Grinding Machines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.76 Billion |

| Market Size (2031) | USD 8.59 Billion |

| Growth Rate (2026 - 2031) | 4.89% CAGR |

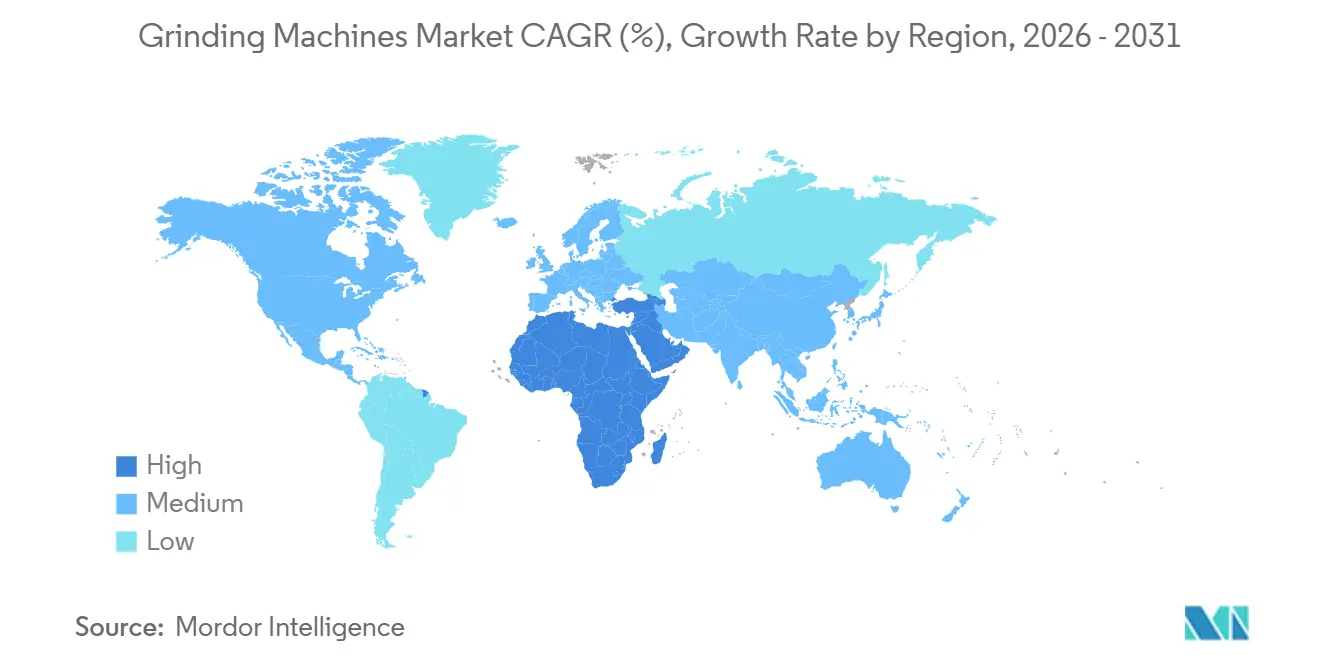

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Grinding Machines Market Analysis by Mordor Intelligence

The Grinding Machines Market size is expected to increase from USD 6.47 billion in 2025 to USD 6.76 billion in 2026 and reach USD 8.59 billion by 2031, growing at a CAGR of 4.89% over 2026-2031.

Growth reflects steady demand for precision components in complex assemblies, stronger investment in CNC automation to stabilize quality and throughput, and regional capacity additions in Asia-Pacific and the Middle East that lift installed bases. Productivity gains in U.S. manufacturing, supported by capital spending in advanced machining and better scrap control, are reinforcing the shift toward automated precision grinding. Energy efficiency policies and total-cost-of-ownership scrutiny are shaping procurement criteria, which pushes OEMs to build machines with efficient spindles, sensor-based process control, and connectivity for energy monitoring. Workforce imbalances and wage pressures are also nudging buyers toward integrated grinding cycles on multitasking platforms that reduce setups and operator dependency. Meanwhile, activity in aerospace turbines and electrified drivetrains is creating sustained programs where tolerance stacks and surface integrity demand repeatable sub-micron performance.

Key Report Takeaways

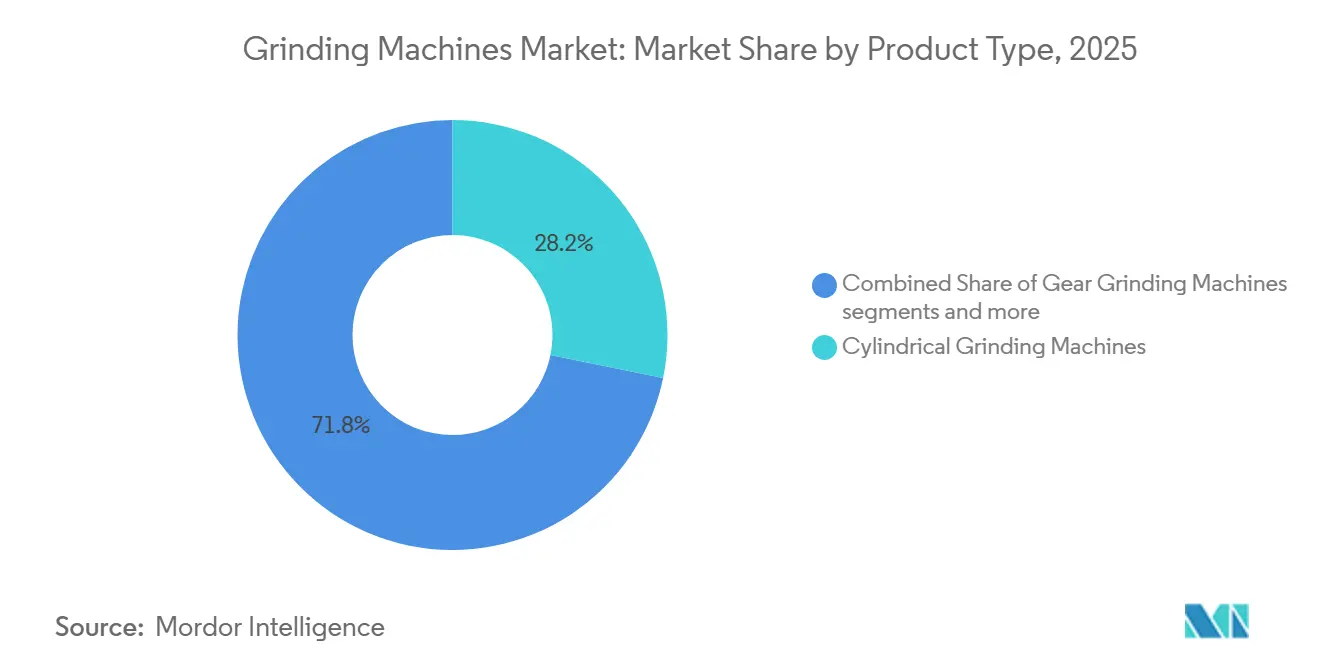

- By product type, cylindrical grinding machines led with 28.21% share of the grinding machines market size in 2025, while gear grinding machines are projected to grow at the fastest rate, registering a CAGR of 6.23% through 2031.

- By control type, CNC grinding machines held 68.14% in the grinding machines market share in 2025, and the segment recorded the highest projected growth at a 5.41% CAGR through 2031.

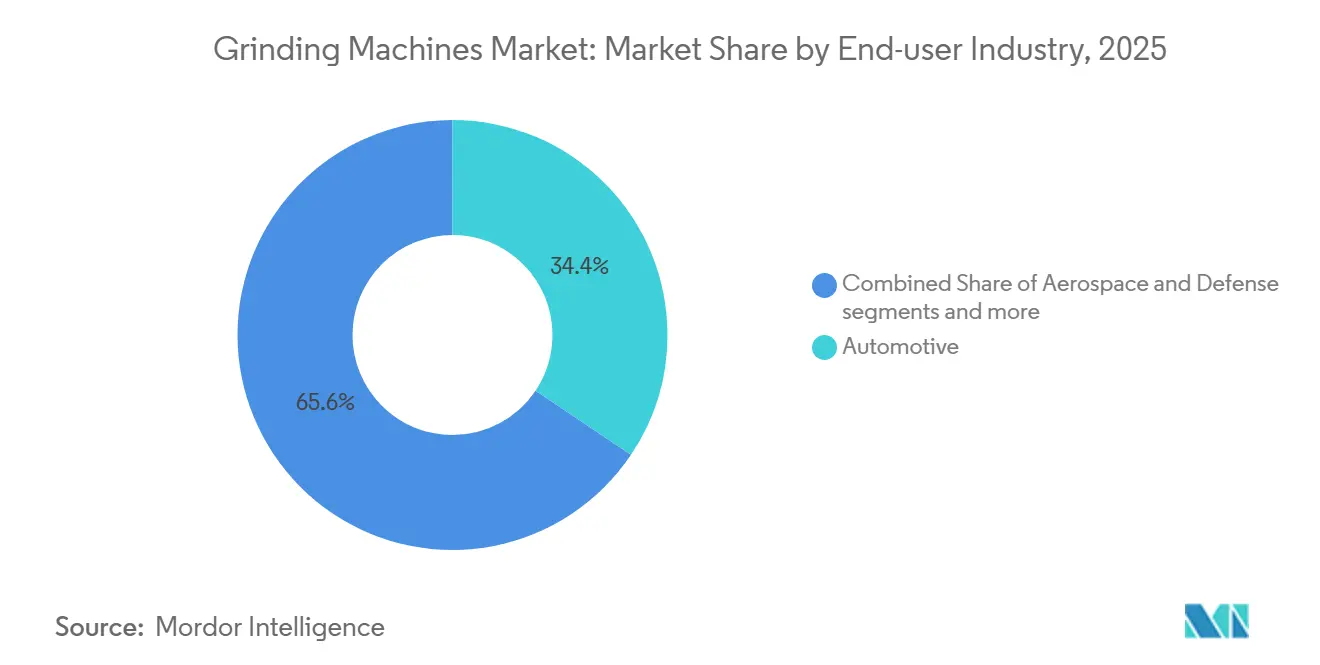

- By end-user industry, automotive accounted for 34.41% of demand in 2025, while aerospace and defense were the fastest growing with a 5.87% CAGR to 2031.

- By geography, Asia-Pacific held 45.87% share in 2025, while the Middle East and Africa are expected to advance at a 6.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Grinding Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-precision components demand | +1.2% | Global, with a focus on North America and EU aerospace clusters | Medium term (2-4 years) |

| Automotive engine and transmission expansion | +1.8% | APAC core markets with spill-over into ASEAN and Mexico | Short term (≤ 2 years) |

| Bearing manufacturing growth | +0.6% | Japan, Germany, and select U.S. industrial belts | Long term (≥ 4 years) |

| Adoption of hard-to-machine materials | +0.9% | Aerospace in the U.S., UK, France, and energy hubs in the UAE and KSA | Medium term (2-4 years) |

| Tool and die requirements | +0.5% | Germany, Italy, and regional tool-making hubs | Long term (≥ 4 years) |

| Aerospace turbine component ramp-up | +0.9% | North America and the EU, with early gains in Indian MRO facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for High-Precision Components Across Industries

Manufacturers are raising dimensional and geometric precision to meet global quality frameworks such as AS9100 for aerospace and IATF 16949 for automotive, which has strengthened the case for high-performance cylindrical grinding. Cylindrical platforms routinely deliver diameter tolerances near ±1 micrometer with roundness within low single-digit micrometers, which reduces secondary finishing and improves process capability at volume. In semiconductor equipment, precision grinding supports spindle accuracy and stable runout while sustainability programs seek to cut embedded emissions, as seen in TSMC’s deployment of coolant recycling that lowered CO₂ output while preserving sub-3-micrometer circular accuracy on critical spindles. U.S. manufacturing productivity gains reported for 2025 reflect sustained modernization of machine assets, which includes CNC grinding cells that lower scrap and stabilize cycle times.[1]U.S. Bureau of Labor Statistics, “Productivity and Costs by Industry, Manufacturing and Mining Industries, 2025,” U.S. Bureau of Labor Statistics, bls.gov Machine builders are embedding in-process gauging and adaptive control to maintain tolerance bands without frequent operator intervention, which aligns with factory efforts to reduce variability under tighter customer audits.

Automotive Engine and Transmission Manufacturing Expansion

Motor vehicle assemblies in the United States remained resilient into early 2026, which supported consistent demand for crankshafts, camshafts, and precision gears that require grinding to manage NVH thresholds in both ICE and electrified platforms. Germany recorded a 1% year-over-year rise in passenger-car output in February 2026, while battery-electric registrations advanced to 46,300 units, which reinforced the need for tighter tooth-flank topographies and high-speed gear finishes to meet drivetrain durability goals. VDA. EV architecture elevates rotational speeds and stack tolerances, which shift more gear-finishing work to generating and form grinding with CBN wheels and accurate dressing. Energy efficiency objectives and lifecycle cost discipline are encouraging the use of high-efficiency spindles and modern controls that monitor energy per part to meet site-level targets.[2] U.S. Department of Energy, “Federal Building Energy Efficiency Rules and Requirements,” U.S. Department of Energy, energy.gov CNC-based workflows that bring sensing and analytics to grinding processes are gaining traction with tier suppliers that are rebalancing line designs for flexible production runs.

Growth in the Bearing Manufacturing Industry

Bearing producers for wind turbines, industrial drives, and aerospace actuators depend on grinding to reach ultra-smooth finishes and strict roundness that extends service life under high load and speed. Technology transfer from semiconductor and precision platforms is visible in recent OEM portfolios, where ultra-precision edge control and thermal stability help preserve tolerances during long-cycle operations. Suppliers are strengthening machine bases, linear motors, and hydrostatic technologies to reduce heat generation and drift, which keeps parts in spec during extended production windows. Investment programs in Asia are expanding capacity for rolling elements and rings that feed both domestic buildouts and export flows to North America and Europe. Process capability reporting tied to customer quality clauses is pushing the adoption of in-process gauging and digital records that trace wheel specs, dressing intervals, and coolant condition at the lot level.

Rising Adoption of Hard-to-Machine Materials

Aerospace, medical, and energy components rely more on superalloys and engineered materials that are difficult to cut with conventional methods, which raises the role of grinding in final finishing to protect surface integrity. Multitasking machines that consolidate turning, milling, and grinding in one setup are gaining users who want to limit handling and maintain datum references across operations. Wheel technologies and controls are evolving together as OEMs integrate acoustic emission sensing, real-time load monitoring, and adaptive feeds to prevent burn and chatter on heat-resistant alloys. Quality systems across aerospace and medical value chains require traceable parameters and electronic records, which fit best with CNC grinders that log speed, infeed, dwell, and wheel condition into plant systems. Factory programs that target reduced energy per part are accelerating the move to efficient spindles and servo axes to support continuous work on hard substrates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High equipment and infrastructure investment | -0.9% | Global, most acute in Latin America and Southeast Asia | Short term (≤ 2 years) |

| Shortage of skilled grinding machine operators | -1.3% | North America, Western Europe, and Japan | Medium term (2-4 years) |

| High costs of wheels and consumables | -0.4% | Global | Short term (≤ 2 years) |

| Competition from advanced hard turning | -0.2% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Extremely High Equipment and Infrastructure Investment

The capital outlay for industrial CNC grinders typically ranges from USD 80,000 to USD 500,000 per unit, and configurations with automation, gauging, and five-axis capability can push higher. Ownership costs extend beyond the machine and can include CAD or CAM licenses, rigging and installation, precision foundations, three-phase power, and air systems, which can be a hurdle for smaller shops. Public-sector buyers apply life-cycle cost tests that favor efficient equipment with measurable savings over time, which has increased demand for documented energy performance and predictive maintenance. Financial conditions in emerging markets can slow modernization plans for small and mid-sized manufacturers who struggle to fund the full stack of machines, software, and auxiliary systems. Buyers who phase automation and metrology additions often see better risk control, yet they must carry slightly longer payback windows. The grinding machines market reflects these realities in delayed purchase decisions during lulls and faster commitments when backlogs and utilization rise.

Severe Shortage of Skilled Grinding Machine Operators

Open roles in North American manufacturing remained high entering 2026, and wage inflation strengthened for precision machining roles, which has elevated automation interest in grinding cells. Employers report multi-year training cycles to develop full-scope CNC grinder talent while competing for a limited pipeline of candidates. Software that automates CAM and simplifies setup can ease bottlenecks, but adoption varies by plant maturity and IT readiness. Digital fluency demands are rising due to energy and quality frameworks that require detailed process records and verified control of variables within each lot. As a result, many facilities are standardizing on CNC platforms with embedded logging and analytics to reduce operator burden and raise consistency, which supports a gradual shift toward lights-out or lightly supervised grinding.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cylindrical Machines Anchor Volume, Gear Grinders Capture Electrification Upside

Cylindrical machines held 28.21% of the grinding machines market share in 2025, which reflects their broad role in OD and ID finishing across shafts, bearing races, and precision pins. Platforms like STUDER S31 illustrate thermal stability and modular setups for a wide range of work lengths, and these capabilities support repeatable precision over long runs. Gear grinders are pacing the category as EV powertrains expand, since tighter topographies and quiet running require higher-quality tooth finishing that favors generating and form grinding. The grinding machines market benefits from the adoption of vitrified CBN wheels and smarter dressing routines that compress cycle time while holding form. Users also seek in-process gauging for pitch and profile checks to reduce manual handling and defect risk between stations. Lightweight machine bases and linear motor drives are being deployed to contain thermal drift during long cycles in busy cells. Shops aiming for smoother program changes are pushing for simplified user interfaces that cut non-cut time and support flexible shifts in product mix in the grinding machines market.

Gear grinding systems are expanding at a 6.23% CAGR to 2031 for the grinding machines market size, which reflects the continuous buildout of EV and hybrid drivetrains and demand for low-noise e-axles. Surface grinders remain workhorses for die faces, mold inserts, and plate work, where flatness and finish values support downstream assembly. Centerless grinders enable high-rate throughput for cylindrical parts in fuel, medical, and motion systems, though setup requires specific expertise. Tool and cutter grinders address cutting-tool production and regrind, and integrated metrology reduces rework while maintaining geometry. Specialty and belt solutions round out the portfolio by covering deburring and conformal finishing on complex shapes. Across product groups, the grinding machines industry is aligning with energy and data requirements that reward efficient spindles, better coolant management, and digital traceability for every batch.

By Control Type: CNC Automation Dominates Amid Labor Arbitrage and Precision Mandates

CNC platforms captured 68.14% of the grinding machines market share in 2025, and the segment is growing at 5.41% as users seek consistency and scalable quality in complex parts. The grinding machines market size for CNC is projected to expand at a 5.41% CAGR between 2026 and 2031, supported by sensing, analytics, and user-friendly cycles that shorten programming and setup. New cycles integrate external, internal, and end-face grinding into multitasking machines, which reduces handling and maintains datum control across steps. OEM portfolios increasingly bundle predictive features and dashboards to monitor spindle load, vibration, and energy usage in real time. These enhancements lower the skill barrier in plants that are replacing retirees while training less-experienced operators to manage precision-critical processes in the grinding machines market.

Manual grinders remain a fixture in maintenance and prototyping, and they can be cost-effective for small batches and irregular geometries when skilled operators are available. Entry prices are lower than CNC equivalents, yet wage inflation and tight labor markets erode the advantage in many shops. Plants pursuing energy tracking and traceability see a better fit with CNC because logs and records are easier to generate and audit. Digital twins and integrated metrology support higher first-pass yield without over-inspection, which strengthens ROI even at moderate volumes. As a result, the grinding machines industry continues to shift investment to CNC platforms with modular automation that can scale up or down as order books change.

By End-User Industry: Automotive Anchors Demand, Aerospace Accelerates on Turbine Backlogs

Automotive accounted for 34.41% of demand in 2025 as crankshaft, camshaft, bearing, and gear finishing stayed central to ICE and hybrid build schedules. U.S. motor-vehicle assemblies held to a steady range through 2025 and early 2026, which supported plant utilization for core driveline components.[3]Board of Governors of the Federal Reserve System, “Industrial Production and Capacity Utilization G.17, Motor Vehicle Assemblies Table,” Federal Reserve Board, federalreserve.gov Growth in battery-electric registrations in Germany underscores the need for better gear quality to control noise and extend life at higher motor speeds. Aerospace and defense is advancing at a 5.87% CAGR through 2031 for the grinding machines market size, driven by turbine engine output and MRO work that requires traceable finishes on superalloys. Employment gains in air transportation add confidence to near-term maintenance cycles and production ramps.

General machinery and metal fabrication maintain a stable base of work for hydraulic components, spindles, and gearboxes, which ties grinding demand to broader capital-goods cycles. Electrical and electronics producers need consistent shaft and rotor finishes for motors and generators, and semiconductor-equipment suppliers have highlighted sustainability projects that sustain precision without sacrificing emissions targets. Energy-related projects in oil, gas, and power rely on large cylindrical grinders for pumps and turbine shafts with higher load envelopes. Medical-device programs demand repeatable sub-micron accuracy for implant and instrument components with reliable electronic records under regulatory frameworks. Public-sector and infrastructure-linked orders create follow-on work in rail and heavy equipment as suppliers look to extend part life with improved surface prep and coatings after precision grinding.

Geography Analysis

Asia-Pacific accounted for a 45.87% share of the grinding machines market size in 2025, supported by strong automotive, electronics, and capital equipment ecosystems, and by announced capacity additions from leading machine-tool OEMs. Recent investment plans, such as JTEKT’s new plant in Gujarat, with production slated for FY2027, signal sustained localization of precision platforms to serve domestic and export programs. Regional buyers prioritize flexible CNC cells with embedded measurement and energy monitoring to mitigate operator gaps and reduce kilowatt-hours per part. The grinding machines market in Asia-Pacific also benefits from suppliers that integrate automation for lights-out cells in automotive and bearing hubs where throughput and consistency matter.

The Middle East and Africa are projected to post the fastest growth as industrial diversification programs fund energy, utilities, and process-sector projects that draw on heavy rotating equipment and precision components. Public program pipelines in the Gulf have expanded since 2024, which improves visibility for suppliers of grinders, metrology, and services that support turbines, pumps, and valves. Local-content policies are encouraging OEMs to establish service hubs and parts inventory, which reduces downtime on critical assets and strengthens aftermarket ties. Plants that adopt efficient spindles, better coolant management, and digitized maintenance will be well-positioned to meet energy and cost metrics as new capacity comes online.

North America maintains a large installed base and continues to adopt CNC automation to offset wage pressure and skill shortages. Manufacturing average hourly earnings rose through late 2025, which intensifies the case for process consolidation and robotic loading in grinding cells. Reshoring programs emphasize predictive maintenance, digital twins, and flexible automation, which support the shift to networked CNC grinders over manual machines. Europe’s course reflects regulatory drivers and automotive demand changes, with energy efficiency mandates pushing spindle and axis upgrades to reduce energy per unit in line with site targets. Together, these dynamics create a grinding machines market where precision, energy performance, and digital traceability are common selection filters across regions.

Competitive Landscape

The grinding machines market features established OEMs with broad portfolios, complemented by mid-sized specialists and regional players that address specific process or size envelopes. The formation of United Machining Solutions in July 2025 brought multiple brands together under one umbrella to offer surface, cylindrical, tool grinding, EDM, and high-speed milling with shared digital capabilities. DMG MORI expanded its integrated approach with a grinding technology cycle for multitasking machines, which reduces setups and simplifies execution for external, internal, and end-face grinding. These moves show how leading suppliers address precision, throughput, and labor constraints by packaging grinding alongside other processes with user-friendly software and sensing.

Competition centers on automation, energy performance, and software ease-of-use. JTEKT’s precision platforms emphasize hydrostatic and hybrid bearing technologies aimed at thermal stability and smooth motion, which help extend wheel life and improve finish. Danobatgroup’s cylindrical range targets space efficiency, higher workpiece weights, and integrated measurement to reduce operator touches and sustain lights-out operation. UNITED GRINDING has continued to layer in analytics dashboards and automation-ready features across surface, cylindrical, and tool grinding, which helps customers improve utilization and predict maintenance windows.

Aftermarket and lifecycle services are becoming more integral as plants seek uptime guarantees and smoother technology refreshes. Fives Machining Systems partnered with Prestige Equipment to offer trade-in, appraisal, and OEM-backed maintenance services, which give buyers more options to manage installed bases and fund upgrades. DMG MORI and the University of Tokyo created a research center focused on process integration and sustainability to reduce the global machine population by consolidating capabilities, which supports quality, energy, and footprint targets. As capability lines blur between milling, turning, and grinding, the grinding machines market is moving toward integrated systems with simpler workflows and better data capture.

Grinding Machines Industry Leaders

Amada Machine Tools

ANCA Pty Ltd

DANOBATGROUP

DMG MORI Co., Ltd.

Fives Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: DMG MORI introduced a “Grinding” technology cycle for NTX series multitasking machines that enables external, internal, and end-face grinding with AE-sensor contact detection and a zero-sludge coolant system with 5-micrometer cyclone filtration.

- March 2026: Danobatgroup showcased the CGX cylindrical grinder at BIEMH 2026, featuring a compact footprint and an MDM-100 measuring system with ±1.5-micrometer accuracy and 1-micrometer repeatability for fully automatic measurements.

- February 2026: Fives Machining Systems and Prestige Equipment partnered to expand lifecycle options that include surplus sales, trade-ins, certified appraisals, OEM-backed maintenance, retrofits, and machine health assessments.

- November 2025: UNITED GRINDING launched the STUDER S31 universal grinding machine with a traveling tailstock for center distances from 400 to 1,600 millimeters and introduced WALTER tool-grinding models with safety and high-speed features for advanced shops.

Global Grinding Machines Market Report Scope

The Grinding Machines Market Report is Segmented by Product Type (Surface, Cylindrical, Centerless, Gear, Tool & Cutter Machines, and Others), by Control Type (CNC, and Manual), by End-user Industry (Automotive, Aerospace, General Machinery, Electronics, Energy, Medical, and Others), and by Geography (North America, Europe, Asia-Pacific, and Middle East, South America). Market Forecasts are Provided in Value (USD Billion).

| Surface Grinding Machines |

| Cylindrical Grinding Machines |

| Centerless Grinding Machines |

| Gear Grinding Machines |

| Tool & Cutter Grinding Machines |

| Others (Belt Grinders, Special Purpose Grinding Machines, etc.) |

| CNC Grinding Machines |

| Conventional/Manual Grinding Machines |

| Automotive |

| Aerospace & Defense |

| General Machinery & Metal Fabrication |

| Electrical & Electronics |

| Energy (Oil & Gas, Power Generation) |

| Medical Devices |

| Others (Railway, Construction Equipment) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product Type | Surface Grinding Machines | |

| Cylindrical Grinding Machines | ||

| Centerless Grinding Machines | ||

| Gear Grinding Machines | ||

| Tool & Cutter Grinding Machines | ||

| Others (Belt Grinders, Special Purpose Grinding Machines, etc.) | ||

| By Control Type | CNC Grinding Machines | |

| Conventional/Manual Grinding Machines | ||

| By End-user Industry | Automotive | |

| Aerospace & Defense | ||

| General Machinery & Metal Fabrication | ||

| Electrical & Electronics | ||

| Energy (Oil & Gas, Power Generation) | ||

| Medical Devices | ||

| Others (Railway, Construction Equipment) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the grinding machines market growth outlook to 2031?

The grinding machines market size is expected to rise from USD 6.76 billion in 2026 to USD 8.59 billion by 2031 at a 4.89% CAGR.

Which product category leads demand in 2026?

Cylindrical platforms anchor volume and held 28.21% share in 2025, while gear grinders are the fastest growing due to EV drivetrain needs.

How dominant are CNC grinders compared to manual machines?

CNC machines held 68.14% share in 2025 and are growing at 5.41% as factories prioritize precision, automation, and data capture.

Which end-use sector is expanding the fastest?

Aerospace and defense is advancing at a 5.87% CAGR through 2031, driven by turbine engine production and MRO activity that require traceable finishes.

What region accounts for the largest portion of demand?

Asia-Pacific accounted for 45.87% of demand in 2025 based on installed capacity and ongoing investments by OEMs and suppliers.

What are the main constraints to faster adoption?

High upfront equipment and infrastructure costs and a sustained shortage of experienced operators, which increase the value of CNC automation and lifecycle services.

Page last updated on: