Floor Grinding Machine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

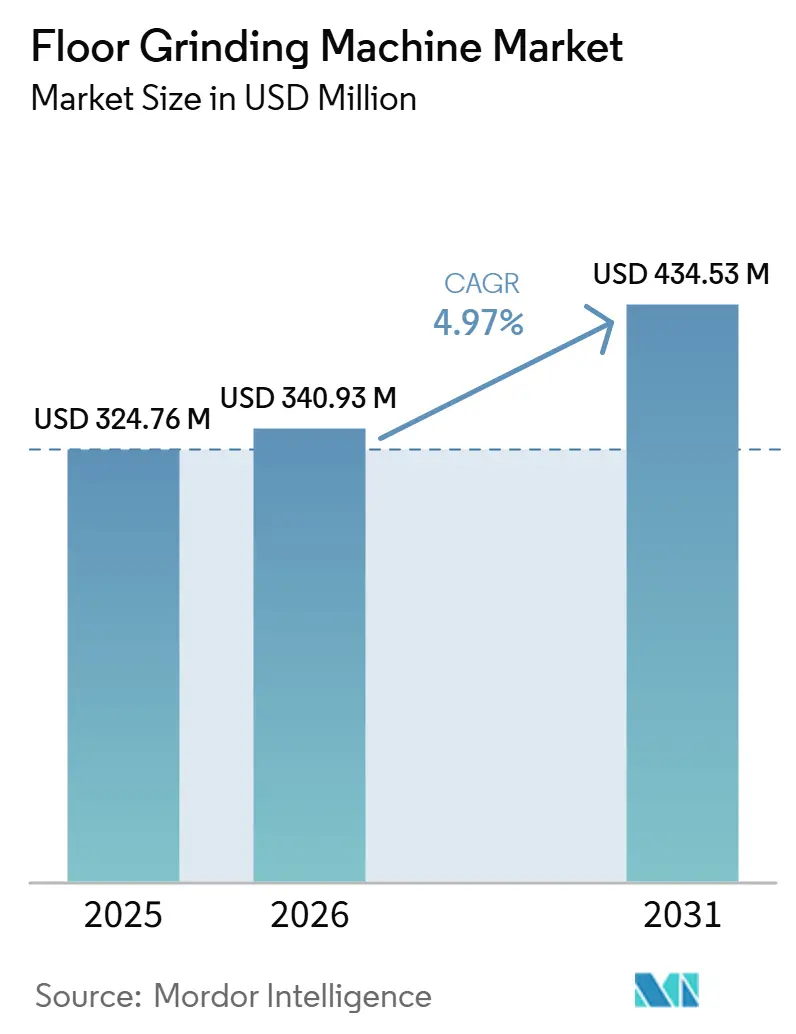

| Market Size (2026) | USD 340.93 Million |

| Market Size (2031) | USD 434.53 Million |

| Growth Rate (2026 - 2031) | 4.97% CAGR |

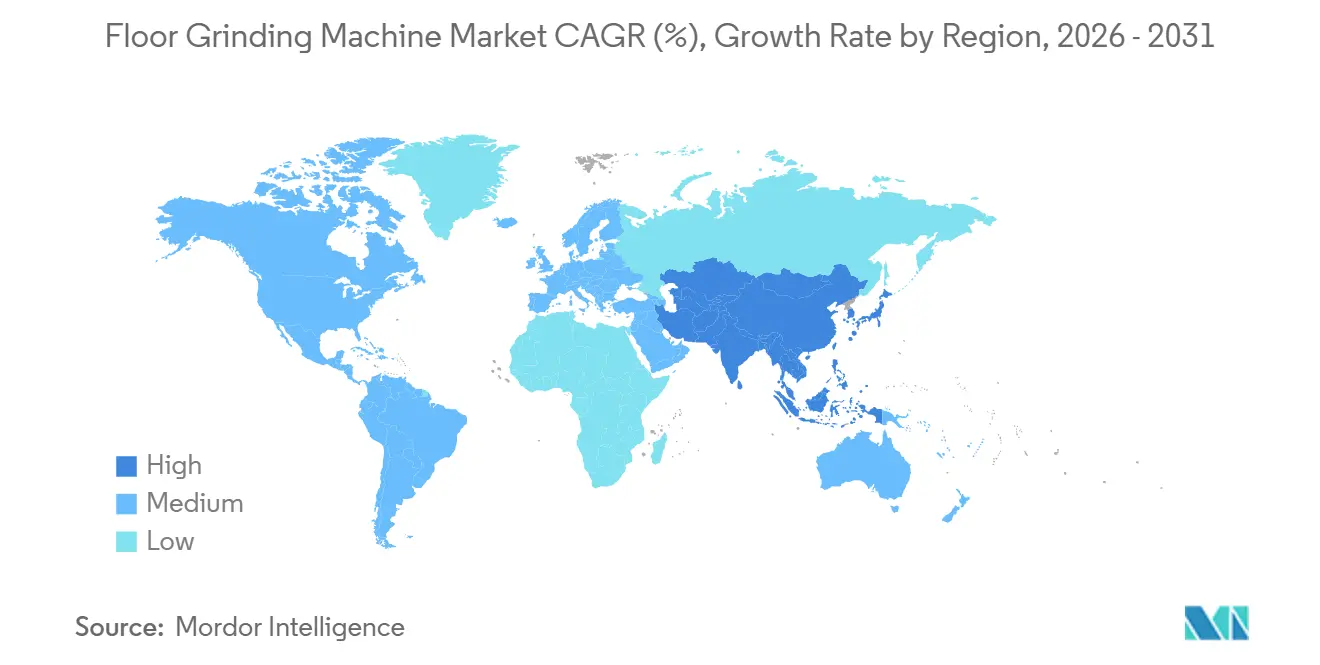

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Floor Grinding Machine Market Analysis by Mordor Intelligence

The Floor Grinding Machine Market size is expected to increase from USD 324.76 million in 2025 to USD 340.93 million in 2026 and reach USD 434.53 million by 2031, growing at a CAGR of 4.97% over 2026-2031.

Demand is consolidating around electrification, remote operation, and consumable innovation as contractors adapt to persistent labor scarcity and higher upfront equipment thresholds. Interest in autonomy is rising as suppliers showcase production-ready compactors and guidance platforms that reduce operator exposure and improve site productivity. Industrial demand is accelerating on the back of data center buildouts and manufacturing reshoring, while funding and scheduling volatility keep commercial projects cautious. Asia-Pacific leads both installed base and growth as maintenance backlogs and logistics investments offset softness in parts of China’s state-led infrastructure pipeline. Equipment pricing dynamics remain a watch point as the Producer Price Index for construction machinery stays elevated and many contractors bring forward purchases to hedge tariff exposure.

Key Report Takeaways

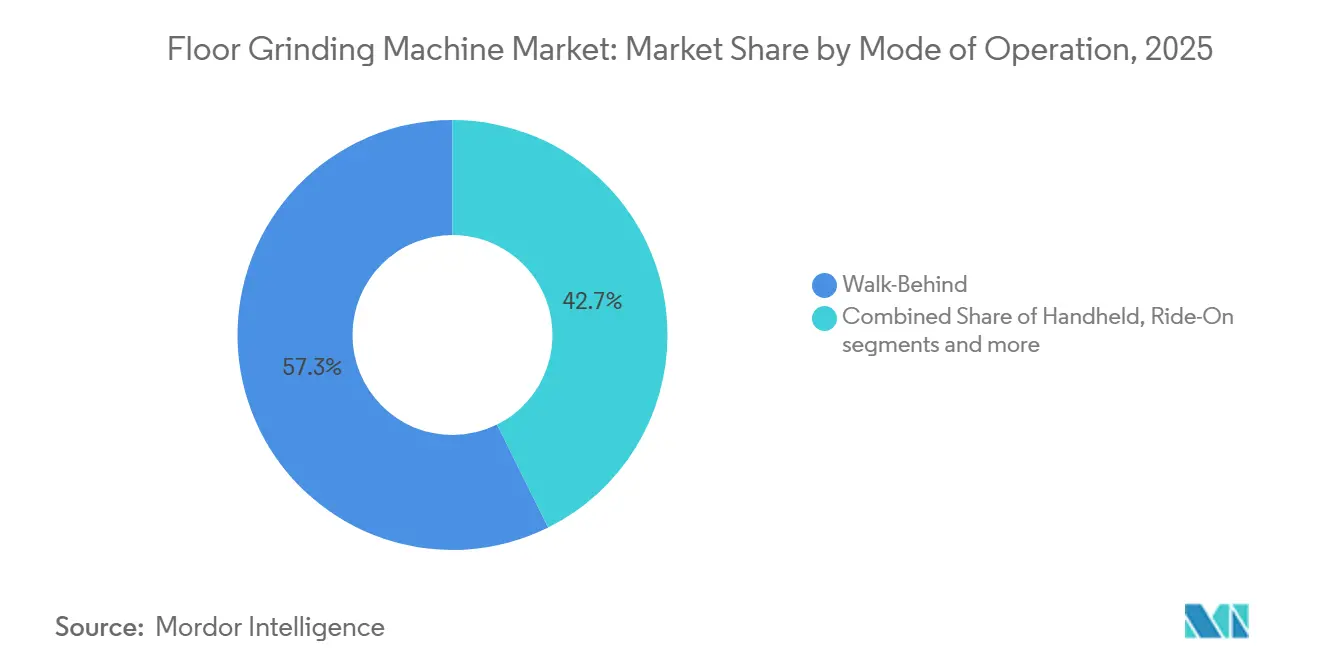

- By mode of operation, walk-behind led with 57.34% of the floor grinding machine market share in 2025, while others, including remote-controlled and autonomous variants, recorded the highest projected CAGR at 6.12% through 2026-2031.

- By grinding mechanism, dry systems held 64.81% share in 2025, while wet systems are forecast to expand at a 6.23% CAGR to 2026-2031.

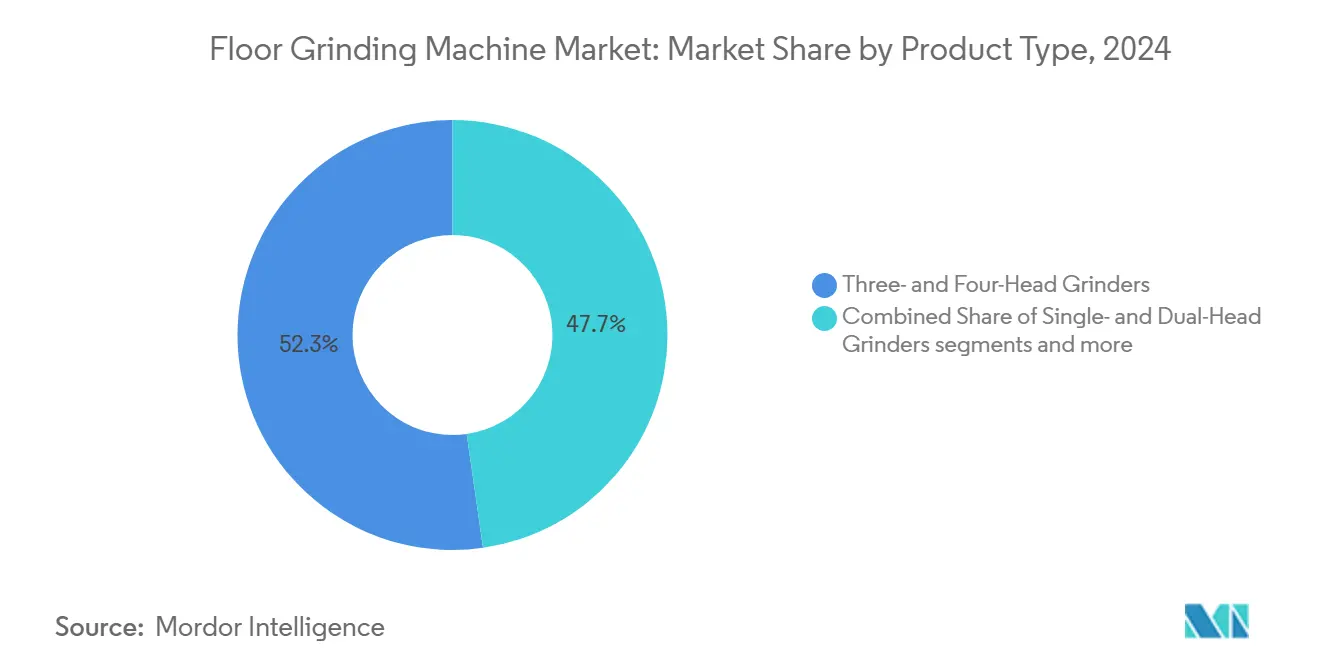

- By product type, three- and four-head grinders accounted for 46.71% of 2025 volume, while other configurations, including custom and multi-head designs, recorded a 5.76% projected CAGR to 2026-2031.

- By end-user vertical, commercial accounted for 52.80% in 2025, while industrial is projected to post the fastest 5.34% CAGR through 2026-2031.

- By geography, Asia-Pacific held 43.21% of the floor grinding machine market size in 2025 and is projected to expand at a 6.47% CAGR to 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Floor Grinding Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Popularity of Polished Concrete Flooring | +1.2% | Global, with early gains in North America data centers, Asia-Pacific logistics hubs | Medium term (2-4 years) |

| Expansion of Warehouse and Logistics Infrastructure | +0.9% | APAC core, spill-over to the Middle East and Africa | Medium term (2-4 years) |

| Rising Commercial and Industrial Renovation Activity | +1.0% | North America & EU, driven by aging infrastructure mandates | Short term (≤ 2 years) |

| Increasing Demand for Decorative and Stained Concrete Floors | +0.7% | North America residential & commercial, emerging in Latin America | Long term (≥ 4 years) |

| Growth in Epoxy and Resinous Flooring Installations | +1.1% | Global, compliance-driven in pharmaceuticals, food processing, and electronics manufacturing | Short term (≤ 2 years) |

| Infrastructure Maintenance and Concrete Repair Programs | +0.8% | North America, Europe, municipal bridge and pavement programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Popularity of Polished Concrete Flooring

Nonresidential construction starts in the United States show a 53.3% year-over-year increase to USD 80.3 billion in January 2026, signaling a strong pipeline that supports sustained floor preparation activity in large facilities. Data center spending rose 32% in 2025 and is poised to grow by 26% in 2026 and 17% in 2027, which anchors demand for high-spec polished concrete in hyperscale projects that require durable, low-maintenance slabs. Owners continue to manage risk as the AIA reports a prolonged period of weaker billings along with broad reports of postponements, which keep contractors focused on methods that cut material use and compress schedules. Polished concrete systems cut material consumption and speed up schedules, and vendor documentation shows significant energy and program-time savings for surface preparation paths that avoid heavy toppings and long cure windows. The ACI 310.1-20 specification provides a clear framework for finish levels and process steps, which helps standardize procurement on large federal and commercial builds. Labor remains the binding constraint, and persistent craft shortages keep interest high in process designs and equipment choices that reduce passes and contain on-site headcount in the floor grinding machine market. [1]AGC Research Team, “2025 Workforce Survey Analysis,” Associated General Contractors of America, agc.org

Expansion of Warehouse and Logistics Infrastructure

Warehouse construction is normalizing after the pandemic surge as near-term growth remains muted in 2026 with modest improvement projected for 2027, which shifts activity toward selective upgrades rather than broad new footprints. Even with that moderation, the share of e-commerce and logistics assets in overall building spending expanded compared to 2019, and retrofit cycles keep recurring demand for slab repair, grinding, and epoxy overlays. In China, headline infrastructure and land supply metrics contracted in 2025 while private infrastructure investment edged up, an investment mix that favors logistics parks and cold storage where hard-wearing surfaces and surface preparation standards are tightly specified.[2]National Bureau of Statistics of China, “Statistical Communiqué of the PRC on the 2025 National Economic and Social Development,” NBS China, stats.gov.cn Energy-focused renovation programs in mature Asia markets document significant savings from HVAC, lighting, and envelope upgrades, and those projects frequently incorporate slab preparation stages that rely on grinders for adhesion-critical finishes. Contractors continue to hedge tariff exposure through bid adjustments and earlier purchasing decisions, a behavior that influences fleet refresh timing and the capacity available for surface preparation packages in the floor grinding machine market. Compliance expectations for seamless, cleanable surfaces remain high in controlled environments, and U.S. federal resinous-flooring specifications continue to influence material and process choices in logistics-linked facilities.

Rising Commercial and Industrial Renovation Activity

Institutional categories are moving higher through 2027, with healthcare among the brightest spots, and that steady program mix supports recurring surface preparation requirements for coatings and polish systems in active buildings. Monthly nonresidential starts data confirms renewed momentum in early 2026, and renovation packages in occupied facilities tend to favor mechanical grinding sequences that control dust and enable faster returns to service. City-level requirements elevate the baseline for rehabilitation planning, including Physical Needs Assessments and scope inclusion rules that trigger floor system replacements when effective remaining life thresholds are reached. Municipal programs also support surface rehabilitation, with Dallas outlining multi-year street and sidewalk investments and referencing automated assessment methods that raise inspection consistency across pavement assets. Smaller local projects add to the pipeline through permeable pavement and parking lot upgrades that require mechanical preparation for adhesion and flatness control. State cost indices underscore material volatility that owners and contractors must navigate when planning scope for slab repairs and overlays in the floor grinding machine market.[3]Colorado DOT EEMA, “Construction Cost Index Q3 2025,” Colorado Department of Transportation, codot.gov

Increasing Demand for Decorative and Stained Concrete Floors

Public specifications in Canada outline concrete finishing requirements, curing windows, and product performance criteria for floor hardeners and sealers that shape surface preparation workflows in public buildings. Contractors continue to balance aesthetics and performance in plazas, lobbies, and atriums, which drives demand for repeatable multi-step grinding sequences and compatible densifier and stain systems in the floor grinding machine market. Supply chain sentiment has improved for many categories, although electrical equipment remains a notable bottleneck that can delay project closeout for flooring packages that rely on dust extraction power and control components. Training and certification outlays remain meaningful parts of a contractor’s cost structure, which can slow adoption of advanced decorative systems that require more steps and complexity. Operator credential rules in key states maintain experience and exam standards for crane and heavy-equipment roles, and those requirements indirectly shape staffing availability for flooring preparation crews that integrate heavier equipment. Associations provide nationally recognized certifications with five-year validity that support safety and consistency goals as decorative and specialty flooring activity expands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Investment for Professional Equipment | -0.9% | Global, acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Shortage of Trained and Experienced Operators | -1.1% | North America, Europe, Australia, and severe in crane and heavy equipment roles | Medium term (2-4 years) |

| Physical Demands and Operator Fatigue Issues | -0.5% | Global, intensified by an aging workforce | Long term (≥ 4 years) |

| High Consumable Costs Impacting Project Economics | -0.7% | Global, tied to steel volatility and diamond-tool margins | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Investment for Professional Equipment

Pricing indices for construction machinery remain elevated in early 2026, which extends payback periods for new grinders and dust extraction systems. In Canada, machinery and equipment prices for construction end uses also trend higher, which compounds acquisition hurdles for smaller contractors. Many firms adjusted bids and procurement timing in response to tariffs and proposed duties, and that behavior impacts the cadence of fleet refresh across the floor grinding machine market. Certification and training add to upfront costs, including state-level programs with defined tuition and time commitments that must be managed against job-site schedules. States that require documented experience and examinations for crane operators preserve safety baselines but increase hurdles for companies that need to scale heavy-equipment operations in surface preparation. Vendor disclosures also show margin pressure in construction equipment businesses in 2024, which reinforces the role of consumables and services in total cost of ownership decisions.

Shortage of Trained and Experienced Operators

Most construction firms report difficulty filling open roles, and skilled equipment operators are among the hardest jobs to staff, which constrains project throughput. Surveys show widespread craft openings and persistent skills gaps, and firms also report early attrition and credential limitations among candidates. Labor scarcity causes schedule delays and forces contractors to rebalance crews, which places a premium on grinders and dust extraction that simplify operation and reduce physical strain. State certification regimes reinforce experience and knowledge requirements for heavy equipment, and those standards shape the available pool for roles adjacent to floor preparation tasks. National certifications provide consistent baselines and are recognized across employers, which helps firms manage mobility and safety in the floor grinding machine market. Immigration channels remain a limited relief valve for many firms, which maintains pressure on wages and training budgets during 2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Operation: Walk-Behind Dominance Meets Autonomous Momentum

Walk-behind grinders held 57.34% in 2025, a position sustained by retrofit economics and broad operator familiarity that reduces changeover time across removal and polishing tasks in the floor grinding machine market. Ride-on platforms are favored for high-throughput environments such as large logistics retrofits and data center slabs, where coverage targets justify higher capital, although staff availability remains a constraint for many crews. Remote-controlled and autonomous variants are projected to grow at 6.12% through 2031 as suppliers introduce systems that reduce operator exposure and provide steadier productivity. Autonomous compactors and connected asset platforms showcased in 2026 highlight the direction of jobsite automation that will influence floor equipment controls and safety features over time. Handheld and edge-focused models fill specialty roles near columns and walls, reducing manual fatigue and extending the life of corner work in the floor grinding machine industry.

This mix reflects persistent hiring challenges that push contractors to favor platforms with simpler training paths and less intensive supervision in the floor grinding machine market. Remote controls help address fall hazards and reduce fatigue hours, which aligns with safety and productivity objectives at prime contractors and owners. Vendors continue to integrate guidance, dust control, and telematics features that support consistent outcomes and lower rework probability on fast-track jobs. The floor grinding machine market size for others, including remote-controlled and autonomous variants, is projected to expand at a 6.12% CAGR through 2031, which sets a higher bar for user interfaces and support ecosystems. As 2026 progresses, firms that balance training pipelines with incremental autonomy adoption are best positioned to protect margins on complex surface preparation packages.

By Grinding Mechanism: Dry Systems Lead on Cleanroom Mandates, Wet Gains on Infrastructure Cycles

Dry grinding machines commanded 64.81% share in 2025, supported by HEPA-grade dust extraction and highly efficient separation that maintains air quality in sensitive environments within the floor grinding machine market. Federal specifications for resinous flooring in controlled and mission-critical spaces reinforce dust containment and surface profile requirements that align well with dry grinding setups. Wet grinding systems, although smaller in base, are projected to grow at 6.23% through 2031 as bridge-deck rehabilitation and permeable pavement programs sustain demand for slurry-compatible preparation where airborne silica must be suppressed. Municipal investment rounds and state-level cost changes in concrete and reinforcing steel add to the public-works pipeline that often uses wet methods for specific prep and polishing tasks in the floor grinding machine market.

Equipment designs with integrated water tanks and corrosion-resistant guards improve changeover time and reduce cleanup, which supports broader use of wet cycles where jobsite conditions permit. Electrical component bottlenecks can slow equipment deliveries for both mechanisms, and contractors report delays that ripple into surface preparation timelines in 2026. The floor grinding machine industry continues to match mechanism choices to environmental controls and schedule needs, with dust extraction and filtration performance often determining the method for healthcare and semiconductor facilities. The floor grinding machine market size for wet grinding is set to advance at a 6.23% CAGR through 2031, supported by public infrastructure maintenance and municipal resurfacing plans.

By Product Type: Three- and Four-Head Balance Throughput with Custom Configurations Rising

Three- and four-head grinders accounted for 46.71% of unit volume in 2025, balancing throughput and portability for mid-scale contractors that require predictable performance in varied interiors within the floor grinding machine market. Larger planetary systems provide steady coverage rates while fitting common elevators and door widths, which makes them practical for retrofit projects with constrained logistics. Single- and dual-head grinders continue to anchor residential and edge work where capital costs and setup simplicity matter most, with vendor offerings addressing safety and productivity in small-area removal and polish. Custom and multi-head configurations are on a faster growth path at 5.76% as large projects move to 24-hour cycles and prioritize consistent flatness and gloss outcomes across very large bays in the floor grinding machine market.

Equipment examples illustrate the range of options from heavy multi-head units for expansive areas to redesigned planetary grinders that improve balance and operating ergonomics. Starts data for early 2026 suggests a robust slate for big-box and hyperscale builds, although contractors continue to report cancellations and postponements in some categories based on funding conditions. Product innovation continued with self-operating grinders and refined remote-control systems that reduce physical strain and deliver more consistent passes in the floor grinding machine market. Training and safety remain central themes, and many firms cite inexperienced labor as a top site challenge, which supports designs that simplify operation and maintenance.

By End-User Vertical: Commercial Leads Installed Base, Industrial Sprints on Reshoring, and Data Centers

Commercial applications held 52.80% in 2025, supported by the wide adoption of polished concrete in retail, hospitality, and offices under standardized finish specifications that enable predictable outcomes across portfolios in the floor grinding machine market. Momentum in early 2026 is visible in starts data while forecasts still call for measured growth in commercial segments, which keeps attention on fast, predictable surface preparation sequences. Industrial facilities are on a faster path at a 5.34% CAGR, reflecting reshoring and expansion in higher-spec manufacturing, and those projects rely on surface preparation that supports resinous and polish systems in regulated environments. Project examples and disclosures from autonomy providers show large-scale excavation and equipment coordination that point to broader digital adoption patterns across site work and interiors.

Residential use remains a smaller share and centers on decorative overlays and localized surface correction, while institutional and infrastructure applications benefit from healthcare and municipal program stability. Workforce gaps continue to pressure schedules and budgets for all end-users in 2026, which keeps owners and contractors focused on equipment and methods that reduce operator hours and training intensity in the floor grinding machine market. The floor grinding machine market size for industrial users is projected to expand at a 5.34% CAGR, and specification frameworks for coatings and resinous systems support repeatable preparation methods that scale across sites.

Geography Analysis

Asia-Pacific led with 43.21% in 2025 and is projected to grow at a 6.47% CAGR, and that combination reflects strong retrofit demand in logistics, manufacturing, and institutional assets despite a softer backdrop for state-led infrastructure in parts of the region in the floor grinding machine market. China’s 2025 statistics show declines in certain infrastructure and land supply categories while private infrastructure investment increased, which points to a more granular project mix that emphasizes interior upgrades and targeted expansions. Japan’s published evaluations of office energy retrofits highlight the scope for performance upgrades that often include slab preparation for coatings and finishes. Regional product strategies include upgraded dust extraction and tool ecosystems as suppliers align with growth pockets and compliance needs. The floor grinding machine market size in Asia-Pacific benefits from ongoing investments in logistics hubs and sensitive manufacturing, where dust control and repeatable surface profiles are central to project success.

North America exhibits near-term volatility with a strong start to 2026 in nonresidential construction alongside cautious multi-year forecasts for several commercial categories in the floor grinding machine market. Data centers are a primary bright spot with sustained double-digit growth through 2027, and that activity anchors high-spec polish and coating work. City programs in places like Dallas and project rounds in suburbs such as Brookfield add recurring work in sidewalks, streets, and green parking areas that require mechanical preparation. Bridge and pier repair initiatives also support wet grinding demand within civil scopes. Labor constraints remain a widespread limiter on throughput, and pricing indices for construction machinery underline higher input costs that guide capital planning in 2026 in the floor grinding machine market.

In Europe, renovation cycles and resinous-flooring mandates play central roles as institutional facilities move higher in 2026 and 2027, and coatings suppliers document low-VOC, EN-standard-compliant systems for sensitive interior uses. U.S. federal specifications for resinous flooring are frequently referenced across allied facilities, and their emphasis on bonding and moisture conditions supports consistent preparation workflows. Leading vendors continue to invest in electrification, dust extraction, and automated features that align with European standards and sustainability priorities in the floor grinding machine market. Canadian machinery price indices remain elevated, and firms report ongoing craft shortages, which indicates that pricing and labor will continue to shape European and transatlantic project delivery conditions.

Competitive Landscape

The floor grinding machine market is moderately concentrated across a set of global and regional manufacturers with complementary tool ecosystems, and leading players continue to emphasize consumables and accessories for margin resilience. Husqvarna, Bartell Global, and Scanmaskin anchor premium planetary segments, while EDCO, Terrco, and National Flooring Equipment maintain strong positions in walk-behind and single-disc niches. The strategic focus is shifting from unit pricing to interoperability, battery platforms, and HEPA-grade dust control, which raises switching costs and strengthens lifetime value through tool and accessory attachment in the floor grinding machine market.

Corporate actions reflect tightening integration across equipment and tooling as firms seek scale advantages and distribution reach. Product redesigns improve balance, transport, and operating ergonomics in the mid-size planetary class, which targets high-utilization contractors working across commercial and institutional interiors. Dust management is a key differentiator with multi-stage separation and high-efficiency filtration published by suppliers to meet project cleanliness and uptime needs in the floor grinding machine market.

Automation momentum is visible across adjacent equipment categories and influences expectations for grinder controls and jobsite connectivity. Companies document trials that coordinate autonomous and human-operated assets at scale, which reinforces practical pathways to staged autonomy adoption. Training partnerships and five-year credential frameworks help incumbents maintain safety and compliance across fleets as electronic and automated features expand in the floor grinding machine market.

Floor Grinding Machine Industry Leaders

Husqvarna Group

Blastrac

Superabrasive (Lavina)

Klindex

Scanmaskin

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Husqvarna launched the Autogrinder along with expanded electrification offerings and new energy-efficient corded floor grinders plus the DE 130 H dust extractor.

- January 2025: Tyrolit Group acquired 100% of Scanmaskin Group with plans to invest in floor preparation product portfolios while retaining operations in Lindome, Sweden.

Global Floor Grinding Machine Market Report Scope

The Floor Grinding Machine Market Report is Segmented by Mode of Operation (Handheld, Walk-Behind, Ride-On, and Others including Remote-Controlled/Autonomous), Grinding Mechanism (Wet Grinding Machines and Dry Grinding Machines), Product Type (Single- & Dual-Head Grinders, Three- & Four-Head Grinders, and Other Configurations including Custom/Multi-Head Configurations), End-user Vertical (Commercial, Industrial, Residential, and Others including Institutional and Infrastructure), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Handheld |

| Walk-Behind |

| Ride-On |

| Others (Remote-Controlled/Autonomous) |

| Wet Grinding Machines |

| Dry Grinding Machines |

| Single- & Dual-Head Grinders |

| Three- & Four-Head Grinders |

| Other Configurations (Custom / Multi-Head Configurations, specialized, etc.) |

| Commercial |

| Industrial |

| Residential |

| Others (Institutional, Infrastructure (Airports, Hospitals, etc.)) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Mode of Operation | Handheld | |

| Walk-Behind | ||

| Ride-On | ||

| Others (Remote-Controlled/Autonomous) | ||

| By Grinding Mechanism | Wet Grinding Machines | |

| Dry Grinding Machines | ||

| By Product Type | Single- & Dual-Head Grinders | |

| Three- & Four-Head Grinders | ||

| Other Configurations (Custom / Multi-Head Configurations, specialized, etc.) | ||

| By End-user Vertical | Commercial | |

| Industrial | ||

| Residential | ||

| Others (Institutional, Infrastructure (Airports, Hospitals, etc.)) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the floor grinding machine market size outlook and CAGR to 2031?

The floor grinding machine market size is expected to increase from USD 340.93 million in 2026 to USD 434.53 billion by 2031 at a 4.97% CAGR over 2026-2031.

Which region leads growth in the floor grinding machine market through 2031?

Asia-Pacific leads both base and growth, holding 43.21% in 2025 and projected to grow at a 6.47% CAGR through 2031.

Which mode of operation holds the largest position in 2025?

Walk-behind grinders led with 57.34% in 2025, supported by retrofit economics and operator familiarity.

How are regulations shaping material and method choices for floor preparation?

UFGS resinous-flooring specifications and ACI polished-concrete standards drive dust control, surface profile, and finish requirements that align closely with dry grinding and defined multi-step sequences.

What risks could affect equipment pricing and availability in 2026?

Elevated machinery price indices and tariff-driven procurement shifts, along with bottlenecks of electrical equipment, can delay deliveries and extend payback periods.

Which companies are shaping product and technology roadmaps?

Husqvarna expanded electrification and launched a self-operating grinder, while Caterpillar and Oshkosh showcased autonomous and AI-enabled systems, and Bedrock reported scaled autonomy trials.

Page last updated on: