US Evidence Management Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Growth Rate | 11.91% CAGR |

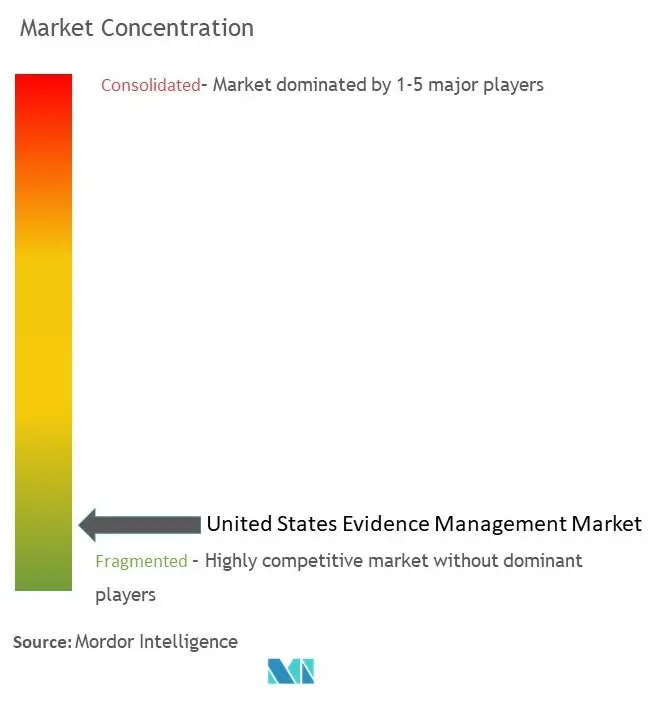

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Evidence Management Market Analysis by Mordor Intelligence

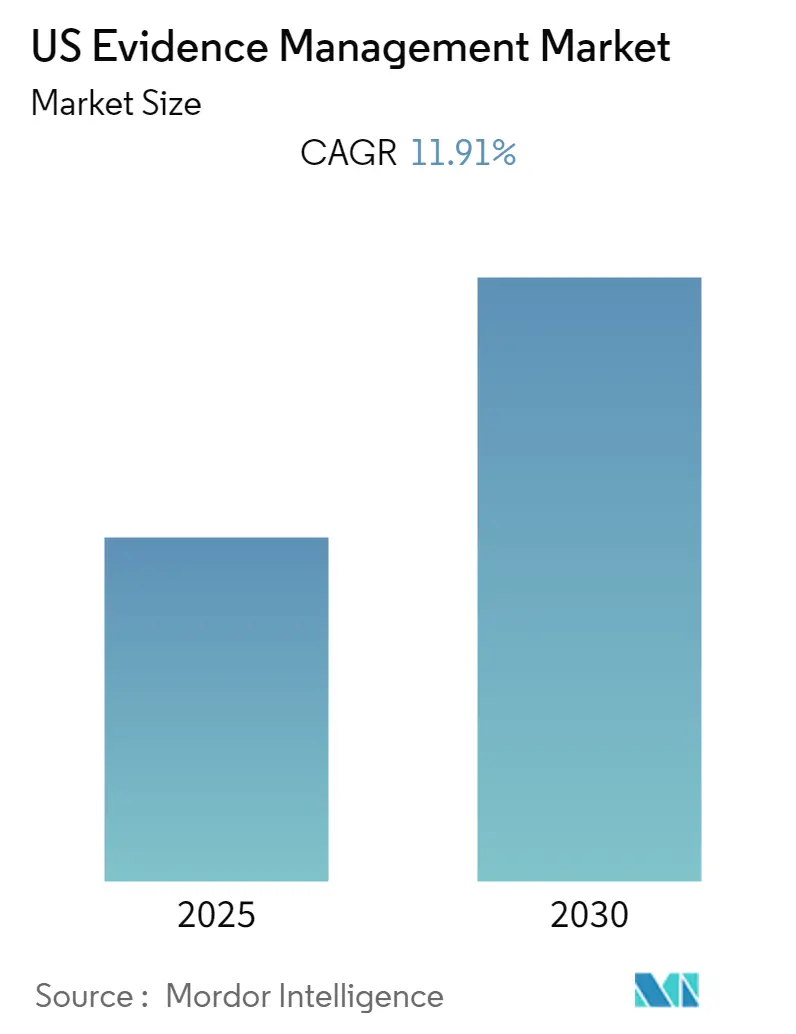

The US Evidence Management Market is expected to register a CAGR of 11.91% during the forecast period.

The digital evidence management landscape is undergoing a fundamental transformation as organizations move away from traditional spreadsheet-based systems toward centralized digital repositories. This shift is driven by the exponential growth in digital evidence sources, including smartphones, surveillance cameras, and social media platforms. The integration of artificial intelligence (AI) and machine learning (ML) capabilities has revolutionized evidence processing, enabling automated data classification, facial recognition, and object detection. According to Federal Trade Commission data, consumers reported losing approximately USD 8.8 billion to fraud in 2022, highlighting the critical need for advanced digital evidence management solutions to combat sophisticated criminal activities.

Cloud-based evidence management systems have emerged as the cornerstone of modern law enforcement operations, offering enhanced accessibility, scalability, and cost-effectiveness. The Department of Justice demonstrated its commitment to modernizing evidence management by announcing more than USD 370 million in grant awards in October 2022, supporting law enforcement operations and evidence-based strategies. These investments have accelerated the adoption of body-worn cameras, digital evidence management systems, and advanced analytics platforms, enabling law enforcement agencies to streamline their operations and improve investigation efficiency.

Smart surveillance technologies are revolutionizing public safety through the integration of IoT-enabled devices and advanced analytics. The implementation of smart streetlights equipped with cameras, microphones, and sensors is enhancing urban security by collecting real-time data on traffic, accidents, and criminal activities. In Seattle alone, there were 739 confirmed criminal shootings and rounds fired in 2022, representing a 19% increase from the previous year, emphasizing the growing importance of comprehensive surveillance and digital evidence storage systems.

The industry is witnessing a significant shift toward integrated evidence management platforms that combine physical and digital evidence handling capabilities. These solutions incorporate advanced features such as automated chain of custody tracking, secure cloud storage, and sophisticated analytics tools. Law enforcement agencies are increasingly adopting these platforms to manage the growing volume of digital evidence, including body-worn camera footage, surveillance videos, and electronic communications. The evolution of open architecture technologies and enhanced processing power has enabled seamless integration between different forensic evidence management systems, improving operational efficiency and investigation outcomes.

Worldwide, activity is shaped by contributions from multiple countries and regions, with United states representing one among them. The global report on evidence management market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

US Evidence Management Market Trends and Insights

Rising Crime Rates Globally Lead to Market Expansion

The increasing crime rates across the United States have created an urgent need for sophisticated evidence documentation systems to handle the growing volume of criminal cases and associated evidence. According to the Seattle Police Department, overall crime increased by 4% in 2022 compared to 2021, with a total of 49,577 violent and property and evidence offenses reported. The violent crime rate in Seattle climbed to 736 per 100,000 people in 2022 from 729 per 100,000 in 2021, while property crime rates rose from 5,730 to 5,784 per 100,000. This surge in criminal activities has led to a significant increase in digital evidence collection from various sources, including surveillance cameras, body-worn cameras, and other digital devices, necessitating robust police evidence management solutions.

The escalating complexity of criminal investigations is further demonstrated by the rise in serious crimes, with Seattle recording 52 homicides in 2022, marking the second-highest number after 2020, and a 19% increase in confirmed criminal shootings and rounds fired incidents, totaling 739 cases. In response to these challenges, the Department of Justice announced more than $370 million in grant awards in October 2022 to fund state, local, and Tribal crime reduction efforts and evidence-based strategies. These investments support critical initiatives such as training programs for improving resilience and wellness, funding body-worn camera programs, and enhancing public safety while expanding community engagement. Law enforcement agencies across the country are increasingly adopting law enforcement evidence management systems to efficiently collect, store, and analyze the enormous volume of digital recordings and evidence generated from these incidents, making it an essential tool in modern law enforcement operations. The adoption of advanced evidence documentation solutions is crucial in addressing the challenges posed by rising crime rates.

Segment Analysis: By Deployment

Cloud Segment in US Evidence Management Market

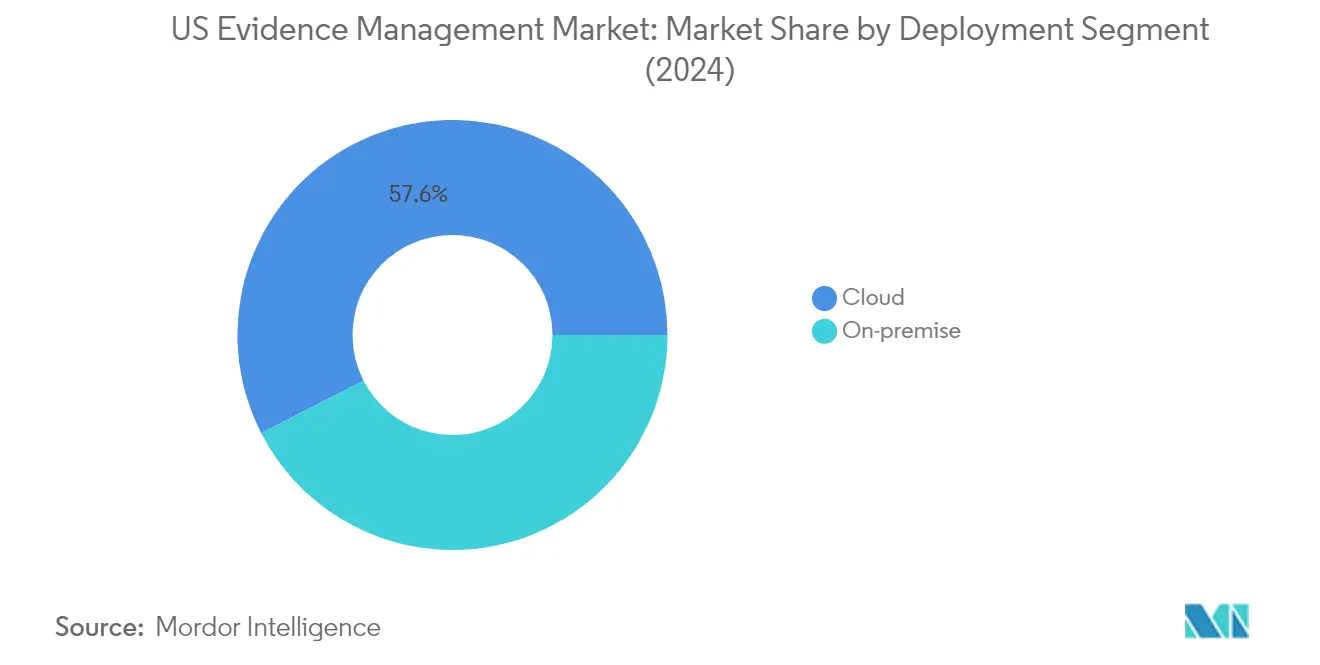

The cloud segment has emerged as the dominant force in the US evidence management market, commanding approximately 58% of the market share in 2024. This segment's prominence is driven by its ability to provide extensive digital evidence management and search capabilities, allowing users to efficiently organize and search through massive volumes of digital evidence. Cloud platforms enable seamless attachment of metadata like timestamps, geolocation, file traits, and tags to evidence files, facilitating easy categorization and retrieval of specific evidence when needed. The segment's growth is further propelled by its superior integration capabilities with existing law enforcement and legal department systems, including body-worn cameras, CCTV systems, forensic analysis tools, and case management systems. Cloud-based evidence management solutions offer organizations the benefit of enterprise-grade video security while minimizing their security infrastructure's physical footprint. The segment is experiencing the fastest growth with a projected growth rate of approximately 12% from 2024-2029, driven by factors such as technological advancements, integration with digital forensics tools, scalability, and cost-effectiveness.

On-Premise Segment in US Evidence Management Market

The on-premise segment continues to maintain a significant presence in the US evidence management market, offering organizations greater control over their evidence management infrastructure. This deployment model involves implementing evidence management systems within an organization's physical infrastructure, with software and hardware installed and operated on the premises. The segment's value proposition lies in its ability to offer enhanced customization and integration capabilities with existing platforms, allowing organizations to modify evidence management software to meet their unique requirements. On-premise solutions are particularly appealing to organizations that prioritize direct control over their data security and compliance measures. The segment has adapted to modern requirements by incorporating advanced digital evidence capture technology, supporting various formats including photos, videos, and audio recordings from modern cameras, video recorders, body-worn cameras, and drones.

Segment Analysis: By Component

Software Segment in US Evidence Management Market

The software segment maintains its dominant position in the US evidence management market, commanding approximately 50% of the market share in 2024. This segment's prominence is driven by the increasing adoption of digital evidence management solutions that enable police departments to efficiently control digital and physical evidence through paperless systems. The software solutions employ advanced barcode technology for initiating and managing the chain of custody, eliminating traditional tickler files and enabling automated alerts for overdue checkouts and notifications. Modern evidence management software leverages cloud technology for secure data storage and allows users to access the system from the field, enabling officers to capture images and videos, record interviews, and enter driver's license barcodes into the system directly from crime scenes. The segment's growth is further supported by the integration of artificial intelligence and machine learning capabilities, which enhance evidence processing, analysis, and management efficiency.

Services Segment in US Evidence Management Market

The services segment is projected to experience the highest growth rate of approximately 14% during the forecast period 2024-2029. This accelerated growth is attributed to the increasing demand for specialized services such as investigation and consulting, system integration, support and maintenance, and training and education. Evidence management service providers offer crucial expertise in structured investigations, helping organizations track problem sources and enhance evidence processes. The segment's expansion is also driven by the growing need for comprehensive training services that help staff develop essential skills in managing modern evidence systems. These services extend beyond initial implementation, offering ongoing support and training to organizations maintaining yearly maintenance contracts. The rise in complex digital evidence handling requirements and the need for expert guidance in implementing and optimizing evidence management systems further contribute to the segment's rapid growth.

Remaining Segments in Component Segmentation

The hardware segment represents a crucial component of the evidence management market, encompassing essential tools such as body-worn cameras, vehicle dash cameras, citywide cameras, and public transit video systems. This segment plays a vital role in evidence collection and documentation, providing law enforcement agencies with the physical infrastructure needed for comprehensive evidence gathering. The hardware components are continuously evolving with technological advancements, incorporating features like improved video quality, enhanced storage capabilities, and better integration with software systems. The segment's importance is underscored by its role in providing tangible tools that form the foundation of modern evidence collection and management practices.

Competitive Landscape

Top Companies in US Evidence Management Market

The US evidence management market features prominent players like NICE Ltd, IBM Corporation, Oracle Corporation, Hitachi Vantara, and Panasonic Corporation leading the competitive landscape. These companies are actively pursuing product innovation through the integration of advanced technologies like artificial intelligence, machine learning, and cloud computing into their evidence management solutions. Strategic partnerships and collaborations with law enforcement agencies and government bodies have become crucial for market expansion. Companies are focusing on developing comprehensive digital evidence management platforms that can handle multiple evidence types while ensuring data security and chain of custody. The market is witnessing increased investment in research and development to enhance software capabilities, improve user interfaces, and provide seamless integration with existing systems. Operational agility is being achieved through cloud-based solutions and flexible deployment options, allowing companies to better serve the evolving needs of law enforcement and judicial organizations.

Market Dominated by Technology Conglomerates and Specialists

The US evidence management market exhibits a fragmented competitive structure with a mix of global technology conglomerates and specialized evidence management solution providers. The larger technology companies leverage their extensive resources, established infrastructure, and deep expertise in data management to offer comprehensive evidence management solutions integrated with their broader portfolio of products. These companies benefit from existing relationships with government agencies and law enforcement organizations, while specialized players differentiate themselves through focused solutions and domain expertise in forensics and evidence handling.

The market is experiencing active consolidation through mergers and acquisitions, as larger players seek to expand their capabilities and market presence. Companies are acquiring specialized software providers and startups to enhance their technological capabilities, particularly in areas such as digital evidence processing, video analytics, and cloud-based evidence management. Strategic partnerships between hardware manufacturers and software providers are becoming increasingly common, creating integrated solutions that address the full spectrum of evidence management needs. The competitive dynamics are further shaped by the entry of new players bringing innovative solutions, particularly in areas such as artificial intelligence-powered analytics and cloud-based evidence management platforms.

Innovation and Integration Drive Market Success

Success in the US evidence management market increasingly depends on providers' ability to deliver comprehensive, integrated solutions that address the complex needs of law enforcement agencies and judicial systems. Companies must focus on developing scalable platforms that can handle the growing volume and variety of digital evidence while ensuring compliance with evolving regulatory requirements. The ability to provide seamless integration with existing law enforcement systems, body-worn cameras, and other evidence collection devices is becoming crucial for market success. Vendors need to invest in robust cybersecurity measures and maintain strict chain of custody protocols to build trust with end-users.

For new entrants and smaller players, success lies in identifying and addressing specific market niches or technological gaps in the current evidence management ecosystem. Companies must develop specialized capabilities in areas such as video analytics, mobile evidence collection, or cloud-based storage solutions to differentiate themselves from established players. The market's future will be shaped by the ability to adapt to changing regulatory requirements, particularly around data privacy and evidence handling protocols. End-user concentration in government and law enforcement sectors necessitates building strong relationships and understanding of specific organizational needs, while also maintaining flexibility to address varying requirements across different jurisdictions and agency sizes. Additionally, the integration of a forensic management system can enhance the precision and reliability of evidence documentation processes.

US Evidence Management Industry Leaders

NICE Ltd

Omnigo Software LLC (QueTel Corporation)

Open Text Corporation

Hitachi Vantara LLC (Hitachi Ltd)

Panasonic Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2023: Motorola Solutions announced the launch of its advanced V700 body camera with mobile broadband capabilities to give public safety agencies another critical source of real-time field intelligence and collaboration. Critical evidence might be recovered after an incident even if a recording was not initiated through the Record-After-The-Fact feature. AI may be applied during evidence analysis to transcribe footage for a clear record of events.

- April 2023: Axon Enterprise Inc. announced the launch of an advanced body-worn camera (BWC), the Axon Body 4 (AB4). The product is a communications beacon that enables law enforcement to live stream their situations intuitively.

US Evidence Management Market Report Scope

Evidence management is the control and administration of evidence related to an event so that it can be used to prove the event's circumstances to all stakeholders involved. The study analyzes the factors driving and challenging the adoption of evidence management systems, covering all physical tools, software for record-keeping, and services involved in installing and upkeep an evidence management system in the United States.

The United States evidence management market is segmented by deployment (on-premise and cloud) and by component (hardware (body-worn camera, vehicle dash camera, citywide camera, and public transit video) and software (services (consulting, training, and support)). The market sizes and forecasts are provided in terms of value in USD for all the segments.

| On-premise |

| Cloud |

| Hardware | Body-worn Camera |

| Vehicle Dash Camera | |

| Citywide Camera | |

| Public Transit Video | |

| Software | |

| Services (Consulting, Training, and Support) |

| By Deployment | On-premise | |

| Cloud | ||

| By Component | Hardware | Body-worn Camera |

| Vehicle Dash Camera | ||

| Citywide Camera | ||

| Public Transit Video | ||

| Software | ||

| Services (Consulting, Training, and Support) | ||

Key Questions Answered in the Report

What is the current US Evidence Management Market size?

The US Evidence Management Market is projected to register a CAGR of 11.91% during the forecast period (2025-2030)

Who are the key players in US Evidence Management Market?

NICE Ltd, Omnigo Software LLC (QueTel Corporation), Open Text Corporation, Hitachi Vantara LLC (Hitachi Ltd) and Panasonic Corporation are the major companies operating in the US Evidence Management Market.

What years does this US Evidence Management Market cover?

The report covers the US Evidence Management Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the US Evidence Management Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: