Metal Cutting Tools Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 27.46 Billion |

| Market Size (2030) | USD 32.53 Billion |

| Growth Rate (2025 - 2030) | 3.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

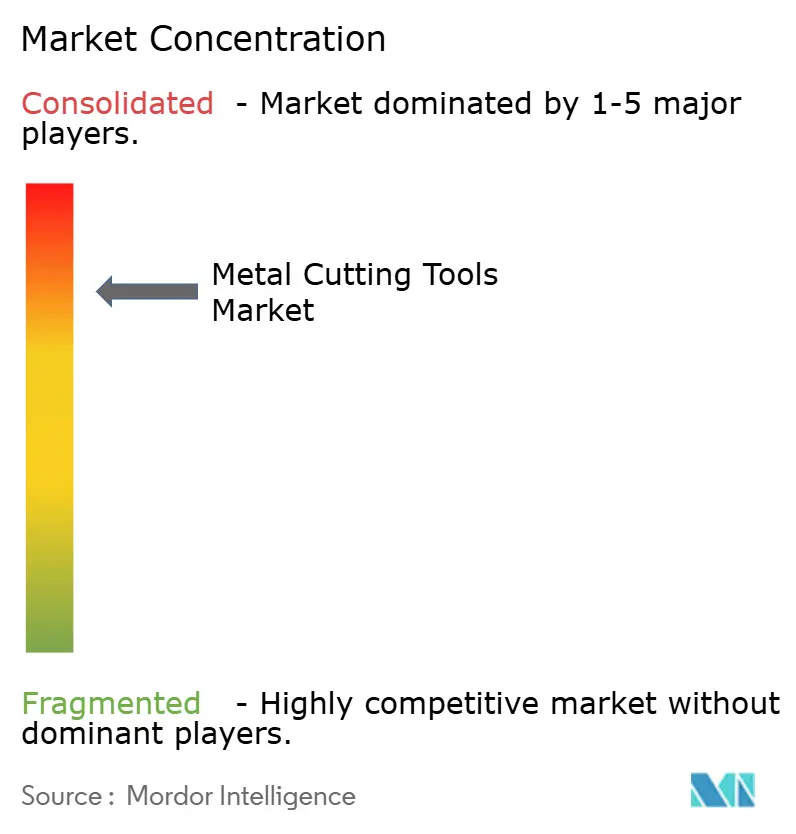

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metal Cutting Tools Market Analysis by Mordor Intelligence

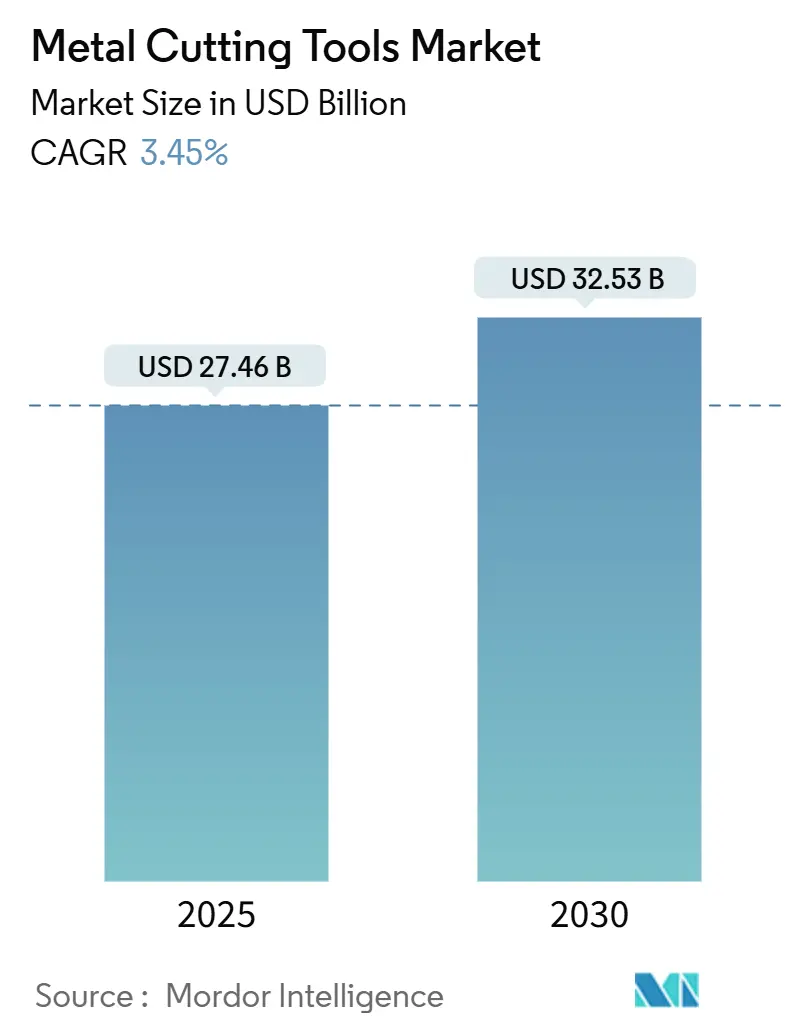

The Metal Cutting Tools Market size is estimated at USD 27.46 billion in 2025, and is expected to reach USD 32.53 billion by 2030, at a CAGR of 3.45% during the forecast period (2025-2030). Stable investment in precision manufacturing, surging electric-vehicle (EV) output, and a recovering aerospace backlog lift demand for high-performance cutters that can machine aluminum, titanium, and composite alloys efficiently. Industry 4.0 integration increases the value of smart tools that transmit wear data and interface seamlessly with digital twins, steering procurement away from commodity inserts toward sensor-enabled solutions. Asia-Pacific retains its status as the largest production hub thanks to China’s industrial rebound and India’s incentive programs, while North American buyers accelerate the reshoring of tooling purchases for supply-chain security. Consolidation among top suppliers continues as Sandvik, Kennametal, and IMC Group acquire software firms and specialty grades to bundle digital machining services with physical tools.

Key Report Takeaways

- By tool type, milling tools led with a 38% revenue share in 2024, while gear-cutting tools are projected to post the fastest 7.8% CAGR to 2030.

- By material, carbide commanded 63% of the metal cutting tools market share in 2024; polycrystalline diamond (PCD) tools are forecast to expand at an 8.5% CAGR through 2030.

- By end-user, automotive held 27% of the 2024 demand, whereas EV manufacturing is poised for a 9.2% CAGR to 2030.

- By geography, Asia-Pacific accounted for 48% of global sales in 2024 and is expected to grow at a 6.4% CAGR to 2030.

Global Metal Cutting Tools Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-led rebound in automotive production | +1.2% | Global (APAC, North America) | Medium term (2-4 years) |

| Industrialisation surge across APAC | +0.8% | APAC & MEA | Long term (≥ 4 years) |

| Industry 4.0 demand for smart tools | +0.6% | Global (developed markets) | Medium term (2-4 years) |

| Expanding aerospace backlog | +0.5% | North America & Europe | Short term (≤ 2 years) |

| Rise of difficult-to-machine alloys | +0.4% | Global | Long term (≥ 4 years) |

| Hybrid additive–subtractive manufacturing | +0.3% | North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV-Led Rebound in Automotive Production

EV platforms demand ±0.1 mm tolerances for battery housings and ultra-flat laminations for electric motors, driving rapid uptake of PCD and coated-carbide cutters that withstand abrasive aluminum chips while delivering 20–200 times the life of uncoated grades. High-pressure coolant systems and vibration-damping shanks become standard to maintain surface integrity on lightweight alloys. Automated cells rely on predictable wear data, so tooling suppliers integrate RFID or Bluetooth sensors that alert operators before catastrophic failure. As global EV volume climbs, procurement shifts from price-driven contracts to life-cycle cost evaluations that reward vendors offering condition-monitoring software and regrinding services.

Industrialization Surge Across APAC

Recovery in China’s Purchasing Managers’ Index above the 50-point threshold and India’s Production-Linked Incentive schemes for 14 sectors boost capital expenditure on CNC machining centers that need premium inserts. Indonesia’s Making Indonesia 4.0 and Malaysia’s Industry4WRD policies further widen the regional customer base for advanced tooling. Local factories increasingly specify ISO-compliant toolholders with embedded chips for usage tracking to align with sustainability audits. Demand for reconditioning grows as firms embrace circular-economy practices, extending cutter life by up to 70% and reducing raw-material imports.

Industry 4.0 Demand for Smart Tools

Machine-agnostic sensor modules now stream temperature, vibration, and cutting-force data directly to shopfloor MES dashboards, cutting unplanned downtime by 25% in early adopter plants. AI-driven parameter optimization shortens setup by 40%, while digital twins allow virtual validation of tool paths, slashing scrap in first-article runs. Software capability, therefore, becomes a key differentiator; firms without in-house coding teams risk margin erosion as customers favor integrated tool-and-code bundles. Open-protocol communication standards, such as MTConnect, speed adoption, although cybersecurity for edge devices remains a concern.

Expanding Aerospace Backlog

Rising build rates for narrow-body jets and engine overhauls sustain strong demand for cutters that hold edge integrity in Ti-6Al-4V at 800 °C. Manufacturers switch to multi-layer CVD-coated carbide and whisker-reinforced ceramic end-mills to reduce notch wear. Hybrid repair cells combine laser cladding with five-axis finishing, spawning new SKUs optimized for additive re-machining. Strict traceability rules push toolmakers to supply batch-level wear data and quality certificates, favoring organized vendors over spot-market resellers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility (tungsten, cobalt) | -0.4% | Global, with China supply concentration risk | Short term (≤ 2 years) |

| Laser / water-jet substitution | -0.3% | Global, concentrated in sheet metal processing | Medium term (2-4 years) |

| Tool re-conditioning lengthening tool life | -0.2% | Global, mature markets leading adoption | Medium term (2-4 years) |

| Near-net-shape AM cuts metal-removal volumes | -0.1% | North America & Europe early adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility (Tungsten, Cobalt)

China’s tighter export qualifications for ammonium para-tungstate triggered a 10% rise in sodium tungstate spot prices in early 2025, inflating cemented-carbide costs. The restart of South Korea’s Sangdong mine offers partial relief, yet global dependence on Chinese supply remains above 75%. Cobalt fluctuations further strain margins because specialty grades require strict chemistry for thermal stability. Toolmakers respond by stockpiling raw materials, broadening supplier bases, and accelerating R&D into alternative binders, but pass-through costs still dampen near-term cutter demand for general-purpose applications.

Laser / Water-Jet Substitution

Fiber-laser systems cut 4 mm stainless steel at 30 m/min and achieve ±0.05 mm repeatability, reducing demand for mechanical sawing in sheet-metal shops. Water-jets add flexibility to trim composites without heat-affected zones, encroaching on some milling tasks. Yet lasers struggle with parts thicker than 25 mm, and water-jets exhibit slower cycle times on high-volume runs, leaving traditional tools indispensable for heavy machining and 3-D geometries. Hybrid workflows that laser-cut blanks before milling features partially offset substitution losses by creating new finishing requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tool Type: Milling Retains the Productivity Edge

Milling tools captured 38% of 2024 global revenue, reflecting their versatility for roughing and precision finishing across automotive, aerospace, and general engineering components. The metal cutting tools market size for milling will expand steadily as five-axis machines dominate new equipment purchases, enabling complex shapes in a single setup. Adoption of high-helix, multi-flute geometries improves chip evacuation in aluminum EV housings, while vibration-damped holders cut cycle time on thin-wall aerospace parts. Embedded RFID tags help track insert life, a critical feature as unmanned machining hours rise.

Gear-cutting tools, though just 6% of 2024 sales, are forecast to register the fastest 7.8% CAGR through 2030 on the back of EV planetary transmissions and utility-scale wind-turbine gearboxes. Suppliers roll out indexable carbide hobs with advanced AlTiCrN coatings that resist adhesive wear in austempered iron. Concurrently, turning and drilling maintain relevance in powertrain shafts and precision hole-making for aero-structures. Sawing faces headwinds from fiber-laser substitution, but demand for large-diameter carbide-tipped bandsaw blades persists in steel service centers.

By Material: Carbide Dominates, PCD Accelerates

Carbide continued to hold a commanding 63% share of the metal cutting tools market in 2024, headlined by fine-grain grades that balance toughness and hot hardness across steels and cast irons. Advances in nano-layer coatings extend edge life by up to 30% and allow dry machining at higher parameters, aligning with sustainability goals. The emergence of powder-bed binder-jet printing for cemented-carbide blanks enables complex coolant-through channels that boost chip evacuation.

PCD is projected to grow at an 8.5% CAGR, the highest among materials, as automakers substitute aluminum for stamped steel to reduce vehicle mass and extend EV range. Multi-edge PCD end-mills deliver 10 µm surface roughness in a single pass, eliminating secondary polishing steps. CBN remains the tool of choice for hardened steels above 58 HRC in gearbox and bearing races, while cermets fill the cost-performance gap for mid-range ISO P workpieces. Emerging ceramic grades leverage reinforced SiAlON matrices to tackle heat-resistant superalloys at cutting speeds beyond 300 m/min.

By End-User Industry: Automotive Dominant, EV Drives Momentum

The automotive sector absorbed 27% of global cutting-tool demand in 2024, reflecting engine block, transmission, and chassis machining volumes. Yet powertrain electrification reshapes requirements toward thin-wall aluminum casings, stator stacks, and battery trays. Suppliers invest in diamond-coated router bits and solid-carbide slot drills tailored for battery-cell frames. Inline measurement probes within machining centers tighten process capability to Cp 1.67 or better.

EV manufacturing is set to clock a robust 9.2% CAGR through 2030, outpacing combustion-engine segments and underpinning long-term growth for advanced tool grades. Aerospace follows closely, capitalizing on renewed aircraft deliveries and defense modernization. General machinery and medical devices remain steady, the latter demanding ultra-sharp micro-tools under 0.5 mm for orthopedic implants, where burr-free edges are vital to biocompatibility.

Geography Analysis

Asia-Pacific commanded 48% of 2024 global revenue and is forecast to post a 6.4% CAGR to 2030, reinforcing its position as the nucleus of the metal cutting tools market. Chinese OEMs accelerate five-axis machine adoption to climb the value chain, while India’s incentives channel USD 26 billion into electronics, automotive, and white-goods plants. Japan and South Korea maintain leadership in high-precision machining, though both navigate tighter tungsten supply due to Chinese export controls, prompting diversification into Vietnamese and Rwandan concentrates. Southeast Asian economies implement Industry 4.0 roadmaps, boosting demand for smart cutters with in-tool sensors.

North America benefits from surging EV assembly lines and a revived aerospace build rate that spurs procurement of PVD-coated inserts for titanium and nickel alloys. U.S. reshoring policies encourage OEMs to dual-source cutting tools locally, sustaining small-batch specialist firms as strategic suppliers. Canada’s linkage with U.S. automotive tooling chains provides a stable baseline demand, while Mexico attracts new drivetrain machining hubs seeking cost-effective yet durable cutters to serve near-shore assembly plants.

Europe remains a hotbed of tooling innovation, with Germany’s machine-tool cluster pioneering hybrid additive-subtractive platforms that require proprietary end-mills capable of machining as-built alloy microstructures. France leverages Airbus ramp-ups to secure long-term contracts for CBN and ceramic inserts, whereas Italy and Spain drive regional consumption through machinery exports. Regulatory pressure to lower carbon footprints pushes re-sharpening and recycling initiatives, helping extend tool life and reduce tungsten waste.

Competitive Landscape

Consolidation defines current market dynamics as established suppliers acquire niche technology firms to embed digital capabilities within their portfolios. Sandvik completed eight takeovers under its Mastercam banner in early 2025, expanding CAM software breadth and reinforcing its tool-to-code integration strategy. Kennametal counters with High-Infinity PVD coatings and micro-boring systems targeting medical and aerospace applications, while ramping efficiency programs to offset raw-material inflation. ISCAR’s LOGIQUICK series promises faster chip clearance in tough alloys by combining wiper geometry with precision-ground chip splitters.

Mid-tier players pursue specialization to fend off the scale advantages of conglomerates. Walter AG partners with Heller Maschinenfabrik to co-develop machining packages, bundling cutters, tool data, and kinematic simulation for turnkey projects. GWS Tool Group’s acquisition of Peterson Tool broadens custom-carbide capabilities, signaling investor appetite for engineered-to-order niches. Meanwhile, Hyperion Materials & Technologies strengthens vertical integration by absorbing Damen Carbide Tool to secure a premium blank supply.

Digital differentiation gains prominence. Firms embed edge-computing chips in toolholders to stream wear analytics, offering subscription-based dashboards that generate recurring revenue. Start-ups exploit this shift by delivering cloud-native optimization platforms compatible with any ISO-standard shank, challenging incumbents to accelerate their software roadmaps. Sustainability also rises on boardroom agendas; leading brands launch take-back programs that recycle worn carbide, appealing to OEM ESG goals.

Metal Cutting Tools Industry Leaders

Sandvik AB (Sandvik Machining Solutions)

Kennametal Inc.

IMC Group (ISCAR, Ingersoll, Tungaloy)

Mitsubishi Materials Corp.

OSG Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Mastercam (Sandvik) acquired Barefoot CNC, CAD/CAM Solutions, CamTech Engineering Services, and CIMCO’s probing technology, rounding out eight takeovers in 2025 to extend its CAM ecosystem.

- February 2025: Sandvik scheduled Capital Markets Day for May 2025 to showcase digital machining and automation priorities.

- January 2025: Sandvik bought FASTech, a U.S. CAM reseller, strengthening distribution and support for digital manufacturing customers.

- January 2025: GWS Tool Group purchased Peterson Tool Company, expanding precision-carbide custom tooling in North America.

Global Metal Cutting Tools Market Report Scope

| Milling Tools |

| Turning Tools |

| Drilling Tools |

| Sawing Tools |

| Grinding Tools |

| Others (boring, threading, etc.) |

| Carbide |

| High-Speed Steel |

| Cermet |

| Ceramic |

| PCD (Poly-crystalline Diamond) |

| CBN (Cubic Boron Nitride) |

| Automotive |

| Aerospace & Defense |

| General Machinery |

| Construction Equipment |

| Power Generation & Oil-Gas |

| Medical Devices |

| Electronics & Semiconductors |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Tool Type | Milling Tools | |

| Turning Tools | ||

| Drilling Tools | ||

| Sawing Tools | ||

| Grinding Tools | ||

| Others (boring, threading, etc.) | ||

| By Material | Carbide | |

| High-Speed Steel | ||

| Cermet | ||

| Ceramic | ||

| PCD (Poly-crystalline Diamond) | ||

| CBN (Cubic Boron Nitride) | ||

| By End-User Industry | Automotive | |

| Aerospace & Defense | ||

| General Machinery | ||

| Construction Equipment | ||

| Power Generation & Oil-Gas | ||

| Medical Devices | ||

| Electronics & Semiconductors | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the metal cutting tools market?

The metal cutting tools market size is USD 27.46 billion in 2025 and is projected to reach USD 32.53 billion by 2030.

Which region dominates global demand?

Asia-Pacific accounts for 48% of worldwide revenue and is forecast to grow at a 6.4% CAGR through 2030.

What tool type leads sales today?

Milling tools hold the largest 38% market share thanks to their versatility across automotive, aerospace, and general engineering components.

Which material segment is growing fastest?

Polycrystalline diamond tools are expected to log an 8.5% CAGR to 2030, driven by the shift toward aluminum machining in EV and aerospace production.

How are suppliers responding to Industry 4.0?

Leading companies embed sensors in cutters, acquire CAM software firms, and provide cloud dashboards that help users predict wear and optimize cutting parameters.

What raw-material risks affect pricing?

Volatility in tungsten and cobalt supply—exacerbated by Chinese export controls—adds cost pressure and may limit availability of standard carbide tools in the near term.

Page last updated on: