Vegetable Oils In Beauty And Personal Care Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

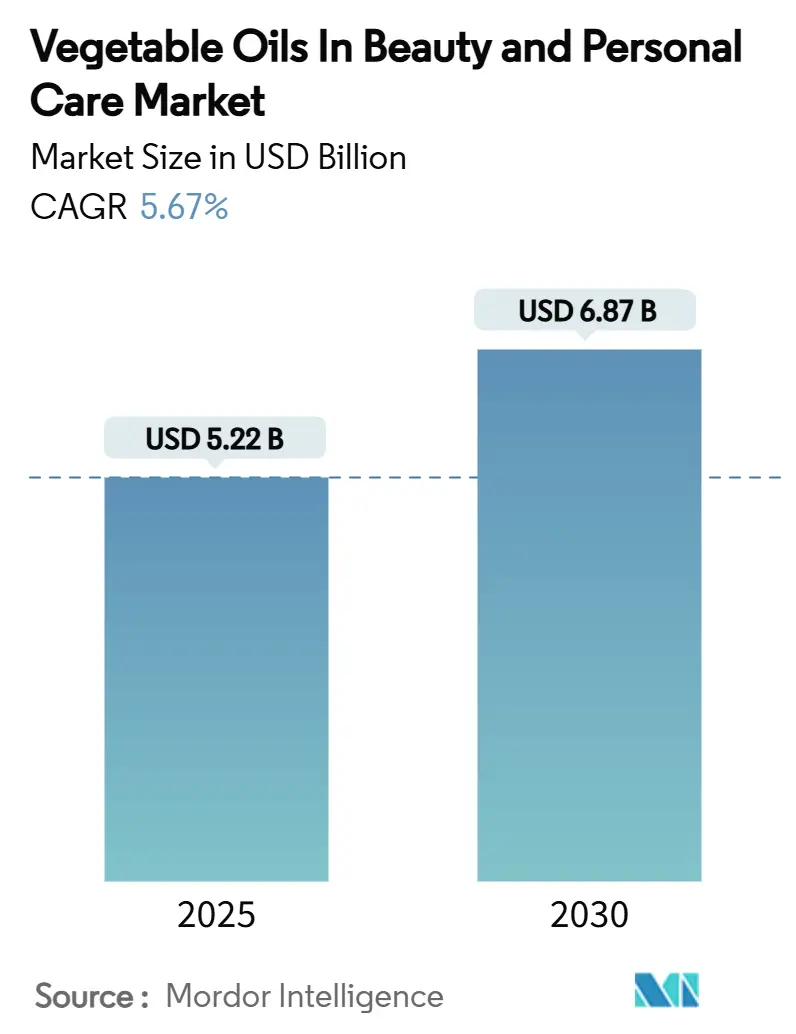

| Market Size (2025) | USD 5.22 Billion |

| Market Size (2030) | USD 6.87 Billion |

| Growth Rate (2025 - 2030) | 5.67% CAGR |

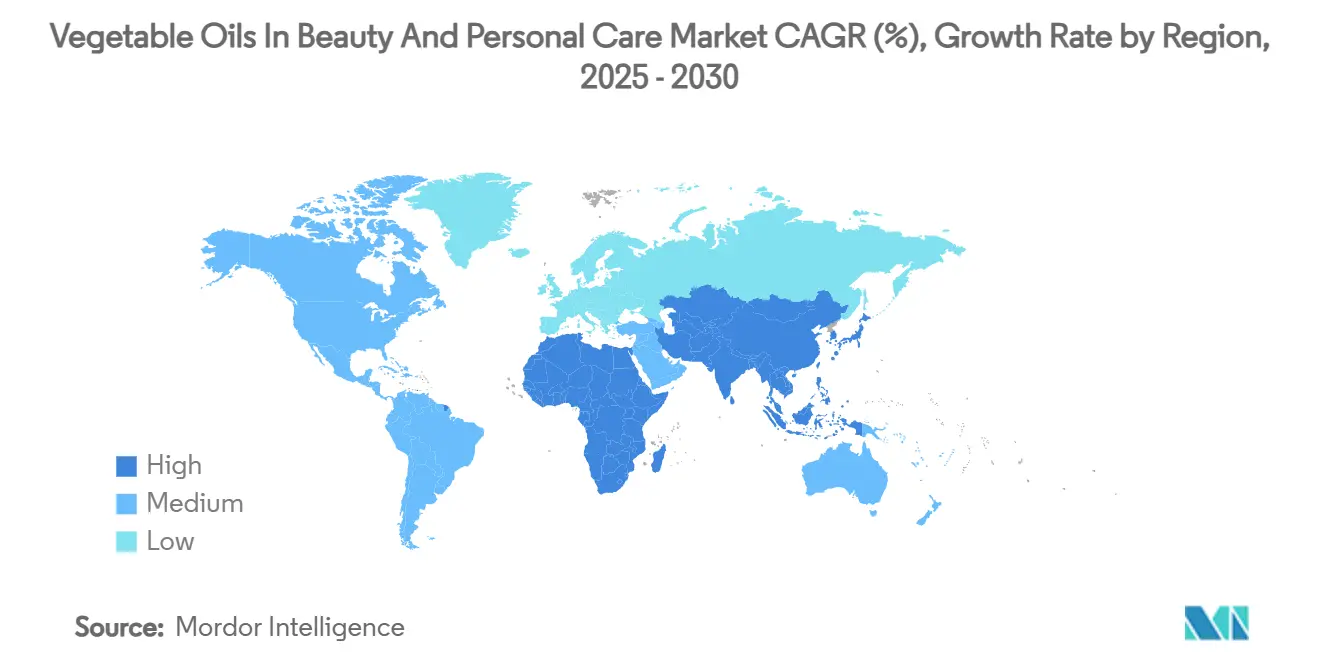

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

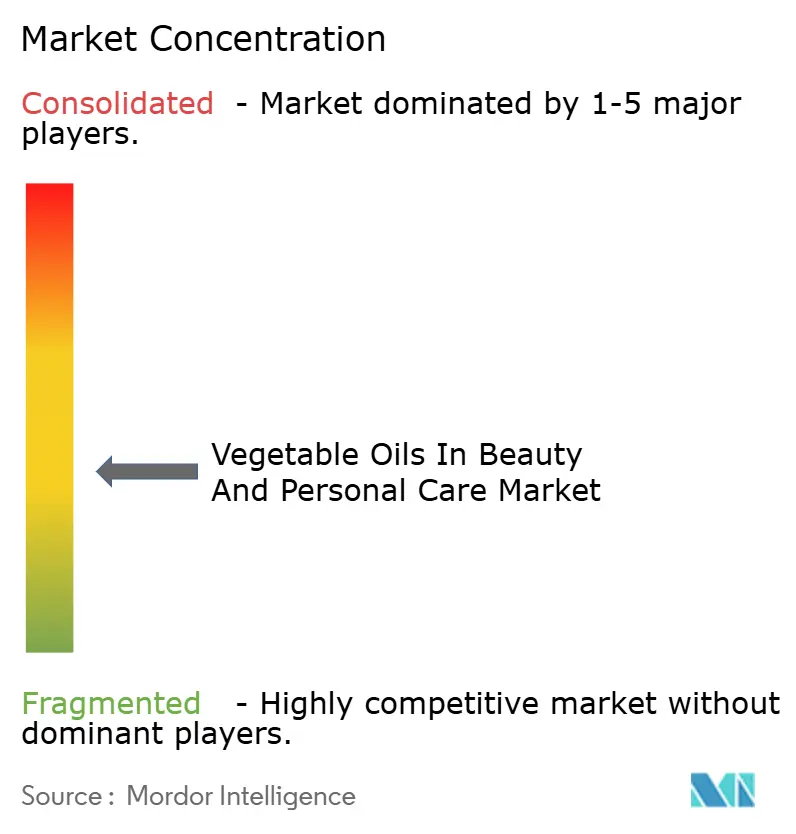

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vegetable Oils In Beauty And Personal Care Market Analysis by Mordor Intelligence

The vegetable oils in the beauty and personal care market size are anticipated to be valued at USD 5.22 billion in 2025 and are forecast to reach USD 6.87 billion by 2030, growing at a 5.67% CAGR during the forecast period. The surge in demand for plant-based emollients, coupled with regulatory shifts favoring safer ingredients and advancements in extraction efficiency, is driving their adoption in skincare, haircare, and fragrances. Techniques like supercritical CO₂ extraction and low-energy drying now retain up to 90% of delicate bioactives, granting brands a competitive quality advantage and bolstering their clean-label assertions. Major beauty conglomerates are ensuring sustainable sourcing through vertical integration and collaborations with raw-material experts. In contrast, smaller entities are carving out their niche by emphasizing provenance storytelling and specialized efficacy. However, challenges persist: supply-chain vulnerabilities linked to climate fluctuations, delays in certification, and issues of adulteration are squeezing margins. This has led to heightened investments in traceability and rigorous quality testing.

Key Report Takeaways

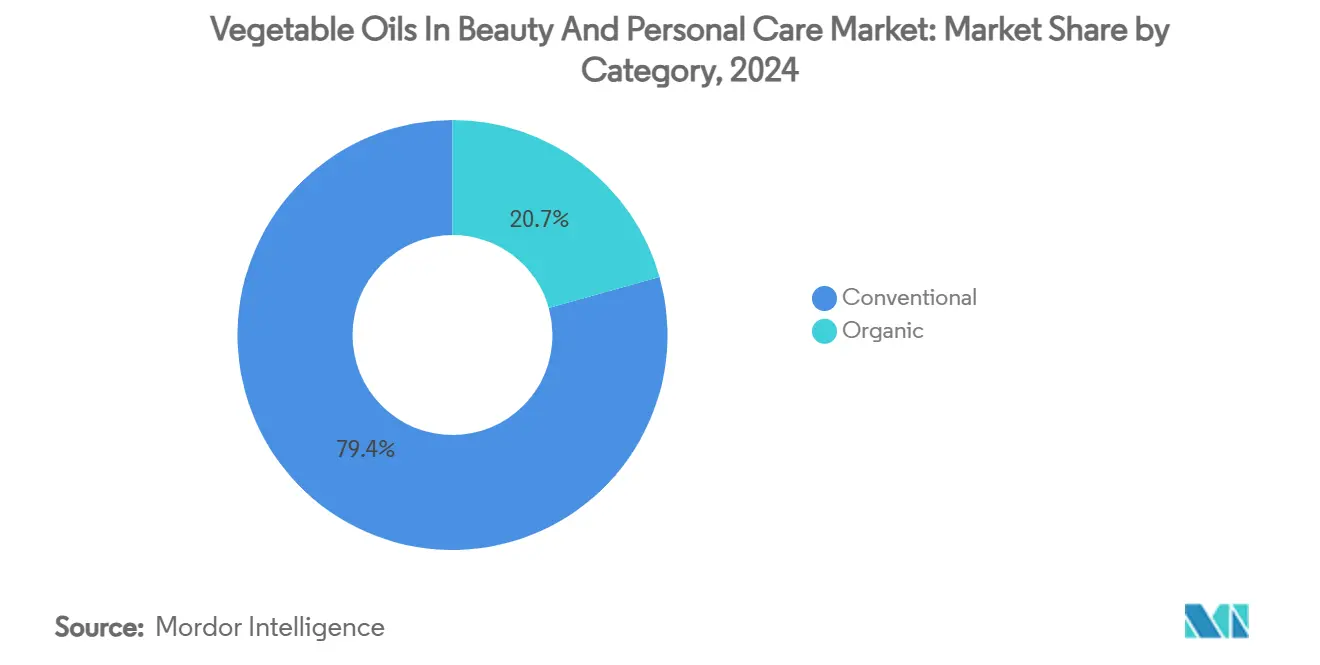

- By category, conventional oils led with 79.35% of revenue in 2024, while the organic segment is set to expand at an 8.63% CAGR through 2030.

- By product type, coconut oil captured 34.12% of sales in 2024; castor oil is projected to post a 7.26% CAGR to 2030.

- By application, skincare accounted for 47.76% of value in 2024, whereas fragrance and aromatherapy are advancing at a 9.74% CAGR over the same horizon.

- By geography, the Asia-Pacific held a 42.31% share in 2024, and the Middle East and Africa region is expected to climb at an 8.16% CAGR to 2030.

Global Vegetable Oils In Beauty And Personal Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Innovations in extraction and preservation | +1.2% | Europe and North America, global rollout | Medium term (2-4 years) |

| Regulatory push toward natural emollients | +0.9% | EU and North America, spillover to APAC | Short term (≤2 years) |

| Formulation technology advancements | +0.8% | Global | Medium term (2-4 years) |

| Rise of the clean-beauty movement | +1.1% | North America and EU, expanding to APAC | Long term (≥4 years) |

| Hyperspectral quality testing | +0.6% | Initially developed markets | Long term (≥4 years) |

| Demand for transparency in ingredients | +0.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Innovations in Extraction and Preservation

Supercritical CO₂ systems now boast extraction yields exceeding 90%, all while sidestepping solvent residues. This not only preserves valuable polyphenols and tocopherols but also enhances skin-barrier performance[1]Source: S. M. Pourmortazavi, “Supercritical Fluid Extraction of Essential Oils,” TrAC Trends in Analytical Chemistry, sciencedirect.com. Meanwhile, Croda's innovative low-energy Zeodration process minimizes thermal damage, providing formulators with a ready-to-use powder that boasts a reduced carbon footprint. Techniques like microwave-assisted and enzyme-based methods are not only slashing processing times and energy consumption but also facilitating smaller batch runs. This is particularly appealing to premium brands that emphasize terroir storytelling. Brands that swiftly adopt these technologies find themselves with enhanced pricing power, as they can clearly highlight their sustainability achievements and functional advantages on packaging. With regulatory bodies tightening their grip on residual solvent limits and carbon disclosures, mainstream producers are feeling the pressure to upgrade, leading to an accelerated investment payback.

Regulatory Push Toward Natural Emollients

Under 21 CFR Part 701, the US FDA now mandates full ingredient disclosure, pushing formulators to adopt shorter, more recognizable labels, predominantly featuring vegetable oils[2]Source: US Food and Drug Administration, “21 CFR Part 701 – Cosmetic Labeling,” ecfr.gov. In Europe, a 2025 ban on certain carcinogens is driving reformulations, paving the way for natural oils to replace synthetic esters in legacy SKUs. Additionally, state-level regulations, like Washington’s Toxic-Free Cosmetics Act, heighten compliance costs for petro-derived ingredients. Meanwhile, EU restrictions on microplastics are hastening the quest for biodegradable, oil-based rheology modifiers. Brands with established botanical portfolios are poised for the market shift, while those lagging behind grapple with the dual challenge of clearing old inventories and financing reformulations.

Rise of the Clean-Beauty Movement

As consumers increasingly opt for clean beauty products, major beauty conglomerates are reformulating their offerings, driven by a surge in demand for organic skincare. L'Oréal, in a bid to lead this transformation, has forged partnerships with biotechnology firms, aiming for a significant milestone: 95% of its ingredients to be bio-based by 2030. This shift not only underscores a broader industry pivot towards renewable sources but also opens up lucrative avenues for vegetable oil producers in the supply chain. However, the clean beauty movement isn't just about changing ingredients. It's also about rethinking packaging. Companies like Dow are at the forefront, collaborating to craft bio-based packaging alternatives that not only perform but also lessen environmental harm. This evolving landscape is leading to a fragmentation in the market. While premium natural brands are reaping substantial rewards, mass-market players find themselves grappling with margin pressures as they navigate the reformulation journey.

Hyperspectral Quality Testing Unlocks New Efficacy Claims

With over 80% accuracy, Vis-NIR and ¹H-NMR methods now verify oil purity, effectively curbing adulteration and facilitating a “pharma-grade” positioning[3]Source: Spectroscopy Online, “New Spectroscopy Method Shows Promise for Detecting Olive Oil Fraud,” spectroscopyonline.com. On-site phenolic measurements, made possible by smartphone plug-ins, empower farm-level quality sorting, bolstering origin claims. These analytics, tied to batch codes via blockchain ledgers, significantly reduce audit costs and enhance consumer trust. Brands certifying antioxidant levels or omega-fatty-acid profiles not only differentiate themselves but also justify premium shelf prices. Laboratories adopting these tools into their standard operating procedures benefit from streamlined regulatory reporting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonal and regional availability constraints | –0.8% | Tropics, global buyers | Short term (≤2 years) |

| Price spikes in certified-organic supply chains | –0.6% | Premium segments worldwide | Medium term (2-4 years) |

| Mislabeling and adulteration risks | –0.4% | Unregulated markets | Long term (≥4 years) |

| Oxidation and shelf-stability issues | –0.5% | Warm climates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Seasonal and Regional Availability Constraints

After disrupted monsoons, intensified climate swings have driven a 12% surge in coconut-oil prices. Meanwhile, geopolitical tensions cast a shadow over palm-kernel alternatives[4]Source: Ohoh Organic, “Oil Price Changes and Why,” ohohorganic.com. Limited organic-certified acreage creates bottlenecks, especially when demand surges around product launches. Processors face extended lead times as they await volume consolidation from smallholder farms, leading to delivery delays and heightened inventory costs. While brands respond by multi-sourcing and engaging in forward contracting, smaller firms find it challenging to muster the capital needed to maintain safety stocks for six months or longer. This supply instability thus curtails rapid expansion in burgeoning regions.

Price Spikes in Certified-Organic Supply Chains

After adverse weather slashed yields, the cost of organic cocoa butter surged, highlighting how stringent certification rules, as noted by Ohoh Organic, hinder the use of crop-protection inputs that could stabilize output. Certification mandates a transition period of 18 to 24 months, binding growers to elevated overheads until new premiums are realized. In times of shortages, luxury brands shoulder the increased costs, while mid-tier masstige lines might entirely forgo organic claims, stunting the category's growth. Additionally, risk-hedging tools like futures contracts remain underutilized for niche beauty oils, leaving mid-tier manufacturers with limited financial safeguards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Conventional Oils Maintain Scale While Organic Gains Ground

In 2024, conventional vegetable oils dominate the market with a 79.35% share, thanks to established supply chains and cost advantages that make them a staple in mass-market formulations. However, the organic segment is making waves, boasting an impressive 8.63% CAGR projected through 2030, indicating a notable shift in consumer preferences towards premium, certified ingredients. While conventional oils leverage economies of scale for competitive pricing across skincare, haircare, and cosmetics, organic variants, with their 40-60% price premium, find their niche in the luxury and prestige segments. This growth in the organic sector is fueled by regulatory pressures in developed markets and a consumer base willing to pay more for verified sustainability, presenting a golden opportunity for brands that can effectively highlight the value of certified ingredients.

Companies are now venturing into hybrid categories, merging the efficiency of conventional methods with organic principles. They're crafting "clean conventional" products that adhere to sustainability standards, albeit without the full organic certification, hinting at a potential shake-up of traditional category boundaries. Meanwhile, biotechnology-derived ingredients are carving out a new niche, marrying the scalability of conventional methods with the purity of organic claims. A case in point is Croda's launch of biotech-derived ceramides on February 27, 2024, which deliver organic-level performance at conventional prices. This blending of technologies indicates a shift in category definitions, moving away from the age-old organic vs. conventional debate to classifications based on performance, aligning more closely with consumer priorities.

By Product Type: Coconut Oil Leads; Castor Oil Accelerates

Coconut oil commands a dominant 34.12% share of the market, thanks to its versatility. It's not just an emollient in skincare; it also conditions hair and serves as a base in color cosmetics. Meanwhile, castor oil, with a 7.26% CAGR, is witnessing a surge in demand, driven by its specialized performance in premium formulations. Coconut oil's appeal in clean beauty products is largely due to its medium-chain fatty acids, known for their antimicrobial properties. Recent studies from Beni-Suef University in 2024 highlighted these oils' effective antiviral and antibacterial activities, bolstering their adoption in products prioritizing natural preservation. Castor oil's ascent can be traced to its unique ricinoleic acid, which offers film-forming and viscosity-enhancing benefits, making it a favorite for long-wear cosmetics and therapeutic skincare.

Despite facing supply constraints, argan oil continues to enjoy steady demand in premium segments. In contrast, newer entrants like sacha inchi and marula oils are carving out niche markets. Their appeal lies in distinct fatty acid profiles and sustainability narratives, resonating with today's conscious consumers, as noted by Taylor & Francis in 2023. Jojoba oil, technically classified as a wax, boasts sensory benefits that render it indispensable in specific formulations. Its non-comedogenic properties are particularly sought after for acne-prone skin, a sentiment echoed by Vantage Group on September 14, 2025. The market is shifting towards functional specialization, with suppliers now focusing on specific oils for their targeted attributes. This shift presents opportunities for those who can offer technical differentiation and application expertise.

By Application: Skincare Dominates; Fragrance and Aromatherapy Surge

In 2024, skincare applications dominate with a 47.76% market share, underscoring the pivotal role of vegetable oils in moisturizers, serums, and treatment products. Meanwhile, the fragrance and aromatherapy segments are witnessing a robust 9.74% CAGR, as consumers increasingly seek multisensory experiences that meld therapeutic benefits with emotional wellness. The maturity of the skincare segment has intensified competition, pushing innovation towards specialized formulations targeting specific concerns like barrier repair, anti-aging, and sensitive skin management. Fragrance and aromatherapy applications leverage the natural aromatic properties of certain vegetable oils, crafting fragrance profiles that resonate with clean beauty trends and offer unique aromatherapeutic benefits, setting them apart from synthetic fragrances.

Haircare applications, while stable, are growing at a more measured pace. Here, vegetable oils predominantly act as conditioning agents and scalp treatments. Coconut and argan oils lead the pack, celebrated for their moisture retention and damage repair capabilities. In the realm of color cosmetics, there's a swift evolution underway. Formulators are increasingly gravitating towards natural substitutes for synthetic waxes and emollients. Plant-based waxes, notably carnauba and candelilla, are gaining momentum, even if they come with performance compromises compared to their synthetic counterparts, as highlighted by OCL Journal in 2022. The segmentation of applications is increasingly mirroring consumer lifestyle trends. Wellness-centric applications are outpacing traditional beauty categories, hinting at a burgeoning market for crossover products that seamlessly integrate cosmetics with therapeutic treatments.

Geography Analysis

Asia-Pacific commands a 42.31% share, underscoring its deep-rooted preference for botanical remedies. The region boasts abundant tropical feedstocks and hosts cost-competitive manufacturing hubs in Indonesia, the Philippines, and China. With rising middle-class incomes and a nod to K-beauty trends, per-capita spending on natural oils is on the rise. Local OEMs adeptly cater to both domestic needs and export demands. E-commerce platforms are not just selling; they're turbocharging brand launches, enabling niche products like coconut and camellia oils to flourish without the burden of extensive physical storefronts. Moreover, government incentives for exporting high-value oleochemicals bolster the region's dominant position.

In the Middle East & Africa, a robust 8.16% CAGR is on the horizon, spurred by a premiumization trend in GCC markets and a global allure for native oils like argan and baobab. Local processors are setting up value-added cold-pressing facilities, ensuring more profits stay within the region. In luxury hubs like Dubai and Riyadh, retailers are curating blends that resonate with the desert's hydration needs, justifying their premium pricing. Meanwhile, digital beauty platforms in major African cities are elevating consumer awareness to global clean-beauty benchmarks, pushing brands towards transparent sourcing.

North America and Europe, while already saturated, continue to upscale as regulations tighten the use of certain synthetics. The EU's clampdown on microplastics and carcinogens positions vegetable oils as a compliant alternative. Concurrently, US retailers are leaning towards “no-list” policies, emphasizing plant-based derivatives. This regulatory landscape, combined with a shift towards premium SKUs featuring encapsulated or enhanced oils, drives a steady low to mid single-digit CAGR. Furthermore, regional R&D hubs are at the forefront, crafting climate-resilient and microbiome-friendly products, and sharing their expertise globally.

Competitive Landscape

In the beauty and personal care sector, the market for vegetable oils is witnessing a blend of established players and emerging disruptors. Major players like BASF, AAK AB, Aromantic Ltd, and Croda International are not just focusing on sustainable ingredient sourcing but are also harnessing AI for formulation optimization. A notable example is L'Oréal's collaboration with IBM, aiming to craft AI models that could transform sustainable cosmetics, particularly in ingredient selection and formulation efficiency, as highlighted by L'Oréal & IBM on January 16, 2025.

Ingredient suppliers, such as Croda International and BASF, are actively acquiring to bolster their botanical extraction capabilities. Croda's takeover of Alban Muller fortifies its stance on natural actives, while BASF's innovative climate-adaptive formulations set it apart in the realm of sustainable emollients. There's a burgeoning opportunity at the crossroads of biotechnology and traditional extraction, where firms can blend the scalability of synthetic production with the allure of natural ingredients.

The competitive landscape is increasingly leaning towards technology-driven differentiation. Companies are channeling investments into unique extraction methods, authentication technologies, and transparent supply chain systems, creating hurdles for smaller entrants. The uptick in patent filings for supercritical extraction and oleosome technology underscores a heated R&D race. While the market's moderate concentration hints at potential consolidation, it also paves the way for niche players to carve out specialized positions, as noted by Croda International on July 29, 2024. New entrants are harnessing biotechnology to derive traditional oils via fermentation, posing a challenge to agricultural supply chains and aligning with the rising demand for sustainable, traceable ingredients in the clean beauty movement.

Vegetable Oils In Beauty And Personal Care Industry Leaders

Croda International

BASF SE

AAK AB

Avril SCA

Vantage Specialty Chemicals, Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: BASF launched three natural-based innovations at in-cosmetics Global 2025, including Dehyton PK45 GA/RA derived from Rainforest Alliance Certified coconut oil, demonstrating the industry's shift toward certified sustainable sourcing that commands premium pricing while meeting clean beauty standards.

- January 2025: L'Oréal partnered with IBM to build the first AI model for sustainable cosmetics, aiming to optimize production processes and utilize renewable ingredients while reducing energy and material waste.

- December 2024: Eternis Fine Chemicals acquired Sharon Personal Care, expanding manufacturing and distribution capabilities across India, Europe, and the US, with a focus on sustainability and innovation in personal care products.

Global Vegetable Oils In Beauty And Personal Care Market Report Scope

| Organic |

| Conventional |

| Coconut Oil |

| Argan Oil |

| Castor Oil |

| Jojoba Oil |

| Olive Oil |

| Other Oils |

| Skin-care |

| Hair-care |

| Color-cosmetics |

| Fragrance and Aromatherapy |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Category | Organic | |

| Conventional | ||

| By Product Type | Coconut Oil | |

| Argan Oil | ||

| Castor Oil | ||

| Jojoba Oil | ||

| Olive Oil | ||

| Other Oils | ||

| By Application | Skin-care | |

| Hair-care | ||

| Color-cosmetics | ||

| Fragrance and Aromatherapy | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of vegetable oils used in beauty and personal care?

The segment stands at USD 5.22 billion in 2025 and is projected to reach USD 6.87 billion by 2030 at a 5.67% CAGR.

Which product type leads sales?

Coconut oil leads with 34.12% share, favored for its versatility across skincare, haircare, and color cosmetics.

Why are organic vegetable oils gaining traction?

Regulatory pressure and consumer willingness to pay premiums for certified sustainable ingredients fuel an 8.63% CAGR in the organic segment.

Which region generates the highest revenue?

Asia-Pacific contributes 42.31% of global sales, supported by abundant raw materials and strong consumer preference for botanical ingredients.

Page last updated on: