Drilling Machines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.82 Billion |

| Market Size (2031) | USD 11.44 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Drilling Machines Market Analysis by Mordor Intelligence

The Drilling Machines Market size was valued at USD 8.37 billion in 2025 and estimated to grow from USD 8.82 billion in 2026 to reach USD 11.44 billion by 2031, at a CAGR of 5.34% during the forecast period (2026-2031). Growth is tied to high-precision, multi-spindle requirements in electric-vehicle battery lines, recovering commercial aerospace output, and expanding wind-turbine component capacity. Continued automation, wider use of lightweight materials, and demand for deep-hole, large-radial formats keep capital expenditures on track even as commodity volatility persists. Rising investments by battery producers, gearbox suppliers, and shipyards sustain equipment backlogs despite short-term procurement hesitancy in oil and gas applications. Major suppliers are broadening retrofit services and digital suites to offset skilled-operator scarcity and differentiate in technically demanding bids.

Key Report Takeaways

• By product type, radial drilling machines led with a 32.45% revenue share in 2024, while deep-hole/BTA & gun drilling is expected to register the fastest 6.8% CAGR through 2030.

• By operation, manual systems accounted for 45.65% of the drilling machines market share in 2024, whereas CNC/automatic systems are forecast to expand at a 7.3% CAGR to 2030.

• By technology, mechanical/electric platforms captured 62.34% of the drilling machines market size in 2024; hydraulic systems are projected to rise at a 7.2% CAGR until 2030.

• By end-user, automotive commanded 25.67% of the 2024 revenue pool, yet aerospace & defense exhibits the fastest 8.1% CAGR over the projection period.

• By geography, Asia-Pacific held 46.76% of 2024 revenue with a 7.1% CAGR outlook to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Drilling Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in EV & Renewable-Energy Manufacturing Requiring High-Precision Multi-Spindle Drilling | +1.2% | Global, with APAC leading, North America & EU following | Medium term (2-4 years) |

| Accelerating Commercial Aerospace Production Boosting Demand for Large Radial Machines | +0.9% | North America & EU core, spill-over to APAC | Short term (≤ 2 years) |

| Global Expansion of Wind-Turbine Gearbox Capacity Spurring Deep-Hole Drill Investments | +0.8% | Global, with Europe & APAC leading offshore development | Long term (≥ 4 years) |

| Rise of On-Site Modular Construction Fueling Portable Magnetic Drill Adoption | +0.6% | North America & EU, emerging in APAC urban centers | Medium term (2-4 years) |

| Localization Mandates in Defense Shipbuilding Programs Worldwide | +0.5% | Global, with emphasis on APAC naval expansion | Long term (≥ 4 years) |

| Upstream Oilfield Revamps Increasing Demand for Heavy-Duty Tooling | +0.4% | Global, with MENA & North America leading | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in EV & Renewable-Energy Manufacturing Requiring High-Precision Multi-Spindle Drilling

Battery pack assembly now demands sub-micron hole tolerances, pushing cell suppliers to specify multi-spindle systems that can maintain rigidity at elevated throughput. Leading battery groups have integrated closed-loop torque tools and 3-D positioning to control clamp-force variation, lifting annual line capacity while safeguarding electrode alignment. Similar precision thresholds are migrating into solar-tracker mounts and nacelle hubs, where lightweight aluminum sections must be drilled without compromising fatigue performance. Equipment vendors have reacted by hard-mounting vibration sensors in spindle heads and pairing them with edge-computing modules that adjust feed rates in milliseconds. Demand is strongest in the Asia-Pacific corridor, but European gigafactories and North American utility-scale solar yards also seek identical capabilities[1]Fatih Birol, “Global EV Outlook 2024,” International Energy Agency, iea.org.

Accelerating Commercial Aerospace Production Boosting Demand for Large Radial Machines

Airframe primes are ramping single-aisle programs back to 60 aircraft per month, renewing tenders for long-reach radial drills that cut titanium frame members in one-setup passes. Five-axis automation and pallet pools allow fuselage sections to move through fewer stations while sustaining 25 µm positional repeatability. Digital twins now feed real-time torque and thrust data to manufacturing execution systems, flagging tool-wear anomalies before rivet misalignment can occur. The approach is critical for sustainability credentials, as material scrap reductions directly lower Scope 3 emissions. North American tier-ones remain the pacesetters, yet EU aerostructure suppliers are mirroring capacity additions to meet backlog recovery targets.

Global Expansion of Wind-Turbine Gearbox Capacity Spurring Deep-Hole Drill Investments

Offshore turbine ratings crossing the 15 MW threshold require gargantuan gearboxes machined to micrometer pitch errors across shafts exceeding 2 m in length. Deep-hole and BTA drills with counter-rotating workpiece fixtures keep thermal deviation under control and shorten single-hole cycles by up to 30%[2]Francesco La Camera, “Renewable Power Generation Costs 2024,” International Renewable Energy Agency, irena.org. Gearbox makers are retrofitting legacy cells with oil-mist evacuation systems that cut tool temperature spikes, extending cutter life in high-alloy forgings. European offshore yards concentrate such investments, though Chinese coastal clusters and emerging Indian suppliers are rapidly following suit. Long-term maintenance contracts further stimulate demand for identical machines at field-repair depots, securing service revenue for OEMs.

Rise of On-Site Modular Construction Fueling Portable Magnetic Drill Adoption

Prefabricated steel frame factories pre-drill beam webs before shipment, but variances appear once modules are craned into place. Contractors, therefore, specify portable magnetic drills equipped with self-centering bushings to finish alignment bores on elevated platforms. New battery packs yield 8-hour autonomy, freeing operators from power cords and reducing fall hazards. Equipment firms have bundled cloud dashboards into these drills, allowing project managers to check hole counts and spindle loads from tablets. Uptake is brisk in mid-rise residential blocks in Western Europe and in U.S. data-center projects where schedule compression is paramount.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commodity-Investment Cyclicality Dampening Capital Equipment Orders | -0.8% | Global, with particular impact on resource-dependent economies | Short term (≤ 2 years) |

| Global CNC-Operator and Machinist Skill Shortage | -0.6% | Global, with acute shortages in North America & EU | Medium term (2-4 years) |

| Substitution by Additive Manufacturing for Complex Geometries | -0.4% | Global, with early adoption in aerospace & medical sectors | Long term (≥ 4 years) |

| High Up-Front Cost of 5-Axis Drilling Centers for Small & Medium Enterprises | -0.3% | Global, with particular impact on emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Commodity-Investment Cyclicality Dampening Capital Equipment Orders

Oil-field service firms expand machine-tool fleets when crude averages above breakeven, yet they swiftly defer procurement under price dips. Drilling contractors, therefore, swing between over-capacity and deferred maintenance, creating unpredictable quoting cycles for machine builders. Mid-stream fabrication yards mirror this rhythm, delaying purchase commitments until final investment decisions close. Currency swings add further uncertainty for Latin American miners sourcing dollar-denominated equipment[3]Cindy B. Taylor, “Form 10-K 2024,” U.S. Securities and Exchange Commission (Oil States International filing), sec.gov. The result is elongated sales funnels requiring vendors to carry higher working capital in spares and demo fleets to capture short-window orders.

Global CNC-Operator and Machinist Skill Shortage

Retirement rates exceed apprenticeship intake across most OECD economies, leaving machine halls understaffed for multi-axis programs. Manufacturers compensate by layering conversational interfaces on controls and embedding vision-based part probing to reduce manual offsets. Equipment builders co-fund community-college labs and sponsor international skills competitions, but cohort sizes remain insufficient. The deficit inflates wage pressure and pushes smaller shops toward outsourcing high-precision steps. In parallel, AI-powered code-generators are gaining traction, yet their deployment progress is constrained by cyber-security audits and insurance compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Deep-Hole Drilling Drives Specialized Growth

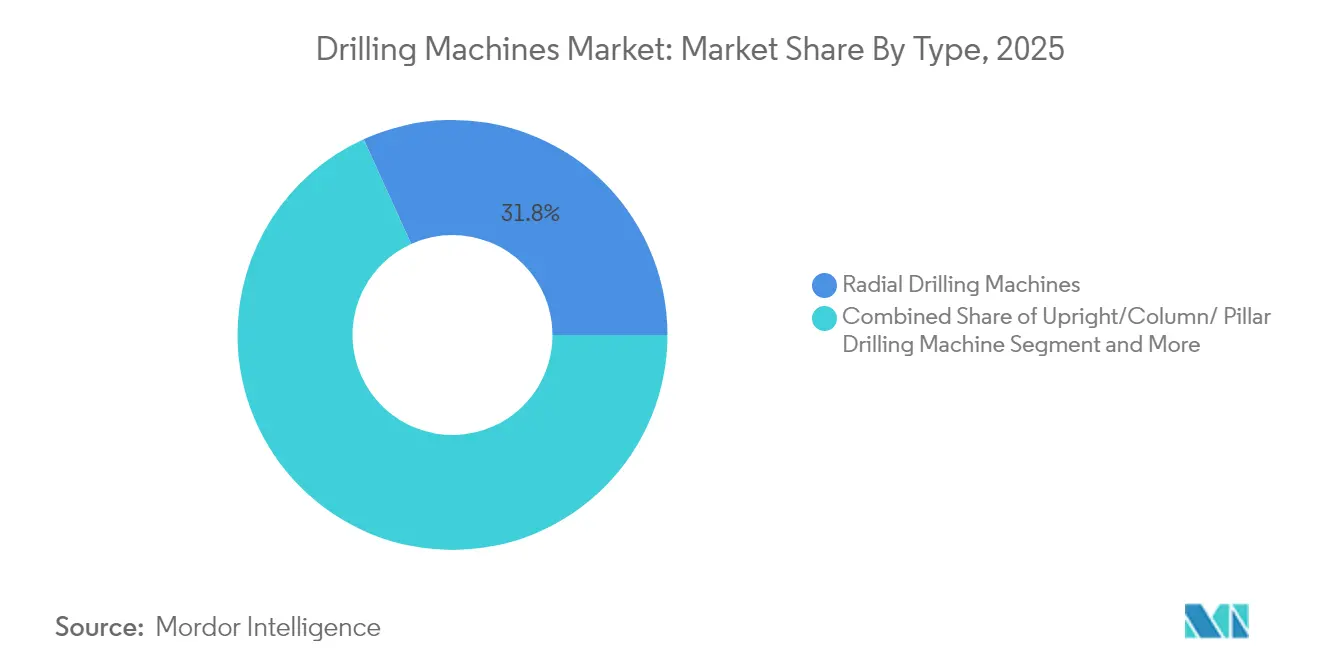

Radial machines generated the largest revenue in 2024 on the strength of their versatility across automotive chassis, general machinery, and medium-sized casting work. At a 31.78% share, they anchor production cells that pair vertical mills and turning centers to complete prismatic components in balanced takt flows. Demand remains buoyant as vehicle OEMs still deliver volume models whose steel and iron knuckles fall within radial capacity envelopes. Yet the deep-hole/BTA subset is rising fastest, logging a 6.54% CAGR amid broader adoption in large-bore energy parts, pressure-vessel tube sheets, and aerospace wing spars. Buyers cite lower per-hole cycle times, improved coolant delivery, and automated chip evacuation as reasons for switching.

The niche commands incremental premium margins, given its complex push-pull tooling and tight concentricity specifications. Multinational defense yards and offshore gearbox consortiums opt for gantry configurations able to reclaim heat distortion in-process. Portable magnetic and micro-drill clusters round out the category, feeding electronics and field-service channels with compact units amenable to fast redeployment. These variants, though a smaller slice of the drilling machines market, pioneer sensor fusion and battery modules that later migrate to heavier classes, creating a virtuous technology loop.

By Operation: Automation Accelerates Despite Manual Dominance

Manual rigs still occupy 45.02% of the installed base thanks to low entry costs and simple maintenance. Job-shops handle mixed-lot repair work where fixture turnover outweighs cycle efficiency, preserving the appeal of hand-feed quills and mechanical depth stops. Nevertheless, CNC/automatic systems chart the steepest 7.06% CAGR as large build-to-print houses modernize to meet traceability mandates and mitigate labor gaps. Machine builders bundle code simulation, tool-life dashboards, and shop-floor MES links as standard rather than chargeable add-ons.

Semi-automatic formats form an intermediate tier, marrying hydraulic feeds to operator supervision. They thrive in custom heavy-equipment lines where geometry changes every batch, yet cut depths stay high. Digital retrofits further blur lines; IoT spindle probes mounted on vintage columns broadcast vibration and thrust data to cloud analytics, squeezing extra utilization from sunk assets. Such retrofits enlarge the drilling machines market by inserting subscription software revenue atop hardware already depreciated.

By Technology: Hydraulic Systems Gain Momentum

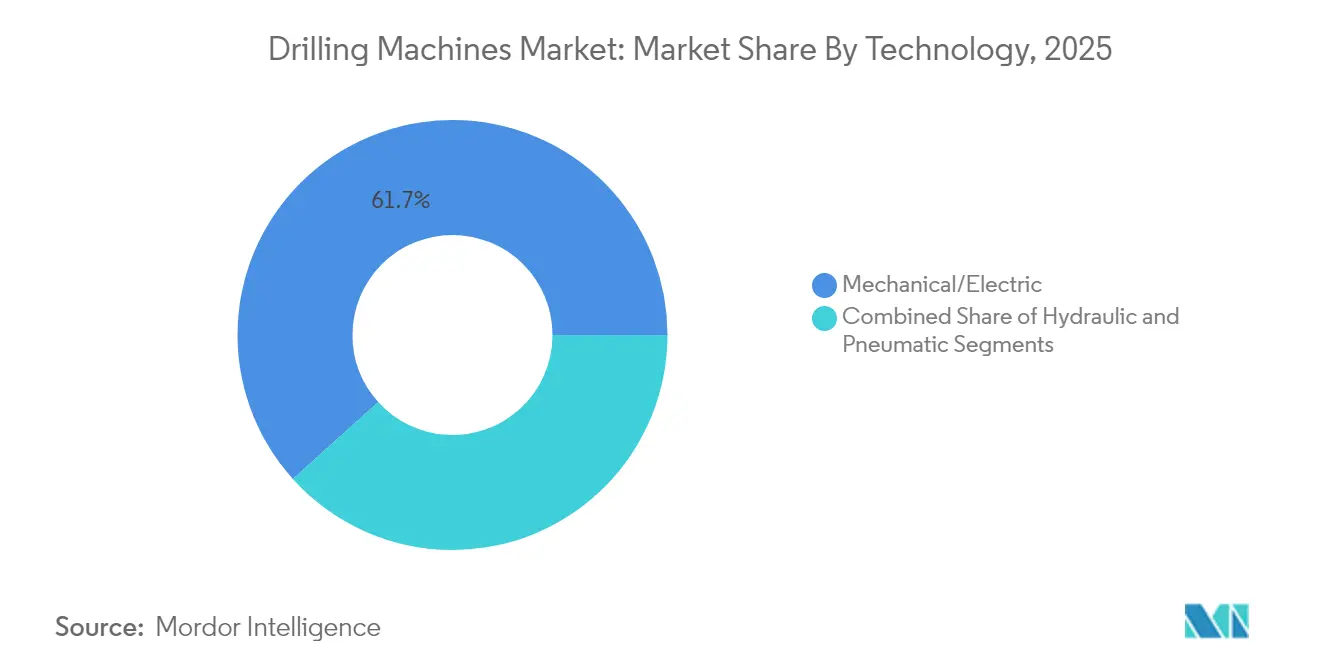

In the drilling machine market, mechanical/electric technology captured 61.68% revenue in 2025, a testament to widespread 3-phase infrastructure and decades of field familiarity. Their belt-driven spindles cope well with mild-steel throughput and reduce total cost of ownership for light manufacturing. Even so, hydraulic systems out-pace on percentage terms, advancing 6.96% annually. Operators appreciate high torque at low rpm for nickel-alloy forgings, plus stepless feed control that eases chatter on deep bores. They are standard in oil-field tool-joint machining where API thread tolerances are unforgiving.

Hybrid concepts now incorporate hydraulic clamping with electric spindle drives, balancing energy efficiency with force density. Pneumatic units, while a minor share, remain indispensable in volatile-gas environments such as LNG skid packages. Looking forward, regenerative servo-hydraulics tied to variable-frequency drives stand to trim energy draw by double digits, aligning with plant decarbonization pledges and buoying the drilling machines market against legislative pressures.

By End-User Industry: Aerospace Outpaces Automotive Growth

Automotive groups made up 25.12% of 2025 revenue in the drilling machine market, leveraging gang drilling stations to churn engine-block water jackets and suspension brackets. Electrification, however, re-shapes demand toward battery-tray and e-axle housings that prefer lightweight material drill parameters. Meanwhile, aerospace & defense bookings accelerate at an 7.74% CAGR as narrow-body production ramps and navy programs stipulate in-country machining for hull penetrations and missile launch tubes. That surge draws incremental requests for angle-head, deep-hole rigs anchored by robust rotaries to resist titanium cutting forces.

Fabrication & industrial machinery integrators sustain steady orders for universal columns, benefiting from infrastructure stimulus spanning bridge refurbishments and rail networks. Energy, oil & gas buyers revive capex to exploit high-natural-gas price windows, targeting automated hydraulic lines for mud-motor housings and sub-salt casing strings. Electronics manufacturers, in contrast, gravitate to micro-drill solutions, achieving 40 µm positional accuracy for multilayer substrates, a micro-niche yet intellectually rich vector that diversifies the drilling machines market.

By Work-Piece Material: Composites Drive Innovation

Metals keep the lion’s share, 33.94% in 2025, since steel, aluminum, and super-alloys still dominate structural components and pressure vessels. Nonetheless, composites, polymers & plastics achieve the best 7.91% growth clip on the back of aerospace skin panels and EV body-in-white inserts. Their stacked-ply nature complicates chip evacuation and tool entry, fostering ultrasonic-assisted drills and dusk-capture vacuum collars. Process windows shrink compared with metals, pushing OEMs to deploy in-spindle force sensors that prevent delamination by modulating peck cycles.

Wood applications remain an evergreen, serving furniture and mass-timber building domains. Meanwhile, ceramics, glass, and concrete categories command specialized diamond-tipped equipment. Recent acquisitions by ultra-precision machine firms reveal a strategic tilt toward nano-level spindle control in glass wafer drilling, further extending the technology envelope and cementing the drilling machines market as a platform for cross-material convergence.

Geography Analysis

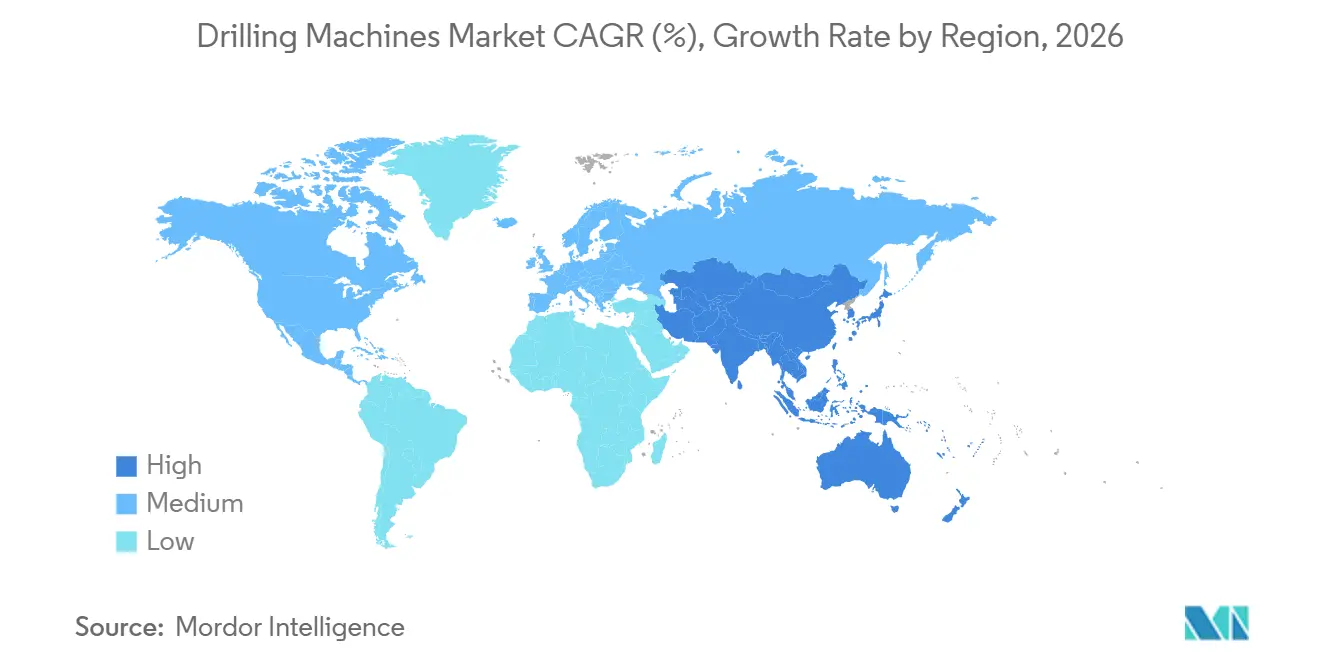

Asia-Pacific captured 46.20% of 2025 revenue in the drilling machine market and is projected to maintain a robust 6.98% CAGR through 2031. China’s machine-tool park continues to swell, propelled by state incentives for domestic CNC controllers that challenge entrenched foreign incumbents. Japanese builders localize component machining across ASEAN to blunt currency risks, while Indian fabrication clusters modernize under Production-Linked Incentive schemes. Rising cell factories, offshore wind yards, and metro-car foundries keep spindle utilization high, lifting service and retrofit opportunities.

North America’s installed base remains technologically advanced yet underutilized in commodity down-cycles. Reshoring incentives and clean-energy tax credits now underwrite new composite-capable cells for aerospace stringers and battery-module carriers, brightening order books for high-end builders. Canada’s petrochemical plants and U.S. Gulf Coast yards upgrade to hydraulic deep-hole rigs to support LNG expansion, stabilizing the drilling machines market size for heavy-duty formats against cyclic rig counts.

Europe, though mature, pivots toward zero-emission mandates, accelerating the retirement of legacy 3-axis drills in favor of servo-electric gantries with in-line power analyzers. German integrators test predictive greasing algorithms that cut unplanned downtime by 12% on wind-tower flange lines. Southern European shipyards, galvanized by naval-fleet renewal, tender for large-diameter column machines with 6-m stroke capacity to produce bulkhead penetrations in a single pass.

The Middle East and Africa anticipate a 31% uplift in drilling rig demand, translating into yard upgrades in UAE jack-up refurbishments and Saudi fabrication villages aligned with Vision 2030 steel programs. Sub-Saharan rail infrastructure modernizations call for mobile magnetic drills able to process track joints under field conditions. South American prospects center on Brazilian pre-salt developments and Argentine shale growth, which both require tubular dressing shops equipped with high-torque hydraulic drill presses.

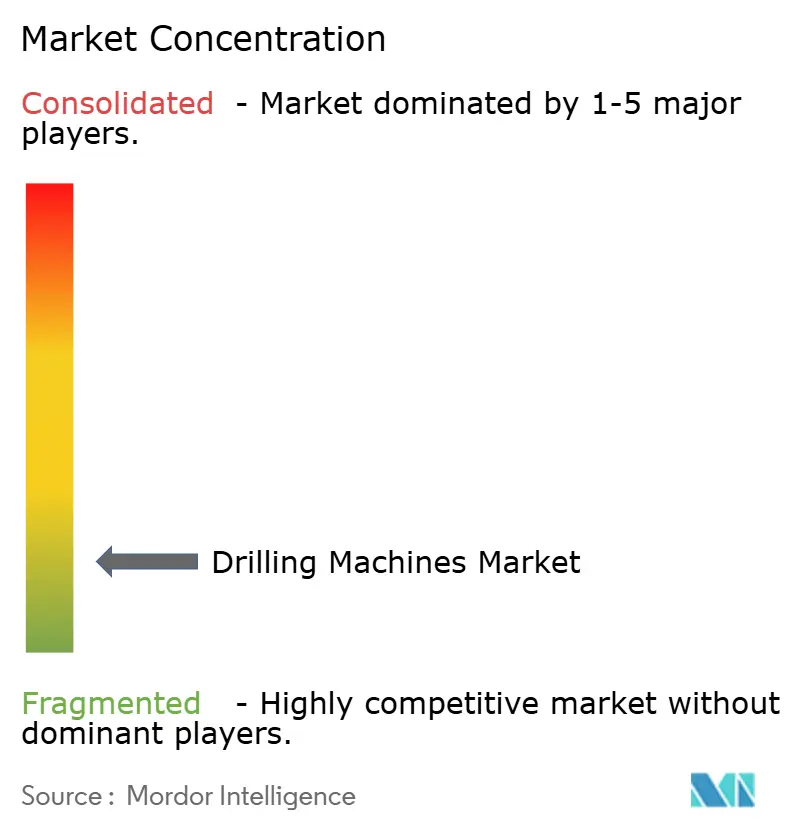

Competitive Landscape

The sector is moderately fragmented. Global groups such as DMG MORI, Mazak, and Okuma operate multi-continent plants, leveraging brand equity and end-to-end service contracts to defend share. DMG MORI alone fields 17 production facilities and 116 direct sales points, enabling 72-hour spare-parts delivery in key markets. Mid-tier challengers pursue mergers to scale; the 2025 acquisition of Kern Microtechnik by AMETEK adds nano-precision platforms to an already broad metrology and motion-control stack.

Digital differentiation tops strategic agendas. Hurco’s conversational AI code generator reduces first-article programming times by half, directly addressing the operator bottleneck. United Grinding’s pending purchase of GF Machining Solutions extends its micro-drilling competencies into die-sinking EDM, forming a cradle-to-finish play across metallic and composite workpieces. Competitive tension also surfaces in retrofit ecosystems: firms bundle spindle-mount IoT kits on subscription, turning dormant legacy fleets into connected revenue channels.

Regional policies amplify the contest. Defense offset clauses in India and Saudi Arabia compel primes to source sub-systems domestically, opening windows for indigenous drill builders to supply naval hull penetrations. Conversely, East-Asian export rebates encourage overseas builders to relocate assembly lines into ASEAN, accelerating price pressure in volume-driven segments. Meanwhile, component shortages in high-precision ball screws spur vertical integration moves several OEMs now in-house grind critical linear-motion parts to derisk supply.

Drilling Machines Industry Leaders

DMG MORI

Dalian Machine Tool Corporation

Shenyang Machine Tool Corp Ltd (SMTCL)

ERNST LENZ Maschinenbau GmbH

Fehlmann AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: InCompass purchased Bridgeport Machine Tool Company, bolstering vertical milling and drilling coverage.

- February 2025: AFM Cluster members announced 20 million EUR expansions in 5-axis machining lines to meet surging aerospace component orders.

- February 2025: AMETEK acquired Kern Microtechnik for annual sales of EUR 50 million to enhance ultra-precision machining capabilities.

- February 2025: Cascadia Capital’s Advanced Manufacturing Report highlighted elevated M&A activity and steady industrial-production indices supporting equipment demand.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the drilling machines market as all newly manufactured, factory-based equipment that removes material by rotating a drill bit, including radial, upright, gang, deep-hole, and multi-spindle models sold to industrial end users worldwide. Mordor Intelligence tracks transaction values at ex-works prices for these machines.

Scope Exclusions: Handheld power drills, construction site rigs, down-hole petroleum equipment, and consumable cutting tools are excluded.

Segmentation Overview

- By Type

- Radial Drilling Machines

- Upright/Column/ Pillar Drilling Machines

- Sensitive/Bench Drilling Machines

- Gang Drilling Machines

- Deep-Hole/BTA & Gun Drilling Machines

- Portable Drilling Machines

- Turret Drilling Machines

- Others (Magnetic, Micro/Mini Drilling, Special-Purpose Drilling Machines)

- By Operation

- Manual

- Semi-Automatic

- CNC/Automatic

- By Technology / Power Source

- Mechanical/Electric

- Hydraulic

- Pneumatic

- By End-user Industry

- Automotive

- Aerospace & Defense

- Fabrication & Industrial Machinery

- Construction

- Oil & Gas and Energy

- Electronics & Electricals

- Shipbuilding & Marine

- Other End-users (Heavy Equipment, Medical Devices, etc.)

- By Work-piece Material

- Metals

- Composites, Polymers & Plastics

- Wood

- Others (Ceramics, Glass, Concrete, etc.)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Peru

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Qatar

- Kuwait

- Turkey

- Egypt

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Targeted interviews with plant engineers, procurement heads, and regional distributors across Asia-Pacific, North America, and Europe validate utilization rates, warranty norms, and emerging composite-material drilling demand, while short surveys quantify inventory turns.

Desk Research

Our analysts begin with tier-one, non-paywalled datasets, including UN Comtrade HS 8459 flows, CECIMO shipment surveys, National Bureau of Statistics of China machinery output, and the US Census M33L series, so we can anchor production, trade, and average selling prices. Company 10-Ks, investor decks, and trade-show catalogs then reveal model launches and regional discounting.

Paid sources such as D&B Hoovers for OEM splits and IMTMA cost benchmarks help us reconcile producer revenues with public totals before layering macro demand signs like global light-vehicle builds and commercial aircraft deliveries. The sources cited are illustrative; many additional publications and regulatory disclosures supported data checks.

Market-Sizing & Forecasting

We start with a top-down reconstruction of 2024 production and net-export volumes, which are then split by machine type and end use through sampled ASP × volume checks from dealer quotes and selected OEM financials. Variables such as automotive power-train hole counts, commercial jet build schedules, wind-turbine gearbox orders, spindle-speed adoption, and capital-goods sentiment feed an ARIMA forecast running to 2030. Bottom-up supplier roll-ups act as a guardrail; gaps above five percent trigger model revision.

Data Validation & Update Cycle

Outputs undergo dual-analyst variance review against customs anomalies, quarterly earnings, and trade-show order books. Material deviations prompt fresh expert calls. Reports refresh each year, with interim updates for major events, so clients receive the latest view.

Why Mordor's Drilling Machines Baseline Stands Firm

Published estimates differ because firms mix dissimilar machine classes, price bases, and refresh timing. By keeping scope tight and updating with live production and ASP evidence, we offer a dependable baseline.

Key gaps arise when others pool handheld drills or oil-field rigs with factory machines, apply list rather than transacted prices, or convert currencies at spot rates; some also extend past CAGRs mechanically, whereas Mordor Intelligence rebuilds the model each cycle.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.37 B (2025) | Mordor Intelligence | - |

| USD 28.60 B (2024) | Global Consultancy A | Includes handheld and construction rigs; uses list prices |

| USD 30.00 B (2025) | Industry Journal B | Bundles drilling tools; spot FX; biennial refresh |

These contrasts show that once scope, price basis, and update rhythm are aligned, Mordor's disciplined approach delivers a clear, repeatable baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the drilling machines market?

The Drilling Machines Market stood at USD 8.82 billion in 2026 and is projected to reach USD 11.44 billion by 2031.

Which region leads the drilling machines market?

Asia-Pacific holds the largest 46.20% share and is set to expand at a 6.98% CAGR through 2031.

Which product segment is growing fastest?

Deep-hole/BTA & gun drilling machines are forecast to post the quickest 6.54% CAGR as energy and aerospace users seek specialized bores.

What role do composites play in future demand?

Drilling solutions for carbon-fiber and polymer stacks are advancing, with the composites segment expected to grow 7.91% annually through 2031.

Page last updated on: