Vertical Milling Machine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.30 Billion |

| Market Size (2031) | USD 16.90 Billion |

| Growth Rate (2026 - 2031) | 3.39% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vertical Milling Machine Market Analysis by Mordor Intelligence

The Vertical Milling Machine Market size was valued at USD 13.78 billion in 2025 and is estimated to grow from USD 14.30 billion in 2026 to reach USD 16.90 billion by 2031, at a CAGR of 3.39% during the forecast period (2026-2031).

Purchases are advancing on the back of deliberate capacity additions that target throughput, precision, and uptime rather than speculative expansion cycles. Production floor strategies emphasize single-set-up machining, tighter tolerance control, and automation-ready systems, which together support steady growth in the vertical milling machine market as manufacturers refit lines for aerospace, automotive, energy, and medical applications. Policy-led investment in U.S. manufacturing and energy supply chains is keeping order momentum intact and supporting localization of complex machining programs across North America. OEM consolidation is raising the bar on scale advantages in procurement and R&D, and it is reinforcing the role of end-to-end service and digital support in winning multi-year, multi-site contracts. The vertical milling machine market is also being shaped by the need to relieve skilled labor constraints through embedded intelligence in controls and the scalable use of robotics and pallet systems.

Key Report Takeaways

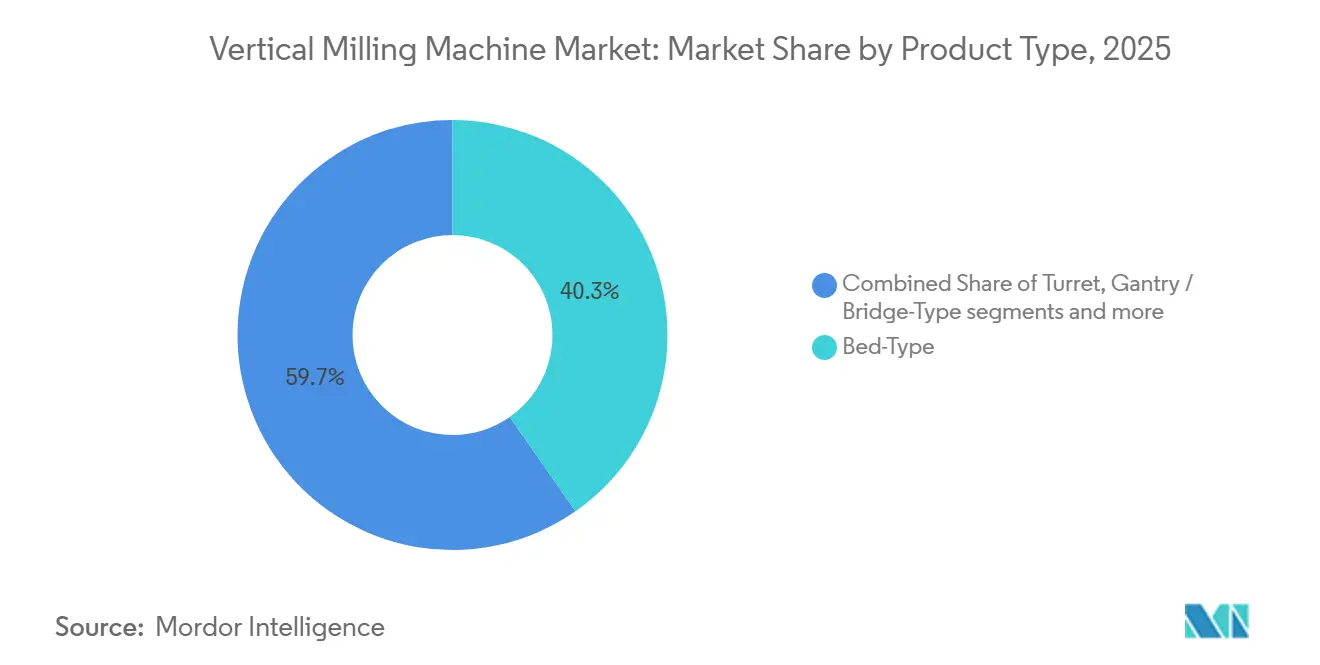

- By product type, Bed-Type led with 40.31% of the vertical milling machine market size in 2025, while Gantry or Bridge-Type posted the fastest segment growth at 4.78% CAGR through 2026-2031.

- By axis configuration, the three-axis commanded 54.78% vertical milling machine market share in 2025, and five-axis and above recorded the highest projected CAGR at 5.61% to 2026-2031.

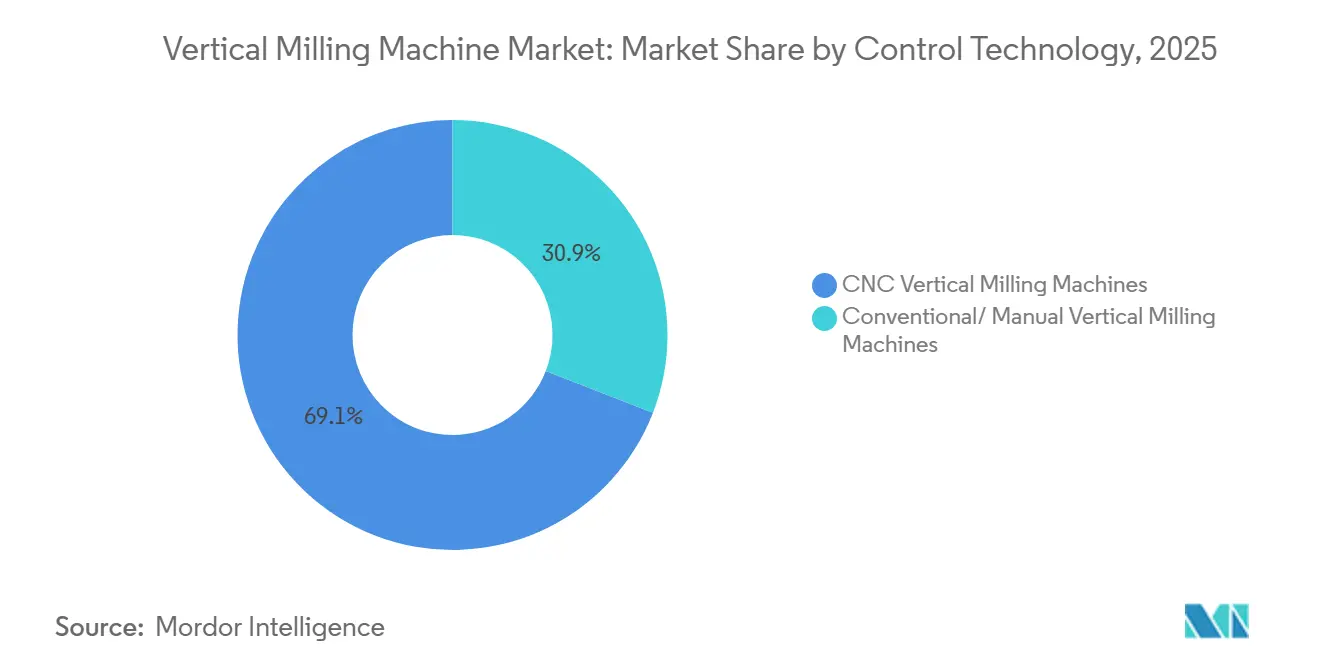

- By control technology, CNC vertical milling machines represented 69.12% of the vertical milling machine market share in 2025 and are projected to expand at a 6.73% CAGR through 2031, the fastest within control technology.

- By end-user industry, automotive accounted for 53.21% of demand in 2025, while aerospace and defense were the fastest growing at 6.12% CAGR through 2026-2031.

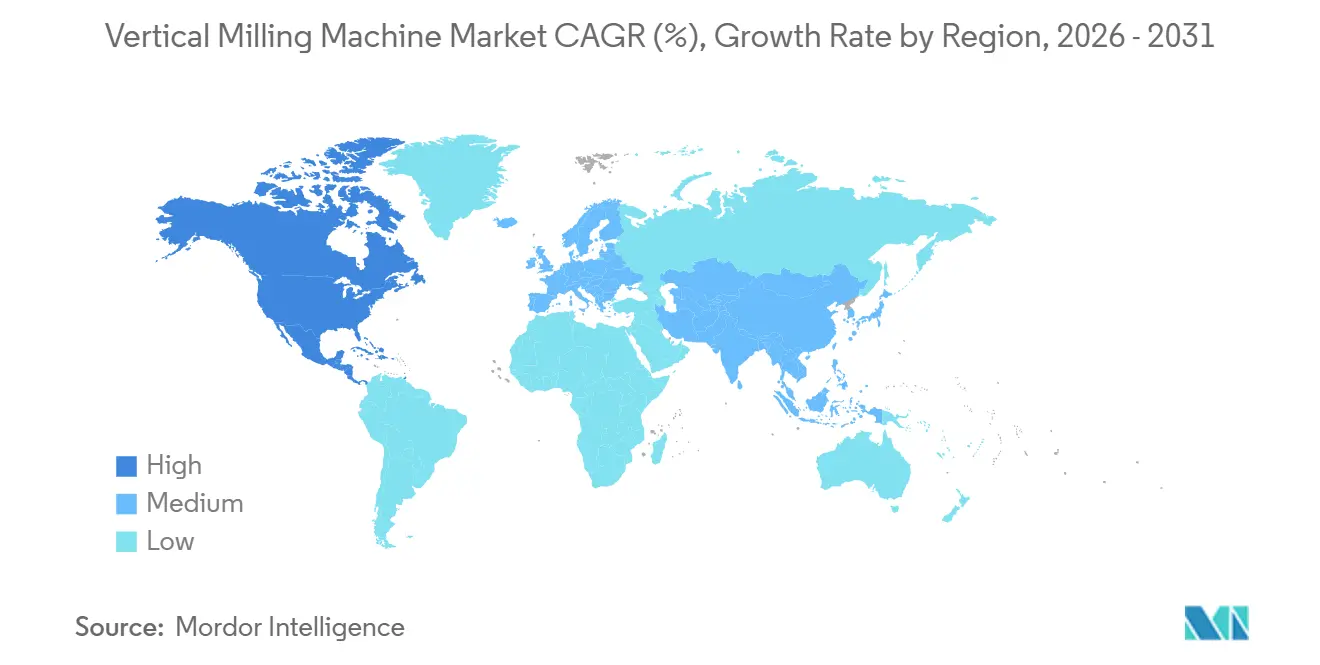

- By geography, Asia-Pacific captured 47.89% in 2025, and North America is projected to grow at the highest regional CAGR of 5.21% through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vertical Milling Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing aerospace and defense manufacturing activity | +1.2% | Global, with concentration in North America, Europe core (France, UK, Germany), APAC (Japan, South Korea) | Medium term (2-4 years) |

| Expansion of automotive lightweighting initiatives | +0.9% | North America, Europe (Germany, Italy), APAC core (China, India, Japan) | Short term (≤ 2 years) |

| Rising demand for precision medical devices and implants | +0.6% | North America (USA dominant), Europe (Germany, Switzerland), APAC (Singapore, South Korea) | Long term (≥ 4 years) |

| Increasing adoption of CNC and multi-axis machining | +1.4% | Global, with early leadership in APAC manufacturing hubs, North America, Western Europe | Short term (≤ 2 years) |

| Growth in contract manufacturing and job shop operations | +0.7% | Global, particularly APAC (China, Vietnam, India), Mexico, and Central Europe | Medium term (2-4 years) |

| Infrastructure development and construction equipment demand | +0.5% | North America, Middle East (Saudi Arabia, UAE), APAC (China, India) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Aerospace and Defense Manufacturing Activity

Aerospace and defense maintain a high requirement for accuracy, repeatability, and uptime that favors single-setup vertical five-axis mills on titanium and high-nickel alloys. Lockheed Martin delivered 191 F-35 aircraft in 2025, demonstrating strong program execution that sustains demand for precision structural parts and landing gear machining capacity. Airbus reported 793 commercial aircraft deliveries in 2025 and targeted 870 deliveries in 2026, while its backlog supported years of production cover that underpins investment in large-format molds, fixtures, and wing tooling for vertical mill cells. Tiered supplier networks are responding by adding capacity in both three-axis and five-axis formats to meet lead time and geometry requirements across airframe, engine, and landing systems. Federal and private investments to strengthen domestic energy and industrial supply chains are also reinforcing U.S. machining infrastructure for dual-use components with higher precision profiles.[1]U.S. Department of Energy, “Progress Update Winter 2025,” energy.gov Together, these forces keep the vertical milling machine market on a steady multi-year footing as aerospace programs scale output, refresh fleets, and maintain complex spares pipelines.

Expansion of Automotive Lightweighting Initiatives

Automakers continue to balance vehicle mass, cost, and performance, which sustains demand for aluminum and advanced steel tooling machined on vertical platforms. The latest SAFE Vehicles Rule III proposal from NHTSA details mass-reduction levels and material strategies that influence die and fixture design, supporting more investment in vertical milling capacity for high-cavity dies and battery component tooling.[2]National Highway Traffic Safety Administration, “The Safer Affordable Fuel-Efficient (SAFE) Vehicles Rule III for Model Years 2022 to 2031 Passenger Cars and Light Trucks,” federalregister.gov OEMs are optimizing closure systems, body structures, and chassis parts, which drives a mix of aluminum and steel dies, and raises the need for quick material changeover and robust vibration control on bed-type systems. Electric vehicle platforms add new machining workloads for motor housings, battery trays, and e-axle components that fit well with high-rigidity vertical setups. The EPA’s 2025 Automotive Trends Report confirms rising average vehicle weight, which maintains urgency around design-driven mass reduction and supports orders for updated dies, fixtures, and precision jigs.[3]U.S. Environmental Protection Agency, “The 2025 EPA Automotive Trends Report,” epa.gov This operating context encourages manufacturers and tier suppliers to secure new vertical milling machine market capacity that addresses both lightweight and heavy-duty tool steels in the same cell.

Rising Demand for Precision Medical Devices and Implants

Medical device programs require stable, high-accuracy vertical platforms that achieve stringent dimensional tolerances and fine surface finishes in titanium and cobalt-chromium. Five-axis vertical mills complete complex contours in fewer setups, which is central to implant geometry control and throughput gains across small and mid-volume runs. CNC machining of medical-grade titanium commonly targets low surface roughness and tight tolerances on features that affect osseointegration and fatigue life, and these needs reinforce investment in premium spindle assemblies and closed-loop thermal compensation. Post-print machining of additively manufactured implants is expanding as device companies scale 3D-printed porous architectures, which places more five-axis vertical mills downstream of printers to finish mating surfaces and critical channels. Hospitals and contract manufacturers are diversifying supply to reduce single-source risk and are placing more emphasis on validation-ready vertical cells with traceable workflows for quality audits. This environment sustains a higher precision baseline that supports the vertical milling machine market in 2026 across orthopedic, spine, and cardiovascular device lines.

Increasing Adoption of CNC and Multi-Axis Machining

Production teams are replacing multi-setup routes with single-setup strategies on vertical platforms to reduce fixturing errors, compress total cycle time, and stabilize quality yield. This adoption trend includes an upgrade path from three-axis to five-axis machines for complex aerospace brackets and orthopedic implants, supported by control advances and integrated probing. Momentum in U.S. manufacturing technology orders through 2025 showed a strong appetite to refresh machining assets and enabled more shops to add automation-ready vertical centers. Control platforms are evolving toward embedded analytics, better toolpath stability, and interfaces that reduce the programming burden for shops moving to simultaneous contouring. As users gain confidence in unattended shifts using pallet systems and robots, the vertical milling machine market benefits from incremental capacity gains without proportional labor additions. The result is a gradual shift of complex geometry work from multi-setup patterns to lights-out cells around vertical five-axis machines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capital investment requirements | -1.1% | Global, more acute in emerging markets (Southeast Asia, Latin America, Africa) | Short term (≤ 2 years) |

| Shortage of skilled machine operators and programmers | -0.8% | North America, Europe (Germany, Italy, UK), Japan | Medium term (2-4 years) |

| Long lead times for machine delivery and installation | -0.5% | Global supply chain impact, concentrated delays in Europe, North America | Short term (≤ 2 years) |

| Competition from alternative machining technologies | -0.3% | APAC (China, South Korea), selective adoption in Europe aerospace hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Investment Requirements

The cost gap between entry-level three-axis vertical mills and large-format five-axis platforms remains material, which segments purchasing by balance sheet and credit access. U.S. manufacturing technology orders set a new monthly record in December 2025 and ended the year up 22.5%, yet the most advanced vertical machines carry high unit prices that require structured financing and multi-year planning. Leasing plays a greater role in closing the access gap, with terms that extend across machine life while preserving working capital and smoothing cash flows. Equipment and software investment growth in 2026 is projected to moderate versus 2025’s surge, which will still support steady replacement cycles but could limit step-ups to five-axis configurations for smaller shops. These financing dynamics keep the vertical milling machine market expanding, but they tilt adoption curves toward phased upgrades and automation add-ons rather than wholesale fleet changes. Cost visibility and total cost of ownership benchmarks are therefore critical to move buyers from trials to multi-cell deployments on vertical platforms.

Shortage of Skilled Machine Operators and Programmers

Operator and programmer shortages continue to constrain throughput even when spindle hours are available, which keeps training and workflow simplification high on the agenda. Investments in training capacity are expanding as automation leaders scale facilities to develop more integrators and technicians for CNC-robotic workcells. Shops are also rebalancing tasks between skilled machinists and automation operators by using probing, offset automation, and standardized workholding to reduce setup variation. Control improvements that simplify five-axis programming are helping alleviate the specialist bottleneck and make advanced vertical machining more accessible to mid-size job shops. These steps allow more lights-out operation on vertical platforms and support near-term productivity gains even when hiring remains difficult. The skills trend reinforces the adoption of automation-ready vertical mills and underpins steady expansion in the vertical milling machine market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Gantry Configurations Address Extreme-Scale Machining While Bed-Type Anchors Volume Production

Bed-Type systems held 40.31% share in 2025 within the vertical milling machine market as users prioritized structural rigidity and vibration damping for heavy, interrupted cuts and large workpieces. That position is reinforced by demand from automotive die lines and aerospace structures, where long travel and stiffness are critical to finish quality across multi-shift operations. These machines anchor production floors that need predictable chip evacuation, thermal stability, and consistent accuracy in tool steels and other hard alloys. The vertical milling machine market also benefits from bed-type platforms that are automation-ready and support palletization, which raises spindle utilization for high-mix schedules. For plants that must switch between aluminum dies and hardened steel tools, bed-type provide a stable base with quick tool changes and process repeatability that fits volume production targets. This stability profile keeps bed-type configurations central to capital planning in 2026 for users seeking a balance of capacity, part size range, and uptime.

Gantry or bridge-type configurations hold a smaller installed base yet posted the fastest growth with a 4.78% CAGR through 2031 as users pursue single-setup machining for extreme-scale parts. Wind turbine hubs, large frames, and long housings make one-setup access valuable, and gantry clearances enable multi-sided milling without re-fixturing. Turret and knee-type remain in play for toolrooms, prototyping, and small-batch jobs that prioritize setup speed and direct manual control. These roles keep the vertical milling machine market diversified across product types, with gantry formats expanding where bridge rigidity and overhead clearance outweigh higher capex. Users are also pairing large vertical mills with automation cells to stabilize throughput and to minimize idle time across large work envelopes. The mix of heavy-duty bed-type cells and expanding gantry work underpins steady share dynamics and a resilient growth path.

By Axis Configuration: Five-Axis Systems Penetrate Production Floors as Programming Barriers Erode

Three-axis machines commanded 54.78% share in 2025 as the most familiar and cost-accessible format across general machining applications in the vertical milling machine market. This installed base remains strong due to simpler programming, abundant operator experience, and a wide ecosystem of tooling and workholding. The format addresses a broad set of parts at attractive cost points and supports automation with pallet changers that can move utilization higher without advanced kinematics. Users with prismatic parts continue to rely on three-axis mills for repeatable, predictable production, which keeps the category central to shop economics. The segment also benefits from control updates that improve stability, toolpath smoothness, and probing workflows that cut setup time.

Five-axis and above configurations were the fastest growing, with a projected 5.61% CAGR through 2031, as shops consolidate multiple setups into one pass to cut defects and compress start-to-finish time in the vertical milling machine market. Aerospace brackets, impellers, and orthopedic implants are among the parts that now move to vertical five-axis cells to gain accuracy, repeatability, and higher throughput. Many users are adopting conversational interfaces and templated toolpaths to lower the programming burden, which helps first-time five-axis buyers migrate from three-axis routes. Four-axis machines remain a practical middle step for indexed milling on multiple faces where full simultaneous contouring is not yet necessary. As confidence grows in unattended shifts on five-axis cells with pallets and robots, shops expand capacity without one-for-one increases in labor. These adoption patterns are contributing to a steady reweighting of the installed base over the forecast period.

By Control Technology: CNC Dominance Coexists with Manual-Vertical Milling Machines Resurgence in Training and Prototyping Niches

CNC Vertical Milling Machines represented 69.12% of the vertical milling machine market share in 2025 and are projected to expand at a 6.73% CAGR through 2031, the fastest within control technology. CNC platforms anchor audited and repeatable production with CAM integration, in-process probing, and traceable workflows that satisfy quality regimes. High stiffness frames, responsive spindle assemblies, and refined control algorithms allow tighter geometries at higher feed rates without loss of stability. Pallet systems, robot tending, and standardized workholding raise spindle utilization and reduce setup variation for multi-shift operations. These features align with programs that prize consistent cycle time, lower scrap, and higher uptime, which supports continued share gains for CNC within the vertical milling machine market.

Conventional or manual mills keep roles in training and one-off repair or prototype tasks, but their adoption is being overtaken by entry-level CNC units as shops standardize on digital workflows. User-friendly interfaces, conversational programming, and embedded simulation shorten the learning curve for first-time CNC adopters and help small shops consolidate steps into single-setup runs. Probing cycles, tool life monitoring, and closed-loop offsets enable unattended shifts that expand capacity without matching headcount growth. At a 6.73% growth rate, CNC becomes the primary engine of vertical milling machine market size expansion during 2026 to 2031.

By End-User Industry: Automotive Retooling Drives Volume, Aerospace Demands Precision Premium

Automotive accounted for 53.21% of demand in 2025 as OEMs and tier suppliers retooled dies, fixtures, and battery components to support platform transitions. This spend included expanded use of vertical mills to cut aluminum and tooling steels with stable accuracy and predictable chip control. Manufacturing technology orders in the United States showed that contract machine shops and automotive programs increased capital spending into late 2025, which supported broad-based upgrades to vertical machining cells. The work concentrates on stamping dies, e-motor housings, pack trays, and joining fixtures that require stiffness and thermal stability. These investment patterns sustain the vertical milling machine market because they rely on rigid architectures for repeat jobs across multiple shifts.

Aerospace and defense is the fastest-growing end-user with a 6.12% CAGR as production ramps and backlogs encourage capacity additions for high-value parts. Airbus reported 793 deliveries in 2025 and targeted 870 in 2026, which supports long-run visibility for tooling and precision machining capacity on vertical platforms. Precision categories in electronics, semiconductor equipment, and medical devices also contribute to the vertical milling machine market through tighter tolerance requirements and finish standards that suit high-rigidity vertical cells. Energy and power applications add turbine blade roots, gearbox housings, and generator components that benefit from single-setup five-axis strategies. The overall end-user mix provides a breadth of workloads that together underpin steady capital plans through 2031.

Geography Analysis

Asia-Pacific captured 47.89% in 2025 and remains the largest regional base for the vertical milling machine market. Electronics and automotive manufacturing footprints across China, Japan, South Korea, India, and Southeast Asia keep machine utilization high, while supplier networks expand capacity to serve export demand. Local builders and global brands compete across small, mid, and large formats, and that improves access to automation-ready vertical platforms. APAC’s strength in contract manufacturing and job shops also supports three-axis and four-axis vertical installs that handle high part variability. Regional training and certification programs are expanding to address skills gaps, and they reinforce the need for both manual and CNC platforms as a blended approach to grow the workforce. These dynamics keep APAC a demand anchor with a broad mix of vertical milling use cases.

North America recorded the fastest projected regional CAGR at 5.21% through 2031 due to reshoring, infrastructure buildout, and incentives that favor domestic production of strategic components. The U.S. Department of Energy highlighted federal and private investments that strengthen energy and industrial supply chains, which are increasing local demand for precision machining capacity on vertical platforms. U.S. manufacturing technology orders reached a record high in December 2025 and closed the year up 22.5%, which reflects the continued modernization of the machine base and supports the adoption of automation-ready vertical centers. Canada and Mexico participate through integrated supply chains that support automotive, aerospace, and electronics programs. Shops across the region are scaling five-axis cells to consolidate setups and are using pallets and robots to address skilled labor gaps. These moves enhance the readiness of the regional base to take on complex parts and to reduce lead times.

Europe maintains a deep installed base and a sophisticated demand profile for high-accuracy vertical mills in automotive tooling, aerospace, and energy. Consolidation moves that integrate European service and support networks, such as DN Solutions acquiring HELLER in January 2026, reinforce local ecosystems that are essential to uptime and lifecycle performance on complex vertical platforms. Precision users across Germany, Italy, France, and the UK continue to favor vertical machines with strong rigidity, thermal control, and control sophistication to meet geometry and repeatability requirements. Policy frameworks in Europe also encourage energy-efficient production that aligns with modern spindles, high-pressure coolant, and toolpath strategies that shorten cycle times. These attributes contribute to the vertical milling machine market by emphasizing high-value, audited work that benefits from single-setup accuracy and automation.

Competitive Landscape

The vertical milling machine market remains moderately fragmented with a long tail of regional builders and specialized solution providers. Top-tier vendors such as Haas Automation, DMG MORI, Yamazaki Mazak, Okuma, and Makino collectively hold a significant but not dominant share, leaving space for niche players in ultra-precision, micro-milling, and high-speed aluminum machining. Competitive strategies are split between high-volume standardized platforms with sharp price points and premium solutions that bundle automation, control intelligence, and digital services. In the premium segment, integrated software, toolpath stability, digital twins, and app-driven workflows help cut cycle times and stabilize quality on complex jobs, which can justify premium pricing when uptime and scrap rates dominate ROI models. In the value segment, competitive parts availability, entry-level pricing, and straightforward controls sustain volume leadership at job shops and contract manufacturers that focus on three-axis work.

M&A momentum is reshaping scale and capabilities across Europe and Asia. In January 2026, DN Solutions completed the acquisition of HELLER for approximately EUR 2 billion, creating a combined production footprint of more than 13,400 machines and expanding service coverage for high-end milling and multi-tasking systems. This scale supports procurement leverage across controls, spindles, linear guides, and automation components, and it can accelerate R&D release cycles for next-generation vertical platforms. Strategic focus is also moving toward modular automation that allows buyers to add robots and pallet pools incrementally rather than committing to turnkey multi-million-dollar lines in a single step. These shifts keep ROI pathways flexible and enable a wider range of users to enter lights-out production with vertical cells.

Skills and integration capacity remain strategic bottlenecks, and ecosystem investments are responding. FANUC announced a USD 90 million expansion in Michigan with a large training footprint targeted to grow the pipeline of integrators and technicians for CNC-robotic workcells in automotive, aerospace, and medical equipment. This addresses a core adoption barrier and helps more users move from pilot cells to standard work around unattended vertical milling. At the same time, users are pressing vendors for life-of-machine service support and faster parts logistics that keep uptime consistent as workloads shift toward complex, tight-tolerance jobs. The net effect is a vertical milling machine market where scale, service, and integration capacity are as decisive as spec sheets in competitive outcomes.

Vertical Milling Machine Industry Leaders

Haas Automation

DMG MORI

Yamazaki Mazak

Okuma Corporation

Makino Milling Machine

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: DN Solutions completed its acquisition of HELLER for approximately EUR 2 billion, consolidating production capacity of over 13,400 machines annually and expanding a portfolio that spans turning, milling, and multi-tasking centers.

- January 2026: In 2025, Lockheed Martin achieved a milestone with 191 F-35 deliveries. The company had also secured advanced contracts, which bolstered the demand for precision machining, particularly for titanium and landing gear components.

- January 2026: Airbus reported 793 commercial aircraft delivered in 2025 and targeted 870 for 2026 with a record backlog, sustaining multi-year requirements for complex tooling and precision machining capacity.

- December 2025: The Association For Manufacturing Technology reported December 2025 U.S. manufacturing technology orders of USD 814.3 million, a record monthly high, and full-year 2025 orders of USD 5.74 billion, up 22.5% year over year.

Global Vertical Milling Machine Market Report Scope

The Vertical Milling Machine Report is Segmented by Product Type (Turret, Bed-Type, Knee-Type, Gantry/Bridge-Type, and Others), by Axis Configuration (3-Axis, 4-Axis, 5-Axis & Above), Control Technology (CNC, and Conventional/Manual), by End-User Industry (Automotive, Aerospace & Defense, Electronics & Semiconductor, Medical Devices, Energy & Power, and Others), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Turret |

| Bed-Type |

| Knee-Type |

| Gantry / Bridge-Type |

| Others (turn-mill, specialized, etc.) |

| 3-Axis |

| 4-Axis |

| 5-Axis & Above |

| CNC Vertical Milling Machines |

| Conventional/ Manual Vertical Milling Machines |

| Automotive |

| Aerospace & Defense |

| Electronics & Semiconductor |

| Medical Devices |

| Energy & Power |

| Others (General Manufacturing, Job Shops, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Turret | |

| Bed-Type | ||

| Knee-Type | ||

| Gantry / Bridge-Type | ||

| Others (turn-mill, specialized, etc.) | ||

| By Axis Configuration | 3-Axis | |

| 4-Axis | ||

| 5-Axis & Above | ||

| By Control Technology | CNC Vertical Milling Machines | |

| Conventional/ Manual Vertical Milling Machines | ||

| By End-User Industry | Automotive | |

| Aerospace & Defense | ||

| Electronics & Semiconductor | ||

| Medical Devices | ||

| Energy & Power | ||

| Others (General Manufacturing, Job Shops, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the vertical milling machine market?

The vertical milling machine market size is USD 13.8 billion in 2025 and is projected to reach USD 16.9 billion by 2031 at a 3.39% CAGR from 2026 to 2031.

Which product type leads and which is growing fastest in the vertical milling machine market?

Bed-Type VMC leads with 40.31% in 2025, while Gantry or Bridge-Type VMC records the fastest growth at 4.78% CAGR to 2031.

How are control technologies evolving in the vertical milling machine market?

CNC systems hold 69.12% of deployments and remain dominant for audited, repeatable production, while Conventional or Manual units are growing at 6.73% CAGR as schools and prototype shops maintain hands-on needs.

Which end-user segments are most important for the vertical milling machine market?

Automotive accounted for 53.21% in 2025, and aerospace and defense is the fastest growing end-user with a 6.12% CAGR through 2031.

Which regions drive demand in the vertical milling machine market?

Asia-Pacific holds 47.89% of demand, and North America is growing fastest at a 5.21% regional CAGR through 2031 on the back of reshoring and policy-linked investment.

What is shaping the competitive landscape of the vertical milling machine market in 2026?

Consolidation moves like DN Solutions acquiring HELLER, growing investment in automation and training capacity, and service-led differentiation are shaping outcomes for premium and value segments.

Page last updated on: