Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

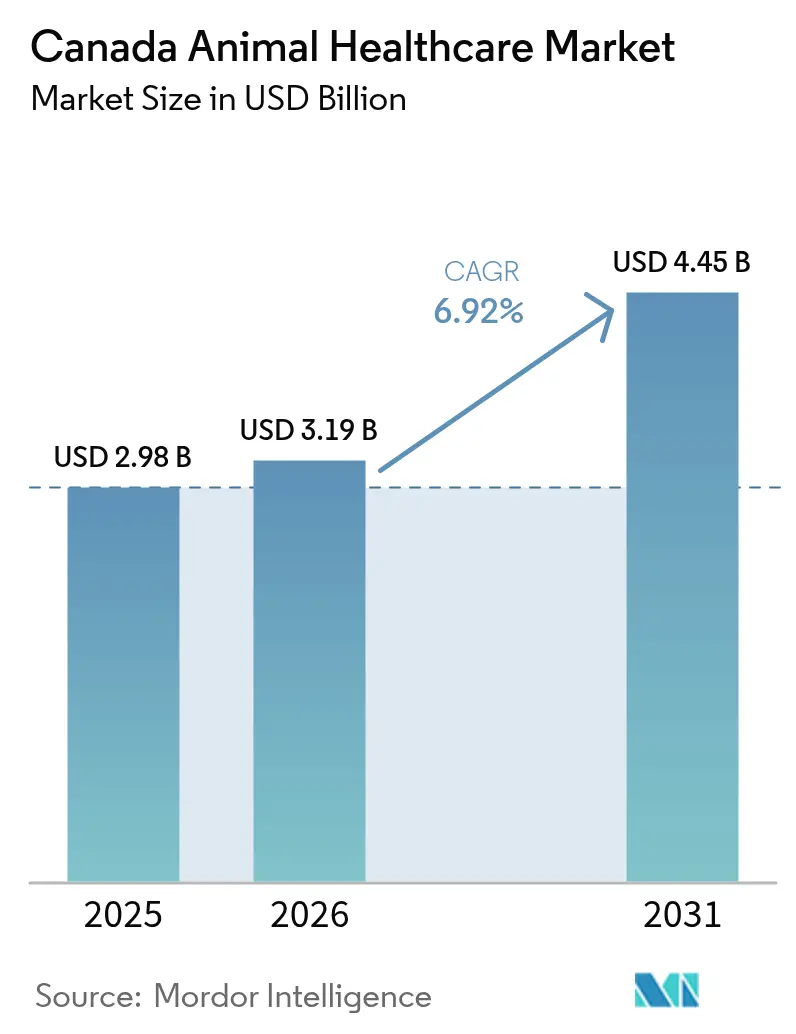

| Base Year Market Size (2025) | USD 2.98 Billion |

| Market Size (2026) | USD 3.19 Billion |

| Market Size (2031) | USD 4.45 Billion |

| Growth Rate (2026 - 2031) | 6.92% CAGR |

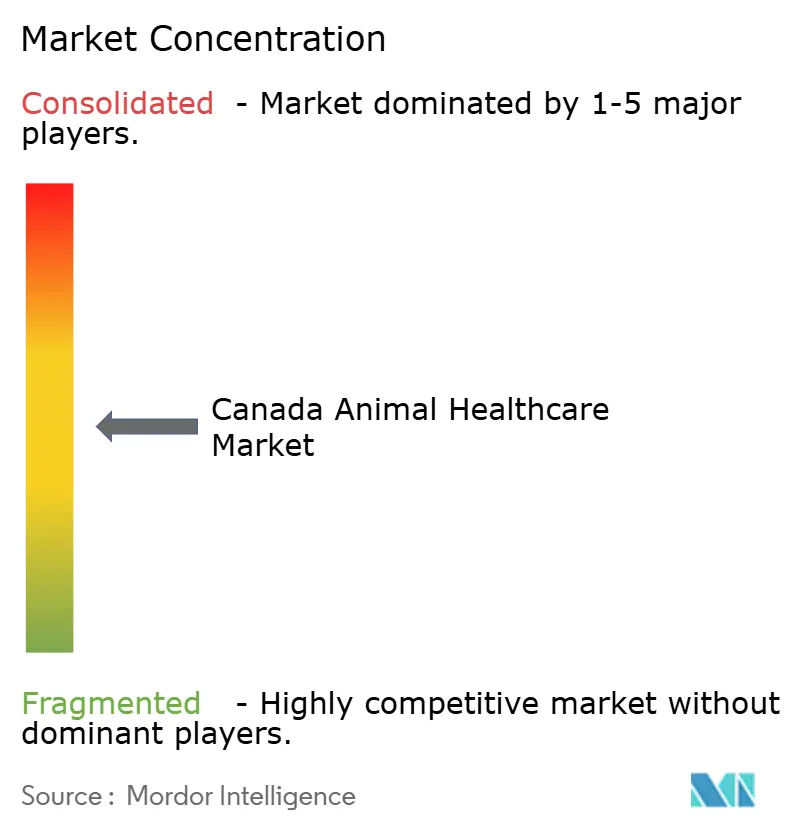

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Animal Healthcare Market Analysis by Mordor Intelligence

The Canada Animal Healthcare Market size is expected to increase from USD 2.98 billion in 2025 to USD 3.19 billion in 2026 and reach USD 4.45 billion by 2031, growing at a CAGR of 6.92% over 2026-2031.

Heightened pet-owner willingness to pay for monoclonal antibodies, rising livestock biosecurity mandates, and a rapid shift toward point-of-care diagnostics are combining to lift revenue even as antimicrobial-use restrictions reshape therapeutic portfolios. Federal funding for foot-and-mouth disease (FMD) and highly pathogenic avian influenza (HPAI) vaccine banks is accelerating demand for production-animal biologics while provincial pharmacist-dispensing reforms open new retail channels that compress clinic margins. Diagnostic suppliers are capitalizing on workflow decentralization by embedding benchtop analyzers and AI-enabled cytology into primary-care settings. Companion-animal premiumization underpins average-ticket growth in urban centers, yet cost sensitivity in rural livestock practice sustains bifurcated demand patterns that favor multi-species portfolios and vertically integrated distribution networks.

Key Report Takeaways

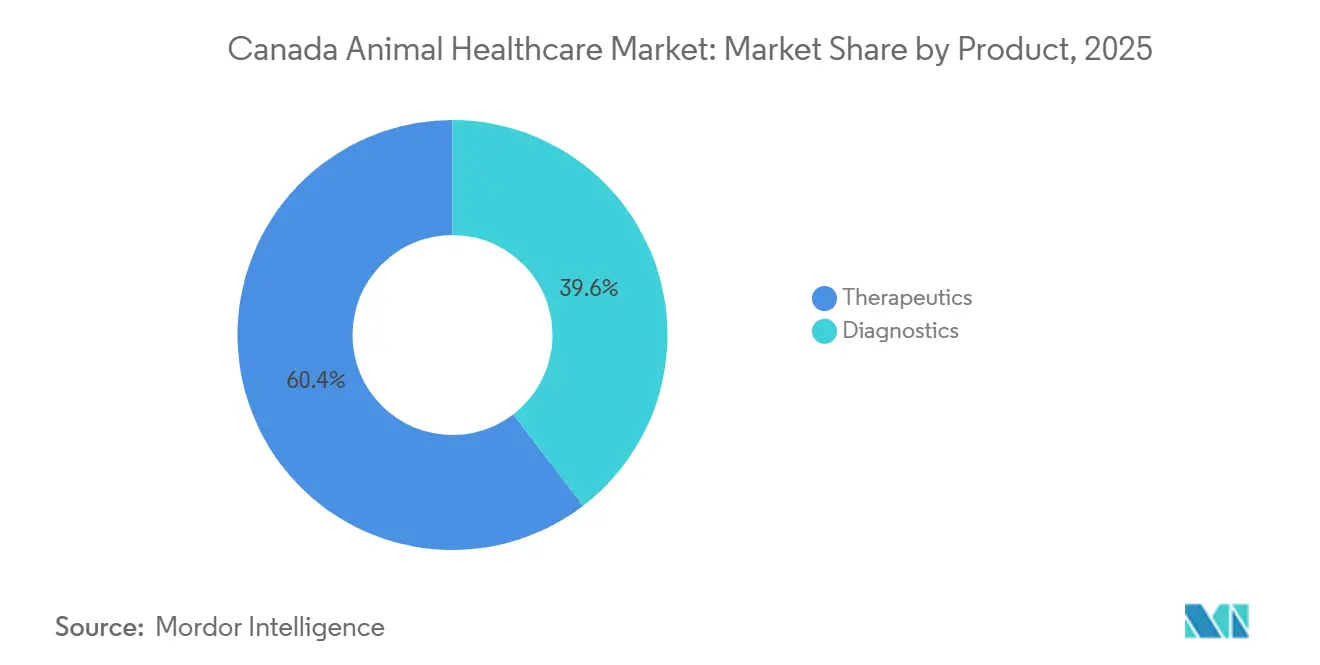

- By product category, therapeutics led with 60.4% revenue share in 2025, while diagnostics is forecast to expand at a 7.86% CAGR through 2031.

- By animal type, dogs and cats accounted for 56.1% of 2025 revenue, whereas poultry is projected to advance at a 7.12% CAGR to 2031.

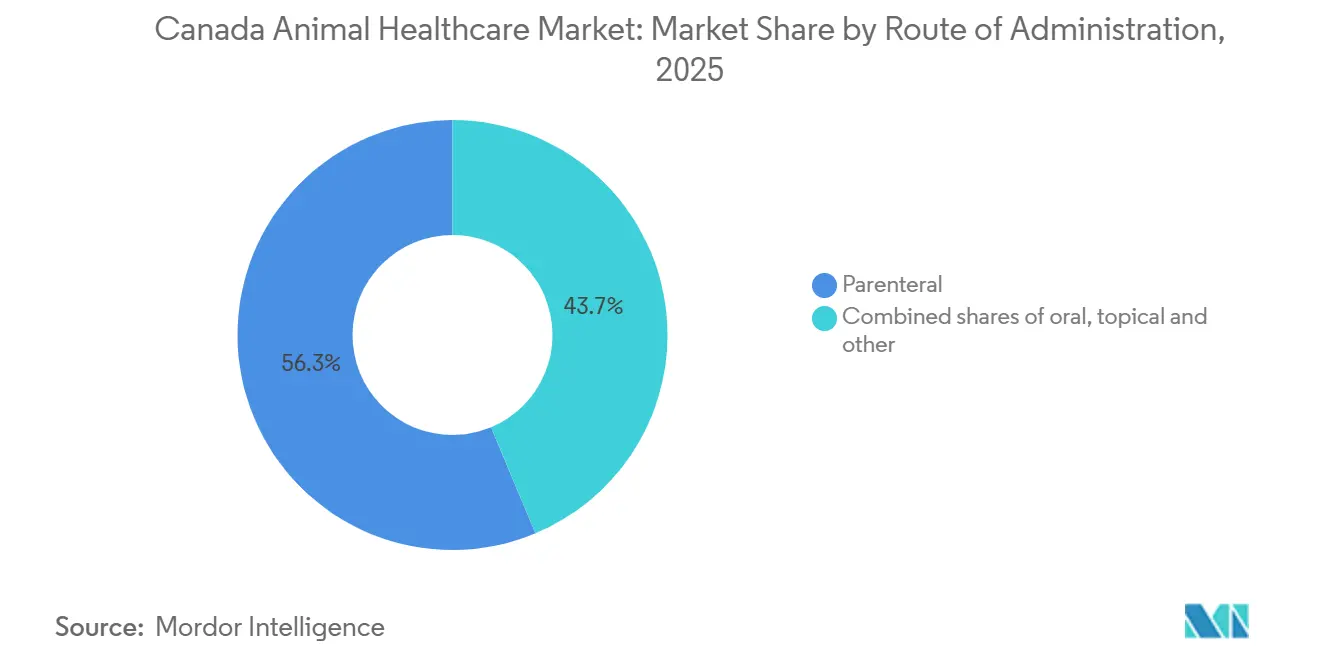

- By route of administration, parenteral delivery represented 56.3% share of the Canada animal healthcare market size in 2025 and oral formulations are predicted to grow at a 7.33% CAGR over 2026-2031.

- By end user, veterinary hospitals and clinics held 57.7% Canada animal healthcare market share in 2025, while point-of-care settings exhibit the highest projected CAGR at 8.32% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Animal Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Pet Ownership & Premiumization of Companion-Animal Care | +1.8% | National, highest intensity in Ontario, British Columbia, Alberta urban centers | Medium term (2-4 years) |

| Rapid Adoption of Advanced Diagnostics (POCT & Molecular) | +1.5% | National, led by corporate veterinary chains and academic institutions | Short term (≤ 2 years) |

| National FMD & HPAI Vaccine-Bank Investments Boosting Biologics Demand | +1.2% | National, elevated focus in British Columbia poultry, Alberta and Saskatchewan livestock | Long term (≥ 4 years) |

| Growth in Pet Insurance Penetration Expanding Spend Capacity | +0.9% | National, concentrated in Ontario and British Columbia metropolitan areas | Medium term (2-4 years) |

| Pharmacist-Dispensing Reforms Opening New Distribution Channels | +0.7% | Provincial, led by Ontario, Alberta, Quebec with potential national expansion | Medium term (2-4 years) |

| Mandatory Farm-Level AMU Benchmarking Driving Vaccines & Alternatives | +0.6% | National, most acute in Alberta, Saskatchewan, Quebec livestock-intensive regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Pet Ownership & Premiumization of Companion-Animal Care

Sixty percent of Canadian households owned a dog or cat in 2024, underpinning steady demand for core vaccinations and chronic-disease management [1]Canadian Animal Health Institute, “2024 Pet Population Survey,” cahi-icsa.ca. Premiumization is visible in the rapid uptake of monoclonal antibodies such as Librela, which command monthly prices above CAD 100 yet reduce long-term NSAID exposure and renal risk. Annual household pet spending reached CAD 9.3 billion in 2023, with veterinary services absorbing the largest share. Ontario’s 2024 Veterinary Professionals Act widened the telemedicine scope, enabling remote follow-ups that support bundled care plans. Urban clinics now package diagnostics, therapeutics, and digital monitoring to differentiate in competitive metro areas, while rural large-animal clients remain underserved.

Rapid Adoption of Advanced Diagnostics (POCT & Molecular)

Point-of-care platforms compress turnaround times from days to minutes, enabling same-visit therapy decisions that lift compliance and clinic throughput. IDEXX’s inVue Dx cellular analyzer, launched in November 2024, delivers AI-assisted cytology in 10 minutes, displacing manual microscopy in routine cases. The Catalyst Pancreatic Lipase Test provides quantitative pancreatitis results within 10 minutes, outperforming reference-lab assays that require up to 48 hours. On the production-animal side, CFIA’s National Centre for Foreign Animal Disease upgraded to Oxford Nanopore and Illumina sequencing between 2023 and 2026, enabling real-time pathogen characterization during outbreaks. Prairie Diagnostic Services cut Salmonella serotyping turnaround from four weeks to 24 hours by adopting Nanopore sequencing in 2024. Regulatory guidance from the College of Veterinarians of Ontario in December 2024 acknowledged the innovation speed yet flagged validation and liability gaps for AI-enabled devices.

National FMD & HPAI Vaccine-Bank Investments Boosting Biologics Demand

Federal Budget 2023 earmarked CAD 57.5 million over five years to establish vaccine banks for FMD and HPAI, recognizing the export threat posed by transboundary diseases [2]Government of Canada, “Budget 2023 Vaccine Bank Investments,” budget.gc.ca. Canada has not yet authorized routine poultry vaccination, but 11.2 million birds were culled between 2022 and 2024, underscoring the economic risk. Autogenous vaccines are gaining momentum in swine and poultry, leveraging CFIA’s streamlined approval path for farm-specific pathogens. This dual strategy, emergency banks plus autogenous products, lets producers hedge outbreak risk without committing to blanket immunization policies that could trigger trade sanctions. Long-term biologic demand is therefore tethered to both national contingency planning and farm-level customization.

Growth in Pet Insurance Penetration Expanding Spend Capacity

Gross written pet-insurance premiums reached CAD 583.9 million in 2024, rising 20.7% year-over-year, yet penetration remains below 5% of eligible pets. Carriers such as Trupanion embed coverage into practice-management software, enabling real-time claims adjudication and reducing owner hesitation toward elective diagnostics. Insured pets generate higher lifetime revenue because coverage absorbs high-ticket imaging or oncology costs that can exceed CAD 5,000 per episode. Provincial rules vary. Ontario permits direct-to-consumer sales, while Quebec requires insurer licensing, creating regional experimentation with wellness bundles and telemedicine riders. As penetration approaches the 10-15% range seen in the United Kingdom, premium therapeutics and diagnostics should decouple from immediate out-of-pocket constraints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Veterinary Services & Therapeutics | −0.8% | National, most acute in rural and lower-income urban areas | Short term (≤ 2 years) |

| Counterfeit & Grey-Market Medicines | −0.5% | National, concentrated in e-commerce and cross-border channels | Medium term (2-4 years) |

| Veterinarian Workforce Shortages in Rural Large-Animal Practice | −0.4% | National, most severe in Prairie provinces, Northern Ontario, rural Quebec | Long term (≥ 4 years) |

| Provincial Take-Back / Stewardship Fees Increasing Product Exit Risk | −0.3% | Provincial, led by British Columbia and Ontario extended-producer-responsibility programs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Veterinary Services & Therapeutics

Veterinary service prices have risen faster than general inflation, driven by labor shortages, diagnostic-equipment capex, and pharmaceutical price hikes, pushing routine exams with vaccinations to above CAD 300 and emergency visits past CAD 2,000 [3]Canadian Veterinary Medical Association, “Cost of Care Report,” canadianveterinarians.net. Premium biologics such as Librela and Solensia cost CAD 100-150 per month, limiting access for multi-pet households. Rural communities face compounded burdens because a shortage of veterinarians forces long travel or defers care, especially in large-animal sectors. The Competition Bureau’s October 2024 study highlighted exclusive distribution agreements as cost inflators and recommended pharmacist dispensing, which Ontario, Alberta, and Quebec have begun adopting. Until insurance penetration or public subsidies expand, discretionary categories, such as dental, behavioral, and wellness diagnostics, will see volume constraints.

Counterfeit & Grey-Market Medicines

E-commerce and cross-border mail provide entry points for counterfeit or diverted veterinary medicines, undermining product integrity and complicating adverse-event tracking. CFIA pursues sporadic enforcement, but surveillance is less robust than in human pharmaceuticals. Grey-market imports, often genuine products sourced from lower-priced jurisdictions, skirt authorized channels and erode manufacturer revenue. The pandemic-era swing to online purchasing amplified direct-to-owner pathways that bypass veterinary oversight, enabling prescription parasiticides to circulate without valid scripts. Provincial colleges lack resources to audit web sales, while federal border controls focus on human and agricultural biosecurity. Absent serialization mandates, veterinary supply chains remain vulnerable until CFIA, Canada Border Services Agency, and provincial regulators coordinate a track-and-trace regime.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Diagnostics Outpace Therapeutics in Innovation Velocity

Therapeutics commanded 60.4% of Canada animal healthcare market share in 2025, supported by vaccines, parasiticides, anti-infectives, and monoclonal antibodies. Diagnostics captured the balance but are set to grow at a 7.86% CAGR through 2031, the strongest category trajectory. Vaccine revenue remains resilient across both companion and production animals; however, innovation momentum has shifted toward autogenous and recombinant platforms that target farm-specific pathogens. Parasiticides evolved from spot-ons to flavored chewables such as Simparica Trio and NexGard PLUS, blending flea, tick, heartworm, and intestinal-parasite protection in one dose. Diagnostics growth hinges on point-of-care immunoassays and AI-enabled imaging that shorten decision cycles. IDEXX’s inVue Dx automates cytology in primary-care clinics, while molecular platforms anchor surveillance in production-animal sectors, underscoring how diagnostics now set the pace for innovation.

Diagnostics generate sticky consumable revenue and lock practices into proprietary ecosystems, insulating suppliers from price competition. Immunodiagnostic tests dominate companion-animal practice, but molecular assays and next-generation sequencing are penetrating livestock surveillance, aided by CFIA’s genomics upgrades. Digital pathology and AI-driven radiology analysis remain nascent yet represent the next wave of diagnostic differentiation.

By Animal Type: Companion Dominance Meets Poultry Urgency

Dogs and cats generated 56.1% of 2025 revenue, reflecting Canada’s 7.9 million dogs and 8.5 million cats and the premiumization trend in urban centers. Poultry is set for the fastest growth at a 7.12% CAGR, driven by HPAI surveillance, autogenous-vaccine adoption, and biosecurity spend in British Columbia’s Fraser Valley. Equine and livestock segments provide stable demand for reproductive vaccines and joint-health products, but face workforce shortages that cap service capacity.

Companion-animal spend is concentrated in specialty diagnostics and monoclonal antibodies, with Mars-owned VCA Canada operating more than 120 hospitals that aggregate complex-care demand. Poultry urgency is shaped by export-market risk; Canada’s HPAI Vaccination Task Force continues to assess trade-partner acceptance before endorsing routine immunization. Livestock growth depends on competitive export access and ongoing antimicrobial-use reductions, nudging producers toward preventive biologics and probiotics.

By Route of Administration: Oral Gains Ground on Parenteral Incumbency

Parenteral formats captured 56.3% of 2025 revenue owing to vaccine dominance and injectable biologics. Oral formulations are forecast to expand at a 7.33% CAGR, benefiting from palatable chewables that improve owner compliance and eliminate injection-site risks. Topical spot-ons face share pressure but remain relevant for rapid ectoparasite knockdown, especially in livestock pour-on treatments.

Oral parasiticides such as Simparica Trio, NexGard PLUS, and Credelio treat fleas, ticks, and internal parasites in one chewable dose, positioning them as convenient alternatives to monthly topical applications. Extended-release injectables like ProHeart 12 streamline heartworm prevention for owners who struggle with adherence, though higher upfront costs temper adoption. Ontario’s telemedicine rules allow remote prescription refills for oral medications, reinforcing oral growth in under-served regions.

By End User: Point-of-Care Settings Disrupt Hospital-Centric Models

Veterinary hospitals and clinics held 57.7% of 2025 revenue, but point-of-care and in-house settings are poised for an 8.32% CAGR through 2031 as decentralized diagnostics gain traction. Academic and research institutes focus on surveillance and vaccine development, accounting for a smaller yet strategically important share.

Benchtop chemistry analyzers, hematology systems, and rapid immunoassays allow same-visit diagnoses, cutting turnaround from days to minutes. IDEXX’s integrated ecosystem locks clinics into proprietary consumables, creating high recurring revenue. Portable ultrasound priced below CAD 10,000 enables imaging in mobile practices, broadening diagnostic reach beyond brick-and-mortar hospitals. Telemedicine, legitimized by Ontario’s 2024 legislation, offers follow-up care without in-person visits, easing rural access constraints and complementing in-house diagnostic capability.

Competitive Landscape

The Canada animal healthcare market is moderately concentrated. Multinational therapeutics leaders Zoetis, Boehringer Ingelheim, Merck Animal Health, and Elanco defend vaccine and parasiticide franchises, while IDEXX and Heska dominate in-clinic diagnostics through proprietary analyzers that lock clinics into consumables. Provincial pharmacist-dispensing reforms threaten clinic mark-ups on pharmaceuticals, compressing margins and encouraging service-based revenue diversification.

Corporate consolidation reached a significant portion of veterinary practices, with Mars-owned VCA Canada operating over 120 hospitals that leverage scale in procurement and specialist staffing. Independent clinics retain pricing power in underserved rural markets, particularly for large-animal work where workforce shortages create excess demand. Emerging disruptors include point-of-care molecular-diagnostic suppliers that offer same-day pathogen identification and digital-health platforms integrating telemedicine, remote monitoring, and practice-management software.

Biologics innovation favors incumbents with regulatory expertise and cold-chain assets, yet smaller players can carve niches in autogenous vaccines and equine joint-health products. AI-enabled diagnostic imaging tools expand beyond cytology to radiography and ultrasound interpretation, but province-level guidance on liability and validation remains nascent, allowing early adopters to differentiate without heavy regulatory burden.

Canada Animal Healthcare Industry Leaders

Idexx Laboratories

Virbac Corporation

Zoetis Animal Healthcare

Boehringer Ingelheim Pharma GmbH & Co. KG.

Merck & Co., Inc.

- *Disclaimer: Major Players sorted in no particular order

Geography Analysis

Canada applies a single national regulatory framework via CFIA for biologics and therapeutics, yet provincial veterinary colleges impose practice standards that fragment service delivery models. Ontario, British Columbia, and Alberta anchor companion-animal spend thanks to dense urban pet populations, dual-income households, and corporate hospital chains that support specialty care. British Columbia’s Fraser Valley, Canada’s poultry heartland, faces recurring HPAI outbreaks, driving demand for surveillance diagnostics and autogenous vaccines even as routine flock immunization waits on trade-partner consensus.

The Prairie provinces, Alberta, Saskatchewan, and Manitoba, dominate cattle and swine production. CIPARS antimicrobial-use benchmarking pressures producers to replace therapeutic antibiotics with preventive biologics, reinforcing demand for vaccines and probiotics. Rural regions struggle with veterinarian shortages; the Canadian Veterinary Medical Association projects widening gaps as retirements outpace new rural-practice entrants, elevating labor costs and limiting service availability. Provincial pharmacist-dispensing reforms fracture traditional clinic revenue streams, yet they improve owner access to prescriptions in areas without local veterinary pharmacies.

Pet-insurance penetration is highest in Ontario and British Columbia metros, where real-time claims adjudication reduces financial friction at checkout, but remains below 5% nationally, leaving headroom for growth. Federal vaccine-bank funding targets FMD and HPAI preparedness, benefiting Prairie livestock and British Columbia poultry sectors by mitigating catastrophic disease risk.

Recent Industry Developments

- January 2026: Health Canada and the Canadian Food Inspection Agency cleared the first gene-edited pigs that can withstand porcine reproductive and respiratory syndrome virus, a pathogen long blamed for high piglet losses and steep economic hits, after Genus PLC and its PIC Canada unit used CRISPR-Cas9 to switch off the viral entry point on the animals’ cells.

- October 2025: Zoetis secured approval for Lenivia in Canada, a new companion-animal therapeutic, during Q3 2025.

- September 2025: Merck Animal Health Canada obtained approval for Bravecto Quantum, the first once-yearly injectable for flea and tick control in dogs.

Canada Animal Healthcare Market Report Scope

The animal healthcare market comprises therapeutic and diagnostic products and solutions for companion and farm animals. Companion animals can be tamed or adopted for companionship or as house/office guards, and farm animals are raised for meat and milk-based products. Companion animals include canines, felines, and equines.

The Canada animal healthcare market is segmented by product, animal type, route of administration, end-user, and geography. By product, it is segmented into therapeutics (vaccines, parasiticides, anti-infectives, medical feed additives, monoclonal antibodies & biologics) and diagnostics (immunodiagnostic tests, molecular diagnostics, diagnostic imaging, clinical chemistry & hematology, and digital pathology & AI platforms. By animal type, the market is segmented into companion animals, equine, and livestock. By route of administration, the market is segmented into oral, parenteral, topical, and other routes. By End users, the market is segmented into veterinary hospitals & clinics, academic & research institutes, and point-of-care / in-house settings. For each segment, the market size and forecast are provided in terms of value (USD).

By Product

| Therapeutics | Vaccines |

| Parasiticides | |

| Anti-infectives | |

| Medical Feed Additives | |

| Monoclonal Antibodies & Biologics | |

| Diagnostics | Immunodiagnostic Tests |

| Molecular Diagnostics (PCR, qPCR, NGS) | |

| Diagnostic Imaging | |

| Clinical Chemistry & Hematology | |

| Digital Pathology & AI Platforms |

By Animal Type

| Companion Animals |

| Equine |

| Livestock |

By Route of Administration

| Oral |

| Parenteral |

| Topical |

| Other Routes |

By End User

| Veterinary Hospitals & Clinics |

| Academic & Research Institutes |

| Point-of-Care / In-House Settings |

| By Product | Therapeutics | Vaccines |

| Parasiticides | ||

| Anti-infectives | ||

| Medical Feed Additives | ||

| Monoclonal Antibodies & Biologics | ||

| Diagnostics | Immunodiagnostic Tests | |

| Molecular Diagnostics (PCR, qPCR, NGS) | ||

| Diagnostic Imaging | ||

| Clinical Chemistry & Hematology | ||

| Digital Pathology & AI Platforms | ||

| By Animal Type | Companion Animals | |

| Equine | ||

| Livestock | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| Topical | ||

| Other Routes | ||

| By End User | Veterinary Hospitals & Clinics | |

| Academic & Research Institutes | ||

| Point-of-Care / In-House Settings | ||

Key Questions Answered in the Report

How fast is pet insurance adoption growing in Canada?

Gross written premiums rose 20.7% year-over-year to CAD 583.9 million in 2024, yet penetration remains below 5%, indicating large headroom for growth.

Which product segment is expanding quickest?

Diagnostics are projected to grow at a 7.86% CAGR through 2031 as point-of-care platforms and AI-enabled analyzers spread to primary-care clinics.

What drives poultry health spending?

Recurring HPAI outbreaks in British Columbia’s Fraser Valley and national surveillance mandates underpin a 7.12% CAGR for poultry therapeutics and diagnostics through 2031.

How are pharmacist-dispensing reforms affecting veterinary clinics?

Reforms in Ontario, Alberta, and Quebec open retail channels for prescriptions, reducing clinic pharmaceutical mark-ups and incentivizing service-based revenue models

Why are monoclonal antibodies gaining traction in companion animals?

Products like Librela and Solensia provide targeted pain relief with fewer systemic side effects, supporting premium pricing despite monthly costs above CAD 100.

Page last updated on: