High Speed Steel Cutting Tools Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 16.21 Billion |

| Market Size (2031) | USD 20.73 Billion |

| Growth Rate (2026 - 2031) | 5.04% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Speed Steel Cutting Tools Market Analysis by Mordor Intelligence

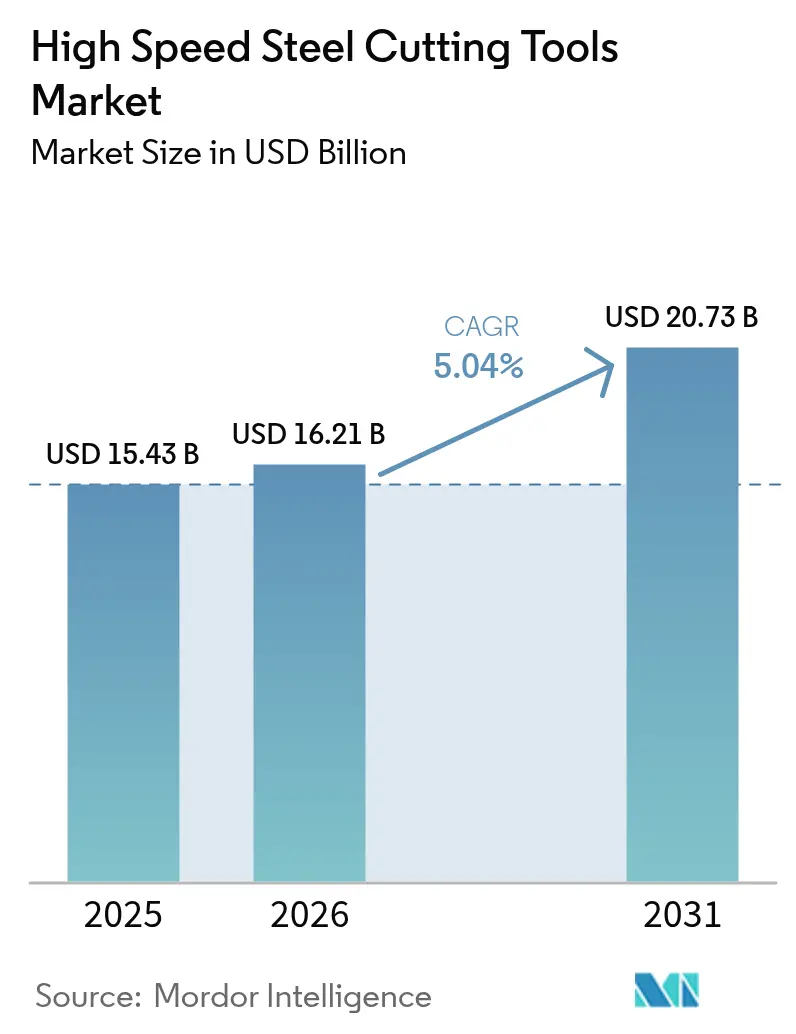

The High Speed Steel Cutting Tools Market size market is expected to grow from USD 15.43 billion in 2025 to USD 16.21 billion in 2026 and is forecast to reach USD 20.73 billion by 2031 at 5.04% CAGR over 2026-2031. A resurgence of mid-volume machining, rapid industrialization in Asia, and wider use of powder metallurgy are the primary growth engines. Manufacturers are adopting cobalt-enriched grades for aerospace alloys, expanding e-commerce channels for DIY buyers, and refining adaptive CNC strategies that stretch tool life. Supply-side pressures remain, including volatile molybdenum and cobalt prices and the automotive sector’s gradual pivot to carbide and PCD tools. Competitive moves center on targeted acquisitions, digital tool management, and carbon-neutral production commitments.

Key Report Takeaways

- By tool type, milling cutters led with 32.10% of High Speed Steel Cutting Tools market share in 2025, while taps are forecast to expand at a 6.67% CAGR through 2031.

- By material grade, conventional HSS held 47.45% revenue share in 2025; powder metallurgy HSS is projected to advance at an 8.14% CAGR to 2031.

- By production process, the forged segment commanded 84.72% share of the High Speed Steel Cutting Tools market size in 2025; powder metallurgy will grow at 9.34% CAGR between 2026 and 2031.

- By distribution channel, direct OEM sales held 60.54% of 2025 revenue, whereas the e-commerce/DIY retail channel shows an 11.12% CAGR outlook.

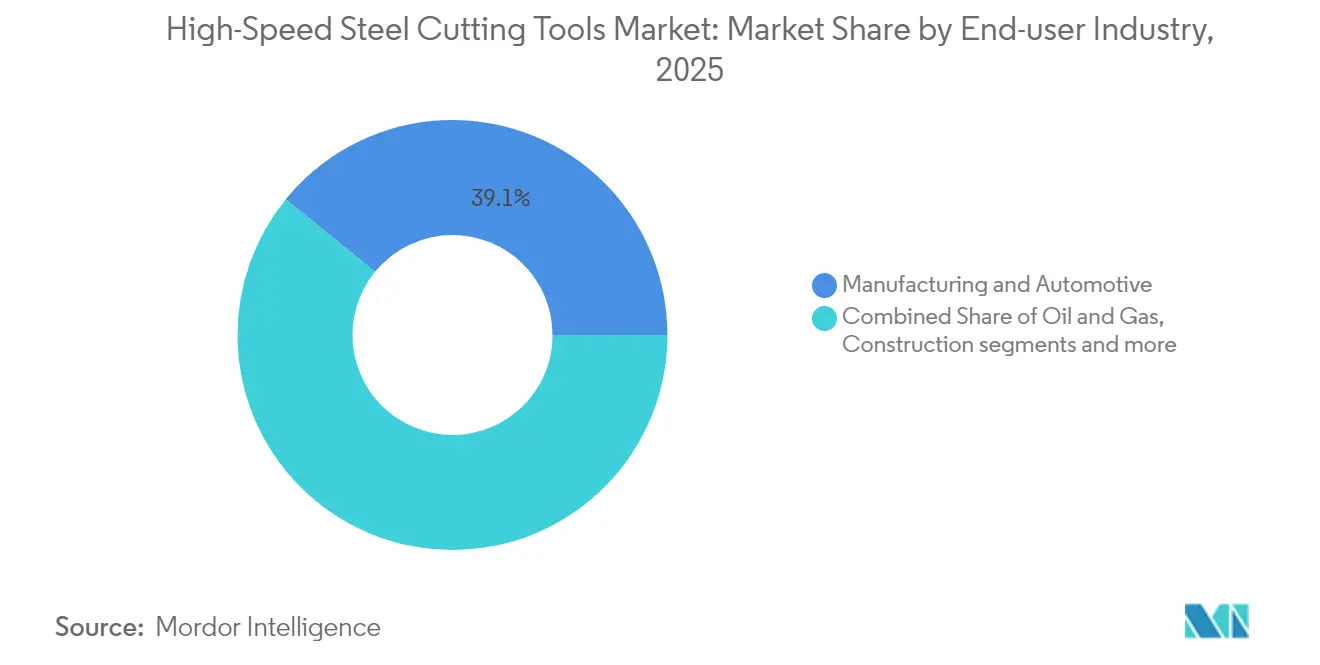

- By end-user industry, manufacturing & automotive contributed 39.12% revenue in 2025; energy generation is rising fastest at 6.93% CAGR to 2031.

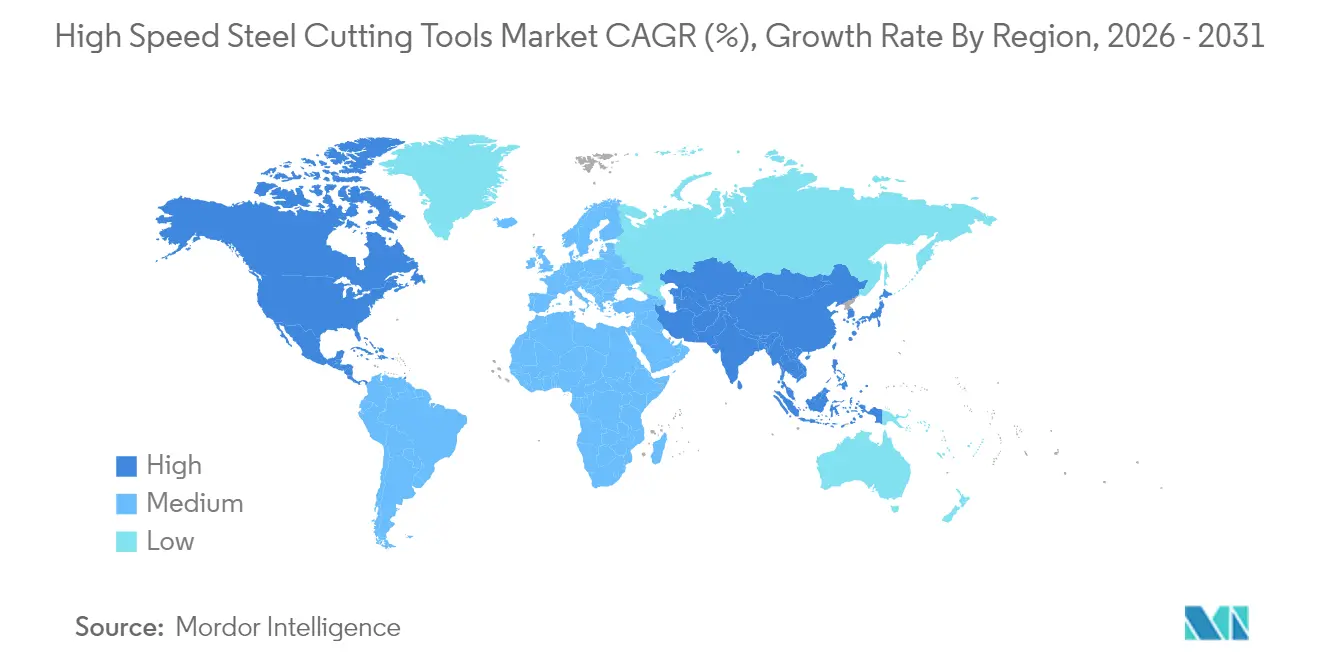

- By geography, Asia accounted for 45.68% of 2025 revenue and also records the highest regional CAGR at 6.14% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global High Speed Steel Cutting Tools Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for low-cost tooling in emerging Asian job shops | +1.2% | Asia | Short term (≤ 2 years) |

| DIY & home-improvement retail boom in North America | +1.0% | North America | Short term (≤ 2 years) |

| Re-shoring-led adoption of versatile HSS in North America & Europe | +0.8% | North America & Europe | Medium term (2-4 years) |

| CNC-based adaptive machining extending HSS tool life | +0.7% | Global (early uptake in Europe & North America) | Medium term (2-4 years) |

| Uptake of cobalt-enriched M42 HSS for aerospace alloys | +0.6% | Global (focus on North America & Europe) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demand for Low-cost Tooling in Emerging Asian Job Shops

Mounting numbers of tier-2 and tier-3 job shops across China, India, and ASEAN markets favor low initial tooling outlays. Conventional HSS tools meet that priority, especially as basic CNC adoption lets operators extend tool life by optimizing feeds and speeds. Chinese provincial support for indigenous machine-tool makers entrenches domestic sourcing, locking in repetitive demand cycles. The same trend spreads through India’s automotive component clusters and Vietnam’s electronics supply base, anchoring robust consumption for standard HSS milling cutters and drills.

DIY & Home-Improvement Retail Boom in North America

North American home-owners, hobbyists, and “prosumers” are driving double-digit online growth for consumer-grade HSS bits, taps, and hole saws. Tool makers now tailor geometries, coatings, and packaging to stand out on digital shelves, while power-tool brands bundle starter sets with cordless drills and compact lathes. Upskilled enthusiasts demanding industrial-style performance at modest price points have expanded the addressable segment, reinforcing the channel’s 11.4% CAGR outlook.

Re-shoring-led Adoption of Versatile HSS in North America & Europe

Policy incentives and risk mitigation strategies are drawing production back to the United States, Canada, and the European Union. Reshored plants frequently process broader part mixes in smaller lots, making versatile HSS tools a cost-effective choice for secondary cuts, fixturing runs, and prototyping. Hybrid manufacturing cells pairing additive, subtractive, and inspection modules often reserve coated carbide tools for finish passes while deploying HSS for roughing and setup work. Local supply arrangements shorten lead times and help align with “made-near-home” procurement programs.

Uptake of Cobalt-enriched M42 HSS for Aerospace Alloys

Aerospace primes continue to accelerate flight-ready builds of new-generation narrow-body and regional jets. When removing large volumes of nickel-based superalloys, machinists are choosing cobalt-rich M42 grades for hot hardness retention up to 650 °C.[1]International Energy Agency, “Global Critical Minerals Outlook 2024” iea.org Longer tool life offsets cobalt price swings and slashes insert changes on complex blisks and casings, supporting backlog reduction targets across engine programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift toward carbide & PCD tools in automotive | −1.1% | Global (pronounced in Europe & North America) | Medium term (2-4 years) |

| Volatility in molybdenum & cobalt prices | −0.9% | Global | Short term (≤ 2 years) |

| Limited European PM-HSS capacity & supply bottlenecks | −0.6% | Europe (with impact on global supply chains) | Medium term (2-4 years) |

| Carbon-neutrality-driven tool-life mandates | −0.5% | Europe (spillover to North America & Japan) | Long term (≥ 5 years) |

| Source: Mordor Intelligence | |||

Rapid Shift Toward Carbide & PCD Tools in Automotive

Electric vehicle platforms rely on thin-walled aluminum housings, composite brackets, and high-strength steel reinforcements. Carbide and PCD cutters deliver higher surface integrity and throughput on such materials, gradually displacing HSS in power-train, battery, and chassis lines. Automotive tooling decisions influence upstream tier suppliers and steel service centers, amplifying the drag on HSS demand, especially in Europe’s high-volume plants.

Volatility in Molybdenum & Cobalt Prices

High Speed Steel Cutting Tools market growth faces margin erosion when alloy inputs spike. Spot cobalt rates fluctuate with battery-sector pull and logistical risks in the Democratic Republic of Congo. Molybdenum supply tightness after 2023 mine curtailments compounds cost exposure.[2]United States Geological Survey, “Mineral Commodity Summaries 2024,” usgs.govToolmakers adjust purchase contracts, experiment with vanadium-rich chemistries, and roll out supply-surcharge clauses to buffer earnings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tool Type: Milling Cutters Remain the Workhorse while Taps Advance Fastest

Milling cutters generated 32.10% of global 2025 revenue and anchor the High Speed Steel Cutting Tools market by virtue of their flexibility in face, slot, and profile machining. The segment benefits from continual refinement of radial chip thinning and high-efficiency roughing methods that raise metal-removal rates without compromising finish. Taps, in contrast, secure the quickest 6.67% CAGR through 2031 as thread-forming formats cut cycle times and avoid chip evacuation challenges. Chip-free threading aligns with automotive electronics housings and thin-section die-cast parts, pushing adoption across Asia and Eastern Europe.

Cost-sensitive job shops still prize HSS drills, reamers, and broaches for hole-making and finishing, while saws and countersinks meet niche needs in maintenance and repair. Digital design platforms now simulate chip flow, rake angle, and coolant delivery to customize cutting edges for each substrate. By leveraging such software, toolmakers unlock new shelf life even within standard HSS chemistries, reinforcing milling cutters’ central role in the High Speed Steel Cutting Tools market.

By Material Grade: Conventional HSS Dominates as PM-HSS Accelerates

Conventional M-series grades held 47.45% revenue share in 2025 thanks to broad availability and competitive pricing for mid-toughness jobs. Powder metallurgy variants command only 14.62% of output today, yet they capture disproportionate growth at 8.14% CAGR. Uniform carbide dispersion, refined grain boundaries, and reduced segregation give PM-HSS an edge when machining aerospace fasteners or medical implants where minimal chipping is critical. Cobalt-rich M42 and M35 maintain a strategic niche for heat-resistant alloys, bridging the cost gulf between PM and standard types.

The High Speed Steel Cutting Tools market size attached to PM-HSS is poised to expand as Europe resolves capacity gaps and as Asian players upscale domestic atomizing lines. Additive manufacturing trials also explore HSS powder blends with tailored hardness gradients, broadening future design possibilities and supporting long-term material-grade diversification across the High Speed Steel Cutting Tools market.

By Production Process: Powder Metallurgy Challenges Conventional Forging

Traditional forging accounted for 84.72% of 2025 tool volumes and underpins dependable supply for mainstream users. Yet powder metallurgy’s 9.34% CAGR up to 2031 illustrates a decisive shift toward microstructural uniformity and near-net-shape economics. Less waste lowers energy per finished part, aligning with carbon-neutral roadmaps embraced by European automotive and aerospace OEMs. Toolmakers able to scale PM capacity can, therefore, command premium pricing and capture higher customer lock-in.

The High Speed Steel Cutting Tools market now features hybrid production flows where PM blanks receive laser sintering of edge treatments before final grind. Such combinations yield sharper cutting edges and tighter tolerance control. Regional clustering of PM capacity will influence sourcing decisions, with North American and East Asian sintering hubs filling current European shortfalls.

By Distribution Channel: E-commerce Redraws the Procurement Map

Direct OEM sales retained 60.54% of 2025 invoices as on-site application engineers remain essential for complex cutting challenges. However, the e-commerce channel’s 11.12% CAGR reshapes how workshops, maintenance depots, and homeowners discover, compare, and purchase tools. Detailed parametric search, instant inventory checks, and tutorial videos accelerate purchase decisions, shrinking the quote cycle. Industrial distributors respond with digital portals linked to local stock, adding subscription-based regrind pickups and tool-room audits. Together, these shifts widen visibility for challenger brands within the High Speed Steel Cutting Tools market.

By End-user Industry: Energy Generation Gains Pace

Manufacturing & automotive operations generated 39.12% of global turnover in 2025, reflecting the sector’s high volume of hole-making and milling. The energy segment posts the fastest 6.93% CAGR through 2031. Wind-turbine hubs, steam-turbine overhauls, and gas-pipeline spools require robust HSS cutters for refurb and secondary machining tasks. Oil & gas, mining, and construction hold steady via constant field maintenance cycles. Healthcare device makers lean on ultra-sharp reamers and burr-free drills for implant cavities, establishing an emerging premium niche inside the High Speed Steel Cutting Tools industry.

Geography Analysis

Asia leads the High Speed Steel Cutting Tools market with a 45.68% revenue share and a 6.14% CAGR forecast, thanks to China’s electronics and machine-tool build-outs, India’s automotive clusters, and Vietnamese assembly exports. Domestic tool makers now climb the value chain, adopting TiN and AlCrN coatings and pushing PM adoption, thereby reducing reliance on imports and cementing regional self-sufficiency.

North America ranks second and is revitalized by reshoring programs, defense offsets, and a thriving DIY culture. Hybrid machining cells in aerospace and energy plants require versatile cutters that thrive in adaptive CNC environments. E-commerce penetration also gives small workshops direct access to specialty taps and reamers, broadening High Speed Steel Cutting Tools market participation.

Europe sustains a technologically advanced yet capacity-constrained scenario. Limited PM-HSS supply elongates lead times for premium cutters. Nevertheless, German, French, and UK plants emphasize sustainable reconditioning and closed-loop recycling to hit carbon-reduction targets. Tool life monitoring and ISO 14001 programs elevate demand for data-rich HSS solutions despite carbide encroachment in automotive drivetrain lines.

South & Central America depend on Brazil’s industrial base, while the Middle East leans on energy equipment refurbishment and ongoing infrastructure builds. Africa’s demand cluster arises in South African mining supply and Egyptian component plants. Collectively, these emerging territories reflect the High Speed Steel Cutting Tools market’s potential for diversification and localized value-add.

Competitive Landscape

The competitive arena is moderately concentrated. Sandvik AB, Kennametal Inc., OSG Corporation, YG-1 Co. Ltd., and Dormer Pramet strengths include multi-grade product portfolios, global coatings capacity, and digital tooling ecosystems. Sandvik’s 2025 purchase of Suzhou Ahno expanded premium penetration in China, underlining a strategy of localized bet-building.

Mid-tier specialists such as Guhring, Erasteel, and Mitsubishi Materials invest in PM plant upgrades, cobalt-lean chemistries, and MSC-connected e-stores. Regional challengers in India and Vietnam exploit cost-plus models, often serving the DIY and job-shop tiers with uncoated or basic TiN options. Differentiation increasingly comes from data-enabled life-cycle services. Platforms that tie tool IDs to CNC dashboards advise on feeds, forces, and predictive re-sharpening, elevating switching barriers.

White-space opportunities cluster around medical devices, hydrogen-ready turbine parts, and small-batch prototyping centers. Firms offering turnkey tool-room audits, regrind logistics, and carbon-footprint dashboards win preference in public tenders and sustainability-driven bids, solidifying their positions in the High Speed Steel Cutting Tools market.

High Speed Steel Cutting Tools Industry Leaders

Sandvik AB

Kennametal Inc.

OSG Corporation

Sumitomo Electric Industries Ltd.

Nachi-Fujikoshi Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Guhring KG added Southeast Asian tap reconditioning sites to support regional sustainability goals.

- April 2025: Sandvik AB acquired a majority stake in Suzhou Ahno to deepen its premium tool presence in China.

- April 2025: Erasteel SAS secured certification for carbon-neutral HSS production.

- February 2025: Dormer Pramet unveiled HSS cutters tailored for wind-turbine machining.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the high-speed steel cutting tools market as new metal-removal tools forged from molybdenum or tungsten-based alloys that keep hardness near 600 deg C. It covers end mills, drills, taps, reamers, and broaches that reach users through OEM, industrial distribution, and e-commerce channels worldwide. We capture value at the first commercial sale, in constant 2024 US dollars, across six end-use industries and five regional clusters.

Scope Exclusions: The model omits resharpened or used tooling, non-HSS cutters (carbide, ceramic, PCD, CBN), and wood-only tools.

Segmentation Overview

- By Tool Type

- Milling Cutters

- Drills

- Taps

- Reamers & Broaches

- Others (Saws, Countersinks)

- By Material Grade

- Conventional HSS (M-Series)

- High-Cobalt HSS (T-Series/M42/M35)

- Powder-Metallurgy HSS (PM-HSS)

- By Production Process

- Conventional Forged

- Powder Metallurgy

- By Distribution Channel

- Direct OEM Sales

- Industrial Distributors

- E-commerce/DIY Retail

- By End-user Industry

- Manufacturing & Automotive

- Oil & Gas

- Mining & Quarrying

- Agriculture, Fishing & Forestry

- Construction

- Healthcare & Pharmaceutical

- Energy Generation (Turbines & Nuclear)

- Other End users (distributive trade, etc.)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- UAE

- Turkey

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with tool-room managers, spindle-OEM buyers, and national distributors across Asia-Pacific, Europe, and North America refined powder-metallurgy uptake, regional discounting, and e-commerce momentum. An online survey of fabricators helped us close data gaps before locking the assumptions.

Desk Research

We started with shipment codes from United Nations Comtrade, Eurostat Prodcom, and the China Association of Machine Tool Builders that signal yearly volume swings by tool type. Analysts pulled producer price trends from the US Bureau of Labor Statistics, patent counts through Questel, and technical papers on ScienceDirect to trace alloy evolution. Public filings, investor decks, and tender notices revealed average selling prices and channel splits, while D&B Hoovers isolated pure-play HSS suppliers operating in mixed portfolios. This list is illustrative; many other sources informed checks and clarifications.

Market-Sizing & Forecasting

According to Mordor Intelligence, the core estimate begins with a top-down reconstruction of global production and trade volumes, converted to value through blended average prices, and is cross-checked with supplier roll-ups for the ten largest manufacturers. Key drivers, including industrial production indices, machine-tool installations, alloy surcharge trends, light-vehicle output, and construction equipment builds, feed a multivariate regression that extends the view to 2030. Where interviews revealed atypical local pricing, we revised ASPs through scenario analysis rather than overstating volume.

Data Validation & Update Cycle

Two senior analysts compare outputs with independent signals such as coating-material imports and machine-tool capital spending; any variance beyond three percentage points triggers rework. Reports refresh annually, and material events prompt interim updates so clients receive the latest view.

Why Mordor's High-Speed Steel Cutting Tools Baseline Deserves Trust

Published values often diverge because firms apply different product mixes, price years, and refresh cadences. Our disciplined scope, yearly primary engagement, and dual-path modeling narrow these gaps.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 15.43 B (2025) | Mordor Intelligence | - |

| USD 8.70 B (2024) | Global Consultancy A | Excludes e-commerce channels; applies 2018 price deck |

| USD 11.30 B (2022) | Trade Journal B | Counts refurbished tools; omits Asia OEM direct sales |

| USD 8.92 B (2024) | Niche Analytics C | Mixes HSS blanks with finished tools; uses uniform growth factor |

The comparison shows that when refreshed prices, clear exclusions, and routine primary checks are combined, Mordor analysts deliver a balanced, transparent baseline that decision-makers can replicate without proprietary datasets.

Key Questions Answered in the Report

What is the current market size of the High Speed Steel Cutting Tools market?

The market size of the High Speed Steel Cutting Tools market is USD 16.21 billion in 2026.

Who are the key players in High Speed Steel Cutting Tools Market?

BIG Kaiser Precision Tooling, Erasteel, Kennametal, Inc., OSG Korea Corporation and Niagara Cutter, Inc. are the major companies operating in the High Speed Steel Cutting Tools Market.

Which is the fastest growing region in High Speed Steel Cutting Tools Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in High Speed Steel Cutting Tools Market?

In 2025, the Asia Pacific accounts for the largest market share in High Speed Steel Cutting Tools Market.

Page last updated on: