Machining Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

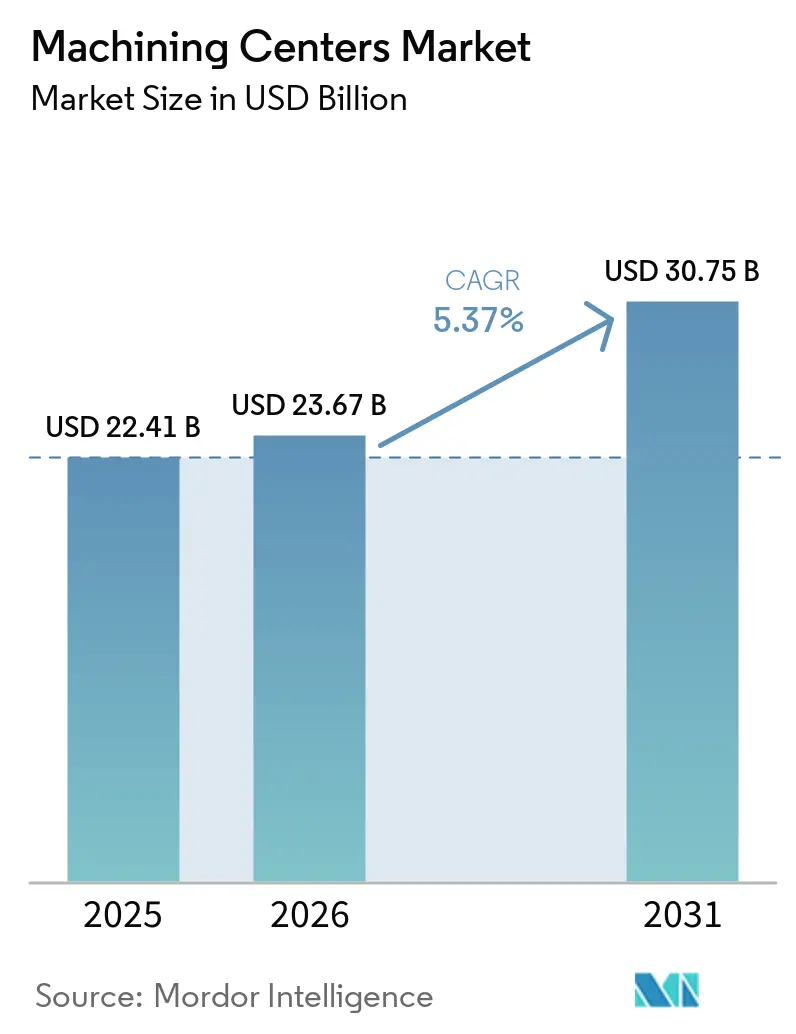

| Market Size (2026) | USD 23.67 Billion |

| Market Size (2031) | USD 30.75 Billion |

| Growth Rate (2026 - 2031) | 5.37% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Machining Centers Market Analysis by Mordor Intelligence

The Machining Centers Market size is projected to expand from USD 22.41 billion in 2025 and USD 23.67 billion in 2026 to USD 30.75 billion by 2031, registering a CAGR of 5.37% between 2026 to 2031.

Capital spending is holding up as aerospace, defense, and energy programs move to higher production rates and require reliable multi-axis capacity, which supports steady order intake in the machining centers market. Medical device manufacturers are aligning with the FDA’s Quality Management System Regulation in 2026, which raises documentation and precision bars and encourages upgrades to sub-micron capable vertical and 5-axis platforms. Electrification of vehicle fleets and the spread of hybrids create a wide set of aluminum machining needs across battery enclosures, motor housing, and thermal components, lifting near-term demand for horizontal and multi-tasking lines. Contract manufacturing is also scaling capacity as sourcing complexity rises and reshoring pushes more work into flexible, automation-ready cells. These shifts collectively reinforce a balanced growth profile for the machining centers market through the forecast period.

Key Report Takeaways

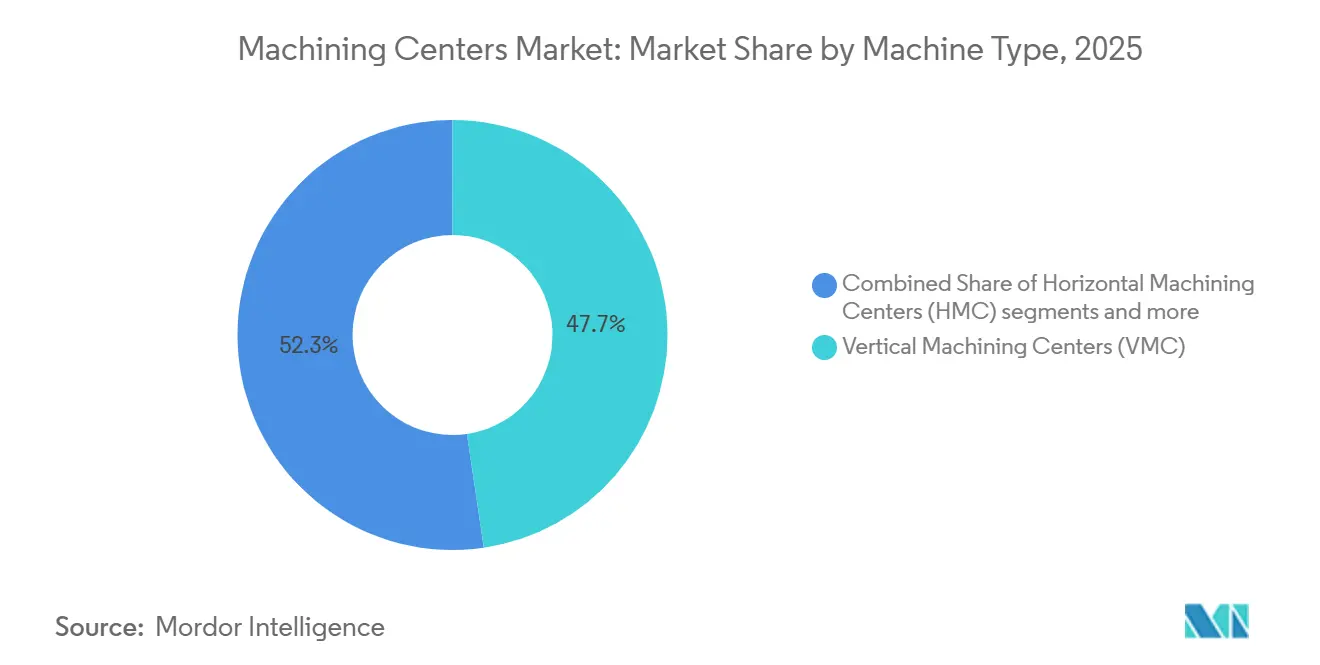

- By machine type, vertical machining centers led with 47.68% market share of the machining centers market size in 2025, while universal and 5-axis configurations are projected to expand at a 6.12% CAGR through 2031.

- By axis configuration, 3-axis systems held 52.34% share in 2025, with 5-axis and above advancing at a 6.78% CAGR through 2031.

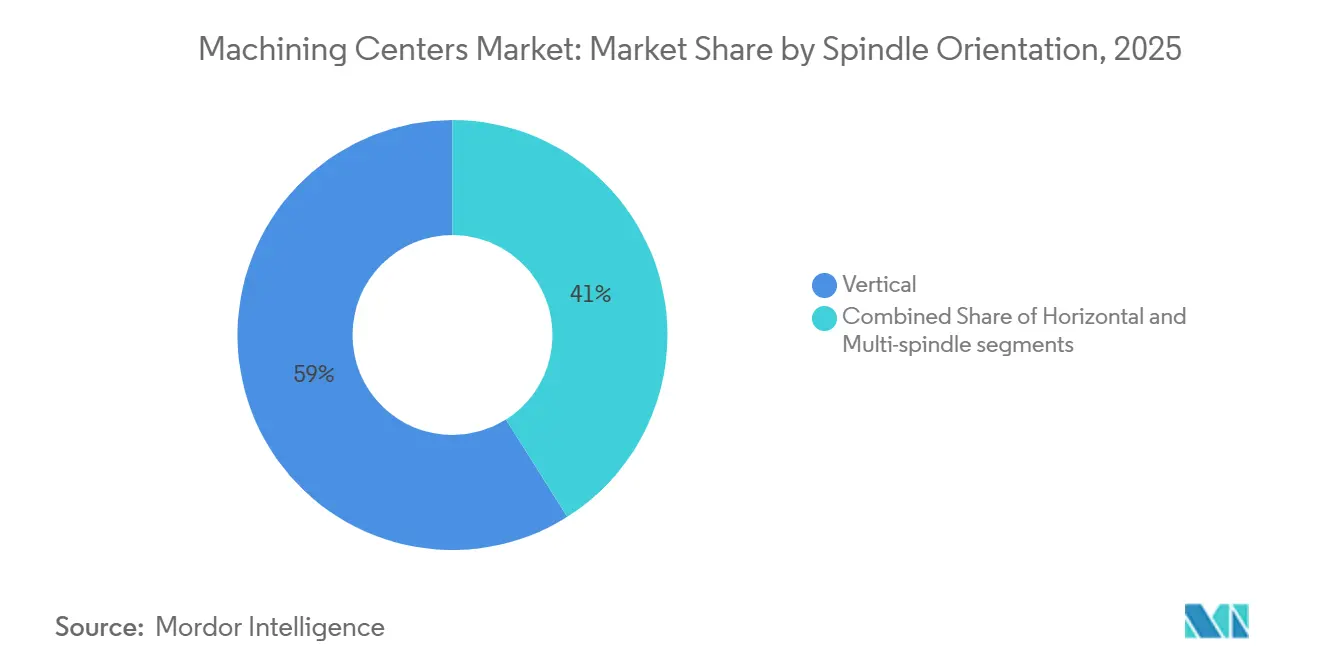

- By spindle orientation, vertical setups accounted for 58.97% of the machining centers market share in 2025, and multi-spindle architectures are growing at a 7.34% CAGR to 2031.

- By structure type, column type designs represented 43.12% of installations in 2025, while gantry type machines are set to grow at a 6.43% CAGR through 2031.

- By end user, automotive captured 36.78% share in 2025, and aerospace and defense is the fastest growing at a 7.89% CAGR to 2031.

- By geography, Asia Pacific accounted for 54.69% of global consumption in 2025, with a 7.12% CAGR outlook through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Machining Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aerospace Component Manufacturing Capacity Expansion | +0.9% | Global, concentrated in North America (U.S. defense, commercial aviation), Europe (Airbus supply chain), Asia-Pacific (MRO hubs) | Medium term (2-4 years) |

| Medical Device Manufacturing Precision Requirements | +0.6% | Global, particularly North America (FDA jurisdiction), Europe (CE marking), with spillover to India and ASEAN contract manufacturing | Medium term (2-4 years) |

| Electric Vehicle Powertrain Component Production | +1.1% | Global, strongest in China, North America, Europe, emerging in India | Short term (≤ 2 years) |

| Mold and Die Industry Growth in Emerging Markets | +0.7% | APAC core (China, India, Vietnam, Thailand), spill-over to MEA and Latin America | Medium term (2-4 years) |

| Replacement Demand for Aging Machine Tool Fleets | +0.8% | Global, acute in North America and Europe (installed base from 1990s-2000s), moderate in Asia-Pacific | Long term (≥ 4 years) |

| Contract Manufacturing Outsourcing by OEMs | +0.9% | Global, with concentration in North America nearshoring, Mexico, Central Europe, and ASEAN Tier 2/3 suppliers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aerospace Component Manufacturing Capacity Expansion

Aerospace programs are moving ahead with multi-year capacity investments that lift demand for horizontal and 5-axis machining platforms. Pratt & Whitney committed USD 200 million to its Columbus, Georgia operations to increase compressor and turbine disk output by 30% by 2028, which ties directly to Geared Turbofan and F135 engine build rates and favors 5-axis and heavy-duty horizontal lines with titanium and nickel capability[1]Raytheon Technologies, “RTX’s Pratt & Whitney Broadens Manufacturing Capabilities with $200 Million Investment in Columbus, Georgia,” Raytheon Media Relations, raytheon.mediaroom.com. Karman Space & Defense is quadrupling launch system production and doubling solid rocket motor nozzle output through a new automated machining hub in Salt Lake City that targets Q4 2026 readiness, which will require high-throughput metallic machining integrated with automated inspection. Honeywell’s expansion in Olathe, Kansas, is building domestic electronics manufacturing depth for avionics and printed circuit board assemblies, reinforcing localized precision manufacturing across the flight systems value chain. Ramping such capacity requires multi-axis cells, pallet automation, and consistent thermal management to stabilize tolerance at higher feeds and speeds, which is a priority across North American and European aerospace clusters. These investments set up a 2 to 4 year impact window that aligns with commissioning, process validation, and rate readiness, which in turn underpins near term demand in the machining centers market.

Medical Device Manufacturing Precision Requirements

The 2026 Quality Management System Regulation raises the bar on traceability and process control for medical device manufacturers, which elevates the need for sub-micron machining and in-process gauging. The regulation aligns with ISO principles and updates scores of sections across 21 CFR, which solidifies quality systems and documentation that depend on stable machining processes. Capacity additions support the trend, with new cleanrooms and compliant production environments being installed to serve precision parts and assemblies for medical use cases. Investments in thermal compensation, probing cycles, and digital twin validation are spreading to reduce scrap and to pass audits with consistent, verifiable machining outcomes. This driver is strongest in the United States under FDA jurisdiction and extends to Europe under CE marking, with a growing effect in India and ASEAN contract manufacturing hubs that serve multinational OEMs. The 2 4-year impact timeline matches certification cycles and equipment lead times, which keeps the medical pipeline supportive for the machining centers market.

Electric Vehicle Powertrain Component Production

Vehicle electrification is shifting machining workloads from engine blocks to battery enclosures, motor housing, and thermal management hardware, which favors fast horizontal cells and multi-tasking centers. The EPA reports that BEV and PHEV combined output reached approximately 10% of U.S. light-duty production in 2024 and is projected to rise to 12% in 2025, while hybrid share reached 19%, which all create machining demand for aluminum structures and thermal components[2]U.S. Environmental Protection Agency, “The 2025 EPA Automotive Trends Report: Fuel Economy, and Technology Since 1975,” EPA, epa.gov. Battery cost metrics in 2025 moved down to USD 128 133 per kWh ranges in U.S. datasets, which supports adoption trends and capacity plans that flow through to Tier 1 and Tier 2 machining requirements. General Motors announced a USD 4 billion investment program across United States plants in 2025-2026 to increase domestic output of internal combustion and electric vehicles, with EV capacity being prioritized at Factory ZERO and other sites, which catalyzes orders for horizontal cells with palletization and integrated metrology. In North America and Europe, retooling is in motion at OEMs and Tier suppliers as EV and hybrid programs ramp, which compresses lead times for machining centers with automation-ready features. That short-term window of two years is supportive of the machining centers market as powertrain mix shifts require fast cycle times and process consolidation.

Mold and Die Industry Growth in Emerging Markets

Tooling capacity in Asia is expanding with additional precision machining cells to serve consumer goods, automotive interiors, and electronics. In late 2025 and early 2026, new facilities and expansions with advanced CNC equipment and lifting capacity were commissioned to increase die casting mold output for automotive and other sectors. Injection molding machine localization is also scaling, with new plants in China adding production area and R&D capability to serve packaging, medical, and automotive customers, which induces upstream demand for machining centers that produce mold bases, cavities, and electrodes. United States trade data for 2025 reflected monthly mold exports near USD 42 million, although volumes fell year to date by 33.7% through September due to price dynamics and input cost pressures, which reinforces the cost competitiveness gap that favors APAC toolmakers and pushes localization strategies. The medium term impact period aligns with mold design validation cycles and capacity commissioning across APAC and spillover regions. These moves guide steady purchases of 3-axis and 5-axis VMCs with high-speed spindles for electrode finishing and mirror surface cavity work, which sustains demand in the machining centers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Investment Barriers for Small Job Shops | -0.5% | Global, acute in North America and Europe where financing costs are elevated; moderate in Asia-Pacific | Long term (≥ 4 years) |

| Skilled CNC Operator and Programmer Shortage | -0.7% | Global, most severe in North America and Europe (aging workforce); emerging in Asia-Pacific as automation accelerates | Short term (≤ 2 years) |

| Long Lead Times from Japanese and German Manufacturers | -0.3% | Global, impacting all regions dependent on high-end imported machining centers | Medium term (2-4 years) |

| Economic Uncertainty Delaying Capital Equipment Purchases | -0.6% | Global, with pronounced effects in cyclical industries (automotive, construction equipment); moderate in defense-linked sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skilled CNC Operator and Programmer Shortage

Open positions for machinists and CNC programmers continue to weigh on throughput, which limits how fast plants can ramp complex work. Industry sources estimate a significant gap through 2030 in the United States as retirements keep pace with demand, while short training cycles cannot fully cover the skills needed for multi-axis programming, setup, and inspection. Time to proficiency is measured in years for advanced CAM roles, which does not align with quarterly delivery cycles and creates recurring bottlenecks in light-out programs. Larger manufacturers often partner with technical colleges and offer higher wages, which can draw talent away from small job shops and intensify hiring friction. The net effect is idle time on expensive multi-axis assets and slower adoption of process consolidation when teams cannot support programming and setup across shifts. This restraint is most acute in North America and Europe and is spreading in APAC as automation projects raise the baseline skill requirements, which keeps this a near-term drag for the machining centers market.

Economic Uncertainty Delaying Capital Equipment Purchases

Manufacturers are reevaluating equipment timelines as material inflation, tariffs, and policy uncertainty complicate ROI math for capital equipment. In 2025-26, 98% of manufacturing leaders reported material cost pressures affecting sourcing strategies, and 71% cited geopolitics as a factor in long term supply chain planning, which results in more cautious capital spending behavior. Tariff mitigation has also become widespread, with nearly all respondents taking steps to counteract impacts, which can shift buying decisions and financing windows. Entry-level cells can produce paybacks under one to two years under high utilization, yet those assumptions weaken when demand softens, or billing rates decline, and high-speed 5-axis investments require disciplined loading and uptime to meet target returns. These headwinds are prominent in cyclical sectors tied to consumer demand and construction, while defense-linked work has shown more resilience due to multi-year contracts. The posture is likely to keep some orders deferred to later planning cycles, which tempers near-term upside for the machining centers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Vertical Centers Anchor Volume While 5 Axis Commands Premium Growth

Vertical machining centers held 47.68% of the machining centers market share in 2025, while universal and 5-axis machines are projected to expand at a 6.12% CAGR through 2031. Vertical configurations dominate high-volume work for automotive and job shop environments because tooling access, chip evacuation, and ergonomics support fast changeovers. Recent vertical 5-axis introductions also push higher spindle speeds, better rigidity, and more comprehensive technology cycles, which widens the set of parts that can be consolidated on a single platform. Horizontal machining centers remain the second largest category and are preferred for palletized automation and heavy cutting, which favors their use in powertrain, aerospace structural parts, and larger prismatic components. Multi-tasking centers that integrate turning and milling reduce setups, improve geometric integrity, and help plants cope with labor constraints by compressing process routes into single machine workflows.

In higher mix and lower volume programs, 5-axis verticals with probing and tool monitoring enable quick part family changeovers and contamination control, while horizontals tied to flexible manufacturing systems secure predictable throughput. OEM design changes that increase contour complexity, thin walls, and integrated features are a catalyst for universal and 5-axis upsizing within the machining centers market. Further gains are likely as digital twin validation and on-machine measurement accelerate first article approval cycles, and as new coolant management systems enhance tool life and surface finish. This mix favors suppliers with deeper automation portfolios, spindle options matched to material families, and software suites that can be deployed across fleets in the machining centers market.

By Axis Configuration: 3 Axis Volume Contrasts with 5 Axis Precision Imperative

The 3-axis segment accounted for 52.34% of the machining centers market share in 2025, while 5-axis and above systems are set to advance at a 6.78% CAGR through 2031. Three-axis platforms remain the workhorse for many prismatic parts and present a lower capital barrier for shops focused on general machining, prototypes, and fixtures, which supports their continued prevalence. Growth at the premium end is guided by parts needing simultaneous 5-axis motion to maintain surface continuity and to cut cycle time without repositioning. Advancements in direct drive rotary axes, RTCP functions, and higher speed contouring enable better surface quality on complex surfaces, which is a priority for aerospace, medical, and high-end automotive applications.

Productivity features like built-in pallet changers, more robust tool matrices, and predictive maintenance capabilities are becoming standard in 5-axis cells, which support lights-out ambitions and higher spindle utilization. Integrated solutions that deliver fast chip-to-chip times and full 6 side machining can reclaim thousands of hours annually in high-mix shops, an outcome that is attractive as labor remains constrained. This positions 5-axis adoption to continue its steady climb, particularly where quality systems and tighter audits push for more process control across the machining centers market. As more Tier suppliers consolidate processes, the machining centers market size tied to advanced axis configurations should benefit from sustained demand adjacent to regulated and safety-critical products.

By Spindle Orientation: Vertical Dominance Meets Multi Spindle Productivity Push

Vertical spindle orientation accounted for a 58.97% share in 2025, while multi-spindle configurations are on track for a 7.34% CAGR to 2031. Verticals continue to be the default for many prismatic parts because operators can load, inspect, and reset quickly, and gravity-assisted chip flow improves stability for many materials. Horizontals serve heavy cuts and integrate well with pallet systems, which boosts spindle utilization and stabilizes flow in automated cells; recent horizontal introductions trimmed cycle time and power consumption, which helps meet energy and cost targets. Multi-spindle machines are scaling in high-volume automotive and hydraulics applications because parallel operations compress cycle times and support output goals where lines run at high utilization.

Convergence between spindle architecture and automation remains a lever for productivity in the machine-center market. Horizontal lines paired with gantry or robotic loaders lower changeover waste and permit more unattended hours, while vertical multi-tasking platforms with intelligent cycle support reduce operator dependency. This trend is reinforced by energy-efficient spindle designs and regenerative systems that support corporate sustainability goals. The net effect is a gradual increase in adoption of multi-spindle and horizontal systems in high-volume settings, with verticals retaining a large installed base across job shops.

Geography Analysis

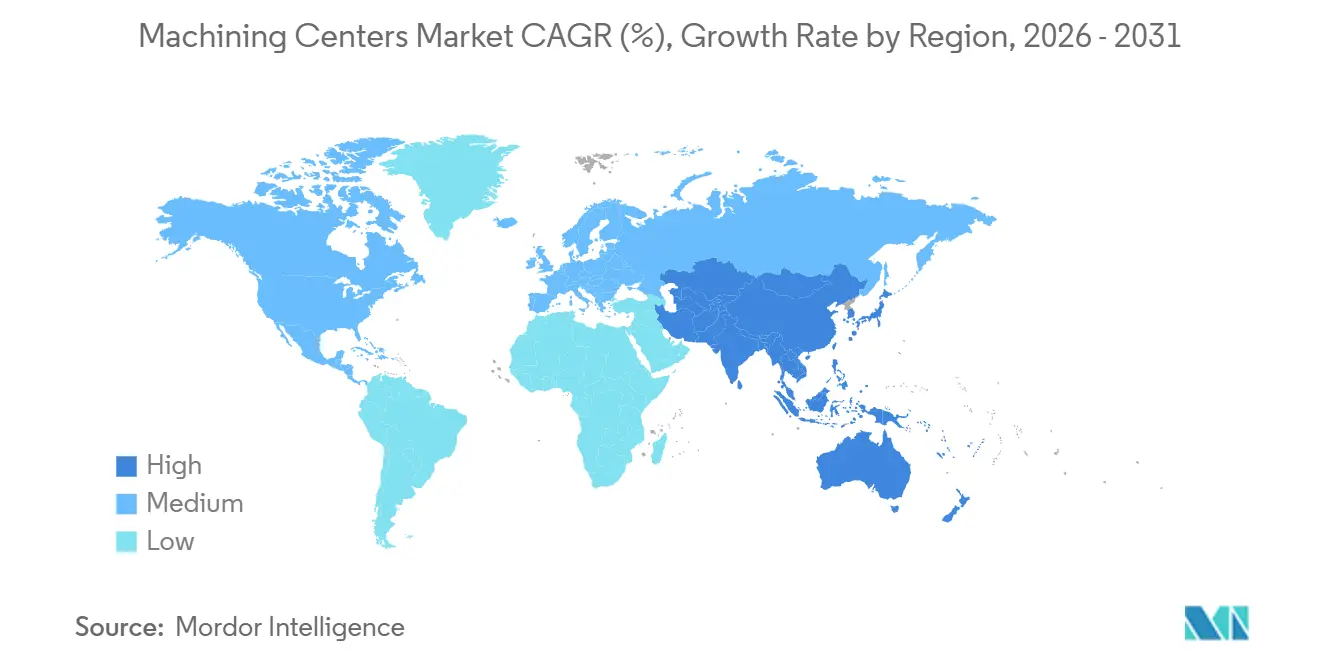

Asia Pacific accounted for 54.69% of global consumption in 2025 and is projected to grow at a 7.12% CAGR through 2031, driven by strong industrial expansion and manufacturing depth. China continues to scale both imports and exports, surpassing Germany with a 19% share of global machine tool exports in H1 2025, reflecting rising domestic capabilities alongside demand for high-precision systems. Imports remain led by Japan, Germany, and Taiwan, highlighting continued reliance on advanced horizontals and 5-axis machines. At the same time, new plants in China are expanding mid- to high-end production capacity, reinforcing the region’s manufacturing base.

India is strengthening its position through policy support such as Production Linked Incentive schemes and capital goods programs, which are expanding the addressable market for precision manufacturing. The PLI Auto scheme and sanctioned capital goods projects are supporting capability building, centers of excellence, and testing infrastructure. This policy push, combined with a focus on skill development, is enabling India to move into higher-value components and assemblies. Together with China, these trends position Asia Pacific as the primary growth engine for the machining centers market.

North America gained strong momentum in 2025, supported by aerospace, defense, and automotive reshoring, with record U.S. manufacturing technology orders signaling tight capacity and near-term demand. Europe, led by Germany and Italy, continues to benefit from a sophisticated industrial base and sustainability-driven capex cycles, while consolidation enhances OEM capabilities. The Middle East and Africa are gradually expanding through diversification and energy investments, though reliance on imported machine tools remains high. Overall, Asia Pacific anchors growth, while North America and Europe provide stable demand across high-value and regulated sectors.

Competitive Landscape

Fragmentation continues to define the machining centers market, with a wide mix of global OEMs, regional specialists, and niche players competing across industries and geographies. Despite selective consolidation, customers still rely on diverse suppliers based on application needs, service proximity, and cost-performance balance. Competition remains focused on thermal stability, energy efficiency, and digital integration, alongside the ability to deliver flexible, automation-ready systems. This ensures no single group of players dominates the market landscape.

Recent acquisitions reflect portfolio expansion rather than structural consolidation. DN Solutions’ acquisition of HELLER and MODIG’s purchase of LiCON enhance technological depth and regional reach, particularly in aerospace, semiconductors, and high-volume manufacturing. However, these moves occur within a still highly competitive ecosystem where multiple established and emerging players continue to operate. As a result, the supplier base remains broad and competitive across regions.

Technology differentiation remains the primary competitive lever across all tiers of players. DMG MORI and Okuma are advancing energy-efficient designs, AI-driven diagnostics, and digital twin capabilities to support productivity and unattended operations. At the same time, vendors are focusing on modular upgrades, retrofit solutions, and service models that lower upfront costs for smaller manufacturers. This emphasis on innovation, accessibility, and lifecycle value reinforces the market’s fragmented and competitive nature.

Machining Centers Industry Leaders

DMG MORI

Yamazaki Mazak

Okuma Corporation

Haas Automation

Makino Milling Machine

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: DMG MORI CO., LTD. and The University of Tokyo established the Machining Transformation Research Center (MX Center) within the Graduate School of Engineering, effective April 1, 2026. The center aims to consolidate global in-use machine tools from five million to one million units by 2050 through process integration, automation, and digitalization, funded by donations from DMG MORI to The University of Tokyo Fund. Research focuses on cutting, grinding, additive manufacturing, digital twins, and applications in energy, aerospace, medical, and semiconductor sectors.

- March 2026: DMG MORI launched the NMV 3000/5000 DCG 2nd Generation 5 axis controlled vertical machining centers, featuring a 49% Y axis rigidity improvement (NMV 5000 only), speedMASTER high-speed 5-axis spindles reaching 20,000 rpm (30,000 rpm optional), 17% cycle time reduction, and 2.67 times higher aluminum chip evacuation rates compared to previous models. Optional Gear Production+ consolidates gear processing from rough hobbing to grinding on one machine. The series targets aviation, aerospace, mold making, semiconductor, and mobility industries.

- January 2026: DN Solutions, the world's third largest machine tool manufacturer, completed its acquisition of German high-end machine tool manufacturer HELLER, pending regulatory approvals in Germany, the United States, and the United Kingdom. The strategic partnership is expected to boost consolidated sales to approximately EUR 2 billion (USD 2.2 billion) and produce over 13,400 machines annually, significantly expanding the range of solutions in semiconductors, aerospace, and dual-use industries while enhancing the service network in Europe and North America.

Global Machining Centers Market Report Scope

The Machining Centers Market Report is Segmented by Machine Type (Horizontal Machining Centers, and more), by Axis Configuration (3-Axis, and more), by Spindle Orientation (Horizontal, Vertical, and more), by Structure Type (Column-Type, Gantry-Type, and more), by End-User Industry (Automotive, Energy, and more), and by Geography (North America, Europe, and more). The Market Forecasts are Provided in Terms of Value (USD).

| Horizontal Machining Centres (HMC) |

| Vertical Machining Centres (VMC) |

| Universal / 5-Axis Machining Centres |

| Multi-Tasking Machining Centers (MTM) |

| Others (Gantry / Bridge-Type Centres, Turn-Mill Centers) |

| 3-Axis |

| 4-Axis |

| 5-Axis & Above |

| Horizontal |

| Vertical |

| Multi-spindle |

| Column-Type |

| Gantry-Type |

| Moving-Table |

| Automotive |

| Aerospace & Defense |

| Energy (Oil-Gas, Renewables) |

| Medical Devices |

| Mold and Die Manufacturing |

| Others (General Manfacturing, Job Shops, Electronics, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Machine Type | Horizontal Machining Centres (HMC) | |

| Vertical Machining Centres (VMC) | ||

| Universal / 5-Axis Machining Centres | ||

| Multi-Tasking Machining Centers (MTM) | ||

| Others (Gantry / Bridge-Type Centres, Turn-Mill Centers) | ||

| By Axis Configuration | 3-Axis | |

| 4-Axis | ||

| 5-Axis & Above | ||

| By Spindle Orientation | Horizontal | |

| Vertical | ||

| Multi-spindle | ||

| By Structure Type | Column-Type | |

| Gantry-Type | ||

| Moving-Table | ||

| By End-User Industry | Automotive | |

| Aerospace & Defense | ||

| Energy (Oil-Gas, Renewables) | ||

| Medical Devices | ||

| Mold and Die Manufacturing | ||

| Others (General Manfacturing, Job Shops, Electronics, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current machining centers market size and projected CAGR to 2031?

The machining centers market size is USD 23.67 billion in 2026 and is projected to reach USD 30.75 billion by 2031 at a 5.37% CAGR.

Which machine type leads and which grows fastest through 2031 in the machining centers market?

Vertical machine centers led with 47.68% share in 2025, while universal and 5-axis configurations grow fastest at a 6.12% CAGR through 2031.

Which axis configuration is most prevalent in the machining centers market?

3 axis systems hold 52.34% share in 2025, though 5 axis and above are the fastest growing at a 6.78% CAGR through 2031.

Which region accounts for the largest share of the machining centers market?

Asia Pacific accounts for 54.69% of global consumption in 2025 and is projected to grow at a 7.12% CAGR through 2031.

What end user drives the highest volume in the machining centers market?

Automotive holds 36.78% share in 2025, while aerospace and defense are the fastest growing end user at a 7.89% CAGR through 2031.

What technology themes are shaping competition in the machining centers market?

Energy efficiency, thermal stability, multi axis process integration, and digital twin enabled predictive maintenance are primary themes, as seen in recent platform launches and software features.

Page last updated on: