Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

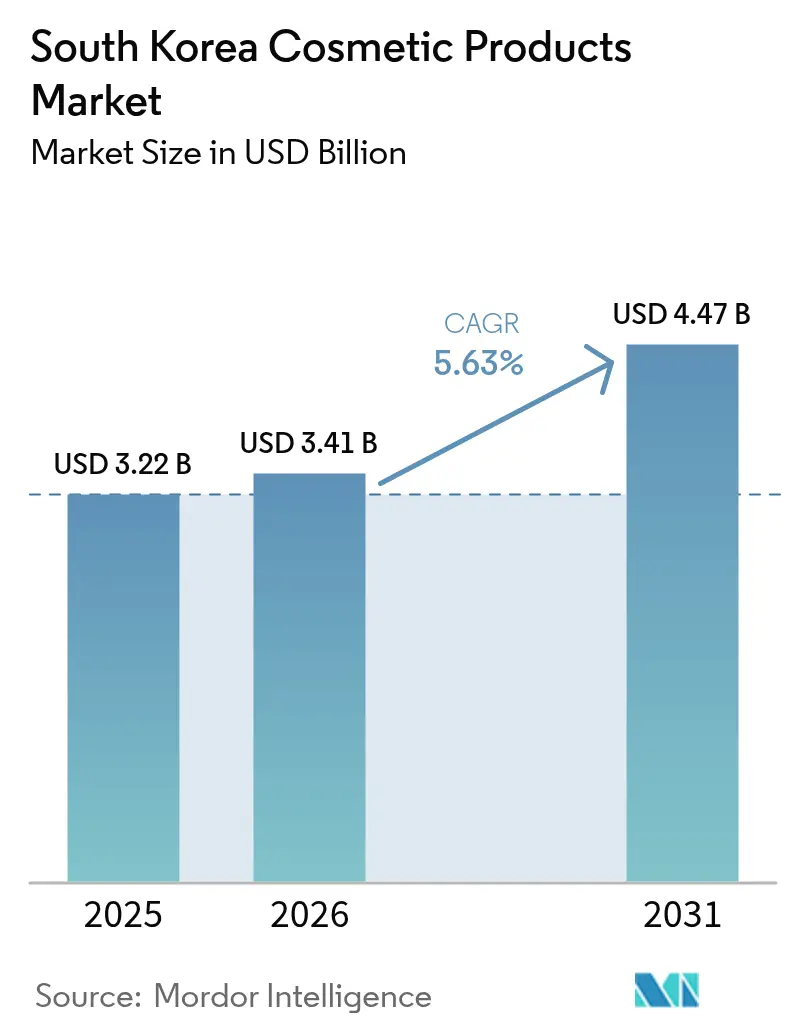

| Base Year Market Size (2025) | USD 3.22 Billion |

| Market Size (2026) | USD 3.41 Billion |

| Market Size (2031) | USD 4.47 Billion |

| Growth Rate (2026 - 2031) | 5.63% CAGR |

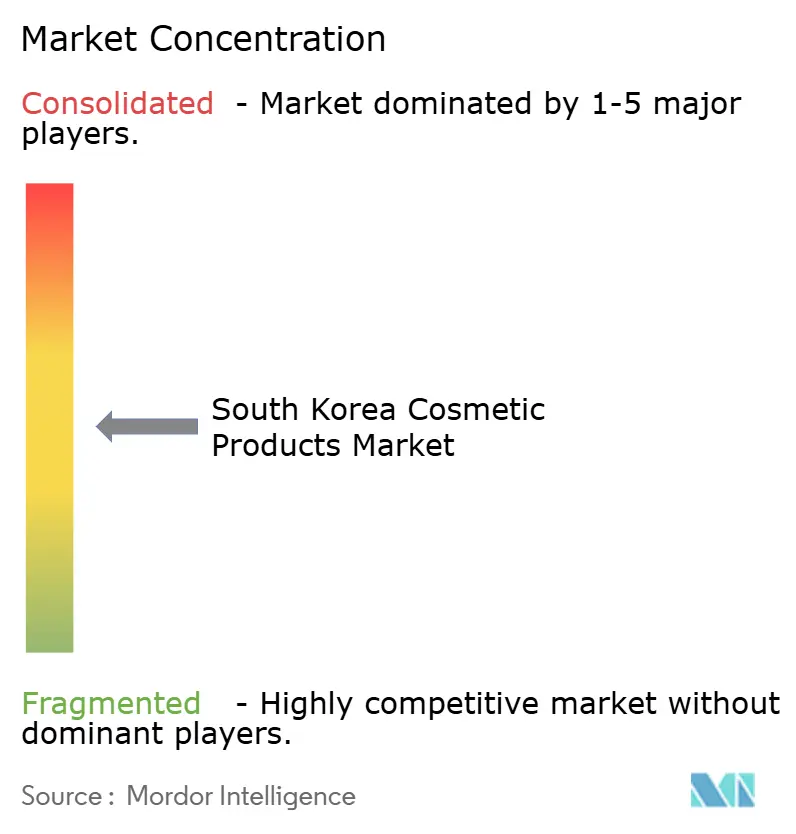

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Korea Cosmetic Products Market Analysis by Mordor Intelligence

South Korea cosmetic products market size in 2026 is estimated at USD 3.41 billion, growing from 2025 value of USD 3.22 billion with 2031 projections showing USD 4.47 billion, growing at 5.63% CAGR over 2026-2031. Core growth stems from surging demand for clean-label ingredients, the proliferation of live-commerce, and technology-enabled personalization tools that improve product matching and lessen return rates. Domestic majors leverage vertically integrated R&D to refresh legacy hero SKUs while hundreds of indie labels, supported by ODM giants, feed consumers’ appetite for novelty and niche positioning. Luxury houses are migrating to local e-commerce marketplaces, where mobile-first millennials and Gen Z shoppers seek convenience and exclusive drops, offsetting sluggish department-store traffic. Meanwhile, the government’s stricter ingredient-safety protocols and counterfeit crackdowns heighten compliance costs yet lift overall consumer confidence, creating a regulatory moat that favors well-capitalized players. Exports top USD 10.2 billion, ranking third globally, underscoring the sector’s dual domestic and outbound opportunity mix.

Key Report Takeaways

- By product type, Facial Cosmetics led with 40.78% of the South Korea cosmetics products market share in 2025, while Lip and Nail Make-up Products are projected to record the fastest 6.98% CAGR through 2031.

- By category, Conventional formulations captured 72.68% share of the South Korea cosmetics products market size in 2025; Organic products will expand at an 7.89% CAGR to 2031.

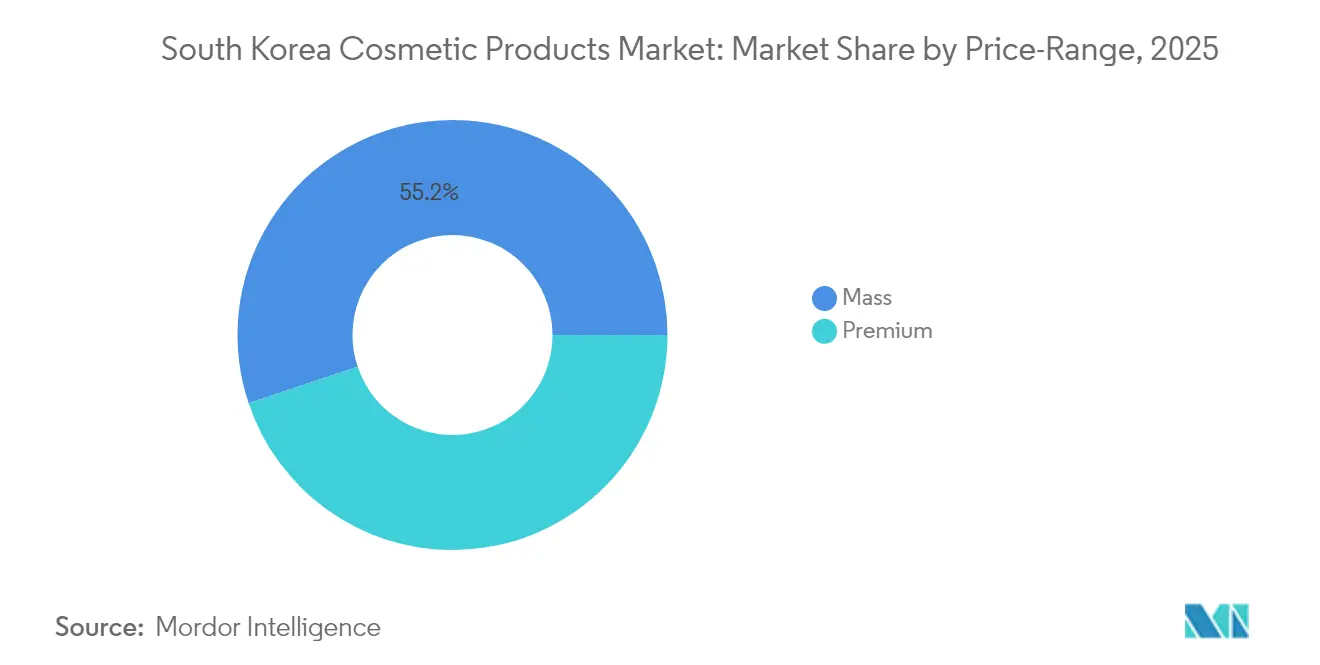

- By price range, Mass-market lines accounted for 55.15% share of the South Korea cosmetics products market size in 2025, whereas Premium lines are set to rise at a 6.18% CAGR through 2031.

- By distribution channel, Health and Beauty Stores held 54.10% of the South Korea cosmetics products market share in 2025, with Online Retail Stores predicted to post the quickest 7.12% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Cosmetic Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inclusive Product Assortments for Diverse Consumers | +0.6% | National, with early gains in Seoul metropolitan area and Busan | Medium term (2-4 years) |

| Increasing Preference for Natural and Clean Formulations | +0.9% | National, spill-over to export markets (US, Japan, Europe) | Long term (≥ 4 years) |

| Enhanced Brand Visibility Through Promotions and Sampling | +0.5% | National, concentrated in Seoul, Seongsu-dong, and tier-2 cities | Short term (≤ 2 years) |

| Influence of Social Media and Online Personalities | +1.1% | National, amplified by the global K-pop and Hallyu wave, reaches | Short term (≤ 2 years) |

| Heightened Awareness of Contemporary Beauty Trends | +0.7% | National, with Seoul and Gyeongsang regions leading adoption | Medium term (2-4 years) |

| Growth of E-Commerce and Digital Sales Platforms | +1.2% | National, accelerated by Coupang, Naver, and Olive Young, online expansion | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Inclusive Product Assortments for Diverse Consumers

Brands are expanding shade ranges and formulation options to address South Korea's increasingly heterogeneous consumer base, which includes expatriates, multicultural families, and domestic consumers seeking personalized solutions. Amorepacific introduced an in-store robot foundation matching across more than 100 shades, enabling precise color selection that previously required multiple testers. This inclusivity extends beyond complexion products. Hera's expansion into Thailand in August 2024 showcased liquid foundations and lip tints tailored for Southeast Asian skin tones, signaling that domestic learnings are informing export strategies. The shift reflects recognition that one-size-fits-all formulations no longer satisfy consumers who expect brands to acknowledge individual skin types, undertones, and lifestyle preferences.

Increasing Preference for Natural and Clean Formulations

Consumer demand for natural and organic ingredients is accelerating, driven by heightened awareness of synthetic chemical risks and a broader wellness movement. Isoi's whitening serum, which contains Bulgarian rose oil and arbutin, held the number-one position in Olive Young's essence category for 11 consecutive years and launched a limited 1+1 promotional set in March 2024, underscoring sustained interest in plant-derived actives. PNStory, a vegan K-beauty SME founded in 2017, reported a significant year-on-year sales growth after securing listings at Incheon Airport duty-free and Olive Young, leveraging patented phytoncide and bamboo-water formulations that underwent clinical trials and hypoallergenic testing. The Ministry of Food and Drug Safety's 2025 amendments to ingredient-safety protocols further incentivize brands to adopt clean formulations, as compliance with stricter standards becomes a competitive differentiator [1]Source: The Ministry of Food and Drug Safety, "Regulations", mfds.go.kr.

Enhanced Brand Visibility Through Promotions and Sampling

Experiential marketing and large-scale promotional events are proving effective in driving trial and conversion, particularly for emerging indie brands lacking established distribution. Musinsa hosted a Beauty Festa pop-up in Seongsu-dong from August 29 to 31, 2024, featuring 36 brands, 86% of which were small- and medium-sized enterprises, 28% launched within the past three years, and 81% lacked their own physical stores. The event attracted significant foot traffic through experiential features such as a photo booth generating personalized "Beauty ID Cards" based on skin type and color, alongside Lucky Box promotions offering products worth KRW 500,000 (approximately USD 375). Lotte Duty Free ran a month-long online festival in April 2024 with 486 brands and discounts up to 70%, leveraging rising international travel.

Influence of Social Media and Online Personalities

Social media platforms and beauty creators wield outsized influence over purchase decisions, with brands increasingly structuring campaigns around influencer partnerships and live-commerce broadcasts. Amorepacific's Mise-en-scène launched a global campaign in May 2024 with K-pop group aespa as ambassadors, releasing five short-form ads tailored to each member and promoting personalized hair-serum solutions across approximately 10 countries, including Korea, China, Japan, Thailand, Indonesia, and Malaysia. Olive Young's live-commerce platform recorded seven broadcasts in orders in the first half of 2024, all featuring new-entry brands or product launches, demonstrating that creator-led content can generate material sales for emerging players. The integration of KakaoTalk Gift and Naver Brand Store into daily consumer routines amplifies reach, as younger cohorts prefer seamless mobile purchasing over traditional e-commerce checkouts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in Counterfeit and Fake Products | -0.4% | National, with a higher incidence in online marketplaces and cross-border e-commerce | Short term (≤ 2 years) |

| Elevated Import Duties on International Cosmetic Brands | -0.3% | National, affecting international brands without FTA benefits | Medium term (2-4 years) |

| Strict Safety and Regulatory Compliance Requirements | -0.5% | National, governed by the Ministry of Food and Drug Safety (MFDS) | Long term (≥ 4 years) |

| Allergic Reactions to Synthetic Cosmetic Ingredients | -0.3% | National, with heightened scrutiny on parabens, phthalates, and formaldehyde | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increase in Counterfeit and Fake Products

Counterfeit cosmetics undermine brand equity and pose safety risks, prompting intensified enforcement by the Ministry of Food and Drug Safety. MFDS launched crackdowns in 2024, imposing penalties on distributors selling fake products and tightening traceability requirements for online marketplaces. The proliferation of counterfeit goods is particularly acute in cross-border e-commerce, where lower-priced imitations exploit consumer price sensitivity and erode trust in authentic products. Brands are responding by integrating blockchain-based authentication and QR-code verification, but the cat-and-mouse dynamic with counterfeiters persists. The reputational damage from safety incidents linked to fake products can spill over to legitimate brands, making industry-wide collaboration on anti-counterfeiting measures a strategic priority.

Elevated Import Duties on International Cosmetic Brands

South Korea applies an 8% general tariff on cosmetics imports, raising landed costs for international brands without free-trade agreement benefits. This duty structure creates a pricing disadvantage relative to domestic manufacturers, particularly in the mass-market segment where consumers exhibit high price elasticity. While FTAs with the European Union and the United States mitigate tariffs for certain brands, smaller international players lacking FTA coverage face margin compression or must pass costs to consumers, limiting their competitiveness[2]Source: European Commission, "EU-South Korea Free Trade Agreement", trade.ec.europa.eu. The tariff environment indirectly benefits domestic majors and ODM specialists, who can leverage local production to avoid import duties and respond more rapidly to trend shifts without cross-border logistics delays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Facial Cosmetics Lead, Lip and Nail Surge

Facial Cosmetics held a 40.78% share in 2025, reflecting entrenched consumer investment in skincare-makeup hybrids such as cushion compacts, BB creams, and tinted moisturizers that deliver coverage while addressing hydration and UV protection. Lip and Nail Make-up Products will grow fastest at 6.98% CAGR through 2031, propelled by the demure makeup trend's emphasis on subtle, muted lip colors and the rise of gel-polish formulations that extend wear time without salon visits. Eye Cosmetics occupies a middle position, benefiting from innovations in long-wearing eyeliners and multi-use shadow sticks that simplify application for time-pressed consumers. Hera's Sensual Powder Matte lip tint, introduced during the brand's Thailand expansion in August 2024, exemplifies the shift toward MLBB (my lips but better) shades that align with natural aesthetics.

The product-type segmentation reveals a strategic tension between established categories and emerging opportunities. Facial Cosmetics remains the largest segment due to the Korean beauty ritual's emphasis on pre-makeup skincare, and the global popularity of cushion compacts. Laneige's Neo Cushion, which won a Red Dot Award in May 2025 for its refillable design, illustrates how sustainability concerns are being integrated into core product formats. Lip and Nail products are gaining share as consumers seek affordable self-expression tools that deliver visible transformation without the complexity of full-face makeup. Eye Cosmetics face competition from minimalist trends that prioritize skin over color, yet innovations such as CLIO's Kill Cover line, offering multiple cushion variants and high-coverage concealers, demonstrate that brands can sustain relevance by addressing specific pain points like dark circles and blemishes.

By Category: Conventional Dominates, Organic Accelerates

Conventional products commanded a 72.68% share in 2025, underscoring the reality that most consumers prioritize efficacy, texture, and price over organic certification. The Organic segment will expand at 7.89% CAGR through 2031, driven by younger cohorts who view clean-label formulations as aligned with broader wellness values and environmental responsibility. Brands such as PNStory, which secured vegan certification and underwent hypoallergenic testing, reported year-on-year sales growth after entering Olive Young and Incheon Airport duty-free, demonstrating that organic positioning can unlock premium pricing and distribution access. The Ministry of Food and Drug Safety's 2025 amendments to ingredient-safety protocols further incentivize organic formulations, as brands seek to preempt regulatory risk by adopting cleaner ingredient decks.

The category split highlights a bifurcation in consumer priorities. Conventional formulations benefit from decades of R&D investment, established supply chains, and consumer familiarity, making them the default choice for mass-market buyers focused on value. Organic products appeal to a smaller but growing segment willing to pay premiums for transparency, natural sourcing, and sustainability claims. Isoi's Cera MD Repair Lotion, which received functional approval from MFDS for itch relief caused by dryness, combines organic positioning with clinical efficacy, bridging the gap between wellness and performance. Brands that successfully communicate both clean credentials and tangible benefits, such as improved barrier function or reduced irritation, will capture disproportionate share in the Organic segment's high-growth trajectory.

By Price Range: Mass Holds Majority, Premium Gains Momentum

Mass-market products accounted for 55.15% of 2025 sales, reflecting South Korea's price-sensitive consumer base and the dominance of value-oriented retailers such as Olive Young, which operates over 1,400 stores domestically and has become the primary discovery channel for new brands. Premium offerings will grow at a 6.18% CAGR through 2031, propelled by luxury brands' strategic pivot to Korean e-commerce platforms and the aspirational appeal of imported prestige labels among affluent millennials. Naver Brand Store brands rose from 61 in 2021 to 87 in 2024, as luxury players recognized that digital channels could reach younger consumers who avoid department stores. Shiseido's Clé de Peau Beauté opened a spa in Seoul in March 2025, combining retail with experiential services to justify premium pricing and deepen brand engagement.

The price-range dynamics underscore a market where volume and value strategies coexist but serve distinct consumer segments. Mass-market brands leverage ODM partnerships with Cosmax and Kolmar Korea to achieve cost efficiencies and rapid product iteration, enabling aggressive promotional pricing. Olive Young's live-commerce broadcasts frequently feature discounts up to 70%, driving trial among budget-conscious shoppers. Premium brands, facing margin pressure from elevated import duties and distribution costs, are investing in brand storytelling, limited-edition collaborations, and personalized services to justify higher price points.

By Distribution Channel: Health and Beauty Stores Anchor, Online Surges

Health and Beauty Stores captured 54.10% of 2025 distribution, anchored by CJ Olive Young's near-monopoly in the specialty retail segment. The retailer opened a dedicated live-commerce studio in October 2024 to strengthen its mobile broadcast platform, where viewers rose year-on-year in the first half of 2024. Online Retail Stores will grow fastest at a 7.12% CAGR through 2031, driven by live-commerce adoption, AI-powered virtual try-on tools, and same-day delivery services that compress the gap between discovery and purchase. Supermarkets and Hypermarkets serve a convenience-driven segment seeking everyday essentials, while Other Distribution Channels, including duty-free, direct-to-consumer, and pop-up formats, cater to niche audiences and experiential shoppers.

The channel landscape reflects a structural shift from passive browsing to active engagement. Olive Young's introduction of "Partner Live" in October 2024 allows merchant brands to run their own live broadcasts with production and marketing support, democratizing access to live-commerce and enabling smaller brands to build direct relationships with consumers. Online channels offer superior economics for brands, lower overhead, real-time inventory visibility, and granular consumer data, but require investment in content creation, influencer partnerships, and logistics infrastructure. The 7.12% CAGR for Online Retail Stores suggests that digital-first brands will capture disproportionate growth, while traditional retailers must integrate experiential elements and omnichannel capabilities to defend share.

Regulatory Landscape

South Korea cosmetics regulation is overseen by the Ministry of Food and Drug Safety (MFDS) under the Cosmetics Act and related enforcement rules, with a growing focus on substantiated safety and post-market controls. In April 2026, amended provisions took effect to strengthen oversight and public disclosure related to directly purchased overseas cosmetics, aligning compliance expectations for cross-border e-commerce listings and tightening scrutiny of products circulating outside traditional import channels.

In July 2026, MFDS issued an advance legislative notice (Notice No. 2026-331) to amend the Enforcement Rules of the Cosmetics Act. The update introduced product safety assessment documentation requirements on a phased schedule beginning in 2028, moving toward broader coverage by 2031. The notice also shortened recall plan submission timelines (from 5 days to 3 days) and expanded eligibility for customized cosmetics refilling sales, increasing both documentation burden and operational accountability for manufacturers, importers, and marketplace-facing brand owners.

Competitive Landscape

The South Korea cosmetics products market exhibits moderate concentration, as domestic majors Amorepacific and LG Household & Health Care command substantial shares through vertically integrated operations spanning R&D, manufacturing, and multi-brand portfolios, yet face persistent pressure from indie brands enabled by ODM specialists Cosmax and Kolmar Korea. The competitive dynamic favors agility; brands that rapidly iterate on trends, leverage influencer partnerships, and adopt AI-powered personalization tools are capturing share from incumbents burdened by legacy product lines and slower decision cycles.

Opportunities exist in personalized cosmetics, and grew year-on-year, with 64.7% of consumers aware of customized offerings and 85.4% expressing willingness to recommend such products. Technology adoption is becoming a strategic imperative for competitive positioning. Amorepacific's six consecutive CES Innovation Awards, including recognition in 2025 for an AI makeup application tool, illustrate how integrating generative AI, voice interaction, and virtual try-on can differentiate brands in a crowded market.

APR Corp, a beauty-tech startup, reported overseas sales exceeding KRW 100 billion (approximately USD 75 million) in the third quarter of 2024, with overseas revenue rising 78.6% year-on-year, demonstrating that device-led strategies can unlock premium pricing and global distribution. Emerging disruptors such as Mixsoon and Skinidea are securing listings at Costco and developing dedicated brands for US consumers, leveraging K-beauty's global reputation while avoiding the commoditization risks of mature domestic channels. The interplay between scale advantages and niche innovation creates a dynamic ecosystem where no single strategy guarantees sustained leadership.

South Korea Cosmetic Products Industry Leaders

-

Amorepacific Corporation

-

LG Household & Health Care Co., Ltd.

-

Kolmar Korea Co., Ltd.

-

Cosmax Co., Ltd.

-

CJ Olive Networks

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Export-oriented growth creates room for brands and manufacturers to package Korea-origin innovation into scalable, compliant assortments for the United States and other destinations. South Korea became the worlds second-largest cosmetics exporter in 2025, with exports reaching USD 11.4 billion and a trade surplus of USD 10.1 billion. The first half of 2026 recorded a USD 7 billion export total, with the United States as the largest destination (20.7% share), which supports opportunities in channel partnerships and digital-first assortment building that translate domestic hero formats (such as skincare-makeup hybrids and clean-label positioning) into export-ready claims, labeling, and content.

On the supply side, capacity expansion and compliance-driven modernization offer practical pathways to serve both domestic retail concentration and export requirements. Examples in 2026 include new and expanding manufacturing footprints in adjacent beauty categories (such as fillers and skin boosters) and announced build-outs for future cosmetics capacity, pointing to investment in automated, quality-controlled production. At the same time, MFDS moves in 2026 toward phased safety assessment documentation and tighter monitoring of directly purchased overseas cosmetics, raising the value of maintaining complete product files, traceability, and recall readiness while still supporting fast trend-cycle launches for online and health and beauty retail channels.

Recent Industry Developments

- May 2026: Amorepacific launched Mamonde exclusively on Amazon Premium Beauty. The move formalized a major digital-first export channel play for a legacy K-beauty brand, using an owned brand storefront environment to scale discovery and conversion outside Korea.

- October 2025: Kolmar Korea was selected as the lead company for South Koreas government-backed AI Factory Alliance project (2025-2029). The initiative supports advanced manufacturing and data-driven production upgrades that strengthen ODM competitiveness for fast-iteration K-beauty brands.

- October 2024: CJ Olive Young opened a dedicated live-commerce studio to expand its mobile broadcast commerce capabilities. The investment reinforced live-commerce as a mainstream sell-through lever for product launches and new-entry brands across Koreas largest health and beauty specialty channel.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of cosmetic products sold in South Korea, including makeup items across mass and premium price ranges, counted at the point they are purchased through offline or online channels.

Scope exclusions: this sizing excludes beauty devices, aesthetic clinic procedures, and general personal care items like soaps, shampoos, and deodorants unless they are explicitly marketed and sold as cosmetic products.

Segmentation Overview

-

By Product Type

- Facial Cosmetics

- Eye Cosmetics

- Lip and Nail Make-up Products

-

By Category

- Conventional

- Organic

-

By Price Range

- Mass

- Premium

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Health and Beauty Stores

- Online Retail Stores

- Other Distribution Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market structure and anchor the model to publicly visible demand and trade signals in South Korea. We reviewed official statistics and open publications, including Statistics Korea (KOSIS) for consumer and macro indicators, Korea Customs Service trade statistics for import and export trends, and Ministry of Food and Drug Safety notices for product compliance cues that can influence launches and reformulations.

To translate these signals into market value, we also used sources such as Korea International Trade Association data releases, industry association pages and periodic briefs, and public company filings and investor presentations for comments on channel mix and category momentum. Patent databases were selectively checked to understand formulation and claim innovation intensity, and an import and export shipment-level database was used where it helped validate trade direction and timing. These desk sources are not exhaustive, and other public documents and references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating how demand is moving across key channels in South Korea, especially online retail, specialty stores, and modern trade, where promotion intensity can quickly change value growth. We spoke with a mix of brand-side leaders, distributors, retailers, and supporting service providers so assumptions on price mix, premiumization, and new product ramp-up could be checked across viewpoints.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 14% | |

| Mid tier: 47% | Functional/Unit leaders: 37% | |

| Smaller Players: 14% | Managers: 49% |

Market-Sizing & Forecasting

The core sizing logic starts with a top-down build that reconstructs South Korea cosmetics value using category splits, channel shares, and price band mix, then aligns the structure to visible consumption and trade direction. Once the structure is in place, the totals are corroborated with selective bottom-up approximations, such as sampled average selling price checks for key product baskets and volume proxies gathered through channel discussions, before final totals are adjusted.

Inputs used in the model include premium versus mass mix shifts, online retail share changes, promotional intensity and discounting patterns, new product launch cadence, and import and export momentum that affects availability and assortment in the market. Where bottom-up coverage was incomplete for small brands or fragmented channels, gaps were handled through controlled scaling factors that were rechecked with distributors and retail-side respondents to keep the model realistic.

For forecasting, scenario analysis was used because demand is sensitive to channel volatility and pricing moves. The scenarios were built around expected shifts in online penetration, premiumization, and trade dynamics. The final forecast path was then cross-checked with expert expectations gathered during primary discussions to keep the trajectory practical.

Data Validation & Update Cycle

Validation was done through multiple checks so the market totals remain consistent with independent signals, not just one data series. We compared model outputs against observable indicators such as trade movement, channel growth narratives, and price mix direction, then investigated sharp variances that did not match what interviewees described.

Before sign-off, the work is reviewed in steps, including logic review of assumptions, year-over-year variance checks, and a final pass to ensure definitions and inclusions are applied consistently. The report is refreshed annually, and interim updates are made when material events occur that can change demand, pricing, or channel structure. Right before delivery, an analyst completes a fresh update sweep so clients receive the latest view.

Mordor Intelligence's South Korea Cosmetics Products Market Market Size Compared With Other Published Estimates

Published market sizes for South Korea cosmetics do not always align because the scope can shift between makeup-only definitions and broader beauty and personal care baskets. Base years and currency timing choices also differ across publishers. Differences also come from how each publisher treats online discounting and premium mix changes, which can move the value number even when volumes look stable.

By tracking channel-level value shares and refreshing discount and price mix assumptions, Mordor Intelligence keeps this estimate focused on cosmetic products sold in South Korea (makeup-led scope) rather than folding in adjacent personal care categories that widen the total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.22 B (2025) | |

| Global Consultancy A | USD 18.39 B (2025) | Uses a broader cosmetics basket that includes skin care, hair care, bath and shower, deodorants, and fragrances, which expands the boundary beyond makeup-focused cosmetic products. A longer forecast window also tends to smooth short-term channel swings and discount cycles. |

| Industry Publisher B | USD 17.45 B (2023) | Anchors the value on a different base year and a wider definition that blends multiple personal care and fragrance categories with cosmetics. The gap also reflects different treatment of retail versus channel pricing during promotional periods and currency conversion timing. |

The spread in the table is mainly explained by category boundaries and timing, not by small math differences. When scope is kept tight to cosmetic products and the price mix is checked against channel realities, the final number stays traceable to a defined demand pool and repeatable steps.

Key Questions Answered in the Report

What is the current value of the South Korea cosmetics products market?

The market is valued at USD 3.41 billion in 2026 and is projected to reach USD 4.47 billion by 2031.

Which product segment is growing fastest in South Korea?

Lip and Nail Make-up Products are forecast to grow at a 6.98% CAGR through 2031, the quickest among all categories.

How significant are online channels for beauty sales in South Korea?

Online Retail Stores are the fastest-growing channel, expected to post a 7.12% CAGR as live-commerce and AI virtual try-ons gain traction.

Why are clean-label cosmetics gaining popularity?

Heightened awareness of synthetic ingredient risks, stricter MFDS regulations, and wellness trends are driving an 7.89% CAGR for Organic products.

Page last updated on: