Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

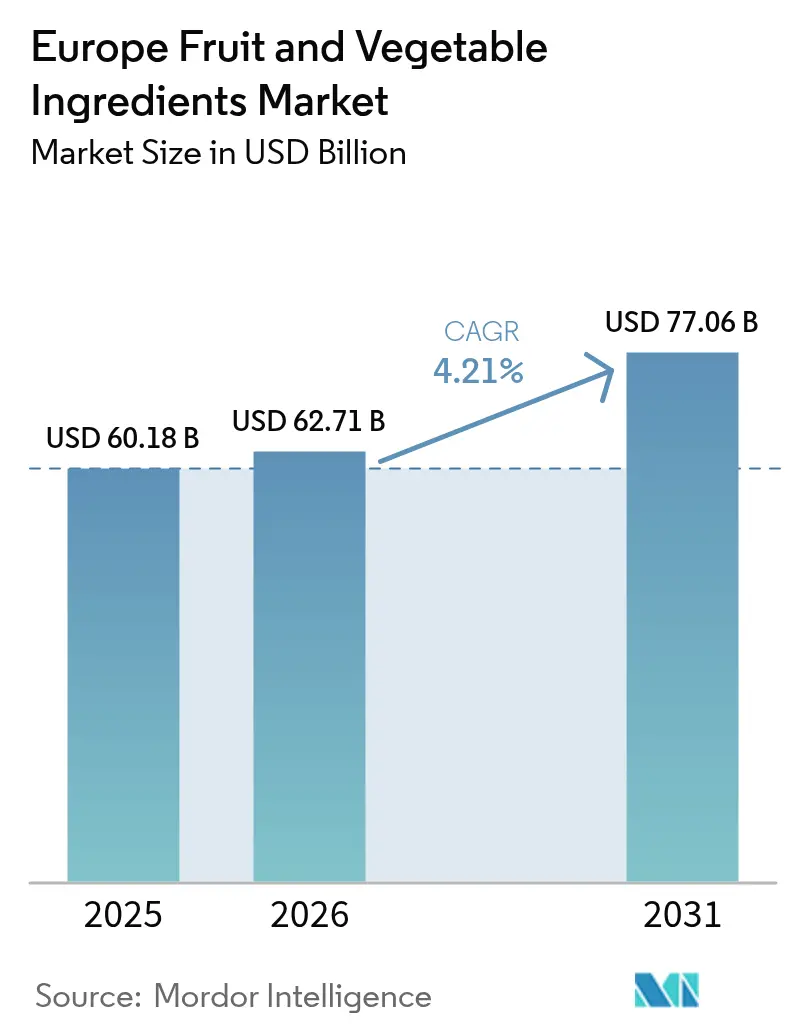

| Base Year Market Size (2025) | USD 60.18 Billion |

| Market Size (2026) | USD 62.71 Billion |

| Market Size (2031) | USD 77.06 Billion |

| Growth Rate (2026 - 2031) | 4.21% CAGR |

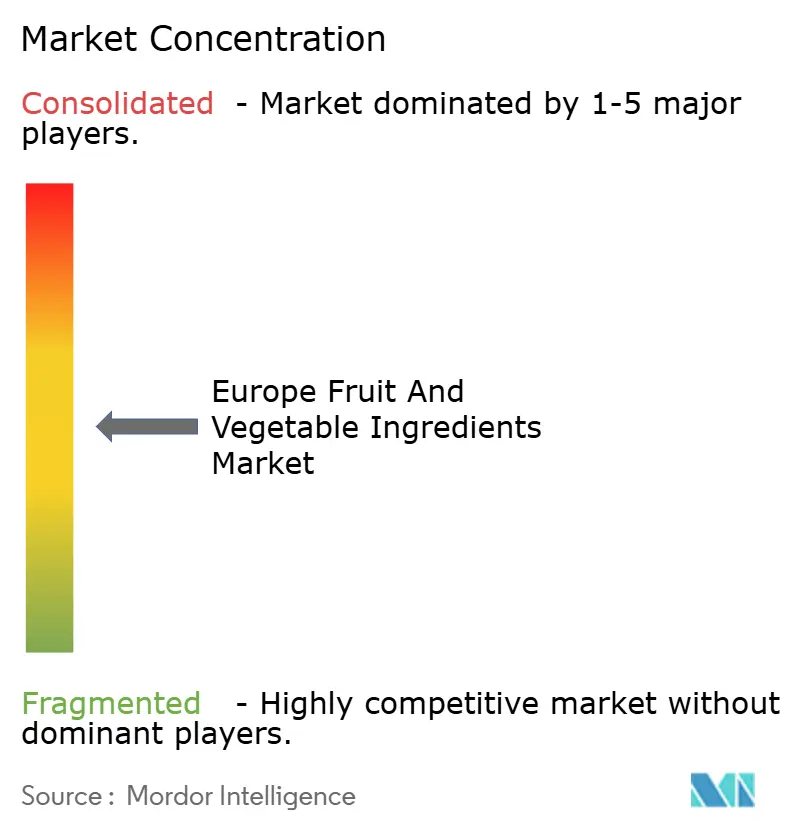

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Fruit And Vegetable Ingredients Market Analysis by Mordor Intelligence

The Europe fruit and vegetable ingredients market size was valued at USD 60.18 billion in 2025 and estimated to grow from USD 62.71 billion in 2026 to reach USD 77.06 billion by 2031, at a CAGR of 4.21% during the forecast period (2026-2031). Demand acceleration pivots on regulatory tightening against synthetic additives, rising clean-label awareness, and technology investments that lengthen shelf life while preserving nutrient density. Reformulation momentum is pronounced across confectionery, bakery, and beverage lines because the European Food Safety Authority’s latest guidance on additives and EU Regulation 1333/2008 discourages the use of titanium dioxide and several azo dyes, prompting brand owners to turn to plant-derived colorants. France’s revised Nutri-Score algorithm, effective March 2025, further penalizes synthetic colorants, pushing retailers to delist non-compliant SKUs. Competitive strategies coalesce around vertical integration, fermentation, and proximity processing, helping suppliers hedge against climate-driven yield volatility and meet traceability mandates. These shifts position the European fruit and vegetable ingredients market as a structural beneficiary of the Farm to Fork strategy, national nutrition plans, and consumer preference for recognizable ingredients.

Key Report Takeaways

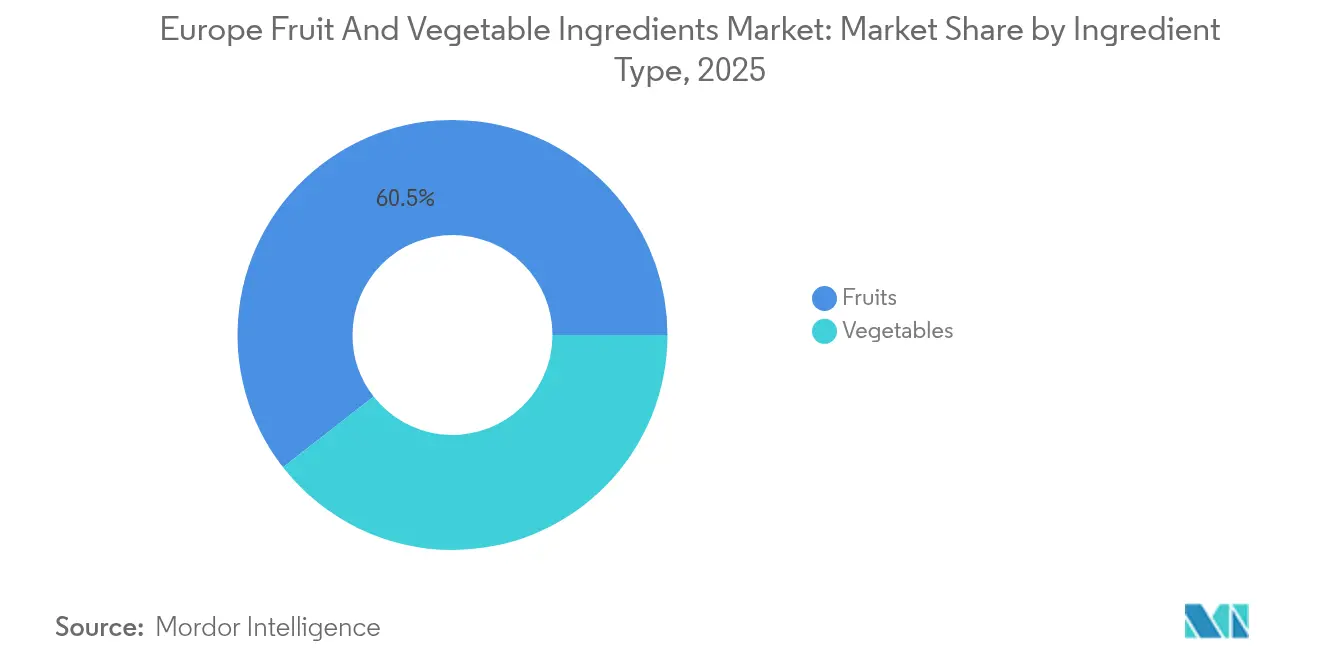

- By ingredient type, fruits led with 60.55% revenue share in 2025; vegetables are projected to expand at a 6.45% CAGR through 2031, the fastest among all ingredient classes.

- By product type, concentrates captured 42.80% of the European fruit and vegetable ingredients market share in 2025, while pastes and purees are forecast to grow at a 5.62% CAGR to 2031.

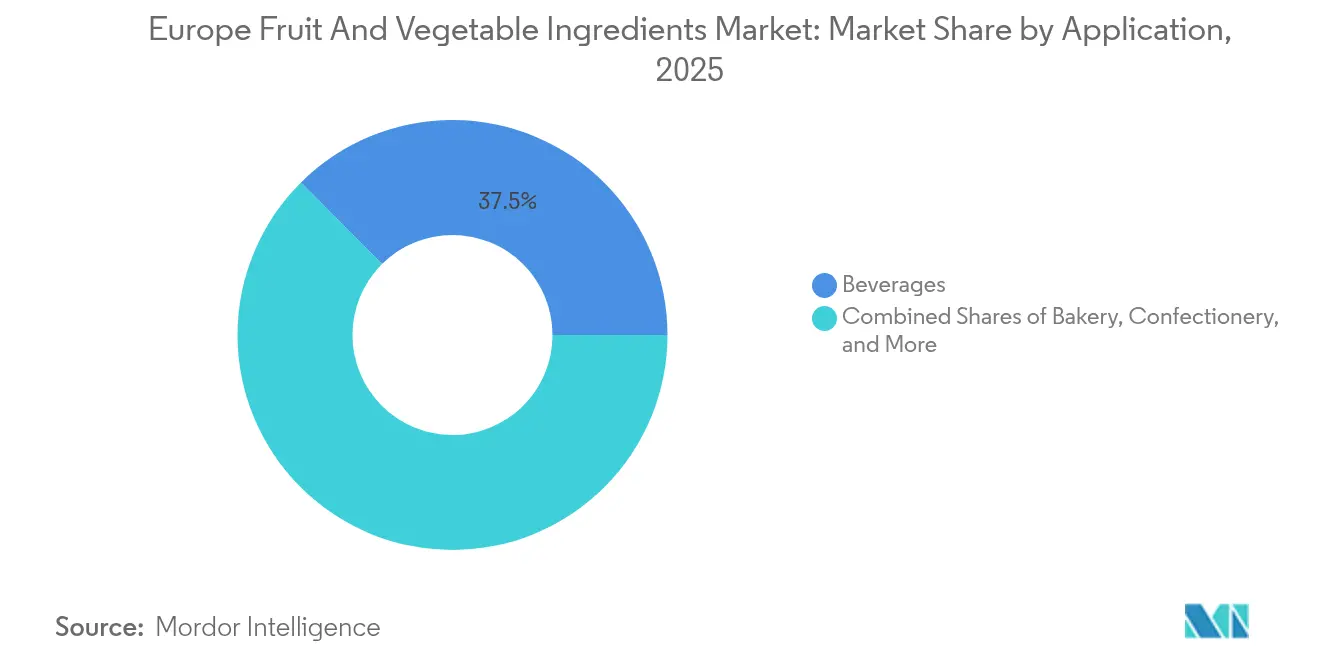

- By application, beverages accounted for 37.45% of the European fruit and vegetable ingredients market in 2025, whereas bakery products are advancing at a 6.22% CAGR through 2031.

- By geography, Germany commanded 31.85% of the European fruit and vegetable ingredients market in 2025; Spain is the fastest-growing geography, registering a 5.58% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Fruit And Vegetable Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean-label and natural color/flavor alternatives | +1.2% | Global, with strongest uptake in Germany, France, UK | Medium term (2-4 years) |

| Rising applications in bakery products | +0.9% | Germany, France, Netherlands, UK | Medium term (2-4 years) |

| Expansion of plant-based dairy & beverage lines in Western Europe | +0.8% | Western Europe (Germany, UK, France, Netherlands) | Short term (≤ 2 years) |

| Government-backed health initiatives | +0.6% | EU-wide, national programs in France, Germany, Spain | Long term (≥ 4 years) |

| Vertical integration efforts by manufacturers securing long-term supplier agreements | +0.5% | Germany, Netherlands, Spain, Italy | Medium term (2-4 years) |

| Growth in fermentation and processing hubs among manufacturers | +0.4% | Germany, France, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Clean-Label and Natural Color/Flavor Alternatives

In 2024, clean-label claims appeared on 42% of new food product launches in the EU, reflecting a growing consumer shift away from artificial additives. This trend is reinforced by stricter regulations targeting synthetic colorants and preservatives. For example, the European Food Safety Authority's 2024 re-evaluation of titanium dioxide (E171) and certain azo dyes has driven reformulations in the confectionery and dairy sectors. As a result, demand for natural alternatives such as anthocyanins from berries, carotenoids from carrots, and chlorophyll from spinach has surged. Additionally, France's updated Nutri-Score algorithm, effective March 2025, will penalize products containing synthetic additives, creating a competitive disadvantage for brands that delay reformulation, as noted by the French Government[1]Source: French Government, “Décret relatif au Nutri-Score,” Légifrance, legifrance.gouv.fr. Although natural color concentrates command a 30-40% price premium over synthetic options, food manufacturers are absorbing these costs to retain their premium shelf positioning. The strategic takeaway is evident: companies that invest in diversified portfolios of fruit and vegetable extracts now are poised to achieve significant margin growth as regulatory pressures increase through 2030.

Rising Applications in Bakery Products

Bakery manufacturers are increasingly incorporating fruit and vegetable ingredients not only in traditional applications but also as functional components to improve fiber content, moisture retention, and shelf stability. The EU's whole-grain labeling thresholds, which require minimum fiber levels for health claims under Regulation (EC) No 1924/2006, have encouraged bakers to include apple fiber, citrus fiber, and beetroot powder in bread and pastry formulations. In July 2024, Ingredion introduced its citrus fibers, FIBERTEX CF 500 and CF 100, aimed at the EMEA bakery segment. These fibers provide water-binding capabilities, enabling bakers to reduce egg and fat usage while preserving crumb structure. This combination of nutritional enhancement and cost efficiency is particularly appealing to industrial bakeries operating with narrow profit margins. In Germany, the artisan bakery sector, which produces approximately 35% of the country's bread, is utilizing vegetable powders to differentiate premium product lines. Carrot and pumpkin variants, in particular, are achieving price premiums of 15-20% over standard offerings. This trend also extends to gluten-free and plant-based bakery segments, where fruit purees are being used as egg substitutes for binding. This approach is reflected in the growing availability of vegan pastries in retail chains across the UK and France during 2024-2025.

Expansion of Plant-Based Dairy and Beverage Lines in Western Europe

In 2024, Western Europe's plant-based dairy and beverage sector transitioned from its niche roots to mainstream prominence. Major brands are now fortifying their products, harnessing fruits and vegetables for enhanced flavor, color, and nutrition. Arla Foods, in 2024, unveiled a plant-based line that cleverly uses fruit concentrates to counteract the beany off-notes of pea and soy proteins, a hurdle that has long limited consumer acceptance. Alpro, in 2024, rolled out its 'Kids' range, infusing vegetable-derived vitamins and natural fruit flavors, positioning it as a direct competitor to dairy milk for children, appealing to parents who value clean labels. Plenish, in 2024, launched a fortified oat milk that combines fruit extracts with added vitamins, ensuring functional benefits while proudly holding an organic certification under EU Regulation 2018/848. The overarching strategy reveals that plant-based beverages are evolving from mere dairy substitutes to functional platforms, emphasizing superior nutrition through fruit and vegetable ingredients. This shift is fueling ingredient demand in Germany, the UK, and the Netherlands. In 2024, these countries witnessed per-capita consumption of plant-based milk exceeding 8 liters annually, propelling consistent growth for fruit concentrates and vegetable extracts projected through 2030.

Government-Backed Health Initiatives

As part of the European Green Deal's Farm to Fork strategy, the European Union targets a 50% reduction in pesticide use and a 20% reduction in fertilizer application by 2030[2]Source: European Commission, “Farm to Fork Strategy,” Publication Office, ec.europa.eu. This initiative is expected to drive higher demand for organic fruits and vegetables. To align with these directives, member states have revised national nutrition programs to encourage food manufacturers to adopt minimally processed, plant-based ingredients. In 2024, France updated its National Nutrition and Health Program (PNNS) 4, recommending a daily consumption of 5 portions of fruits and vegetables. This update has increased institutional demand for ingredient suppliers offering cost-effective solutions for school meals and public catering. Similarly, Germany's Federal Ministry of Food and Agriculture launched a USD 218 million initiative in 2024 to support organic farming and processing infrastructure. This initiative provides direct subsidies to facilities such as freeze-drying and spray-drying units, which convert surplus produce into shelf-stable ingredients. These policy measures are reshaping supply chains, prompting processors to align their capital investments with government priorities to access subsidies and preferential procurement contracts. The long-term outcome is a structural transition toward regionally sourced, minimally processed ingredients that fulfill both sustainability and health objectives.

Restraints Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EU food safety and labeling regulations | -0.7% | EU-wide, particularly Germany, France, Netherlands | Medium term (2-4 years) |

| Short shelf life and perishability of fresh ingredients | -0.5% | All European markets, acute in Southern Europe | Short term (≤ 2 years) |

| Climate change and water scarcity in key growing regions | -0.6% | Southern Europe (Spain, Italy, Greece), spillover to France | Long term (≥ 4 years) |

| Price competition from synthetic alternatives | -0.4% | Price-sensitive segments across EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent EU Food Safety and Labeling Regulations

The European Union's Novel Food Regulation (EU) 2015/2283 mandates stringent pre-market approvals for fruit and vegetable extracts processed via unconventional methods. This regulation extends approval timelines to 18-24 months and inflates compliance costs by an estimated USD 530,000 to USD 1.06 million per dossier, as noted by the European Commission. Such regulatory challenges disproportionately burden small and medium-sized processors, who often lack the technical and financial means to navigate the European Food Safety Authority's (EFSA) scientific evaluation. Under Regulation (EU) No 1169/2011, labeling mandates require comprehensive ingredient disclosures, encompassing processing aids and extraction solvents. This transparency can lead to consumer skepticism, even when the disclosed compounds are naturally derived, as highlighted by the European Commission. A strategic dilemma emerges: regulatory compliance imposes a first-mover disadvantage. Early adopters shoulder the costs of novel food approvals, while their competitors benefit from these established precedents without incurring the same expenses. Germany and France, in particular, adopt stringent interpretations of EU directives. They conduct post-market surveillance, with the authority to recall products if labeling strays from approved specifications. Such regulatory rigor not only decelerates innovation cycles but also deters investments in novel extraction technologies, limiting the market's agility in adapting to shifting consumer preferences.

Short Shelf Life and Perishability of Fresh Ingredients

Fresh fruits and vegetables require an uninterrupted cold-chain logistics system from harvest to processing. This necessity increases landed costs by 15-20% compared to synthetic alternatives and introduces vulnerabilities to the supply chain. Temperature fluctuations during transport can cause enzymatic browning and microbial spoilage, rendering batches unsuitable for food-grade applications and forcing processors to bear financial losses. While Europe's cold-chain infrastructure is advanced, it faces capacity limitations during peak harvest seasons. This issue is particularly pronounced in Southern Europe, where summer temperatures frequently exceed 35°C, straining refrigerated transport networks, as highlighted by the European Environment Agency[3]Source: European Environment Agency, “Climate Change Adaptation in Europe,” eea.europa.eu. To address perishability, processors use techniques such as freeze-drying, spray-drying, and concentration. However, these thermal processes compromise heat-sensitive vitamins and volatile flavor compounds, reducing the nutritional and sensory qualities that justify premium pricing. The strategic takeaway for ingredient suppliers is the need to invest in rapid processing infrastructure near growing regions. Although this approach is capital-intensive, it favors larger, vertically integrated players over smaller processors. Spain and Italy are emerging as key processing hubs by situating drying and concentration facilities within 50 kilometers of major production zones, minimizing transit time and preserving ingredient quality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Vegetables Accelerate on Color Innovation

In 2025, fruits accounted for 60.55% of Europe's fruit and vegetable ingredients market, driven by their strong presence in beverages, confectionery, and dairy due to their flavor and sweetness. Vegetables, with a smaller share, are projected to grow at a 6.45% CAGR through 2031, as their use in natural coloring and fortification rises. Beetroot extract is preferred for its stable red coloring in plant-based products, outperforming berry anthocyanins. Carrot concentrate and green powders like spinach and kale are gaining traction in fortified foods and health-focused products.

Vegetables are transitioning from niche ingredients to mainstream formulation tools, valued for their dual role as colorants and nutrient sources. Fruits remain dominant in taste-driven applications like juices and confections, but their growth is slowing as these markets mature. Vegetables are capturing demand in emerging segments like plant-based proteins and functional snacks, aligning with clean-label trends. Processors expanding vegetable extraction capacity now will benefit from rising plant-based food consumption, particularly in Germany and the Netherlands.

By Product Type: Pastes and Purees Gain on Texture Demands

In 2025, concentrates held 42.80% of the market, valued for their logistical efficiency and extended shelf life, which lower transportation costs and reduce spoilage risks. Pastes and purees are growing at a 5.62% CAGR through 2031, driven by their ability to replicate authentic fruit and vegetable textures in premium applications. Greek-style yogurts and smoothie bowls increasingly use fruit purees for enhanced viscosity and visual appeal, commanding 20-30% price premiums over concentrate-based alternatives. Pieces and powders cater to niche applications like granola bars, instant soups, and dry beverage mixes, where reconstitution properties and particle size are critical. Juices, though mature, are seeing renewed interest in cold-pressed and not-from-concentrate formats that preserve flavor compounds and heat-sensitive vitamins.

The competitive landscape is shifting towards formats that balance convenience with sensory authenticity. Concentrates remain dominant in cost-sensitive segments like private-label beverages and industrial bakeries due to their standardized flavor profiles and consistent performance. Pastes and purees are gaining traction in premium markets, where consumers prioritize whole-fruit content and scrutinize ingredient lists. Processors must diversify product portfolios, as no single format meets all application needs. Germany's beverage sector, consuming 35% of the country's fruit and vegetable ingredients, is fragmented, with premium brands favoring purees and mass-market players relying on concentrates.

By Application: Bakery Outpaces Beverages on Fiber Fortification

In 2025, beverages accounted for 37.45% of application demand, driven by their reliance on fruit concentrates and vegetable juices for flavor and color. Bakery products are growing at a 6.22% CAGR through 2031, fueled by fiber fortification mandates and clean-label reformulation. EU regulations under (EC) No 1924/2006 require minimum fiber levels for "source of fiber" and "high fiber" claims, prompting bakers to use apple fiber, citrus fiber, and vegetable powders. Ingredion's FIBERTEX CF 500 and CF 100, launched in July 2024, address this demand by reducing fat and egg usage while maintaining crumb structure. Confectionery and dairy applications are mature, with growth slowing as premium segment penetration exceeds 70%.

Soups, sauces, and ready-to-eat products are gaining traction as manufacturers adopt clean-label formulations, replacing synthetic thickeners with vegetable purees and fruit concentrates. Bakery's strong performance reflects shifting consumer priorities, with fiber and whole-grain claims driving purchases in Northern Europe. Beverages face saturation in core categories like fruit juices, pushing innovation into functional hydration and plant-based milk alternatives. Processors focusing on bakery-grade fibers and purees can capture higher margins, as these products command 15-20% price premiums over beverage concentrates. Germany's artisan bakery sector, producing 35% of the country's bread, uses vegetable powders like carrot and pumpkin to differentiate premium lines, achieving similar price premiums.

Geography Analysis

In 2025, Germany holds a 31.85% share of Europe's food processing market, reaffirming its position as the continent's leading hub. The country features a concentrated industrial bakery and beverage sector, emphasizing clean-label formulations. Germany's strict interpretation of EU food safety directives creates a high-compliance environment that benefits established ingredient suppliers with robust quality management systems certified to ISO 22000 and FSSC 22000 standards. Germany's artisan bakery sector, which produces approximately 35% of the nation's bread, has adopted fruit and vegetable powders to differentiate premium product lines. Carrot and pumpkin variants, in particular, command a 15-20% price premium over standard offerings. In the UK, discount retailers dominate the grocery market with a 40-45% share, applying downward pricing pressure that limits the adoption of premium natural ingredients in private-label categories.

France's updated Nutri-Score algorithm, effective March 2025, penalizes synthetic additives, creating a regulatory advantage for fruit and vegetable extracts in confectionery and dairy applications, as noted by the French Government. Italy's processing sector is concentrated in the Po River basin, where tomato paste and citrus concentrate production face yield fluctuations due to water scarcity. This challenge is driving processors to diversify sourcing, increasingly relying on Spain and Greece, as highlighted by the European Environment Agency. Spain is experiencing rapid growth, with a 5.58% CAGR projected through 2031. This growth is driven by investments in freeze-drying and spray-drying infrastructure, which extend shelf life while preserving nutritional value. Spain's proximity to North African growing regions and competitive labor costs position it as a key processing hub for citrus, stone fruits, and tomatoes destined for Northern European markets.

The Netherlands leverages its advanced logistics infrastructure and biotech expertise to attract fermentation investments. Companies like Symrise and Ingredion have established R&D facilities to develop nature-identical flavor molecules from fruit metabolites, as reported by Symrise. A critical insight is the division of geographic competitiveness: Southern Europe excels in raw material sourcing and thermal processing, while Northern Europe leads in fermentation, formulation expertise, and proximity to end-use markets. Processors adopting a dual-site strategy, conducting primary processing in Spain or Italy and secondary formulation in Germany or the Netherlands, can optimize costs while maintaining flexibility to meet customer requirements. The "Rest of Europe" category, which includes Eastern European countries such as Poland and Romania, represents a growing market. Rising disposable incomes and regulatory harmonization driven by EU accession are expanding the demand for premium natural ingredients.

Competitive Landscape

The European fruit and vegetable ingredients market exhibits moderate fragmentation, indicating that multinational ingredient houses coexist with regional specialists and vertically integrated processors. Competitive strategies emphasize vertical integration, fermentation technology, and geographic diversification to mitigate raw material volatility and regulatory complexity. Tate & Lyle's USD 1.8 billion acquisition of CP Kelco in June 2024, completed in November 2024, exemplifies the consolidation wave, as the deal provides direct access to citrus peel and apple pomace from contracted orchards in Spain and Italy, ensuring consistent pectin and fiber feedstock Reuters. Symrise's investment in Cellibre's precision fermentation platform in October 2025 signals a strategic pivot toward bioprocessing routes that bypass agricultural constraints, producing nature-identical flavor molecules from fruit metabolites with cost parity to traditional extraction.

White-space opportunities exist in vegetable-derived colorants for plant-based proteins, freeze-dried fruit pieces for premium snacking, and fermentation-derived compounds that eliminate pesticide residues while maintaining organic certification. Emerging disruptors are leveraging fermentation and enzyme technology to democratize access to premium ingredients, challenging incumbents that rely on agricultural sourcing. Ingredion's partnership with Cosaic, announced in November 2025, focuses on fermentation-derived ingredients for plant-based applications, targeting the EMEA market with scalable production capacity Ingredion.

The strategic implication is that technology adoption will determine competitive positioning through 2030, as processors that integrate fermentation capacity by 2027 will gain structural cost advantages over traditional extraction methods. Market leaders are also pursuing geographic expansion into Eastern Europe, where EU accession-driven regulatory harmonization and rising disposable incomes are expanding addressable demand for premium natural ingredients. The competitive landscape is likely to consolidate further, as regulatory compliance costs and capital requirements for fermentation infrastructure favor scale players, yet niche specialists with proprietary extraction methods or exclusive grower contracts will retain defensible positions in premium segments.

Europe Fruit And Vegetable Ingredients Industry Leaders

Archer Daniels Midland Company

Döhler Group SE

Südzucker AG

Kerry Group

Symrise AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Abaca Fruit Purees launched premium fruit purées in the United Kingdom. Every bottle contains a 100% fruit purée base and is designed for drinks of all kinds, alcoholic and non-alcoholic.

- February 2024: Frulact Group acquired International Flavors and Fragrances Inc.'s fruit preparation business, which produces fruit, vegetable, herb, and meat solutions for the food, beverage, and pet food markets, particularly in Western Europe, the Nordics, and North Africa.

- February 2024: GNT Group launched plant-based Exberry brown concentrates. The new Shade Autumn Brown (carrot and caramelised sugar syrup) and Shade Golden Brown (apple and caramelised sugar syrup) provided clear reddish-brown and caramel hues for low-pH soft drinks, including colas, energy drinks, and iced lattes.

Europe Fruit And Vegetable Ingredients Market Report Scope

Fruit and vegetable ingredients are suitable for various food and beverage applications, helping to increase the appeal of food items. The European Fruit and Vegetable Ingredient Market is segmented by ingredient type, product type, application, and geography. By ingredient type, the market is segmented into fruits and vegetables. By product type, the market is segmented into concentrates, pastes and purees, pieces and powders, and juices. By application, the market is segmented into beverages, confectionery products, bakery products, soups and sauces, dairy products, and RTE products. Based on geography, the market is segmented into Germany, the United Kingdom, France, Russia, Italy, Spain, and the Rest of Europe. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Ingredient Type (Value)

| Fruits |

| Vegetables |

By Product Type (Value)

| Concentrates |

| Pastes and Purees |

| Pieces and Powders |

| Juices |

By Application

| Beverages |

| Confectionery Products |

| Bakery Products |

| Soups and Sauces |

| Dairy Products |

| RTE Products |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Rest of Europe |

| By Ingredient Type (Value) | Fruits |

| Vegetables | |

| By Product Type (Value) | Concentrates |

| Pastes and Purees | |

| Pieces and Powders | |

| Juices | |

| By Application | Beverages |

| Confectionery Products | |

| Bakery Products | |

| Soups and Sauces | |

| Dairy Products | |

| RTE Products | |

| By Geography | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe fruit and vegetable ingredients market in 2026?

It is valued at USD 62.71 billion in 2026 and is projected to reach USD 77.06 billion by 2031 at a 4.21% CAGR.

Which ingredient type is expanding fastest?

Vegetable-derived ingredients grow at a 6.45% CAGR thanks to their dual role as colorants and nutrient fortifiers.

What product format is gaining popularity in premium applications?

Pastes and purees are rising at a 5.62% CAGR because they deliver authentic mouthfeel in yogurts and smoothies.

Which country shows the highest market share?

Germany holds 31.85% of regional value due to its robust bakery and beverage industries.

Page last updated on: