Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.09 Billion |

| Market Size (2026) | USD 2.21 Billion |

| Market Size (2031) | USD 2.89 Billion |

| Growth Rate (2026 - 2031) | 5.56% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Cosmetics Products Market Analysis by Mordor Intelligence

The Italy cosmetics products market size was valued at USD 2.09 billion in 2025 and estimated to grow from USD 2.21 billion in 2026 to reach USD 2.89 billion by 2031, at a CAGR of 5.56% during the forecast period (2026-2031). This growth is underpinned by Italy's prominent role as Europe's contract-manufacturing hub, where 67% of the continent's makeup and 55% of global volumes are produced. The market is further bolstered by increasing consumer preference for natural formulations, the appeal of premium-priced products, and the shift toward digital-first shopping experiences. Export performance has also been strong, with a 12% year-on-year increase in 2024, reaching EUR 7.9 billion (USD 8.6 billion), showcasing a balanced growth strategy that leverages both domestic and international markets. Regulatory developments are shaping the market as well, with the February 2025 ban on nanomaterials and the planned 2026 expansion of fragrance-allergen regulations driving faster reformulation cycles, which agile Italian suppliers are well-positioned to capitalize on. Additionally, e-commerce has seen significant growth, with sales rising by 13.5% to EUR 1.3 billion (USD 1.4 billion) in 2024, fueled by consumer interest in tools that provide ingredient transparency and the growing popularity of subscription-based models.

Key Report Takeaways

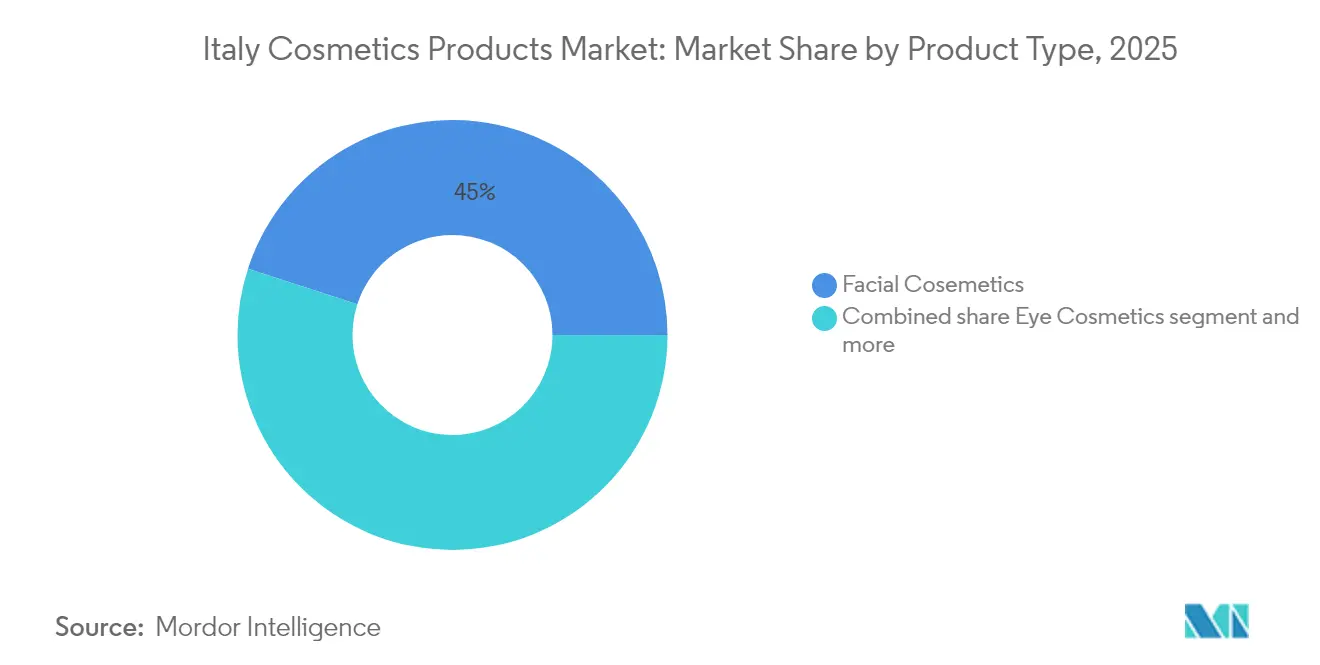

- By product type, facial cosmetics led with 45.01% value share in 2025, while eye cosmetics are set to post the fastest 6.31% CAGR through 2031 on the back of tiktok-driven demand for statement looks.

- By category, mass products controlled 61.88% of sales in 2025; however, premium products will narrow the gap with a 6.28% CAGR to 2031 as affluent shoppers trade up to dermatologist-endorsed and Made-in-Italy lines.

- By ingredients, conventional formulations retained 69.02% share in 2025, yet natural and organic variants will expand at a 6.72% CAGR, the highest rate across all segmentation types, reflecting a transparency-first consumer mindset.

- By distribution channel, Specialty Stores captured 36.52% revenue in 2025, but online retail Stores will accelerate at a 6.41% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Cosmetics Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong consumer shift toward natural, organic, and "clean" beauty products | +1.2% | National, with concentration in Northern urban centers (Milan, Turin, Bologna) | Medium term (2–4 years) |

| High consumer awareness of ingredient safety and transparency | +0.9% | National, amplified by pharmacy and specialty-store channels | Short term (≤ 2 years) |

| Rising interest in men's grooming, including beard care and skincare | +0.7% | National, early adoption in metropolitan areas | Medium term (2–4 years) |

| Growth in professional and dermo-cosmetic channels | +0.8% | National, pharmacy-led with spillover to specialty stores | Medium term (2–4 years) |

| Increasing collaboration between cosmetic brands, dermatologists, and research institutions | +0.6% | National, concentrated in Lombardy and Emilia-Romagna (Cosmetic Valley) | Long term (≥ 4 years) |

| Strong Italian heritage in beauty, fragrance, and fashion, supporting premium and niche cosmetic brands | +1.0% | National, with export amplification to Europe and United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong Consumer Shift Toward Natural, Organic, and "Clean" Beauty Products

The increasing demand for natural and organic cosmetics is significantly shaping formulation priorities and transforming supply chain collaborations across Italy. Among all ingredient categories, natural and organic ingredients are experiencing the fastest growth, while conventional and synthetic formulations continue to maintain a substantial market share. This trend indicates that the rising popularity of "clean" beauty is contributing to overall market expansion rather than replacing traditional products. Consumers are increasingly adopting a hybrid approach, combining certified-natural products, such as serums, with conventional items like foundations to address their skincare needs. Italian certification bodies, such as the Institute for Ethical and Environmental Certification (ICEA) and the Italian Association for Organic Agriculture (AIAB), have been setting organic cosmetics standards for over a decade. However, the adoption of these standards has accelerated in recent years. Retailers like Esselunga's EsserBella chain, which operates in regions including Lombardy, Piedmont, Emilia-Romagna, Liguria, and Tuscany, have expanded shelf space for COSMOS-certified brands[1]Source: Cosmos Standard, “Organic and natural certification for cosmetics,” cosmos-standard.org. Additionally, these retailers have introduced in-store skin diagnostics to help consumers select ingredient-transparent products, further driving the growth of the natural and organic cosmetics market. Innovation among ingredient suppliers plays a crucial role in the evolution of this market. For instance, dsm-firmenich partnered with ExoLab Italia to develop and commercialize plant-derived exosomes for anti-aging formulations. This development provides a biotechnology-based alternative to synthetic peptides, appealing to dermatologists focused on product efficacy and consumers who prioritize sustainability in their purchasing decisions.

High Consumer Awareness of Ingredient Safety and Transparency

Transparency has transitioned from being merely a marketing advantage to becoming a fundamental expectation, especially in pharmacy and specialty channels where pharmacists play a critical role as gatekeepers. BioNike, recognized as Italy's leading dermocosmetics brand, achieved €89.1 million (USD 97 million) in sales during 2024 and holds a 4.8% volume share in Italian pharmacies. The brand has built its reputation by offering hypoallergenic and fragrance-free formulations, which are supported by clinical trials and complete ingredient transparency. Regulation 2023/1545, which significantly expands the fragrance-allergen list from 26 to over 80 substances, is set to take effect on July 31, 2026, for new products and July 31, 2028, for existing stock[2]Source: European Union “Regulation (EU) 2024/1938 Of The European Parliament And Of The Council,” eur-lex.europa.eu. This regulatory change will require brands to reformulate their products to comply or face the risk of being removed from European Union markets. Amazon, recognizing the importance of transparency and personalization, opened its first parapharmacy in Milan on February 13, 2025. This facility features Perfect Corporation's artificial intelligence skin-diagnostic mirrors, which analyze 15 skin concerns and recommend products with a full breakdown of ingredients. The combined impact of regulatory mandates and increasing consumer awareness is accelerating product life cycles, pushing brands to plan for reformulation every two years instead of the traditional five-year cycle.

Rising Interest in Men's Grooming, Including Beard Care and Skincare

Men's grooming is transitioning from a niche segment to the mainstream, with Italian brands such as Bullfrog, which was established in Milan in the year 2013, expanding their professional salon networks and introducing beard-care kits priced between seventeen euros and forty-eight euros and ninety cents. These kits include oils, balms, and styling tools. The global men's skincare market is experiencing growth at a pace faster than the overall cosmetics market, and Italy's position as a developed market aligns with higher per-capita consumption. This trend is driven by increasing disposable income and the convergence of grooming habits. Intercos Group, which reported net sales of nine hundred eighty-eight million two hundred thousand euros (equivalent to one billion one hundred million United States dollars) for the year 2023, witnessed a significant forty-seven percent growth in its hair and body unit, reaching two hundred thirty-one million three hundred thousand euros (equivalent to two hundred fifty-two million United States dollars). This growth was partly driven by independent men's grooming brands that emphasize minimalist packaging and multifunctional formulations. Furthermore, the expansion of this category is reshaping promotional strategies, as brands increasingly leverage male influencers on platforms such as TikTok and Instagram to reduce the stigma associated with skincare routines and encourage the adoption of daily moisturizers and sunscreen.

Growth in Professional and Dermo-Cosmetic Channels

Pharmacy and professional channels are experiencing higher value growth compared to mass retail, indicating a consumer preference for prescriber-endorsed products and in-store consultations. In 2024, Italy's pharmacy channel achieved EUR 2.2 billion (USD 2.4 billion) in sales, with BioNike accounting for EUR 89.1 million (USD 97 million) and a 4.8% volume share. This highlights the trust pharmacists hold in recommending dermocosmetics for sensitive skin, rosacea, and post-procedure care. Davines Group reported EUR 263 million (USD 286 million) in revenue for 2023, reflecting a 14% increase, and is expanding its production capacity by 50% to meet the growing demand from professional salons that value the brand's B Corp certification and sustainable sourcing. The resilience of these channels during economic downturns—pharmacies and salons continue to attract foot traffic even when discretionary spending declines—positions them as strategic priorities for brands aiming to secure stable cash flow.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex and evolving Europe and national cosmetic regulations on safety, ingredients, and labelling | -0.8% | National, with Europe-wide compliance requirements | Short term (≤ 2 years) |

| Restrictions or tighter limits on certain ingredients | -0.6% | National, driven by Europe directives | Medium term (2–4 years) |

| High marketing and promotional spend needed to stand out in crowded digital and retail channels | -0.5% | National, intensified in e-commerce and social media | Short term (≤ 2 years) |

| Consumer scepticism toward greenwashing and unsubstantiated claims | -0.4% | National, particularly among Millennial and Gen Z cohorts | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Complex and Evolving Europe and National Cosmetic Regulations on Safety, Ingredients, and Labelling

Regulatory compliance costs are on the rise as the European Union enforces overlapping directives that significantly reduce reformulation timelines and demand more comprehensive documentation. Regulation 2024/858, which will come into effect on February 1, 2025, prohibits twelve forms of nanomaterials, including styrene/acrylates copolymer, copper, silver, gold, and platinum nanoparticles. This regulation requires brands to conduct thorough audits of their entire supply chains and replace restricted ingredients in products such as sunscreens, anti-aging serums, and color cosmetics. Furthermore, Regulation 2023/2055 imposes restrictions on the use of microplastics in rinse-off cosmetics, with a compliance deadline of October 17, 2035. This mandates formulators to replace materials like polyethylene and polypropylene beads with biodegradable alternatives such as jojoba esters or cellulose. These changes result in a notable increase in raw material costs and necessitate rigorous stability testing to maintain product shelf life. The fragmented enforcement framework, where Italy's Ministry of Health performs spot checks and individual regions enforce additional labeling requirements, creates a complex compliance environment that increases the likelihood of unintentional violations and associated penalties.

Restrictions or Tighter Limits on Certain Ingredients

Ingredient restrictions are limiting formulation options, compelling brands to explore alternative chemistries that may not match the performance of traditional active ingredients. Regulation 2023/1545 has expanded the fragrance-allergen list from 26 to over 80 substances, with compliance deadlines set for July 2026, for new products and July 31, 2028, for existing stock. This regulation impacts not only perfumes but also scented lotions, shampoos, and color cosmetics that use fragrances to mask base odors. Additionally, the microplastics ban affects products such as exfoliating scrubs and toothpastes, where polyethylene beads previously offered a cost-effective solution for abrasion. Biodegradable alternatives, such as bamboo powder or walnut shell, require new sourcing arrangements and may alter product texture, potentially leading to consumer dissatisfaction and returns. In response, Chromavis, an Italian color-cosmetic formulator, has developed VeilCoat technology for loose-powder foundations. This innovation eliminates synthetic polymers while maintaining blendability; however, it requires 18–24 months of research, development, and clinical testing before reaching commercialization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Facial Cosmetics Anchor, Eye Cosmetics Surge

Facial cosmetics accounted for 45.01% of the product-type share in 2025, emphasizing the category's extensive range of offerings, which include cleansers, moisturizers, serums, and sunscreens. This category is regarded as a daily-use essential rather than a discretionary purchase, making it a staple in consumers' routines. The consistent demand for these products highlights their importance in everyday skincare and beauty regimens, ensuring their dominant position in the market.

In contrast, eye cosmetics are expected to grow at a compound annual growth rate (CAGR) of 6.31% through 2031, marking the fastest growth among all product types. This surge is fueled by increasing consumer interest in products such as colored mascara, false eyelashes, and statement eyeshadow palettes, trends that have gained traction on social media platforms like TikTok. Events such as Milan Fashion Week Spring/Summer 2026 further amplified this demand, with bold eye looks taking center stage. IL Cosmetics, recognized as Italy's leading nail polish manufacturer in Europe and the second-largest globally, has strategically diversified its portfolio. The company introduced its first powders at Cosmoprof Bologna 2025, utilizing patented "Baked Rodio" technology, and launched "Lash-Tattoo Mascara" at MakeUp New York in September 2025. These initiatives reflect a deliberate effort by Italian suppliers to expand beyond nail products and tap into the growing opportunities within the eye cosmetics market.

By Category: Premium Gains Ground, Mass Retains Volume

Mass products accounted for 61.88% of the category share in 2025. However, premium products are projected to grow at a compound annual growth rate (CAGR) of 6.28% through 2031, gradually closing the gap as wealthier consumers increasingly prefer dermatologist-endorsed formulations, niche fragrances, and products with Made-in-Italy provenance. Dolce & Gabbana Beauty reported EUR 1.5 billion (USD 1.6 billion) in first-year in-house sales in 2024 and has set an ambitious target of EUR 4 billion (USD 4.3 billion) by 2026–2027. The brand's strategy focuses on leveraging all-Italian production facilities near Milan, enabling it to offer premium price points ranging from EUR 80 to EUR 150 (USD 87 to USD 163) for lipsticks and foundations. This approach underscores the growing demand for high-quality, locally produced luxury items.

LVMH's Perfumes and Cosmetics division, which includes premium brands distributed in Italy, recorded EUR 4.136 billion (USD 4.5 billion) in revenue for the first half of 2024, reflecting a 6% organic growth. Dior Sauvage retained its position as the number one global fragrance, demonstrating the enduring appeal of luxury products even as inflationary pressures challenge discretionary spending. On the other hand, mass products continue to dominate in terms of volume, supported by widespread availability through supermarket and hypermarket distribution channels. These channels accounted for 73% of nail varnish sales in 2024 and experienced a growth of 5.3%, as consumers increasingly prioritize convenience and competitive pricing for their routine purchases.

By Ingredients: Conventional Dominates, Natural Accelerates

Conventional and synthetic ingredients accounted for 69.02% of the market share in 2025. However, natural and organic formulations are expected to grow at a compound annual growth rate (CAGR) of 6.72% through 2031, representing the fastest growth rate among all segmentation types. This growth is primarily driven by increasing consumer demand for greater transparency in product ingredients and third-party certifications. COSMOS-certified Italian brands, including BEMA COSMETICI, ARGITAL, L'ERBOLARIO, and OFFICINA NATURAE, are expanding their production capabilities to align with retailer requirements for sustainable product assortments. For example, Esselunga's EsserBella chain has dedicated over 20% of its shelf space to certified-natural products across its 47 stores located in Northern and Central Italy. This shift highlights the growing importance of sustainability in consumer purchasing decisions.

Innovation in ingredient development is progressing rapidly. dsm-firmenich, in collaboration with ExoLab Italia, is working to commercialize plant-derived exosomes for use in anti-aging serums, offering a biotechnology-based alternative to synthetic peptides. Furthermore, Evonik launched a sustainable emollients manufacturing plant in Germany in September 2024, employing enzymatic processes that reduce carbon emissions by 40%. Despite these advancements, conventional formulations continue to dominate the market due to their cost-effectiveness, stability, and reliable performance. Synthetic preservatives, such as phenoxyethanol and parabens, extend product shelf life to 36 months, whereas natural alternatives often require refrigeration or have shorter use-by dates, which can complicate logistics and lead to increased waste. Chromavis, an Italian color-cosmetic formulator, supports hybrid approaches that combine natural pigments with synthetic binders. This approach aims to achieve both clean-label appeal and long-wear performance, as demonstrated in its VeilCoat loose-powder foundation, which eliminates synthetic polymers while maintaining blendability.

By Distribution Channel: Specialty Stores Lead, Online Surges

In 2025, specialty stores accounted for 36.52% of the distribution share, driven by prominent chains such as Sephora, Douglas, and Esselunga's EsserBella, which operates 47 stores. These specialty stores distinguish themselves by offering curated product assortments, opportunities for product sampling, and a range of beauty services, including consultations for skin, hair, nails, brows, and makeup. These personalized services provide a unique shopping experience that mass retailers are unable to replicate. Supermarkets and hypermarkets, while not the fastest-growing distribution channel, played a significant role by contributing to 73% of nail varnish sales in 2024 and achieving a growth rate of 5.3%. This performance underscores the importance of convenience and competitive pricing in influencing routine consumer purchases. Esselunga, Italy's leading supermarket chain with 189 stores and a revenue of EUR 9.326 billion (USD 10.1 billion) in 2023, has strategically dedicated sections for perfume and beauty products. Additionally, the company operates 47 EsserBella specialty stores, showcasing a hybrid strategy that successfully caters to both convenience-driven and experience-driven shoppers.

The increasing shift toward online shopping is transforming inventory management practices. Brands are now required to maintain distinct stock-keeping units (SKUs) tailored to specific sales channels. For e-commerce, this includes smaller product sizes and subscription-friendly formats, while retail channels prioritize full-size products and gift sets. While this approach adds complexity to inventory management, it enables brands to implement price segmentation effectively, addressing diverse consumer preferences and purchasing behaviors. Italian consumers are progressively adopting digital services, and the market is becoming more advanced. This digital transformation is driven by government investments in infrastructure and the efforts of key operators. Approximately 50 million Italians (85% of the population) use the internet, and nearly 40 million are expected to shop online in 2024.

Geography Analysis

Italy's cosmetics market plays a significant role as both a major consumption hub and a manufacturing center. Domestic consumption is projected to reach EUR 13.4 billion (USD 14.6 billion) in 2024, reflecting a growth rate of 6.9%. Meanwhile, exports are expected to reach EUR 7.9 billion (USD 8.6 billion), marking a 12% increase. This dual role underscores Italy's importance as both a key end-market for cosmetics and a contract manufacturing base for international brands. The concentration of production in Lombardy's "Cosmetic Valley," centered in Crema and nearby municipalities, provides Italian manufacturers with a distinct logistical advantage. Companies such as Ancorotti Group, employing over 500 people and anticipating revenue of EUR 220 million (USD 239 million) in 2025, and Intercos Group, which reported EUR 988.2 million (USD 1.1 billion) in sales in 2023, can deliver finished goods to European retailers within 48 hours. This speed is unmatched by suppliers from Asia, giving Italian manufacturers a competitive edge.

The northern regions of Italy, including Lombardy, Piedmont, and Emilia-Romagna, dominate both production and retail activities in the cosmetics market. Esselunga's 47 EsserBella specialty stores are predominantly located in these areas, with Milan serving as a central hub for fashion and beauty crossover events. For instance, Milan Fashion Week Spring/Summer 2026 featured Vivetta's runway, which showcased emerging trends such as colored mascara and bold eye makeup looks. Central Italy, led by Tuscany and Lazio, contributes to the market through niche fragrance houses and artisanal brands. A notable example is Dr. Vranjes Firenze, a brand acquired by L'Occitane in April 2024 for an undisclosed amount. The company leverages its Florentine heritage to offer premium home fragrances and personal scents, priced between EUR 150 and EUR 300 (USD 163 and USD 326), appealing to a high-end consumer base.

Southern Italy, while less developed in comparison to the northern regions, is gradually narrowing the gap. Rising disposable incomes and the expansion of retail networks are driving growth in this part of the country. For example, Esselunga opened new stores in Genova and Cascina Merlata in 2023, both of which include EsserBella outlets. These developments signal a growing retail presence in Southern Italy, contributing to the overall expansion of the cosmetics market in the region.

Regulatory Landscape

Italy follows the EU cosmetics framework under Regulation (EC) No 1223/2009, which requires each product to undergo a safety assessment, be supported by a Product Information File, and have a designated Responsible Person before sale. Market entry is tied to notification in the EU Cosmetic Product Notification Portal (CPNP), while Italian-specific requirements place additional emphasis on compliant labeling in Italian under Article 19 and on adherence to Good Manufacturing Practice expectations.

Enforcement and controls are handled primarily by the Ministero della Salute through market surveillance activities, including documentation checks and analytical or microbiological testing. Italy also uses customs controls for imported goods and operates cosmetovigilance systems for collecting reports of undesirable effects, which increases the need for traceability, rapid corrective actions (including withdrawal/recall), and substantiation of safety and claims across both offline retail and e-commerce listings.

Competitive Landscape

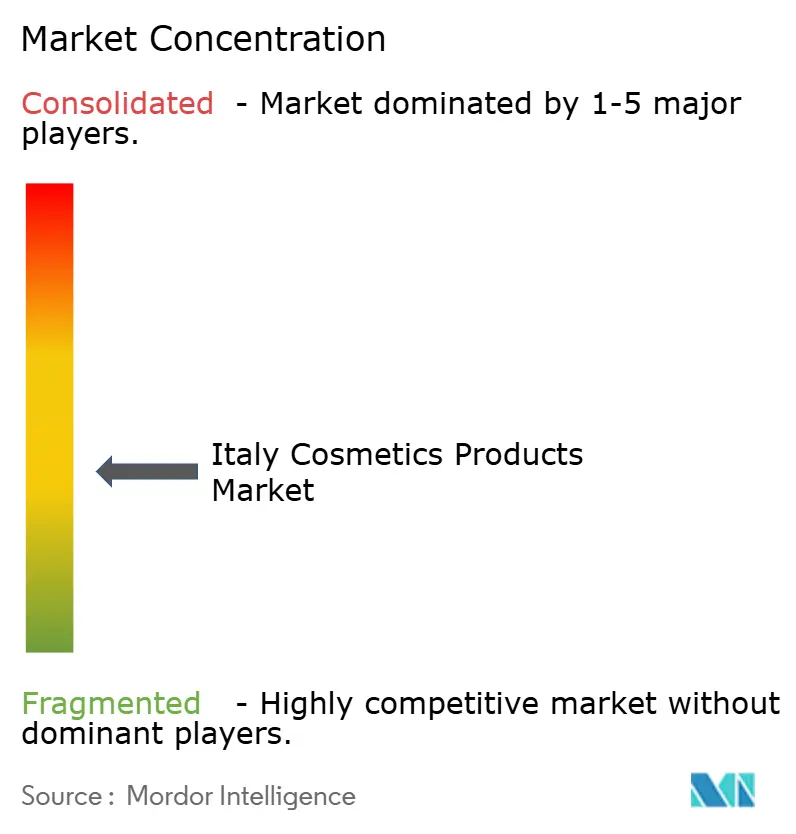

The Italy Cosmetics Products Market is moderately fragmented, featuring a mix of multinational corporations (L'Oréal, Beiersdorf, Unilever, Procter & Gamble), established Italian brands (KIKO Milano, Davines, Caudalie), and dynamic contract manufacturers (Intercos, Ancorotti, Art Cosmetics). This fragmentation presents opportunities in areas such as dermocosmetics, men's grooming, and niche perfumery, where smaller players can establish strong positions through clinical validation, artisanal branding, or collaborations with influencers. Private equity activity is reshaping the competitive landscape, as evidenced by L Catterton's USD 1.5 billion acquisition of KIKO Milano in April 2024 and Givaudan's acquisition of B.Kolor in July 2024. These developments highlight institutional investors' recognition of Italian brands' growth potential and export capabilities.

Technological advancements are driving competitive differentiation. For instance, Intercos Group, despite experiencing a cyberattack in early 2024 that temporarily disrupted IT and production, anticipates 6–8% sales growth in 2024. The company is also expanding its facilities in Poland, Italy, South Korea, China, and India to cater to independent brands that prioritize speed and customization over large-scale production.

Regulatory compliance is emerging as a key competitive factor. Companies with in-house regulatory expertise, such as L'Oréal and Beiersdorf, are better positioned to adapt quickly to new regulations, including Regulation 2024/858's nanomaterial ban and Regulation 2023/1545's expanded allergen list. This capability provides a first-mover advantage in reformulating stock-keeping units (SKUs), giving these companies a competitive edge over smaller players that rely on external consultants.

Italy Cosmetics Products Industry Leaders

Beiersdorf AG

L'Oreal S.A.

Unilever PLC

The Estée Lauder Companies Inc.

Kenvue Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulation-driven reformulation and claims compliance are creating space for Italian brands, contract manufacturers, and testing providers that can compress time-to-compliance and support documentation for safety and substantiation. Two near-term anchors are the expanded EU fragrance-allergen labeling requirements that take effect on July 31, 2026 for new products (and July 31, 2028 for existing stock), and Italy's Legislative Decree 20 February 2026, No. 30, which transposes Directive (EU) 2024/825 on environmental claims with application effective 27 September 2026. Together, these changes raise demand for compliant fragrance strategies, alternative ingredients, packaging redesign, and evidence-backed communication, especially for premium, dermocosmetic, and "clean" positioning.

Digital-first discovery and personalization are also becoming a more central execution point in Italy, supported by investments in AI-enabled skin and trend analytics. Amazon opened its first parapharmacy in Milan on February 13, 2025 with AI skin-diagnostic mirrors and ingredient transparency features, while L'Oreal Italia renewed a three-year partnership with Navla (Datrix) in April 2026 to use generative AI and digital intelligence for search and trend analysis. Separately, sustainability programs with auditable targets can support differentiated offers in professional and retail channels, including Pettenon Cosmetics publishing its fifth sustainability report in May 2026 with a 2026-2028 ESG plan and carbon neutrality across production sites.

Recent Industry Developments

- April 2026: L'Oreal Italia renewed its three-year partnership with Navla (Datrix) to deploy generative AI and digital intelligence for search performance and trend analysis. The renewal reinforces data-driven content optimization and faster product and campaign iteration.

- May 2025: Goop Beauty entered Italy through a one-year exclusive partnership with The Beautyaholic's Shop, a niche local retailer focused on clean beauty. The agreement provided an established route-to-market for a new entrant while reinforcing the role of curated specialty retail in building premium and ingredient-led brands.

- April 2024: L Catterton acquired KIKO Milano for USD 1.5 billion, increasing financial backing for international expansion beyond its domestic base. The transaction underscored continued investor interest in scalable Italian beauty brands and supported broader competitive pressure across mass and accessible premium segments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is counted as the value of cosmetics and make-up products sold in Italy, across common retail routes, covering premium and mass offerings and tracking spending in USD.

Scope exclusions: We do not include upstream cosmetics supply chain value, such as raw materials, packaging, machinery, or contract manufacturing services.

Segmentation Overview

- By Product Type

- Facial Cosemetics

- Eye Cosmetics

- Lip and Nail Make-up Products

- By Category

- Premium Products

- Mass Products

- By Ingredients

- Natural and Organic

- Conventional/Synthetic

- By Distribution Channel

- Specialty Stores

- Supermarkets/Hypermarkets

- Online Retail Stores

- Other Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped set the sizing boundaries and also identified the main demand signals to anchor the model. We referred to public sources such as ISTAT household spending series for Italy, Eurostat trade statistics for relevant product groups, and Italian customs import and export releases where those tables were available.

We also used publications from Italian and European industry bodies and compliance references around labeling requirements, since those help explain shifts in mix and pricing for cosmetics. To translate those signals into a usable sizing model, we reviewed brand and retailer disclosures such as annual reports, investor presentations, and audited filings, then followed with reputable press coverage on channel trends. Where needed, we supplemented with subscribed databases for company financial intelligence, patent scans for active ingredients and formulation trends, and shipment-level import and export checks when public tables were not detailed enough. The desk sources listed above are illustrative only, and many other public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to test what desk research could not fully explain, especially the split between premium and mass, the pace of price increases, and the direction of online and specialty retail in Italy. We spoke with a mix of brand owners, distributors, specialty store contacts, and ingredient and manufacturing experts across Italy, and then we pressure-checked assumptions with sales and category managers who see day-to-day movement.

Inputs from these discussions were used to close gaps, settle conflicting signals, and confirm that the final totals match realistic buying patterns in the main cosmetics and make-up channels.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 19% | |

| Mid tier: 47% | Functional/Unit leaders: 28% | |

| Smaller Players: 19% | Managers: 53% |

Market-Sizing & Forecasting

Sizing started from a top-down demand pool build-up, using national consumption signals and channel weights to reconstruct total spend on cosmetics products in Italy for the base period. Once the first cut was ready, we corroborated it with selective bottom-up checks, mainly sampled brand revenue splits by category, distributor and retailer channel checks, and simple volume times average selling price sanity tests for fast-moving subcategories.

A few inputs that mattered in the model were the premium versus mass mix, online share shifts versus offline, average selling price movement by category, and the pace of new product launches and reformulations (since these change mix). We also checked import dependence for certain product groups because availability and pricing can shift when supply tightens. When a variable was not consistently visible in public data, the gap was handled with interview-led ranges, then narrowed using cross-checks against channel growth and trade flows.

For forecasting, we relied on scenario analysis built around expected price normalization, channel share change, and mix upgrades within skincare and make-up, since those were the variables interviewees could discuss with the most confidence. Each scenario was then converted into a single view after checking that implied per-capita spending changes stayed realistic for Italy.

Data Validation & Update Cycle

Validation was done through repeated checks across unrelated signals, so the final numbers do not depend on one source or one assumption. We compared the model output against observed channel growth narratives, import and export direction, and published company commentary, and then investigated variances that looked too large for one year.

Before sign-off, the analysis is reviewed in steps, with calculations rechecked and assumptions compared against what respondents said in later calls. The report is refreshed annually, and interim updates are made when material events change pricing, channel access, or category demand. Right before delivery, we run a fresh data pass so clients receive the latest updated view.

Mordor Intelligence's Italy Cosmetics Products Market Market Size Measured Against Other Published Estimates

Published market sizes for Italy cosmetics can look far apart, even when they sound like they cover the same topic. The gap usually comes from how each study defines product scope, whether it combines cosmetics with wider beauty and personal care, and how prices and currency timing are treated in the base year.

The benchmark table shows a much smaller total here because, in Mordor Intelligence's model, only cosmetics and make-up product value is counted, while broader beauty and personal care baskets (including items like oral care, deodorants, or bath and shower) are kept outside the scope.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.21 B (2026) | |

| Trade Publisher A | USD 13.21 B (2025) | Uses a wider definition that bundles cosmetics with adjacent beauty and personal care categories, which expands the demand pool beyond cosmetics-only spend. It also reports a different base year, so price and channel mix timing do not line up one-to-one. |

| Industry Association B | USD 13.60 B (2023) | Often presented as a domestic consumption total across many channels and may be reported in local currency before conversion, which can shift the USD value depending on exchange timing. The scope can also include a wider set of beauty categories than cosmetics products alone. |

After aligning the definitions, the spread is easier to understand and does not automatically mean any one number is wrong. Our method stays traceable because each step ties back to clear product coverage, channel weights, and price logic that can be repeated when new data is released.

Key Questions Answered in the Report

How large is the Italy cosmetics products market in 2026?

The Italy cosmetics products market size is USD 2.21 billion in 2026 and is projected to reach USD 2.89 billion by 2031.

Which product type is growing fastest in Italy?

Eye Cosmetics lead growth with a 6.31% CAGR forecast through 2031, outpacing all other categories.

What drives premium cosmetics growth in Italy?

Made-in-Italy heritage, dermatologist-endorsed formulas, and niche fragrances underpin a 6.28% CAGR for premium lines.

How important is e-commerce for Italian cosmetics?

Online channels is expected to grow at a 6.41% CAGR, making digital a critical distribution pillar.

Page last updated on: