Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 112.03 Billion |

| Market Size (2031) | USD 131.63 Billion |

| Growth Rate (2026 - 2031) | 3.28% CAGR |

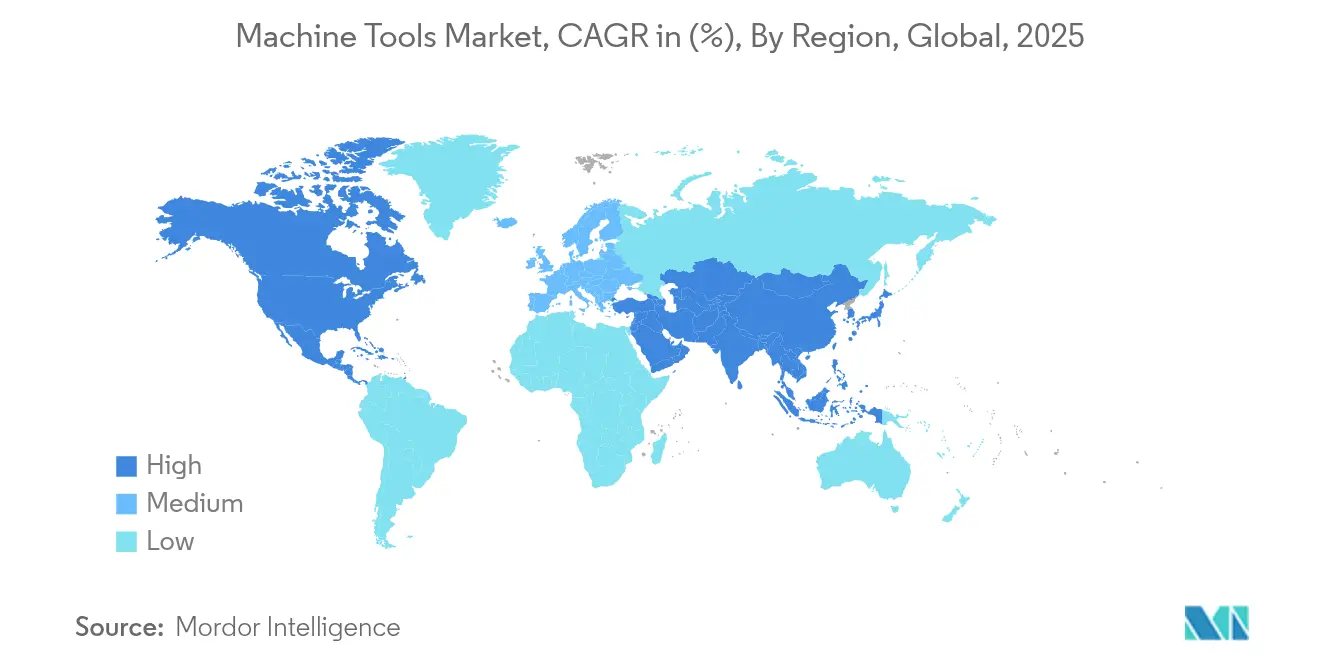

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Machine Tools Market Analysis by Mordor Intelligence

The Machine Tools Market size in 2026 is estimated at USD 112.03 billion, growing from 2025 value of USD 108.47 billion with 2031 projections showing USD 131.63 billion, growing at 3.28% CAGR over 2026-2031. This expansion occurs against a backdrop of realigned supply chains, stricter trade rules, and record investment in semiconductor fabs, each of which demands ultra-precision machining capacity. ASML’s High-NA EUV systems, which cost more than USD 400 million apiece, exemplify how next-generation lithography is lifting the performance bar for nanometer-level metal cutting and finishing [1]Jordan Novet, “ASML’s USD 400 Million High-NA EUV Machines Set New Precision Standard,” CNBC, cnbc.com. Electrification in automotive and ongoing aerospace modernization are spurring purchases of multi-axis machining centers, while Industry 4.0 projects increasingly bundle AI-enabled CNC controls that self-optimize feed rates and tool paths. Regional investment patterns show Asia drawing the bulk of new capacity additions, yet reshoring incentives in the United States and tariff uncertainty in Europe are tilting future demand toward more diversified plant footprints. Direct sales still dominate the global distribution mix, but e-commerce portals are accelerating procurement cycles for mid-ticket CNC models and replacement tooling.

Key Report Takeaways

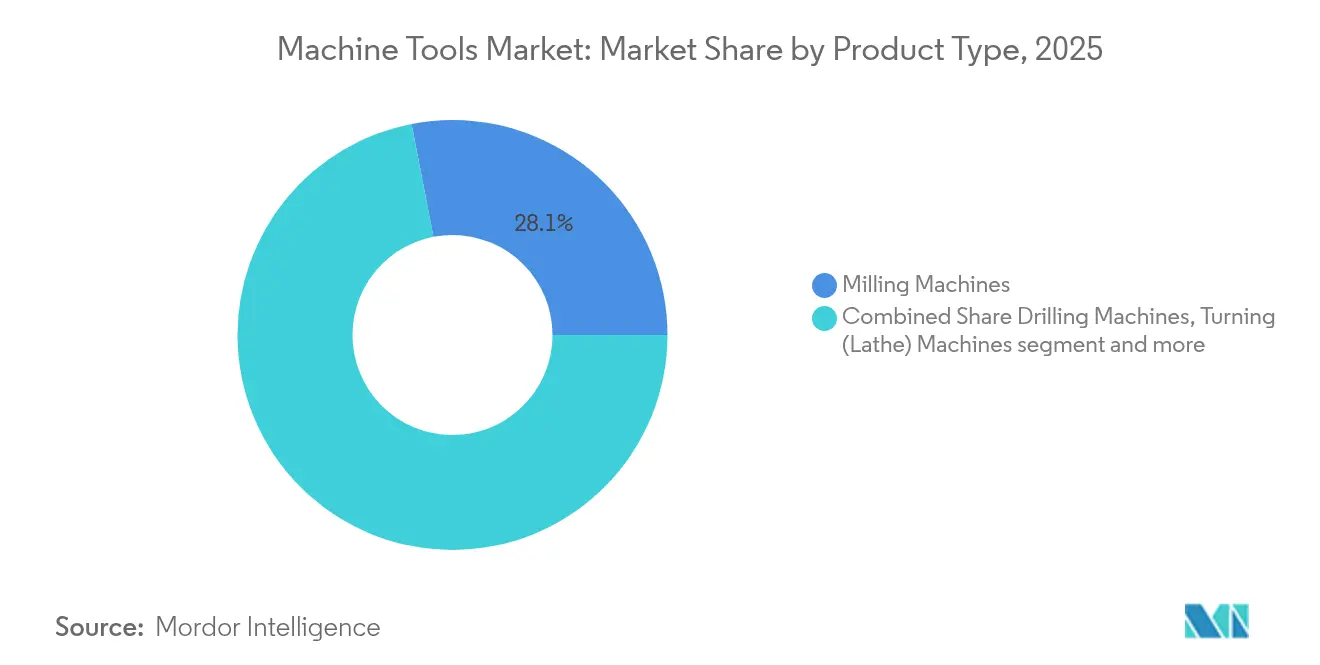

- By product type, Milling machines held 28.05% of the machine tools market share in 2025; multi-axis machining centers are projected to grow at a 6.88% CAGR to 2031.

- By technology, CNC platforms accounted for 68.55% of the machine tools market share in 2025 and will expand at a 6.08% CAGR through 2031.

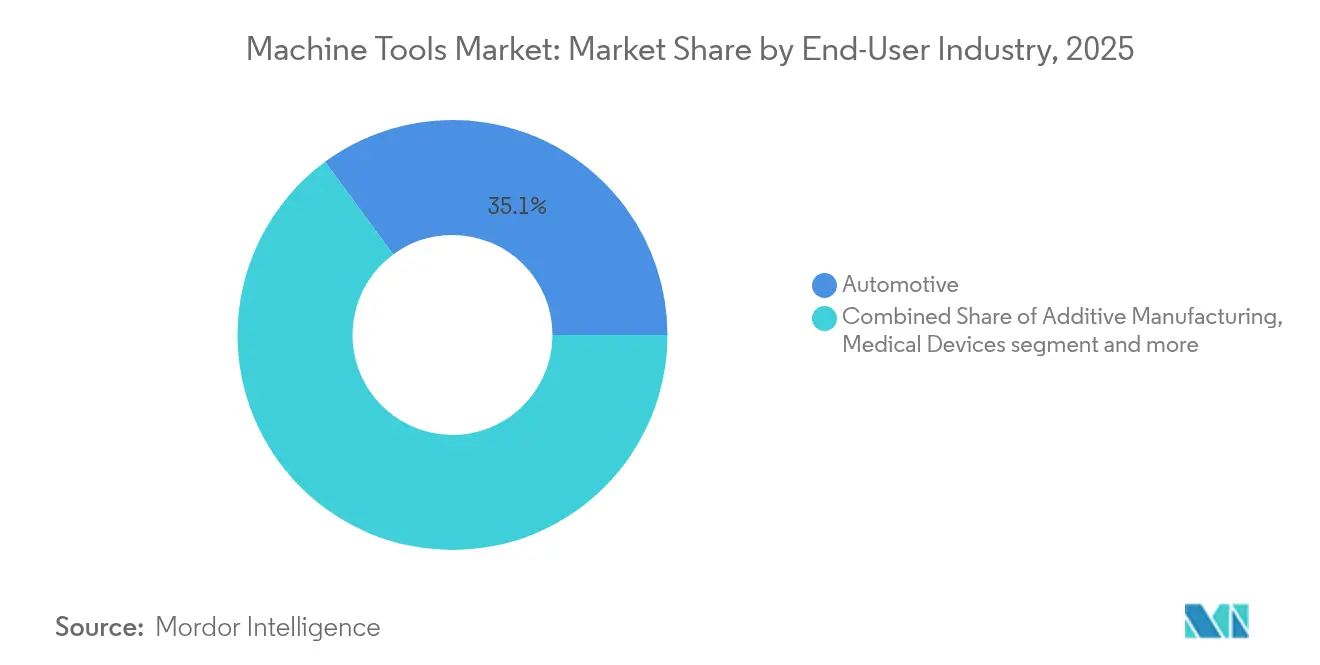

- By end-user industry, Automotive contributed 35.10% of the machine tools market size in 2025, whereas aerospace & defence leads future growth with a 6.62% CAGR.

- By sales channel, Direct sales represented 55.20% of the machine tools market size in 2025; online/e-commerce platforms are advancing at a 7.74% CAGR.

- By region, Asia Pacific captured 45.10% revenue share in 2025 and will rise at a 6.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Machine Tools Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification Surge Driving Precision e-Powertrain Machining | +0.8% | Global, with concentration in China, Germany, US | Medium term (2-4 years) |

| Semiconductor Fab Expansion Necessitating Ultra-Precision Equipment | +0.7% | APAC core, spill-over to US Southwest | Long term (≥ 4 years) |

| Industry 4.0 Adoption Boosting Demand for Smart CNC Platforms | +0.6% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Lightweight Alloy & Composite Uptake Requiring High-Speed Multi-Axis Tools | +0.5% | Aerospace hubs: US, EU, emerging in India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Electrification Surge Driving Precision e-Powertrain Machining

Electric-vehicle motor plants are pushing tolerances to micro-scale ranges, often pairing automated stator insertion and hairpin winding with five-axis machining centers that eliminate secondary finishing steps. ZF targets 70% automation for EV drive-train lines by 2030, and Chinese suppliers project annual output exceeding 120 million e-motors by 2034. General Motors and Mercedes-Benz have both insourced e-motor housing production, favouring machines that cut aluminum-silicon alloys without creating pass-off chatter. Demand is intensifying for in-process gauging, coolant management, and closed-loop compensation to suppress electromagnetic noise that would otherwise arise from micron-level form errors.

Semiconductor Fab Expansion Necessitating Ultra-Precision Equipment

Global 300 mm fab spending is forecast to hit USD 137 billion in 2027, with the Americas doubling outlays in three years. ASML’s multi-ton projection optics require diamond-turning and air-bearing grinding systems that hold sub-50 nm form error over 1 m travel. TSMC’s USD 165 billion Arizona complex exemplifies how sovereign chip programs create local pull for ultraprecision machine shops that can keep heavy components in-state during assembly. Clean-room compatibility, hydrostatic slideways, and contamination-free lubrication schemes are now baseline specifications for equipment makers serving this niche.

Industry 4.0 Adoption Boosting Demand for Smart CNC Platforms

Machine builders are embedding adaptive control and digital twin software directly into new models. Siemens’ MACHINUM suite reports double-digit reductions in tool wear, while Haas Automation’s MyHaas cloud links spindle data, probe offsets, and maintenance logs in real time. TRUMPF’s AI-assisted laser equipment demonstrates similar gains, signaling a shift from isolated CNC controllers toward network-native machining cells. These capabilities lower programming barriers, shorten first-article approval times, and unlock predictive scheduling based on live energy tariffs.

Lightweight Alloy & Composite Uptake Requiring High-Speed Multi-Axis Tools

Aerospace primes are designing components around titanium aluminide and carbon-fibre reinforced polymers, both of which generate high heat and rapid tool wear when cut on legacy machines. Challenge Machine’s five-axis cells with automatic pallet changers achieved 15% sales growth after demonstrating unattended rough-to-finish milling of thin-walled jet-engine casings. Demand for through-spindle cryogenic cooling and vibration-damped toolholders is driving retrofit activity across first-tier suppliers. Medical-device OEMs mirror these requirements, insisting on surface finishes that prevent biofilm formation and flash corrosion.

Restraints Impact Analysis of Machine Tools Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex and lengthy payback for advanced CNC | -0.6% | Global, pronounced in cost-sensitive markets | Medium term (2-4 years) |

| Surging specialty steel & linear-motion costs | -0.4% | Global, acute in steel-dependent regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capex & Lengthy Payback for Advanced CNC Systems

Atlanta Fed surveys reveal that 80% of manufacturers weigh interest rates heavily before committing to capital equipment, a dynamic amplified by prime-rate increases in 2025. A top-tier five-axis cell can exceed USD 3 million installed, pushing breakeven past five years for medium-volume job shops. Equipment-as-a-service contracts are emerging as an interim solution, though many CFOs remain wary of residual value risk once software upgrades render early-generation controllers obsolete.

Surging Specialty Steel & Linear-Motion Component Costs

World Bank indices show metals pricing climbing 9% year-on-year, with precision ball screws and guideways seeing the steepest hikes amid tungsten export controls from China[2]World Bank, “Metals and Minerals Price Index Update,” worldbank.org. OEMs are absorbing higher bills of materials or postponing new-model introductions, driving up lead times for standard horizontal machining centers. Several European builders report double ordering of critical components to hedge against logistics delays, a strategy that ties up working capital and elevates final equipment quotes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Machine Tools Market Segment Analysis

By Product Type – Multi-Axis Centers Lead Innovation Drive

The multi-axis segment started 2026 commanding USD 26.29 billion of the machine tools market size and is heading toward a 6.88% CAGR to 2031. Milling machines retain the biggest revenue pool with 28.05% share in 2025, yet growth now concentrates on simultaneous five-axis platforms that finish complex housings in one clamp. Automakers replacing ICE cylinder-block lines with e-drive casing cells embrace multi-axis machines to lower floor-space and handling costs. Aerospace primes add high-torque tilt-spindle centres to mill titanium spars while maintaining 0.015 mm flatness over 1.2 m lengths. Toolroom operators still rely on three-axis knee mills, but retrofit kits with digital readouts and probing keep them competitive for maintenance work.

Demand for laser cutting systems is rebounding as AI-guided parameter wizards reduce scrap rates on thin-gauge stainless. Electrical-discharge machining maintains a niche in tool-and-die cavities that require micro-corner radii which mills cannot reach economically. Hybrid machines that mix directed-energy deposition with finish milling are entering prototype labs where cycle-time savings outweigh equipment cost. Plasma and waterjet platforms serve heavy-fabrication yards; however, both are starting to integrate closed-loop height control to maintain cut quality on warped plates.

By Technology – CNC Dominance Accelerates Through AI Integration

CNC platforms represented 68.55% revenue in 2025 and will climb at 6.08% CAGR, solidifying their position at the heart of the machine tools market. Emerging controllers employ GPU-accelerated algorithmsthat translate STEP files directly to optimized toolpaths, slashing programming time for short-run parts. China’s First Automation secured nearly RMB 100 million to localize servo drives and PLC stacks, highlighting strategic efforts to de-risk foreign firmware dependencies. Conventional manual machines endure in small workshops and vocational schools, yet new builds are trending toward servo-ready frames even when purchased without controls, anticipating future retrofits. Hybrid additive-subtractive systems occupy the cutting edge, combining laser metal deposition with five-axis milling to eliminate support-structure removal steps in aerospace brackets.

Digital twins now simulate tool deflection and thermal drift, allowing off-machine validation that prevents collision during first-article runs. ChatCNC™ plug-ins recognise prismatic features and auto-generate rough-to-finish sequences, enabling less-experienced programmers to achieve veteran-level cycle times. Predictive analytics platforms flag spindle anomalies well before catastrophic failure, an especially valuable feature for lights-out processing where operator oversight is minimal.

By End-User Industry – Aerospace Overtakes Traditional Automotive Growth

Automotive kept its grip on 35.10% of 2025 revenue, yet the sector is in transition as internal-combustion machining contracts sunset alongside EV drivetrain ramp-ups. Aerospace & defence will post the fastest 6.62% CAGR thanks to pent-up jetliner demand and record defence modernisation budgets. GE Aerospace allocated USD 650 million in 2024 for new component lines that require five-axis blisk milling, fibre-optic in-cycle inspection, and adaptive tool compensation. Electrical & electronics manufacturers are expanding clean-room machining to support plasma-etch chamber parts, while medical-device firms specify 6,000 rpm grinding spindles for cobalt-chrome knee implants.

Industrial machinery OEMs seek modular machining cells that flex between prototype and series production without costly re-validation. Shipbuilding and marine yards, subject to cyclical naval funding, demand large-envelope gantry mills that can handle 15-m propeller blades with contour accuracy better than 0.3 mm. Wind-tower hubs and gearbox housings meanwhile add volume in the energy segment, pushing machine builders to develop hydrostatic-guided horizontals capable of 30-ton table loads.

By Sales Channel – Digital Disruption Accelerates Direct Engagement

Direct engagement generated 55.20% of the machine tools market size in 2025 because complex quotations often mandate on-site time studies and fixture concept reviews. Nonetheless, web-based tender portals now list mid-range CNC lathes complete with financing calculators, compressing deal cycles from months to weeks. Younger procurement teams favour online specification configurators that compare spindle power, axis acceleration, and IoT options side-by-side, thereby eroding dealer exclusivity. E-commerce-driven revenue is climbing at 7.74% CAGR as pandemic-born remote-demo tools become standard practice.

Dealers respond by bundling tool management, coolant supply, and operator training to safeguard margins. Subscription models that charge per spindle hour appeal to job shops coping with lumpy contract loads, shifting capex to predictable opex. TRUMPF’s remote operations centre solved half of reported U.S. laser-machine downtimes within 15 minutes during an unmanned night shift trial. System integrators are also profiting; they design turnkey cells combining robots, conveyors, and vision systems, reducing OEM risk and ensuring accountability for takt-time commitments.

Geography Analysis

APAC Machine Tools Market

Asia-Pacific Leads Amid Strategic Shifts, While North America Reshores and Europe Innovates Through Headwinds. Asia-Pacific entered 2026 with 45.10% of global revenue and a 6.05% CAGR outlook as governments funnel incentives into EV, aerospace, and semiconductor clusters. China is upgrading small-batch workshops into high-end CNC cell factories to offset looming 25% U.S. tariffs on mid-range machinery. India’s production-linked incentive program is steering capital toward 300 mm wafer fabs and defence airframe work, generating orders for precision horizontals and vertical machining centres. Japan leverages decades of motion-control know-how to export ultra-precision grinders that hold sub-micron repeatability across multi-shift duty cycles, while South Korea’s consumer-electronics conglomerates invest in machining capacity for foldable-phone hinge plates and camera modules. ASEAN nations such as Vietnam and Thailand gain share as OEMs adopt a China-plus-one sourcing model that values geographic risk dispersion.

North America Machine Tools Market

North America benefits from reshoring policies aimed at rebuilding strategic manufacturing self-reliance. United States consumption reached its highest 11.9% share since 2001 as regional tool builders added capacity for large-format vertical lathes used in space-launch structures. Mexico’s 9.1% uptick stems from near-shore vehicle assembly, with state-backed industrial parks in Nuevo León offering 24-hour permit approvals. Canada draws machine-tool orders from the mining sector and low-carbon energy projects, though overall momentum is tempered by skilled-labour shortages, a constraint echoed across the entire continent.

Germany and Nordics Machine Tools Market

Europe faces margin erosion from elevated electricity costs and currency volatility, yet it preserves a commanding lead in high-accuracy five-axis and laser-metal-deposition systems. German builders are responding to soft domestic orders by pushing into after-sales contracts and retrofits, including spindle-exchange programmes that guarantee 48-hour turnaround. TRUMPF invested EUR 530 million in R&D during 2025 to maintain its edge in beam-source efficiency despite a 9% revenue dip. Nordic firms highlight sustainability leadership by offering carbon-footprint certificates with each new machine shipment, a feature increasingly mandated in public-sector tenders.

Regulatory Landscape

Regulation affecting machine tool design, conformity, and cross-border shipments is tightening, with a visible shift toward safety, cybersecurity, and traceability requirements that extend into CNC and connected-machine architectures. In the European Union, Regulation (EU) 2026/789 entered into force in April 2026 and adds compliance obligations around machinery safety and risk management, which are increasingly relevant for AI-assisted monitoring and networked controls. This is reinforcing certification-first procurement for CE-marked equipment.

Trade and customs controls are also becoming more document-intensive for machine tool flows and critical subassemblies. In the United States, U.S. Customs and Border Protection actions in July 2026 requiring electronic submission and real-time validation for CBP Form 346 raise the compliance bar for CNC imports. China General Administration of Customs Announcement No. 77 of 2026 (June 2026) introduces end-to-end supervision for exports of metal-cutting equipment, including buyer qualification and end-use verification. Europe is also linking industrial components more directly to carbon reporting via the CBAM transition framework, with an October 2026 expansion signaled to cover certain steel-intensive components used in metal-cutting machinery. That increases embedded-carbon accounting needs for exporters and assemblers.

Value Chain Analysis

The machine tools value chain begins with upstream metals and precision components, moves into OEM design and integration, and ends with downstream commissioning and application engineering for end users across automotive, aerospace and defence, electrical and electronics, industrial machinery, and job shops. Inputs include castings and structural weldments, precision ball screws and linear guides, high-end electric spindles, encoders and grating scales, CNC controllers and servo drives, and software layers that support connectivity and process optimization. As CNC platforms account for 68.55% of industry revenues in 2025, controller stacks, sensors, and digital interfaces (including OPC-UA connectivity) are increasingly treated as critical-path items alongside mechanical assemblies.

Production and delivery performance is sensitive to bottlenecks in high-precision imported components and qualification cycles for alternates. Mid-to-high-end CNC machine delivery times into Europe and the United States have been cited at roughly 14 to 18 weeks in 2026, while domestic alternatives for certain restricted or scarce components require multi-month validation, commonly referenced as 6 to 9 months. That extends lead times for advanced configurations. Downstream, OEM direct sales remain the dominant route (55.20% of 2025 market value), but online channels are accelerating mid-range procurement. System integrators also bundle robots, conveyors, probing, and metrology into turnkey cells, tightening coordination between machine OEMs, automation partners, and plant MES and quality systems.

Competitive Landscape

Competitive Landscape

The competitive arena mixes century-old incumbents and digital-native challengers, producing moderate fragmentation yet intense rivalry on software and service dimensions. Yamazaki Mazak, DMG MORI, and TRUMPF continue to command premium price points through global support networks and proprietary control stacks. Sandvik’s 2025 buyout of CNC Software Inc. (Mastercam) confirms a vertical integration playbook that links CAM expertise directly to cutting-tool portfolios, tightening customer lock-in and shortening feedback loops for insert development. United Grinding’s agreement to purchase GF Machining Solutions will consolidate electro-discharge and laser-texturing know-how under one roof, creating a multi-process powerhouse aimed at aerospace engine manufacturers.

Emerging Chinese brands pose a volume-driven threat in mid-spec vertical machining centres, frequently bundling in-house IoT dashboards at no extra cost. Western OEMs answer by shipping machines pre-configured with OPC-UA connectors that mesh with factory-wide MES platforms, reducing integration overhead. Predictive-maintenance subscription tiers, now standard on high-speed grinders, guarantee uptime percentages in return for semi-annual fee schedules. Remote support continues to differentiate premium suppliers; TRUMPF’s video-diagnostic solution replicates factory-acceptance tests online, letting customers approve final cutting parameters without transoceanic travel.

White-space opportunities revolve around AI-driven programming aids, lights-out pallet systems, and hybrid manufacturing centres that alter supply-chain economics by combining additive and subtractive processes in one envelope. Early adopters report 30% reduction in part count when topology-optimized brackets are printed, stress-relieved, and finish-milled in a single setup. As geopolitical restrictions persist, component localisation becomes a selling point; builders able to source 70% of subassemblies domestically gain preferential financing from state-owned banks.

Machine Tools Industry Leaders

TRUMPF Group

DMG Mori Seiki Co., Ltd

Yamazaki Mazak Corporation

JTEKT Corporation

Doosan Machine Tools

- *Disclaimer: Major Players sorted in no particular order

Machine Tools Market Companies Covered in this Report

- Yamazaki Mazak Corporation

- DMG MORI Co. Ltd

- TRUMPF Group

- JTEKT Corporation

- Doosan Machine Tools

- Okuma Corporation

- Makino Milling Machine Co. Ltd

- Haas Automation Inc.

- FANUC Corporation

- Hyundai Wia Corp.

- Schuler AG

- Sandvik AB (Seco & Walter)

- GF Machining Solutions

- Fives Group

- GROB-Werke GmbH & Co. KG

- Hermle AG

- EMAG GmbH & Co. KG

- Hardinge Inc.

- HURCO Companies Inc.

- Amada Co. Ltd

Market Opportunities and Future Outlook

Opportunities are concentrating where end users pay for precision, automation, and connected performance, rather than basic capacity. Semiconductor-fab buildouts and advanced equipment supply chains are raising demand for ultra-precision grinding, air-bearing and hydrostatic slideway platforms, and contamination-controlled machining specifications, which aligns with the report emphasis on CNC and multi-axis machining centers. At the same time, EV drivetrain and aerospace structure investments support spending on five-axis cells, in-process gauging, and AI-enabled controls that reduce programming and first-article time, reinforcing the shift toward smart CNC platforms and integrated automation.

A second opportunity area involves expanded localized manufacturing capacity and stronger regional support footprints, which helps buyers manage both lead times and compliance complexity. On the capacity side, Jyoti CNC Automation announced in June 2026 a capacity expansion by 10,000 units to reach 16,000 machines per year, and Precision Tsugami (China) reported an RMB 150 million investment into two new plants to add around 3,000 CNC machine tools of capacity. Demand signals are also supportive: AMT reported total 2025 US manufacturing technology orders of USD 5.74 billion (up 22.5% versus 2024), along with a record December 2025 monthly order value of USD 814.3 million. Together, these point to whitespace for builders and distributors that can supply automation-ready CNC packages with faster configuration, financing, and service responsiveness through direct and online channels.

Recent Industry Developments in Machine Tools Market

- July 2026: TRUMPF announced a strategic partnership with Mate Precision Technologies to broaden its sheet metal tooling portfolio for fabricators. The partnership expands TRUMPF's ability to bundle machine, tooling, and process know-how in a single offer, tightening its position in laser cutting and connected fabrication cells.

- May 2026: DMG MORI held a topping-out ceremony for its new European headquarters and technology center in Munich, with opening planned for Q1 2027. The site is intended to strengthen regional customer support, applications engineering, and demonstration capacity, which is increasingly important as buyers evaluate AI-enabled CNC workflows and automation packages before committing to high-capex platforms.

- April 2026: TRUMPF introduced automated sorting solutions for North American 2D laser-cutting machines, including SortMaster Station and SortMaster Vision, with Station availability in the United States scheduled for September 2026. Automated part handling targets labor constraints and supports higher-throughput, lights-out sheet-metal workflows that improve utilization of installed machine capacity.

Machine Tools Market Report Scope and Research Methodology

Market Definition and Coverage

This market tracks revenue from new machine tools that shape metal or other rigid materials through cutting, forming, drilling, grinding, and related precision operations, sold into industrial production and fabrication.

Scope exclusions: We exclude used or refurbished machines, software-only upgrades, and most aftermarket services that are not sold as part of a new machine purchase.

Segments Covered in This Report

- By Product

- Metal Cutting Tools

- Milling Machines

- Drilling Machines

- Turning (Lathe) Machines

- Grinding Machines

- Laser Cutting Machines

- Electrical Discharge Machines (EDM)

- Waterjet Cutting Machines

- Plasma Cutting Machines

- Multi-Axis Machining Centres

- Others (Boring, etc.)

- Metal Forming Tools

- Presses (Mechanical, Hydraulic, Servo)

- Forging Machines

- Bending Machines

- Others (Shearing, Extrusion, Rolling, etc.)

- Metal Cutting Tools

- By Technology

- Conventional Machines (Manually or Semi-Manually)

- CNC Machines

- Additive Manufacturing / Hybrid Machines

- By End-User Industry

- Automotive

- Aerospace & Defence

- Electrical & Electronics

- Industrial Machinery & Equipment

- Medical Devices

- Shipbuilding & Marine

- Precision Engineering

- Energy & Power

- Metal Fabrication (Job Shops, etc.)

- Other Industries (Railway, Other General Manufacturing, etc.)

- By Sales Channel

- Direct Sales (OEMs to End Users)

- Dealers & Distributors

- Online / E-commerce

- Others (System Integrators, Events & Exhibitions, Rebuilders & Refurbished, etc.)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Peru

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- Kuwait

- Turkey

- Egypt

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research begins with public statistics to set the demand and supply frame. We reviewed sources such as UN Comtrade and national customs dashboards for import and export trends, and we used industrial production series from agencies such as the US Federal Reserve and similar national statistics offices.

To anchor the manufacturing base, we referenced manufacturing output and PMI-style indicators from sources such as the World Bank, OECD, and national ministries of industry and trade. We also checked industry bodies and public technical publications, including organizations such as AMT and selected peer-reviewed journals, to confirm definitions and technology shifts, for example the mix of CNC and conventional tools. Company annual reports and investor presentations were used to validate regional exposure and product mix, and a paid subscription for company financials and a shipment-level import-export database were used selectively where public series are not granular enough. These desk sources are illustrative, and we used additional public references to cross-check, clarify, and validate data points.

Primary Interviews and Surveys

Primary work focused on manufacturers, distributors, and large end users in automotive, general engineering, and aerospace supply chains, since demand cycles differ across these buying groups. We also spoke with repair and retrofit specialists and industry consultants to pressure-test average selling price assumptions, replacement cycles, and the share of integrated CNC cells that gets booked with machine tool revenue across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 17% | APAC: 43% |

| Mid tier: 45% | Functional/Unit leaders: 36% | EMEA: 35% |

| Smaller Players: 20% | Managers: 47% | Americas: 22% |

Market-Sizing & Forecasting

Our sizing starts with a top-down build that reconstructs country and regional demand using manufacturing output signals, trade flows for machine tools and major categories, and investment cycles in metalworking capacity. Once this demand pool is formed, it is adjusted using replacement demand logic, known production hubs, and the typical share of CNC versus conventional equipment purchased by major end-use industries.

To keep the numbers grounded, we corroborate totals with selective bottom-up approximations that use sampled average selling prices multiplied by expected unit shipments, plus channel checks from distributors and integrators. Variables that matter in the model include industrial production growth, PMI direction, automotive and aerospace output trends, the pace of factory automation adoption, and machine tool pricing movement tied to components and materials. For forecasting, we use scenario analysis around the manufacturing cycle, and the base case is informed by expert views on capacity additions and order book momentum. Where bottom-up inputs are incomplete for smaller markets, gaps are handled using proxy indicators such as import dependence, machine tool intensity per manufacturing value added, and cross-country normalization before final rollup.

Data Validation & Update Cycle

Each estimate is checked through triangulation across independent signals, so large deviations are flagged early and corrected before finalization. Outliers at the country level are reviewed against trade statistics, production trends, and interview feedback, then a second analyst review is performed to confirm assumptions and math steps are consistent.

If a major shift is detected, such as policy-driven reshoring, sudden tariff changes, or sharp currency movement that impacts machine pricing, we re-contact sources and rerun key sensitivities. Reports are refreshed annually, and interim updates are made when material events change demand or pricing expectations. Before delivery, we recheck the latest public releases so clients receive an updated view.

Mordor Intelligence's Machine Tools Market Size Compared Against Other Published Estimates

Published market values for machine tools often do not match, and the difference is usually not about math alone. It is more often tied to what is counted as a machine tool sale, how CNC systems are treated, and whether services and accessories are included in the same number.

Some published figures fold accessories, refurbished equipment, and service revenue into the same pool, and they also project price increases faster than what channel checks support. For Mordor Intelligence, the count is limited to new, factory-built machine tool equipment sales, with integrated CNC cells included but used machines, software-only upgrades, and most aftermarket services excluded. This keeps the estimate tied to equipment purchase decisions in manufacturing.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 108.47 B (2025) | |

| Global Consultancy A | USD 117.20 B (2025) | Uses a wider inclusion set that appears to capture a broader range of machine-tool-adjacent demand, and it does not clearly separate equipment-only revenue from service and upgrade spend in its public summary. |

| Industry Publisher B | USD 109.30 B (2025) | Includes accessories as a stated tool type and may blend mixed revenue lines across conventional and CNC ecosystems, which can shift the total depending on how attachments and add-ons are priced and counted. |

The spread in the table is explained mainly by scope choices and pricing assumptions rather than a single forecasting formula. When the scope is kept to new equipment sales and then validated against trade flow signals and buyer replacement behavior, the final size becomes easier to trace back to repeatable steps and clearer demand drivers.

Key Questions Answered in the Report

How large is the machine tools market in 2026?

The Machine Tools Market size is expected to reach USD 112.03 billion in 2026 and grow at a CAGR of 3.28% to reach USD 131.63 billion by 2031.

Which product segment is expanding the fastest?

Multi-axis machining centers are expected to grow at a 6.88% CAGR between 2026 and 2031, the highest among all product categories.

Why is aerospace demand outpacing automotive growth in this market?

Aerospace & defence programs need high-speed, multi-axis machining for titanium and composite parts, pushing their segment to a 6.62% CAGR versus a mature automotive base.

How is Industry 4.0 reshaping machine tool purchasing decisions?

AI-enabled CNC controls, digital twins, and predictive maintenance services are becoming standard, turning machines into connected assets that provide real-time performance data.

What role do online sales channels play in equipment procurement?

E-commerce platforms now grow at an 7.74% CAGR, offering configuration tools and financing calculators that shorten buying cycles for mid-range CNC models.

Which regions are most attractive for new machine tool investments?

Asia-Pacific leads with 45.10% revenue share and a 6.05% CAGR, while North America is buoyed by reshoring incentives and semiconductor factory construction.

Page last updated on: