Edible Films And Coatings For Fruits And Vegetables Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.05 Billion |

| Market Size (2031) | USD 1.46 Billion |

| Growth Rate (2026 - 2031) | 6.84% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Edible Films And Coatings For Fruits And Vegetables Market Analysis by Mordor Intelligence

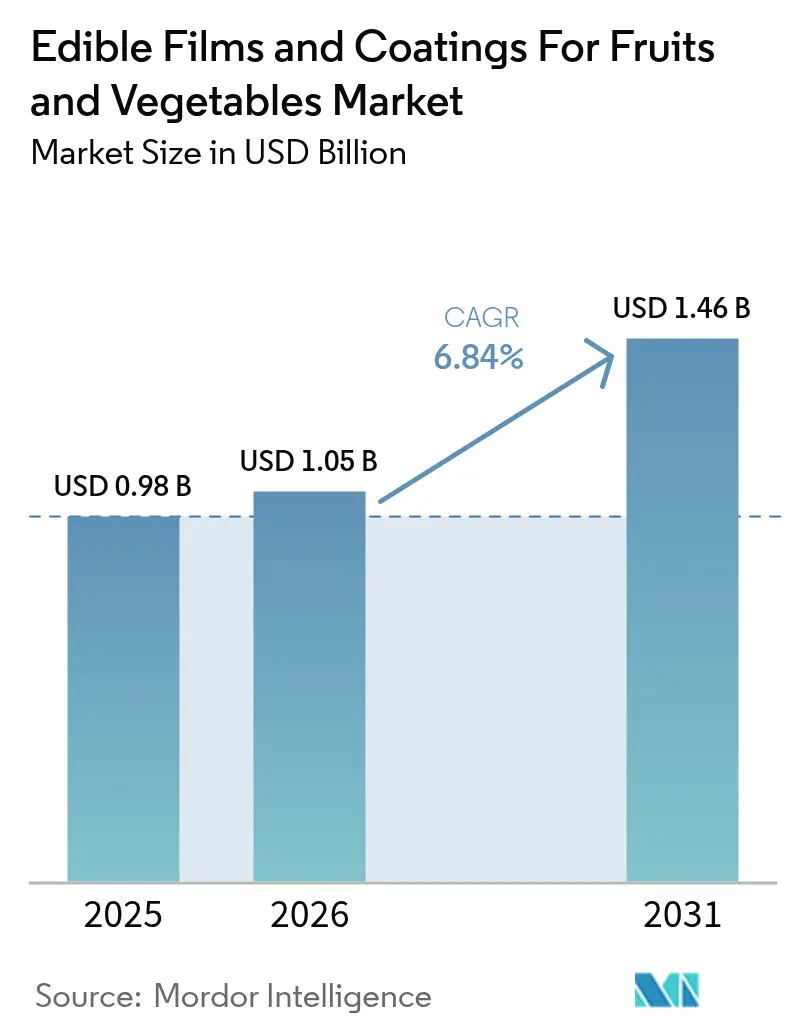

The edible films and coatings for fruits and vegetables market size was valued at USD 0.98 billion in 2025 and estimated to grow from USD 1.05 billion in 2026 to reach USD 1.46 billion by 2031, at a CAGR of 6.84% during the forecast period (2026-2031). Retailers and exporters are replacing synthetic fungicides and plastic wraps with plant-based, biodegradable barriers that slow respiration, cut moisture loss, and curb microbial growth, thereby reducing post-harvest waste. Regulatory bans on single-use plastics in the European Union and state-level mandates in the United States reinforce this shift. At the same time, cold-chain gaps in Asia-Pacific and South America heighten demand for coatings that extend shelf life without refrigeration. Moreover, ingredient suppliers and start-ups are racing for formulation patents and fast-track regulatory clearances, with composite films emerging as the preferred platform for moisture-sensitive produce. Raw-material cost swings, especially in chitosan and alginate, remain a profitability risk, yet the convergence of sustainability goals and food-loss reduction targets keeps growth momentum intact.

Key Report Takeaways

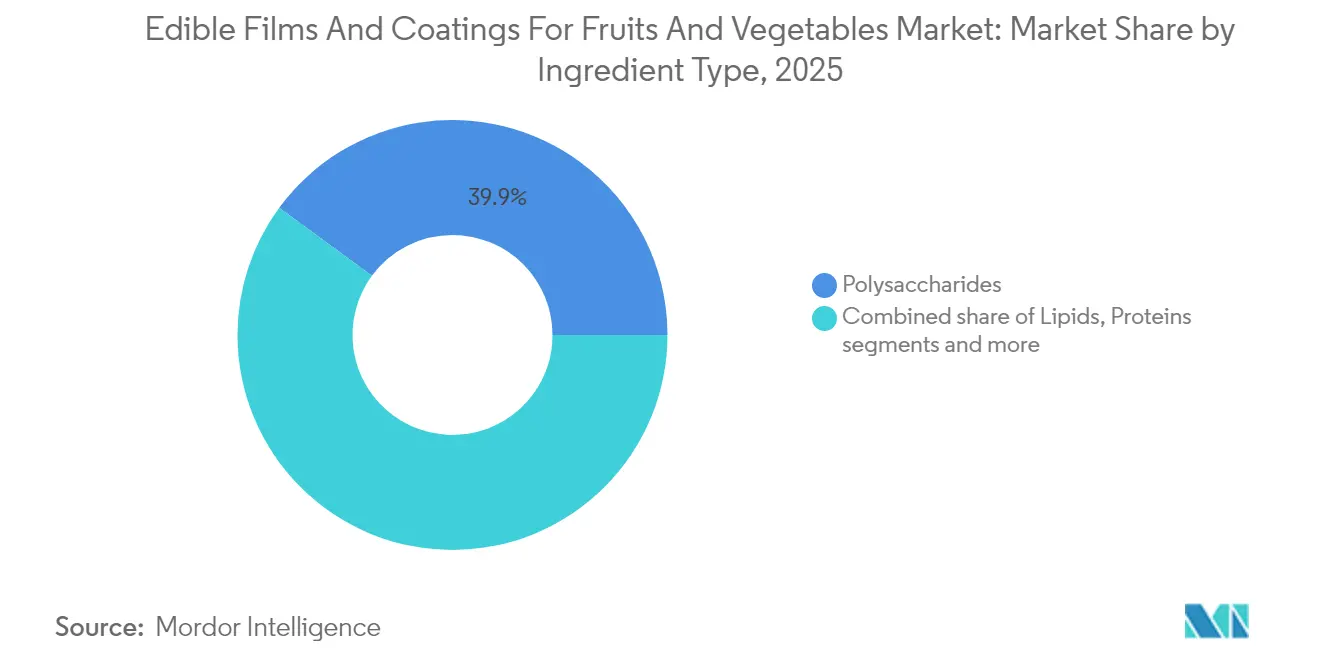

- By ingredient type, polysaccharides led with 39.92% revenue share in 2025, while composites are forecast to expand at a 7.62% CAGR to 2031, underscoring performance gains from multi-layer films that pair lipids and proteins.

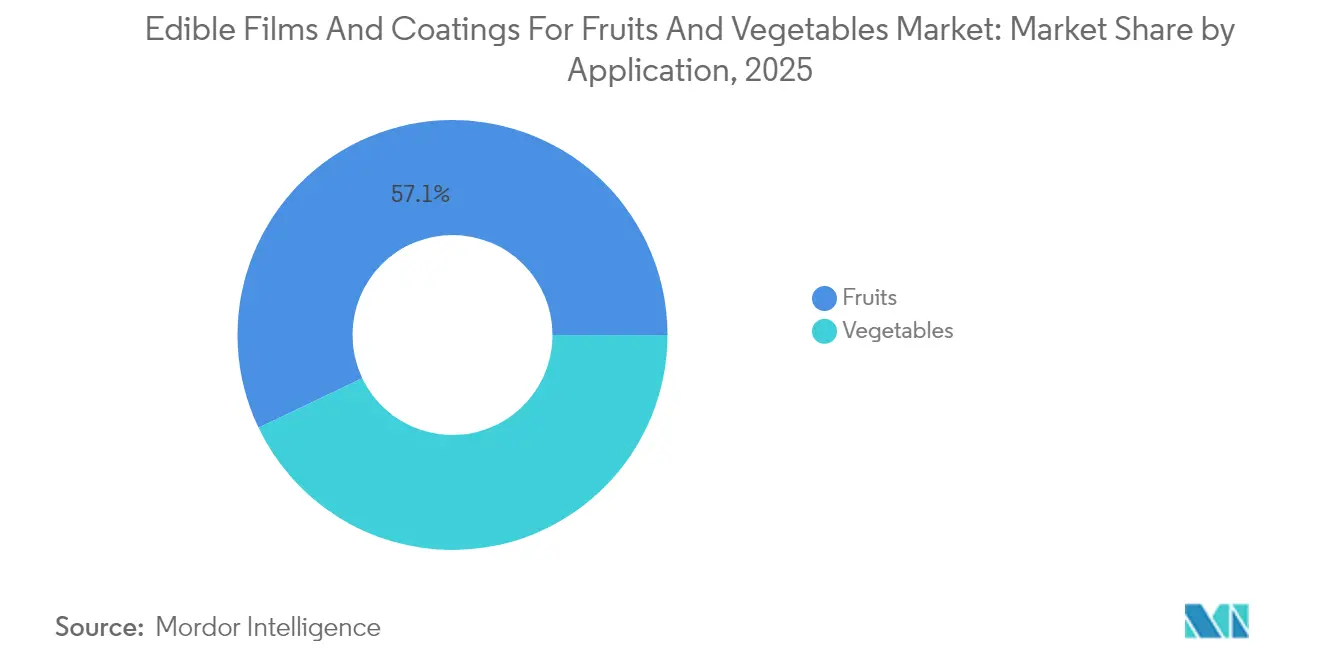

- By application, fruits captured 57.10% of the edible films and coatings for fruits and vegetables market share in 2025; vegetables are projected to grow at an 8.25% CAGR through 2031 as leafy-greens packers adopt cellulose sprays.

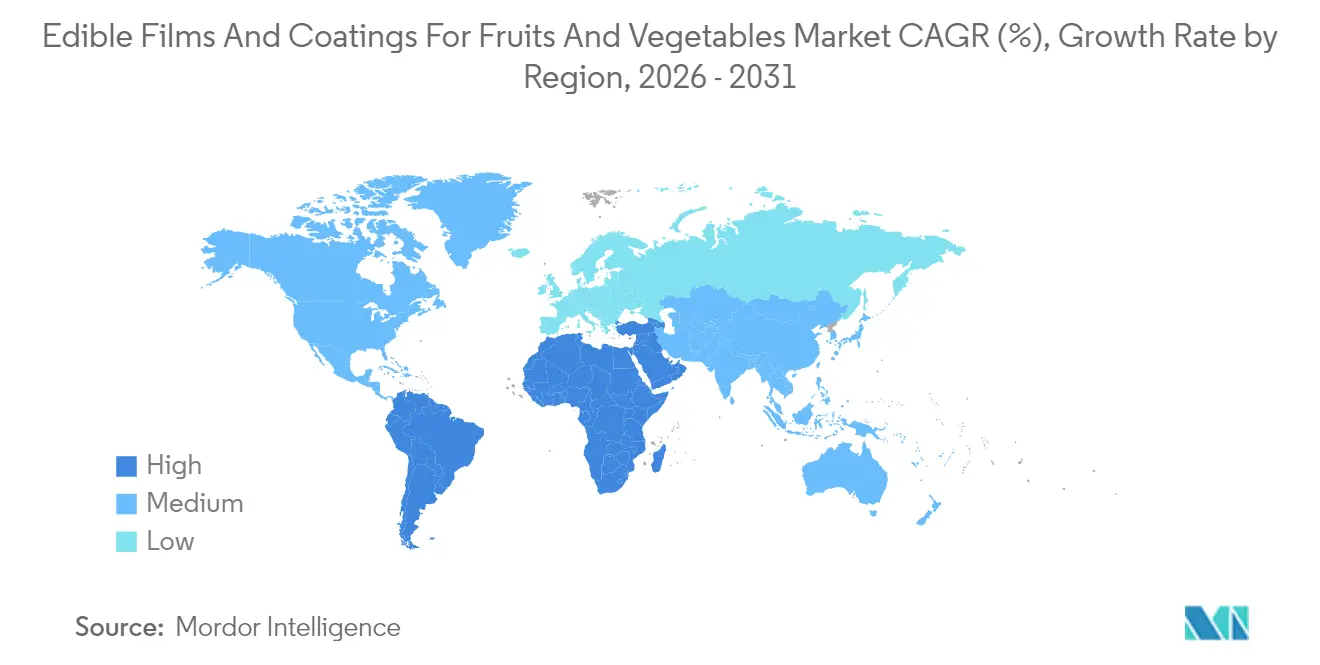

- By geography, Asia-Pacific commanded 35.18% revenue in 2025, while South America is set to post the fastest 7.28% CAGR between 2026 and 2031 on the back of large-scale produce exports.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Edible Films And Coatings For Fruits And Vegetables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer shift toward clean-label and natural preservatives replaces synthetics | +1.4% | Global, with early adoption in North America and Western Europe | Medium term (2-4 years) |

| Innovations like plant-based coatings extend shelf life | +1.6% | Global, led by Asia-Pacific supply chains and South American exporters | Short term (≤ 2 years) |

| Regulatory push to reduce plastic waste boosts biodegradable alternatives | +1.2% | Europe (SUP Directive), North America (state-level bans), spillover to Asia-Pacific | Long term (≥ 4 years) |

| Need to minimize post-harvest losses in perishable produce | +1.3% | Asia-Pacific, Sub-Saharan Africa, South America | Medium term (2-4 years) |

| Incorporation of bioactive compounds for added nutrition and safety | +0.8% | North America, Europe, urban Asia-Pacific markets | Long term (≥ 4 years) |

| Consumer preference for sustainable, environmentally aligned packaging | +0.9% | Global, strongest in Scandinavia, Germany, California | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer shift toward clean-label and natural preservatives replaces synthetics

The increasing consumer preference for clean-label and natural preservatives is driving the adoption of edible films and coatings for fruits and vegetables. This shift is fueled by heightened scrutiny of product labels and a growing demand for health-conscious and sustainable choices. Edible films and coatings, typically plant-derived and composed of minimal ingredients, offer an effective alternative to synthetic additives. The Food Standards Agency’s Food and You 2: Wave 9 survey in 2024 revealed that 53% of United Kingdom adults check ingredient lists, and 50% review nutritional information at least occasionally when purchasing food, underscoring the importance of transparency in preservative systems [1]Source: Food Standards Agency, "Food and You 2: Wave 9 Key Findings", food.gov.uk. Edible coatings made from polysaccharides, proteins, and lipids provide a "label-friendly" solution by extending shelf life and maintaining freshness through physical barrier functions, often incorporating naturally derived antimicrobials or antioxidants to support “no artificial preservatives” claims without compromising quality. Companies like Apeel (now operating as Oliver) have demonstrated the effectiveness of such coatings in reducing waste and maintaining plant-based ingredient lists, as seen in partnerships with retailers like Kroger in the United States. Premium and organic brands are increasingly adopting invisible coatings that preserve taste and appearance while extending shelf life, aligning with consumer preferences for fresh-looking produce without "chemical-sounding" additives. Mainstream supermarket private labels are also under pressure to adopt clean-label attributes, driving the broader application of edible coatings across categories such as berries, pome fruits, and leafy greens. Regulatory and NGO scrutiny on synthetic preservatives further supports this trend, with manufacturers leveraging GRAS or widely accepted bio-based materials for strategic flexibility. Clear communication about the natural, plant-based composition of these coatings builds consumer trust, supports premium pricing, and enhances brand equity. Additionally, as awareness of food waste grows, clean-label coatings are positioned as a natural method of shelf-life extension, appealing to environmentally conscious consumers. This convergence of label scrutiny, natural ingredient preferences, and sustainability expectations is reinforcing consumer demand and driving growth in the market for edible films and coatings for fruits and vegetables.

Innovations like plant-based coatings extend shelf life

Plant-based coatings, formulated from polysaccharides, plant proteins, and lipids, are gaining traction as effective solutions for extending the shelf life of fruits and vegetables. These coatings create thin, edible barriers that minimize moisture loss and gas exchange, preserving firmness, visual appeal, and marketability. This aligns with the increasing consumer preference for plant-based solutions. According to the Good Food Institute Europe, by 2025, 51% of adults in the United Kingdom and Germany plan to adjust their diets by either increasing plant-based food consumption or reducing animal meat and dairy intake, with approximately 20% intending to do both [2]Source: Good Food Institute Europe (GFI Europe), "Research: Four in 10 German and UK Adults Plan to Eat More Plant-based Food", gfieurope.org. This shift in dietary habits is driving demand for plant-based technologies, including packaging and preservation solutions, making bio-based coatings more attractive to retailers and brands emphasizing "plant-forward" strategies. These coatings can be tailored for specific produce categories, such as berries, citrus fruits, or leafy greens, by modifying film-former blends and permeability to ensure extended shelf life without compromising texture or sensory quality, which is critical for retail acceptance. Companies like Hazel Technologies demonstrate how plant-derived compounds can effectively slow ripening and spoilage in fresh produce supply chains, integrating seamlessly into existing packing and distribution workflows while maintaining a natural, label-friendly appeal. Retailers expanding plant-based and flexitarian product ranges increasingly seek alignment between product contents and preservation methods, positioning plant-based edible films and coatings as complementary solutions. This technology is particularly advantageous in export-heavy categories like avocados, berries, and stone fruits, where extended transit times highlight the benefits of shelf-life extension, reducing shrinkage and write-offs at the retail level. Successful outcomes, such as reduced waste and improved on-shelf quality, further drive research and development into new plant sources, bioactive components, and advanced processing techniques, reinforcing plant-based coatings as a key growth driver in the edible films and coatings market.

Regulatory push to reduce plastic waste boosts biodegradable alternatives

Efforts to reduce plastic waste are driving the adoption of biodegradable alternatives through increasingly stringent regulations on single-use plastics, extended producer responsibility, and packaging recyclability. These measures diminish the appeal of traditional plastic films while raising compliance and reputational risks for retailers and fresh-produce brands. Policies in regions such as the European Union and parts of North America are steering retailers toward low-plastic or plastic-free fresh aisles, prompting supermarket chains to seek solutions that preserve product quality while adhering to reuse, composting, or minimal-packaging frameworks. Edible films and coatings are emerging as a strategic option for unpackaged or minimally packaged fruits and vegetables. These coatings, derived from polysaccharides, plant proteins, and lipids, are biodegradable or even edible, aligning more closely with policy and organizational expectations for circularity compared to conventional petrochemical plastics. This proactive approach is particularly attractive to premium and sustainability-focused retailers, where packaging serves as a visible indicator of environmental commitment. Transitioning from clamshells or plastic wraps to invisible edible coatings on products such as berries or cucumbers provides a clear narrative for sustainability efforts. Companies like Apeel, working with retailers in Europe and the United States, have demonstrated that edible coatings can replace or significantly reduce plastic packaging for items such as avocados and citrus while maintaining the shelf life required by retailers. These examples highlight how regulatory-driven plastic reduction directly supports the adoption of edible coatings. As pilot programs expand into chain-wide implementations, they provide reference cases for regulators and industry associations, showcasing the feasibility of producing high-quality, lower-plastic fresh produce. This feedback loop of stricter regulations, successful case studies, and rising retailer expectations drives investment in advanced biodegradable coatings, which meet food-contact safety standards and offer improved barrier performance tailored to specific produce categories, reinforcing their role as a growth driver in the market.

Need to minimize post-harvest losses in perishable produce

Minimizing post-harvest losses in perishable produce is a critical priority, as stakeholders across the value chain, including growers, packers, and retailers, face direct financial impacts when fruits and vegetables spoil before sale. Reliable shelf-life extension technologies are essential to address this issue. According to data from the Food and Agriculture Organization Sustainable Development Goals Indicator, fruits and vegetables have the highest global post-harvest loss, rising from 23.2% in 2015 to 25.4% in 2023 [3]Source: Food and Agriculture Organization of the United Nations (FAO), "SDG Indicators Data Portal", fao.org. This increase is driven by their high perishability and specific handling requirements, underscoring the limitations of existing cold-chain systems and conventional packaging in reducing waste. The adoption of edible films and coatings has emerged as a solution, acting as selective barriers to moisture and gases to slow respiration and senescence. These technologies extend the marketability of products such as berries, leafy greens, and stone fruits while reducing their susceptibility to damage during transport and display. Exporters and large growers benefit from fewer rejected pallets and higher pack-out rates, while retailers experience lower shrink, improved on-shelf quality, and reduced out-of-stocks, incentivizing the integration of coatings into post-harvest protocols. As sustainability and food security considerations grow, reducing post-harvest losses aligns with corporate environmental, social, and governance targets and national commitments to sustainable development goals. This focus drives research and development into commodity-specific coating formulations to address challenges such as high respiration in berries or rapid wilting in leafy greens, making solutions more effective and scalable. The combination of financial losses, highlighted waste levels, and policy pressures positions the reduction of post-harvest losses as a key driver for the edible films and coatings market for fruits and vegetables.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs from natural, agricultural raw materials | -0.9% | Global, acute in regions with limited chitosan or alginate supply (Sub-Saharan Africa, Southeast Asia, South America) | Short term (≤ 2 years) |

| Poor moisture barrier in polysaccharide films compared to plastics | -0.6% | Humid tropical climates (Southeast Asia, Central America, Sub-Saharan Africa), leafy-greens applications globally | Medium term (2-4 years) |

| Variability in performance across fruit/vegetable types | -0.5% | Global, particularly acute in mixed-produce packhouses in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Reliance on seasonal inputs causing supply disruptions | -0.7% | Regions dependent on crustacean-shell chitosan (North America, Asia-Pacific) and seaweed alginate (Norway, Chile, Japan) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High production costs from natural, agricultural raw materials

The high production costs associated with natural, agricultural raw materials present a significant challenge for the edible films and coatings market. These products depend on biopolymers such as proteins, polysaccharides, and lipids, which are often more expensive and less price-stable than commodity petrochemical resins. This is particularly evident when these materials are derived from food-grade crops or specialty by-products that require additional purification and quality control. Seasonal variability, competing uses in food and feed, and fragmented supply chains further exacerbate procurement risks, forcing manufacturers to maintain higher-cost inventories or enter long-term contracts with elevated raw material prices. Achieving the desired barrier, mechanical, and sensory properties typically requires multi-component formulations that include plasticizers, emulsifiers, and natural antimicrobials or antioxidants, increasing ingredient complexity and cost per kilogram compared to conventional plastic films. Processing these natural materials into consistent coatings demands precise control of parameters such as pH, temperature, and viscosity, along with specialized application systems for dipping or spraying irregular fruit and vegetable surfaces. These factors contribute to higher capital and operating expenses, deterring smaller packers from adoption. Unlike conventional plastic packaging, which benefits from decades of industrial-scale production and standardized processes, edible coating production is still developing large-scale infrastructure, resulting in relatively high unit costs and limited economies of scale in many regions. For brand owners and retailers targeting value-conscious or price-sensitive consumers, the premium associated with coated produce can be a deterrent, especially when the added cost cannot be easily passed on to consumers without risking a decline in sales volumes. These factors collectively hinder faster and broader adoption of edible films and coatings for fruits and vegetables globally.

Poor moisture barrier in polysaccharide films compared to plastics

The limited moisture barrier properties of polysaccharide films compared to plastics present a significant challenge for their application in packaging. Polysaccharides are naturally hydrophilic, causing their films to absorb and transmit water vapor readily. This characteristic restricts their ability to control moisture migration in high-humidity supply chains for fresh produce, making them less effective than plastic films in preventing dehydration or surface condensation. Moisture sensitivity not only reduces barrier performance but also leads to plasticization and softening of the film, resulting in a loss of mechanical strength, stickiness, or cracking over time. These issues undermine the reliability of polysaccharide films for fruits and vegetables requiring robust handling from the packhouse to the retail shelf. To mitigate these limitations, packers often enhance polysaccharide coatings by incorporating lipids, cross-linkers, or nanoparticles, or by combining them with secondary packaging, which increases formulation and processing complexity and reduces the cost-benefit advantage over simple plastic films. The moisture barrier gap is particularly problematic in long or fluctuating cold-chain routes for products like berries and leafy greens, where even minor changes in water activity can cause textural damage, microbial growth, or visual defects, discouraging retailers from fully transitioning away from plastic wraps. Many commercial solutions, such as those offered by AgroFresh, rely on composite or multi-layer approaches that integrate polysaccharides with hydrophobic components rather than using pure polysaccharide films. While these hybrid solutions improve moisture resistance, they dilute the simplicity and sustainability narrative and may raise regulatory or recyclability concerns if non-edible or less biodegradable components are introduced. For smaller producers and regional packers, the need for advanced formulation expertise and tighter process control to manage water vapor permeability creates a technical barrier to entry, slowing the broader adoption of edible films and coatings beyond early adopters and large integrated suppliers. The inherently poor moisture barrier of polysaccharide films compared to plastics, along with the additional engineering required to address this limitation, remains a key technical restraint on their widespread substitution for conventional packaging in the edible films and coatings market for fruits and vegetables.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Composites Gain as Multi-Layer Functionality Outpaces Single-Ingredient Films

Polysaccharides remain a key component of composite systems, holding 39.92% of the market share in 2025. Materials such as chitosan, recognized for its Generally Recognized as Safe status by the Food and Drug Administration, and alginate, valued for its seaweed-derived sustainability, make polysaccharides an attractive base matrix. Proteins, including whey, soy, and zein, accounted for approximately 24.78% of the market volume in 2025. These proteins are increasingly co-formulated with polysaccharides due to their excellent film-forming properties and compatibility with bioactive additives like nisin and natamycin, which enhance structural integrity and microbial protection. Lipids, such as carnauba wax and shellac, continue to play a critical role as outer moisture-barrier components, particularly in tropical fruit exports where reducing transpiration and maintaining gloss are essential for preserving visual appeal and weight during extended shipping periods. Companies like Decco demonstrate how lipid-focused layers are integrated into composite systems tailored to meet regulatory and customer requirements across different regions. The combined strengths of polysaccharides for sustainability, proteins for structural and functional benefits, and lipids for moisture control are driving the increasing adoption of composite ingredient systems in the edible films and coatings market for fruits and vegetables.

Besides, composites are projected to grow at a compound annual growth rate of 7.62% during 2026-2031, surpassing the market average of 6.84%. This growth is driven by the ability of composite systems, which combine polysaccharides, proteins, and lipids, to deliver enhanced performance in moisture control, gas-barrier properties, and mechanical strength, capabilities that single-ingredient films often lack. Hydrophobic lipids act as effective water-vapor barriers, while proteins provide oxygen and aroma barriers along with cohesive strength. These features address the high water-vapor transmission rates of standalone polysaccharide layers, making composites particularly suitable for moisture-sensitive products such as leafy greens and thin-skinned berries. Composite coatings can also be customized to match specific respiration rates and surface properties, reducing reliance on plastic overwrap. Furthermore, composites enable the integration of bioactive agents, such as antimicrobials, antioxidants, and nutraceuticals, into distinct layers, allowing controlled release near the produce surface while optimizing the outer layer for handling and appearance. Companies like Sufresca illustrate how multi-component systems can be tailored to various commodities and packaging conditions while maintaining label-friendly formulations.

By Application: Vegetables Accelerate as Leafy-Greens Packers Adopt Cellulose Sprays

The vegetable segment is projected to grow at a compound annual growth rate of 8.25% during 2026-2031, driven by the increasing adoption of cellulose-based spray coatings by leafy greens, nightshade, and root-crop packers. These coatings effectively reduce wilting and moisture loss while integrating seamlessly into existing washing and drying processes. Despite this growth, fruits accounted for 57.10% of the market share in 2025, supported by high-value categories such as citrus, berries, pome fruits, and stone fruits. Coatings in the fruit segment enhance display life and reduce fungal spoilage, particularly in export and premium retail channels. Citrus fruits, including oranges, lemons, and grapefruits, represent the largest sub-segment due to fungicide-integrated wax systems that meet stringent United States and European Union phytosanitary standards while preserving gloss and minimizing weight loss during long-haul shipments. Berries, particularly strawberries and blueberries, are the fastest-growing sub-segment, benefiting from technologies that extend shelf life and reduce shrinkage. Stone fruits, such as peaches and plums, and pome fruits, including apples and pears, increasingly utilize protein-based coatings that suppress storage molds and improve pack-out rates in cold chains.

The vegetable segment's accelerated growth reflects structural changes in fresh-cut salad, meal-kit, and convenience channels, where maintaining texture and appearance is critical to meeting retailer requirements and reducing waste. Leafy greens, nightshades, and root vegetables benefit from coatings that reduce water loss, limit post-harvest rot, and extend marketable life. For instance, cellulose coatings support longer shelf life for leafy greens, while chitosan-based systems protect nightshades from rot, and alginate coatings extend the storage life of root vegetables. These advancements are driving a portfolio shift, positioning vegetables as the faster-growing application segment within the edible films and coatings market.

Geography Analysis

Asia-Pacific accounted for a 35.18% market share in 2025, driven by increasing cold-chain capacity, export-oriented strategies, and supportive policies. Investments such as China’s USD 24.4 billion cold-chain infrastructure and India’s National Centre for Cold Chain Development initiatives aim to address post-harvest loss rates of approximately 13%. Edible coatings are increasingly viewed as complementary to refrigeration, providing a protective micro-barrier around individual fruits and vegetables. For example, Maharashtra’s grape-export clusters have demonstrated a 12% to 15% reduction in spoilage during ocean transport to Europe by combining cold storage with coatings, showcasing the potential for broader adoption in other high-value horticulture regions. However, regulatory requirements in countries like Indonesia and Thailand, which mandate separate approvals for each coating formulation and use case, delay time-to-market. This complexity benefits larger players such as Decco and AgroFresh, which possess in-house regulatory expertise and regional presence, enabling them to navigate multi-country registrations more efficiently than smaller competitors.

South America is projected to grow at a 7.28% compound annual growth rate during 2026 to 2031, the fastest regional growth rate, driven by export-oriented horticulture and increasing sustainability pressures. Brazil’s USD 166.5 billion agricultural export sector plays a pivotal role, with the Ministry of Agriculture promoting alginate coatings for mango and papaya exports to reduce rejection rates at European ports. Chile’s exporters of blueberries, cherries, and table grapes have adopted composite films to extend transit tolerance during long ocean voyages to China and the United States, achieving an additional five to seven days of post-arrival shelf life, which supports premium pricing in distant markets. In countries like Colombia and Peru, where rural cold-chain infrastructure is limited, coatings that extend shelf life without relying solely on refrigeration are strategically valuable. International suppliers and regional innovators are targeting these markets with solutions that balance robustness under variable conditions with regulatory compliance for key export destinations.

North America and Europe, with their mature cold-chain networks, are shaping the market through sustainability mandates, plastic-reduction policies, and clean-label consumer preferences. In the European Union, the Single-Use Plastics Directive is driving demand for cellulose and alginate films and coatings that meet compostability standards and integrate with paper-based packaging systems. Similarly, California’s legislation requiring recyclable or compostable single-use packaging by 2032 has led West Coast berry growers to trial alginate sprays that enable fibre-based or open packaging formats, reducing or eliminating plastic trays while maintaining transport resilience. Meanwhile, the Middle East and Africa remain emerging markets, with adoption concentrated in high-value niches such as South Africa’s citrus industry and the United Arab Emirates’ premium date sector. However, fragmented regulatory frameworks and the lack of harmonized edible-coating standards in countries like Nigeria and Egypt require suppliers to secure country-specific approvals, increasing entry costs and slowing market penetration.

Competitive Landscape

The market for edible films and coatings for fruits and vegetables is characterized by moderate fragmentation, with competition between large multinational ingredient suppliers and smaller, innovative start-ups. Companies such as Tate and Lyle, RPM International, and Kerry utilize their extensive ingredient portfolios, regulatory expertise, and established relationships with major retailers and packers. These organizations focus on scaling cellulose, alginate, protein, and lipid systems into standardized, food-grade coating solutions that can be applied across various regions and produce categories. Their efforts are centered on platform technologies, including film-forming starch or protein systems, emulsifiers, and texturants, which are adapted into coating formats and supported by technical services for packhouses requiring reliability and seamless integration with existing processing lines. Meanwhile, specialized innovators like Hazel Technologies, Apeel Sciences, and Mori Inc. target specific, high-impact applications such as berries, avocados, and leafy greens, where shelf-life extension offers clear returns on investment. These start-ups differentiate themselves through proprietary lipid, protein, or bioactive systems, driving innovation beyond commodity ingredients.

Opportunities in the market are increasingly focused on bioactive coatings and composite formulations that combine barrier performance with antimicrobial or antioxidant functionality. For example, Mori Inc. employs silk-protein-based coatings to create ultra-thin, breathable layers capable of carrying bioactive compounds while maintaining label-friendly attributes. This approach addresses gaps left by traditional wax or simple polysaccharide coatings. Composite systems that integrate hydrophobic lipids with oxygen-barrier proteins and polysaccharides are also gaining attention. These systems address the moisture and gas-exchange limitations of single-ingredient films and enable commodity-specific customization for products such as berries, citrus, or leafy greens. While start-ups often pilot these innovations with specific growers and retailers, multinationals focus on industrializing and standardizing successful concepts into globally scalable ingredient systems. As regulatory and retailer expectations tighten around plastic reduction and clean-label requirements, bioactive and composite coatings present significant growth opportunities by delivering shelf-life, safety, and sustainability benefits within a single solution.

Strategic partnerships and ecosystem-building are becoming increasingly important in shaping competition within this market, blurring the boundaries between ingredient suppliers, technology firms, and fresh-produce brands. Large ingredient companies are collaborating with coating specialists to combine their formulation and regulatory expertise with proprietary actives or application technologies developed by start-ups. These collaborations aim to accelerate regulatory approvals and reduce commercialization risks for global retailers. Simultaneously, innovators like Hazel Technologies work closely with exporters and packers to develop data-rich case studies demonstrating waste reduction and quality improvements. These results are used to negotiate broader adoption and co-branded programs. Retailers and grower–shipper groups, particularly in high-value categories and export-oriented regions, are emerging as key decision-makers. They often conduct multi-vendor trials, comparing multinational platforms with start-up solutions under real supply-chain conditions. This dynamic fosters continuous improvement in performance, cost, and integration ease, reinforcing a competitive landscape where success depends on delivering differentiated, bioactive, and composite coating solutions that are technically robust, regulatory-compliant, and economically viable.

Edible Films And Coatings For Fruits And Vegetables Industry Leaders

-

Apeel Sciences

-

RPM International Inc.

-

Tate & Lyle PLC

-

Sufresca

-

Hazel Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Swedish food-tech start-up Saveggy introduced an additive-free, edible, plant-based coating for fresh produce, providing an alternative to plastic packaging. The coating was made using two ingredients: rapeseed oil and oat oil. Saveggy aimed to scale this solution to significantly reduce plastic usage in packaging and help minimize food waste in fresh produce.

- June 2025: Akorn Technology, a manufacturer of natural coatings for fresh fruits and vegetables, introduced a new edible coating for cucumbers aimed at extending shelf life and replacing single-use plastic wraps. Akorn’s patented edible coatings utilize upcycled, non-GMO plant materials to provide a natural solution for prolonging shelf life and improving quality. The company sought to meet the demands of consumers and retailers in the US, Europe, and other regions for sustainable packaging alternatives made from bio-based and compostable materials.

- May 2024: Apeel Sciences, a company specializing in supply chain solutions for the fresh produce industry through edible coatings, announced the launch of "The Apeel Leverage," an initiative aimed at improving the fresh produce supply chain. By utilizing its plant-based technology, Apeel aimed to enhance operational efficiency, broaden market access, and optimize product quality and retail performance. The initiative began with its first pillar, "Expand Offerings with Confidence."

Global Edible Films And Coatings For Fruits And Vegetables Market Report Scope

Edible films and coatings are thin layers of edible materials, such as edible biopolymers and food-grade additives, applied on fruits and vegetables that play an important role in their conservation, distribution, and marketing. Some of their functions are to protect the product from mechanical damage, physical, chemical, and microbiological activities.

The edible films and coatings for fruits and vegetables market report is segmented by ingredient type into proteins, polysaccharides, lipids, composites, application into fruits—citrus, berries, pome fruits, stone fruits; vegetables—leafy greens, nightshades, root and tuber, and by geography into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Proteins |

| Polysaccharides |

| Lipids |

| Composites |

| Fruits | Citrus |

| Berries | |

| Pome Fruits | |

| Stone Fruits | |

| Vegetables | Leafy Greens |

| Nightshades | |

| Root and Tuber |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Ingredient Type | Proteins | |

| Polysaccharides | ||

| Lipids | ||

| Composites | ||

| By Application | Fruits | Citrus |

| Berries | ||

| Pome Fruits | ||

| Stone Fruits | ||

| Vegetables | Leafy Greens | |

| Nightshades | ||

| Root and Tuber | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the edible films and coatings for fruits and vegetables market growing?

The market is expanding at a 6.84% CAGR between 2026 and 2031, moving from USD 1.05 billion to USD 1.46 billion.

Which ingredient segment leads current revenue?

Polysaccharides hold 39.92% of 2025 revenue due to chitosan’s antimicrobial traits and alginate’s sustainability profile.

Which application offers the quickest growth?

Vegetable coatings are forecast to rise at an 8.25% CAGR as cellulose films reduce wilting in leafy greens.

What region captures the largest share?

Asia-Pacific commands 35.18% of global revenue, supported by major cold-chain investments and high produce volumes.

Page last updated on: