United States Online Trading Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

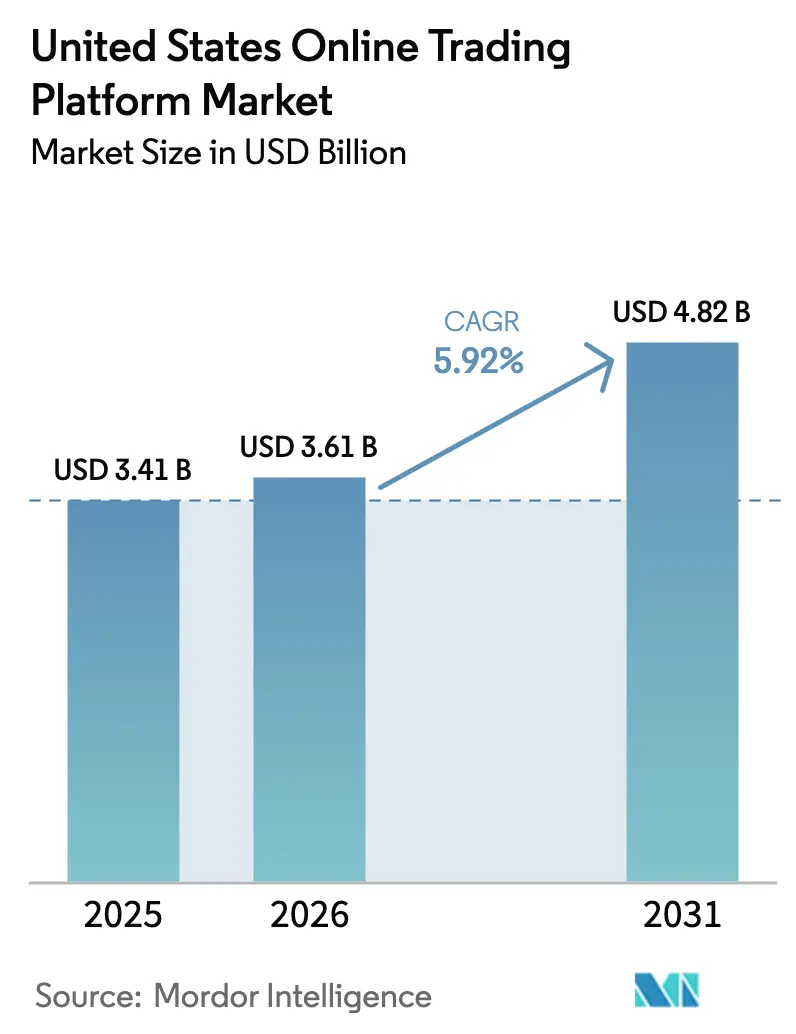

| Base Year Market Size (2025) | USD 3.41 Billion |

| Market Size (2026) | USD 3.61 Billion |

| Market Size (2031) | USD 4.82 Billion |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Online Trading Platform Market Analysis by Mordor Intelligence

The US online trading platform market size was valued at USD 3.41 billion in 2025 and estimated to grow from USD 3.61 billion in 2026 to reach USD 4.82 billion by 2031, at a CAGR of 5.92% during the forecast period (2026-2031). Rising retail participation, reinforced by commission-free trades and fractional shares, is sustaining double-digit growth in new account openings while increasing platform operating scale requirements. Mobile-first design, cloud deployment, and AI-enabled analytics are expanding use cases beyond basic equity trading into fixed-income, crypto, and alternative assets. Meanwhile, compliance costs driven by FINRA’s proposed fee increases and the Securities and Exchange Commission’s (SEC) focus on AI governance are pressuring margins, tilting competitive advantage toward firms with broad asset bases and strong technology stacks. The tension between ease of access and regulatory scrutiny is expected to shape strategic investment in cybersecurity, data-privacy controls, and post-trade automation over the outlook period.

Key Report Takeaways

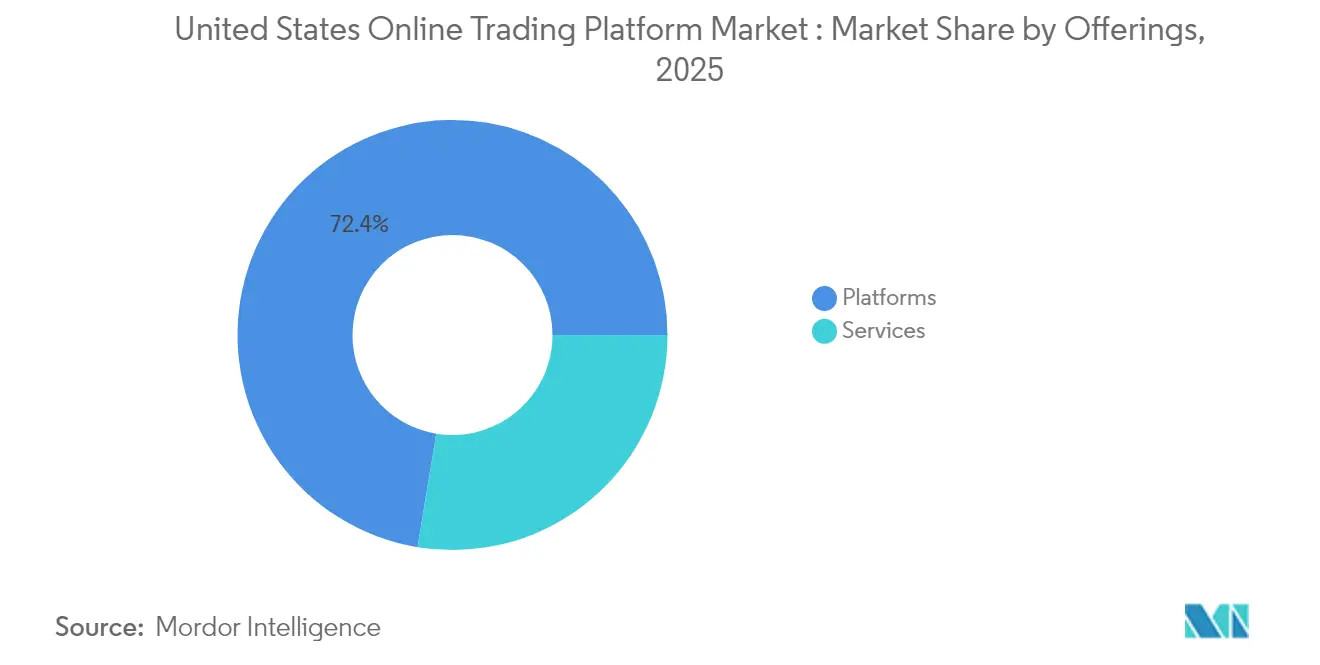

- By offerings, platforms led with 72.40% of US online trading platform market share in 2025, whereas services are on track to grow at a 7.78% CAGR through 2031.

- By deployment mode, cloud accounted for 61.40% share of the US online trading platform market size in 2025 and is expanding at 9.27% CAGR to 2031.

- By type, beginner-focused interfaces captured 56.30% revenue share in 2025; advanced platforms are projected to rise at an 8.12% CAGR to 2031.

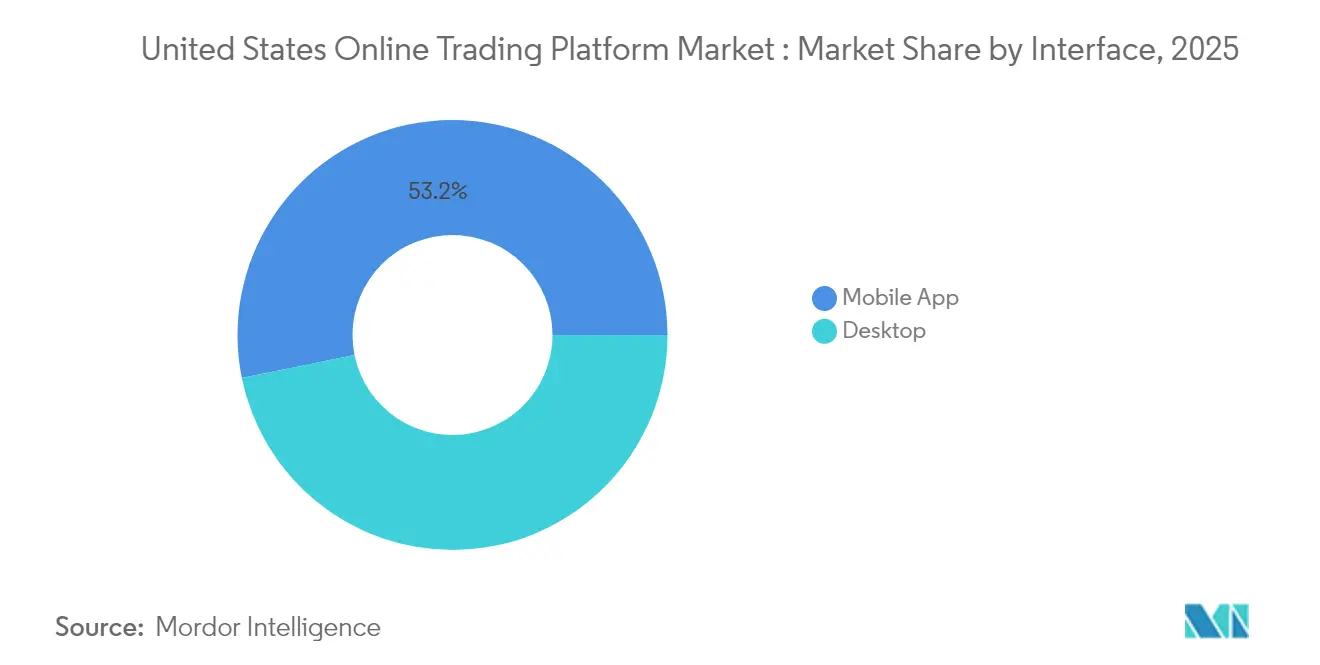

- By interface, mobile apps held 53.20% share of the US online trading platform market size in 2025, while desktop solutions are growing at 7.74% CAGR.

- By end user, retail investors dominated with 80.40% market share in 2025, yet institutional investors exhibit the fastest growth at 7.52% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with United states representing one among them. The global report on online trading platform market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

United States Online Trading Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of commission-free trades & fractional shares | +1.8% | Global, with strongest impact in North America | Medium term (2-4 years) |

| Smartphone ubiquity accelerating mobile trading adoption | +1.5% | Global, particularly strong in APAC and North America | Short term (≤ 2 years) |

| AI-driven robo-advisory & predictive analytics integration | +1.2% | North America & EU leading, expanding to APAC | Long term (≥ 4 years) |

| Growing retail investor base (Gen Z & Millennials) | +1.0% | Global, with demographic concentration in urban centers | Medium term (2-4 years) |

| Diversification into crypto & alternative asset classes | +0.8% | North America leading, selective EU adoption | Medium term (2-4 years) |

| 24-hour trading windows unlocking after-hours liquidity | +0.6% | North America, with pilot expansions to other regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Commission-Free Trades and Fractional Shares

Commission-free pricing reshaped competitive positioning by removing cost barriers and shifting monetization toward payment-for-order-flow and cash-management yields. Robinhood’s 2024 revenue of USD 2.95 billion, with 61% sourced from order flow, illustrates how ancillary income models offset zero-commission execution.[1]U.S. Securities and Exchange Commission, “SEC Announces Enforcement Results for Fiscal Year 2024,” sec.gov Fractional trading broadens access to high-price equities and serves as an acquisition funnel for first-time investors. Academic evidence shows micro-lot trades contain useful liquidity signals that tighten spreads over time. Platforms continue introducing USD 1 entry-points to capture untapped share in lower-income cohorts, but the resulting order-flow concentration heightens regulatory focus on best-execution quality.

Smartphone Ubiquity Accelerating Mobile Trading Adoption

More than 64% of Gen Z and 68% of Millennials prefer mobile banking, reinforcing a mobile-first orientation in brokerage design.[2]American Bankers Association, “Consumer Survey Banking Methods 2024,” aba.com AI-enabled sentiment engines embedded in apps reduce manual research time and can lower operating costs by 25% for institutions adopting algorithmic support. Social-trading features, however, nudge risk-taking: peer-performance feeds correlate with larger bet sizes yet lower satisfaction when volatility rises. Regulators are evaluating whether gamified prompts overstimulate trading frequency, signalling future disclosure mandates on behavioral nudges.

AI-Driven Robo-Advisory & Predictive Analytics Integration

Assets managed by robo-advisors surpassed USD 1 trillion in 2025 and continue to rise despite documented trust gaps among low-income households.[3]Springer, “Scoring the Ethics of AI Robo-Advice,” link.springer.com The SEC’s penalties against two advisers for “AI-washing” underscore enforcement around marketing accuracy. Hybrid models that blend machine outputs with human oversight record higher adherence rates and mitigate behavioral inertia, suggesting an emerging standard rather than full autonomy. Platforms investing in explainable AI stand to improve conversion among cautious demographics and differentiate on transparency.

Growing Retail Investor Base (Gen Z & Millennials)

Transfers by investors under 40 have tripled over the past decade, placing sustained demand on digital channels.[4]JPMorgan Chase Institute, “The Changing Demographics of Retail Investors,” jpmorganchase.com Participation rates rose faster among Black and Hispanic investors, indicating progress in financial inclusion. Social-media-driven episodes such as WallStreetBets demonstrated collective influence, but academic review reveals negative holding-period returns on positions opened at peak chatter, reinforcing education needs. Platforms integrating financial-literacy modules can improve retention while satisfying upcoming SEC guidance on digital engagement practices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened cyber-security & data-privacy breaches | -1.2% | Global, with acute impact in North America and EU | Short term (≤ 2 years) |

| Complex & evolving SEC / CFTC / FINRA compliance costs | -0.8% | North America, with spillover to global operations | Medium term (2-4 years) |

| Looming ban/reform of Payment-for-Order-Flow (PFOF) model | -0.7% | North America, with potential global regulatory spillover | Medium term (2-4 years) |

| Market saturation among discount brokers squeezing margins | -0.5% | North America, with selective impact in mature markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened Cyber-Security & Data-Privacy Breaches

The probability of extreme loss events from cyber incidents quadrupled since 2017, magnifying systemic risk across interconnected trading ecosystems. FINRA’s 2025 report flags new account fraud and quantum-computing vulnerabilities as near-term threats. The 2023 ransomware attack that disrupted 60 credit unions spotlighted third-party dependency risk. Average phishing breach costs remain modest in headline terms, but potential reputational erosion for platforms handling margin balances is far higher. Cyber-resilience investment and multi-factor authentication protocols are becoming core differentiators alongside execution quality.

Complex & Evolving SEC / CFTC / FINRA Compliance Costs

FINRA is phasing in fee increases that will add USD 450 million in annual costs by 2029. The 2025 SEC examination priorities expand oversight into AI deployment, T+1 post-trade timing, and record-keeping of off-channel communications. Implementation of the Securities Lending and Transparency Engine introduces granular reporting fees, while T+1 settlement compresses reconciliation windows and elevates real-time automation requirements. Record penalties of USD 8.2 billion in 2024 illustrate rising financial exposure from compliance lapses. Platforms with mature governance frameworks and scalable cloud infrastructure will absorb these costs more effectively, reinforcing consolidation trends.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offerings: Platforms Consolidating Service Integration

Platforms captured 72.40% revenue in 2025 and remain the anchor around which value-added services are layered. The US online trading platform market size for platforms is poised to expand steadily as integrated research, margin lending, and cash-management features enhance stickiness. Services grow at an 7.78% CAGR, signaling that consulting, advisory APIs, and third-party data feeds drive incremental revenue without forcing full stack development. Competitive differentiation is shifting from raw execution speed toward breadth of ancillary capabilities such as tax-loss harvesting or ESG screening. Elevated compliance overhead accelerates platform mergers, allowing acquirers to spread regulatory costs and monetize through cross-selling. Conversely, niche providers are positioning as service-layer partners rather than standalone brokers, inserting themselves into platform ecosystems via open APIs.

The pricing pivot away from commissions increases reliance on net interest income and payment-for-order-flow rebates, exposing revenue to rate cycles and policy shifts. Service providers delivering algorithmic best-execution analysis or liquidity sourcing models gain importance as platforms seek to defend spreads amid scrutiny. The US online trading platform market will likely witness hybrid revenue stacks where core platform access remains free, while premium analytics, coaching, or tax tools follow a subscription or usage-based model. This twin-track strategy helps stabilize earnings against volume volatility and aligns product roadmaps with user sophistication curves.

By Deployment Mode: Cloud Accelerates Efficiency

Cloud deployments held 61.40% share in 2025 and grew fastest at 9.27% CAGR, underscoring strategic preference for elastic capacity, micro-services architecture, and embedded security updates. The US online trading platform market share advantage for cloud is amplified by the push toward 24-hour trading windows and real-time settlement that strain legacy on-premises data centers. Cloud native analytics shorten release cycles, enabling rapid compliance patching when regulations shift. Major providers are introducing FINRA-ready logging templates and isolated tenancy modules that mitigate data-sovereignty concerns, persuading previously reluctant institutional clients.

On-premises systems persist where ultra-low latency or proprietary hardware acceleration is non-negotiable, such as high-frequency trading desks. Yet even these users adopt hybrid stacks, routing less sensitive workloads to the cloud for cost savings. As the US online trading platform industry standardizes post-trade messaging around ISO 20022 and real-time affirmation, cloud’s scalability becomes vital. Vendor concentration risk is addressed through multi-cloud failover architectures and zero-trust network frameworks. Cloud adoption also supports environmental mandates, with providers offering renewable-energy credits that help platforms meet ESG disclosure requirements

By Type: Advanced Platforms Attract Sophisticated Users

Beginner-focused apps secured 56.30% share in 2025 by simplifying onboarding and promoting micro-investing. Nevertheless, advanced platforms are sprinting ahead at 8.12% CAGR, reflecting user migration toward deeper analytics, conditional orders, and multi-asset coverage. The US online trading platform market size for advanced tiers is expanding as experienced investors prioritize direct-market-access and smart-routing engines that reduce slippage. Advanced platforms typically charge modest commissions or tiered subscriptions, cushioning them from swings in order-flow revenue and aligning incentives with execution quality.

Gamification tactics that once drove engagement for beginners face regulatory examination, nudging providers to add risk controls and educational overlays. As portfolios grow, users seek performance attribution tools, tax-efficient rebalancing, and cross-asset correlation dashboards. Advanced platforms integrate these modules, potentially in partnership with third-party fintech engines, to capture migrating users. Success hinges on balancing complexity with usability, ensuring that interface depth does not overwhelm but progressively unveils sophisticated functions.

By Interface: Desktop Regains Momentum Among Serious Traders

Mobile held 53.20% share in 2025, but desktop usage is reviving with 7.74% CAGR as frequent traders revert to larger screens for multimonitor charting and keyboard shortcuts. Deep option-chain analytics, strategy builders, and algorithm back-testing engines perform better on desktop environments. The US online trading platform market size attached to desktop users reflects higher average revenue per account, as this cohort often trades derivatives and maintains margin balances. Mobile retains primacy for rapid order entry and portfolio monitoring; however, interoperability across devices becomes a hygiene factor.

Desktop innovation focuses on customizable workspaces, latency-optimized data feeds, and AI-assisted scripting that transforms natural-language instructions into executable code. Meanwhile, mobile apps are evolving toward micro-learning hubs, pushing bite-sized market insights and risk alerts. Platforms achieving seamless state-sync between devices reinforce loyalty and limit account portability. Regulatory proposals targeting behavioral prompts could reshape mobile interface design, further elevating desktop’s analytical edge among professionals.

By End User: Institutional Uptake Accelerates

Retail investors account for 80.40% share, anchoring platform economics through scale of individual accounts. Institutional investors, however, are growing at 7.52% and require advanced order-management systems, compliance reporting, and connectivity into custodial workflows. As wealth managers digitize front-office interactions, the US online trading platform market opens new subscription revenue for white-label dashboards and digital-advice portals. Institutions also view digital channels as distribution arms for model portfolios, structured notes, and private-market allocations.

Retail flows remain sensitive to macro-volatility and social-media sentiment, demanding robust customer-support and real-time risk education. Institutional flows, by contrast, provide steadier asset levels and contribute to liquidity depth that benefits retail price discovery. Platforms that tailor feature sets-automated Model Delivery for advisors and community chat moderation for retail-capture synergies while satisfying divergent compliance obligations. Growth in both cohorts suggests a future where multi-segment architectures outcompete single-segment incumbents.

Geography Analysis

The United States remains the focal point of the US online trading platform market, supported by equity markets representing 47.4% of global capitalization and a rule framework that balances investor protection with innovation. The May 2024 shift to T+1 settlement improved affirmation rates and reduced trade fails, demonstrating operational resilience. National adoption of spot Bitcoin ETFs in 2024 widened asset coverage, stimulating incremental order flow in the US online trading platform market. State-level variations, particularly around digital-asset licensing, inject complexity; platforms often segment functionality by residency to comply with divergent rules.

Urban regions exhibit higher penetration, driven by concentration of Gen Z and Millennial users. Rural adoption lags but is accelerating via financial-literacy initiatives and improved broadband coverage. Federal Reserve policy directly influences platform revenue through margin rates and cash sweep yields. Tightening cycles expand net-interest income, while easing phases intensify competition for order flow. Meanwhile, cybersecurity statutes enacted in California and New York impose stricter breach-notification and vendor-risk standards, pushing nationwide firms to elevate baseline controls.

International expansion by US platforms remains measured. Europe’s progression toward T+1 by 2027 and debates in Asia over best-execution parity may ease cross-border scaling. However, data-localization laws and divergent stances on crypto custody constrain full-feature replication abroad. Partnerships with local broker-dealers or acquisition of licensed entities are emerging as preferred entry modes. Conversely, foreign platforms eyeing US entry face high compliance thresholds, especially around pattern-day-trading rules and consolidated audit-trail reporting.

Competitive Landscape

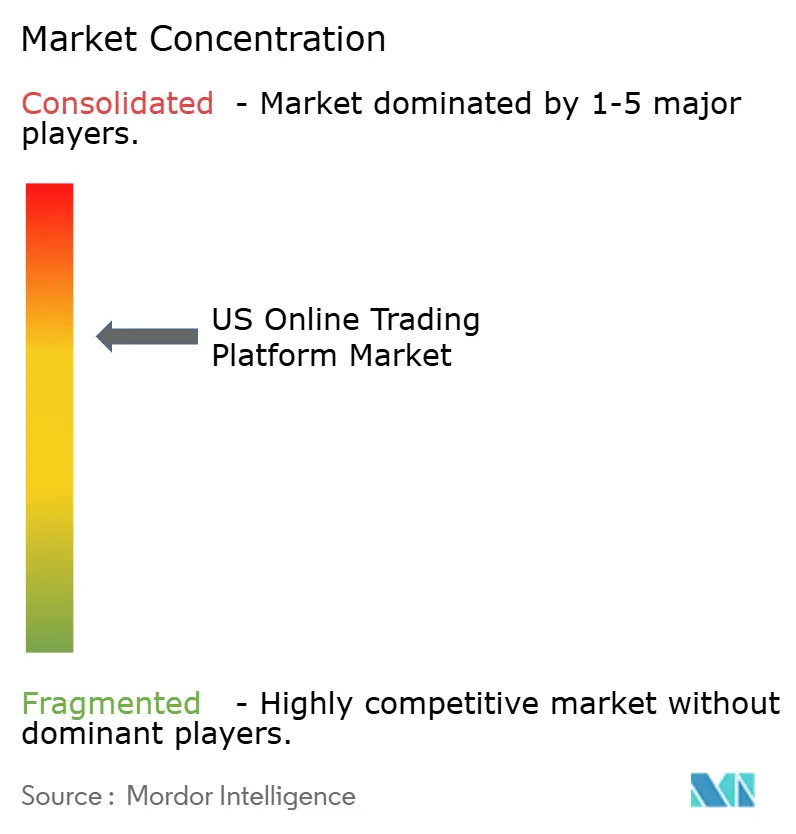

Market structure is moderately concentrated, with the five largest providers controlling a substantial portion of assets yet leaving room for niche innovators. Charles Schwab manages USD 10.1 trillion in client assets and Fidelity USD 13.7 trillion, leveraging scale to offset fee compression. Interactive Brokers competes through low-cost margin lending and global exchange connectivity. Consolidation continues, illustrated by Schwab’s absorption of TD Ameritrade, which unified technology stacks and broadened product coverage.

Strategic plays revolve around vertical integration—banking, advisory, and payments—aimed at lifting customer lifetime value and reducing churn. Simultaneously, horizontal diversification into crypto, futures, and prediction markets addresses asset-class migration. Schwab’s rollout of 24/5 trading and Interactive Brokers’ stock split both target liquidity expansion and retail share-of-wallet. Technology spending prioritizes AI-driven personalization, with natural-language trade assistants and anomaly-detection engines reducing support costs.

Regulation is reshaping competitive moats. Firms with robust compliance automation can onboard emerging products faster, creating time-to-market advantages. Conversely, rising fixed costs push smaller players toward white-label arrangements or niche specialization such as community-based ESG portfolios. Emerging entrants emphasize social-trading overlays but must contend with potential IOSCO rules limiting engagement gamification. In summary, scale, breadth of asset coverage, and compliance agility define positioning in the evolving US online trading platform market.

United States Online Trading Platform Industry Leaders

Fidelity Investments Institutional Operations Company, Inc.

The Charles Schwab Corporation

Interactive Brokers LLC

Merrill Lynch, Pierce, Fenner and Smith Inc. (Bank of America Corporation)

E*TRADE LLC (Morgan Stanley)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Interactive Brokers announced a 4-for-1 stock split to improve share accessibility and broaden its investor base.

- May 2025: Charles Schwab expanded 24-hour trading for retail clients via thinkorswim, adding hundreds of ETFs and demonstrating demand for round-the-clock liquidity.

- March 2025: The SEC established a dedicated Crypto Task Force to draft comprehensive digital-asset guidelines, signaling forthcoming clarity on custody, disclosures, and market-structure obligations.

- February 2025: FINRA released its 2025 Regulatory Oversight Report outlining heightened focus on cybersecurity threats, third-party vendor governance, and after-hours trading controls.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States online trading platform market as the yearly gross revenue earned by purpose-built digital interfaces, mobile, desktop, or web, that let retail and institutional investors place, manage, and settle trades in securities, forex, crypto, and listed derivatives through FINRA-registered intermediaries. Coverage spans licensed brokerage software, white-label portals, and related SaaS support fees.

Scope Exclusion: Pure payment gateways, stand-alone robo-advisory portfolios lacking self-directed order entry, and hardware terminals are left out.

Segmentation Overview

- By Offerings

- Platforms

- Services

- By Deployment Mode

- Cloud

- On-Premises

- By Type

- Beginner-focused Platforms

- Advanced-trader Platforms

- By Interface

- Mobile App

- Desktop

- By End-user

- Retail Investors

- Institutional Investors

Detailed Research Methodology and Data Validation

Primary Research

We spoke with brokerage CTOs, cloud-hosting partners, compliance officers, and frequent traders across the Northeast, Sunbelt, and Pacific regions to verify fee structures, active-user ratios, and mobile engagement patterns. We then reconciled those insights with desk findings.

Desk Research

Mordor analysts compiled macro and micro indicators from the SEC's 13F filings, FINRA account-opening reports, Federal Reserve Financial Accounts tables, SIFMA trade-volume dashboards, and Bureau of Labor Statistics ICT wage series. Regulatory dockets and consumer tech surveys enriched our demand lens. Paid utilities such as D&B Hoovers for vendor revenues and Dow Jones Factiva for press analytics anchored company-level baselines. This list is illustrative; many other authoritative feeds supported data collection and validation.

Market-Sizing & Forecasting

One top-down pass converts FINRA active account counts into a demand pool, multiplies by average revenue per account, and adjusts for trade-volume elasticity plus margin-interest spreads. Select bottom-up cross-checks, sampled supplier revenues and app-store monetization data, flag outliers and guide tweaks. Key variables include smartphone trading share, average daily equity volume, cloud-migration rates, regulatory fee schedules, and disposable personal income. Forecasts are generated through multivariate regression blended with scenario analysis to capture shifts in interest rates and crypto adoption. Parameters are stress-tested with interview consensus.

Data Validation & Update Cycle

Outputs pass three layers of review: automated variance scans versus historical series, peer review by senior analysts, and re-contact of sources when deviations exceed five percent. Reports refresh every twelve months, with mid-cycle patches for material events.

Why Mordor's US Online Trading Platform Baseline Commands Reliability

Published values diverge because providers mix geographies, bundle ancillary software, or rely on opaque fee assumptions. For instance, one external publisher pegs 2024 US revenues at USD 12.5 billion by folding in clearing-house software and robo-advisory assets. Another source posts a 2024 baseline of USD 3.0 billion yet rolls the figure forward from 2019 without adjusting for surging mobile trades. Our disciplined scope, annual refresh, and dual-approach modeling keep estimates transparent and repeatable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.41 B (2025) | Mordor Intelligence | Scope and assumptions fully disclosed |

| USD 12.5 B (2024) | Global Consultancy A | Bundles clearing software and robo-advice assets |

| USD 3.0 B (2024) | Regional Consultancy B | Rolls forward historic CAGR, omits mobile monetization shift |

These contrasts show that once scope creep and outdated baselines are stripped away, Mordor delivers a balanced reference point anchored to observable user counts and disclosed fee yields.

Key Questions Answered in the Report

What is the current size of the US online trading platform market?

The market stands at USD 3.61 billion in 2026 and is projected to reach USD 4.82 billion by 2031.

Which segment is growing fastest within the US online trading platform market?

Cloud deployment leads growth at a 9.27% CAGR as platforms migrate to scalable, compliance-ready infrastructure.

How are commission-free models funded?

Platforms rely on payment-for-order-flow rebates, net-interest income from cash balances, and premium subscription services to offset zero-commission execution.

Why is desktop usage rising after years of mobile dominance?

Serious traders favor larger displays and advanced analytics available on desktop platforms, which support multi-monitor setups and low-latency data feeds.

What regulatory changes will impact platforms most through 2031?

FINRA fee increases, SEC oversight of AI deployment, and T+1 post-trade settlement deadlines constitute the most significant cost and technology pressures.

How concentrated is the competitive landscape?

The top five firms control slightly above 70% of assets, indicating moderate concentration with room for specialized entrants that can navigate regulatory hurdles effectively.

Page last updated on: