Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

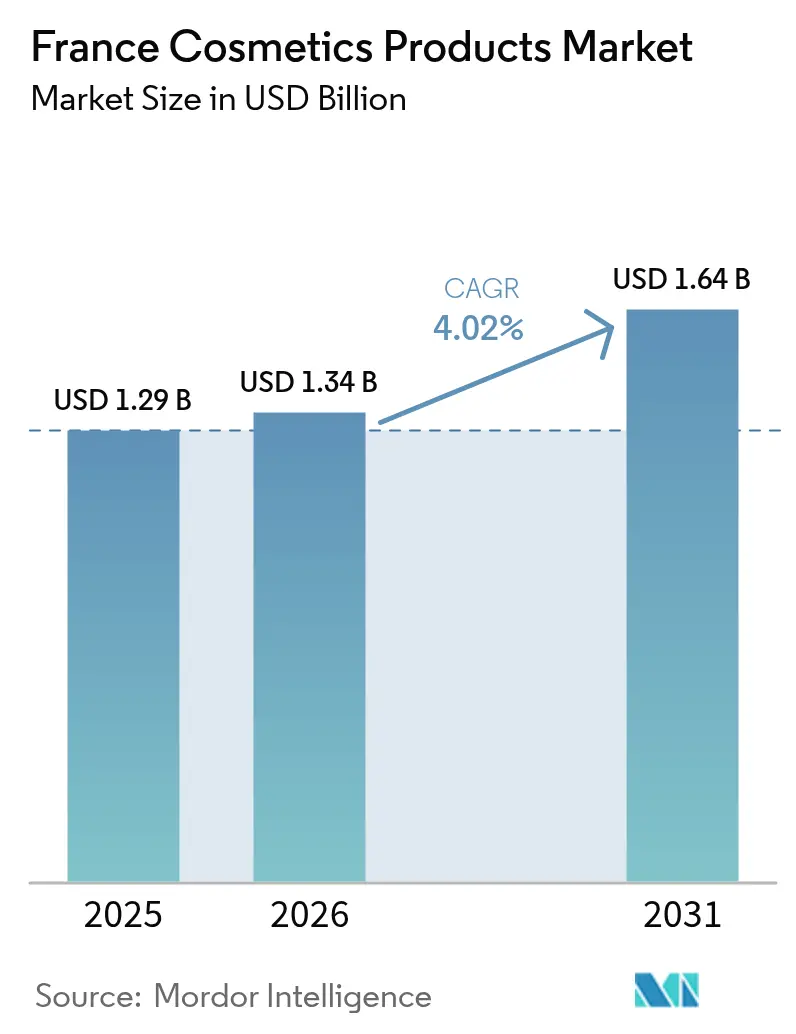

| Base Year Market Size (2025) | USD 1.29 Billion |

| Market Size (2026) | USD 1.34 Billion |

| Market Size (2031) | USD 1.64 Billion |

| Growth Rate (2026 - 2031) | 4.02% CAGR |

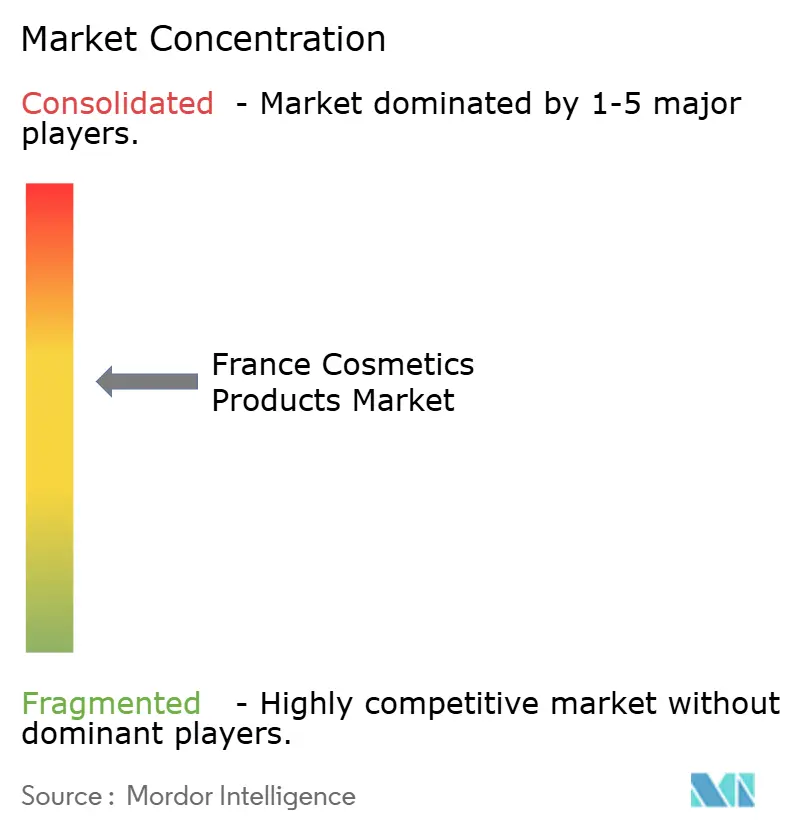

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Cosmetics Products Market Analysis by Mordor Intelligence

The France cosmetics products market size is expected to grow from USD 1.29 billion in 2025 to USD 1.34 billion in 2026 and is forecast to reach USD 1.64 billion by 2031 at 4.02% CAGR over 2026-2031. Pharmacy sales continue to strengthen as consumers favor clinically backed actives and pharmacist recommendations, while digital channels expand reach and fuel direct-to-consumer growth; L’Oréal generated 28.2% of domestic sales online in 2024, and Yves Rocher aims to double its current 10% online share within three years. Innovation in ingredients remains a key catalyst, with launches such as BASF’s Pepsensyal peptide and Clariant’s CycloRetin providing evidence-based anti-aging benefits that support premium pricing.

Key Report Takeaways

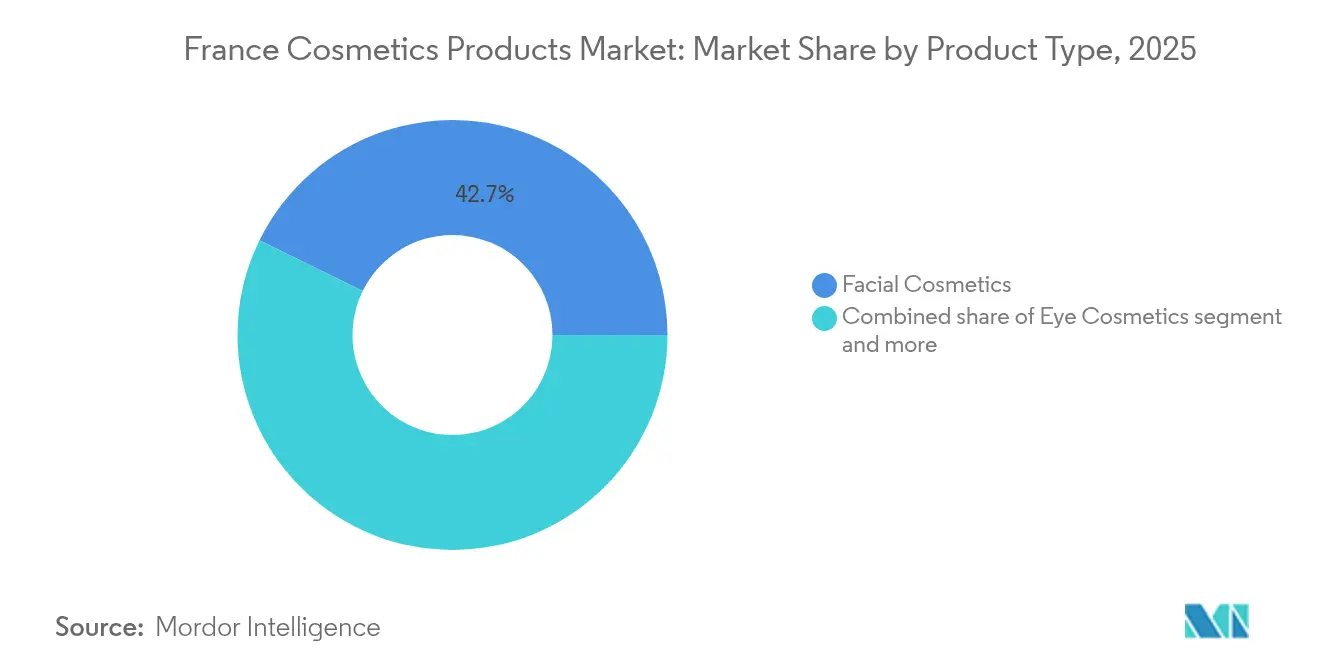

- By product type, facial cosmetics commanded 42.74% of the French cosmetics market share in 2025, while eye cosmetics are on course to expand at a 5.52% CAGR through 2031.

- By category, mass products retained a 56.10% share of the France cosmetics products market size in 2025, yet premium products are advancing at a 5.78% CAGR to 2031

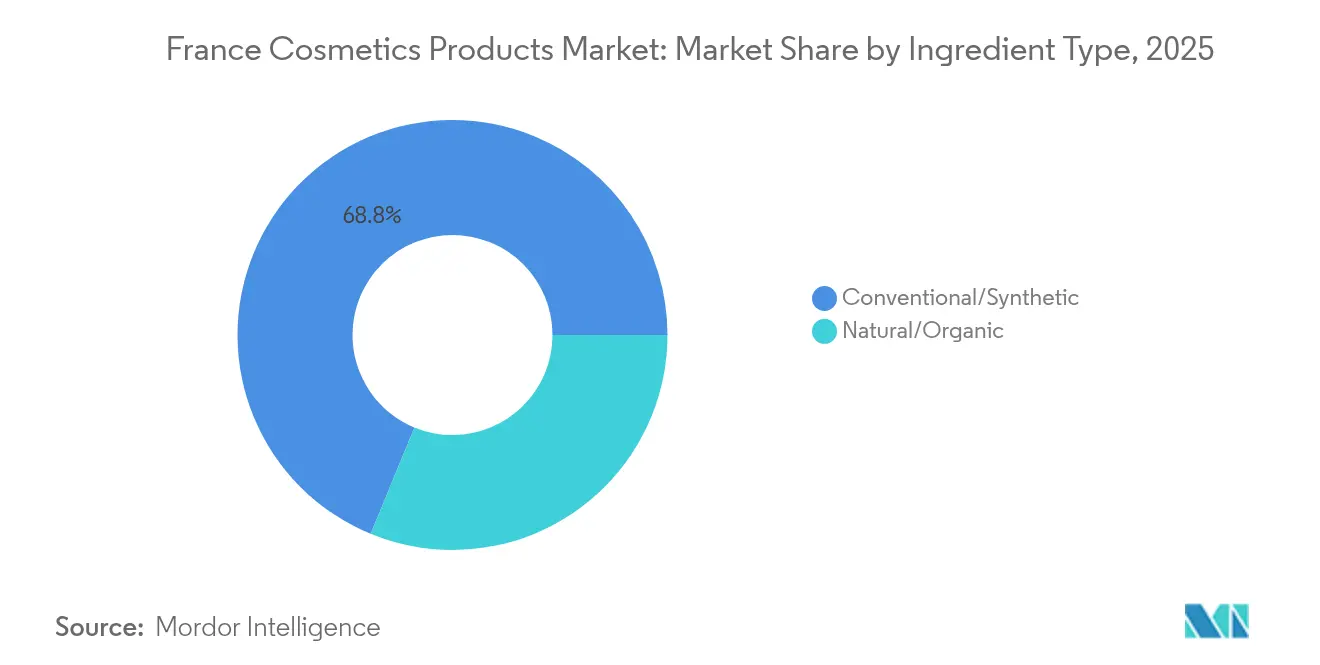

- By ingredient type, conventional formulations held 68.79% of the French cosmetics products market share in 2025, and natural/organic products are forecast to rise at a 6.21% CAGR toward 2031.

- By distribution, supermarkets/hypermarkets led with a 37.88% share in 2025, while online channels are projected to grow at a 5.96% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Cosmetics Products Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surge in online beauty commerce | +1.2% | National, with concentration in Île-de-France and major urban centers | Short term (≤ 2 years) |

| Premiumisation of make-up products | +0.9% | National, strongest in Paris, Lyon, Marseille selective retail | Medium term (2-4 years) |

| Shift to natural and organic formulations | +0.8% | National, with rural and peri-urban early adoption | Medium term (2-4 years) |

| Pharmacy-led dermocosmetic boom | +1.0% | National, particularly strong in pharmacy-dense regions | Short term (≤ 2 years) |

| Scientific and active ingredient innovation | +0.7% | National, driven by R&D hubs in Île-de-France, Auvergne-Rhône-Alpes | Long term (≥ 4 years) |

| Growth of microbiome-friendly and sensitive-skin products | +0.5% | National, with early gains in pharmacy and specialty channels | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in online beauty commerce

French health and beauty e-commerce expanded rapidly in 2024, with 32% of internet users purchasing online in Q2, and overall e-commerce grew 15% year-on-year. Cosmetics captured an outsized share, thanks to personalized diagnostics and subscription models that mass retailers cannot match, according to the French E-commerce Federation[1]Source: Fédération du e-commerce et de la vente à distance, “Baromètre 2024,” fevad.com. L’Oréal’s e-commerce penetration reached 28.2% in 2024, demonstrating how heritage brands are shifting online. Meanwhile, Yves Rocher’s September 2024 marketplace launch aims to double its online revenue share to 20% within three years by aggregating third-party beauty labels. Digital acceleration is also fueling direct-to-consumer disruptors, such as Typology Paris, which are winning over younger consumers who prioritize ingredient transparency and interactive digital experiences over traditional branding. Amazon’s move into physical parapharmacy further blurs channel boundaries, pressuring incumbents to invest in omnichannel fulfillment and real-time inventory visibility. Meanwhile, regulation is tightening: the European Commission’s forthcoming Digital Product Passport, under the Ecodesign Regulation, will require end-to-end traceability, favoring digitally native brands that are already equipped with granular product data infrastructure[2]Source: European Commission, “Ecodesign Regulation and Digital Product Passport,” ec.europa.eu.

Premiumization of make-up products

Louis Vuitton’s Autumn 2025 debut of La Beauté, a collection comprising 55 lipsticks, 10 balms, and 8 eyeshadow palettes created in collaboration with Pat McGrath, illustrates how luxury fashion houses increasingly view makeup as a high-margin, brand-extending category that requires far less capital investment than leather goods, according to Vogue Business. Premium beauty products are expanding at a 5.96% CAGR through 2030, outpacing mass-market offerings because they command 2-3× higher price points while maintaining broadly similar formulation and packaging cost structures. Department stores report that in 2023, luxury items represented 50% of beauty sales, compared with 20% for premium and 11% for prestige products, underscoring the outsize spending power of the top consumer quintile, according to the International Association of Department Stores (IADS). This premiumization is especially evident in color cosmetics, where lip and eye makeup lead department-store beauty sales. Trends showcased during Paris Fashion Week 2025, including deep reds, burgundies, and plums, are fueling demand for high-ticket, limited-edition launches that routinely sell out within weeks.

Shift to natural and organic formulations

Natural and organic cosmetics are projected to grow at a 6.43% CAGR through 2030, the fastest among ingredient categories, as French consumers increasingly prefer natural/bio products and routinely scrutinize ingredient labels before making a purchase. Brands are responding with deeper control of their supply chains: Clarins plans to cultivate one-third of its ingredients in-house by 2030, reinforcing traceability and premium positioning, while Laboratoires Expanscience now operates 19 raw-material supply chains and opened a second processing plant in Peru in June 2024 to support 350 avocado producers, evidence that natural sourcing requires long-term partnerships and capital investment that mass-market players struggle to match. Regulatory pressure is amplifying the shift: the EU Cosmetics Regulation and France’s ANSES continue to tighten oversight of synthetic preservatives and fragrance allergens, with Safety Gate 2024 data showing that cosmetics made up 36% of product alerts, many tied to the banned allergen butylphenyl methylpropional. Although natural formulations help brands avoid these compliance risks, they carry higher input costs, allowing premium brands to absorb margin pressure while mass-market competitors remain more cautious.

Pharmacy-led dermocosmetic boom

The pharmacy channel in France is poised for strong growth in 2024, outpacing other distribution formats, as consumers view pharmacists as trusted advisors on skin health and are willing to pay premiums for products offered in a clinical setting. Facial-care sales illustrate that dermocosmetic brands have established defensible positions by investing in clinical trials and dermatologist endorsements. Notably, pharmacy makeup sales rose 14% in 2024, extending the dermocosmetic halo beyond skincare into color cosmetics, which selective and mass retailers traditionally dominate. Innovations such as Pierre Fabre’s Avène sunscreen, featuring 33% less plastic packaging and photocorrecteur SKUs, demonstrate how pharmacy brands are also leading the way in sustainability, offering a dual value proposition that resonates with French consumers. The channel’s structural advantage in sunscreen sales is underpinned by long-standing pharmacist-consumer trust and regulatory frameworks that protect pharmacy-exclusive distribution for certain categories, a barrier that mass retailers cannot easily replicate.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent EU and French ingredient regulations | -0.6% | National, aligned with EU-wide enforcement | Medium term (2-4 years) |

| High cost of natural and sustainable inputs | -0.5% | National, particularly affecting small and mid-sized producers | Short term (≤ 2 years) |

| Counterfeit products impact premium segments | -0.4% | National, with concentration in online and parallel import channels | Short term (≤ 2 years) |

| Rising raw material price volatility | -0.4% | Global, with pass-through effects on French manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent EU and French ingredient regulations

The regulatory environment for cosmetics in France and the EU imposes a complex, multi-layered compliance burden that elevates market-entry costs and slows innovation. Oversight by France’s ANSES, DGCCRF, and ANSM complements the European Commission’s Cosmetics Regulation, with DGCCRF assuming responsibility for Good Manufacturing Practice controls in January 2024, adding a domestic enforcement layer atop EU-wide rules (DGCCRF)[3]Source: DGCCRF, “Contrôles BPF 2024,” economie.gouv.fr/dgccrf. Safety Gate 2024 reported that 36% of product alerts involved cosmetics, frequently citing banned fragrance allergen butylphenyl methylpropional, undeclared allergens, microbiological contamination, and heavy metals, highlighting widespread compliance risks amid intensifying enforcement. Furthermore, the European Commission’s Recommendation 2024/915 on anti-counterfeiting measures and the forthcoming Digital Product Passport under the Ecodesign Regulation will mandate end-to-end supply chain traceability, favoring large, digitally mature companies over smaller producers (ECHA). Ingredient-level regulatory changes, such as the ECHA Risk Assessment Committee’s proposed classification of p-cymene as Repr. 1B would restrict essential oils and necessitate reformulation across hundreds of SKUs, demonstrating how granular regulations cascade through portfolios. While these measures enhance consumer safety, they impose an estimated -0.6% drag on CAGR by delaying product launches, raising formulation costs, and creating entry barriers that protect incumbents at the expense of innovation.

High cost of natural and sustainable inputs

Natural and organic cosmetics are expanding at a 6.43% CAGR, but they face structural cost pressures because natural raw materials are exposed to agricultural yield variability, fair-trade premiums, and traceability obligations that synthetic ingredients largely avoid. Clarins’ plan to source one-third of its ingredients in-house by 2030 entails significant capital investment in farming partnerships and processing facilities, expenses that mass-market players cannot easily absorb without eroding margins. Laboratoires Expanscience’s second processing plant in Peru, inaugurated in June 2024, supports 350 avocado producers through long-term contracts that ensure fair prices and environmental stewardship. However, this vertically integrated model is capital-intensive and slow to scale. Ingredient-supplier consolidation, exemplified by Solabia’s September 2024 acquisition of PolymerExpert, reflects efforts to achieve economies of scale in bio-based chemistry, though M&A premiums ultimately increase input costs for manufacturers. The price gap between natural and synthetic actives can exceed 50%, forcing brands to balance margin compression against potential volume losses from higher prices. This cost dynamic is estimated to impose a -0.5% drag on CAGR in the short term as brands navigate the transition toward natural formulations without alienating price-sensitive consumers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Eye Cosmetics Outpace Facial Care Growth

Facial cosmetics accounted for 42.74% of the French market in 2025, remaining the largest segment due to foundations, concealers, and skincare-makeup hybrids that benefit from the dermocosmetic boom. However, eye cosmetics are projected to grow at a 5.52% CAGR through 2031, the fastest among product types, driven by Paris Fashion Week 2025 trends such as metallic accents, reverse eyeliner, and icy/frosted eyeshadows, which accelerate product innovation cycles (MakeUp in Paris). Luxury entrants are emphasizing this category: Louis Vuitton’s La Beauté autumn 2025 launch includes 8 eyeshadow palettes alongside 55 lipsticks and 10 balms, reflecting the high-margin, high-repurchase potential of eye makeup (Vogue Business).

Shifts from glass skin to soft matte finishes and the return of brown tones are micro-trends that increase SKU proliferation and shorten product life cycles, favoring brands with agile supply chains and digital-first distribution. L’Oréal’s mass-market adaptations, such as Cool Silver, Revitalift Laser, and Bright Reveal SPF50, illustrate how runway-inspired innovation quickly cascades to drugstore shelves, compressing the trend-to-market cycle. Facial-care innovation increasingly relies on mechanism-based formulations, as seen with Beiersdorf’s Nivea Q10 Dual Action serum launched in April 2024, which incorporates anti-glycation technology and clinical substantiation, creating barriers that protect incumbents. By contrast, eye cosmetics are more trend-driven and lightly regulated, enabling faster product cycles and lower entry barriers, explaining their higher growth despite a smaller market share and why premium brands are disproportionately investing in this category to capture younger, trend-conscious consumers.

By Category: Premium Gains as Mass Contracts

Mass cosmetics accounted for 56.10% of the French market in 2025, reflecting broad accessibility and appeal to price-sensitive consumers through supermarkets, hypermarkets, and drugstores. However, premium products are expanding at a 5.78% CAGR through 2031, driven by consumers trading up to higher-priced, efficacy-backed offerings even as mass volume growth slows. Luxury entrants signal this strategic pivot: Louis Vuitton’s La Beauté launch, Balmain Beauty’s EUR 250 (USD 272) fragrances, and Estée Lauder’s Paris fragrance atelier opening in 2025 demonstrate that fashion houses are leveraging brand equity and customer loyalty to capture a greater share of the cosmetics market. French consumers’ strong brand literacy and willingness to pay for provenance and craftsmanship reinforce this trend.

Mass brands retain a majority share because of their widespread distribution and affordability, yet growth is increasingly concentrated in premium and dermocosmetic segments. L’Oréal’s Dermatological Beauty division grew 9.8% in 2024, outpacing its mass-market brands Garnier, Maybelline, and L’Oréal Paris, while Yves Rocher’s EUR 1.2 billion (USD 1.31 billion) revenue and target to double online sales to 20% within three years highlight mid-tier brands’ investment in digital channels to compete on convenience and personalization. The mass-to-premium shift varies by product type, sunscreen remains 50% pharmacy-distributed, maintaining a structural advantage for dermocosmetics, but overall, French consumers are increasingly willing to pay a premium for clinical efficacy, ingredient transparency, and brand prestige.

By Ingredient Type: Natural Formulations Gain Despite Cost Headwinds

Natural and organic formulations are projected to grow at a 6.21% CAGR through 2031, the fastest among ingredient types, despite structural cost and formulation challenges that conventional and synthetic ingredients avoid. Conventional ingredients dominated the market with 68.79% share in 2025, benefiting from cost efficiency, stability, and regulatory familiarity; however, consumer preference is shifting toward traceable, bio-based options. Brands are responding to the trend with vertical integration and strategic sourcing. Clarins aims to produce one-third of its ingredients in-house by 2030, while Laboratoires Expanscience operates 19 supply chains, including a second processing plant in Peru, inaugurated in June 2024, to support 350 avocado producers, demonstrating the long-term investment required for natural sourcing. Contract manufacturers are also adapting: PHARMA & BEAUTY Group reported that 98% of its cosmetic formulas are of natural origin and achieved Ecocert certification across all five French production sites, highlighting industry-wide alignment with the natural trend.

Regulation reinforces this shift. The EU Cosmetics Regulation and France’s ANSES increasingly scrutinize synthetic preservatives and fragrance allergens, with Safety Gate 2024 reporting that cosmetics accounted for 36% of product alerts, many related to banned allergens such as butylphenyl methylpropional. Natural formulations mitigate these compliance risks but face challenges including microbiological stability, shorter shelf life, and higher cost of goods, which premium brands can absorb while mass-market players remain constrained. Supplier consolidation further supports scalability: Solabia’s acquisition of PolymerExpert in September 2024 and L’Oréal and Evonik’s minority stake in Abolis Biotechnologies as part of a EUR 35 million (USD 38.15 million) fundraising round illustrate investment in end-to-end bio-based ingredient value chains. Collectively, these developments indicate that natural formulations represent a structural industry shift requiring R&D, manufacturing innovation, and supply-chain reconfiguration, rather than a temporary niche trend.

By Distribution Channel: Online Gains as Pharmacy Thrives

In 2025, supermarkets and hypermarkets accounted for 37.88% of cosmetics distribution in France, yet online retail is outpacing traditional channels with a projected 5.96% CAGR through 2031, driven by L’Oréal’s 28.2% e-commerce penetration, Yves Rocher’s ambition to double its online sales to 20% of revenue, and Amazon’s entry into European physical parapharmacy. Digital adoption is accelerating: 32% of French internet users purchased health and beauty products online in Q2 2024, while overall e-commerce grew 15% year-on-year, with cosmetics capturing a disproportionate share due to personalized diagnostics, subscription models, and direct-to-consumer engagement that mass retailers cannot replicate. Yves Rocher’s September 2024 marketplace launch, which aggregates third-party beauty brands, mirrors Amazon and Sephora, highlighting a structural shift toward multi-brand, omnichannel, data-driven retail. Meanwhile, specialty stores such as Sephora, Nocibé, and Marionnaud continue to gain market share through vertical integration and curated experiences.

The pharmacy channel demonstrated the strongest value growth in 2024, reflecting French consumers’ trust in pharmacists as credible advisors on skin health and their willingness to pay a premium for clinically endorsed products. Notably, pharmacy-based makeup sales expanded, indicating that the dermocosmetic halo is extending beyond skincare into color cosmetics. Conversely, supermarkets and hypermarkets are losing ground due to their inability to match the personalization of specialty stores, clinical credibility of pharmacies, and convenience of online platforms. Across Europe, the online fashion and beauty market is showing strong growth, reinforcing the structural pivot toward digital distribution and omnichannel retailing.

Geography Analysis

France serves as both the production hub and primary consumption market for cosmetics, highlighting a trend of consumers trading up to higher-priced, efficacy-backed products rather than simply increasing purchase volumes. The pharmacy channel underlines the defensible positions of dermocosmetic brands, which leverage clinical trials and dermatologist endorsements to sustain growth in facial care and sunscreen segments. France is also the world’s largest cosmetics exporter, reinforcing its brands’ global pricing power and equity, while the sector employs 226,000 people and generates EUR 71 billion (USD 77.37 billion) in turnover, making it a strategic component of French industrial policy and export competitiveness.

R&D and production are concentrated in Île-de-France, Auvergne-Rhône-Alpes, and Provence-Alpes-Côte d’Azur, with L’Oréal headquartered in Clichy, NAOS laboratories in Aix-en-Provence, and PHARMA & BEAUTY Group operating five plants nationwide. Active-ingredient innovation remains strong, exemplified by BASF’s Pepsensyal peptide launch in October 2024 from Pulnoy, delivering measurable reductions in crow’s feet roughness and dermal re-densification. Paris continues to anchor the luxury cosmetics market, with launches such as Louis Vuitton’s La Beauté, Estée Lauder’s Paris fragrance atelier (2025), and Balmain Beauty’s Les Éternels fragrances targeting affluent, brand-conscious consumers. Meanwhile, rural and peri-urban regions are early adopters of natural and organic products, reflecting widespread consumer attention to ingredient transparency.

The regulatory environment is multi-layered, governed by ANSES (ingredient safety), DGCCRF (market surveillance and GMP enforcement since January 2024), and ANSM (drug-cosmetic borderline products), creating high barriers to entry that favor established players. Counterfeit cosmetics pose a geographic and digital risk, with French Customs seizing 20 million counterfeit items in 2023, 92% originating from China and Turkey, and annual losses estimated at EUR 800 million (USD 872 million), disproportionately impacting premium brands. The European Commission’s Recommendation 2024/915 on anti-counterfeiting and the forthcoming Digital Product Passport under the Ecodesign Regulation will mandate end-to-end traceability, favoring large, digitally mature companies. France’s strategic location as a gateway to the EU single market, combined with its luxury brand heritage, R&D infrastructure, and regulatory sophistication, ensures continued global relevance, even as online distribution and direct-to-consumer models begin to erode the advantages of physical retail density and pharmacy networks.

Competitive Landscape

The France cosmetics market demonstrates moderate concentration, with the top five players, L’Oréal, Clarins, Estée Lauder, Coty, and LVMH, holding substantial share, yet facing persistent pressure from direct-to-consumer insurgents like Typology Paris and luxury fashion houses that bypass traditional conglomerates. L’Oréal’s EUR 43.48 billion (USD 47.36 billion) in sales for 2024, up 5.1% like-for-like, and EUR 8.69 billion (USD 9.47 billion) in operating profit provide the margin flexibility to sustain R&D investments exceeding EUR 1.3 billion (USD 1.42 billion) annually and omnichannel expansion, with 28.2% e-commerce penetration. Strategic consolidation is evident: Kering’s October 2025 sale of its beauty division, including Creed and long-term Gucci, Bottega Veneta, and Balenciaga licenses, to L’Oréal for EUR 4 billion (USD 4.36 billion) underscores the challenge of scaling beauty platforms profitably, as Kering Beauté posted a EUR 60 million operating loss in H1 2025. Similarly, L’Occitane’s 2024 privatization at EUR 6.5 billion (USD 7.08 billion) signals pressure on mid-tier players that lack either mass-market scale or ultra-luxury positioning.

White-space opportunities are emerging in microbiome-friendly formulations, biotech-derived actives, and refillable packaging, exemplified by Laboratoires Expanscience’s Mustela refillable trial, which achieves 76% plastic reduction and 220g CO₂ savings per user annually, metrics that resonate with eco-conscious French consumers. Strategic patterns emphasize vertical integration of natural ingredient supply chains, omnichannel distribution, and clinical substantiation. Clarins’ commitment to grow one-third of its ingredients in-house by 2030 strengthens traceability and premium positioning, while fifteen major companies, including L’Oréal, Clarins, Chanel, Dior, Estée Lauder, Nuxe, and Shiseido, formed the Trasce consortium to enhance supply-chain transparency, reflecting recognition that raw material sourcing is a strategic risk. L’Oréal’s August 2024 acquisition of a 10% stake in Swiss dermatology firm Galderma signals a pivot toward beauty technology and medical-aesthetic adjacencies.

Innovation and digital engagement differentiate incumbents from insurgents. The INPI ranked L’Oréal as France’s 3rd largest patent filer in 2024, a return to the top ranks after a decade, signaling renewed investment in proprietary technology. Emerging disruptors like Typology Paris leverage direct-to-consumer distribution and ingredient transparency to capture younger cohorts, while 900.care, with EUR 21 million (USD 22.89 million) in funding, scales solid cosmetics and refillable formats. Overall, the competitive landscape is bifurcating: scale players invest in biotech partnerships and clinical substantiation, while insurgents compete on transparency, sustainability, and digital engagement, leaving mid-tier brands with insufficient resources for either approach vulnerable to margin compression and market share erosion.

France Cosmetics Products Industry Leaders

L'Oréal S.A.

Groupe Clarins SA

The Estée Lauder Companies

Coty Inc.

LVMH Moët Hennessy Louis Vuitton

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: L'Oréal and Evonik took minority stakes in Abolis Biotechnologies to build a bio-based ingredient value chain.

- September 2024: Yves Rocher launched a multi-brand marketplace, targeting 20% of its online revenue within three years.

- June 2024: Laboratoires Expanscience opened a second Peruvian plant supporting 350 avocado farmers under sustainable contracts.

France Cosmetics Products Market Report Scope

The cosmetic products market encompasses a wide range of products used for cleansing, beautifying, and enhancing personal appearance. The France cosmetics products market is segmented by product type, category, ingredient type, and distribution channel. The cosmetics/makeup products segment is segmented into facial cosmetics, cosmetic eye products, and lip and nail makeup products. By category, the market is segmented into mass and premium products. By ingredient types, the market is segmented into natural/organic and conventional/synthetic. Based on the distribution channel, the market studied is segmented into specialty stores, supermarkets/hypermarkets, online retail stores, and other distribution channels. The market sizing has been conducted in value terms (USD) for all the aforementioned segments.

By Product Type

| Facial Cosmetics |

| Eye Cosmetics |

| Lip and Nail Make-up Products |

By Category

| Premium Products |

| Mass Products |

By Ingredient Type

| Natural/Organic |

| Conventional/Synthetic |

By Distribution Channel

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Other Channels |

| By Product Type | Facial Cosmetics |

| Eye Cosmetics | |

| Lip and Nail Make-up Products | |

| By Category | Premium Products |

| Mass Products | |

| By Ingredient Type | Natural/Organic |

| Conventional/Synthetic | |

| By Distribution Channel | Specialty Stores |

| Supermarkets/Hypermarkets | |

| Online Retail Stores | |

| Other Channels |

Key Questions Answered in the Report

How fast are online sales growing within the France cosmetics products market?

Online channels are expanding at a 5.96% CAGR through 2031 and already represent 28.2% of L'Oréal’s domestic turnover.

Which product type shows the quickest growth?

Eye cosmetics lead with a projected 5.52% CAGR through 2031, driven by fashion-led innovation cycles.

What is driving premiumisation in France?

Luxury houses entering make-up, clinically backed actives, and consumer willingness to trade up for efficacy are raising average prices.

What are the main regulatory hurdles for new entrants?

Multi-layered EU and French ingredient regulations, GMP audits by DGCCRF, and upcoming Digital Product Passports increase compliance costs.

Page last updated on: