Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

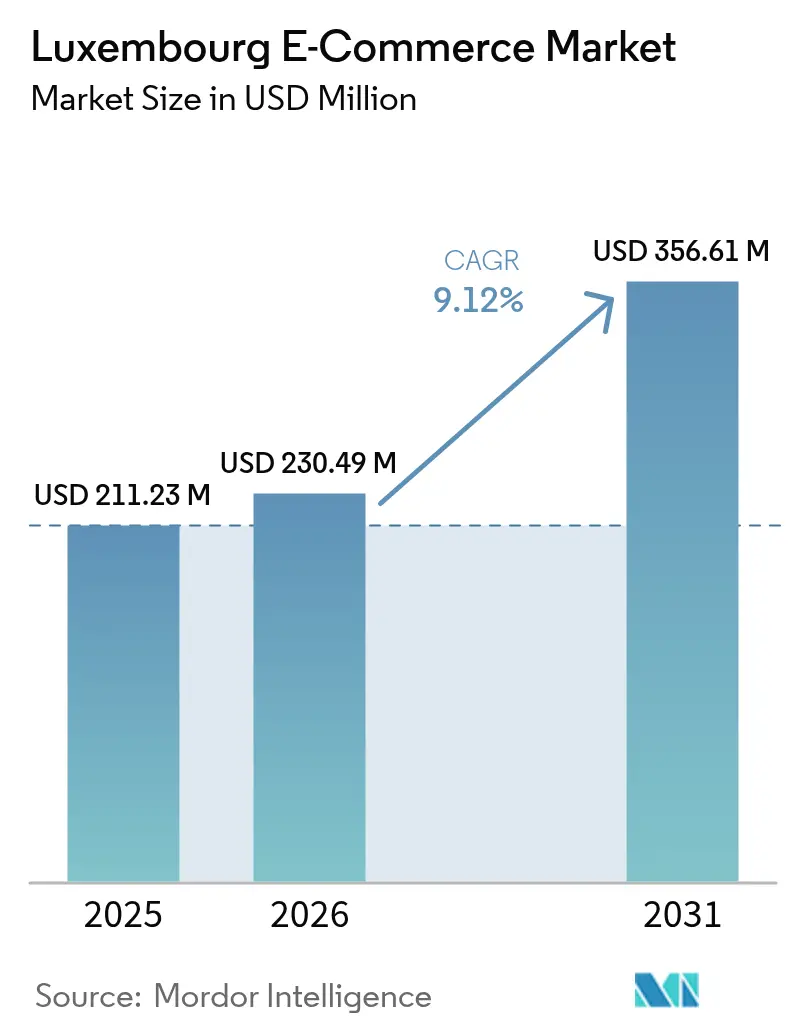

| Base Year Market Size (2025) | USD 211.23 Million |

| Market Size (2026) | USD 230.49 Million |

| Market Size (2031) | USD 356.61 Million |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

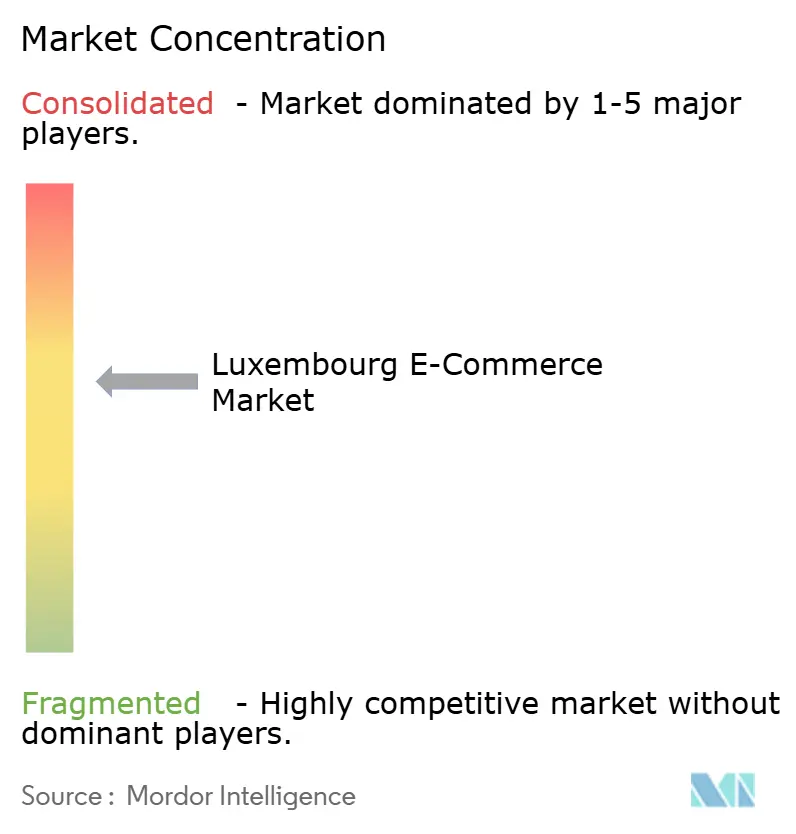

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Luxembourg E-Commerce Market Analysis by Mordor Intelligence

The Luxembourg e-commerce market size is expected to grow from USD 211.23 million in 2025 to USD 230.49 million in 2026 and is forecast to reach USD 356.61 million by 2031 at 9.12% CAGR over 2026-2031. Consistent cross-border purchasing—now 88% of all online transactions—magnifies addressable demand while leveraging the EU Digital Single Market rules that eliminate geo-blocking and simplify VAT settlement. Corporate tax relief from 17% to 16% in 2025 strengthens the country’s appeal as a regional headquarters location for digital merchants. Rapid 5G and fibre deployment, now covering 99.60% and 94.70% of the population respectively, underpins mobile-first shopping journeys and real-time logistics coordination. [1]Gouvernement du Grand-Duché de Luxembourg, “Digital Decade: National Strategic Roadmap for Luxembourg,” gouvernement.lu Meanwhile, the EU Packaging and Packaging Waste Regulation (PPWR) forces retailers to redesign fulfilment and invest in recyclable materials, adding cost pressures yet opening innovation niches for reusable packaging providers. [2]European Parliament, “New EU Rules to Reduce, Reuse and Recycle Packaging,” europarl.europa.eu Intensifying fintech adoption—exemplified by Wero’s rollout—compresses checkout friction, speeds settlements, and accelerates wallet usage.

Key Report Takeaways

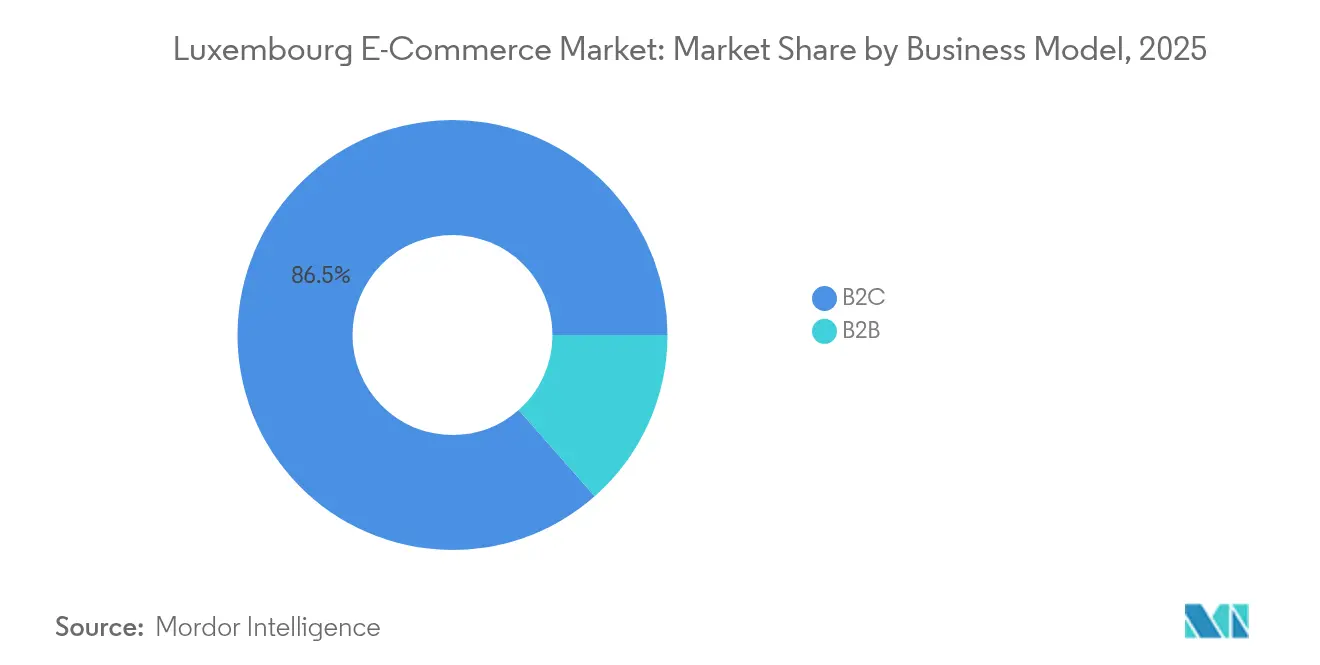

- By business model, the B2C segment held 86.50% of the Luxembourg e-commerce market share in 2025, while B2B is forecast to expand at a 11.85% CAGR through 2031.

- By device, desktop and laptop commanded 63.20% of the Luxembourg e-commerce market size in 2025; smartphone/mobile usage is advancing at a 12.95% CAGR to 2031.

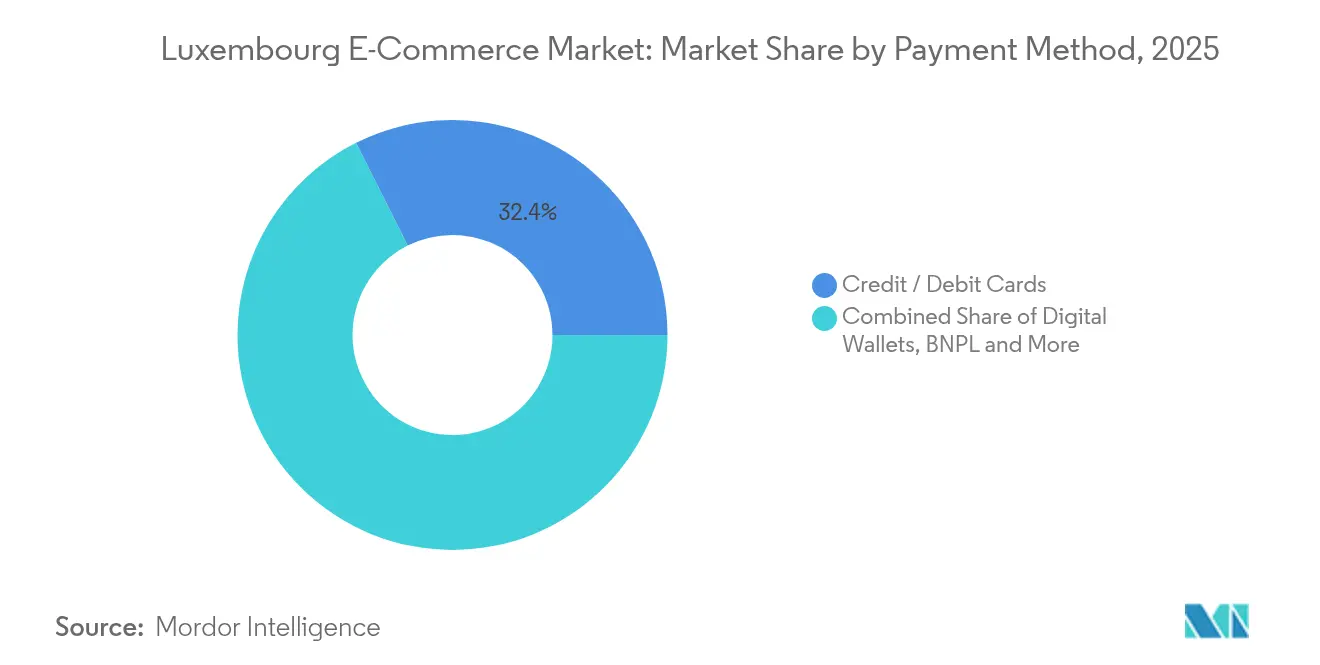

- By payment method, credit/debit cards led with 32.40% revenue share in 2025, whereas digital wallets record the fastest 13.98% CAGR outlook to 2031.

- By B2C product category, fashion and apparel accounted for a 28.30% share of the Luxembourg e-commerce market size in 2025, but food and beverages is growing at a 13.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Luxembourg E-Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ubiquitous high-speed fibre and 5G coverage | +1.8% | National, with spillover to Greater Region | Medium term (2-4 years) |

| EU Digital Single Market compliance pressure | +1.2% | EU-wide, concentrated in Luxembourg | Short term (≤ 2 years) |

| Explosive rise of cross-border shoppers (≳80%) | +2.4% | Luxembourg-centric, extending to neighboring markets | Long term (≥ 4 years) |

| Fintech-led instant-payment rails (Payconiq, SEPA Inst) | +1.5% | Benelux region, expanding EU-wide | Medium term (2-4 years) |

| Government-backed "LetzShop.lu" omni-channel push | +0.8% | National, with cross-border merchant integration | Short term (≤ 2 years) |

| Corporate tax incentives attracting e-commerce HQs | +1.9% | Luxembourg-focused, regional operational impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ubiquitous high-speed fibre and 5G coverage

Nation-wide 5G and fibre availability ensures uninterrupted mobile browsing and supports advanced features such as augmented-reality try-ons that fashion platforms use to trim return rates. Instant loading times lower bounce rates for cross-border shoppers, boosting conversion on marketplaces serving Luxembourg customers. Elevated bandwidth also encourages video-rich product pages that historically slowed legacy sites. Seamless connectivity lets retailers push dynamic pricing in real time, reflecting currency movements relevant to German or French listings that Luxembourg residents view. Logistics orchestration benefits, too: last-mile couriers receive live rerouting instructions, trimming failed deliveries and carbon footprints.

EU Digital Single Market compliance pressure

Harmonised rules allow platforms to operate one storefront across the bloc, erasing friction previously caused by fragmented VAT, data-privacy or geo-blocking constraints. Luxembourg merchants exploit this policy clarity to scale into neighbouring countries without bespoke integrations. Mandatory accessibility upgrades effective June 2025 widen addressable demand among disabled users, though compliance spend rises. Electronic invoicing obligations, phased in by 2030, standardise audit trails and cut manual errors, accelerating cross-border refunds. eIDAS 2.0 digital identities further lift trust, especially for first-time international shoppers wary of fraud.

Explosive rise of cross-border shoppers (≳80%)

A limited domestic SKU pool propels residents toward German, French and Chinese platforms, giving Luxembourg the highest cross-border purchase ratio in Europe. This habit boosts parcel volumes funneled through Luxembourg Airport’s cargo hub and Post Luxembourg’s PackUp lockers, which already handle 21% of parcels. Heavy reliance on neighbouring corridors intensifies negotiations with DHL Express, which is expanding facilities and targeting net-zero emissions by 2050. Cross-border habits also condition consumers to expect sophisticated language tailoring and multi-currency displays, compelling domestic SMEs to adopt enterprise-grade localisation tools. Payment preferences converge on pan-EU wallets that bypass FX fees, reinforcing ecosystem lock-in for Wero.

Fintech-led instant-payment rails (Payconiq, SEPA Inst)

The European Payments Initiative’s acquisition of Payconiq places Luxembourg at the epicentre of SEPA-instant innovation, enabling real-time B2C and B2B settlements. Instant disbursement mitigates cash-flow strain on SMEs awaiting card clearing, encouraging them to widen SKU assortments. For shoppers, one-click checkout inside Wero or Digicash slashes cart-abandonment tied to 3-D Secure friction. Merchant service fees decline relative to scheme cards, which helps offset rising packaging-compliance costs. Rapid settlement further supports cross-border subscription commerce models, which rely on predictable receivables.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High fulfilment costs for last-mile in micro-state | -1.4% | Luxembourg-specific, affecting cross-border logistics | Medium term (2-4 years) |

| Shrinking bricks-and-mortar retail base limiting click-and-collect nodes | -0.9% | Urban Luxembourg, with rural spillover effects | Short term (≤ 2 years) |

| Stricter EU sustainability packaging rules | -1.1% | EU-wide, concentrated compliance costs in Luxembourg | Short term (≤ 2 years) |

| Dependence on foreign logistics corridors (DE, BE, FR) | -0.7% | Regional, affecting Luxembourg's supply chain resilience | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High fulfilment costs for last-mile in micro-state

Low population density yields sub-optimal drop densities, inflating unit delivery costs compared with urbanised neighbours. PackUp lockers trim costs but still require customers to self-collect, limiting usefulness for bulky or perishable goods. Electric-van rollout—now 60% of Post Luxembourg’s fleet—cuts emissions yet front-loads capex burdens that smaller carriers lack scale to absorb. Route-optimisation algorithms struggle with cross-border customs windows, particularly when shipments traverse German or Belgian hubs overnight. Start-ups such as B-ON pursue volume manufacturing of e-vans to lower TCO, although commercial adoption depends on sustained parcel growth.

Stricter EU sustainability packaging rules

The PPWR caps empty space at 50% per parcel and mandates recyclability by 2030, forcing retailers to redesign inserts, fillers and box SKUs. Smaller merchants reliant on standardised Amazon FBA cartons face higher penalties for non-compliance than larger multinationals that can invest in right-sizing machinery. Extended Producer Responsibility provisions shift disposal costs up the chain, tightening GM margins. Retailers must build reverse-logistics capacity to recuperate reusable packaging, challenging in a territory where last-mile density is already thin. On the upside, compliance investments could spur competitive differentiation via eco-labels, appealing to Luxembourg’s environmentally conscious shoppers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2B acceleration despite B2C dominance

The B2C segment controlled 86.50% of 2025 revenue, reflecting consumer appetite for international marketplaces and the structural openness of the Luxembourg e-commerce market. B2B transactions, although smaller, are scaling at a 11.85% CAGR as procurement teams adopt digital catalogues and automate invoice flows under e-invoicing mandates. The Luxembourg e-commerce market size for B2B platforms is projected to widen as banks and fund administrators procure IT services online. Tax advantages on qualifying IP income attract SaaS vendors that use the duchy as a base to serve Benelux corporates.

Marketplace convergence is blurring model boundaries: TikTok Shop lets artisans sell D2C while sourcing wholesale from Asian suppliers, creating hybrid flows. Zalando’s ZEOS fulfilment arm, posting 11.6% Q1 2025 B2B revenue growth, demonstrates how consumer-facing giants repurpose infrastructure to monetise brands seeking EU distribution. Strategic anchor tenants further increase warehouse utilisation, improving economies of scale for Luxembourg operators. Collectively, these shifts position the Luxembourg e-commerce market to capture incremental value from enterprise procurement digitalisation.

By Device Type: Mobile surge challenges desktop supremacy

Desktop and laptop retained a 63.20% share in 2025, yet mobile’s 12.95% CAGR signals an impending pivot as 5G eradicates latency barriers. The Luxembourg e-commerce market size attributed to smartphones will surpass legacy channels once streamlined authentication inside digital wallets reaches critical mass. Larger screens remain indispensable for complex cross-border price comparisons, especially for luxury goods. However, impulse-driven categories such as beauty convert predominantly on mobile push notifications timed around salary credit dates.

Augmented-reality fitting rooms embedded in retailer apps elevate fashion conversion, capitalising on Luxembourg’s high disposable income. Amazon’s anticipatory shipping algorithms, protected by US8615473B2, optimise inventory allocation near mobile-heavy cohorts. Tablet and smart-TV shopping remain niche but offer potential for group purchasing in family settings. Continuous scroll UX patterns on mobile shorten the path-to-checkout, raising AOV when paired with BNPL widgets.

By Payment Method: Digital wallets disrupt card dominance

Credit/debit cards held a 32.40% slice of 2025 turnover while digital wallets are scaling at 13.98% CAGR, catalysed by Wero’s SEPA-instant backbone. Luxembourg e-commerce market share for cards is eroding as merchants chase lower MDRs and faster settlement cycles. Wallet ecosystems integrate loyalty points and one-click UX that outclass legacy 3-D Secure flows. BNPL uptake skews toward high-ticket electronics, with default risk mitigated through instant credit-scoring APIs plugged into Luxembourg’s credit bureau.

Merchant acceptance of Digicash widened after the Payconiq acquisition, demonstrating network-effect economics. Stripe and Adyen deploy local acquiring to minimise FX conversions on cross-border purchases, making Luxembourg’s wallet mix diverse yet interoperable. Regulatory sandboxes accelerate pilot programmes such as Joybiiz, automating meal-voucher disbursement for corporate staff. Over time, card networks may reposition as rails for wallet top-ups rather than direct checkout tools.

By B2C Product Category: Food delivery transforms traditional fashion leadership

Fashion and apparel captured 28.30% revenue owing to residents’ preference for German and French fashion portals. Food and beverages, however, is racing ahead at a 13.92% CAGR as urban professionals substitute cooking for delivery convenience. Luxembourg e-commerce market size for meal delivery receives tailwinds from rising minimum wages that boost discretionary spend. Sustainability rules push operators to invest in reusable containers, nudging AOV upward to cover deposit schemes.

Just Eat Takeaway.com’s Northern Europe unit posted EUR 692 million (USD 747 million) revenue in H1 2024, reflecting demand elasticity. Furniture and DIY segments benefit from cross-border price arbitrage, particularly during German VAT holiday periods. Electronics vendors exploit Luxembourg’s multilingual workforce by offering multilingual after-sales chatbots. Regulatory clarity around alcohol delivery opens adjacent growth in premium beverages, provided age-verification APIs are embedded at checkout.

Geography Analysis

Luxembourg’s micro-state geography caps domestic volume yet unlocks the broader Greater Region, encompassing parts of Germany, France and Belgium that collectively account for 60% of EU GDP. Within national borders the Luxembourg e-commerce market relies on 99% internet penetration, reflecting pervasive digital literacy. Cross-border workers, enabled to telework 34 days from home, redirect delivery addresses to residences, boosting B2C parcel density on the German periphery.

Integration with neighbouring customs-free corridors enhances logistics resilience yet creates dependency on foreign network capacity. DHL Express’ sustainability roadmap secures low-emission options for Luxembourg shippers, differentiating service propositions for eco-aware consumers. Payment systems mirror this regional mesh: Wero’s sequential launch across Belgium, France, Germany and now Luxembourg demonstrates how contiguous roll-outs accelerate adoption.

Luxembourg Airport’s cargo centre and river port consolidate inbound flows before final-mile execution. However, last-mile inefficiency persists in rural communes where click-and-collect points are sparse. Government efforts to stimulate domestic platforms via LetzShop.lu attract only 1.4 million visits in 2023, underscoring entrenched preference for international sites. Forward-looking strategies therefore prioritise interoperability with foreign systems rather than import-substitution.

Competitive Landscape

International titans shape purchasing behaviour: Amazon logged USD 638 billion revenue in 2024 with 9% international segment growth, maintaining psychological top-of-mind status in the Luxembourg e-commerce market. [4]Amazon.com, Inc., “Amazon 2024 Annual Report,” s2.q4cdn.com Zalando advanced its ecosystem model, delivering EUR 2.4 billion (USD 2.59 billion) Q1 2025 revenue and securing 91.5% of About You’s shares to consolidate fashion scale. Shopify’s 27% revenue surge signals platform-as-a-service headroom for Luxembourg SMEs lacking home-grown IT teams.

Post Luxembourg repurposed its declining mail network into INFLOW, bundling storage, pick-pack-ship and returns management, thereby capturing value upstream of parcel handoff. Fintech niche players such as Edonys provide specialised benefits wallets, strengthening local service differentiation. Electric-vehicle OEM B-ON pilots scale manufacturing to reduce TCO for last-mile fleets, offering strategic synergy with INFLOW’s sustainability goals.

Competitive strategy gravitates toward vertical integration: Amazon patents anticipatory shipping, Zalando extends fulfilment to third-party brands, and Post Luxembourg internalises e-commerce warehousing. Payment players compete on open-loop wallet interoperability, aiming to pre-empt closed-loop dominance. Regulatory compliance capability—particularly around PPWR and e-invoicing—emerges as a moat, favouring incumbents with legal resources over emerging boutiques.

Luxembourg E-Commerce Industry Leaders

Amazon.com, Inc.

Luxcaddy (Itix S.A.)

LetzShop.lu (État du Luxembourg)

Zalando SE

Shein Group Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Zalando SE logged 6.5% GMV growth to EUR 3.5 billion (USD 3.78 billion) and confirmed FY 2025 guidance, signalling confidence in its ecosystem strategy.

- May 2025: Shopify Inc. achieved USD 2.36 billion Q1 revenue and a 15% free-cash-flow margin, illustrating platform scalability for Luxembourg merchants.

- May 2025: POST Luxembourg unveiled the INFLOW brand to consolidate e-fulfilment services, aiming to retain value threatened by cross-border carriers.

- March 2025: Zalando posted EUR 10.6 billion (USD 11.45 billion) 2024 revenue and announced 4-9% 2025 growth targets, leveraging About You integration for assortment depth.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Luxembourg's e-commerce market as every online merchandise transaction executed by buyers located inside the Grand Duchy with merchants incorporated and taxed in Luxembourg. The value base is net merchandise value expressed in constant 2024 US dollars; it spans retail-facing B2C webshops and domestic B2B portals that invoice goods electronically through local payment rails and fulfillment nodes, capturing orders placed via desktop, mobile, and emerging connected devices. According to Mordor Intelligence, service-only verticals such as travel bookings are tracked separately and do not flow into this merchandise total.

Scope Exclusions: Cross-border purchases settled with merchants registered abroad, peer-to-peer classifieds, and purely digital service platforms (streaming, gaming credits) are left outside the sizing exercise.

Segmentation Overview

- By Business Model

- B2C

- B2B

- By Device Type

- Smartphone / Mobile

- Desktop and Laptop

- Other Device Types

- By Payment Method

- Credit / Debit Cards

- Digital Wallets

- BNPL

- Other Payment Method

- By B2C Product Category

- Beauty and Personal Care

- Consumer Electronics

- Fashion and Apparel

- Food and Beverages

- Furniture and Home

- Toys, DIY and Media

- Other Product Categories

Detailed Research Methodology and Data Validation

Primary Research

Mordor engaged founders of mid-sized webshops, payment aggregators, and last-mile operators across Luxembourg City, Esch, and Ettelbruck. Interviews clarified domestic versus cross-border order splits, average return rates, and adoption of one-click wallets, while short surveys with B2B portal managers validated invoice frequency and blended take-rates. Insights from these dialogues helped us refine assumptions harvested during desk work.

Desk Research

We began with official datasets from STATEC's retail trade panel, Eurostat's Digital Economy tables, Banque centrale du Luxembourg card-payment bulletins, and Post Luxembourg parcel dashboards, which together outline domestic shopper counts, ticket sizes, and shipment flows. Additional context came from industry associations such as the Luxembourg Confederation of Commerce and publicly available filings lodged with the Registre de Commerce et des Sociétés. To anchor company revenues and media sentiment, Mordor analysts tapped D&B Hoovers, Dow Jones Factiva, and Volza import-export snapshots. These examples illustrate the caliber of secondary inputs; many further open-source records were reviewed to substantiate trends and ratios.

Market-Sizing & Forecasting

The baseline is built top-down. Total card and bank-initiated online transaction values are recreated from BCEE and BCL data, then filtered through shopper origin-destination matrices to isolate purchases with locally domiciled merchants. Results are stress-tested with selective bottom-up roll-ups of disclosed webshop revenues and parcel manifests. Key variables like online shopper penetration, average basket value, SME webstore density, VAT OSS filings, and mobile share of visits feed a multivariate regression that projects demand to 2030. Where bottom-up gaps emerge, weighted interpolation aligned to category growth norms closes residual holes.

Data Validation & Update Cycle

Our two-stage analyst review flags any variance above five percent versus independent metrics, prompting re-contact of sources before sign-off. Models refresh each year, and material events (tax changes, logistics strikes) trigger a mid-cycle patch so clients receive the latest calibrated view.

Why Mordor's Luxembourg E-Commerce Baseline Commands Reliability

Published estimates often differ; definitions, inclusion of cross-border turnover, and refresh cadence typically drive the gaps.

Key gap drivers in this market stem from whether foreign-hosted merchants are counted, if values are gross of VAT, and how B2B flows are treated. Mordor's scope focuses on domestically generated merchandise value, excludes imported GMV, and updates annually, whereas many public figures bundle all Luxembourg-origin spending or rely on infrequent household surveys.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 211 m (2025) | Mordor Intelligence | |

| USD 1.14 bn (2024) | Global Consultancy A | Includes consumer spend at foreign webshops; counts gross GMV and VAT |

| USD 1.21 bn (2024) | Industry Database B | Adds cross-border flows and omits B2B separation |

| USD 1.60 bn (2024) | Regional Firm C | Combines B2C, B2B, and C2C and assumes full pass-through of mobile commerce growth |

The comparison shows that once imported transactions and multi-channel overlaps are stripped out, the domestic market is far smaller. By grounding estimates in verifiable payment and registry data, Mordor Intelligence delivers a transparent, reproducible baseline clients can trust for planning and benchmarking.

Key Questions Answered in the Report

What is the current value of the Luxembourg e-commerce market?

It reached USD 230.49 million in 2026 and is forecast to hit USD 356.61 million by 2031.

Which segment is expanding fastest within the Luxembourg e-commerce market?

B2B transactions are growing at a 11.85% CAGR, outpacing the consumer side.

Why is cross-border shopping so dominant in Luxembourg?

Limited domestic assortment, close proximity to large EU neighbours and harmonised Digital Single Market rules mean 88% of online orders originate from foreign platforms.

How will EU packaging regulations affect Luxembourg online retailers?

The PPWR demands fully recyclable packaging and caps empty space, raising compliance costs but creating innovation opportunities in reusable materials.

What payment method is gaining most traction?

Digital wallets such as Wero are scaling at a 13.98% CAGR, eroding the 32.40% share held by traditional cards.

How are local logistics providers responding to rising parcel volumes?

Post Luxembourg launched the INFLOW e-fulfilment brand and expanded PackUp lockers to cut last-mile costs and capture value lost to foreign couriers.

Page last updated on: