand for energy modalities that cut operative time and post-operative analgesic use.

The Asia Pacific region represents the fastest-growing opportunity, with China and India together accounting for more than 50% of the regional companion-animal base in 2025. Growth near 9.7% CAGR stems from expanding middle-class spending and rising adoption of wellness care plans. However, uneven regulatory landscapes and a shortage of board-certified surgeons create pockets of unmet demand, underscoring the need for scalable training solutions and mid-priced equipment tiers. Covetrus’s recent filings highlight strategic investment in APAC distribution channels to capture this upside.

Competitive Landscape

Market Concentration

The market shows moderate concentration as top multinational device firms pivot familiar human-surgery systems into veterinary formats. Johnson & Johnson’s ENSEAL X1 Curved Jaw Tissue Sealer, launched in 2021, features impedance-based feedback that adapts energy to tissue thickness, cutting lateral heat by up to 33%. Smith+Nephew and Medtronic likewise exploit cross-divisional R&D to introduce scaled-down generators with veterinary presets and single-use disposables tailored for smaller anatomies.

White-space innovation now centers on AI-enabled generators that pair wirelessly with handpieces. Google Patent US-2025-039288-A1 describes situational recognition protocols that auto-select power curves based on tissue occlusion, a capability likely to reach commercial rollout by 2027. Meanwhile, B. Braun channels EUR 1.2 billion (USD 1.4 billion) of annual R&D spending into expanding its Caiman vessel-sealing line, adding ergonomic grips preferred in veterinary dentistry and ophthalmology.

Regional distributors such as Patterson and DJO strengthen their portfolios through acquisitions that fill consumables gaps and extend field service reach. The resulting ecosystem of bundled hardware, disposables, and financing packages represents a competitive moat, making it harder for single-product entrants to gain traction. Software upgrades that unlock new energy modes via subscription further bind clinics to established suppliers.

Veterinary Electrosurgery Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Johnson & Johnson MedTech debuted a next-generation electrosurgical generator engineered for cross-modal energy delivery, targeting both human and veterinary markets.

- January 2025: The Swedish University of Agricultural Sciences and Surgical Science unveiled a virtual-reality module for canine laparoscopic ovariectomy, enhancing skill transfer without animal use.

- September 2024: Patterson Companies acquired Infusion Concepts (U.K.) and Mountain Vet Supply (U.S.) to extend the distribution of critical-care and energy products.

- August 2024: DJO closed on Companion Animal Health, integrating laser therapy into surgical suites and positioning for bundled sales with electrosurgical units.

Table of Contents for Veterinary Electrosurgery Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Demand For Pet Health Insurance

- 4.2.2Growth In Companion Animal Population

- 4.2.3Increasing Adoption Of Minimally-Invasive Surgeries In Veterinary Care (MIS)

- 4.2.4Shift Toward Elective Wellness Procedures

- 4.2.5AI-Assisted Intra-Operative Energy Modulation Improving Safety

- 4.2.6Surge In Specialty Referral Hospitals With Advanced Surgical Suites

- 4.3Market Restraints

- 4.3.1Rising Pet-Care Costs

- 4.3.2Device-Related Thermal Injury Concerns & Litigation

- 4.3.3Supply-Chain Dependence On Limited RF Component Vendors

- 4.3.4Shortage Of Board-Certified Veterinary Surgeons In Developing Regions

- 4.4Supply Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitute Products

- 4.7.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value)

- 5.1By Product

- 5.1.1Bipolar Electrosurgical Instruments

- 5.1.2Monopolar Electrosurgical Instruments

- 5.1.3Consumables & Accessories

- 5.2By Application

- 5.2.1General Surgery

- 5.2.2Gynecological & Urological Surgery

- 5.2.3Dental Surgery

- 5.2.4Orthopedic Surgery

- 5.2.5Ophthalmic Surgery

- 5.2.6Others

- 5.3By Animal Type

- 5.3.1Small Animals

- 5.3.2Large Animals

- 5.4By End User

- 5.4.1Veterinary Hospitals

- 5.4.2Specialty & Referral Centers

- 5.4.3Veterinary Clinics

- 5.5Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia Pacific

- 5.5.4Middle East & Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East & Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Symmetry Surgical Inc.

- 6.3.2Avante Health Solutions (DRE Veterinary)

- 6.3.3B. Braun SE

- 6.3.4Medtronic

- 6.3.5Covetrus

- 6.3.6Integra LifeSciences Holdings Corp.

- 6.3.7KARL STORZ SE & Co. KG

- 6.3.8Eickemeyer Veterinary Equipment

- 6.3.9Burtons Medical Equipment

- 6.3.10Kwanza Veterinary

- 6.3.11Macan Manufacturing

- 6.3.12Heal Force

- 6.3.13Bovie Animal Health (Symmetry subsidiary)

- 6.3.14Aspen Surgical

- 6.3.15Jorgensen Laboratories

- 6.3.16BOWA-electronic

- 6.3.17Ethicon (Johnson & Johnson)

- 6.3.18Olympus Corporation

- 6.3.19Eickmeyer USA

- 6.3.20Shenzhen Mindray Bio-Medical Electronics

7. Market Opportunities & Future Outlook

- 7.1White-space & unmet-need assessment

Global Veterinary Electrosurgery Market Report Scope

As per the scope of the report, electrosurgery involves the application of a high-frequency electrical current through an animal's body. Veterinary electrosurgery devices are used for surgical cutting and for controlling bleeding in surgical procedures. The Veterinary Electrosurgery Market is segmented by Product (Bipolar Electrosurgical Instruments, Monopolar Electrosurgical Instruments and Consumables and accessories), Application (General Surgery, Gynecological and urological Surgery, Dental Surgery, Orthopedic Surgery and Others), Animal Type (Small Animals and Large Animals), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.