Vegetable Concentrates Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

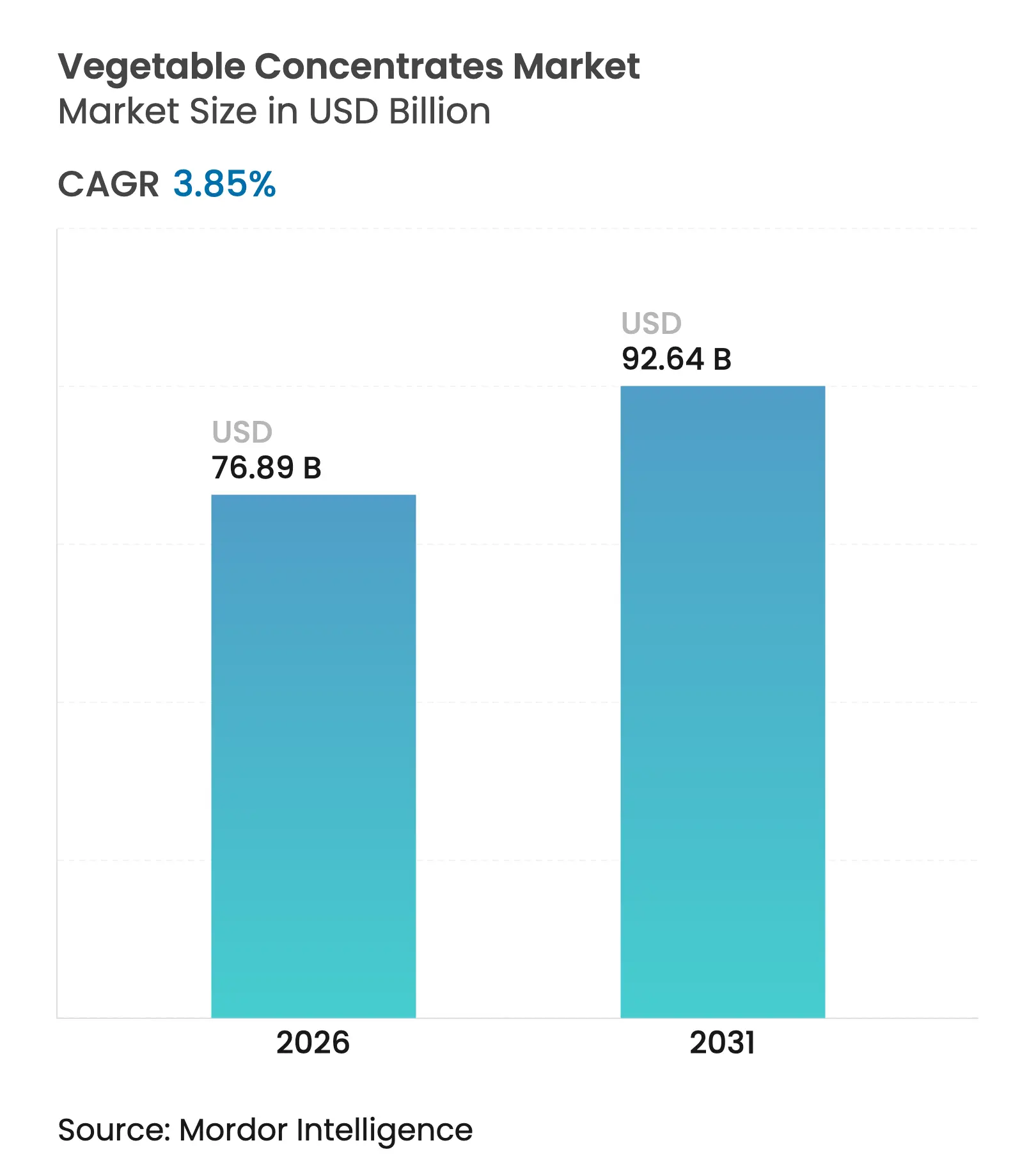

| Market Size (2026) | USD 76.89 Billion |

| Market Size (2031) | USD 92.64 Billion |

| Growth Rate (2026 - 2031) | 3.85 % CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Vegetable Concentrates Market Analysis by Mordor Intelligence

The vegetable concentrates market size is expected to grow from USD 74.04 billion in 2025 to USD 76.89 billion in 2026 and is forecast to reach USD 92.64 billion by 2031 at 3.85% CAGR over 2026-2031. This growth reflects a consistent shift from synthetic additives to botanical ingredients. Regulatory scrutiny of artificial colorants by organizations such as the European Food Safety Authority (EFSA) and the United States Food and Drug Administration (FDA) has accelerated reformulation cycles, leading beverage and confectionery brands to increasingly adopt vegetable concentrates as natural pigments and nutrient carriers. Advancements in processing technologies, including pulsed electric field extraction to preserve flavor volatiles and spray drying to retain anthocyanins, have elevated vegetable concentrates from cost-effective extenders to premium functional components. Consumer preference for clean-label products, as highlighted by Kerry Group’s 2024 survey, continues to drive demand for carotene-rich carrot and nitrate-rich beetroot concentrates, particularly in functional beverages. Additionally, the market is benefiting from the rising adoption of plant-based proteins. Pea-derived concentrates, in particular, are gaining traction due to their ability to meet both nutritional and sensory requirements.

Key Report Takeaways

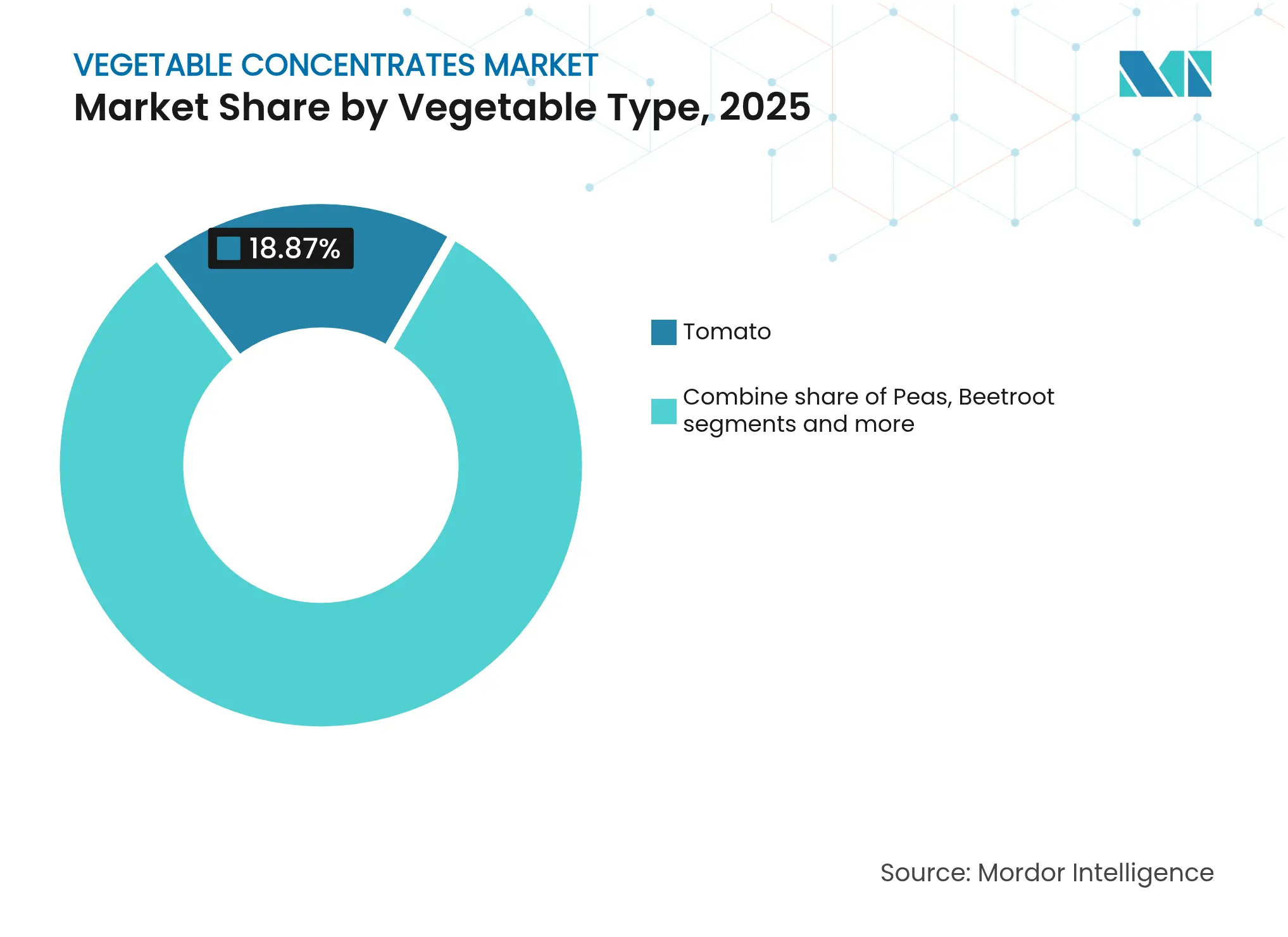

- By vegetable type, tomatoes dominated with 18.87% of vegetable concentrates market share in 2025, while peas are forecast to register a 4.68% CAGR through 2031.

- By category, paste and puree formats accounted for 85.62% of the vegetable concentrates market size in 2025, whereas pieces and powder are projected to expand at a 4.95% CAGR.

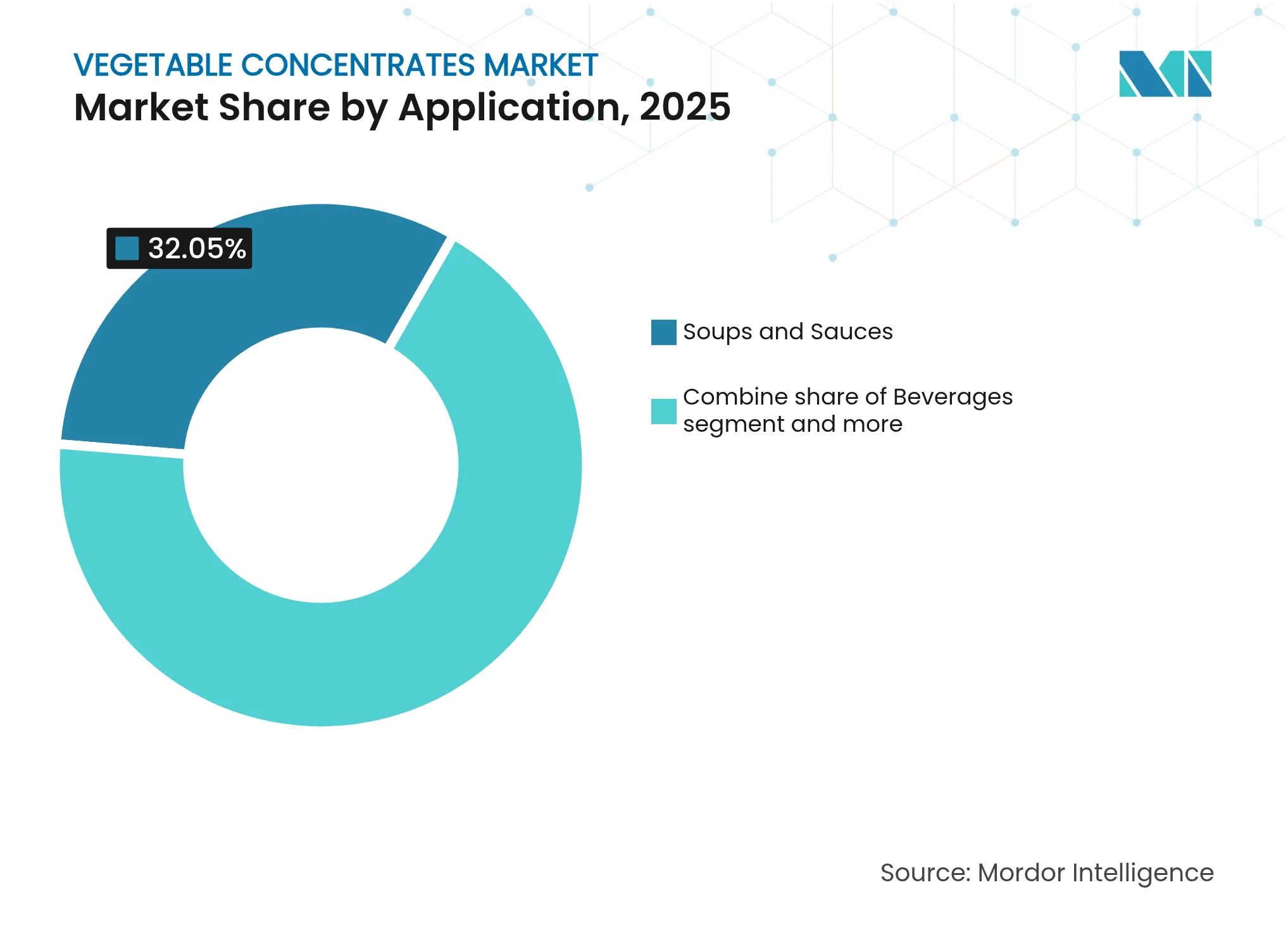

- By application, soups and sauces led with 32.05% of 2025 spending, but beverages are advancing at a 4.81% CAGR to 2031.

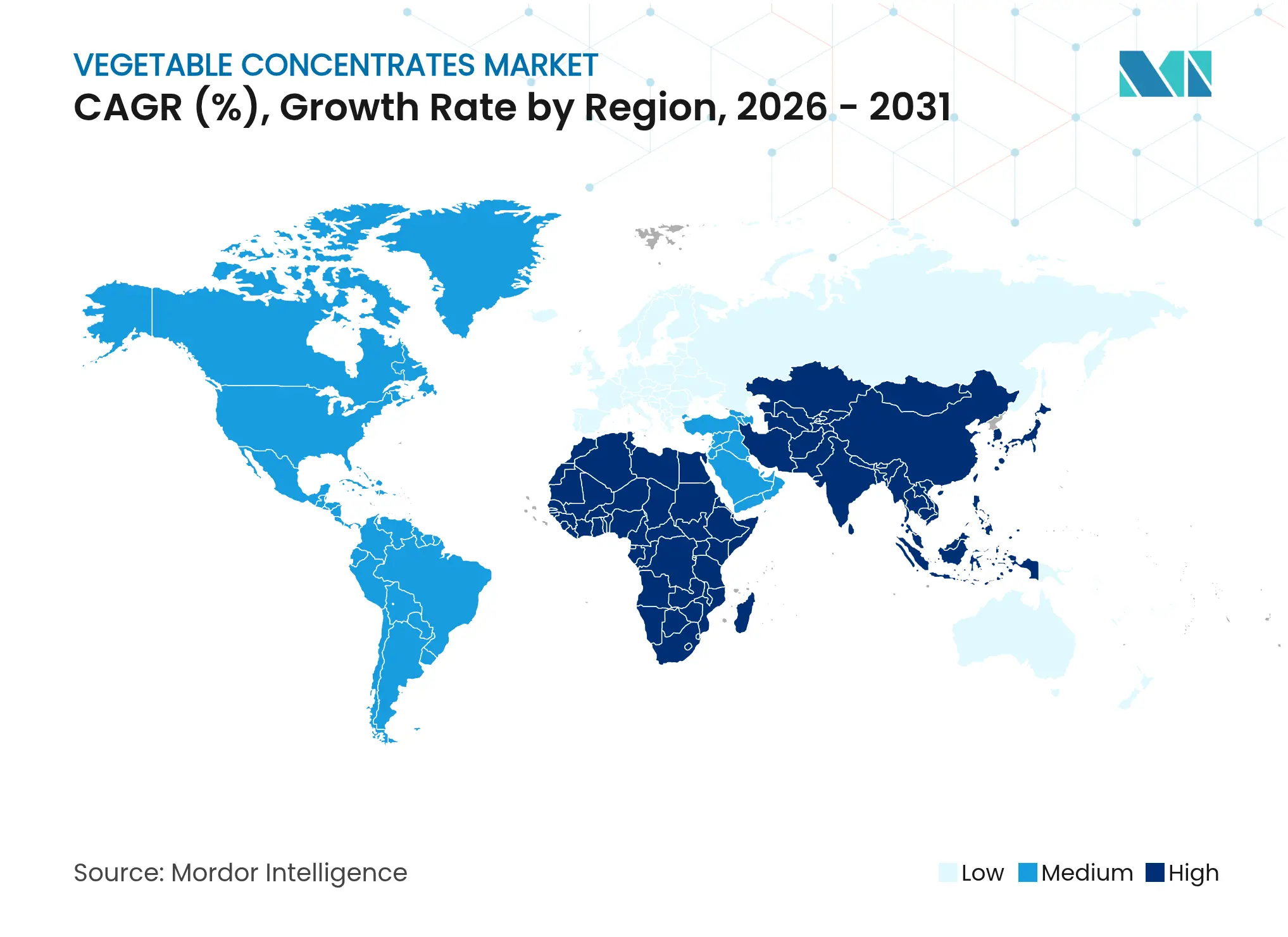

- By geography, Europe held 31.62% of 2025 value, yet Asia-Pacific is poised for the fastest 5.25% CAGR over the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vegetable Concentrates Market Trends and Insights

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising health awareness increases use of vegetable concentrates in nutrient-enriched foods and beverages Rising health awareness increases use of vegetable concentrates in nutrient-enriched foods and beverages | +0.8% | Global, with stronger uptake in North America and Western Europe | Medium term (2-4 years) | (~)% Impact on CAGR Forecast:+0.8% | Geographic Relevance:Global, with stronger uptake in North America and Western Europe | Impact Timeline:Medium term (2-4 years) |

Growing clean-label demand boosts vegetable concentrates as natural alternatives to artificial additives Growing clean-label demand boosts vegetable concentrates as natural alternatives to artificial additives | +1.0% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) | |||

Expansion of plant-based foods drives demand for vegetable concentrates for natural color, flavor, and nutrition Expansion of plant-based foods drives demand for vegetable concentrates for natural color, flavor, and nutrition | +0.9% | Global, led by North America and Europe, expanding into Asia-Pacific | Medium term (2-4 years) | |||

Increasing consumption of soups and ready meals supports use of vegetable concentrates for taste consistency and convenience Increasing consumption of soups and ready meals supports use of vegetable concentrates for taste consistency and convenience | +0.6% | Europe, North America, urban Asia-Pacific markets | Short term (≤ 2 years) | |||

Growth of functional beverages encourages use of vegetable concentrates for immunity and digestive health positioning Growth of functional beverages encourages use of vegetable concentrates for immunity and digestive health positioning | +0.5% | North America, Asia-Pacific (China, India), Europe | Medium term (2-4 years) | |||

Advancements in concentration technologies improve nutrient, color, and flavor retention Advancements in concentration technologies improve nutrient, color, and flavor retention | +0.4% | Global, with early adoption in Europe and North America | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising health awareness increases the use of vegetable concentrates in nutrient-enriched foods and beverages

Consumers are increasingly examining ingredient labels for micronutrient content, prompting manufacturers to fortify products with vegetable concentrates that provide vitamins, minerals, and phytonutrients without relying on synthetic additives. According to a 2024 survey by Kerry Group, 51% of global consumers actively seek clean-label products, and 56% are willing to pay a premium for natural flavors over artificial ones. This trend has driven the adoption of carrot and beetroot concentrates in functional beverages, as their beta-carotene and nitrate content support immunity and cardiovascular health claims. The use of pulsed electric field extraction, a method that preserves heat-sensitive compounds, has enabled concentrate suppliers to meet the nutritional standards required for on-pack health claims in markets regulated by the European Food Safety Authority (EFSA) and the United States Food and Drug Administration (FDA). This shift is particularly evident in children's snacks and sports nutrition products, where vegetable concentrates are replacing synthetic colorants while contributing to daily vegetable intake goals. As regulatory bodies impose stricter limits on artificial additives, the growing focus on health awareness is expected to sustain demand growth through 2028, particularly in North America and Western Europe, where label transparency significantly influences purchasing decisions.

Growing clean-label demand boosts vegetable concentrates as natural alternatives to artificial additives

The clean-label movement has significantly influenced ingredient sourcing strategies, with vegetable concentrates becoming preferred substitutes for synthetic colorants, flavor enhancers, and preservatives. European Union regulations, particularly the Novel Foods Regulation (EU) 2015/2283, have limited the use of certain artificial additives, prompting manufacturers to reformulate with plant-based alternatives [1]Source: European Union, “Regulation (EU) 2015/2283 of The European Parliament and of The Council,” eur-lex.europa.eu. For example, tomato concentrate is now used as a natural umami enhancer in soups and sauces, reducing dependence on monosodium glutamate, while beetroot concentrate provides vibrant red hues in confectionery without requiring an E-number declaration. Döhler GmbH reported in 2024 that demand for its natural color portfolio, primarily based on vegetable concentrates, increased by 18% year-over-year as confectionery brands reformulated to meet retailer clean-label requirements. This trend is not confined to Europe; in North America, heightened FDA scrutiny of synthetic dyes has led bakery and beverage producers to adopt carrot and pumpkin concentrates for yellow and orange coloring [2]Source: United States Food & Drug Administration, “How to Cut Food Waste and Maintain Food Safety,” fda.gov.

Expansion of plant-based foods drives demand for vegetable concentrates for natural color, flavor, and nutrition

The rapid growth of the plant-based food market has driven a corresponding increase in demand for vegetable concentrates that enhance both sensory appeal and nutritional value. Plant-based meat analogs, projected to reach significant market size in 2024, utilize beetroot and tomato concentrates to mimic the appearance of animal proteins while contributing nutrients such as iron and lycopene. Pea concentrates have become particularly important due to their neutral flavor and high protein content, often exceeding 80 percent on a dry-weight basis. These attributes enable formulators to enhance dairy alternatives and protein bars without compromising taste. In 2024, Ingredion Incorporated expanded its pea protein production capacity by 30 percent, responding to growing demand from plant-based beverage manufacturers seeking clean-label binding agents. Beyond meat and dairy substitutes, vegetable concentrates are increasingly used in plant-forward snacks and ready meals. They provide umami flavor and natural sweetness, reducing the need for added sugars and sodium. The synergy between plant-based product innovation and the adoption of vegetable concentrates is anticipated to contribute 0.9 percentage points to the market's compound annual growth rate (CAGR). Asia-Pacific is expected to emerge as a high-growth region, driven by the rising acceptance of flexitarian diets in urban areas of China and India.

Increasing consumption of soups and ready meals supports the use of vegetable concentrates for taste consistency and convenience

The global trend toward convenience-focused eating has transformed vegetable concentrates from cost-saving components into essential ingredients that ensure consistency across batches and extend shelf life. Ready meals, which accounted for significant global sales in 2024, rely on tomato and carrot concentrates to provide standardized flavor profiles during production, minimizing the variability associated with fresh vegetable sourcing. Morning Star Company, the largest tomato processor in the United States, noted in its 2024 annual review that concentrate sales to soup and sauce manufacturers increased by 12%, driven by food service operators seeking ingredients with longer shelf life and stable pricing. Technologies such as freeze-drying and spray-drying have further enhanced the value of concentrates by preserving volatile aromatic compounds that fresh vegetables often lose during transport and storage. In Europe, where ready-meal penetration exceeds 60% in urban households, vegetable concentrates help manufacturers meet clean-label requirements while maintaining the flavor intensity consumers associate with restaurant-quality meals.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Preference for fresh vegetables limits demand for processed concentrates Preference for fresh vegetables limits demand for processed concentrates | -0.4% | Global, particularly in affluent urban markets with strong farm-to-table movements | Short term (≤ 2 years) | (~)% Impact on CAGR Forecast:-0.4% | Geographic Relevance:Global, particularly in affluent urban markets with strong farm-to-table movements | Impact Timeline:Short term (≤ 2 years) |

Fresh, frozen, and chilled vegetables compete with processed options Fresh, frozen, and chilled vegetables compete with processed options | -0.3% | North America, Europe, developed Asia-Pacific markets | Medium term (2-4 years) | |||

Flavor authenticity and freshness decline after processing or storage Flavor authenticity and freshness decline after processing or storage | -0.2% | Global, with heightened sensitivity in premium segments | Medium term (2-4 years) | |||

Color and nutrient degradation during processing and storage can reduce functional and visual appeal Color and nutrient degradation during processing and storage can reduce functional and visual appeal | -0.2% | Global, affecting products with extended shelf-life requirements | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Preference for fresh vegetables limits demand for processed concentrates

A group of health-conscious consumers continues to associate fresh vegetables with superior nutrition and taste, creating challenges for the adoption of concentrates in premium product categories. The farm-to-table movement, particularly prominent in urban centers across North America and Europe, has reinforced the perception that processing reduces phytonutrient content and sensory quality[3]Source: U.S. Department of Agriculture, “Baseline Projections,” usda.gov. Although modern concentration techniques retain 85 to 90 percent of water-soluble vitamins, consumer surveys indicate that 42 percent of respondents still believe fresh vegetables are nutritionally superior, regardless of the processing method. This perception gap has constrained the penetration of concentrates in high-margin categories such as cold-pressed juices and premium soups, where brands emphasize "fresh" claims as key differentiators. The restraint is particularly pronounced in markets with strong local agricultural production. For example, regions like California and the Netherlands have experienced slower adoption of concentrates in retail channels, as consumers prioritize seasonal and locally sourced produce. While ingredient suppliers have launched education campaigns to highlight the nutrient retention capabilities of advanced processing methods, the preference for fresh produce is expected to reduce the market's compound annual growth rate (CAGR) by 0.4 percentage points. This impact is most evident among affluent demographics, where price sensitivity is low, and the provenance of products is highly valued.

Fresh, frozen, and chilled vegetables compete with processed options

The availability of high-quality frozen and chilled vegetables has increased competition, particularly in food service and industrial applications where cost efficiency and convenience are critical. In the United States, frozen vegetable sales in 2024 are expected to benefit from advancements in flash-freezing technologies, which preserve texture and nutrients at levels comparable to concentrates but at lower per-unit costs for bulk buyers. Major food service operators, including suppliers to quick-service restaurants, have increasingly chosen frozen diced tomatoes and carrot slices over concentrates when recipe formats permit. This preference is driven by superior mouthfeel and reduced complexity in reconstitution. In Europe, the chilled vegetable segment has gained market share in ready-meal production, supported by short supply chains and robust cold-chain infrastructure. Manufacturers in this segment prioritize clean-label appeal and the visual authenticity provided by whole or minimally processed vegetables. This competitive dynamic is particularly evident in applications such as stir-fry kits and salad bowls, where vegetable concentrates offer limited functional advantages compared to frozen or chilled alternatives.

Segment Analysis

By Vegetable Type: Peas Ascend as Protein-Driven Demand Reshapes Portfolio Mix

Peas are projected to grow at a rate of 4.68% from 2026 to 2031, surpassing all other vegetable types as plant-based protein formulators prioritize ingredients that offer functional benefits without altering flavor profiles. Tomato concentrates accounted for 18.87% of 2025 revenue, driven by their widespread use in soups, sauces, and ready meals, where their umami depth and natural acidity are critical. However, the rising demand for pea concentrates highlights a broader market shift. Manufacturers of dairy alternatives and meat analogs are increasingly utilizing pea protein isolates and concentrates due to their neutral taste, high lysine content, and allergen-free characteristics. Ingredion's 2024 capacity expansion in pea processing, which added 15,000 metric tons of annual output, reflects this strategic focus on the segment.

Carrot concentrates serve dual purposes as natural colorants and sources of beta-carotene, with applications in beverages and confectionery, particularly as synthetic dyes face growing regulatory scrutiny. Beetroot concentrates have gained popularity in sports nutrition products due to their nitrate content, which supports endurance-related claims. Meanwhile, pumpkin concentrates remain a niche product, primarily used in seasonal bakery items and baby food formulations. Regulatory developments are influencing vegetable-type preferences; the European Food Safety Authority's (EFSA) approval of specific health claims for vegetable-derived nutrients has accelerated the adoption of carrot and beetroot concentrates in products targeting cardiovascular and immune health.

Note: Segment shares of all individual segments available upon report purchase

By Category: Pieces and Powder Gain as Snack and Supplement Brands Demand Shelf-Stable Formats

The pieces and powder formats market is projected to grow at a rate of 4.95% from 2026 to 2031, outpacing the growth of paste and purees, which are expected to account for an 85.62% market share in 2025. The dominance of paste and purees is primarily due to their ease of use in industrial recipes such as soups, sauces, and ready meals, where liquid or semi-liquid inputs ensure consistent blending. In contrast, the pieces and powder segment is gaining traction in applications that prioritize shelf stability, portion control, and reconstitution flexibility. For example, snack manufacturers are increasingly using vegetable powders in extruded chips and crackers to boost fiber content and support "contains real vegetables" claims, without requiring modifications to production lines designed for dry ingredients.

Technological advancements in spray drying have played a key role in driving this growth. Innovations such as enhanced nozzle designs to minimize particle agglomeration and encapsulation techniques to preserve volatile compounds have improved the sensory quality of reconstituted powders. These advancements have reduced the performance gap between powders and paste-based products, making powders a more competitive option across various applications.

By Application: Beverages Accelerate as Functional Positioning Drives Vegetable Ingredient Adoption

The beverages segment is projected to grow at a rate of 4.81% from 2026 to 2031, marking the fastest growth among applications. This growth is attributed to manufacturers utilizing vegetable concentrates to support claims related to immunity, digestive health, and energy, while avoiding synthetic additives. Soups and sauces accounted for 32.05% of the application spending in 2025, driven by their dependence on tomato and carrot concentrates for flavor consistency and natural coloring. However, the growth in the beverage segment is primarily fueled by cold-pressed vegetable juices, smoothies, and functional drinks, which highlight vegetable concentrates as nutrient-rich alternatives to fruit-based formulations.

In confectionery products, vegetable concentrates are predominantly used as natural colorants, replacing synthetic dyes in gummies and hard candies to align with clean-label requirements in Europe and North America. Similarly, bakery products incorporate pumpkin and carrot concentrates to enhance moisture retention and provide natural sweetness, thereby reducing the need for added sugar in items such as muffins and breads.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Europe emerged as the leading segment in 2025, accounting for 31.62% of the market value. This dominance is attributed to stringent regulatory frameworks and a strong consumer preference for organic and traceable ingredients. The European Food Safety Authority's Novel Foods Regulation (EU) 2015/2283 has imposed restrictions on synthetic additives, compelling manufacturers to reformulate their products using vegetable concentrates that align with clean-label standards. Countries such as Germany, the United Kingdom, and the Netherlands are at the forefront of concentrate consumption, driven by well-established food processing industries and high per-capita spending on premium ready meals and functional beverages.

The Asia-Pacific region is anticipated to be the fastest-growing segment, with a projected growth rate of 5.25% from 2026 to 2031. This rapid expansion is driven by urbanization, increasing disposable incomes, and the growing popularity of Western-style convenience foods. China and India are leading this growth trajectory. China's ready-meal market, valued at USD 28 billion in 2024, increasingly incorporates vegetable concentrates to ensure flavor consistency in large-scale production. In India, the rising middle class and the proliferation of quick-service restaurants have significantly increased the demand for tomato and carrot concentrates, particularly in sauces and beverages. Additionally, Indonesia and Thailand are emerging as important production hubs for vegetable concentrates, leveraging their lower labor costs and abundant vegetable supplies to meet both domestic and export demands.

North America also accounted for a significant share of the market in 2024, with the United States and Canada driving demand through advancements in functional beverages and the growing adoption of plant-based food products. The United States Food and Drug Administration's increased scrutiny of synthetic dyes has further accelerated the shift toward vegetable concentrates in confectionery and bakery products. Carrot and beetroot concentrates are increasingly being used as natural coloring agents, offering a clean-label alternative without the need for E-number declarations.

Competitive Landscape

Market Concentration

The vegetable concentrates market is highly fragmented, with a concentration score of 3 out of 10, indicating the presence of numerous regional processors, specialty ingredient providers, and vertically integrated agricultural cooperatives. This fragmentation creates opportunities for mid-sized players with proprietary drying technologies and direct farm relationships to gain market share from multinational ingredient suppliers, which often face challenges in matching local flavor profiles and ensuring quick turnaround times.

Strategic trends in the market highlight two distinct approaches. Large companies, such as Archer Daniels Midland and Ingredion, focus on achieving scale through acquisitions and capacity expansions. On the other hand, smaller specialists like Kanegrade and Van Drunen Farms focus on differentiation by offering organic certifications, custom formulations, and technical support for product development.

Adopting advanced technology is a critical factor in staying competitive. Companies investing in techniques such as pulsed electric field extraction, supercritical carbon dioxide (CO2) processing, and encapsulation methods can charge premium prices by delivering concentrates with improved nutrient retention and sensory quality. Furthermore, there are untapped opportunities in functional beverage applications, where vegetable concentrates can support claims related to immunity and digestive health, as well as in plant-based meat alternatives, where beetroot and tomato concentrates enhance visual appeal and improve consumer acceptance.

Vegetable Concentrates Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Natalie’s Orchid Island Juice Company and King of Pops launched Sweet Greens popsicles, using Natalie’s 100% Pineapple Celery Kale Zinc Juice to create a clean‑label, plant‑based frozen treat that showcases concentrated vegetable‑fruit juice as a functional ingredient in value‑added beverages and snacks.

- May 2025: Bunge introduced a new line of soy protein concentrates and announced a major capacity expansion at its Morristown, Indiana facility, designed to supply clean-tasting, neutral-colored, cost‑effective plant protein concentrates for snacks, bakery, meat alternatives, and beverages worldwide.

- November 2024: BENEO showcased faba‑bean protein, rice ingredients and Meatless texturates at Fi Europe 2024, offering plant‑based cheeses, chocolate, fish, meat analogues and ready meals that demonstrate scalable, cost‑efficient use of legume‑ and cereal‑based concentrates across the plant‑based value chain

Table of Contents for Vegetable Concentrates Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising health awareness increases the use of vegetable concentrates in nutrient-enriched foods and beverages

- 4.2.2Growing clean-label demand boosts vegetable concentrates as natural alternatives to artificial additives

- 4.2.3Expansion of plant-based foods drives demand for vegetable concentrates for natural color, flavor, and nutrition

- 4.2.4Increasing consumption of soups and ready meals supports the use of vegetable concentrates for taste consistency and convenience

- 4.2.5Growth of functional beverages encourages the use of vegetable concentrates for immunity and digestive health positioning

- 4.2.6Advancements in concentration technologies improve nutrient, color, and flavor retention

- 4.3Market Restraints

- 4.3.1Preference for fresh vegetables limits demand for processed concentrates

- 4.3.2Fresh, frozen, and chilled vegetables compete with processed options

- 4.3.3Flavor authenticity and freshness decline after processing or storage

- 4.3.4Color and nutrient degradation during processing and storage can reduce functional and visual appeal

- 4.4Supply Chain Analysis

- 4.5Regulatory Outlook

- 4.6Porter’s Five Forces

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers/Consumers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitute Products

- 4.6.5Intensity of Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1By Vegetable Type

- 5.1.1Tomato

- 5.1.2Carrot

- 5.1.3Beetroot

- 5.1.4Peas

- 5.1.5Pumpkin

- 5.1.6Other Vegetable Types

- 5.2By Category

- 5.2.1Paste and Purees

- 5.2.2Pieces and Powder

- 5.3By Application

- 5.3.1Beverages

- 5.3.2Confectionery Products

- 5.3.3Bakery Products

- 5.3.4Soups and Sauces

- 5.3.5Other Applications

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.1.4Rest of North America

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3Italy

- 5.4.2.4France

- 5.4.2.5Spain

- 5.4.2.6Netherlands

- 5.4.2.7Poland

- 5.4.2.8Belgium

- 5.4.2.9Sweden

- 5.4.2.10Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2India

- 5.4.3.3Japan

- 5.4.3.4Australia

- 5.4.3.5Indonesia

- 5.4.3.6South Korea

- 5.4.3.7Thailand

- 5.4.3.8Singapore

- 5.4.3.9Rest of Asia-Pacific

- 5.4.4South America

- 5.4.4.1Brazil

- 5.4.4.2Argentina

- 5.4.4.3Colombia

- 5.4.4.4Chile

- 5.4.4.5Peru

- 5.4.4.6Rest of South America

- 5.4.5Middle East and Africa

- 5.4.5.1South Africa

- 5.4.5.2Saudi Arabia

- 5.4.5.3United Arab Emirates

- 5.4.5.4Nigeria

- 5.4.5.5Egypt

- 5.4.5.6Morocco

- 5.4.5.7Turkey

- 5.4.5.8Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Ranking Analysis

- 6.4Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1Archer Daniels Midland

- 6.4.2Döhler GmbH

- 6.4.3Ingredion Incorporated

- 6.4.4AGRANA Beteiligungs AG

- 6.4.5SVZ International B.V.

- 6.4.6SunOpta Inc.

- 6.4.7Symrise AG

- 6.4.8Olam International Ltd.

- 6.4.9Kanegrade Ltd.

- 6.4.10Van Drunen Farms

- 6.4.11Hans Zipperle SpA

- 6.4.12European Freeze Dry

- 6.4.13Milne Fruit Products

- 6.4.14Kerr Concentrates (Ingredion)

- 6.4.15AGRANA Fruit US

- 6.4.16AGUSA

- 6.4.17Silva International

- 6.4.18Conesa Group

- 6.4.19Red Gold

- 6.4.20Morning Star Co.

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Global Vegetable Concentrates Market Report Scope

The global vegetable concentrates market is segmented by category, vegetable type, application, and geography. By category, the market studied is segmented into paste and purees, and pieces and powders. By vegetable type the market studied is segmented into, carrots, tomato, peas, beetroot, pumpkin and others. By application, the market studied is segmented into, beverages, confectionery products, bakery products, soups and sauces and other applications. Also, the study provides an analysis of the vegetable concentrates market in the emerging and established markets across the world, including North America, Europe, Asia-Pacific, South America, and Middle-East and Africa.